Gann Single Square Swing Trading System with Gann AnglesGann Single Square Swing Trading System

This script automatically detects "squares" - geometric patterns where price movement equals time movement. When price moves the same distance as the number of bars (time), it creates powerful support/resistance levels based on Gann theory.

Key Visual Elements

• Box: The detected square pattern

• Dark Blue Line (50%): Most important trading level

• Green Lines: Profit target levels (125%, 150%)

• Red Lines: Stop loss levels (-25%, -50%)

• Colored Angle Lines: Gann angles for trend direction

• Quality Score: Blue label showing setup strength (aim for 70%+)

Simple Trading Rules

LONG Trades (Green 🟢 Square)

1. Entry: Buy when price touches the dark blue 50% line from above

2. Stop Loss: Place below the red -25% line

3. Take Profit: Exit at green 125% line (first target) or 150% line (second target)

SHORT Trades (Red 🔴 Square)

1. Entry: Sell when price touches the dark blue 50% line from below

2. Stop Loss: Place above the red -25% line

3. Take Profit: Exit at green 125% line (first target) or 150% line (second target)

Entry Checklist

✅ Square quality score > 70%

✅ Price touches 50% level (dark blue line)

✅ Volume above average (if volume filter enabled)

✅ Clear square formation visible

Alerts

The script generates automatic alerts when price reaches the 50% trading level. Enable alerts in TradingView to get notified of setups.

Bottom Line: Wait for the alert → Check quality score → Enter at 50% level → Set stop at red line → Take profit at green line.

Cerca negli script per "entry"

MA Shift (Offset Only + Flip Dots)Indicator Overview

This custom moving average indicator shifts the SMA away from price by a fixed percent or ATR multiple. It delivers a clear, uncluttered view of trend direction and momentum while keeping the price bars visible. A single offset line glows in semi-transparent shading and changes color based on trend state. When the price crosses the base SMA, a small dot marks the flip point.

Key Features

Adjustable Length

Choose any SMA period (default six) to suit your time frame and trading style.

Flexible Offset Mode

Percent mode places the line a fixed percentage above or below the SMA.

ATR mode spaces the line dynamically based on market volatility.

Direction Toggle

Shift the line up or down away from candles.

Glow Effect

A wide, semi-transparent band highlights the offset line for easy visibility.

Trend-Flip Dots

A tiny circle appears below the bar when the trend turns up and above the bar when it turns down, helping you spot reversals at a glance.

Custom Candle and Bar Coloring

Bars and candles recolor to reflect the current trend, reinforcing visual clarity.

How It Works

Base SMA Calculation

The indicator computes a standard SMA on your chosen source (high+low 2 by default).

Offset Application

It then adds or subtracts the percent or ATR-based distance to create a second line.

Trend Detection

When price moves above the SMA, the offset line and bars turn to your “up” color. When price drops below, they switch to your “down” color.

Flip Signals

On the bar that triggers a color change, a dot marks the exact reversal point.

Trading Signals and Usage

Trend Confirmation

Use the offset line as a clean trend guide. Price consistently above the line with green bars signals a bullish regime. Price below the line with orange bars signals bearish control.

Entry and Exit

Long Entry: Wait for a flip-up dot and a green close above the offset line.

Short Entry: Watch for a flip-down dot and an orange close below the offset line.

Stops and Targets: Place stops just inside the offset line on pullbacks for dynamic risk management.

Avoiding Whipsaws

The visual separation helps you ignore minor noise around price. Combine flip dots with bar color to filter false turns.

Confluence with MACD

Pair this offset SMA with the MACD for stronger signals:

MACD Trend Filter

Require the MACD line to be above its signal line (and histogram above zero) before taking a long flip-up from the offset MA.

Momentum Confirmation

When the offset SMA flips to a downtrend, look for the MACD histogram to turn negative. That alignment avoids fade-against-momentum trades.

Entry Timing

Use the MACD crossover as a lead-in filter and the offset SMA flip as the actual trigger. This two-step approach keeps you on the right side of larger moves.

Publishing Tips on TradingView

Description: Summarize features and usage in the indicator’s “About” field.

Inputs: List each setting clearly so users know how to tweak period, offset mode, percent/ATR values and color choices.

Examples: Include a chart snapshot showing a long setup with both the offset SMA flip and a confirming MACD crossover.

Release Notes: Mention version defaults (six-period SMA, ten-percent offset) and invite feedback for improvements.

Tags: Use relevant keywords like “Moving Average,” “Offset Indicator,” “Trend Filter,” and “MACD Confluence” to make it easy to find.

With its simple dot signals and customizable glow, this offset SMA becomes a powerful visual tool—especially when paired with MACD—for spotting clean trend entries and exits.

50/100 EMA Crossover with Candle Confirmation📘 **50/100 EMA Crossover with Candle Confirmation – Strategy Description**

The **50/100 EMA Crossover with Candle Confirmation** is a trend-following strategy designed to filter high-probability entries by combining exponential moving average (EMA) crossovers with strong price action confirmation. This strategy aims to reduce false signals commonly associated with EMA-only systems by requiring a **candle close confirmation in the direction of the trend**, making it more reliable for intraday or swing trading across Forex, crypto, and stock markets.

---

### 🔍 **Core Logic**

* The strategy is based on the interaction of the **50 EMA** (fast-moving average) and the **100 EMA** (slow-moving average).

* **Trend direction** is determined by the crossover:

* **Bullish Trend**: When the 50 EMA crosses **above** the 100 EMA.

* **Bearish Trend**: When the 50 EMA crosses **below** the 100 EMA.

* To **filter out false breakouts**, a **candle confirmation** is used:

* For a **Buy signal**: After a bullish crossover, wait for a strong bullish candle (e.g., full-body green candle) to **close above both EMAs**.

* For a **Sell signal**: After a bearish crossover, wait for a strong bearish candle to **close below both EMAs**.

---

### ✅ **Entry Conditions**

**Buy Entry:**

* 50 EMA crosses above 100 EMA.

* Latest candle closes **above both EMAs**.

* Candle must be bullish (green/full body preferred).

**Sell Entry:**

* 50 EMA crosses below 100 EMA.

* Latest candle closes **below both EMAs**.

* Candle must be bearish (red/full body preferred).

---

### 🛑 **Exit or Take-Profit Options**

* **Fixed TP/SL**: 1:2 or 1:3 risk-reward.

* **Trailing Stop**: Based on recent swing highs/lows or ATR.

* **EMA Exit**: Exit trade when the candle closes on the opposite side of 50 EMA.

---

### ⚙️ **Best Settings**

* **Timeframes**: 5M, 15M, 1H, 4H (works well on most).

* **Markets**: Forex, Crypto (e.g., BTC/ETH), Indices (e.g., NASDAQ, NIFTY50).

* **Recommended filters**:

* Use with RSI divergence or volume confirmation.

* Avoid using during high-impact news (especially on lower timeframes).

---

### 🧠 **Why This Works**

The 50/100 EMA crossover provides a **medium-term trend signal**, reducing noise seen in fast EMAs (like 9 or 21). The candle confirmation adds a **momentum filter**, ensuring price supports the directional bias. This makes it suitable for traders who want a balance of trend and entry precision without overcomplicating with too many indicators.

---

### 📈 **Advantages**

* Simple yet effective for identifying trends.

* Filters out fakeouts using candle confirmation.

* Easy to automate in Pine Script or other trading bots.

* Can be combined with support/resistance or SMC zones for better confluence.

---

### ⚠️ **Limitations**

* May lag slightly in ranging markets.

* Late entries possible due to confirmation candle.

* Works best with additional volume or volatility filter.

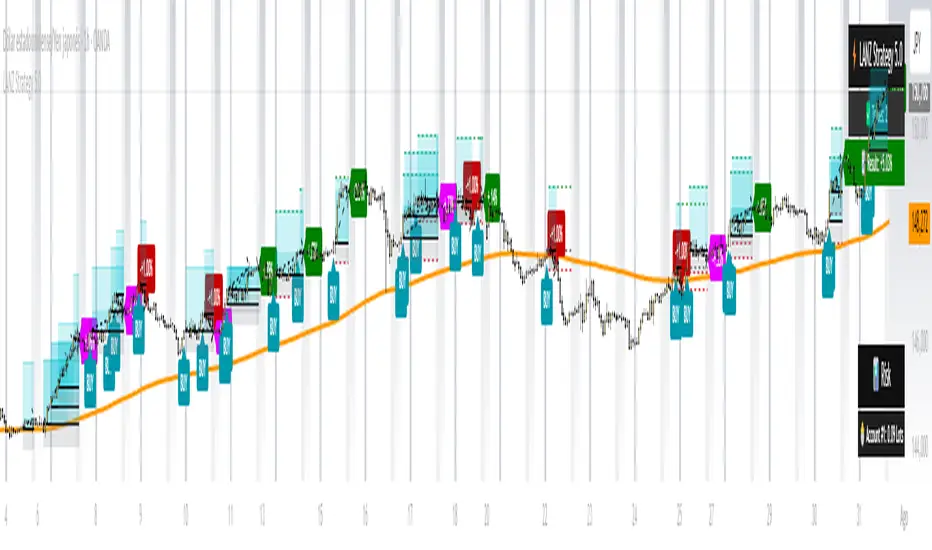

LANZ Strategy 5.0🔷 LANZ Strategy 5.0 — Intraday BUY Signals, Dynamic Lot Size per Account, Real-Time Dashboard and Smart Execution

LANZ Strategy 5.0 is a powerful intraday tool designed for traders who need a visual-first, data-backed BUY system, enhanced with risk-aware lot size calculation and a real-time performance dashboard. This indicator intelligently detects strong momentum setups and provides visual and statistical clarity throughout the session.

