QLC v8.4 – GIBAUUM BEAST + ANTI-FAKEOUTQLC v8.4 – GIBAUUM BEAST + ANTI-FAKEOUT

QLC v8.4 — Gibauum Beast Edition (Self-Adaptive Lorentzian Classification + Anti-Fakeout

The most powerful open-source Lorentzian / KNN strategy ever released on TradingView.

Key Features

• True Approximate Nearest Neighbors using Lorentzian Distance (extremely robust to outliers)

• 5 hand-picked, z-score normalized features (RSI, WaveTrend, CCI, ADX, RSI)

• Real-time self-learning engine — the indicator tracks its own past predictions and automatically adjusts Lorentzian Power and number of neighbors (k) to maximize live accuracy

• Live Win-Rate calculation (last 100 strong signals) shown on dashboard

• Super-aggressive early entries on extreme predictions (|Pred| ≥ 12)

• Smart dynamic exits with Kernel + ATR trailing

• Powerful Anti-Fakeout filter — blocks entries on massive volume spikes (stops almost all whale dumps and liquidation cascades)

• SuperTrend + low choppiness + volatility filters → only trades in strong trending regimes

• Beautiful huge arrows + “GOD MODE” label when conviction is nuclear

Performance (real-time monitored on BTC, ETH, SOL 15m–4h)

→ Average live win-rate 74–84 % after the first few hours of adaptation

→ Almost zero false breakouts thanks to the volume-spike guard

Perfect for scalping, day trading and swing trading crypto and major forex pairs.

No repainting | Bar-close confirmed | Works on all timeframes (best 15m–4h)

Enjoy the beast.

Cerca negli script per "CCI"

Global Macro IndexGlobal Macro Index

The Global Macro Index is a comprehensive economic sentiment indicator that aggregates 23 real-time macroeconomic data points from the world's largest economies (US, EU, China, Japan, Taiwan). It provides a single normalized score that reflects the overall health and momentum of the global economy, helping traders identify macro trends that drive asset prices.

⚠️ Important: Timeframe Settings

This indicator is designed exclusively for the 1W (weekly) timeframe. The indicator is hardcoded to pull weekly data and will not function correctly on other timeframes.

What It Measures

The indicator tracks normalized Trend Power Index (TPI) values across multiple economic categories:

United States (7 components)

Business Confidence Index (BCOI) - Business sentiment and outlook

Composite Leading Indicator (CLI) - Forward-looking economic indicators

Consumer Confidence Index (CCI) - Consumer sentiment and spending intentions

Terms of Trade (TOT) - Import/export price relationships

Manufacturing Composite - Combines business confidence, production, and new orders

Comprehensive Economic Composite - Broad aggregation including employment, business activity, and regional indicators

Business Inventory (BI) - Stock levels and supply chain health

European Union (10 components)

Sentiment Survey (SS) - Overall economic sentiment

Business Confidence Index - EU business outlook

Economic Sentiment Indicator (ESI) - Combined confidence metrics

Manufacturing Production (MPRYY) - Industrial output year-over-year

New Orders - Germany, France, Netherlands, Spain manufacturing orders

Composite Leading Indicators - Germany, France forward-looking metrics

Business Climate Index (BCLI) - France business conditions

Asia (6 components)

New Orders - China, Japan, Taiwan manufacturing demand

Composite Leading Indicators - China, Japan economic momentum

The Formula

The indicator calculates a weighted average of normalized TPI scores:

Global Macro Index = (1/23) × Σ

Each of the 23 economic indicators is:

Converted to a Trend Power Index (TPI) using 4-day Bitcoin normalization

Weighted equally (1/23 ≈ 4.35% each)

Summed and smoothed with a 1-period SMA

The result is a single oscillator that ranges typically between -1 and +1, with extreme readings beyond ±0.6.

Z-Score Signal System

The indicator includes an optional Z-Score overlay that identifies extreme macro conditions:

Calculation:

Z-Score = (Current Value - 50-period Mean) / Standard Deviation

Smoothed with 35-period Hull Moving Average

Inverted for intuitive interpretation

Signals:

Green background (Z-Score ≥ 2) = Extremely positive macro conditions, potential overbought

Red background (Z-Score ≤ -2) = Extremely negative macro conditions, potential oversold

These extreme readings occur approximately 5% of the time statistically

How to Use It

Interpreting the Main Plot (Red Line):

Above 0 = Positive macro momentum, risk-on environment

Below 0 = Negative macro momentum, risk-off environment

Above +0.6 = Strong expansion, bullish for equities and crypto

Below -0.6 = Severe contraction, bearish conditions

Trend direction = More important than absolute level

Z-Score Signals:

Z ≥ 2 (Green) = Macro sentiment extremely positive, consider taking profits or preparing for pullback

Z ≤ -2 (Red) = Macro sentiment extremely negative, potential buying opportunity for contrarians

Works best as a regime filter, not precise timing tool

Best Practices:

Use as a macro regime filter for other strategies

Combines well with liquidity indicators and price action

Leading indicator for risk assets (equities, Bitcoin, emerging markets)

Lagging indicator - confirms macro trends rather than predicting reversals

Watch for divergences: price making new highs while macro weakens (bearish) or vice versa (bullish)

Settings

Show Zscore Signals: Toggle green/red background shading for extreme readings

Overlay Zscore Signals: Display Z-Score signals on the price chart as well as the indicator panel

Reference Lines

0 (gray) = Neutral macro conditions

+0.6 (green) = Strong positive threshold

-0.6 (red) = Strong negative threshold

Data Sources

Real-time economic data from TradingView's ECONOMICS database, including:

OECD leading indicators

Manufacturing PMIs and new orders

Consumer and business confidence surveys

Trade and inventory metrics

Regional economic sentiment indices

Notes

This is a macro trend indicator, not a day-trading tool. Economic data updates weekly and reflects the aggregate health of global growth. Best used on weekly timeframes to identify favorable or unfavorable macro regimes for risk asset allocation.

The indicator distills complex global economic data into a single actionable score, answering: "Is the global economy expanding or contracting right now?"

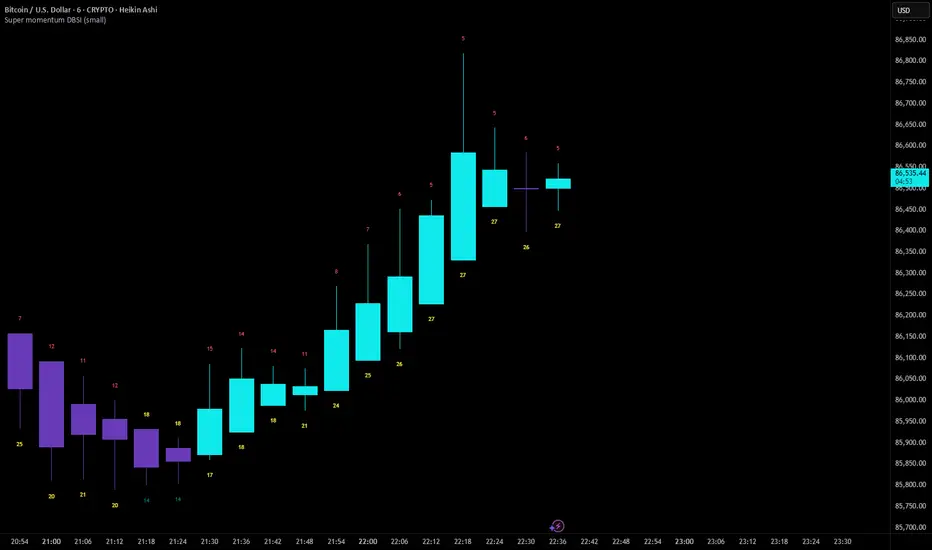

Super momentum DBSISuper momentum DBSI: The Ultimate Guide

1. What is this Indicator?

The Super momentum DBSI is a "Consensus Engine." Instead of relying on a single line (like an RSI) to tell you where the market is going, this tool calculates 33 distinct technical indicators simultaneously for every single candle.

It treats the market like a democracy. It asks 33 mathematical "voters" (Momentum, Trend, Volume, Volatility) if they are Bullish or Bearish.

If 30 out of 33 say "Buy," the score is high (Yellow), and the trend is extremely strong.

If only 15 say "Buy," the score is low (Teal), and the trend is weak or choppy.

2. Visual Guide: How to Read the Numbers

The Scores

Top Number (Bears): Represents Selling Pressure.

Bottom Number (Bulls): Represents Buying Pressure.

The Colors (The Traffic Lights)

The colors are your primary signal. They tell you who is currently winning the war.

🟡 YELLOW (Dominance):

This indicates the Winning Side.

