FVG Detector LibraryLibrary "FVG Detector Library"

🔵 Introduction

To save time and improve accuracy in your scripts for identifying Fair Value Gaps (FVGs), you can utilize this library. Apart from detecting and plotting FVGs, one of the most significant advantages of this script is the ability to filter FVGs, which you'll learn more about below. Additionally, the plotting of each FVG continues until either a new FVG occurs or the current FVG is mitigated.

🔵 Definition

Fair Value Gap (FVG) refers to a situation where three consecutive candlesticks do not overlap. Based on this definition, the minimum conditions for detecting a fair gap in the ascending scenario are that the minimum price of the last candlestick should be greater than the maximum price of the third candlestick, and in the descending scenario, the maximum price of the last candlestick should be smaller than the minimum price of the third candlestick.

If the filter is turned off, all FVGs that meet at least the minimum conditions are identified. This mode is simplistic and results in a high number of identified FVGs.

If the filter is turned on, you have four options to filter FVGs :

1. Very Aggressive : In addition to the initial condition, another condition is added. For ascending FVGs, the maximum price of the last candlestick should be greater than the maximum price of the middle candlestick. Similarly, for descending FVGs, the minimum price of the last candlestick should be smaller than the minimum price of the middle candlestick. In this mode, a very small number of FVGs are eliminated.

2. Aggressive : In addition to the conditions of the Very Aggressive mode, in this mode, the size of the middle candlestick should not be small. This mode eliminates more FVGs compared to the Very Aggressive mode.

3. Defensive : In addition to the conditions of the Very Aggressive mode, in this mode, the size of the middle candlestick should be relatively large, and most of it should consist of the body. Also, for identifying ascending FVGs, the second and third candlesticks must be positive, and for identifying descending FVGs, the second and third candlesticks must be negative. In this mode, a significant number of FVGs are eliminated, and the remaining FVGs have a decent quality.

4. Very Defensive : In addition to the conditions of the Defensive mode, the first and third candlesticks should not resemble very small-bodied doji candlesticks. In this mode, the majority of FVGs are filtered out, and the remaining ones are of higher quality.

By default, we recommend using the Defensive mode.

🔵 How to Use

🟣 Parameters

To utilize this library, you need to provide four input parameters to the function.

"FVGFilter" determines whether you wish to apply a filter on FVGs or not. The possible inputs for this parameter are "On" and "Off", provided as strings.

"FVGFilterType" determines the type of filter to be applied to the found FVGs. These filters include four modes: "Very Defensive", "Defensive", "Aggressive", and "Very Aggressive", respectively exhibiting decreasing sensitivity and indicating a higher number of Fair Value Gaps (FVG).

The parameter "ShowDeFVG" is a Boolean value defined as either "true" or "false". If this value is "true", FVGs are shown during the Bullish Trend; however, if it is "false", they are not displayed.

The parameter "ShowSuFVG" is a Boolean value defined as either "true" or "false". If this value is "true", FVGs are displayed during the Bearish Trend; however, if it is "false", they are not displayed.

FVGDetector(FVGFilter, FVGFilterType, ShowDeFVG, ShowSuFVG)

Parameters:

FVGFilter (string)

FVGFilterType (string)

ShowDeFVG (bool)

ShowSuFVG (bool)

🟣 Import Library

You can use the "FVG Detector" library in your script using the following expression:

import TFlab/FVGDetectorLibrary/1 as FVG

🟣 Input Parameters

The descriptions related to the input parameters were provided in the "Parameter" section. In this section, for your convenience, the code related to the inputs is also included, and you can copy and paste it into your script.

PFVGFilter = input.string('On', 'FVG Filter', )

PFVGFilterType = input.string('Defensive', 'FVG Filter Type', )

PShowDeFVG = input.bool(true, ' Show Demand FVG')

PShowSuFVG = input.bool(true, ' Show Supply FVG')

🟣 Call Function

You can copy the following code into your script to call the FVG function. This code is based on the naming conventions provided in the "Input Parameter" section, so if you want to use exactly this code, you should have similar parameter names or have copied the "Input Parameter" values.

FVG.FVGDetector(PFVGFilter, PFVGFilterType, PShowDeFVG, PShowSuFVG)

Cerca negli script per "gaps"

Gap Removal IndicatorThis gap indicator shows the price of your chosen instrument as if no gaps had occurred overnight. It can be especially useful on highly-volatile exchange-listed instruments that track other 24/7 assets, because the normal candlestick chart of these instruments will create a large amount of noise that may decrease the accuracy of your indicators or make the trend harder to see.

Gaps are determined with the following code:

daychange = ta.change(dayofmonth)

gapup = daychange and open > math.max(open,close)

gapdown = daychange and open < math.min(open,close)

Whereas the gap value is determined by taking the overnight difference in prices:

downgap_change = math.min(open,close) - open

upgap_change = open - math.max(open,close)

The gap changes are cumulatively added and subtracted from the initial closing price to create the gap-adjusted price. The price will depend on how many bars your subscription allows, so pay more attention to the relative differences and/or trend than the cumulative gap-adjusted price itself.

The gap indicator comes pre-built with normal candlestick and Heikin-Ashi candle types, and four indicators (two EMAs, Bollinger bands, and a supertrend). All elements are configurable.