📌 This is an indicator, not a strategy — It does not place trades automatically but provides precise conditions, alerts, and visual guides to support execution.

🧠 Core Logic & Features

BUY Entry Conditions (Signal Engine)

A BUY signal is triggered when:

The current price is above the EMA200 (trend filter)

The last 3 candles are bullish (candle body close > open)

You are within the defined session window (NY time)

When all conditions are met and you haven’t reached the daily trade limit, a signal appears on the chart and an optional alert is triggered.

Operational Hours Filter (NY Time)

You define:

Start time (e.g., 01:15 NY)

End time (e.g., 16:00 NY)

The system only evaluates and executes signals within this period. If a BUY setup occurs outside the window, it’s ignored. The chart is also highlighted with a transparent teal background to visually show active trading hours.

Lot Size Panel with Per-Account Risk Management

Designed for traders managing multiple accounts or capital sources. You can enable up to 5 accounts, each with:

Its own capital

Its own risk percentage per trade

The system uses the defined SL in pips, plus the instrument’s pip value, to calculate the lot size per account. All values are shown in a dedicated panel at the bottom-right, automatically updating with each new trade.

The emojis (🐣🦊🦁🐲🐳) distinguish each account visually.

Trade Visualization with Customizable Lines

When a signal is triggered:

An Entry Point (EP) line is drawn at the candle’s close.

A Stop Loss (SL) line is placed X pips below the entry.

A Take Profit (TP) line is placed Y pips above the entry.

All three lines are fully customizable in style, color, and thickness. You define how many bars the lines should extend.

Outcome Tracking & Real-Time Dashboard

Each trade outcome is measured:

SL hit = –1.00%

TP hit = +3.00%

Manual close = calculated dynamically based on price at close time

Each result is labeled on the chart near its level, and stored.

The top-right dashboard updates in real time:

✅ Number of trades

📈 Cumulative % gain/loss of the day (color-coded)

Alerts You Can Trust:

You’ll get a Buy Alert when a valid signal is formed

You’ll get a Trade Executed Alert when the visual operation is plotted

You’ll get a SL/TP Hit Alert with price and result

You’ll get a Manual Close Alert if the configured time is reached and the trade is still active

⚙️ Step-by-Step Execution Flow

At every bar, the system checks:

Are we within the session time window?

Is price above EMA?

Are the last 3 candles bullish?

✅ If yes:

A BUY signal is plotted

Entry/SL/TP lines are drawn

Lot sizes are calculated and displayed

Trade is added to the daily count

🕐 At the configured Manual Close time (e.g., 16:00 NY):

If the trade is still open, it's closed

A label is added with the exact result in %

💡 Ideal For:

Intraday traders who operate within fixed time sessions

Traders managing multiple accounts or capital pools

Anyone who wants full visual clarity of every decision point

Traders who appreciate dynamic lot size calculation and clean execution tracking

👨💻 Credits:

💡 Developed by: LANZ

🧠 Strategy concept & execution model: LANZ

🧪 Tested on: 1H charts with visual-only execution

📈 Designed for: Clarity, adaptability, and full intraday control

Pullback Pro Dow Strategy v7 (ADX Filter)

### **Strategy Description (For TradingView)**

#### **Title:** Pullback Pro: Dow Theory & ADX Strategy

---

#### **1. Summary**

This strategy is designed to identify and trade pullbacks within an established trend, based on the core principles of Dow Theory. It uses market structure (pivot highs and lows) to determine the trend direction and an Exponential Moving Average (EMA) to pinpoint pullback entry opportunities.

To enhance trade quality and avoid ranging markets, an ADX (Average Directional Index) filter is integrated to ensure that entries are only taken when the trend has sufficient momentum.

---

#### **2. Core Logic: How It Works**

The strategy's logic is broken down into three main steps:

**Step 1: Trend Determination (Dow Theory)**

* The primary trend is identified by analyzing recent pivot points.

* An **Uptrend** is confirmed when the script detects a pattern of higher highs and higher lows (HH/HL).

* A **Downtrend** is confirmed by a pattern of lower highs and lower lows (LH/LL).

* If neither pattern is present, the strategy considers the market to be in a range and will not seek trades.

**Step 2: Entry Signal (Pullback to EMA)**

* Once a clear trend is established, the strategy waits for a price correction.

* **Long Entry:** In a confirmed uptrend, a long position is initiated when the price pulls back and crosses *under* the specified EMA.

* **Short Entry:** In a confirmed downtrend, a short position is initiated when the price rallies and crosses *over* the EMA.

**Step 3: Confirmation & Risk Management**

* **ADX Filter:** To ensure the trend is strong enough to trade, an entry signal is only validated if the ADX value is above a user-defined threshold (e.g., 25). This helps filter out weak signals during choppy or consolidating markets.

* **Stop Loss:** The initial Stop Loss is automatically and logically placed at the last market structure point:

* For long trades, it's placed at the `lastPivotLow`.

* For short trades, it's placed at the `lastPivotHigh`.

* **Take Profit:** Two Take Profit levels are calculated based on user-defined Risk-to-Reward (R:R) ratios. The strategy allows for partial profit-taking at the first target (TP1), moving the remainder of the position to the second target (TP2).

---

#### **3. Input Settings Explained**

**① Dow Theory Settings**

* **Pivot Lookback Period:** Determines the sensitivity for detecting pivot highs and lows. A smaller number makes it more sensitive to recent price swings; a larger number focuses on more significant, longer-term pivots.

**② Entry Logic (Pullback)**

* **Pullback EMA Length:** Sets the period for the Exponential Moving Average used to identify pullback entries.

**③ Risk & Exit Management**

* **Take Profit 1 R:R:** Sets the Risk-to-Reward ratio for the first take-profit target.

* **Take Profit 1 (%):** The percentage of the position to be closed when TP1 is hit.

* **Take Profit 2 R:R:** Sets the Risk-to-Reward ratio for the final take-profit target.

**④ Filters**

* **Use ADX Trend Filter:** A master switch to enable or disable the ADX filter.

* **ADX Length:** The lookback period for the ADX calculation.

* **ADX Threshold:** The minimum ADX value required to confirm a trade signal. Trades will only be placed if the ADX is above this level.

---

#### **4. Best Practices & Recommendations**

* This is a trend-following system. It is designed to perform best in markets that exhibit clear, sustained trending behavior.

* It may underperform in choppy, sideways, or strongly ranging markets. The ADX filter is designed to help mitigate this, but no filter is perfect.

* **Crucially, you must backtest this strategy thoroughly** on your preferred financial instrument and timeframe before considering any live application.

* Experiment with the `Pivot Lookback Period`, `Pullback EMA Length`, and `ADX Threshold` to optimize performance for a specific market's characteristics.

---

#### **DISCLAIMER**

This script is provided for educational and informational purposes only. It does not constitute financial advice. All trading involves a high level of risk, and past performance is not indicative of future results. You are solely responsible for your own trading decisions. The author assumes no liability for any financial losses you may incur from using this strategy. Always conduct your own research and due diligence.

Chaikin Oscillator Enhanced📊 What Is the Chaikin Oscillator?

The Chaikin Oscillator is a momentum indicator that helps traders understand the strength of buying and selling pressure in the market, based on volume and price movement.

It is calculated as the difference between two moving averages (short-term and long-term) of the Accumulation/Distribution Line (A/D Line). This line combines price and volume to show whether money is flowing into or out of an asset.

________________________________________

🧠 Simple Concept

• When big traders are buying, they usually do so with volume support—the Chaikin Oscillator picks this up.

• When volume is rising but price is falling, or vice versa, it shows hidden strength or weakness.

So, this indicator helps you see what the smart money is doing, even if the price isn’t moving much.

________________________________________

🛠️ How It Works

• Oscillator Value Above Zero → More buying pressure (bullish).

• Oscillator Value Below Zero → More selling pressure (bearish).

• Crossing above zero → A potential buy signal.

• Crossing below zero → A potential sell signal.

The histogram (vertical bars) in the indicator changes color:

• Green bars = Positive momentum.

• Red bars = Negative momentum.