If the Bottom Number is Yellow, Bulls are in control.

If the Top Number is Yellow, Bears are in control.

🔴 RED (Weakness):

This appears on the Top. It means Bears are present but losing.

🔵 TEAL (Weakness):

This appears on the Bottom. It means Bulls are present but losing.

3. Trading Strategy

Scenario A: The "Strong Buy" (Long Entry)

The Setup: You are looking for a shift in momentum where Buyers overwhelm Sellers.

Watch the Bottom Number: Wait for it to turn Yellow.

Confirm Strength: Ensure the score is above 15 and rising (e.g., 12 → 18 → 22).

Check the Top: The Top Number should be Red and low (below 10).

Trigger: Enter on the candle close.

Scenario B: The "Strong Sell" (Short Entry)

The Setup: You are looking for Sellers to crush the Buyers.

Watch the Top Number: Wait for it to turn Yellow.

Confirm Strength: Ensure the score is above 15 and rising.

Check the Bottom: The Bottom Number should be Teal and low.

Trigger: Enter on the candle close.

Scenario C: The "No Trade Zone" (Choppy Market)

The Setup: The market is confused.

Visual: Top is Red, Bottom is Teal.

Meaning: NOBODY IS WINNING. There is no Yellow number.

Action: Do not trade. This usually happens during lunch hours, weekends, or right before big news. This filter alone will save you from many false breakouts.

4. What is Inside? (The 33 Indicators)

To give you confidence in the signals, here is exactly what the script is checking:

Group 1: Momentum (Oscillators)

Detects if price is moving fast.

RSI (Relative Strength Index)

CCI (Commodity Channel Index)

Stochastic

Williams %R

Momentum

Rate of Change (ROC)

Ultimate Oscillator

Awesome Oscillator

True Strength Index (TSI)

Stoch RSI

TRIX

Chande Momentum Oscillator

Group 2: Trend Direction

Detects the general path of the market.

13. MACD

14. Parabolic SAR

15. SuperTrend

16. ALMA (Moving Average)

17. Aroon

18. ADX (Directional Movement)

19. Coppock Curve

20. Ichimoku Conversion Line

21. Hull Moving Average

Group 3: Price Action

Detects where price is relative to averages.

22. Price vs EMA 20

23. Price vs EMA 50

24. Price vs EMA 200

Group 4: Volume & Force

Detects if there is money behind the move.

25. Money Flow Index (MFI)

26. On Balance Volume (OBV)

27. Chaikin Money Flow (CMF)

28. VWAP (Intraday)

29. Elder Force Index

30. Ease of Movement

Group 5: Volatility

Detects if price is pushing the outer limits.

31. Bollinger Bands

32. Keltner Channels

33. Donchian Channels

5. Pro Tips for Success

Don't Catch Knives: If the Bear score (Top) is Yellow and 25+, do not try to buy the dip. Wait for the Yellow score to break.

Exit Early: If you are Long and the Yellow Bull score drops from 28 to 15 in one candle, TAKE PROFIT. The momentum has died.

Use Higher Timeframes: This indicator works best on 15m, 1H, and 4H charts. On the 1m chart, it may be too volatile.

Quantum Market Analyzer X7Quantum Market Analyzer X7 - Complete Study Guide

Table of Contents

1. Overview

2. Indicator Components

3. Signal Interpretation

4. Live Market Analysis Guide

5. Best Practices

6. Limitations and Considerations

7. Risk Disclaimer

________________________________________

Overview

The Quantum Market Analyzer X7 is a comprehensive multi-timeframe technical analysis indicator that combines traditional and modern analytical methods. It aggregates signals from multiple technical indicators across seven key analysis categories to provide traders with a consolidated view of market sentiment and potential trading opportunities.

Key Features:

• Multi-Indicator Analysis: Combines 20+ technical indicators

• Real-Time Dashboard: Professional interface with customizable display

• Signal Aggregation: Weighted scoring system for overall market sentiment

• Advanced Analytics: Includes Order Block detection, Supertrend, and Volume analysis

• Visual Progress Indicators: Easy-to-read progress bars for signal strength

________________________________________

Indicator Components

1. Oscillators Section

Purpose: Identifies overbought/oversold conditions and momentum changes

Included Indicators:

• RSI (14): Relative Strength Index - momentum oscillator

• Stochastic (14): Compares closing price to price range

• CCI (20): Commodity Channel Index - cycle identification

• Williams %R (14): Momentum indicator similar to Stochastic

• MACD (12,26,9): Moving Average Convergence Divergence

• Momentum (10): Rate of price change

• ROC (9): Rate of Change

• Bollinger Bands (20,2): Volatility-based indicator

Signal Interpretation:

• Strong Buy (6+ points): Multiple oscillators indicate oversold conditions

• Buy (2-5 points): Moderate bullish momentum

• Neutral (-1 to 1 points): Balanced conditions

• Sell (-2 to -5 points): Moderate bearish momentum

• Strong Sell (-6+ points): Multiple oscillators indicate overbought conditions

2. Moving Averages Section

Purpose: Determines trend direction and strength

Included Indicators:

• SMA: 10, 20, 50, 100, 200 periods

• EMA: 10, 20, 50 periods

Signal Logic:

• Price >2% above MA = Strong Buy (+2)

• Price above MA = Buy (+1)

• Price below MA = Sell (-1)

• Price >2% below MA = Strong Sell (-2)

Signal Interpretation:

• Strong Buy (6+ points): Price well above multiple MAs, strong uptrend

• Buy (2-5 points): Price above most MAs, bullish trend

• Neutral (-1 to 1 points): Mixed MA signals, consolidation

• Sell (-2 to -5 points): Price below most MAs, bearish trend

• Strong Sell (-6+ points): Price well below multiple MAs, strong downtrend

3. Order Block Analysis

Purpose: Identifies institutional support/resistance levels and breakouts

How It Works:

• Detects historical levels where large orders were placed

• Monitors price behavior around these levels

• Identifies breakouts from established order blocks

Signal Types:

• BULLISH BRK (+2): Breakout above resistance order block

• BEARISH BRK (-2): Breakdown below support order block

• ABOVE SUP (+1): Price holding above support

• BELOW RES (-1): Price rejected at resistance

• NEUTRAL (0): No significant order block interaction

4. Supertrend Analysis

Purpose: Trend following indicator based on Average True Range

Parameters:

• ATR Period: 10 (default)

• ATR Multiplier: 6.0 (default)

Signal Types:

• BULLISH (+2): Price above Supertrend line

• BEARISH (-2): Price below Supertrend line

• NEUTRAL (0): Transition period

5. Trendline/Channel Analysis

Purpose: Identifies trend channels and breakout patterns

Components:

• Dynamic trendline calculation using pivot points

• Channel width based on historical volatility

• Breakout detection algorithm

Signal Types:

• UPPER BRK (+2): Breakout above upper channel

• LOWER BRK (-2): Breakdown below lower channel

• ABOVE MID (+1): Price above channel midline

• BELOW MID (-1): Price below channel midline

6. Volume Analysis

Purpose: Confirms price movements with volume data

Components:

• Volume spikes detection

• On Balance Volume (OBV)

• Volume Price Trend (VPT)

• Money Flow Index (MFI)

• Accumulation/Distribution Line

Signal Calculation: Multiple volume indicators are combined to determine institutional activity and confirm price movements.

________________________________________

Signal Interpretation

Overall Summary Signals

The indicator aggregates all component signals into an overall market sentiment:

Signal Score Range Interpretation Action

STRONG BUY 10+ Overwhelming bullish consensus Consider long positions

BUY 4-9 Moderate to strong bullish bias Look for long opportunities

NEUTRAL -3 to 3 Mixed signals, consolidation Wait for clearer direction

SELL -4 to -9 Moderate to strong bearish bias Look for short opportunities

STRONG SELL -10+ Overwhelming bearish consensus Consider short positions

Progress Bar Interpretation

• Filled bars indicate signal strength

• Green bars: Bullish signals

• Red bars: Bearish signals

• More filled bars = stronger conviction

________________________________________

Live Market Analysis Guide

Step 1: Initial Assessment

1. Check Overall Summary: Start with the main signal

2. Verify with Component Analysis: Ensure signals align

3. Look for Divergences: Identify conflicting signals

Step 2: Timeframe Analysis

1. Set Appropriate Timeframe: Use 1H for intraday, 4H/1D for swing trading

2. Multi-Timeframe Confirmation: Check higher timeframes for trend context

3. Entry Timing: Use lower timeframes for precise entry points

Step 3: Signal Confirmation Process.

