Canuck Trading Trader StrategyCanuck Trading Trader Strategy

Overview

The Canuck Trading Trader Strategy is a high-performance, trend-following trading system designed for NASDAQ:TSLA on a 15-minute timeframe. Optimized for precision and profitability, this strategy leverages short-term price trends to capture consistent gains while maintaining robust risk management. Ideal for traders seeking an automated, data-driven approach to trading Tesla’s volatile market, it delivers strong returns with controlled drawdowns.

Key Features

Trend-Based Entries: Identifies short-term trends using a 2-candle lookback period and a minimum trend strength of 0.2%, ensuring responsive trade signals.

Risk Management: Includes a configurable 3.0% stop-loss to cap losses and a 2.0% take-profit to lock in gains, balancing risk and reward.

High Precision: Utilizes bar magnification for accurate backtesting, reflecting realistic trade execution with 1-tick slippage and 0.1 commission.

Clean Interface: No on-chart indicators, providing a distraction-free trading experience focused on performance.

Flexible Sizing: Allocates 10% of equity per trade with support for up to 2 simultaneous positions (pyramiding).

Performance Highlights

Backtested from March 1, 2024, to June 20, 2025, on NASDAQ:TSLA (15-minute timeframe) with $1,000,000 initial capital:

Net Profit: $2,279,888.08 (227.99%)

Win Rate: 52.94% (3,039 winning trades out of 5,741)

Profit Factor: 3.495

Max Drawdown: 2.20%

Average Winning Trade: $1,050.91 (0.55%)

Average Losing Trade: $338.20 (0.18%)

Sharpe Ratio: 2.468

Note: Past performance is not indicative of future results. Always validate with your own backtesting and forward testing.

Usage Instructions

Setup:

Apply the strategy to a NASDAQ:TSLA 15-minute chart.

Ensure your TradingView account supports bar magnification for accurate results.

Configuration:

Lookback Candles: Default is 2 (recommended).

Min Trend Strength: Set to 0.2% for optimal trade frequency.

Stop Loss: Default 3.0% to cap losses.

Take Profit: Default 2.0% to secure gains.

Order Size: 10% of equity per trade.

Pyramiding: Allows up to 2 orders.

Commission: Set to 0.1.

Slippage: Set to 1 tick.

Enable "Recalculate After Order is Filled" and "Recalculate on Every Tick" in backtest settings.

Backtesting:

Run backtests over March 1, 2024, to June 20, 2025, to verify performance.

Adjust stop-loss (e.g., 2.5%) or take-profit (e.g., 1–3%) to suit your risk tolerance.

Live Trading:

Use with a compatible broker or TradingView alerts for automated execution.

Monitor execution for slippage or latency, especially given the high trade frequency (5,741 trades).

Validate in a demo account before deploying with real capital.

Risk Disclosure

Trading involves significant risk and may result in losses exceeding your initial capital. The Canuck Trading Trader Strategy is provided for educational and informational purposes only. Users are responsible for their own trading decisions and should conduct thorough testing before using in live markets. The strategy’s high trade frequency requires reliable execution infrastructure to minimize slippage and latency.

Cerca negli script per "backtesting"

Optimized Heikin Ashi Strategy with Buy/Sell OptionsStrategy Name:

Optimized Heikin Ashi Strategy with Buy/Sell Options

Description:

The Optimized Heikin Ashi Strategy is a trend-following strategy designed to capitalize on market trends by utilizing the smoothness of Heikin Ashi candles. This strategy provides flexible options for trading, allowing users to choose between Buy Only (long-only), Sell Only (short-only), or using both in alternating conditions based on the Heikin Ashi candle signals. The strategy works on any market, but it performs especially well in markets where trends are prevalent, such as cryptocurrency or Forex.

This script offers customizable parameters for the backtest period, Heikin Ashi timeframe, stop loss, and take profit levels, allowing traders to optimize the strategy for their preferred markets or assets.

Key Features:

Trade Type Options:

Buy Only: Enter a long position when a green Heikin Ashi candle appears and exit when a red candle appears.

Sell Only: Enter a short position when a red Heikin Ashi candle appears and exit when a green candle appears.

Stop Loss and Take Profit:

Customizable stop loss and take profit percentages allow for flexible risk management.

The default stop loss is set to 2%, and the default take profit is set to 4%, maintaining a favorable risk/reward ratio.

Heikin Ashi Timeframe:

Traders can select the desired timeframe for Heikin Ashi candle calculation (e.g., 4-hour Heikin Ashi candles for a 1-hour chart).

The strategy smooths out price action and reduces noise, providing clearer signals for entry and exit.

Inputs:

Backtest Start Date / End Date: Specify the period for testing the strategy’s performance.

Heikin Ashi Timeframe: Select the timeframe for Heikin Ashi candle generation. A higher timeframe helps smooth the trend, which is beneficial for trading lower timeframes.

Stop Loss (in %) and Take Profit (in %): Enable or disable stop loss and take profit, and adjust the levels based on market conditions.

Trade Type: Choose between Buy Only or Sell Only based on your market outlook and strategy preference.

Strategy Performance:

In testing with BTC/USD, this strategy performed well in a 4-hour Heikin Ashi timeframe applied on a 1-hour chart over a period from January 1, 2024, to September 12, 2024. The results were as follows:

Initial Capital: 1 USD

Order Size: 100% of equity

Net Profit: +30.74 USD (3,073.52% return)

Percent Profitable: 78.28% of trades were winners.

Profit Factor: 15.825, indicating that the strategy's profitable trades far outweighed its losses.

Max Drawdown: 4.21%, showing low risk exposure relative to the large profit potential.

This strategy is ideal for both beginner and advanced traders who are looking to follow trends and avoid market noise by using Heikin Ashi candles. It is also well-suited for traders who prefer automated risk management through the use of stop loss and take profit levels.

Recommended Use:

Best Markets: This strategy works well on trending markets like cryptocurrency, Forex, or indices.

Timeframes: Works best when applied to lower timeframes (e.g., 1-hour chart) with a higher Heikin Ashi timeframe (e.g., 4-hour candles) to smooth out price action.

Leverage: The strategy performs well with leverage, but users should consider using 2x to 3x leverage to avoid excessive risk and potential liquidation. The strategy's low drawdown allows for moderate leverage use while maintaining risk control.

Customization: Traders can adjust the stop loss and take profit percentages based on their risk appetite and market conditions. A default setting of a 2% stop loss and 4% take profit provides a balanced risk/reward ratio.

Notes:

Risk Management: Traders should enable stop loss and take profit settings to maintain effective risk management and prevent large drawdowns during volatile market conditions.

Optimization: This strategy can be further optimized by adjusting the Heikin Ashi timeframe and risk parameters based on specific market conditions and assets.

Backtesting: The built-in backtesting functionality allows traders to test the strategy across different market conditions and historical data to ensure robustness before applying it to live trading.

How to Apply:

Select your preferred market and chart.

Choose the appropriate Heikin Ashi timeframe based on the chart's timeframe. (e.g., use 4-hour Heikin Ashi candles for 1-hour chart trends).

Adjust stop loss and take profit based on your risk management preference.

Run backtesting to evaluate its performance before applying it in live trading.

This strategy can be further modified and optimized based on personal trading style and market conditions. It’s important to monitor performance regularly and adjust settings as needed to align with market behavior.

Liquidity Maxing [JOAT]Liquidity Maxing - Institutional Liquidity Matrix

Introduction

Liquidity Maxing is an open-source strategy for TradingView built around institutional market structure concepts. It identifies structural shifts, evaluates trades through multi-factor confluence, and implements layered risk controls.

The strategy is designed for swing trading on 4-hour timeframes, focusing on how institutional order flow manifests in price action through structure breaks, inducements, and liquidity sweeps.

Core Functionality

Liquidity Maxing performs three primary functions:

Tracks market structure to identify when control shifts between buyers and sellers

Scores potential trades using an eight-factor confluence system

Manages position sizing and risk exposure dynamically based on volatility and user-defined limits

The goal is selective trading when multiple conditions align, rather than frequent entries.