________________________________________

🎯 How Traders Use It for Entry and Exit

✅ For Entries:

• Buy Entry: When the oscillator crosses above the zero line and the bars turn green, it means buyers are stepping in with volume.

• For better confirmation, combine it with price breaking above a resistance level.

❌ For Exits or Shorts:

• Sell Exit or Short Entry: When the oscillator crosses below the zero line and bars turn red, it suggests selling pressure is growing.

• If the price is also below support, it’s a stronger signal.

________________________________________

🔍 Example Use Case:

1. You’re watching a stock or crypto that's been going sideways.

2. Suddenly, the Chaikin Oscillator crosses above zero, and green bars appear.

3. That’s your early clue that big buyers might be entering.

4. If price confirms this with a breakout, you can enter a long position.

________________________________________

🌐 Where Is It Useful?

The Chaikin Oscillator is great for:

• Stocks (especially volume-heavy large caps)

• ETFs

• Cryptocurrency (on exchanges that provide volume data)

• Forex – less reliable unless volume is proxy-based

⚠️ Important: It won’t work well on instruments where volume data is missing or unreliable (like some CFDs or synthetic assets).

________________________________________

🧭 Pro Tips for Using It:

• Combine it with support/resistance, moving averages, or candlestick patterns.

• Avoid trading only based on this indicator—use it as confirmation.

• Use the alerts (added in the script) so you don’t miss key movements.

________________________________________

RSI-Adaptive T3 + Squeeze Momentum Strategy✅ Strategy Guide: RSI-Adaptive T3 + Squeeze Momentum Strategy

📌 Overview

The RSI-Adaptive T3 + Squeeze Momentum Strategy is a dynamic trend-following strategy based on an RSI-responsive T3 moving average and Squeeze Momentum detection .

It adapts in real-time to market volatility to enhance entry precision and optimize risk.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

The main objective of this strategy is to catch the early phase of a trend and generate consistent entry signals.

Designed to be intuitive and accessible for traders from beginner to advanced levels.

✨ Key Features

RSI-Responsive T3: T3 length dynamically adjusts according to RSI values for adaptive trend detection

Squeeze Momentum: Combines Bollinger Bands and Keltner Channels to identify trend buildup phases

Visual Triggers: Entry signals are generated from T3 crossovers and momentum strength after squeeze release

📊 Trading Rules

Long Entry:

When T3 crosses upward, momentum is positive, and the squeeze has just been released.

Short Entry:

When T3 crosses downward, momentum is negative, and the squeeze has just been released.

Exit (Reversal):

When the opposite condition to the entry is triggered, the position is reversed.

💰 Risk Management Parameters

Pair & Timeframe: BTC/USD (30-minute chart)

Capital (simulated): $30,00

Order size: `$100` per trade (realistic, low-risk sizing)

Commission: 0.02%

Slippage: 2 pips

Risk per Trade: 5%

Number of Trades (backtest period): 181

📊 Performance Overview

Symbol: BTC/USD

Timeframe: 30-minute chart

Date Range: January 1, 2024 – July 3, 2025

Win Rate: 47.8%

Profit Factor: 2.01

Net Profit: 173.16 (units not specified)

Max Drawdown: 5.77% or 24.91 (0.79%)

⚙️ Indicator Parameters

Indicator Name: RSI-Adaptive T3 + Squeeze Momentum

RSI Length: 14

T3 Min Length: 5

T3 Max Length: 50

T3 Volume Factor: 0.7

BB Length: 27 (Multiplier: 2.0)

KC Length: 20 (Multiplier: 1.5, TrueRange enabled)

🖼 Visual Support

T3 slope direction, squeeze status, and momentum bars are visually plotted on the chart,

providing high clarity for quick trend analysis and execution.

🔧 Strategy Improvements & Uniqueness

Inspired by the RSI Adaptive T3 by ChartPrime and Squeeze Momentum Indicator by LazyBear ,

this strategy fuses both into a hybrid trend-reversal and momentum breakout detection system .

Compared to traditional trend-following methods, it excels at capturing early trend signals with greater sensitivity .

✅ Summary

The RSI-Adaptive T3 + Squeeze Momentum Strategy combines momentum detection with volatility-responsive risk management.

With a strong balance between visual clarity and practicality, it serves as a powerful tool for traders seeking high repeatability.

⚠️ This strategy is based on historical data and does not guarantee future profits.

Always use appropriate risk management when applying it.

Contrarian RSIContrarian RSI Indicator

Pairs nicely with Contrarian 100 MA (optional hide/unhide buy/sell signals)

Description

The Contrarian RSI is a momentum-based technical indicator designed to identify potential reversal points in price action by combining a unique RSI calculation with a predictive range model inspired by the "Contrarian 5 Levels" logic. Unlike traditional RSI, which measures price momentum based solely on price changes, this indicator integrates a smoothed, weighted momentum calculation and predictive price ranges to generate contrarian signals. It is particularly suited for traders looking to capture reversals in trending or range-bound markets.

This indicator is versatile and can be used across various timeframes, though it performs best on higher timeframes (e.g., 1H, 4H, or Daily) due to reduced noise and more reliable signals. Lower timeframes may require additional testing and careful parameter tuning to optimize performance.

How It Works

The Contrarian RSI combines two primary components:

Predictive Ranges (5 Levels Logic): This calculates a smoothed price average that adapts to market volatility using an ATR-based mechanism. It helps identify significant price levels that act as potential support or resistance zones.

Contrarian RSI Calculation: A modified RSI calculation that uses weighted momentum from the predictive ranges to measure buying and selling pressure. The result is smoothed and paired with a user-defined moving average to generate clear signals.

The indicator generates buy (long) and sell (exit) signals based on crossovers and crossunders of user-defined overbought and oversold levels, making it ideal for contrarian trading strategies.

Calculation Overview

Predictive Ranges (5 Levels Logic):

Uses a custom function (pred_ranges) to calculate a dynamic price average (avg) based on the ATR (Average True Range) multiplied by a user-defined factor (mult).

The average adjusts only when the price moves beyond the ATR threshold, ensuring responsiveness to significant price changes while filtering out noise.

This calculation is performed on a user-specified timeframe (tf5Levels) for multi-timeframe analysis.

Contrarian RSI:

Compares consecutive predictive range values to calculate gains (g) and losses (l) over a user-defined period (crsiLength).

Applies a Gaussian weighting function (weight = math.exp(-math.pow(i / crsiLength, 2))) to prioritize recent price movements.

Computes a "wave ratio" (net_momentum / total_energy) to normalize momentum, which is then scaled to a 0–100 range (qrsi = 50 + 50 * wave_ratio).

Smooths the result with a 2-period EMA (qrsi_smoothed) for stability.

Moving Average:

Applies a user-selected moving average (SMA, EMA, WMA, SMMA, or VWMA) with a customizable length (maLength) to the smoothed RSI (qrsi_smoothed) to generate the final indicator value (qrsi_ma).

Signal Generation:

Long Entry: Triggered when qrsi_ma crosses above the oversold level (oversoldLevel, default: 1).

Long Exit: Triggered when qrsi_ma crosses below the overbought level (overboughtLevel, default: 99).

Entry and Exit Rules

Long Entry: Enter a long position when the Contrarian RSI (qrsi_ma) crosses above the oversold level (default: 1). This suggests the asset is potentially oversold and due for a reversal.

Long Exit: Exit the long position when the Contrarian RSI (qrsi_ma) crosses below the overbought level (default: 99), indicating a potential overbought condition and a reversal to the downside.

Customization: Adjust overboughtLevel and oversoldLevel to fine-tune sensitivity. Lower timeframes may benefit from tighter levels (e.g., 20 for oversold, 80 for overbought), while higher timeframes can use extreme levels (e.g., 1 and 99) for stronger reversals.

Timeframe Considerations

Higher Timeframes (Recommended): The indicator is optimized for higher timeframes (e.g., 1H, 4H, Daily) due to its reliance on predictive ranges and smoothed momentum, which perform best with less market noise. These timeframes typically yield more reliable reversal signals.

Lower Timeframes: The indicator can be used on lower timeframes (e.g., 5M, 15M), but signals may be noisier and require additional confirmation (e.g., from price action or other indicators). Extensive backtesting and parameter optimization (e.g., adjusting crsiLength, maLength, or mult) are recommended for lower timeframes.

Inputs

Contrarian RSI Length (crsiLength): Length for RSI momentum calculation (default: 5).

RSI MA Length (maLength): Length of the moving average applied to the RSI (default: 1, effectively no MA).

MA Type (maType): Choose from SMA, EMA, WMA, SMMA, or VWMA (default: SMA).

Overbought Level (overboughtLevel): Upper threshold for exit signals (default: 99).

Oversold Level (oversoldLevel): Lower threshold for entry signals (default: 1).

Plot Signals on Main Chart (plotOnChart): Toggle to display signals on the price chart or the indicator panel (default: false).