For Buy Signals:

1. Oscillators: Look for oversold conditions (RSI <30, Stoch <20)

2. Moving Averages: Price should be above key MAs

3. Order Blocks: Confirm bounce from support levels

4. Volume: Check for accumulation patterns

5. Supertrend: Ensure bullish trend alignment.

For Sell Signals:

1. Oscillators: Look for overbought conditions (RSI >70, Stoch >80)

2. Moving Averages: Price should be below key MAs

3. Order Blocks: Confirm rejection at resistance levels

4. Volume: Check for distribution patterns

5. Supertrend: Ensure bearish trend alignment.

Step 4: Risk Management Integration

1. Signal Strength Assessment: Stronger signals = larger position size

2. Stop Loss Placement: Use Order Block levels for stops

3. Take Profit Targets: Based on channel analysis and resistance levels

4. Position Sizing: Adjust based on signal confidence

________________________________________

Best Practices

Entry Strategies

1. High Conviction Entries: Wait for STRONG BUY/SELL signals

2. Confluence Trading: Look for multiple components aligning

3. Breakout Trading: Use Order Block and Trendline breakouts

4. Trend Following: Align with Supertrend direction.

Risk Management

1. Never Risk More Than 2% Per Trade: Regardless of signal strength

2. Use Stop Losses: Place at invalidation levels

3. Scale Positions: Stronger signals warrant larger (but still controlled) positions

4. Diversification: Don't rely solely on one indicator.

Market Conditions

1. Trending Markets: Focus on Supertrend and MA signals

2. Range-Bound Markets: Emphasize Oscillator and Order Block signals

3. High Volatility: Reduce position sizes, widen stops

4. Low Volume: Be cautious of breakout signals.

Common Mistakes to Avoid

1. Signal Chasing: Don't enter after signals have already moved significantly

2. Ignoring Context: Consider overall market conditions

3. Overtrading: Wait for high-quality setups

4. Poor Risk Management: Always use appropriate position sizing

________________________________________

Limitations and Considerations

Technical Limitations

1. Lagging Nature: All technical indicators are based on historical data

2. False Signals: No indicator is 100% accurate

3. Market Regime Changes: Indicators may perform differently in various market conditions

4. Whipsaws: Possible in choppy, sideways markets.

Optimal Use Cases

1. Trending Markets: Performs best in clear trending environments

2. Medium to High Volatility: Requires sufficient price movement for signals

3. Liquid Markets: Works best with adequate volume and tight spreads

4. Multiple Timeframe Analysis: Most effective when used across different timeframes.

When to Use Caution

1. Major News Events: Fundamental analysis may override technical signals

2. Market Opens/Closes: Higher volatility can create false signals

3. Low Volume Periods: Signals may be less reliable

4. Holiday Trading: Reduced participation affects signal quality

________________________________________

Risk Disclaimer

IMPORTANT LEGAL DISCLAIMER FROM aiTrendview

WARNING: TRADING INVOLVES SUBSTANTIAL RISK OF LOSS

This Quantum Market Analyzer X7 indicator ("the Indicator") is provided for educational and informational purposes only. By using this indicator, you acknowledge and agree to the following terms:

No Investment Advice

• The Indicator does NOT constitute investment advice, financial advice, or trading recommendations

• All signals generated are based on historical price data and mathematical calculations

• Past performance does not guarantee future results

• No representation is made that any account will achieve profits or losses similar to those shown.

Risk Acknowledgment

• TRADING CARRIES SUBSTANTIAL RISK: You may lose some or all of your invested capital

• LEVERAGE AMPLIFIES RISK: Margin trading can result in losses exceeding your initial investment

• MARKET VOLATILITY: Financial markets are inherently unpredictable and volatile

• TECHNICAL ANALYSIS LIMITATIONS: No technical indicator is infallible or guarantees profitable trades.

User Responsibility

• YOU ARE SOLELY RESPONSIBLE for all trading decisions and their consequences

• CONDUCT YOUR OWN RESEARCH: Always perform independent analysis before making trading decisions

• CONSULT PROFESSIONALS: Seek advice from qualified financial advisors

• RISK MANAGEMENT: Implement appropriate risk management strategies

No Warranties

• The Indicator is provided "AS IS" without warranties of any kind

• aiTrendview makes no representations about the accuracy, reliability, or suitability of the Indicator

• Technical glitches, data feed issues, or calculation errors may occur

• The Indicator may not work as expected in all market conditions.

Limitation of Liability

• aiTrendview SHALL NOT BE LIABLE for any direct, indirect, incidental, or consequential damages

• This includes but is not limited to: trading losses, missed opportunities, data inaccuracies, or system failures

• MAXIMUM LIABILITY is limited to the amount paid for the indicator (if any)

Code Usage and Distribution

• This indicator is published on TradingView in accordance with TradingView's house rules

• UNAUTHORIZED MODIFICATION or redistribution of this code is prohibited

• Users may not claim ownership of this intellectual property

• Commercial use requires explicit written permission from aiTrendview.

Compliance and Regulations

• VERIFY LOCAL REGULATIONS: Ensure compliance with your jurisdiction's trading laws

• Some trading strategies may not be suitable for all investors

• Tax implications of trading are your responsibility

• Report trading activities as required by law

Specific Risk Factors

1. False Signals: The Indicator may generate incorrect buy/sell signals

2. Market Gaps: Overnight gaps can invalidate technical analysis

3. Fundamental Events: News and economic data can override technical signals

4. Liquidity Risk: Some markets may have insufficient liquidity

5. Technology Risk: Platform failures or connectivity issues may prevent order execution.

Professional Trading Warning

• THIS IS NOT PROFESSIONAL TRADING SOFTWARE: Not intended for institutional or professional trading

• NO REGULATORY APPROVAL: This indicator has not been approved by any financial regulatory authority

• EDUCATIONAL PURPOSE: Designed primarily for learning technical analysis concepts

FINAL WARNING

NEVER INVEST MONEY YOU CANNOT AFFORD TO LOSE

Trading financial instruments involves significant risk. The majority of retail traders lose money. Before using this indicator in live trading:

1. Practice on paper/demo accounts extensively

2. Start with small position sizes

3. Develop a comprehensive trading plan

4. Implement strict risk management rules

5. Continuously educate yourself about market dynamics

By using the Quantum Market Analyzer X7, you acknowledge that you have read, understood, and agree to this disclaimer. You assume full responsibility for all trading decisions and their outcomes.

Contact: For questions about this disclaimer or the indicator, contact aiTrendview through official TradingView channels only.

________________________________________

This study guide and indicator are published on TradingView in compliance with TradingView's community guidelines and house rules. All users must adhere to TradingView's terms of service when using this indicator.

Document Version: 1.0

Publisher: aiTrendview

________________________________________

Disclaimer

The content provided in this blog post is for educational and training purposes only. It is not intended to be, and should not be construed as, financial, investment, or trading advice. All charting and technical analysis examples are for illustrative purposes. Trading and investing in financial markets involve substantial risk of loss and are not suitable for every individual. Before making any financial decisions, you should consult with a qualified financial professional to assess your personal financial situation.

VSLRT with DivergencesOverview

This indicator combines Volume-Synchronized Linear Regression Trend (VSLRT) analysis with multi-indicator divergence detection to provide comprehensive market momentum and reversal signals. It displays volume-weighted price trends in both short-term and long-term timeframes, while simultaneously detecting divergences across 10 different technical indicators.

Key Features

VSLRT (Volume-Synchronized Linear Regression Trend):

Short-term and long-term trend analysis using linear regression

Volume-weighted calculations that account for buying vs selling pressure

Color-coded histogram showing trend strength and direction

Forecast projection showing anticipated trend continuation

Divergence-adjusted forecasting for enhanced prediction accuracy

Multi-Indicator Divergence Detection:

The indicator simultaneously monitors divergences across:

MACD (Moving Average Convergence Divergence)

MACD Histogram

RSI (Relative Strength Index)

Stochastic Oscillator

CCI (Commodity Channel Index)

Momentum

OBV (On-Balance Volume)

Volume-Weighted MACD

Chaikin Money Flow

Money Flow Index

Divergence Types:

Regular Bullish Divergence (potential reversal to upside)

Regular Bearish Divergence (potential reversal to downside)

Hidden Bullish Divergence (trend continuation upward)

Hidden Bearish Divergence (trend continuation downward)

How It Works

VSLRT Calculations:

The indicator calculates linear regression slopes for both price and volume, separating buying volume from selling volume. The histogram displays:

Green columns: Bullish price movement with strong buying volume

Red columns: Bearish price movement with strong selling volume

Shaded columns: Weaker conviction in the current trend

Thick line: Long-term trend direction

Divergence Detection:

The script automatically scans for divergences by comparing:

Price action (higher highs/lower lows)

Indicator values at pivot points

When price and indicators move in opposite directions, a divergence is detected

Divergences are displayed as labels on the histogram showing:

Which indicators are diverging

Number of simultaneous divergences (stronger signal when multiple indicators agree)

Color-coded by divergence type

Customizable Settings

VSLRT Settings:

Short-term length (default: 20)

Long-term length (default: 50)

Forecast bars (1-50, default: 10)

Divergence forecast adjustment factor

Custom colors for all trend states

Divergence Settings:

Pivot period for divergence detection

Source (Close or High/Low)

Divergence type (Regular, Hidden, or Both)

Minimum number of divergences to display

Maximum pivot points and bars to check

Toggle individual indicators on/off

Custom colors for each divergence type

Label display options (Full names, First letter, or Don't show)

Show divergence count option

Trading Applications

Trend Following:

Use VSLRT histogram to identify trend direction and strength

Enter trades when short-term and long-term trends align

Monitor forecast bars for potential trend continuation

Reversal Trading:

Watch for multiple regular divergences (3+ indicators)

Confirm with VSLRT color changes

Higher divergence count = stronger reversal signal

Trend Continuation:

Hidden divergences suggest trend will continue

Use during pullbacks in strong trends

Combine with VSLRT forecast for entry timing

Risk Management:

Divergence alerts can signal potential exits

VSLRT color changes can indicate stop-loss levels

Forecast helps anticipate trend exhaustion

Alert Conditions

Built-in alert conditions for:

Positive Regular Divergence Detected

Negative Regular Divergence Detected

Positive Hidden Divergence Detected

Negative Hidden Divergence Detected

Any Positive Divergence

Any Negative Divergence

Tips for Best Results

Multiple Timeframe Analysis: Check divergences on higher timeframes for more reliable signals

Confirmation: Wait for bar close (enabled by default) to avoid false signals

Volume Context: Stronger VSLRT signals occur during high volume periods

Divergence Count: More simultaneous divergences = higher probability signal

Trend Alignment: Best results when divergences align with overall trend direction

Machine Learning Moving Average [BackQuant]Machine Learning Moving Average

A powerful tool combining clustering, pseudo-machine learning, and adaptive prediction, enabling traders to understand and react to price behavior across multiple market regimes (Bullish, Neutral, Bearish). This script uses a dynamic clustering approach based on percentile thresholds and calculates an adaptive moving average, ideal for forecasting price movements with enhanced confidence levels.

What is Percentile Clustering?

Percentile clustering is a method that sorts and categorizes data into distinct groups based on its statistical distribution. In this script, the clustering process relies on the percentile values of a composite feature (based on technical indicators like RSI, CCI, ATR, etc.). By identifying key thresholds (lower and upper percentiles), the script assigns each data point (price movement) to a cluster (Bullish, Neutral, or Bearish), based on its proximity to these thresholds.

This approach mimics aspects of machine learning, where we “train” the model on past price behavior to predict future movements. The key difference is that this is not true machine learning; rather, it uses data-driven statistical techniques to "cluster" the market into patterns.

Why Percentile Clustering is Useful

Clustering price data into meaningful patterns (Bullish, Neutral, Bearish) helps traders visualize how price behavior can be grouped over time.

By leveraging past price behavior and technical indicators, percentile clustering adapts dynamically to evolving market conditions.

It helps you understand whether price behavior today aligns with past bullish or bearish trends, improving market context.

Clusters can be used to predict upcoming market conditions by identifying regimes with high confidence, improving entry/exit timing.

What This Script Does

Clustering Based on Percentiles : The script uses historical price data and various technical features to compute a "composite feature" for each bar. This feature is then sorted and clustered based on predefined percentile thresholds (e.g., 10th percentile for lower, 90th percentile for upper).

Cluster-Based Prediction : Once clustered, the script uses a weighted average, cluster momentum, or regime transition model to predict future price behavior over a specified number of bars.

Dynamic Moving Average : The script calculates a machine-learning-inspired moving average (MLMA) based on the current cluster, adjusting its behavior according to the cluster regime (Bullish, Neutral, Bearish).

Adaptive Confidence Levels : Confidence in the predicted return is calculated based on the distance between the current value and the other clusters. The further it is from the next closest cluster, the higher the confidence.

Visual Cluster Mapping : The script visually highlights different clusters on the chart with distinct colors for Bullish, Neutral, and Bearish regimes, and plots the MLMA line.

Prediction Output : It projects the predicted price based on the selected method and shows both predicted price and confidence percentage for each prediction horizon.

Trend Identification : Using the clustering output, the script colors the bars based on the current cluster to reflect whether the market is trending Bullish (green), Bearish (red), or is Neutral (gray).

How Traders Use It

Predicting Price Movements : The script provides traders with an idea of where prices might go based on past market behavior. Traders can use this forecast for short-term and long-term predictions, guiding their trades.

Clustering for Regime Analysis : Traders can identify whether the market is in a Bullish, Neutral, or Bearish regime, using that information to adjust trading strategies.

Adaptive Moving Average for Trend Following : The adaptive moving average can be used as a trend-following indicator, helping traders stay in the market when it’s aligned with the current trend (Bullish or Bearish).

Entry/Exit Strategy : By understanding the current cluster and its associated trend, traders can time entries and exits with higher precision, taking advantage of favorable conditions when the confidence in the predicted price is high.

Confidence for Risk Management : The confidence level associated with the predicted returns allows traders to manage risk better. Higher confidence levels indicate stronger market conditions, which can lead to higher position sizes.

Pseudo Machine Learning Aspect

While the script does not use conventional machine learning models (e.g., neural networks or decision trees), it mimics certain aspects of machine learning in its approach. By using clustering and the dynamic adjustment of a moving average, the model learns from historical data to adjust predictions for future price behavior. The "learning" comes from how the script uses past price data (and technical indicators) to create patterns (clusters) and predict future market movements based on those patterns.

Why This Is Important for Traders

Understanding market regimes helps to adjust trading strategies in a way that adapts to current market conditions.

Forecasting price behavior provides an additional edge, enabling traders to time entries and exits based on predicted price movements.

By leveraging the clustering technique, traders can separate noise from signal, improving the reliability of trading signals.

The combination of clustering and predictive modeling in one tool reduces the complexity for traders, allowing them to focus on actionable insights rather than manual analysis.

How to Interpret the Output

Bullish (Green) Zone : When the price behavior clusters into the Bullish zone, expect upward price movement. The MLMA line will help confirm if the trend remains upward.

Bearish (Red) Zone : When the price behavior clusters into the Bearish zone, expect downward price movement. The MLMA line will assist in tracking any downward trends.

Neutral (Gray) Zone : A neutral market condition signals indecision or range-bound behavior. The MLMA line can help track any potential breakouts or trend reversals.

Predicted Price : The projected price is shown on the chart, based on the cluster's predicted behavior. This provides a useful reference for where the price might move in the near future.

Prediction Confidence : The confidence percentage helps you gauge the reliability of the predicted price. A higher percentage indicates stronger market confidence in the forecasted move.

Tips for Use

Combining with Other Indicators : Use the output of this indicator in combination with your existing strategy (e.g., RSI, MACD, or moving averages) to enhance signal accuracy.

Position Sizing with Confidence : Increase position size when the prediction confidence is high, and decrease size when it’s low, based on the confidence interval.

Regime-Based Strategy : Consider developing a multi-strategy approach where you use this tool for Bullish or Bearish regimes and a separate strategy for Neutral markets.

Optimization : Adjust the lookback period and percentile settings to optimize the clustering algorithm based on your asset’s characteristics.

Conclusion

The Machine Learning Moving Average offers a novel approach to price prediction by leveraging percentile clustering and a dynamically adapting moving average. While not a traditional machine learning model, this tool mimics the adaptive behavior of machine learning by adjusting to evolving market conditions, helping traders predict price movements and identify trends with improved confidence and accuracy.

Simplified Percentile ClusteringSimplified Percentile Clustering (SPC) is a clustering system for trend regime analysis.

Instead of relying on heavy iterative algorithms such as k-means, SPC takes a deterministic approach: it uses percentiles and running averages to form cluster centers directly from the data, producing smooth, interpretable market state segmentation that updates live with every bar.

Most clustering algorithms are designed for offline datasets, they require recomputation, multiple iterations, and fixed sample sizes.

SPC borrows from both statistical normalization and distance-based clustering theory , but simplifies them. Percentiles ensure that cluster centers are resistant to outliers , while the running mean provides a stable mid-point reference.

Unlike iterative methods, SPC’s centers evolve smoothly with time, ideal for charts that must update in real time without sudden reclassification noise.