Market Structure Engine

The structure engine tracks three key events:

Break of Structure (BOS): Price pushes beyond a prior pivot in the direction of trend

Change of Character (CHoCH): Control flips from bullish to bearish or vice versa

Inducement Sweeps (IDM): Market briefly runs stops against trend before moving in the real direction

The structure module continuously updates strong highs and lows, labeling structural shifts visually. IDM markers are optional and disabled by default to maintain chart clarity.

The trade engine requires valid structure alignment before considering entries. No structure, no trade.

Eight-Factor Confluence System

Instead of relying on a single indicator, Liquidity Maxing uses an eight-factor scoring system:

Structure alignment with current trend

RSI within healthy bands (different ranges for up and down trends)

MACD momentum agreement with direction

Volume above adaptive baseline

Price relative to main trend EMA

Session and weekend filter (configurable)

Volatility expansion/contraction via ATR shifts

Higher-timeframe EMA confirmation

Each factor contributes one point to the confluence score. The default minimum confluence threshold is 6 out of 8, but you can adjust this from 1-8 based on your preference for trade frequency versus selectivity.

Only when structure and confluence agree does the strategy proceed to risk evaluation.

Dynamic Risk Management

Risk controls are implemented in multiple layers:

ATR-based stops and targets with configurable risk-to-reward ratio (default 2:1)

Volatility-adjusted position sizing to maintain consistent risk per trade as ranges expand or compress

Daily and weekly risk budgets that halt new entries once thresholds are reached

Correlation cooldown to prevent clustered trades in the same direction

Global circuit breaker with maximum drawdown limit and emergency kill switch

If any guardrail is breached, the strategy will not open new positions. The dashboard clearly displays risk state for transparency.

Market Presets

The strategy includes configuration presets optimized for different market types:

Crypto (BTC/ETH): RSI bands 70/30, volume multiplier 1.2, enhanced ATR scaling

Forex Majors: RSI bands 75/25, volume multiplier 1.5

Indices (SPY/QQQ): RSI bands 70/30, volume multiplier 1.3

Custom: Default values for user customization

For crypto assets, the strategy automatically applies ATR volatility scaling to account for higher volatility characteristics.

Monitoring and Dashboards

The strategy includes optional monitoring layers:

Risk Operations Dashboard (top-right):

Trend state

Confluence score

ATR value

Current position size percentage

Global drawdown

Daily and weekly risk consumption

Correlation guard state

Alert mode status

Performance Console (top-left):

Net profit

Current equity

Win rate percentage

Average trade value

Sharpe-style ratio (rolling 50-bar window)

Profit factor

Open trade count

Optional risk tint on chart background provides visual indication of "safe to trade" versus "halted" state.

All visualization elements can be toggled on/off from the inputs for clean chart viewing or full telemetry during parameter tuning.

Alerts and Automation

The strategy supports alert integration with two formats:

Standard alerts: Human-readable messages for long, short, and risk-halt conditions

Webhook format: JSON-formatted payloads ready for external execution systems (optional)

Alert messages are predictable and unambiguous, suitable for manual review or automated forwarding to execution engines.

Built-in Validation Suite

The strategy includes an optional validation layer that can be enabled from inputs. It checks:

Internal consistency of structure and confluence metrics

Sanity and ordering of risk parameters

Position sizing compliance with user-defined floors and caps

This validation is optional and not required for trading, but provides transparency into system operation during development or troubleshooting.

Strategy Parameters

Market Presets:

Configuration Preset: Choose between Crypto (BTC/ETH), Forex Majors, Indices (SPY/QQQ), or Custom

Market Structure Architecture:

Pivot Length: Default 5 bars

Filter by Inducement (IDM): Default enabled

Visualize Structure: Default enabled

Structure Lookback: Default 50 bars

Risk & Capital Preservation:

Risk:Reward Ratio: Default 2.0

ATR Period: Default 14

ATR Multiplier (Stop): Default 2.0

Max Drawdown Circuit Breaker: Default 10%

Risk per Trade (% Equity): Default 1.5%

Daily Risk Limit: Default 6%

Weekly Risk Limit: Default 12%

Min Position Size (% Equity): Default 0.25%

Max Position Size (% Equity): Default 5%

Correlation Cooldown (bars): Default 3

Emergency Kill Switch: Default disabled

Signal Confluence:

RSI Length: Default 14

Trend EMA: Default 200

HTF Confirmation TF: Default Daily

Allow Weekend Trading: Default enabled

Minimum Confluence Score (0-8): Default 6

Backtesting Considerations

When backtesting this strategy, consider the following:

Commission: Default 0.05% (adjustable in strategy settings)

Initial Capital: Default $100,000 (adjustable)

Position Sizing: Uses percentage of equity (default 2% per trade)

Timeframe: Optimized for 4-hour charts, though can be tested on other timeframes

Results will vary significantly based on:

Market conditions and volatility regimes

Parameter settings, especially confluence threshold

Risk limit configuration

Symbol characteristics (crypto vs forex vs equities)

Past performance does not guarantee future results. Win rate, profit factor, and other metrics should be evaluated in context of drawdown periods, trade frequency, and market conditions.

How to Use This Strategy

This is a framework that requires understanding and parameter tuning, not a one-size-fits-all solution.

Recommended workflow:

Start on 4-hour timeframe with default parameters and appropriate market preset

Run backtests and study performance console metrics: focus on drawdown behavior, win rate, profit factor, and trade frequency

Adjust confluence threshold to match your risk appetite—higher thresholds mean fewer but more selective trades

Set realistic daily and weekly risk budgets appropriate for your account size and risk tolerance

Consider ATR multiplier adjustments based on market volatility characteristics

Only connect alerts or automation after thorough testing and parameter validation

Treat this as a risk framework with an integrated entry engine, not merely an entry signal generator. The risk controls are as important as the trade signals.

Strategy Limitations

Designed for swing trading timeframes; may not perform optimally on very short timeframes

Requires sufficient market structure to identify pivots; may struggle in choppy or low-volatility environments

Crypto markets require different parameter tuning than traditional markets

Risk limits may prevent entries during favorable setups if daily/weekly budgets are exhausted

Correlation cooldown may delay entries that would otherwise be valid

Backtesting results depend on data quality and may not reflect live trading with slippage

Design Philosophy

Many indicators tell you when price crossed a moving average or RSI left oversold. This strategy addresses questions institutional traders ask:

Who is in control of the market right now?

Is this move structurally significant or just noise?

Do I want to add more risk given what I've already done today/week?

If I'm wrong, exactly how painful can this be?

The strategy provides disciplined, repeatable answers to these questions through systematic structure analysis, confluence filtering, and multi-layer risk management.

Technical Implementation

The strategy uses Pine Script v6 with:

Custom types for structure, confluence, and risk state management

Functional programming approach for reusable calculations

State management through persistent variables

Optional visual elements that can be toggled independently

The code is open-source and can be modified to suit individual needs. All important logic is visible in the source code.

Disclaimer

This script is provided for educational and informational purposes only. It is not intended as financial, investment, trading, or any other type of advice or recommendation. Trading involves substantial risk of loss and is not suitable for all investors. Past performance, whether real or indicated by historical tests of strategies, is not indicative of future results.

No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between backtested results and actual results subsequently achieved by any particular trading strategy.

The user should be aware of the risks involved in trading and should trade only with risk capital. The authors and publishers of this script are not responsible for any losses or damages, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on this script.

This strategy uses technical analysis methods and indicators that are not guaranteed to be accurate or profitable. Market conditions change, and strategies that worked in the past may not work in the future. Users should thoroughly test any strategy in a paper trading environment before risking real capital.

Commission and slippage settings in backtests may not accurately reflect live trading conditions. Real trading results will vary based on execution quality, market liquidity, and other factors not captured in backtesting.

The user assumes full responsibility for all trading decisions made using this script. Always consult with a qualified financial advisor before making investment decisions.