TASC 2024.01 Gap Momentum System█ OVERVIEW

TASC's January 2024 edition of Traders' Tips features an article titled “Gap Momentum” by Perry J. Kaufman. The article discusses how a trader might create a momentum strategy based on opening gap data. This script implements the Gap Momentum system presented therein.

█ CONCEPTS

In the article, Perry J. Kaufman introduces Gap Momentum as a cumulative series constructed in the same way as On-Balance Volume (OBV) , but using gap openings (today’s open minus yesterday’s close).

To smoothen the resulting time series (i.e., obtain the " signal line "), the author applies a simple moving average . Subsequently, he proposes the following two trading rules for a long-only trading system:

• Enter a long position when the signal line is moving higher.

• Exit when the signal line is moving lower.

█ CALCULATIONS

The calculation of Gap Momentum involves the following steps:

1. Calculate the ratio of the sum of positive gaps over the past N days to the sum of negative gaps (absolute values) over the same time period.

2. Add the resulting gap ratio to the cumulative time series. This time series is the Gap Momentum.

3. Keep moving forward, as in an N-day moving average.

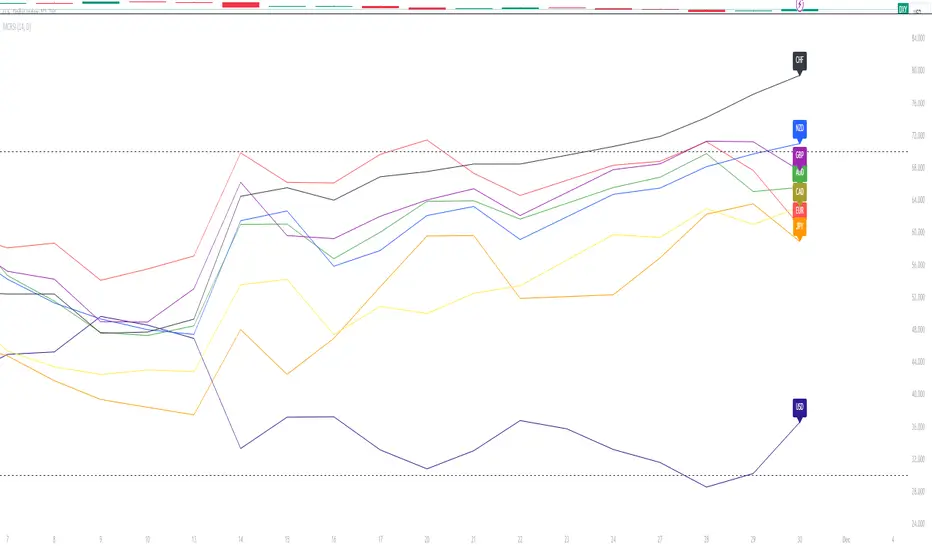

Major Currency RSI Indicator (MCRSI)Experience the power of multi-dimensional analysis with our Multi-Currency RSI Indicator (MCRSI). This innovative tool allows traders to simultaneously track and compare the Relative Strength Index (RSI) of eight different currencies in a single chart.

The MCRSI calculates the RSI for USD (DXY), EUR (EXY), JPY (JXY), CAD (CXY), AUD (AXY), NZD (ZXY), GBP (BXY), and CHF (SXY), covering a broad range of the forex market. Each RSI line is color-coded for easy differentiation and equipped with labels at the last bar for a clutter-free view.

Our indicator is designed with user-friendly customization features. You can easily adjust the length of the RSI and the time frame according to your trading strategy. It also handles gaps in the chart data with the barmerge.gaps_on option, ensuring accurate and consistent RSI calculations.

Whether you are a novice trader seeking to understand market dynamics better or an experienced trader wanting to diversify your technical analysis, the MCRSI offers a unique perspective of the forex market. This multi-currency approach can help identify potential trading opportunities that could be missed when analyzing currencies in isolation.

Harness the power of multi-currency RSI analysis with our MCRSI Indicator. It's time to step up your trading game!

Features:

Tracks 8 different currencies simultaneously

Color-coded RSI lines for easy identification

Customizable RSI length and time frame

Handles gaps in chart data

Last bar labels for a clutter-free view

Ideal for forex traders of all experience levels

How to Use:

Add the MCRSI to your TradingView chart.

Adjust the RSI length and time frame as needed.

Monitor the RSI lines and their intersections for potential trading signals.

Happy trading!

Pocket Pivot BreakoutPocket Pivot Breakout Indicator

The pocket pivot breakout indicator will show a blue arrow under the candle if both the following conditions are met:

1. The percentage change of the candle on that day from open is greater than 3%.

2. The volume on the day of 3% candle is higher than the highest red volume in the past 10 days.

The second condition is based on the 'Pocket Pivot' concept developed by Gil Morales and Chris Kacher.

If only one of the conditions is met, while the other is not, there will be no arrow.

How to use the Pocket Pivot Breakout indicator?

1. If the stock is breaking out of a proper base like (cup & handle, Darvas box etc.), you can use the blue arrow as an indicator to make your initial buy.

2. If you already own a stock, the blue arrow indicator can be used for pyramiding, following a continuation breakout from a proper base.

3. Avoid making a new entry or continuation entry if the stock is too extended from 10ma.

Gap-up > 0.5% Indicator

Gap-up Indicator displays a blue colored candle when a stock gaps up by more than 0.5% compared to previous day's close.