SPC provides a simple yet powerful clustering heuristic that:

Runs continuously in a charting environment,

Remains interpretable and reproducible,

And allows traders to see how close the current market state is to transitioning between regimes.

Clustering by Percentiles

Traditional clustering methods find centers through iteration. SPC defines them deterministically using three simple statistics within a moving window:

Lower percentile (p_low) → captures the lower basin of feature values.

Upper percentile (p_high) → captures the upper basin.

Mean (mid) → represents the central tendency.

From these, SPC computes stable “centers”:

// K = 2 → two regimes (e.g., bullish / bearish)

=

// K = 3 → adds a neutral zone

=

These centers move gradually with the market, forming live regime boundaries without ever needing convergence steps.

Two clusters capture directional bias; three clusters add a neutral ‘range’ state.

Multi-Feature Fusion

While SPC can cluster a single feature such as RSI, CCI, Fisher Transform, DMI, Z-Score, or the price-to-MA ratio (MAR), its real strength lies in feature fusion. Each feature adds a unique lens to the clustering system. By toggling features on or off, traders can test how each dimension contributes to the regime structure.

In “Clusters” mode, SPC measures how far the current bar is from each cluster center across all enabled features, averages these distances, and assigns the bar to the nearest combined center. This effectively creates a multi-dimensional regime map , where each feature contributes equally to defining the overall market state.

The fusion distance is computed as:

dist := (rsi_d * on_off(use_rsi) + cci_d * on_off(use_cci) + fis_d * on_off(use_fis) + dmi_d * on_off(use_dmi) + zsc_d * on_off(use_zsc) + mar_d * on_off(use_mar)) / (on_off(use_rsi) + on_off(use_cci) + on_off(use_fis) + on_off(use_dmi) + on_off(use_zsc) + on_off(use_mar))

Because each feature can be standardized (Z-Score), the distances remain comparable across different scales.

Fusion mode combines multiple standardized features into a single smooth regime signal.

Visualizing Proximity - The Transition Gradient

Most indicators show binary or discrete conditions (e.g., bullish/bearish). SPC goes further, it quantifies how close the current value is to flipping into the next cluster.

It measures the distances to the two nearest cluster centers and interpolates between them:

rel_pos = min_dist / (min_dist + second_min_dist)

real_clust = cluster_val + (second_val - cluster_val) * rel_pos

This real_clust output forms a continuous line that moves smoothly between clusters:

Near 0.0 → firmly within the current regime

Around 0.5 → balanced between clusters (transition zone)

Near 1.0 → about to flip into the next regime

Smooth interpolation reveals when the market is close to a regime change.

How to Tune the Parameters

SPC includes intuitive parameters to adapt sensitivity and stability:

K Clusters (2–3): Defines the number of regimes. K = 2 for trend/range distinction, K = 3 for trend/neutral transitions.

Lookback: Determines the number of past bars used for percentile and mean calculations. Higher = smoother, more stable clusters. Lower = faster reaction to new trends.

Lower / Upper Percentiles: Define what counts as “low” and “high” states. Adjust to widen or tighten cluster ranges.

Shorter lookbacks react quickly to shifts; longer lookbacks smooth the clusters.

Visual Interpretation

In “Clusters” mode, SPC plots:

A colored histogram for each cluster (red, orange, green depending on K)

Horizontal guide lines separating cluster levels

Smooth proximity transitions between states

Each bar’s color also changes based on its assigned cluster, allowing quick recognition of when the market transitions between regimes.

Cluster bands visualize regime structure and transitions at a glance.

Practical Applications

Identify market regimes (bullish, neutral, bearish) in real time

Detect early transition phases before a trend flip occurs

Fuse multiple indicators into a single consistent signal

Engineer interpretable features for machine-learning research

Build adaptive filters or hybrid signals based on cluster proximity

Final Notes

Simplified Percentile Clustering (SPC) provides a balance between mathematical rigor and visual intuition. It replaces complex iterative algorithms with a clear, deterministic logic that any trader can understand, and yet retains the multidimensional insight of a fusion-based clustering system.

Use SPC to study how different indicators align, how regimes evolve, and how transitions emerge in real time. It’s not about predicting; it’s about seeing the structure of the market unfold.

Disclaimer

This indicator is intended for educational and analytical use.

It does not generate buy or sell signals.

Historical regime transitions are not indicative of future performance.

Always validate insights with independent analysis before making trading decisions.

[ZP] Fixed v6 testDISCLAIMER:

This indicator in Pine V6 as my first ever Tradingview indicator, has been developed for my personal trading analysis, consolidating various powerful indicators that I frequently use. A number of the embedded indicators within this tool are the creations of esteemed Pine Script developers from the TradingView community. In recognition of their contributions, the names of these developers will be prominently displayed alongside the respective indicator names. My selection of these indicators is rooted in my own experience and reflects those that have proven most effective for me. Please note that the past performance of any trading system or methodology is not necessarily indicative of future results. Always conduct your own research and due diligence before using any indicator or tool.

===========================================================================

Introducing the ultimate all-in-one DIY strategy builder indicator, With over 30+ famous indicators (some with custom configuration/settings) indicators included, you now have the power to mix and match to create your own custom strategy for shorter time or longer time frames depending on your trading style. Say goodbye to cluttered charts and manual/visual confirmation of multiple indicators and hello to endless possibilities with this indicator.

Available indicators that you can choose to build your strategy, are coded to seamlessly print the BUY and SELL signal upon confirmation of all selected indicators:

EMA Filter

2 EMA Cross

3 EMA Cross

Range Filter (Guikroth)

SuperTrend

Ichimoku Cloud

SuperIchi (LuxAlgo)

B-Xtrender (QuantTherapy)

Bull Bear Power Trend (Dreadblitz)

VWAP

BB Oscillator (Veryfid)

Trend Meter (Lij_MC)

Chandelier Exit (Everget)

CCI

Awesome Oscillator

DMI ( Adx )

Parabolic SAR

Waddah Attar Explosion (Shayankm)

Volatility Oscillator (Veryfid)

Damiani Volatility ( DV ) (RichardoSantos)

Stochastic

RSI

MACD

SSL Channel (ErwinBeckers)

Schaff Trend Cycle ( STC ) (LazyBear)

Chaikin Money Flow

Volume

Wolfpack Id (Darrellfischer1)

QQE Mod (Mihkhel00)

Hull Suite (Insilico)

Vortex Indicator

Total Info Indicator by MikePenzin

Install & Add to Chart

• Copy the script into Pine Editor → click Add to Chart .

• Open the ⚙️ Settings → Inputs to customize.

What It Does

• Displays key info in a floating table — trend, volume, ATR, RSI, stop loss, and more.

• Detects breakouts , smart SELL signals , and opening strength .

• Uses emojis and colours to make trends easy to read: 🟢 good, 🟡 neutral, 🔴 risky.

For Swing Traders

• Works best on Daily or 4H charts.

• Watch for 🟢 Uptrend + ⚡BUY / 🔥BUY breakout signals.

• Use ATR-based Stop Loss (shown in table).

• Avoid new entries a few days before earnings.

Suggested Setup

• 20/50/150 MA Lines: ON

• 200 MA Line: optional

• ATR Multiplier: 1.3

• Breakout Detection: ON (Volume + RSI + Trend filters)

• Smart SELLs: ON (RSI 70, EMA 20)

• Pivots: ON for quick swing levels

How to Read

• MA Row: 🟢 = price above MA (bullish).

• ATR/Stop Loss: Suggests where to place protective stop.

• Volume Info: Today’s vs 20-day average, plus pace.

• RSI & CCI: Shows momentum and overbought/oversold levels.

• Breakouts: ⚡BUY (early), 🔥BUY (confirmed).

• Smart SELLs: RSI🔴 / DIV🟣 / EMA🔵 mean potential exit zones.

Example Use

1️⃣ Find stocks with Uptrend 🟢 , rising volume, and ⚡BUY signal.

2️⃣ Enter near breakout; set Stop = shown level.

3️⃣ Take profits or trail when Smart SELLs appear or RSI peaks.

Tips

• Choose table corner under “Table Visualization.”

• Reduce clutter on small timeframes (turn off Pivots/200 MA).

• Use “Volume speed” to spot surging interest before breakouts.

• Compatible with most equities and ETFs.

Disclaimer

This script is for education & analysis only .

Not financial advice — always manage your own risk.

ajish cci indexthis script is based on cci.this one is working good in index.you can use the indicator for finding the trend change.well working in 1 minite.

Oscillator CandlesticksI've always wondered why we don't use candlesticks for oscillators...then I stopped wondering and made an oscillator with candlesticks.