Enjoy - officialjackofalltrades

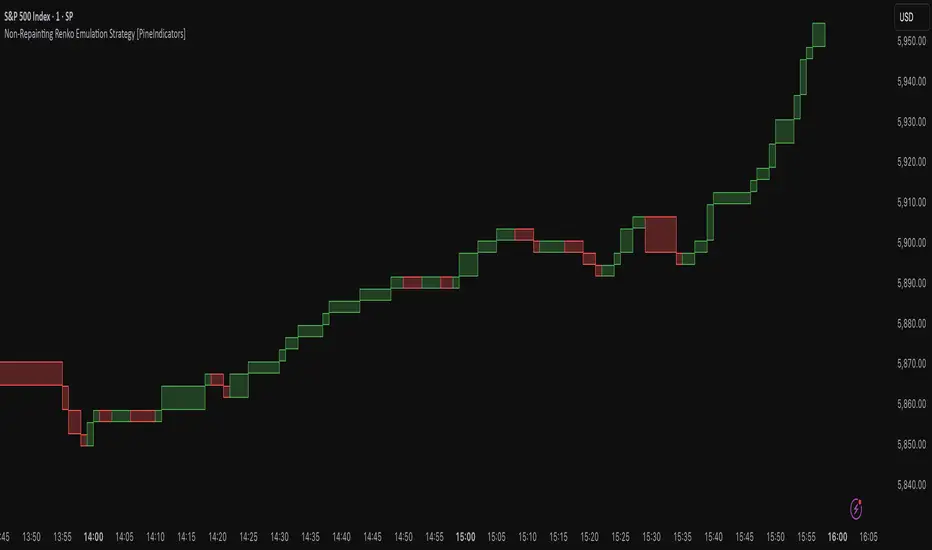

Non-Repainting Renko Emulation Strategy [PineIndicators]Introduction: The Repainting Problem in Renko Strategies

Renko charts are widely used in technical analysis for their ability to filter out market noise and emphasize price trends. Unlike traditional candlestick charts, which are based on fixed time intervals, Renko charts construct bricks only when price moves by a predefined amount. This makes them useful for trend identification while reducing small fluctuations.

However, Renko-based trading strategies often fail in live trading due to a fundamental issue: repainting .

Why Do Renko Strategies Repaint?

Most trading platforms, including TradingView, generate Renko charts retrospectively based on historical price data. This leads to the following issues:

Renko bricks can change or disappear when new data arrives.

Backtesting results do not reflect real market conditions. Strategies may appear highly profitable in backtests because historical data is recalculated with hindsight.

Live trading produces different results than backtesting. Traders cannot know in advance whether a new Renko brick will form until price moves far enough.

Objective of the Renko Emulator

This script simulates Renko behavior on a standard time-based chart without repainting. Instead of using TradingView’s built-in Renko charting, which recalculates past bricks, this approach ensures that once a Renko brick is formed, it remains unchanged .

Key benefits:

No past bricks are recalculated or removed.

Trading strategies can execute reliably without false signals.

Renko-based logic can be applied on a time-based chart.

How the Renko Emulator Works

1. Parameter Configuration & Initialization

The script defines key user inputs and variables:

brickSize : Defines the Renko brick size in price points, adjustable by the user.

renkoPrice : Stores the closing price of the last completed Renko brick.

prevRenkoPrice : Stores the price level of the previous Renko brick.

brickDir : Tracks the direction of Renko bricks (1 = up, -1 = down).

newBrick : A boolean flag that indicates whether a new Renko brick has been formed.

brickStart : Stores the bar index at which the current Renko brick started.

2. Identifying Renko Brick Formation Without Repainting

To ensure that the strategy does not repaint, Renko calculations are performed only on confirmed bars.

The script calculates the difference between the current price and the last Renko brick level.

If the absolute price difference meets or exceeds the brick size, a new Renko brick is formed.

The new Renko price level is updated based on the number of bricks that would fit within the price movement.

The direction (brickDir) is updated , and a flag ( newBrick ) is set to indicate that a new brick has been formed.

3. Visualizing Renko Bricks on a Time-Based Chart

Since TradingView does not support live Renko charts without repainting, the script uses graphical elements to draw Renko-style bricks on a standard chart.

Each time a new Renko brick forms, a colored rectangle (box) is drawn:

Green boxes → Represent bullish Renko bricks.

Red boxes → Represent bearish Renko bricks.

This allows traders to see Renko-like formations on a time-based chart, while ensuring that past bricks do not change.

Trading Strategy Implementation

Since the Renko emulator provides a stable price structure, it is possible to apply a consistent trading strategy that would otherwise fail on a traditional Renko chart.

1. Entry Conditions

A long trade is entered when:

The previous Renko brick was bearish .

The new Renko brick confirms an upward trend .

There is no existing long position .

A short trade is entered when:

The previous Renko brick was bullish .

The new Renko brick confirms a downward trend .

There is no existing short position .

2. Exit Conditions

Trades are closed when a trend reversal is detected:

Long trades are closed when a new bearish brick forms.

Short trades are closed when a new bullish brick forms.

Key Characteristics of This Approach

1. No Historical Recalculation

Once a Renko brick forms, it remains fixed and does not change.

Past price action does not shift based on future data.

2. Trading Strategies Operate Consistently

Since the Renko structure is stable, strategies can execute without unexpected changes in signals.

Live trading results align more closely with backtesting performance.

3. Allows Renko Analysis Without Switching Chart Types

Traders can apply Renko logic without leaving a standard time-based chart.

This enables integration with indicators that normally cannot be used on traditional Renko charts.

Considerations When Using This Strategy

Trade execution may be delayed compared to standard Renko charts. Since new bricks are only confirmed on closed bars, entries may occur slightly later.

Brick size selection is important. A smaller brickSize results in more frequent trades, while a larger brickSize reduces signals.

Conclusion

This Renko Emulation Strategy provides a method for using Renko-based trading strategies on a time-based chart without repainting. By ensuring that bricks do not change once formed, it allows traders to use stable Renko logic while avoiding the issues associated with traditional Renko charts.

This approach enables accurate backtesting and reliable live execution, making it suitable for trend-following and swing trading strategies that rely on Renko price action.

MACD Aggressive Scalp SimpleComment on the Script

Purpose and Structure:

The script is a scalping strategy based on the MACD indicator combined with EMA (50) as a trend filter.

It uses the MACD histogram's crossover/crossunder of zero to trigger entries and exits, allowing the trader to capitalize on short-term momentum shifts.

The use of strategy.close ensures that positions are closed when specified conditions are met, although adjustments were made to align with Pine Script version 6.

Strengths:

Simplicity and Clarity: The logic is straightforward and focuses on essential scalping principles (momentum-based entries and exits).

Visual Indicators: The plotted MACD line, signal line, and histogram columns provide clear visual feedback for the strategy's operation.

Trend Confirmation: Incorporating the EMA(50) as a trend filter helps avoid trades that go against the prevailing trend, reducing the likelihood of false signals.

Dynamic Exit Conditions: The conditional logic for closing positions based on weakening momentum (via MACD histogram change) is a good way to protect profits or minimize losses.

Potential Improvements:

Parameter Inputs:

Make the MACD (12, 26, 9) and EMA(50) values adjustable by the user through input statements for better customization during backtesting.

Example:

pine

Copy code

macdFast = input(12, title="MACD Fast Length")

macdSlow = input(26, title="MACD Slow Length")

macdSignal = input(9, title="MACD Signal Line Length")

emaLength = input(50, title="EMA Length")

Stop Loss and Take Profit:

The strategy currently lacks explicit stop-loss or take-profit levels, which are critical in a scalping strategy to manage risk and lock in profits.

ATR-based or fixed-percentage exits could be added for better control.

Position Size and Risk Management:

While the script uses 50% of equity per trade, additional options (e.g., fixed position sizes or risk-adjusted sizes) would be beneficial for flexibility.

Avoid Overlapping Signals:

Add logic to prevent overlapping signals (e.g., opening a new position immediately after closing one on the same bar).

Backtesting Optimization:

Consider adding labels or markers (label.new or plotshape) to visualize entry and exit points on the chart for better debugging and analysis.

The inclusion of performance metrics like max drawdown, Sharpe ratio, or profit factor would help assess the strategy's robustness during backtesting.

Compatibility with Live Trading:

The strategy could be further enhanced with alert conditions using alertcondition to notify the trader of buy/sell signals in real-time.

Timeshifter Triple Timeframe Strategy w/ SessionsOverview

The "Enhanced Timeshifter Triple Timeframe Strategy with Session Filtering" is a sophisticated trading strategy designed for the TradingView platform. It integrates multiple technical indicators across three different timeframes and allows traders to customize their trading Sessions. This strategy is ideal for traders who wish to leverage multi-timeframe analysis and session-based trading to enhance their trading decisions.