It is turned off by default. To activate it, check the box next to Gap-up > 0.5% in the indicator options.

How to use the Gap-up Indicator?

1. When a stock gaps up, it usually indicates strength, especially if on the day of the gap-up, the stock closes strongly.

2. This indicator should not be used in isolation but with a proper base breakout from a tight consolidation.

3. If a stock is already extended from 10ma, avoid taking any new or continuation entries.

Precautions

1. Avoid buying longs when the general market conditions are not favorable.

2. Avoid buying stocks below 200ma.

3. Avoid making a new entry or pyramid entry if a stock is too extended from 10ma.

Important Points

1. Always choose fundamentally strong stocks showing strong growth in earnings/margins/sales.

2. Buy these fundamentally strong stocks when they are breaking out of proper bases.

3. To learn more about pocket pivots and buyable gap-ups, read the book, Trade Like an O'Neil Disciple (by Gil Morales & Chris Kacher).

Cheers

Simranjit

NDOG + ASIA CONFLUENCENDOG (New Day Opening Gap) Visualization:

The indicator identifies and visualizes New Day Opening Gaps (NDOGs), which are essentially the differences between the opening price of a new trading day and the closing price of the previous day.

For each NDOG identified, it creates a box on the chart that highlights the high and low price range of the NDOG.

The color of these boxes, as well as the number of NDOGs to be displayed, can be customized by the user.

Asia Session Highlighting:

The indicator includes a feature to highlight the Asia trading session, typically spanning from 18:00 to 00:00, but customizable to suit different time zones or preferences.

It does not dynamically calculate or display the Asia session but uses a fixed time input by the user.

The color for highlighting the Asia session can be chosen by the user.

Additional Lines on NDOGs:

The script draws horizontal lines at the high and low of each NDOG, spanning from 18:00 to 00:00, to visually represent the range of the NDOG during the Asia session.

The color of these lines can be customized.

Customizability:

The indicator provides various input options for users to customize the colors of the NDOG boxes and the lines that represent the high and low of the NDOGs.

Purpose and Usage:

This indicator is useful for traders who focus on price gaps between trading days and are particularly interested in the price action during the Asia trading session.

It helps in identifying potential zones of interest where significant price movements or trading activities could occur, especially at the opening of a new trading day.

ICT NWOG/NDOG [Source Code] (fadi)New Week Opening Gap (NWOG) and New Day Opening Gap (NDOG) are areas on the chart where price tend to react to and has the potential of moving from one gap to the next. These gaps can act as support and resistance zones where price can bounce of, or go through and retest. Areas of interest are the high, low, the Consequent Encroachment (C.E.), which is the middle between high and low of each gap.

Event Horizon is the 50% distance between two NWOGs and price tend to react to, and could act as Premium/ Discount between two NWOGs.

New Week Opening Gap (NWOG)

The difference between Friday close, and Sunday open. Consequent Encroachment (C.E.) is the area between two NWOGs.

Settings NWOG

- The Colors in the form of Current/Previous and line style for NWOG

- Background color to use for Current/Previous

- Number of NWOGs to use by the indicator (ICT recommends using minimum of 5)

- Extend Configuration:

-- Always Extend all NWOGs

-- Above and below only Shows the immediate two NWOGs that are above and below current price. These two NWOGs are recalculated as price moves

-- Any that is near current price Any NWOG that is near the current price, this can result in multiple NWOGs being displayed, with some overlapping

- Event Horizon only applicable when using the "Above and below only settings"

-- Show Date label and type of gap

New Day Opening Gap (NDOG)

The difference between Yesterday's close and Today's open.

Settings NDOG

- The Colors in the form of Current/Previous and line style for NDOG

- Background color to use for Current/Previous

- Number of NDOGs to use by the indicator, default is 1 but price tend to react to previous ones as well

- Extend Configuration:

-- Always Extend all NDOGs

-- Above and below only Shows the immediate two NDOGs that are above and below current price. These two NDOGs are recalculated as price moves

-- Any that is near current price Any NDOG that is near the current price, this can result in multiple NDOGs being displayed, with some overlapping

-- Show Date label and type of gap

Other Settings

Number of candles to use in calculation is used to calculate the size of the candles in order to derive the distance from current price. If current candle sizes is more important than over longer period of time then use 14 or near that number

Factor multiplier for distance test is the number above times X value. Lower timeframes require a higher number than a larger timeframe. If day trading, a value between 10 and 20 is probably best. If swing trading, a value between 5 and 10 is probably best.

Buffer How many candles beyond current price to extend the gaps by. this is helpful to provide cleaner view of the price action

Volume Spike Analysis [Trendoscope]The Volume Spike Analysis is designed to detect volume spikes in a trading instrument's data. Rather than relying on the traditional method of comparing volume to its moving average, this indicator employs a distinctive approach to ensure accuracy.

Methodology

Historical Volume Comparison: The indicator first assesses the current bar's volume, say 100k, and looks back historically to determine the last instance when the volume was equal to or exceeded this level.

High Volume Bar Gap Calculation: The intervals or gaps between high volume bars are recorded. These gaps help in determining how common or rare a particular volume spike is.

Spike Magnitude Determination: Here, the extent of the volume spike is gauged in relation to either the median, lowest, or average volume of the intervening bars. The reference metric (median, lowest, or average) can be chosen by the user through the "Volume Spike Reference" input parameter.