The following oscillators are available as a proof of concept:

* Consumer Channel Index (CCI)

* Rate of Change (ROC)

* Relative Strength Index (RSI)

* Trend Strength Index (TSI)

You can add a moving average to the ohlc4 value of the oscillator and choose the type of the moving average and whether it should be influenced by volume.

Cnagda Pure Price ActionCnagda Pure Price Action (CPPA) indicator is a pure price action-based system designed to provide traders with real-time, dynamic analysis of the market. It automatically identifies key candles, support and resistance zones, and potential buy/sell signals by combining price, volume, and multiple popular trend indicators.

How Price Action & Volume Analysis Works

Silver Zone – Logic, Reason, and Trade Planning

Logic & Visualization:

The Silver Zone is created when the closing price is the lowest in the chosen window and volume is the highest in that window.

Visually, a large silver-colored box/rectangle appears on the chart.

Thick horizontal lines (top and bottom) are drawn at the high and low of that candle/bar, extending to the right.

Reasoning:

This combination typically occurs at strong “accumulation” or support areas:

Sellers push the price down to the lowest point, but aggressive buyers step in with high volume, absorbing supply.

Indicates potential exhaustion of selling and likely shift in market control to buyers.

How to Plan Trades Using Silver Zone:

Watch if price returns to the Silver Zone in the future: It often acts as powerful support.

Bullish entries (buys) can be planned when price tests or slightly pierces this zone, especially if new buy signals occur (like yellow/green candle labels).

Place your stop-loss below the bottom line of the Silver Zone.

Target: Look for the nearest resistance or opposing zone, or use indicator’s bullish label as confirmation.

Extra Tip:

Multiple touches of the Silver Zone reinforce its importance, but if price closes deeply below it with high volume, that’s a caution signal—support may be breaking.

Black Zone – Logic, Reason, and Trade Planning (as CPPA):

Logic & Visualization:

The Black Zone is created when the closing price is the highest in the chosen window and volume is the lowest in that window.

Visually, a large black-colored box/rectangle appears on the chart, along with thick horizontal lines at the top (high) and bottom (low) of the candle, extending to the right.

Reasoning:

This combination signals a strong “distribution” or resistance area:

Buyers push the price up to a local high, but low volume means there is not much follow-through or conviction in the move.

Often marks exhaustion where uptrend may pause or reverse, as sellers can soon step in.

How to Plan Trades Using Black Zone:

If price revisits the Black Zone in the future, it often acts as major resistance.

Bearish entries (sells) are considered when price is near, testing, or slightly above the Black Zone—especially if new sell signals appear (like blue/red candle labels).

Place your stop-loss just above the top line of the Black Zone.

Target: Nearest support zone (such as a Silver Zone) or next indicator’s bearish label.

Extra Tip:

Multiple touches of the Black Zone make it stronger, but if price closes far above with rising volume, be cautious—resistance might be breaking.

Support Line – Logic, Reason, and Trade Planning (as Cppa):

Logic & Visualization:

The Support Line is a dynamically drawn dashed line (usually blue) that marks key price levels where the market has previously shown significant buying interest.

The line is generated whenever a candle forms a high price with high volume (orange logic).

The script checks for historical pivot lows, past support zones, and even higher timeframe (HTF) supports, and then extends a blue dashed line from that price level to the right, labeling it (sometimes as “Prev Support Orange, HTF”).

Reasoning:

This line helps you visually identify where demand has been strong enough to hold price from falling further—essentially a floor in the market used by professional traders.

If price approaches or re-tests this line, there’s a good chance buyers will defend it again.

How to Plan Trades Using Support Line:

Watch for price to approach the Support Line during down moves. If you see a bullish candlestick pattern, buy labels (yellow/green), or other indicators aligning, this can be a high-probability entry zone.

Great for planning stop-loss for long trades: place stops just below this line.

Target: Next resistance zone, Black Zone, or the top of the last swing.

Extra Tip:

Multiple confirmations (support line + Silver Zone + bullish label) provide powerful entry signals.

If price closes strongly below the Support Line with volume, be cautious—support may be breaking, and a trend reversal or deeper correction could follow.

Resistance Line – Logic, Reason, and Trade Planning (from CPPA):

Logic & Visualization:

The Resistance Line is a dynamically drawn dashed line (usually purple or red) that identifies price levels where the market has previously faced significant selling pressure.

This line is created when a candle reaches a high price combined with high volume (orange logic), or from a historical pivot high/resistance,

The script also tracks higher timeframe (HTF) resistance lines, labeled as “Prev Resistance Orange, HTF,” and extends these dashed lines to the right across the chart.

Reasoning:

Resistance Lines are visual markers of “supply zones,” where buyers previously failed, and sellers took control.

If the price returns to this line later, sellers may get active again to defend this level, halting the uptrend.

How to Plan Trades Using Resistance Line:

Watch for price to approach the Resistance Line during up moves. If you see bearish candlestick patterns, sell labels (blue/red), or bearish indicator confirmation, this becomes a strong shorting opportunity.

Perfect for placing stop-loss in short trades—put your stop just above the Resistance Line.

Target: Next support zone (Silver Zone) or bottom of the last swing.

If the price breaks above with high volume, avoid shorting—resistance may be failing.

Extra Tip:

Multiple resistances (Resistance Line + Black Zone + bearish label) make short signals stronger.

Choppy movement around this line often signals indecision; wait for a clear rejection before entering trades.

Bullish / Bearish Label – Logic, Reason, and Trade Planning:

Logic & Visualization:

The indicator constantly calculates a "Bull Score" and a "Bear Score" based on several factors:

Trend direction from price slope

Confirmation by popular indicators (RSI, ADX, SAR, CMF, OBV, CCI, Bollinger Bands, TWAP)

Adaptive scoring (higher score for each bullish/bearish condition met)

If Bull Score > Bear Score, the chart displays a green "BULLISH" label (usually below the bar).

If Bear Score > Bull Score, the chart displays a red "BEARISH" label (usually above the bar).

If neither dominates, a "NEUTRAL" label appears.

Reasoning:

The labels summarize complex price action and indicator analysis into a simple, actionable sentiment cue:

Bullish: Majority of conditions indicate buying strength; trend is up.

Bearish: Majority signals show selling pressure; trend is down.

How to Use in Trade Planning:

Use the Bullish label as confirmation to enter or hold long (buy) positions, especially if near support/Silver Zone.

Use the Bearish label to enter/hold short (sell) positions, especially if near resistance/Black Zone.

For best results, combine with candle color, volume analysis, or other labels (yellow/green for buys, blue/red for sells).

Avoid trading against these labels unless you have strong confluence from zones/support levels.

Yellow Label (Buy Signal) – Logic, Reason & Trade Planning:

Logic & Visualization:

The yellow label appears below a candle (label.style_label_up, yloc.belowbar) and marks a potential buy signal.

Script conditions:

The candle must be a “yellow candle” (which means it’s at the local lowest close, not a high, with normal volume).

Volume is decreasing for 2 consecutive candles (current volume < previous volume, previous volume < second previous).

When these conditions are met, a yellow label is plotted below the candle.

Reasoning:

This scenario often marks the end of selling pressure and start of possible accumulation—buyers may be stepping in as sellers exhaust.

Decreasing volume during a local price low means selling is slowing, possibly hinting at a reversal.

How to Trade Using Yellow Label:

Entry: Consider buying at/just above the yellow-labeled candle’s close.

Stop-loss: A bit below the candle’s low (or Silver Zone line, if present).

Target: Next resistance level, Black Zone, or chart’s bullish label.

Extra Tip:

If the yellow label is found at/near a Silver Zone or Support Line, and trend is “Bullish,” the setup gets even stronger.

Avoid trading if overall indicator shows “Bearish.”

Green Label (Buy with Increasing Volume) – Logic, Reason & Trade Planning:

Logic & Visualization:

The green label is plotted below a candle (label.style_label_up, yloc.belowbar) and marks a strong buy signal.

Script conditions:

The candle must be a “yellow candle” (at the local lowest close, normal volume).

Volume is increasing for 2 consecutive candles (current volume > previous volume, previous volume > second previous).

When these conditions are met, a green label is plotted below the candle.

Reasoning:

This scenario signals that buyers are stepping in aggressively at a local price low—the end of a downtrend with strong, rising activity.

Increasing volume at a price low is a classic sign of accumulation, where institutions or large players may be buying.

How to Trade Using Green Label:

Entry: Consider buying at/just above the green-labeled candle’s close for a momentum-based reversal.

Stop-loss: Slightly below the candle’s low, or the Silver Zone/support line if present.