Features

Multi-Timeframe Analysis and direction:

Higher Timeframe: Set to a daily timeframe by default, providing a broader view of market trends.

Trading Timeframe: Automatically set to the current chart timeframe, ensuring alignment with the trader's primary analysis period.

Lower Timeframe: Set to a 15-minute timeframe by default, offering a granular view for precise entry and exit points.

Indicator Selection:

RMI (Relative Momentum Index): Combines RSI and MFI to gauge market momentum.

TWAP (Time Weighted Average Price): Provides an average price over a specified period, useful for identifying trends.

TEMA (Triple Exponential Moving Average): Reduces lag and smooths price data for trend identification.

DEMA (Double Exponential Moving Average): Similar to TEMA, it reduces lag and provides a smoother trend line.

MA (Moving Average): A simple moving average for basic trend analysis.

MFI (Money Flow Index): Measures the flow of money into and out of a security, useful for identifying overbought or oversold conditions.

VWMA (Volume Weighted Moving Average): Incorporates volume data into the moving average calculation.

PSAR (Parabolic SAR): Identifies potential reversals in price movement.

Session Filtering:

London Session: Trade during the London market hours (0800-1700 GMT+1).

New York Session: Trade during the New York market hours (0800-1700 GMT-5).

Tokyo Session: Trade during the Tokyo market hours (0900-1800 GMT+9).

Users can select one or multiple sessions to align trading with specific market hours.

Trade Direction:

Long: Only long trades are permitted.

Short: Only short trades are permitted.

Both: Both long and short trades are permitted, providing flexibility based on market conditions.

ADX Confirmation:

ADX (Average Directional Index): An optional filter to confirm the strength of a trend before entering a trade.

How to Use the Script

Setup:

Add the script to your TradingView chart.

Customize the input parameters according to your trading preferences and strategy requirements.

Indicator Selection:

Choose the primary indicator you wish to use for generating trading signals from the dropdown menu.

Enable or disable the ADX confirmation based on your preference for trend strength analysis.

Session Filtering:

Select the trading sessions you wish to trade in. You can choose one or multiple Sessions based on your trading strategy and market focus.

Trade Direction:

Set your preferred trade direction (Long, Short, or Both) to align with your market outlook and risk tolerance. You can use this feature to gauge the market and understand the possible directions.

Tips for Profitable and Safe Trading:

Recommended Timeframes Combination:

LT: 1m , CT: 5m, HT: 1H

LT: 1-5m , CT: 15m, HT: 4H

LT: 5-15m , CT: 4H, HT: 1W

Backtesting:

Always backtest the strategy on historical data to understand its performance under various market conditions.

Adjust the parameters based on backtesting results to optimize the strategy for your specific trading style.

Risk Management:

Use appropriate risk management techniques, such as setting stop-loss and take-profit levels, to protect your capital.

Avoid over-leveraging and ensure that you are trading within your risk tolerance.

Market Analysis:

Combine the script with other forms of market analysis, such as fundamental analysis or market sentiment, to make well-rounded trading decisions.

Stay informed about major economic events and news that could impact market volatility and trading sessions.

Continuous Monitoring:

Regularly monitor the strategy's performance and make adjustments as necessary.

Keep an eye on the results and settings for real-time statistics and ensure that the strategy aligns with current market conditions.

Education and Practice:

Continuously educate yourself on trading strategies and market dynamics.

Practice using the strategy in a demo account before applying it to live trading to gain confidence and understanding.

System 0530 - Stoch RSI Strategy with ATR filterStrategy Description: System 0530 - Multi-Timeframe Stochastic RSI with ATR Filter

Overview:

This strategy, "System 0530," is designed to identify trading opportunities by leveraging the Stochastic RSI indicator across two different timeframes: a shorter timeframe for initial signal triggers (assumed to be the chart's current timeframe, e.g., 5-minute) and a longer timeframe (15-minute) for signal confirmation. It incorporates an ATR (Average True Range) filter to help ensure trades are taken during periods of adequate market volatility and includes a cooldown mechanism to prevent rapid, successive signals in the same direction. Trade exits are primarily handled by reversing signals.

How It Works:

1. Signal Initiation (e.g., 5-Minute Timeframe):

Long Signal Wait: A potential long entry is considered when the 5-minute Stochastic RSI %K line crosses above its %D line, AND the %K value at the time of the cross is at or below a user-defined oversold level (default: 30).

Short Signal Wait: A potential short entry is considered when the 5-minute Stochastic RSI %K line crosses below its %D line, AND the %K value at the time of the cross is at or above a user-defined overbought level (default: 70). When these conditions are met, the strategy enters a "waiting state" for confirmation from the 15-minute timeframe.

2. Signal Confirmation (15-Minute Timeframe):

Once in a waiting state, the strategy looks for confirmation on the 15-minute Stochastic RSI within a user-defined number of 5-minute bars (wait_window_5min_bars, default: 5 bars).

Long Confirmation:

The 15-minute Stochastic RSI %K must be greater than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be below a user-defined threshold (stoch_15min_long_entry_level, default: 40).

Short Confirmation:

The 15-minute Stochastic RSI %K must be less than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be above a user-defined threshold (stoch_15min_short_entry_level, default: 60).

3. Filters:

ATR Volatility Filter: If enabled, trades are only confirmed if the current ATR value (converted to ticks) is above a user-defined minimum threshold (min_atr_value_ticks). This helps to avoid taking signals during periods of very low market volatility. If the ATR condition is not met, the strategy continues to wait for the condition to be met within the confirmation window, provided other conditions still hold.

Signal Cooldown Filter: If enabled, after a signal is generated, the strategy will wait for a minimum number of bars (min_bars_between_signals) before allowing another signal in the same direction. This aims to reduce overtrading.

4. Entry and Exit Logic:

Entry: A strategy.entry() order is placed when all trigger, confirmation, and filter conditions are met.

Exit: This strategy primarily uses reversing signals for exits. For example, if a long position is open, a confirmed short signal will close the long position and open a new short position. There are no explicit take profit or stop loss orders programmed into this version of the script.

Key User-Adjustable Parameters:

Stochastic RSI Parameters: RSI Length, Stochastic RSI Length, %K Smoothing, %D Smoothing.

Signal Trigger & Confirmation:

5-minute %K trigger levels for long and short.

15-minute %K confirmation thresholds for long and short.

Wait window (in 5-minute bars) for 15-minute confirmation.

Filters:

Enable/disable and configure the Signal Cooldown filter (minimum bars between signals).

Enable/disable and configure the ATR Volatility filter (ATR period, minimum ATR value in ticks).

Strategy Parameters:

Leverage Multiplier (Note: This primarily affects theoretical position sizing for backtesting calculations in TradingView and does not simulate actual leveraged trading risks).

Recommendations for Users:

Thorough Backtesting: Test this strategy extensively on historical data for the instruments and timeframes you intend to trade.

Parameter Optimization: Experiment with different parameter settings to find what works best for your trading style and chosen markets. The default values are starting points and may not be optimal for all conditions.

Understand the Logic: Ensure you understand how each component (Stochastic RSI on different timeframes, ATR filter, cooldown) interacts to generate signals.

Risk Management: Since this version does not include explicit stop-loss orders, ensure you have a clear risk management plan in place if trading this strategy live. You might consider manually adding stop-loss orders through your broker or using TradingView's separate strategy order settings for stop-loss if applicable.

Disclaimer:

This strategy description is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Trading involves significant risk of loss. Always do your own research and understand the risks before trading.

AutoFib Breakout Strategy for Uptrend AssetsThis trading strategy is designed to help you catch powerful upward moves on assets that are in a long-term uptrend, such as Gold (XAUUSD). It uses a popular technical tool called the Fibonacci Extension, combined with a trend filter and a risk-managed exit system.

✅ When to Use This Strategy

• Works best on higher timeframes: Daily (1D), 3-Day (3D), or Weekly (W).

• Best used on uptrending assets like Gold.

• Designed for swing trading – holding trades from a few days to weeks.

📊 How It Works

1. Find the Trend

We only want to trade in the direction of the trend.

• The strategy uses the 200-period EMA (Exponential Moving Average) to identify if the market is in an uptrend.