Spike Percentile Analysis: The calculated spike magnitude (as a percentage of the reference volume) is cataloged. This collection aids in understanding the relative intensity of the current volume spike when compared to previous spikes.

Threshold Comparisons: The indicator then compares the calculated "High Volume Distance Percentile" to the "Last High Volume Distance Percentile" and the "Volume Spike Percentile" to the "Volume Spike Threshold". If these values surpass the preset thresholds, the current bar is flagged as a high volume or volume spike bar.

Visual Components

Bar Highlighting : High volume or volume spike bars are accentuated with bright colors for easy identification. All other bars have increased transparency to reduce visual clutter.

Distance from the High Volume Bar: Indication of the number of bars since the last high volume occurrence and its respective percentile.

Comparative Factors: A factor representing the magnitude by which the current volume surpasses the lowest, median, and average volumes.

Lowest, Median and Average Volumes: The lowest and median volumes are indicated by tooltips on lines marking the respective bars. The average volume is depicted as a dotted horizontal line, with a triangle marker tooltip revealing its value.

This indicator offers a nuanced analysis of volume spikes, aiding traders in making more informed decisions.

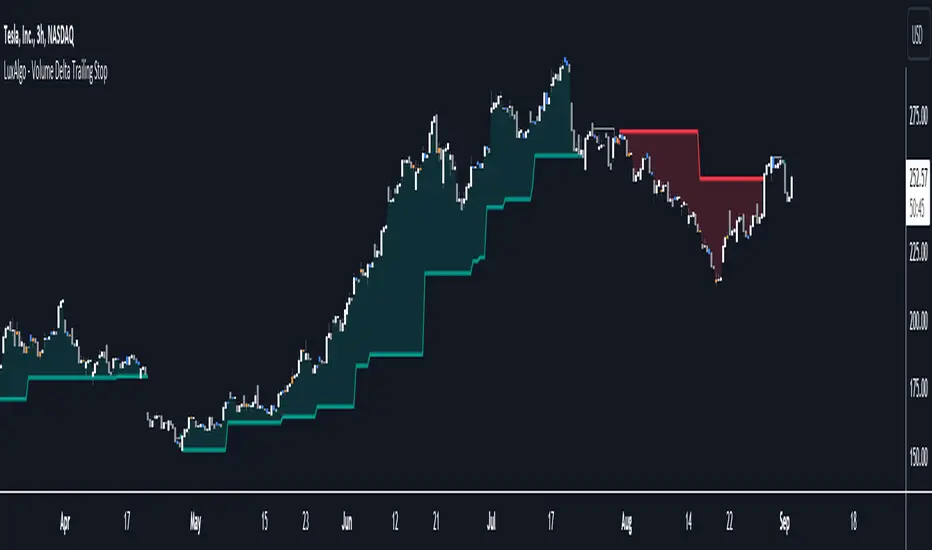

Volume Delta Trailing Stop [LuxAlgo]The ' Volume Delta Trailing Stop ' indicator uses Lower Time Frame (LTF) volume delta data which can provide potential entries together with a Volume-Delta based Trailing Stop-line .

🔶 USAGE

Our 'Volume Delta Trailing Stop' script can show potential entries/Stop Loss lines

A trigger line needs to be broken before a position is taken, after which a Volume Delta-controlled Trailing Stop-line is created:

🔶 DETAILS

🔹 Volume rises when bought or sold

🔹 When the opening price appears on the chart, a buy/sell order has been executed.

If that order is less than the available supply of that particular price, volume will rise, without moving the price.

🔹 When the opening price is the same as the closing price, the volume of that bar can be seen as "neutral volume" (nV); nor "up", nor "down" volume.

Example

A buy order doesn't fill the first available supply in the order book. This price will be the opening price with a certain volume.

When at closing time, price still hasn't moved (the first available supply in the order book isn't filled, or no movement downwards),

the closing price will be equal to the opening price, but with volume. This can be seen as "neutral volume (nV)".

🔹 Delta Volume (ΔV): this is "up volume" minus "down volume"

🔹 Standard volume is colored red when closing price is lower than opening price ( = "down volume").

🔹 Standard volume is colored green when closing price is higher OR equal (nV) than opening price ( = "up volume").

🔹 Neutral Volume

The "Neutral-Volume" is considered "Up-Volume" - setting will dictate whether nV is considered as green 'buy' volume or not.

🔶 EXAMPLE

29 July 10:00 -> 10:05, chart timeframe 5 minutes, open 29311.28, close 29313.89

close > open, so the volume (39.55) is colored green ("up volume").

(The Volume script used in the following examples is the open-source publication Volume Columns w. Alerts (V) from LucF )

Let's zoom to the 1-minute TF:

The same period is now divided into more bars, volume direction (color) is dependable on the difference between open and close.

Counting up and down volume gives a more detailed result, it remains in an upward direction though):

(ΔV = +15.51)

Let's further zoom in to the 1-second TF:

The same period is now divided into even more bars (more possibility for changing direction on each bar)

Here we see several bars that haven't moved in price, but they have volume ("neutral" volume).

(neutral volume is coloured light green here, while up volume is coloured darker green)

When we count all green and red volume bars, the result is quite different:

(ΔV = -0.35)

In total more volume is found when price went downwards, yet price went up in these 5 minutes.