Target: Nearest resistance zone/Black Zone, indicator’s bullish label, or next swing high.

Extra Tip:

If the green label is near other supports (Silver Zone, Support Line), the setup is extra strong.

Use confirmation from Bullish labels or trend signals for best results.

Green label setups are suitable for quick, high momentum trades due to increasing volume

Blue Label (Sell Signal on Decreasing Volume) – Logic, Reason & Trade Planning:

Logic & Visualization:

The blue label is plotted above a candle (label.style_label_down, yloc.abovebar) as a potential sell signal.

Script conditions:

The candle is a “blue candle” (local highest close, but not also lowest, and volume is neither highest nor lowest).

Volume is decreasing over 2 consecutive candles (current volume < previous, previous < two ago).

When these match, a blue label appears above the candle.

Reasoning:

This typically signals buyer exhaustion at a local high: price has gone up, but volume is dropping, suggesting big players may not be buying any more at these levels.

The trend is losing strength, and a reversal or pullback is likely.

How to Trade Using Blue Label:

Entry: Look to sell at/just below the candle with the blue label.

Stop-loss: Just above the candle’s high (or above the Black Zone/resistance if present).

Target: Nearest support, Silver Zone, or a swing low.

Extra Tip:

Blue label signals are stronger if they appear near Black Zones or Resistance Lines, or when the general market label is "Bearish."

As with buy setups, always check for confirmation from trend or volume before trading aggressively.

Blue Label (Sell Signal on Decreasing Volume) – Logic, Reason & Trade Planning:

Logic & Visualization:

The blue label is plotted above a candle (label.style_label_down, yloc.abovebar) as a potential sell signal.

Script conditions:

The candle is a “blue candle” (local highest close, but not also lowest, and volume is neither highest nor lowest).

Volume is decreasing over 2 consecutive candles (current volume < previous, previous < two ago).

When these match, a blue label appears above the candle.

Reasoning:

This typically signals buyer exhaustion at a local high: price has gone up, but volume is dropping, suggesting big players may not be buying any more at these levels.

The trend is losing strength, and a reversal or pullback is likely.

How to Trade Using Blue Label:

Entry: Look to sell at/just below the candle with the blue label.

Stop-loss: Just above the candle’s high (or above the Black Zone/resistance if present).

Target: Nearest support, Silver Zone, or a swing low.

Extra Tip:

Blue label signals are stronger if they appear near Black Zones or Resistance Lines, or when the general market label is "Bearish."

As with buy setups, always check for confirmation from trend or volume before trading aggressively.

Here’s a summary of all key chart labels, zones, and trading logic of your Price Action script:

Silver Zone: Powerful support zone. Created at lowest close + highest volume. Best for buy entries near its lines.

Black Zone: Strong resistance zone. Created at highest close + lowest volume. Ideal for short trades near its levels.

Support Line: Blue dashed line at historical demand; buyers defend here. Look for bullish setups when price approaches.

Resistance Line: Purple/red dashed line at supply; sellers defend here. Great for bearish setups when price nears.

Bullish/Bearish Labels: Summarize trend direction using price action + multiple indicator confirmations. Plan buys, holds on bullish; sells, shorts on bearish.

Yellow Label: Buy signal on decreasing volume and local price low. Entry above candle, stop below, target next resistance.

Green Label: Strong buy on increasing volume at a price low. Entry for momentum trade, stop below, target next zone.

Blue Label: Sell signal on dropping volume and local price high. Entry below candle, stop above, target next support.

Best Practices:

Always combine zone/label signals for higher probability trades.

Use stop-loss near zones/lines for risk management.

Prefer trading in the trend direction (bullish/bearish label agrees with your entry).

if Any Question, Suggestion Feel free to ask

Disclaimer:

All information provided by this indicator is for educational and analysis purposes only, and should not be considered financial advice.

Tunç ŞatıroğluTunç Şatıroğlu's Technical Analysis Suite

Description:

This comprehensive Pine Script indicator, inspired by the technical analysis teachings of Tunç Şatıroğlu, integrates six powerful TradingView indicators into a single, user-friendly suite for robust trend, momentum, and divergence analysis. Each component has been carefully selected and enhanced by beytun to improve functionality, performance, and visual clarity, aligning with Şatıroğlu's approach to technical analysis. The default configuration is meticulously set to match the exact settings of the individual indicators as used by Tunç Şatıroğlu in his training, ensuring authenticity and ease of use for followers of his methodology. Whether you're a beginner or an experienced trader, this suite provides a versatile toolkit for analyzing markets across multiple timeframes.

Included Indicators:

1. WaveTrend with Crosses (by LazyBear, modified): A momentum oscillator that identifies overbought/oversold conditions and trend reversals with clear buy/sell signals via crosses and bar color highlights.

2. Kaufman Adaptive Moving Average (KAMA) (by HPotter, modified): A dynamic moving average that adapts to market volatility, offering a smoother trend-following signal.

3. SuperTrend (by Alex Orekhov, modified): A trend-following indicator that plots dynamic support/resistance levels with buy/sell signals and optional wicks for enhanced accuracy.

4. Nadaraya-Watson Envelope (by LuxAlgo, modified): A non-linear envelope that highlights potential reversals with customizable repainting options for smoother outputs.

5. Divergence for Many Indicators v4 (by LonesomeTheBlue, modified): Detects regular and hidden divergences across multiple indicators (MACD, RSI, Stochastic, CCI, Momentum, OBV, VWMA, CMF, MFI, and more) for early reversal signals.

6. Ichimoku Cloud (TradingView built-in, modified): A multi-faceted indicator for trend direction, support/resistance, and momentum, with enhanced visuals for the Kumo Cloud.

Key Features:

- Authentic Default Settings : Pre-configured to mirror the exact parameters used by Tunç Şatıroğlu for each indicator, ensuring alignment with his proven technical analysis approach.

- Customizable Settings : Enable/disable individual indicators and fine-tune parameters to suit your trading style while retaining the option to revert to Şatıroğlu’s defaults.

- Enhanced User Experience : Modifications improve visual clarity, performance, and usability, with options like repainting smoothing for Nadaraya-Watson and adjustable Ichimoku projection periods.

- Multi-Timeframe Analysis : Combines trend-following, momentum, and divergence tools for a holistic view of market dynamics.

- Alert Conditions : Built-in alerts for SuperTrend direction changes, buy/sell signals, and divergence detections to keep you informed.

- Visual Clarity : Overlays (KAMA, SuperTrend, Nadaraya-Watson, Ichimoku) and pane-based indicators (WaveTrend, Divergences) are clearly distinguished, with customizable colors and styles.

Notes:

- The Nadaraya-Watson Envelope and Ichimoku Cloud may repaint in their default modes. Use the "Repainting Smoothing" option for Nadaraya-Watson or adjust Ichimoku settings to mitigate repainting if preferred.

- Published under the MIT License, with components licensed under GPL-3.0 (SuperTrend), CC BY-NC-SA 4.0 (Nadaraya-Watson), MPL 2.0 (Divergence), and TradingView's terms (Ichimoku Cloud).

Usage:

Add this indicator to your TradingView chart to leverage Tunç Şatıroğlu’s exact indicator configurations out of the box. Customize settings as needed to align with your strategy, and use the combined signals to identify trends, reversals, and divergences. Ideal for traders following Şatıroğlu’s methodologies or anyone seeking a powerful, all-in-one technical analysis tool.

Credits:

Original authors: LazyBear, HPotter, Alex Orekhov, LuxAlgo, LonesomeTheBlue, and TradingView.

Modifications and integration by beytun .

License:

Published under the MIT License, incorporating code under GPL-3.0, CC BY-NC-SA 4.0, MPL 2.0, and TradingView’s terms where applicable.

Commodity Channel Index (CCI)An indicator with increased convenience and customization options. Effective for scalping.

AVGO Advanced Day Trading Strategy📈 Overview

The AVGO Advanced Day Trading Strategy is a comprehensive, multi-timeframe trading system designed for active day traders seeking consistent performance with robust risk management. Originally optimized for AVGO (Broadcom), this strategy adapts well to other liquid stocks and can be customized for various trading styles.