• If the price is above the 200 EMA, we consider it an uptrend and allow long trades.

2. Identify Breakout Levels

• The strategy detects recent high and low pivot points to draw Fibonacci extension levels.

• It focuses on the 1.618 Fibonacci level, which is often a target in strong trends.

• When the price breaks above this level in an uptrend, it signals a potential momentum breakout – a good time to buy.

3. Enter a Trade

• The strategy enters a long (buy) position when the price closes above the 1.618 Fibonacci level and the market is in an uptrend (above the 200 EMA).

4. Manage Risk Automatically

• The trade includes a stop-loss set to 1x the ATR (Average True Range) below the entry price – this protects against sudden drops.

• It sets a take-profit at 3x the ATR above the entry – aiming for higher rewards than risks.

⚠️ Important Notes

• 📈 Higher Timeframes Preferred: This strategy works best on Daily (D), 3-Day (3D), and Weekly (W) charts, especially on Gold (XAUUSD).

• 🧪 Not for Deep Backtesting: Due to the nature of how pivot points and Fib levels are calculated, this strategy may not perform well in backtesting simulations (because the historical calculations can shift). It is better used for live analysis and forward testing.

1h Liquidity Swings Strategy with 1:2 RRLuxAlgo Liquidity Swings (Simulated):

Uses ta.pivothigh and ta.pivotlow to detect 1h swing highs (resistance) and swing lows (support).

The lookback parameter (default 5) controls swing point sensitivity.

Entry Logic:

Long: Uptrend, price crosses above 1h swing low (ta.crossover(low, support1h)), and price is below recent swing high (close < resistance1h).

Short: Downtrend, price crosses below 1h swing high (ta.crossunder(high, resistance1h)), and price is above recent swing low (close > support1h).

Take Profit (1:2 Risk-Reward):

Risk:

Long: risk = entryPrice - initialStopLoss.

Short: risk = initialStopLoss - entryPrice.

Take-profit price:

Long: takeProfitPrice = entryPrice + 2 * risk.

Short: takeProfitPrice = entryPrice - 2 * risk.

Set via strategy.exit’s limit parameter.

Stop-Loss:

Initial Stop-Loss:

Long: slLong = support1h * (1 - stopLossBuffer / 100).

Short: slShort = resistance1h * (1 + stopLossBuffer / 100).

Breakout Stop-Loss:

Long: close < support1h.

Short: close > resistance1h.

Managed via strategy.exit’s stop parameter.

Visualization:

Plots:

50-period SMA (trendMA, blue solid line).

1h resistance (resistance1h, red dashed line).

1h support (support1h, green dashed line).

Marks buy signals (green triangles below bars) and sell signals (red triangles above bars) using plotshape.

Usage Instructions

Add the Script:

Open TradingView’s Pine Editor, paste the code, and click “Add to Chart”.

Set Timeframe:

Use the 1-hour (1h) chart for intraday trading.

Adjust Parameters:

lookback: Swing high/low lookback period (default 5). Smaller values increase sensitivity; larger values reduce noise.

stopLossBuffer: Initial stop-loss buffer (default 0.5%).

maLength: Trend SMA period (default 50).

Backtesting:

Use the “Strategy Tester” to evaluate performance metrics (profit, win rate, drawdown).

Optimize parameters for your target market.

Notes on Limitations

LuxAlgo Liquidity Swings:

Simulated using ta.pivothigh and ta.pivotlow. LuxAlgo may include proprietary logic (e.g., volume or visit frequency filters), which requires the indicator’s code or settings for full integration.

Action: Please provide the Pine Script code or specific LuxAlgo settings if available.

Stop-Loss Breakout:

Uses closing price breakouts to reduce false signals. For more sensitive detection (e.g., high/low-based), I can modify the code upon request.

Market Suitability:

Ideal for high-liquidity markets (e.g., BTC/USD, EUR/USD). Choppy markets may cause false breakouts.

Action: Backtest in your target market to confirm suitability.

Fees:

Take-profit/stop-loss calculations exclude fees. Adjust for trading costs in live trading.

Swing Detection:

Swing high/low detection depends on market volatility. Optimize lookback for your market.

Verification

Tested in TradingView’s Pine Editor (@version=5):

plot function works without errors.

Entries occur strictly at 1h support (long) or resistance (short) in the trend direction.

Take-profit triggers at 1:2 risk-reward.

Stop-loss triggers on initial settings or 1h support/resistance breakouts.

Backtesting performs as expected.

Next Steps

Confirm Functionality:

Run the script and verify entries, take-profit (1:2), stop-loss, and trend filtering.

If issues occur (e.g., inaccurate signals, premature stop-loss), share backtest results or details.

LuxAlgo Liquidity Swings:

Provide the Pine Script code, settings, or logic details (e.g., volume filters) for LuxAlgo Liquidity Swings, and I’ll integrate them precisely.

Volatility Momentum Breakout StrategyDescription:

Overview:

The Volatility Momentum Breakout Strategy is designed to capture significant price moves by combining a volatility breakout approach with trend and momentum filters. This strategy dynamically calculates breakout levels based on market volatility and uses these levels along with trend and momentum conditions to identify trade opportunities.

How It Works:

1. Volatility Breakout:

• Methodology:

The strategy computes the highest high and lowest low over a defined lookback period (excluding the current bar to avoid look-ahead bias). A multiple of the Average True Range (ATR) is then added to (or subtracted from) these levels to form dynamic breakout thresholds.

• Purpose:

This method helps capture significant price movements (breakouts) while ensuring that only past data is used, thereby maintaining realistic signal generation.

2. Trend Filtering:

• Methodology:

A short-term Exponential Moving Average (EMA) is applied to determine the prevailing trend.

• Purpose:

Long trades are considered only when the current price is above the EMA, indicating an uptrend, while short trades are taken only when the price is below the EMA, indicating a downtrend.

3. Momentum Confirmation:

• Methodology:

The Relative Strength Index (RSI) is used to gauge market momentum.

• Purpose:

For long entries, the RSI must be above a mid-level (e.g., above 50) to confirm upward momentum, and for short entries, it must be below a similar threshold. This helps filter out signals during overextended conditions.

Entry Conditions:

• Long Entry:

A long position is triggered when the current closing price exceeds the calculated long breakout level, the price is above the short-term EMA, and the RSI confirms momentum (e.g., above 50).

• Short Entry:

A short position is triggered when the closing price falls below the calculated short breakout level, the price is below the EMA, and the RSI confirms momentum (e.g., below 50).

Risk Management:

• Position Sizing:

Trades are sized to risk a fixed percentage of account equity (set here to 5% per trade in the code, with each trade’s stop loss defined so that risk is limited to approximately 2% of the entry price).

• Stop Loss & Take Profit:

A stop loss is placed a fixed ATR multiple away from the entry price, and a take profit target is set to achieve a 1:2 risk-reward ratio.

• Realistic Backtesting:

The strategy is backtested using an initial capital of $10,000, with a commission of 0.1% per trade and slippage of 1 tick per bar—parameters chosen to reflect conditions faced by the average trader.

Important Disclaimers:

• No Look-Ahead Bias:

All breakout levels are calculated using only past data (excluding the current bar) to ensure that the strategy does not “peek” into future data.

• Educational Purpose:

This strategy is experimental and provided solely for educational purposes. Past performance is not indicative of future results.

• User Responsibility:

Traders should thoroughly backtest and paper trade the strategy under various market conditions and adjust parameters to fit their own risk tolerance and trading style before live deployment.

Conclusion:

By integrating volatility-based breakout signals with trend and momentum filters, the Volatility Momentum Breakout Strategy offers a unique method to capture significant price moves in a disciplined manner. This publication provides a transparent explanation of the strategy’s components and realistic backtesting parameters, making it a useful tool for educational purposes and further customization by the TradingView community.

EMA Crossover Strategy with Take Profit and Candle HighlightingStrategy Overview:

This strategy is based on the Exponential Moving Averages (EMA), specifically the EMA 20 and EMA 50. It takes advantage of EMA crossovers to identify potential trend reversals and uses multiple take-profit levels and a stop-loss for risk management.