Plotted on Lower:

Plotted on Chart:

5 Levels Length (length5Levels): Length for predictive range calculation (default: 200).

Factor (mult): ATR multiplier for predictive ranges (default: 6.0).

5 Levels Timeframe (tf5Levels): Timeframe for predictive range calculation (default: chart timeframe).

Visuals

Contrarian RSI MA: Plotted as a yellow line, representing the smoothed Contrarian RSI with the applied moving average.

Overbought/Oversold Lines: Red line for overbought (default: 99) and green line for oversold (default: 1).

Signals: Blue circles for long entries, white circles for long exits. Signals can be plotted on the main chart (plotOnChart = true) or the indicator panel (plotOnChart = false).

Usage Notes

Use the indicator in conjunction with other tools (e.g., support/resistance, trendlines, or volume) to confirm signals.

Test extensively on your chosen timeframe and asset to optimize parameters like crsiLength, maLength, and mult.

Be cautious with lower timeframes, as false signals may occur due to market noise.

The indicator is designed for contrarian strategies, so it works best in markets with clear reversal patterns.

Disclaimer

This indicator is provided for educational and informational purposes only. Always conduct thorough backtesting and risk management before using any indicator in live trading. The author is not responsible for any financial losses incurred.

Anti-SMT + FVG SignalMade by Laila

Anti-SMT + FVG Strategy

A contrarian price-action strategy that combines SMT illusion with Fair Value Gap (FVG) confirmation and multiple filters.

Strategy Concept

This strategy challenges traditional SMT divergence logic. Instead of entering trades based on expected SMT divergence between correlated pairs (e.g., EURUSD and DXY), it assumes the divergence is false and will reverse. The concept is to take advantage of these false signals, also known as "SMT illusions."

To confirm the setup, the strategy integrates Fair Value Gaps (FVGs), which are price imbalances left unfilled between candle 1 and 3.

Anti-SMT Logic

Short Entry:

EURUSD makes a new high (Candle 1)

DXY does not make a new low

Long Entry:

EURUSD makes a new low (Candle 1)

DXY does not make a new high

This divergence is considered false, and the strategy expects a reversal.

Fair Value Gap (FVG) Confirmation

A trade is only triggered if the price touches a Fair Value Gap during:

Candle 1 (the candle that forms the SMT illusion), or

Candle 2 (entry confirmation)

This helps avoid low-quality setups and increases entry precision.

Additional Filters

To improve robustness and prevent overfitting, the strategy includes:

EMA Trend Filter:

Long entries are allowed only if price is above the 50 EMA

Short entries are allowed only if price is below the 50 EMA

Time Filter:

Trades are only permitted between 08:00 and 18:00 UTC

Cooldown Filter:

A minimum of 10 candles between trades is required to prevent overtrading

Strategy Parameters and Defaults

Optimized for EURUSD on the 4-hour (4H) timeframe

Includes realistic commission and slippage

Uses conservative position sizing (e.g., 1% per trade)

Backtesting over hundreds of trades shows approximately 57% win rate under default conditions

These results are historical and do not guarantee future performance

Purpose and Value

This strategy offers a structured and logical approach to contrarian trading by:

Introducing the concept of false SMT divergence

Using price inefficiencies (FVGs) as confirmation

Filtering trades with realistic and widely accepted conditions

Encouraging quality over quantity through strict entry rules

It is not a simple mashup but a well-defined trading system that blends institutional concepts in a usable framework.

Long-Leg Doji Breakout StrategyThe Long-Leg Doji Breakout Strategy is a sophisticated technical analysis approach that capitalizes on market psychology and price action patterns.

Core Concept: The strategy identifies Long-Leg Doji candlestick patterns, which represent periods of extreme market indecision where buyers and sellers are in equilibrium. These patterns often precede significant price movements as the market resolves this indecision.

Pattern Recognition: The algorithm uses strict mathematical criteria to identify authentic Long-Leg Doji patterns. It requires the candle body to be extremely small (≤0.1% of the total range) while having long wicks on both sides (at least 2x the body size). An ATR filter ensures the pattern is significant relative to recent volatility.

Trading Logic: Once a Long-Leg Doji is identified, the strategy enters a "waiting mode," monitoring for a breakout above the doji's high (long signal) or below its low (short signal). This confirmation approach reduces false signals by ensuring the market has chosen a direction.

Risk Management: The strategy allocates 10% of equity per trade and uses a simple moving average crossover for exits. Visual indicators help traders understand the pattern identification and trade execution process.

Psychological Foundation: The strategy exploits the natural market cycle where uncertainty (represented by the doji) gives way to conviction (the breakout), creating high-probability trading opportunities.

The strength of this approach lies in its ability to identify moments when market sentiment shifts from confusion to clarity, providing traders with well-defined entry and exit points while maintaining proper risk management protocols.

How It Works

The strategy operates on a simple yet powerful principle: identify periods of market indecision, then trade the subsequent breakout when the market chooses direction.

Step 1: Pattern Detection

The algorithm scans for Long-Leg Doji candles, which have three key characteristics:

Tiny body (open and close prices nearly equal)

Long upper wick (significant rejection of higher prices)

Long lower wick (significant rejection of lower prices)

Step 2: Confirmation Wait

Once a doji is detected, the strategy doesn't immediately trade. Instead, it marks the high and low of that candle and waits for a definitive breakout.

Step 3: Trade Execution

Long Entry: When price closes above the doji's high

Short Entry: When price closes below the doji's low

Step 4: Exit Strategy

Positions are closed when price crosses back through a 20-period moving average, indicating potential trend reversal.

Market Psychology Behind It

A Long-Leg Doji represents a battlefield between bulls and bears that ends in a stalemate. The long wicks show that both sides tried to push price in their favor but failed. This creates a coiled spring effect - when one side finally gains control, the move can be explosive as trapped traders rush to exit and momentum traders jump aboard.

Key Parameters

Doji Body Threshold (0.1%): Ensures the body is truly small relative to the candle's range

Wick Ratio (2.0): Both wicks must be at least twice the body size

ATR Filter: Uses Average True Range to ensure the pattern is significant in current market conditions

Position Size: 10% of equity per trade for balanced risk management

Pros:

High Probability Setups: Doji patterns at key levels often lead to significant moves as they represent genuine shifts in market sentiment.

Clear Rules: Objective criteria for entry and exit eliminate emotional decision-making and provide consistent execution.

Risk Management: Built-in position sizing and exit rules help protect capital during losing trades.

Market Neutral: Works equally well for long and short positions, adapting to market direction rather than fighting it.

Visual Confirmation: The strategy provides clear visual cues, making it easy to understand when patterns are forming and trades are triggered.

Cons:

False Breakouts: In choppy or ranging markets, price may break the doji levels only to quickly reverse, creating whipsaws.

Patience Required: Traders must wait for both pattern formation and breakout confirmation, which can test discipline during active market periods.

Simple Exit Logic: The moving average exit may be too simplistic, potentially cutting profits short during strong trends or holding losers too long during reversals.

Volatility Dependent: The strategy relies on sufficient volatility to create meaningful doji patterns - it may underperform in extremely quiet markets.

Lagging Entries: Waiting for breakout confirmation means missing the very beginning of moves, reducing potential profit margins.

Best Market Conditions

The strategy performs optimally during periods of moderate volatility when markets are making genuine directional decisions rather than just random noise. It works particularly well around key support/resistance levels where the market's indecision is most meaningful.

Optimization Considerations

Consider combining with additional confluence factors like volume analysis, support/resistance levels, or other technical indicators to improve signal quality. The exit strategy could also be enhanced with trailing stops or multiple profit targets to better capture extended moves while protecting gains.

Best for Index option,

Enjoy !!

Momentum Fusion v1Momentum Fusion v1

Overview

Momentum Fusion v1 (MFusion) is a multi-oscillator indicator that combines several components to analyze market momentum and trend strength. It incorporates modified versions of classic indicators such as PVI (Positive Volume Index), NVI (Negative Volume Index), MFI (Money Flow Index), RSI, Stochastic, and Bollinger Bands Oscillator. The indicator displays a histogram that changes color based on momentum strength and includes "FUSION🔥" signal labels when extreme values are reached.

Indicator Settings

Parameters:

EMA Length – Smoothing period for the moving average (default: 255).

Smoothing Period – Internal calculation smoothing parameter (default: 15).

BB Multiplier – Standard deviation multiplier for Bollinger Bands (default: 2.0).

Show verde / marron / media lines – Toggles the display of auxiliary lines.

Show FUSION🔥 label – Enables/disables signal labels.

Indicator Components

1. PVI (Positive Volume Index)

Formula:

pvi := volume > volume ? nz(pvi ) + (close - close ) / close * sval : nz(pvi )

Description:

PVI increases when volume rises compared to the previous bar and accounts for price percentage change. The stronger the price movement with increasing volume, the higher the PVI value.