-> This is the heart of our publication, when this divergence occurs, you can see a barcolor changement:

• orange: when price went up, but LTF Volume was mainly in a downward direction.

• blue: when price went down, but LTF Volume was mainly in an upwards direction.

When we split the green "up volume" into "up" and "neutral", the difference is even higher

(here "neutral volume" is colored grey):

(ΔV = -12.76; "up" - "down")

🔶 CONCEPTS

bullishBear = current bar is red but LTF volume is in upward direction -> blue bar

bearishBull = current bar is green but LTF volume is in downward direction -> orange bar

🔹 Potential positioning - forming of Trigger-line

When not in position, the script will wait for a divergence between price and volume direction. When found, a Trigger-line will appear:

• at high when a blue bar appears ( bullishBear ).

• at low when an orange bar appears ( bearishBull ).

Next step is when the Trigger-line is broken by close or high/low (settings: Trigger )

Here, the closing price went under the grey Trigger-line -> bearish position:

🔹 Trailing Stop-line

When the Trigger-line is broken, the Trailing Stop-line (TS-line) will start:

• low when bullish position

• high when bearish position

You can choose (settings -> Trigger -> Close or H/L ) whether close price or high/low should break the Trigger-line

When alerts are enabled ("Any alert() function call"), you'll get the following message:

• ' signal up ' when bullish position

• ' signal down' when bearish position

After that, the TS-line will be adjusted when:

• a blue bullishBear bar appears when in bullish position -> lowest of {low , previous blue bar's high or orange bar's low}

• an orange bearishBull bar appears when in bearish position -> highest of {high, previous blue bar's high or orange bar's low}

When alerts are enabled ("Any alert() function call"), and the TS-line is broken, you'll get the following message:

• ' TS-line broken down ' when out bullish position

• ' TS-line broken up ' when out bearish position

🔹 Reference Point

Default the direction of price will be evaluated by comparing closing price with opening price.

When open and close are the same, you'll get "neutral volume".

You can use "previous close" instead (as in built-in volume indicator) to include gaps.

If close equals open , but close is lower than previous close , it will be regarded as " down volume ",

similar, when close is higher than previous close , it will be regarded as " up volume "

Note, the setting applies for the current timeframe AND Lower timeframe:

Based on: " open " (close - open)

Based on: " previous close " (close - previous close)

🔹 Adjustment

When the TS-line changes, this can be adjusted with a percentage of price , or a multiple of " True Range "

Default (Δ line -> Adjustment - 0)

Δ line -> Adjustment 0.03% (of price)

Δ line -> Mult of TR (10)

🔶 SETTINGS

🔹 LTF: choose your Lower TimeFrame: 1S (seconds), 5S, 10S, 15S, 30S, 1 minute)

🔹 Trigger: Choose the trigger for breaking the Trigger-line ; close or H/L (high when bullish position, low when bearish position)

🔹 Δ line ( Trailing Stop-line ): add/subtract an adjustment when the TS-line changes ( default: Adjustment ):

• Adjustment ( default: 0 ): add/subtract an extra % of price

• Mult of TR : add/subtract a multiple of True Range

🔹 Based on: compare closing price against:

• open

• previous close

🔹 "Neutral-Volume" is considered "Up-Volume" : this setting will dictate whether nV is considered as green 'buy' volume or not.

🔶 CONSIDERATIONS

🔹 The lowest LTF (1S) will give you more detail and will get data close to tick data.

However, a maximum of 100,000 intrabars can be used in calculations .

This means on the daily chart you won't see anything since 1 day ~ 86400 seconds. (just over 1 bar)

-> choose a lower chart timeframe, or choose a higher LTF (5S, 10S, ... 1 minute)

🔹 Always choose a LTF lower than the current chart timeframe.

🔹 Pine Script™ code using this request.security_lower_tf() may calculate differently on historical and real-time bars, leading to repainting .

FVG w/ Fibs [QuantVue]The "FVG w/ Fibs" indicator is a trading tool designed to identify and visualize Fair Value Gaps (FVGs) while overlaying two Fibonacci retracement levels.

• Bullish FVG: Occurs when the low of the current bar is higher than the high of two bars ago, and the previous close is higher than the high of two bars ago.

• Bearish FVG: Occurs when the high of the current bar is lower than the low of two bars ago, and the previous close is lower than the low of two bars ago.

The indicator filters these gaps based on user-defined criteria such as the minimum percentage size of the gap.

Once identified, these FVGs are highlighted on the chart using customizable boxes and the 50% and 61.8% (default settings) Fibonacci retracement levels are calculated and drawn based on the size of the identified FVG.

• Dynamically updates and extends the boxes as the price evolves.

• Alerts / visual changes for FVGs that get filled.

• User option for fills by Wicks or Close

• User-customizable settings for box colors, styles, and Fibonacci level appearances

Give this indicator a BOOST and COMMENT your thoughts!

We hope you enjoy.

Cheers!

Inverse FVG with Rejections [TFO]This indicator is made to look for Inverse Fair Value Gaps (IFVGs) and show rejections from relevant areas. Fair Value Gaps (FVGs) are created when there is an energetic move that leaves a gap between the preceding and following candle's wicks. When that area is violated, we may consider that area as an Inverse FVG, treating it along the lines of a "support turned resistance" type setup with proper context.