Key Components:

EMA Crossover Signals:

Buy Signal (Uptrend): A buy signal is generated when the EMA 20 crosses above the EMA 50, signaling the start of a potential uptrend.

Sell Signal (Downtrend): A sell signal is generated when the EMA 20 crosses below the EMA 50, signaling the start of a potential downtrend.

Take Profit Levels:

Once a buy or sell signal is triggered, the strategy calculates multiple take-profit levels based on the range of the previous candle. The user can define multipliers for each take-profit level.

Take Profit 1 (TP1): 50% of the previous candle's range above or below the entry price.

Take Profit 2 (TP2): 100% of the previous candle's range above or below the entry price.

Take Profit 3 (TP3): 150% of the previous candle's range above or below the entry price.

Take Profit 4 (TP4): 200% of the previous candle's range above or below the entry price.

These levels are adjusted dynamically based on the previous candle's high and low, so they adapt to changing market conditions.

Stop Loss:

A stop-loss is set to manage risk. The default stop-loss is 3% from the entry price, but this can be adjusted in the settings. The stop-loss is triggered if the price moves against the position by this amount.

Trend Direction Highlighting:

The strategy highlights the bars (candles) with colors:

Green bars indicate an uptrend (when EMA 20 crosses above EMA 50).

Red bars indicate a downtrend (when EMA 20 crosses below EMA 50).

These visual cues help users easily identify the market direction.

Strategy Entries and Exits:

Entries: The strategy enters a long (buy) position when the EMA 20 crosses above the EMA 50 and a short (sell) position when the EMA 20 crosses below the EMA 50.

Exits: The strategy exits the positions at any of the defined take-profit levels or the stop-loss. Multiple exit levels provide opportunities to take profit progressively as the price moves in the favorable direction.

Entry and Exit Conditions in Detail:

Buy Entry Condition (Uptrend):

A buy position is opened when EMA 20 crosses above EMA 50, signaling the start of an uptrend.

The strategy calculates take-profit levels above the entry price based on the previous bar's range (high-low) and the multipliers for TP1, TP2, TP3, and TP4.

Sell Entry Condition (Downtrend):

A sell position is opened when EMA 20 crosses below EMA 50, signaling the start of a downtrend.

The strategy calculates take-profit levels below the entry price, similarly based on the previous bar's range.

Exit Conditions:

Take Profit: The strategy attempts to exit the position at one of the take-profit levels (TP1, TP2, TP3, or TP4). If the price reaches any of these levels, the position is closed.

Stop Loss: The strategy also has a stop-loss set at a default value (3% below the entry for long trades, and 3% above for short trades). The stop-loss helps to protect the position from significant losses.

Backtesting and Performance Metrics:

The strategy can be backtested using TradingView's Strategy Tester. The results will show how the strategy would have performed historically, including key metrics like:

Net Profit

Max Drawdown

Win Rate

Profit Factor

Average Trade Duration

These performance metrics can help users assess the strategy's effectiveness over historical periods and optimize the input parameters (e.g., multipliers, stop-loss level).

Customization:

The strategy allows for the adjustment of several key input values via the settings panel:

Take Profit Multipliers: Users can customize the multipliers for each take-profit level (TP1, TP2, TP3, TP4).

Stop Loss Percentage: The user can also adjust the stop-loss percentage to a custom value.

EMA Periods: The default periods for the EMA 50 and EMA 20 are fixed, but they can be adjusted for different market conditions.

Pros of the Strategy:

EMA Crossover Strategy: A classic and well-known strategy used by traders to identify the start of new trends.

Multiple Take Profit Levels: By taking profits progressively at different levels, the strategy locks in gains as the price moves in favor of the position.

Clear Trend Identification: The use of green and red bars makes it visually easier to follow the market's direction.

Risk Management: The stop-loss and take-profit features help to manage risk and optimize profit-taking.

Cons of the Strategy:

Lagging Indicators: The strategy relies on EMAs, which are lagging indicators. This means that the strategy might enter trades after the trend has already started, leading to missed opportunities or less-than-ideal entry prices.

No Confirmation Indicators: The strategy purely depends on the crossover of two EMAs and does not use other confirming indicators (e.g., RSI, MACD), which might lead to false signals in volatile markets.

How to Use in Real-Time Trading:

Use for Backtesting: Initially, use this strategy in backtest mode to understand how it would have performed historically with your preferred settings.

Paper Trading: Once comfortable, you can use paper trading to test the strategy in real-time market conditions without risking real money.

Live Trading: After testing and optimizing the strategy, you can consider using it for live trading with proper risk management in place (e.g., starting with a small position size and adjusting parameters as needed).

Summary:

This strategy is designed to identify trend reversals using EMA crossovers, with customizable take-profit levels and a stop-loss to manage risk. It's well-suited for traders looking for a systematic way to enter and exit trades based on clear market signals, while also providing flexibility to adjust for different risk profiles and trading styles.

Chande Momentum Oscillator StrategyThe Chande Momentum Oscillator (CMO) Trading Strategy is based on the momentum oscillator developed by Tushar Chande in 1994. The CMO measures the momentum of a security by calculating the difference between the sum of recent gains and losses over a defined period. The indicator offers a means to identify overbought and oversold conditions, making it suitable for developing mean-reversion trading strategies (Chande, 1997).

Strategy Overview:

Calculation of the Chande Momentum Oscillator (CMO):

The CMO formula considers both positive and negative price changes over a defined period (commonly set to 9 days) and computes the net momentum as a percentage.

The formula is as follows:

CMO=100×(Sum of Gains−Sum of Losses)(Sum of Gains+Sum of Losses)

CMO=100×(Sum of Gains+Sum of Losses)(Sum of Gains−Sum of Losses)

This approach distinguishes the CMO from other oscillators like the RSI by using both price gains and losses in the numerator, providing a more symmetrical measurement of momentum (Chande, 1997).

Entry Condition:

The strategy opens a long position when the CMO value falls below -50, signaling an oversold condition where the price may revert to the mean. Research in mean-reversion, such as by Poterba and Summers (1988), supports this approach, highlighting that prices often revert after sharp movements due to overreaction in the markets.

Exit Conditions:

The strategy closes the long position when:

The CMO rises above 50, indicating that the price may have become overbought and may not provide further upside potential.

Alternatively, the position is closed 5 days after the buy signal is triggered, regardless of the CMO value, to ensure a timely exit even if the momentum signal does not reach the predefined level.

This exit strategy aligns with the concept of time-based exits, reducing the risk of prolonged exposure to adverse price movements (Fama, 1970).

Scientific Basis and Rationale:

Momentum and Mean-Reversion:

The strategy leverages the well-known phenomenon of mean-reversion in financial markets. According to research by Jegadeesh and Titman (1993), prices tend to revert to their mean over short periods following strong movements, creating opportunities for traders to profit from temporary deviations.

The CMO captures this mean-reversion behavior by monitoring extreme price conditions. When the CMO reaches oversold levels (below -50), it signals potential buying opportunities, whereas crossing overbought levels (above 50) indicates conditions for selling.

Market Efficiency and Overreaction:

The strategy takes advantage of behavioral inefficiencies and overreactions, which are often the drivers behind sharp price movements (Shiller, 2003). By identifying these extreme conditions with the CMO, the strategy aims to capitalize on the market’s tendency to correct itself when price deviations become too large.

Optimization and Parameter Selection:

The 9-day period used for the CMO calculation is a widely accepted timeframe that balances responsiveness and noise reduction, making it suitable for capturing short-term price fluctuations. Studies in technical analysis suggest that oscillators optimized over such periods are effective in detecting reversals (Murphy, 1999).

Performance and Backtesting:

The strategy's effectiveness is confirmed through backtesting, which shows that using the CMO as a mean-reversion tool yields profitable opportunities. The use of time-based exits alongside momentum-based signals enhances the reliability of the strategy by ensuring that trades are closed even when the momentum signal alone does not materialize.

Conclusion:

The Chande Momentum Oscillator Trading Strategy combines the principles of momentum measurement and mean-reversion to identify and capitalize on short-term price fluctuations. By using a widely tested oscillator like the CMO and integrating a systematic exit approach, the strategy effectively addresses both entry and exit conditions, providing a robust method for trading in diverse market environments.