2. NVI (Negative Volume Index)

Formula:

nvi := volume < volume ? nz(nvi ) + (close - close ) / close * sval : nz(nvi )

Description:

NVI tracks price movements during declining volume. If the price rises on low volume, it may indicate a "stealth" trend.

3. Money Flow Index (MFI)

Formula:

100 - 100 / (1 + up / dn)

Description:

An oscillator measuring money flow strength. Values above 80 suggest overbought conditions, while values below 20 indicate oversold conditions.

4. Stochastic Oscillator

Formula:

k = 100 * (close - lowest(low, length)) / (highest(high, length) - lowest(low, length))

Description:

A classic stochastic oscillator showing price position relative to the selected period's range.

5. Bollinger Bands Oscillator

Formula:

(tprice - BB midline) / (upper BB - lower BB) * 100

Description:

Indicates the price position relative to Bollinger Bands in percentage terms.

Key Lines & Histogram

1. Verde (Green Line)

Calculation:

verde = marron + oscp (normalized PVI)

Interpretation:

Higher values indicate stronger bullish momentum. A FUSION🔥 signal appears when the value reaches 750+.

2. Marron (Brown Line)

Calculation:

marron = (RSI + MFI + Bollinger Osc + Stochastic / 3) / 2

Interpretation:

A composite oscillator combining multiple indicators. Higher values suggest overbought conditions.

3. Media (Red Line)

Calculation:

media = EMA of marron with smoothing period

Interpretation:

Acts as a signal line for trend confirmation.

4. Histogram

Calculation:

histo = verde - marron

Colors:

Bright green (>100) – Strong bullish momentum.

Light green (>0) – Moderate bullish momentum.

Orange (<0) – Bearish momentum.

Red (<-100) – Strong bearish momentum.

Signals & Alerts

1. FUSION🔥 (Strong Momentum)

Condition:

verde >= 750

Visualization:

A "FUSION🔥" label appears below the chart.

Alert:

Can be set to trigger notifications when the condition is met.

2. Background Aura

Condition:

verde > 850

Visualization:

The chart background turns teal, indicating extreme momentum.

Usage Recommendations

FUSION🔥 Signal – Can be used as a long entry point when confirmed by other indicators.

Histogram:

1. Green bars – Potential long entry.

2. Red/orange bars – Potential short entry.

3. Media & Marron Crossover – Can serve as an additional trend filter.

4. Suitable for a 5-15 minute time frame

Conclusion

Momentum Fusion v1 is a powerful tool for momentum analysis, combining multiple indicators into a unified system. It is suitable for:

Trend traders (catching strong movements).

Scalpers (identifying short-term impulses).

Swing traders (filtering entry points).

The indicator features customizable settings and visual signals, making it adaptable to various trading styles.

Ergodic Market Divergence (EMD)Ergodic Market Divergence (EMD)

Bridging Statistical Physics and Market Dynamics Through Ensemble Analysis

The Revolutionary Concept: When Physics Meets Trading

After months of research into ergodic theory—a fundamental principle in statistical mechanics—I've developed a trading system that identifies when markets transition between predictable and unpredictable states. This indicator doesn't just follow price; it analyzes whether current market behavior will persist or revert, giving traders a scientific edge in timing entries and exits.

The Core Innovation: Ergodic Theory Applied to Markets

What Makes Markets Ergodic or Non-Ergodic?

In statistical physics, ergodicity determines whether a system's future resembles its past. Applied to trading:

Ergodic Markets (Mean-Reverting)

- Time averages equal ensemble averages

- Historical patterns repeat reliably

- Price oscillates around equilibrium

- Traditional indicators work well

Non-Ergodic Markets (Trending)

- Path dependency dominates

- History doesn't predict future

- Price creates new equilibrium levels

- Momentum strategies excel

The Mathematical Framework

The Ergodic Score combines three critical divergences:

Ergodic Score = (Price Divergence × Market Stress + Return Divergence × 1000 + Volatility Divergence × 50) / 3

Where:

Price Divergence: How far current price deviates from market consensus

Return Divergence: Momentum differential between instrument and market

Volatility Divergence: Volatility regime misalignment

Market Stress: Adaptive multiplier based on current conditions

The Ensemble Analysis Revolution

Beyond Single-Instrument Analysis

Traditional indicators analyze one chart in isolation. EMD monitors multiple correlated markets simultaneously (SPY, QQQ, IWM, DIA) to detect systemic regime changes. This ensemble approach:

Reveals Hidden Divergences: Individual stocks may diverge from market consensus before major moves

Filters False Signals: Requires broader market confirmation

Identifies Regime Shifts: Detects when entire market structure changes

Provides Context: Shows if moves are isolated or systemic

Dynamic Threshold Adaptation

Unlike fixed-threshold systems, EMD's boundaries evolve with market conditions:

Base Threshold = SMA(Ergodic Score, Lookback × 3)

Adaptive Component = StDev(Ergodic Score, Lookback × 2) × Sensitivity

Final Threshold = Smoothed(Base + Adaptive)

This creates context-aware signals that remain effective across different market environments.

The Confidence Engine: Know Your Signal Quality

Multi-Factor Confidence Scoring

Every signal receives a confidence score based on:

Signal Clarity (0-35%): How decisively the ergodic threshold is crossed

Momentum Strength (0-25%): Rate of ergodic change

Volatility Alignment (0-20%): Whether volatility supports the signal

Market Quality (0-20%): Price convergence and path dependency factors

Real-Time Confidence Updates

The Live Confidence metric continuously updates, showing:

- Current opportunity quality

- Market state clarity

- Historical performance influence

- Signal recency boost

- Visual Intelligence System

Adaptive Ergodic Field Bands

Dynamic bands that expand and contract based on market state:

Primary Color: Ergodic state (mean-reverting)

Danger Color: Non-ergodic state (trending)

Band Width: Expected price movement range

Squeeze Indicators: Volatility compression warnings

Quantum Wave Ribbons

Triple EMA system (8, 21, 55) revealing market flow:

Compressed Ribbons: Consolidation imminent

Expanding Ribbons: Directional move developing

Color Coding: Matches current ergodic state

Phase Transition Signals

Clear entry/exit markers at regime changes:

Bull Signals: Ergodic restoration (mean reversion opportunity)

Bear Signals: Ergodic break (trend following opportunity)

Confidence Labels: Percentage showing signal quality

Visual Intensity: Stronger signals = deeper colors

Professional Dashboard Suite

Main Analytics Panel (Top Right)

Market State Monitor

- Current regime (Ergodic/Non-Ergodic)

- Ergodic score with threshold

- Path dependency strength

- Quantum coherence percentage

Divergence Metrics

- Price divergence with severity

- Volatility regime classification

- Strategy mode recommendation

- Signal strength indicator

Live Intelligence

- Real-time confidence score

- Color-coded risk levels

- Dynamic strategy suggestions

Performance Tracking (Left Panel)

Signal Analytics

- Total historical signals

- Win rate with W/L breakdown

- Current streak tracking

- Closed trade counter

Regime Analysis

- Current market behavior

- Bars since last signal

- Recommended actions

- Average confidence trends

Strategy Command Center (Bottom Right)

Adaptive Recommendations

- Active strategy mode

- Primary approach (mean reversion/momentum)

- Suggested indicators ("weapons")

- Entry/exit methodology

- Risk management guidance

- Comprehensive Input Guide

Core Algorithm Parameters

Analysis Period (10-100 bars)

Scalping (10-15): Ultra-responsive, more signals, higher noise

Day Trading (20-30): Balanced sensitivity and stability

Swing Trading (40-100): Smooth signals, major moves only Default: 20 - optimal for most timeframes

Divergence Threshold (0.5-5.0)

Hair Trigger (0.5-1.0): Catches every wiggle, many false signals

Balanced (1.5-2.5): Good signal-to-noise ratio

Conservative (3.0-5.0): Only extreme divergences Default: 1.5 - best risk/reward balance

Path Memory (20-200 bars)

Short Memory (20-50): Recent behavior focus, quick adaptation

Medium Memory (50-100): Balanced historical context

Long Memory (100-200): Emphasizes established patterns Default: 50 - captures sufficient history without lag

Signal Spacing (5-50 bars)

Aggressive (5-10): Allows rapid-fire signals

Normal (15-25): Prevents clustering, maintains flow

Conservative (30-50): Major setups only Default: 15 - optimal trade frequency

Ensemble Configuration

Select markets for consensus analysis:

SPY: Broad market sentiment

QQQ: Technology leadership

IWM: Small-cap risk appetite

DIA: Blue-chip stability

More instruments = stronger consensus but potentially diluted signals

Visual Customization

Color Themes (6 professional options):

Quantum: Cyan/Pink - Modern trading aesthetic

Matrix: Green/Red - Classic terminal look

Heat: Blue/Red - Temperature metaphor

Neon: Cyan/Magenta - High contrast

Ocean: Turquoise/Coral - Calming palette

Sunset: Red-orange/Teal - Warm gradients

Display Controls:

- Toggle each visual component

- Adjust transparency levels

- Scale dashboard text

- Show/hide confidence scores

- Trading Strategies by Market State

- Ergodic State Strategy (Primary Color Bands)

Market Characteristics

- Price oscillates predictably

- Support/resistance hold

- Volume patterns repeat

- Mean reversion dominates

Optimal Approach

Entry: Fade moves at band extremes

Target: Middle band (equilibrium)

Stop: Just beyond outer bands

Size: Full confidence-based position

Recommended Tools

- RSI for oversold/overbought

- Bollinger Bands for extremes

- Volume profile for levels

- Non-Ergodic State Strategy (Danger Color Bands)

Market Characteristics

- Price trends persistently

- Levels break decisively

- Volume confirms direction

- Momentum accelerates

Optimal Approach

Entry: Breakout from bands

Target: Trail with expanding bands

Stop: Inside opposite band

Size: Scale in with trend

Recommended Tools

- Moving average alignment

- ADX for trend strength

- MACD for momentum

- Advanced Features Explained

Quantum Coherence Metric

Measures phase alignment between individual and ensemble behavior:

80-100%: Perfect sync - strong mean reversion setup

50-80%: Moderate alignment - mixed signals

0-50%: Decoherence - trending behavior likely

Path Dependency Analysis

Quantifies how much history influences current price:

Low (<30%): Technical patterns reliable

Medium (30-50%): Mixed influences

High (>50%): Fundamental shift occurring

Volatility Regime Classification

Contextualizes current volatility:

Normal: Standard strategies apply

Elevated: Widen stops, reduce size

Extreme: Defensive mode required

Signal Strength Indicator

Real-time opportunity quality:

- Distance from threshold

- Momentum acceleration

- Cross-validation factors

Risk Management Framework

Position Sizing by Confidence

90%+ confidence = 100% position size

70-90% confidence = 75% position size

50-70% confidence = 50% position size

<50% confidence = 25% or skip

Dynamic Stop Placement

Ergodic State: ATR × 1.0 from entry

Non-Ergodic State: ATR × 2.0 from entry

Volatility Adjustment: Multiply by current regime

Multi-Timeframe Alignment

- Check higher timeframe regime

- Confirm ensemble consensus

- Verify volume participation

- Align with major levels

What Makes EMD Unique

Original Contributions

First Ergodic Theory Trading Application: Transforms abstract physics into practical signals

Ensemble Market Analysis: Revolutionary multi-market divergence system

Adaptive Confidence Engine: Institutional-grade signal quality metrics

Quantum Coherence: Novel market alignment measurement

Smart Signal Management: Prevents clustering while maintaining responsiveness

Technical Innovations

Dynamic Threshold Adaptation: Self-adjusting sensitivity

Path Memory Integration: Historical dependency weighting

Stress-Adjusted Scoring: Market condition normalization

Real-Time Performance Tracking: Built-in strategy analytics

Optimization Guidelines

By Timeframe

Scalping (1-5 min)

Period: 10-15

Threshold: 0.5-1.0

Memory: 20-30

Spacing: 5-10

Day Trading (5-60 min)

Period: 20-30

Threshold: 1.5-2.5

Memory: 40-60

Spacing: 15-20

Swing Trading (1H-1D)

Period: 40-60

Threshold: 2.0-3.0

Memory: 80-120

Spacing: 25-35

Position Trading (1D-1W)

Period: 60-100

Threshold: 3.0-5.0

Memory: 100-200

Spacing: 40-50

By Market Condition

Trending Markets

- Increase threshold

- Extend memory

- Focus on breaks

Ranging Markets

- Decrease threshold

- Shorten memory

- Focus on restores

Volatile Markets

- Increase spacing

- Raise confidence requirement

- Reduce position size

- Integration with Other Analysis

- Complementary Indicators

For Ergodic States

- RSI divergences

- Bollinger Band squeezes

- Volume profile nodes

- Support/resistance levels

For Non-Ergodic States

- Moving average ribbons

- Trend strength indicators

- Momentum oscillators

- Breakout patterns

- Fundamental Alignment

- Check economic calendar

- Monitor sector rotation

- Consider market themes

- Evaluate risk sentiment

Troubleshooting Guide

Too Many Signals:

- Increase threshold

- Extend signal spacing

- Raise confidence minimum

Missing Opportunities

- Decrease threshold

- Reduce signal spacing

- Check ensemble settings

Poor Win Rate

- Verify timeframe alignment

- Confirm volume participation

- Review risk management

Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. Trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results.

The ergodic framework provides unique market insights but cannot predict future price movements with certainty. Always use proper risk management, conduct your own analysis, and never risk more than you can afford to lose.

This tool should complement, not replace, comprehensive trading strategies and sound judgment. Markets remain inherently unpredictable despite advanced analysis techniques.

Transform market chaos into trading clarity with Ergodic Market Divergence.

Created with passion for the TradingView community

Trade with insight. Trade with anticipation.

— Dskyz , for DAFE Trading Systems

Lyapunov Market Instability (LMI)Lyapunov Market Instability (LMI)

What is Lyapunov Market Instability?

Lyapunov Market Instability (LMI) is a revolutionary indicator that brings chaos theory from theoretical physics into practical trading. By calculating Lyapunov exponents—a measure of how rapidly nearby trajectories diverge in phase space—LMI quantifies market sensitivity to initial conditions. This isn't another oscillator or trend indicator; it's a mathematical lens that reveals whether markets are in chaotic (trending) or stable (ranging) regimes.

Inspired by the meditative color field paintings of Mark Rothko, this indicator transforms complex chaos mathematics into an intuitive visual experience. The elegant simplicity of the visualization belies the sophisticated theory underneath—just as Rothko's seemingly simple color blocks contain profound depth.

Theoretical Foundation (Chaos Theory & Lyapunov Exponents)

In dynamical systems, the Lyapunov exponent (λ) measures the rate of separation of infinitesimally close trajectories:

λ > 0: System is chaotic—small changes lead to dramatically different outcomes (butterfly effect)

λ < 0: System is stable—trajectories converge, perturbations die out

λ ≈ 0: Edge of chaos—transition between regimes

Phase Space Reconstruction

Using Takens' embedding theorem , we reconstruct market dynamics in higher dimensions:

Time-delay embedding: Create vectors from price at different lags

Nearest neighbor search: Find historically similar market states

Trajectory evolution: Track how these similar states diverged over time

Divergence rate: Calculate average exponential separation

Market Application

Chaotic markets (λ > threshold): Strong trends emerge, momentum dominates, use breakout strategies

Stable markets (λ < threshold): Mean reversion dominates, fade extremes, range-bound strategies work

Transition zones: Market regime about to change, reduce position size, wait for confirmation

How LMI Works

1. Phase Space Construction

Each point in time is embedded as a vector using historical prices at specific delays (τ). This reveals the market's hidden attractor structure.

2. Lyapunov Calculation

For each current state, we:

- Find similar historical states within epsilon (ε) distance

- Track how these initially similar states evolved

- Measure exponential divergence rate

- Average across multiple trajectories for robustness

3. Signal Generation

Chaos signals: When λ crosses above threshold, market enters trending regime

Stability signals: When λ crosses below threshold, market enters ranging regime

Divergence detection: Price/Lyapunov divergences signal potential reversals

4. Rothko Visualization

Color fields: Background zones represent market states with Rothko-inspired palettes

Glowing line: Lyapunov exponent with intensity reflecting market state

Minimalist design: Focus on essential information without clutter

Inputs:

📐 Lyapunov Parameters

Embedding Dimension (default: 3)

Dimensions for phase space reconstruction

2-3: Simple dynamics (crypto/forex) - captures basic momentum patterns

4-5: Complex dynamics (stocks/indices) - captures intricate market structures

Higher dimensions need exponentially more data but reveal deeper patterns

Time Delay τ (default: 1)

Lag between phase space coordinates

1: High-frequency (1m-15m charts) - captures rapid market shifts

2-3: Medium frequency (1H-4H) - balances noise and signal

4-5: Low frequency (Daily+) - focuses on major regime changes

Match to your timeframe's natural cycle

Initial Separation ε (default: 0.001)

Neighborhood size for finding similar states

0.0001-0.0005: Highly liquid markets (major forex pairs)

0.0005-0.002: Normal markets (large-cap stocks)

0.002-0.01: Volatile markets (crypto, small-caps)

Smaller = more sensitive to chaos onset

Evolution Steps (default: 10)

How far to track trajectory divergence

5-10: Fast signals for scalping - quick regime detection

10-20: Balanced for day trading - reliable signals

20-30: Slow signals for swing trading - major regime shifts only

Nearest Neighbors (default: 5)

Phase space points for averaging

3-4: Noisy/fast markets - adapts quickly

5-6: Balanced (recommended) - smooth yet responsive

7-10: Smooth/slow markets - very stable signals

📊 Signal Parameters

Chaos Threshold (default: 0.05)