Once a Fair Value Gap (FVG) is found with sufficient user-defined displacement, it is saved until price fully closes through that area, at which point it becomes an IFVG, which is also saved until price once again closes through that area.

Users can select a specific time period from which to look for and save FVGs, such as during the New York trading session in the following example.

Lastly, users can enable rejections that look for swing lows in bullish FVGs/IFVGs and swing highs in bearish FVGs/IFVGs. The following picture shows an instance of rejections from both regular and inverse FVGs, meaning the pivots were formed in a mutually shared area between a FVG and IFVG.

RVol LabelThis Code is update version of Code Provided by @ssbukam, Here is Link to his original Code and review the Description

Below is Original Description

1. When chart resolution is Daily or Intraday (D, 4H, 1H, 5min, etc), Relative Volume shows value based on DAILY. RVol is measured on daily basis to compare past N number of days.

2. When resolution is changed to Weekly or Monthly, then Relative Volume shows corresponding value. i.e. Weekly shows weekly relative volume of this week compared to past 'N' weeks. Likewise for Monthly. You would see change in label name. Like, Weekly chart shows W_RVol (Weekly Relative Volume). Likewise, Daily & Intraday shows D_RVol. Monthly shows M_RVol (Monthly Relative Volume).

3. Added a plot (by default hidden) for this specific reason: When you move the cursor to focus specific candle, then Indicator Value displays relative volume of that specific candle. This applies to Intraday as well. So if you're in 1HR chart and move the cursor to a specific candle, Indicator Value shows relative volume for that specific candlestick bar.

4. Updating the script so that text size and location can be customized.

Changes to Updated Label by me

1. Added Today's Volume to the Label

2. Added Total Average Volume to the Label

3. Comparison vs Both in Single Line and showing how much volume has traded vs the average volume for that time of the day

4. Aesthetic Look of the Label

How to Use Relative Volume for Trading

Using Relative Volume (RVol) in trading can be a valuable tool to help you identify potential trading opportunities and gain insight into market behavior. Here are some ways to use RVol in your trading strategy:

Identifying High-Volume Breakouts: RVol can help you spot potential breakouts when the volume surges significantly above its average. High RVol during a breakout suggests strong market interest, increasing the probability of a sustained move in the direction of the breakout.

Confirming Trends and Reversals: RVol can act as a confirmation tool for trends and reversals. A trend accompanied by rising RVol indicates a strong and sustainable move. Conversely, a trend with declining RVol might suggest a weakening trend or potential reversal.

Spotting Volume Divergence: When the price is moving in one direction, but RVol is declining or not confirming the move, it may indicate a divergence. This discrepancy could suggest a potential reversal or trend change.

Support and Resistance Confirmation: High RVol near key support or resistance levels can indicate potential price reactions at those levels. This confirmation can be valuable in determining whether a level is likely to hold or break.

Filtering Trade Signals: Incorporate RVol into your existing trading strategy as a filter. For example, you might consider taking trades only if RVol is above a certain threshold, ensuring that you focus on high-impact trading opportunities.

Avoiding Low-Volume Traps: Low RVol can indicate a lack of interest or participation in the market. In such situations, price movements may be erratic and less reliable, so it's often wise to avoid trading during low RVol periods.

Monitoring News Events: Around significant news events or earnings releases, RVol can help you gauge the market's reaction to the information. High RVol during such events can present trading opportunities but be cautious of increased volatility and potential gaps.

Adjusting Trade Size: During periods of extremely high RVol, it might be prudent to adjust your position size to account for higher risk.

Using Relative Volume in Morning Session

If the Volume traded in first 15 minute to 30 Minutes is already at 50% or 100% depending upon the ticker, it means that it is going to have very high Volume vs average by end of the day.

This gives me conviction for Long or Short Trades

Remember that RVol is not a standalone indicator; it works best when used in conjunction with other technical and fundamental analysis tools. Additionally, RVol's effectiveness may vary across different markets and trading strategies. Therefore, backtesting and validating the use of RVol in your trading approach is essential.

Lastly, risk management is crucial in trading. While RVol can provide valuable insights, it cannot guarantee profitable trades. Always use appropriate risk management strategies, such as setting stop-loss levels, and avoid overexposing yourself to the market based solely on RVol readings.

Bullish and Bearish Candlestick Patterns StrategyThe strategy is a combination of candlestick pattern analysis and Fibonacci retracement levels to identify potential buy and sell signals in the market. Here's how the strategy works and how you can trade accordingly:

Candlestick Pattern Analysis:

The strategy looks for specific bullish and bearish candlestick patterns to identify potential trend reversals or continuations. The bullish patterns include:

Bullish Engulfing: This pattern occurs when a bullish candle fully engulfs the previous bearish candle.

Hammer: It is a single candlestick pattern with a small body and a long lower wick, indicating a potential bullish reversal.

Morning Star: This pattern consists of three candles, with the middle one being a small-bodied candle that gaps down and the other two being bullish candles.

The bearish patterns include:

Bearish Engulfing: Similar to the bullish engulfing, but this time, a bearish candle fully engulfs the previous bullish candle.

Shooting Star: A single candlestick pattern with a small body and a long upper wick, suggesting a potential bearish reversal.

Evening Star: This pattern is the opposite of the morning star, with a small-bodied candle that gaps up between two bearish candles.