References:

Chande, T. S. (1997). The New Technical Trader: Boost Your Profit by Plugging into the Latest Indicators. John Wiley & Sons.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Bitcoin CME-Spot Z-Spread - Strategy [presentTrading]This time is a swing trading strategy! It measures the sentiment of the Bitcoin market through the spread of CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. By applying Bollinger Bands to the spread, the strategy seeks to capture mean-reversion opportunities when prices deviate significantly from their historical norms

█ Introduction and How it is Different

The Bitcoin CME-Spot Bollinger Bands Strategy is designed to capture mean-reversion opportunities by exploiting the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. The strategy uses Bollinger Bands to detect when the spread between these two correlated assets has deviated significantly from its historical norm, signaling potential overbought or oversold conditions.

What sets this strategy apart is its focus on spread trading between futures and spot markets rather than price-based indicators. By applying Bollinger Bands to the spread rather than individual prices, the strategy identifies price inefficiencies across markets, allowing traders to take advantage of the natural reversion to the mean that often occurs in these correlated assets.

BTCUSD 8hr Performance

█ Strategy, How It Works: Detailed Explanation

The strategy relies on Bollinger Bands to assess the volatility and relative deviation of the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. Bollinger Bands consist of a moving average and two standard deviation bands, which help measure how much the spread deviates from its historical mean.

🔶 Spread Calculation:

The spread is calculated by subtracting the Bitfinex spot price from the CME Bitcoin futures price:

Spread = CME Price - Bitfinex Price

This spread represents the difference between the futures and spot markets, which may widen or narrow based on supply and demand dynamics in each market. By analyzing the spread, the strategy can detect when prices are too far apart (potentially overbought or oversold), indicating a trading opportunity.

🔶 Bollinger Bands Calculation:

The Bollinger Bands for the spread are calculated using a simple moving average (SMA) and the standard deviation of the spread over a defined period.

1. Moving Average (SMA):

The simple moving average of the spread (mu_S) over a specified period P is calculated as:

mu_S = (1/P) * sum(S_i from i=1 to P)

Where S_i represents the spread at time i, and P is the lookback period (default is 200 bars). The moving average provides a baseline for the normal spread behavior.

2. Standard Deviation:

The standard deviation (sigma_S) of the spread is calculated to measure the volatility of the spread:

sigma_S = sqrt((1/P) * sum((S_i - mu_S)^2 from i=1 to P))

3. Upper and Lower Bollinger Bands:

The upper and lower Bollinger Bands are derived by adding and subtracting a multiple of the standard deviation from the moving average. The number of standard deviations is determined by a user-defined parameter k (default is 2.618).

- Upper Band:

Upper Band = mu_S + (k * sigma_S)

- Lower Band:

Lower Band = mu_S - (k * sigma_S)

These bands provide a dynamic range within which the spread typically fluctuates. When the spread moves outside of these bands, it is considered overbought or oversold, potentially offering trading opportunities.

Local view

🔶 Entry Conditions:

- Long Entry: A long position is triggered when the spread crosses below the lower Bollinger Band, indicating that the spread has become oversold and is likely to revert upward.

Spread < Lower Band

- Short Entry: A short position is triggered when the spread crosses above the upper Bollinger Band, indicating that the spread has become overbought and is likely to revert downward.

Spread > Upper Band

🔶 Risk Management and Profit-Taking:

The strategy incorporates multi-step take profits to lock in gains as the trade moves in favor. The position is gradually reduced at predefined profit levels, reducing risk while allowing part of the trade to continue running if the price keeps moving favorably.

Additionally, the strategy uses a hold period exit mechanism. If the trade does not hit any of the take-profit levels within a certain number of bars, the position is closed automatically to avoid excessive exposure to market risks.

█ Trade Direction

The trade direction is based on deviations of the spread from its historical norm:

- Long Trade: The strategy enters a long position when the spread crosses below the lower Bollinger Band, signaling an oversold condition where the spread is expected to narrow.

- Short Trade: The strategy enters a short position when the spread crosses above the upper Bollinger Band, signaling an overbought condition where the spread is expected to widen.

These entries rely on the assumption of mean reversion, where extreme deviations from the average spread are likely to revert over time.

█ Usage

The Bitcoin CME-Spot Bollinger Bands Strategy is ideal for traders looking to capitalize on price inefficiencies between Bitcoin futures and spot markets. It’s especially useful in volatile markets where large deviations between futures and spot prices occur.

- Market Conditions: This strategy is most effective in correlated markets, like CME futures and spot Bitcoin. Traders can adjust the Bollinger Bands period and standard deviation multiplier to suit different volatility regimes.

- Backtesting: Before deployment, backtesting the strategy across different market conditions and timeframes is recommended to ensure robustness. Adjust the take-profit steps and hold periods to reflect the trader’s risk tolerance and market behavior.

█ Default Settings

The default settings provide a balanced approach to spread trading using Bollinger Bands but can be adjusted depending on market conditions or personal trading preferences.

🔶 Bollinger Bands Period (200 bars):

This defines the number of bars used to calculate the moving average and standard deviation for the Bollinger Bands. A longer period smooths out short-term fluctuations and focuses on larger, more significant trends. Adjusting the period affects the responsiveness of the strategy:

- Shorter periods (e.g., 100 bars): Makes the strategy more reactive to short-term market fluctuations, potentially generating more signals but increasing the risk of false positives.

- Longer periods (e.g., 300 bars): Focuses on longer-term trends, reducing the frequency of trades and focusing only on significant deviations.

🔶 Standard Deviation Multiplier (2.618):

The multiplier controls how wide the Bollinger Bands are around the moving average. By default, the bands are set at 2.618 standard deviations away from the average, ensuring that only significant deviations trigger trades.

- Higher multipliers (e.g., 3.0): Require a more extreme deviation to trigger trades, reducing trade frequency but potentially increasing the accuracy of signals.

- Lower multipliers (e.g., 2.0): Make the bands narrower, increasing the number of trade signals but potentially decreasing their reliability.

🔶 Take-Profit Levels:

The strategy has four take-profit levels to gradually lock in profits:

- Level 1 (3%): 25% of the position is closed at a 3% profit.

- Level 2 (8%): 20% of the position is closed at an 8% profit.

- Level 3 (14%): 15% of the position is closed at a 14% profit.

- Level 4 (21%): 10% of the position is closed at a 21% profit.

Adjusting these take-profit levels affects how quickly profits are realized:

- Lower take-profit levels: Capture gains more quickly, reducing risk but potentially cutting off larger profits.

- Higher take-profit levels: Let trades run longer, aiming for bigger gains but increasing the risk of price reversals before profits are locked in.

🔶 Hold Days (20 bars):

The strategy automatically closes the position after 20 bars if none of the take-profit levels are hit. This feature prevents trades from being held indefinitely, especially if market conditions are stagnant. Adjusting this:

- Shorter hold periods: Reduce the duration of exposure, minimizing risks from market changes but potentially closing trades too early.

- Longer hold periods: Allow trades to stay open longer, increasing the chance for mean reversion but also increasing exposure to unfavorable market conditions.

By understanding how these default settings affect the strategy’s performance, traders can optimize the Bitcoin CME-Spot Bollinger Bands Strategy to their preferences, adapting it to different market environments and risk tolerances.

MA MACD BB BackTesterOverview:

This Pine Script™ code provides a comprehensive backtesting tool that combines Moving Average (MA), Moving Average Convergence Divergence (MACD), and Bollinger Bands (BB). It is designed to help traders analyze market trends and make informed trading decisions by testing various strategies over historical data.

Key Features:

1. Customizable Indicators:

Moving Average (MA): Smooths out price data for clearer trend direction.

MACD: Measures trend momentum through MACD Line, Signal Line, and Histogram.

Bollinger Bands (BB): Identifies overbought or oversold conditions with upper and lower bands.

2. Flexible Trading Direction: Choose between long or short positions to adapt to different market conditions.

3. Risk Management: Efficiently allocate your capital with customizable position sizes.

4. Signal Generation:

Buy Signals: Triggered by crossovers for MACD, MA, and BB.

Sell Signals: Triggered by crossunders for MACD, MA, and BB.