🎯 Key Features

Multiple Entry Methods

EMA Crossover: Classic trend-following signals using fast (9) and medium (16) EMAs

MACD + RSI Confluence: Momentum-based entries combining MACD crossovers with RSI positioning

Price Momentum: Consecutive price action patterns with EMA and RSI confirmation

Hybrid System: Advanced multi-trigger approach combining all methodologies

Advanced Technical Arsenal

When enabled, the strategy analyzes 8+ additional indicators for confluence:

Volume Price Trend (VPT): Measures volume-weighted price momentum

On-Balance Volume (OBV): Tracks cumulative volume flow

Accumulation/Distribution Line: Identifies institutional money flow

Williams %R: Momentum oscillator for entry timing

Rate of Change Suite: Multi-timeframe momentum analysis (5, 14, 18 periods)

Commodity Channel Index (CCI): Cyclical turning points

Average Directional Index (ADX): Trend strength measurement

Parabolic SAR: Dynamic support/resistance levels

🛡️ Risk Management System

Position Sizing

Risk-based position sizing (default 1% per trade)

Maximum position limits (default 25% of equity)

Daily loss limits with automatic position closure

Multiple Profit Targets

Target 1: 1.5% gain (50% position exit)

Target 2: 2.5% gain (30% position exit)

Target 3: 3.6% gain (20% position exit)

Configurable exit percentages and target levels

Stop Loss Protection

ATR-based or percentage-based stop losses

Optional trailing stops

Dynamic stop adjustment based on market volatility

📊 Technical Specifications

Primary Indicators

EMAs: 9 (Fast), 16 (Medium), 50 (Long)

VWAP: Volume-weighted average price filter

RSI: 6-period momentum oscillator

MACD: 8/13/5 configuration for faster signals

Volume Confirmation

Volume filter requiring 1.6x average volume

19-period volume moving average baseline

Optional volume confirmation bypass

Market Structure Analysis

Bollinger Bands (20-period, 2.0 multiplier)

Squeeze detection for breakout opportunities

Fractal and pivot point analysis

⏰ Trading Hours & Filters

Time Management

Configurable trading hours (default: 9:30 AM - 3:30 PM EST)

Weekend and holiday filtering

Session-based trade management

Market Condition Filters

Trend alignment requirements

VWAP positioning filters

Volatility-based entry conditions

📱 Visual Features

Information Dashboard

Real-time display of:

Current entry method and signals

Bullish/bearish signal counts

RSI and MACD status

Trend direction and strength

Position status and P&L

Volume and time filter status

Chart Visualization

EMA plots with customizable colors

Entry signal markers

Target and stop level lines

Background color coding for trends

Optional Bollinger Bands and SAR display

🔔 Alert System

Entry Alerts

Customizable alerts for long and short entries

Method-specific alert messages

Signal confluence notifications

Advanced Alerts

Strong confluence threshold alerts

Custom alert messages with signal counts

Risk management alerts

⚙️ Customization Options

Strategy Parameters

Enable/disable long or short trades

Adjustable risk parameters

Multiple entry method selection

Advanced indicator on/off toggle

Visual Customization

Color schemes for all indicators

Dashboard position and size options

Show/hide various chart elements

Background color preferences

📋 Default Settings

Initial Capital: $100,000

Commission: 0.1%

Default Position Size: 10% of equity

Risk Per Trade: 1.0%

RSI Length: 6 periods

MACD: 8/13/5 configuration

Stop Loss: 1.1% or ATR-based

🎯 Best Use Cases

Day Trading: Designed for intraday opportunities

Swing Trading: Adaptable for longer-term positions

Momentum Trading: Excellent for trending markets

Risk-Conscious Trading: Built-in risk management protocols

⚠️ Important Notes

Paper Trading Recommended: Test thoroughly before live trading

Market Conditions: Performance varies with market volatility

Customization: Adjust parameters based on your risk tolerance

Educational Purpose: Use as a learning tool and customize for your needs

🏆 Performance Features

Detailed performance metrics

Trade-by-trade analysis capability

Customizable risk/reward ratios

Comprehensive backtesting support

This strategy is for educational purposes. Past performance does not guarantee future results. Always practice proper risk management and consider your financial situation before trading.

Trend Magic EMA RMI Trend Sniper📌 Indicator Name:

Trend Magic + EMA + MA Smoothing + RMI Trend Sniper

📝 Description:

This is a multi-functional trend and momentum indicator that combines four powerful tools into a single overlay:

Trend Magic – Plots a dynamic support/resistance line based on CCI and ATR.

Helps identify trend direction (green = bullish, red = bearish).

Acts as a trailing stop or dynamic level for trade entries/exits.

Exponential Moving Average (EMA) – Smooths price data to highlight the underlying trend.

Customizable length, source, and offset.

Serves as a trend filter or moving support/resistance.

MA Smoothing + Bollinger Bands (Optional) – Adds a secondary smoothing filter based on your choice of SMA, EMA, WMA, VWMA, or SMMA.

Optional Bollinger Bands visualize volatility expansion/contraction.

Great for spotting consolidations and breakout opportunities.

RMI Trend Sniper – A momentum-based system combining RSI and MFI.

Highlights bullish (green) or bearish (red) conditions.

Plots a Range-Weighted Moving Average (RWMA) channel to gauge price positioning.

Provides visual BUY/SELL labels and optional bar coloring for fast decision-making.

📊 Uses & Trading Applications:

✅ Trend Identification: Spot the dominant market direction quickly with Trend Magic & EMA.

✅ Momentum Confirmation: RMI Sniper helps confirm whether the market has strong bullish or bearish pressure.

✅ Dynamic Support/Resistance: Trend Magic & EMA act as adaptive levels for stop-loss or trailing positions.

✅ Volatility Analysis: Optional Bollinger Bands show squeezes and potential breakout setups.

✅ Entry/Exit Signals: BUY/SELL alerts and color-coded candles make spotting trade opportunities simple.

💡 Best Use Cases:

Swing Trading: Follow Trend Magic + EMA alignment for higher probability trades.

Scalping/Intraday: Use RMI signals with bar coloring for quick momentum entries.

Trend Following Strategies: Ride trends until Trend Magic flips direction.

Breakout Trading: Watch for price closing outside the Bollinger Bands with RMI confirmation.

Guppy MMA [Alpha Extract]A sophisticated trend-following and momentum assessment system that constructs dynamic trader and investor sentiment channels using multiple moving average groups with advanced scoring mechanisms and smoothed CCI-style visualizations for optimal market trend analysis. Utilizing enhanced dual-group methodology with threshold-based trend detection, this indicator delivers institutional-grade GMMA analysis that adapts to varying market conditions while providing high-probability entry and exit signals through crossover and extreme value detection with comprehensive visual mapping and alert integration.

🔶 Advanced Channel Construction

Implements dual-group architecture using short-term and long-term moving averages as foundation points, applying customizable MA types to reduce noise and score-based averaging for sentiment-responsive trend channels. The system creates trader channels from shorter periods and investor channels from longer periods with configurable periods for optimal market reaction zones.

// Core Channel Calculation Framework

maType = input.string("EMA", title="Moving Average Type", options= )

// Short-Term Group Construction

stMA1 = ma(close, st1, maType)

stMA2 = ma(close, st2, maType)

// Long-Term Group Construction

ltMA1 = ma(close, lt1, maType)

ltMA2 = ma(close, lt2, maType)

// Smoothing Application

smoothedavg = ma(overallAvg, 10, maType)

🔶 Volatility-Adaptive Zone Framework

Features dynamic score-based averaging that expands sentiment signals during strong trend periods and contracts during consolidation phases, preventing false signals while maintaining sensitivity to genuine momentum shifts. The dual-group averaging system optimizes zone boundaries for realistic market behavior patterns.

// Dynamic Sentiment Adjustment

shortTermAvg = (stScore1 + stScore2 + ... + stScore11) / 11

longTermAvg = (ltScore1 + ltScore2 + ... + ltScore11) / 11

// Dual-Group Zone Optimization

overallAvg = (shortTermAvg + longTermAvg) / 2

allMAAvg = (shortTermAvg * 11 + longTermAvg * 11) / 22

🔶 Step-Like Boundary Evolution

Creates threshold-based trend boundaries that update on smoothed average changes, providing visual history of evolving bullish and bearish levels with performance-optimized threshold management limited to key zones for clean chart presentation and efficient processing.

🔶 Comprehensive Signal Detection

Generates buy and sell signals through sophisticated crossover analysis, monitoring smoothed average interaction with zero-line and thresholds for high-probability entry and exit identification. The system distinguishes between trend continuation and reversal patterns with precision timing.

🔶 Enhanced Visual Architecture

Provides translucent zone fills with gradient intensity scaling, threshold-based historical boundaries, and dynamic background highlighting that activates upon trend changes. The visual system uses institutional color coding with green bullish zones and red bearish zones for intuitive market structure interpretation.

🔶 Intelligent Zone Management

Implements automatic trend relevance filtering, displaying signals only when smoothed average proximity warrants analysis attention. The system maintains optimal performance through smart averaging management and historical level tracking with configurable MA periods for various market conditions.

🔶 Multi-Dimensional Analysis Framework