Fibonacci Retracement Levels:

The strategy uses Fibonacci retracement levels to determine potential support and resistance levels in the market. The main level considered in this strategy is the Fibonacci 0.5 level, which is the midpoint of the previous swing move.

Trading Accordingly:

To trade using this strategy, follow these steps:

a. Observe the Chart: Apply the indicator to your preferred chart, and observe the candlestick patterns and the plotted support, resistance, and Fibonacci 0.5 levels.

b. Buy Signal: A buy signal is generated when any of the bullish candlestick patterns (Bullish Engulfing, Hammer, Morning Star) occur, and the low price of the current candle is above or equal to the Fibonacci 0.5 level. This suggests a potential bullish reversal or continuation of an existing uptrend.

c. Sell Signal: A sell signal is generated when any of the bearish candlestick patterns (Bearish Engulfing, Shooting Star, Evening Star) occur, and the high price of the current candle is below or equal to the Fibonacci 0.5 level. This indicates a potential bearish reversal or continuation of an existing downtrend.

d. Risk Management: Place stop-loss orders to protect your position in case the market moves against your trade. Consider setting the stop-loss below the recent swing low for buy trades and above the recent swing high for sell trades.

e. Take Profit: Set a target for taking profits based on your risk-reward ratio. You can use the recent swing high for buy trades as a potential target and the recent swing low for sell trades.

f. Filter Signals: Keep in mind that not all signals will result in profitable trades. It's essential to filter signals with other technical analysis tools and consider the overall market context.

Remember that no trading strategy guarantees profits, and trading always carries inherent risks. It's crucial to practice proper risk management, use appropriate position sizing, and test the strategy thoroughly in a demo environment before applying it to live trading. Additionally, consider combining this strategy with other indicators or analysis methods to make more informed .

Fair Value Gap (FVG) UnderlayBy analyzing the size and characteristics of candlestick patterns, the Fair Value Gap indicator helps traders spot potential opportunities where the price of a currency or financial asset deviates from its fair value. The FVG is represented as a percentage and displayed as columns in an underlay on the chart.

Calculation and Interpretation:

The calculation of the FVG involves evaluating the body-to-wick ratio of a candlestick. This ratio compares the size of the body (the difference between the open and close prices) to the length of the wicks (the high and low prices). A high body-to-wick ratio indicates a significant price move within the candlestick, potentially signaling a strong market sentiment. The FVG indicator compares the size of the current candlestick with the previous candlesticks over a specified lookback period, typically the last 20 to 40 candlesticks. If the current candlestick meets the criteria for a fair value gap, it is classified as either a Bearish FVG or Bullish FVG, depending on the direction of the price movement.

Interpreting the FVG is relatively straightforward. When a Bearish FVG is detected, it suggests that the price is currently lower than its fair value, indicating a potential upward price movement in the future. This could be an opportunity to consider long positions or buying opportunities. On the other hand, when a Bullish FVG is identified, it implies that the price is higher than its fair value, signaling a possible downward price correction. Traders may consider short-selling or taking profits on long positions in such scenarios.

Coloration:

The coloration of the Fair Value Gap (FVG) indicator plays a crucial role in enhancing its visual representation and aiding interpretation. When a Bearish FVG is identified, the indicator utilizes the color scheme of lime green. This color signifies the potential for an upward price movement as the current price is considered lower than its fair value. On the other hand, a Bullish FVG is represented by the vibrant color of fuchsia, indicating a potential downward price correction as the price exceeds its fair value. The coloration serves as a visual cue, making it easier for traders to quickly identify and differentiate between different types of fair value gaps on the chart. Additionally, the barcolor is aligned with the respective FVG color, providing a comprehensive view of price inefficiencies and aiding traders in their decision-making process.

Potential Applications/Strategies:

The FVG indicator can be applied in various trading strategies and situations. One possible application is in price reversion strategies. Traders can use the FVG to identify overbought or oversold conditions in the market. When a Bullish FVG occurs, it may indicate an opportunity to consider short-selling or taking profits on long positions. Similarly, a Bearish FVG can suggest a potential buying opportunity, expecting the price to revert back to its fair value.

Another application is in confirming existing trends. The FVG can act as a confirmation tool for trends identified by other indicators or analysis techniques. When a Bullish FVG aligns with an uptrend, it may strengthen the bullish bias and provide more confidence in the upward momentum. Conversely, a Bearish FVG in conjunction with a downtrend may reinforce the bearish sentiment and support the idea of further downside potential.

Parameters:

Adjusting the parameters of the FVG indicator can be beneficial based on the trader's trading style and time frame. The body-to-wick ratio threshold and lookback period can be modified to capture different types of fair value gaps and adapt to different market conditions. Shorter lookback periods may help identify more recent FVGs, which could be suitable for short-term traders, while longer periods may capture larger price inefficiencies and cater to longer-term traders.

Limitations:

However, it's important to note that the FVG indicator, like any technical analysis tool, has its limitations. It relies on historical price patterns and may not always accurately predict future price movements. The interpretation of FVGs requires careful analysis and should be used in conjunction with other indicators, technical analysis tools, and fundamental factors to make well-informed trading decisions. Traders should also exercise proper risk management and consider the overall market context when using the FVG indicator.