Lyapunov value above which market is chaotic

0.01-0.03: Sensitive - more chaos signals, earlier detection

0.05: Balanced - optimal for most markets

0.1-0.2: Conservative - only strong trends trigger

Stability Threshold (default: -0.05)

Lyapunov value below which market is stable

-0.01 to -0.03: Sensitive - quick stability detection

-0.05: Balanced - reliable ranging signals

-0.1 to -0.2: Conservative - only deep stability

Signal Smoothing (default: 3)

EMA period for noise reduction

1-2: Raw signals for experienced traders

3-5: Balanced - recommended for most

6-10: Very smooth for position traders

🎨 Rothko Visualization

Rothko Classic: Deep reds for chaos, midnight blues for stability

Orange/Red: Warm sunset tones throughout

Blue/Black: Cool, meditative ocean depths

Purple/Grey: Subtle, sophisticated palette

Visual Options:

Market Zones : Background fields showing regime areas

Transitions: Arrows marking regime changes

Divergences: Labels for price/Lyapunov divergences

Dashboard: Real-time state and trading signals

Guide: Educational panel explaining the theory

Visual Logic & Interpretation

Main Elements

Lyapunov Line: The heart of the indicator

Above chaos threshold: Market is trending, follow momentum

Below stability threshold: Market is ranging, fade extremes

Between thresholds: Transition zone, reduce risk

Background Zones: Rothko-inspired color fields

Red zone: Chaotic regime (trending)

Gray zone: Transition (uncertain)

Blue zone: Stable regime (ranging)

Transition Markers:

Up triangle: Entering chaos - start trend following

Down triangle: Entering stability - start mean reversion

Divergence Signals:

Bullish: Price makes low but Lyapunov rising (stability breaking down)

Bearish: Price makes high but Lyapunov falling (chaos dissipating)

Dashboard Information

Market State: Current regime (Chaotic/Stable/Transitioning)

Trading Bias: Specific strategy recommendation

Lyapunov λ: Raw value for precision

Signal Strength: Confidence in current regime

Last Change: Bars since last regime shift

Action: Clear trading directive

Trading Strategies

In Chaotic Regime (λ > threshold)

Follow trends aggressively: Breakouts have high success rate

Use momentum strategies: Moving average crossovers work well

Wider stops: Expect larger swings

Pyramid into winners: Trends tend to persist

In Stable Regime (λ < threshold)

Fade extremes: Mean reversion dominates

Use oscillators: RSI, Stochastic work well

Tighter stops: Smaller expected moves

Scale out at targets: Trends don't persist

In Transition Zone

Reduce position size: Uncertainty is high

Wait for confirmation: Let regime establish

Use options: Volatility strategies may work

Monitor closely: Quick changes possible

Advanced Techniques

- Multi-Timeframe Analysis

- Higher timeframe LMI for regime context

- Lower timeframe for entry timing

- Alignment = highest probability trades

- Divergence Trading

- Most powerful at regime boundaries

- Combine with support/resistance

- Use for early reversal detection

- Volatility Correlation

- Chaos often precedes volatility expansion

- Stability often precedes volatility contraction

- Use for options strategies

Originality & Innovation

LMI represents a genuine breakthrough in applying chaos theory to markets:

True Lyapunov Calculation: Not a simplified proxy but actual phase space reconstruction and divergence measurement

Rothko Aesthetic: Transforms complex math into meditative visual experience

Regime Detection: Identifies market state changes before price makes them obvious

Practical Application: Clear, actionable signals from theoretical physics

This is not a combination of existing indicators or a visual makeover of standard tools. It's a fundamental rethinking of how we measure and visualize market dynamics.

Best Practices

Start with defaults: Parameters are optimized for broad market conditions

Match to your timeframe: Adjust tau and evolution steps

Confirm with price action: LMI shows regime, not direction

Use appropriate strategies: Chaos = trend, Stability = reversion

Respect transitions: Reduce risk during regime changes

Alerts Available

Chaos Entry: Market entering chaotic regime - prepare for trends

Stability Entry: Market entering stable regime - prepare for ranges

Bullish Divergence: Potential bottom forming

Bearish Divergence: Potential top forming

Chart Information

Script Name: Lyapunov Market Instability (LMI) Recommended Use: All markets, all timeframes Best Performance: Liquid markets with clear regimes

Academic References

Takens, F. (1981). "Detecting strange attractors in turbulence"

Wolf, A. et al. (1985). "Determining Lyapunov exponents from a time series"

Rosenstein, M. et al. (1993). "A practical method for calculating largest Lyapunov exponents"

Note: After completing this indicator, I discovered @loxx's 2022 "Lyapunov Hodrick-Prescott Oscillator w/ DSL". While both explore Lyapunov exponents, they represent independent implementations with different methodologies and applications. This indicator uses phase space reconstruction for regime detection, while his combines Lyapunov concepts with HP filtering.

Disclaimer

This indicator is for research and educational purposes only. It does not constitute financial advice or provide direct buy/sell signals. Chaos theory reveals market character, not future prices. Always use proper risk management and combine with your own analysis. Past performance does not guarantee future results.

See markets through the lens of chaos. Trade the regime, not the noise.

Bringing theoretical physics to practical trading through the meditative aesthetics of Mark Rothko

Trade with insight. Trade with anticipation.

— Dskyz , for DAFE Trading Systems

Livermore-Seykota Breakout StrategyStrategy Name: Livermore-Seykota Breakout Strategy

Objective: Execute breakout trades inspired by Jesse Livermore, filtered by trend confirmation (Ed Seykota) and risk-managed with ATR (Paul Tudor Jones style).

Entry Conditions:

Long Entry:

Close price breaks above recent pivot high.

Price is above main EMA (EMA50).

EMA20 > EMA200 (uptrend confirmation).

Current volume > 20-period SMA (volume confirmation).

Short Entry:

Close price breaks below recent pivot low.

Price is below main EMA (EMA50).

EMA20 < EMA200 (downtrend confirmation).

Current volume > 20-period SMA.

Exit Conditions:

Stop-loss: ATR × 3 from entry price.

Trailing stop: activated with offset of ATR × 2.

Strengths:

Trend-aligned entries with volume breakout confirmation.

Dynamic ATR-based risk management.

Inspired by principles of three legendary traders.

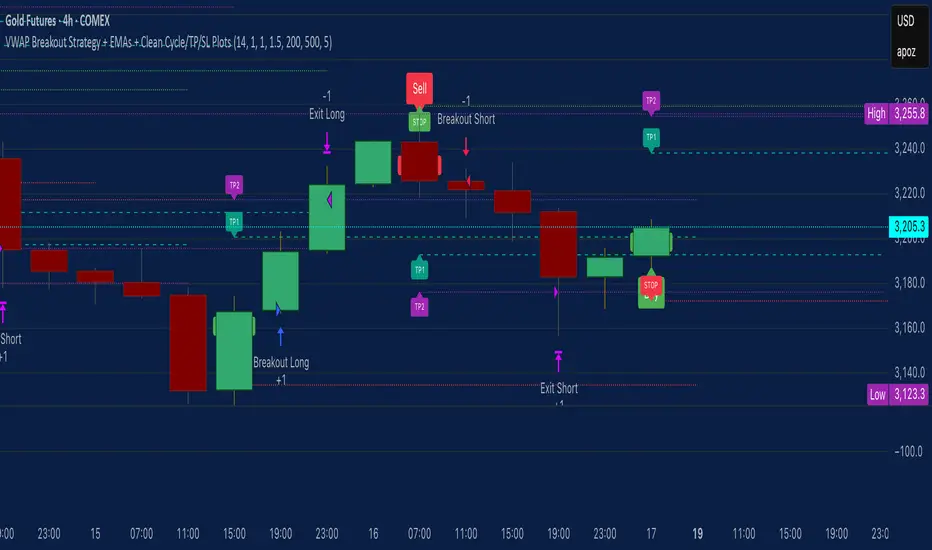

VWAP Breakout Strategy + EMAs + Clean Cycle/TP/SL PlotsHere’s a quick user-guide to get you up and running with your “VWAP Breakout Strategy + EMAs + Clean Cycle/TP/SL Plots” script in TradingView:

⸻

1. Installing the Script

1. Open TradingView, go to Pine Editor (bottom panel).

2. Paste in your full Pine-v6 code and hit Add to chart.

3. Save it (“Save as…”): give it a memorable name (e.g. “VWAP Breakout+EMAs”).

⸻

2. Configuring Your Inputs

Once it’s on the chart, click the ⚙️ Settings icon to tune:

Setting Default What it does

ATR Length 14 Period for average true range (volatility measure)

ATR Multiplier for Stop 1.5 How many ATRs away your stop-loss sits

TP1 / TP2 Multipliers (ATR) 1.0 / 2.0 Distance of TP1 and TP2 in ATR multiples

Show VWAP / EMAs On Toggles the blue VWAP line & EMAs (100/34/5)

Full Cycle Range Points 200 Height of the shaded “cycle zone”

Pivot Lookback 5 How many bars back to detect a pivot low

Round Number Step 500 Spacing of your dotted horizontal lines

Show TP/SL Labels On Toggles all the “ENTRY”, “TP1”, “TP2”, “STOP” tags

Feel free to adjust ATR multipliers and cycle-zone size based on the instrument’s typical range.