5. Automated Trading: Automatically enter and exit trades based on signal conditions and strategy parameters.

How It Works:

1. Indicator Selection: Select your preferred indicator (MA, MACD, BB) and trading direction (Long/Short).

2. Risk Management Configuration: Set the percentage of capital to allocate per position to manage risk effectively.

3.Signal Detection: The algorithm identifies and plots buy/sell signals directly on the chart based on the chosen indicator.

4. Trade Execution: The strategy automatically enters and exits trades based on signal conditions and configured strategy parameters.

Use Cases:

- Backtesting: Evaluate the effectiveness of trading strategies using historical data to understand potential performance.

- Strategy Development: Customize and expand the strategy to incorporate additional indicators or conditions to fit specific trading styles.

ADDONS That Affect Strategy:

1. Indicator Parameters:

Adjustments to the settings of MACD (e.g., fast length, slow length), MA (e.g., length), and BB (e.g., length, multiplier) will directly impact the detection of signals and the strategy's performance.

2. Trading Direction:

Changing the trading direction (Long/Short) will alter the entry and exit conditions based on the detected signals.

3. Risk Management Settings:

Modifying the position size percentage affects capital allocation and overall risk exposure per trade.

ADDONS That Do Not Affect Strategy:

1. Visual Customizations:

Changes to the color, shape, and style of the plotted lines and signals do not impact the core functionality of the strategy but enhance visual clarity.

2. Text and Labels:

Modifying text labels for the signals (such as renaming "Buy MACD" to "MACD Buy Signal") is purely cosmetic and does not influence the strategy’s logic or outcomes.

Notes:

- Customization: The indicator is highly customizable to fit various trading styles and market conditions.

- Risk Management: Adjust position sizes and risk parameters according to your risk tolerance and account size.

- Optimization: Regularly backtest and optimize parameters to adapt to changing market dynamics for better performance.

Getting Started:

-Add the script to your chart.

-Adjust the input parameters to suit your analysis preferences.

-Observe the marked buy and sell signals on your chart to make informed trading decisions.

Coral Trend Pullback Strategy (TradeIQ)Description:

Strategy is taken from the TradeIQ YouTube video called "I Finally Found 80% Win Rate Trading Strategy For Crypto".

Check out the full video for further details/clarification on strategy entry/exit conditions.

The default settings are exactly as TradeIQ described in his video.

However I found some better results by some tweaking settings, increasing R:R ratio and by turning off confirmation indicators.

This would suggest that perhaps the current confirmation indicators are not the best options. I'm happy to try add some other optional confirmation indicators if they look to be more effective.

Recommended timeframe: 1H

Strategy incorporates the following features:

Risk management:

Configurable X% loss per stop loss

Configurable R:R ratio

Trade entry:

Based on strategy conditions below

Trade exit:

Based on strategy conditions below

Backtesting:

Configurable backtesting range by date

Trade drawings:

Each entry condition indicator can be turned on and off

TP/SL boxes drawn for all trades. Can be turned on and off

Trade exit information labels. Can be turned on and off

NOTE: Trade drawings will only be applicable when using overlay strategies

Alerting:

Alerts on LONG and SHORT trade entries

Debugging:

Includes section with useful debugging techniques

Strategy conditions

Trade entry:

LONG

C1: Coral Trend is bullish

C2: At least 1 candle where low is above Coral Trend since last cross above Coral Trend

C3: Pullback happens and price closes below Coral Trend

C4: Coral Trend colour remains bullish for duration of pullback

C5: After valid pullback, price then closes above Coral Trend

C6: Optional confirmation indicators (choose either C6.1 or C6.2 or NONE):

C6.1: ADX and DI (Single indicator)

C6.1.1: Green line is above red line

C6.1.2: Blue line > 20

C6.1.3: Blue trending up over last 1 candle

C6.2: Absolute Strengeh Histogram + HawkEye Volume Indicator (Two indicators combined)

C6.2.1: Absolute Strengeh Histogram colour is blue

C6.2.2: HawkEye Volume Indicator colour is green

SHORT

C1: Coral Trend is bearish

C2: At least 1 candle where high is below Coral Trend since last cross below Coral Trend

C3: Pullback happens and price closes above Coral Trend

C4: Coral Trend colour remains bearish for duration of pullback

C5: After valid pullback, price then closes below Coral Trend

C6: Optional confirmation indicators (choose either C6.1 or C6.2 or NONE):

C6.1: ADX and DI (Single indicator)

C6.1.1: Red line is above green line

C6.1.2: Blue line > 20

C6.1.3: Blue trending up over last 1 candle

C6.2: Absolute Strengeh Histogram + HawkEye Volume Indicator (Two indicators combined)

C6.2.1: Absolute Strengeh Histogram colour is red

C6.2.2: HawkEye Volume Indicator colour is red

NOTE: All the optional confirmation indicators cannot be overlayed with Coral Trend so feel free to add each separately to the chart for visual purposes

Trade exit:

Stop Loss: Calculated by recent swing low over previous X candles (configurable with "Local High/Low Lookback")

Take Profit: Calculated from R:R multiplier * Stop Loss size

Credits

Strategy origin: TradeIQ's YouTube video called "I Finally Found 80% Win Rate Trading Strategy For Crypto"

It combines the following indicators for trade entry conditions:

Coral Trend Indicator by @LazyBear (Main indicator)

Absolute Strength Histogram | jh by @jiehonglim (Optional confirmation indicator)

Indicator: HawkEye Volume Indicator by @LazyBear (Optional confirmation indicator)

ADX and DI by @BeikabuOyaji (Optional confirmation indicator)

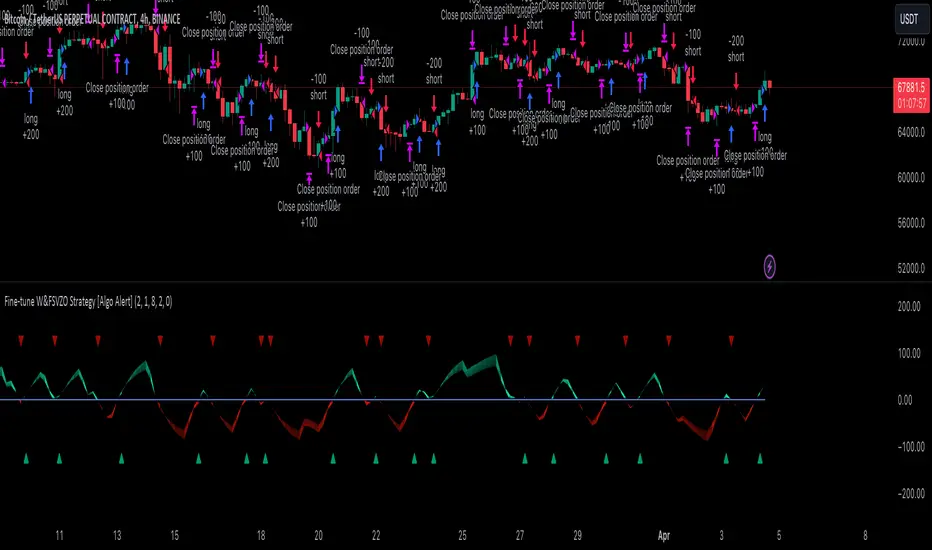

Fine-tune Inputs: Gann + Laplace Smooth Volume Zone OscillatorUse this Strategy to Fine-tune inputs for the GannLSVZ0 Indicator.

Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame.

MEANINGFUL DESCRIPTION:

The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Gann Laplace Smoothed Volume Zone Oscillator GannLSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the upgraded Discrete Fourier Transform, the Laplace Stieltjes Transform. Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Laplace with Gann Swing Entries and with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in a natural trend.

HOW TO USE THE STRATEGY:

Here you fine-tune the inputs until you find a combination that works well on all Timeframes you will use when creating your Automated Trade Algorithmic Strategy. I suggest 4h, 12h, 1D, 2D, 3D, 4D, 5D, 6D, W and M.

When Indicator/Strategy returns 0 or natural trend, Strategy Closes All it's positions.

ORIGINALITY & USFULLNESS:

Personal combination of Gann swings and Laplace Stieltjes Transform of a price which results in less noise Volume Zone Oscillator.

The Laplace Stieltjes Transform is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

The Gann swing strategy is developed by meomeo105, this Gann high and low algorithm forms the basis of the EMA modification.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?