⸻

3. Reading the Signals

• Long Entry:

• Trigger: price crosses above VWAP

• You’ll see a green “Buy” tag at the low of the signal bar, plus an “ENTRY (Long)” label at the close.

• Stop is plotted as a red dashed line below (ATR × 1.5), and TP1/TP2 as teal and purple lines above.

• Short Entry:

• Trigger: price crosses below VWAP

• A red “Sell” tag appears at the high, with “ENTRY (Short)” at the close.

• Stop is the green line above; TP1/TP2 are dashed teal/purple lines below.

⸻

4. Full Cycle Zone

Whenever a new pivot low is detected (using your Pivot Lookback), the script deletes the old box and draws a shaded yellow rectangle from that low up by “Full Cycle Range Points.”

• Use this to visualize the “maximum expected swing” from your pivot.

• You can quickly see whether price is still traveling within a normal cycle or has overstretched.

⸻

5. Round-Number Levels

With Show Round Number Levels enabled, you’ll always get horizontal dotted lines at the nearest multiples of your “Round Number Step” (e.g. every 500 points).

• These often act as psychological support/resistance.

• Handy to see confluence with VWAP or cycle-zone edges.

⸻

6. Tips & Best-Practices

• Timeframes: Apply on any intraday chart (5 min, 15 min, H1…), but match your ATR length & cycle-points to the timeframe’s typical range.

• Backtest first: Use the Strategy Tester tab to review performance, tweak ATR multipliers or cycle size, then optimize.

• Combine with context: Don’t trade VWAP breakouts blindly—look for confluence (e.g. support/resistance zones, higher-timeframe trend).

• Label clutter: If too many labels build up, you can toggle Show TP/SL Labels off and rely just on the lines.

⸻

That’s it! Once you’ve added it to your chart and dialed in the inputs, your entries, exits, cycle ranges, and key levels will all be plotted automatically. Feel free to experiment with the ATR multipliers and cycle-zone size until it fits your instrument’s personality. Happy trading!

RCI Strategy [PineIndicators]RCI Strategy

This strategy leverages the Rank Correlation Index (RCI) — a statistical oscillator that measures the relationship between time and price rank — combined with a configurable moving average filter. It offers clean, rule-based entries and exits, and visually enhanced trade tracking via labeled markers and boxes on the chart.

The RCI Strategy is well-suited for momentum traders looking to capture directional shifts with confirmation through RCI smoothing.

Core Logic

1. Rank Correlation Index (RCI)

Measures how closely price changes correlate with time rankings.

Values range between -100 and +100.

Thresholds at ±80 help identify potential reversals or extremes.

2. RCI Smoothing via Moving Average

A moving average (MA) is applied to the RCI to smooth out fluctuations.

Supported MA types:

SMA

EMA

SMMA (RMA)

WMA

VWMA

Users can disable the smoothing by selecting "None".

Trade Entry Logic

Long Entry: RCI crosses above the selected moving average.

Short Entry: RCI crosses below the moving average.

Entries are restricted by trade direction settings:

Long Only

Short Only

Long & Short

Visual Features

RCI Panel Display

Plots RCI line and its moving average in a separate pane.

Horizontal guide lines at 0, +80, and -80 help visualize signal zones.

Trade Labels on Chart

Buy Label: Plotted when a long entry is executed.

Close Label: Plotted when any position is closed.

Triangle markers for visual emphasis on direction change.

Trade Visualization Boxes

A colored box is drawn between entry and exit prices.

Green = profitable trade; Red = losing trade.

Two horizontal lines connect entry and exit prices for reference.

Customization Parameters

RCI Source: Select input price for the RCI (default: close).

RCI Length: Set sensitivity of the oscillator.

MA Type and Length: Choose and configure the smoothing filter.

Trade Direction Mode: Define whether to allow Long, Short, or both.

Use Cases

Swing traders who want to trade directional reversals with statistical backing.

Traders seeking a clean and visual strategy based on rank momentum.

Environments where both trend and range dynamics occur.

Conclusion

The RCI Strategy is a non-repainting, rule-based trading model that combines rank correlation momentum with smoothed trend logic. Its clean visual markers, labeled trades, and flexible MA filters make it a valuable tool for discretionary and systematic traders alike.

Parabolic RSI Strategy [ChartPrime × PineIndicators]This strategy combines the strengths of the Relative Strength Index (RSI) with a Parabolic SAR logic applied directly to RSI values.

Full credit to ChartPrime for the original concept and indicator, licensed under the MPL 2.0.

It provides clear momentum-based trade signals using an innovative method that tracks RSI trend reversals via a customized Parabolic SAR, enhancing traditional oscillator strategies with dynamic trend confirmation.

How It Works

The system overlays a Parabolic SAR on the RSI, detecting trend shifts in RSI itself rather than on price, offering early reversal insight with visual and algorithmic clarity.

Core Components

1. RSI-Based Trend Detection

Calculates RSI using a customizable length (default: 14).

Uses upper and lower thresholds (default: 70/30) for overbought/oversold zones.

2. Parabolic SAR Applied to RSI

A custom Parabolic SAR function tracks momentum within the RSI, not price.

This allows the system to capture RSI trend reversals more responsively.

Configurable SAR parameters: Start, Increment, and Maximum acceleration.

3. Signal Generation

Long Entry: Triggered when the SAR flips below the RSI line.

Short Entry: Triggered when the SAR flips above the RSI line.

Optional RSI filter ensures that:

Long entries only occur above a minimum RSI (e.g. 50).

Short entries only occur below a maximum RSI.

Built-in logic prevents new positions from being opened against trend without prior exit.

Trade Modes & Controls

Choose from:

Long Only

Short Only

Long & Short

Optional setting to reverse positions on opposite signal (instead of waiting for a flat close).

Visual Features

1. RSI Plotting with Thresholds

RSI is displayed in a dedicated pane with overbought/oversold fill zones.

Custom horizontal lines mark threshold boundaries.

2. Parabolic SAR Overlay on RSI

SAR dots color-coded for trend direction.

Visible only when enabled by user input.

3. Entry & Exit Markers

Diamonds: Mark entry points (above for shorts, below for longs).

Crosses: Mark exit points.

Strategy Strengths

Provides early momentum reversal entries without relying on price candles.

Combines oscillator and trend logic without repainting.

Works well in both trending and mean-reverting markets.

Easy to configure with fine-tuned filter options.

Recommended Use Cases

Intraday or swing traders who want to catch RSI-based reversals early.

Traders seeking smoother signals than price-based Parabolic SAR entries.

Users of RSI looking to reduce false positives via trend tracking.

Customization Options

RSI Length and Thresholds.

SAR Start, Increment, and Maximum values.

Trade Direction Mode (Long, Short, Both).

Optional RSI filter and reverse-on-signal settings.

SAR dot color customization.

Conclusion

The Parabolic RSI Strategy is an innovative, non-repainting momentum strategy that enhances RSI-based systems with trend-confirming logic using Parabolic SAR. By applying SAR logic to RSI values, this strategy offers early, visualized, and filtered entries and exits that adapt to market dynamics.

Credit to ChartPrime for the original methodology, published under MPL-2.0.

HMA 200 + EMA 20 Crossover StrategyThis strategy combines a long-term trend filter using the Hull Moving Average (HMA 200) with a short-term entry trigger using the Exponential Moving Average (EMA 20).

📈 Entry Logic:

Buy Entry: When price is above the HMA 200 and crosses above the EMA 20.

Sell Entry: When price is below the HMA 200 and crosses below the EMA 20.

The strategy closes the current position and reverses on the opposite signal.

⚙️ Strategy Settings (Backtest Configuration):

Position size: 10% of equity per trade

Commission: 0.1% per trade (to simulate broker fees)

Slippage: 2 ticks (to reflect realistic fill conditions)

✅ Purpose:

This script is designed to identify high-probability trades in the direction of the overall trend, avoiding whipsaw conditions. It is useful for traders looking for a dynamic crossover-based system that filters trades based on longer-term momentum.

🔎 Make sure to test across multiple assets and timeframes. For best results, apply this strategy to liquid trending markets like major FX pairs, indices, or high-cap stocks.

ADX and DI - Trader FelipeADX and DI - Trader Felipe

This indicator combines the Average Directional Index (ADX) and the Directional Indicators (DI+ and DI-) to help traders assess market trends and their strength. It is designed to provide a clear view of whether the market is in a trending phase (either bullish or bearish) and helps identify potential entry and exit points.

What is ADX and DI?

DI+ (Green Line):