In conclusion, the Fair Value Gap (FVG) indicator provides traders with valuable insights into price inefficiencies and deviations from fair value. By identifying Bearish and Bullish FVGs, traders can potentially uncover trading opportunities and make more informed decisions. However, it is crucial to combine the FVG indicator with other analysis tools, conduct thorough analysis, and exercise proper risk management to achieve consistent trading success.

Directional Volume EStimate from Price Action (RedK D_VESPA)The "Directional Volume EStimate from Price Action (RedK D_VESPA)" is another weapon for the VPA (Volume Price Analysis) enthusiasts and traders who like to include volume-based insights & signals to their trading. The basic concept is to estimate the sell and buy split of the traded volume by extrapolating the price action represented by the shape of the associated price bar. We then create and plot an average of these "estimated buy & sell volumes" - the estimated average Net Volume is the balance between these 2 averages.

D_VESPA uses clear visualizations to represent the outcomes in a less distracting and more actionable way.

How does D_VESPA work?

-------------------------------------

The key assumption is that when price moves up, this is caused by "buy" volume (or increasing demand), and when the price moves down, this is due to "selling" volume (or increasing supply). Important to note that we are making our Buy/sell volume estimates here based on the shape of the price bar, and not looking into lower time frame volume data - This is a different approach and is still aligned to the key concepts of VPA.

Originally this work started as an improvement to my Supply/Demand Volume Viewer (V.Viewer) , I ended up re-writing the whole thing after some more research and work on VPA, to improve the estimation, visualization and usability / tradability.

Think of D_VESPA as the "Pro" version of V.Viewer -- and please go back and review the details of V.Viewer as the root concepts are the same so I won't repeat them here (as it comes to exploring Balance Zone and finding Price Convergence/Divergence)

Main Features of D_VESPA

--------------------------------------

- Update Supply/Demand calculation to include 2-bar gaps (improved algo)

- Add multiple options for the moving average (MA type) for the calculation - my preference is to use WMA

- Add option to show Net Volume as 3-color bars

- Visual simplification and improvements to be less distracting & more actionable

- added options to display/hide main visuals while maintaining the status line consistency (Avg Supply, Avg Demand, Avg Net)

- add alerts for NetVol moving into Buy (crosses 0 up) or Sell (crosses 0 down) modes - or swing from one mode to the other

(there are actually 2 sets of alerts, one set for the main NetVol plot, and the other for the secondary TF NetVol - give user more options on how to utilize D_VESPA)

Quick techie piece, how does the estimated buy/sell volume algo work ?

------------------------------------------------------------------------------------------

* per our assumption, buy volume is associated with price up-moves, sell volume is associated with price down-moves

* so each of the bulls and bears will get the equivalent of the top & bottom wicks,

* for up bars, bulls get the value of the "body", else the bears get the "body"

* open gaps are allocated to bulls or bears depending on the gap direction

The below sketch explains how D_VESPA estimates the Buy/Sell Volume split based on the bar shape (including gap) - the example shows a bullish bar with an opening gap up - but the concept is the same for a down-bar or a down-gap.

I kept both the "Volume Weighted" and "2-bar Gap Impact" as options in the indicator settings - these 2 options should be always kept selected. They are there for those who would like to experiment with the difference these changes have on the buy/sell estimation. The indicator will handle cases where there is no volume data for the selected symbol, and in that case, it will simply reflect Average Estimated Bull/Bear ratio of the price bar

The Secondary TF Est Average Net Volume:

---------------------------------------------------------

I added the ability to plot the Estimate Average Net Volume for a secondary timeframe - options 1W, 1D, 1H, or Same as Chart.

- this feature provides traders the confidence to trade the lower timeframes in the same direction as the prevailing "market mode"

- this also adds more MTF support beyond the existing TradingView's built-in MTF support capability - experiment with various settings between exposing the indicator's secondary TF plot, and changing the TF option in the indicator settings.

Note on the secondary TF NetVol plot:

- the secondary TF needs to be set to same as or higher TF than the chart's TF - if not, a warning sign would show and the plot will not be enabled. for example, a day trader may set the secondary TF to 1Hr or 1Day, while looking at 5min or 15min chart. A swing/trend trader who frequently uses the daily chart may set the secondary TF to weekly, and so on..

- the secondary TF NetVol plot is hidden by default and needs to be exposed thru the indicator settings.

the below chart shows D_VESPA on a the same (daily) chart, but with secondary TF plot for the weekly TF enabled

Final Thoughts

-------------------

* RedK D_VESPA is a volume indicator, that estimates buy/sell and net volume averages based on the price action reflected by the shape of the price bars - this can provide more insight on volume compared to the classic volume/VolAverage indicator and assist traders in exploring the market mode (buyers/sellers - bullish/bearish) and align trades to it.

* Because D_VESPA is a volume indicator, it can't be used alone to generate a trading signal - and needs to be combined with other indicators that analysis price value (range), momentum and trend. I recommend to at least combine D_VESPA with a variant of MACD and RSI to get a full view of the price action relative to the prevailing market and the broader trend.

* I found it very useful to take note and "read" how the Est Buy vs Est Sell lines move .. they sort of "tell a story" - experiment with this on your various chart and note the levels of estimate avg demand vs estimate avg supply that this indicator exposes for some very valuable insight about how the chart action is progressing. Please feel free to share feedback below.

Simple RangeThe daily price range is a good proxy to judge an instrument’s volatility. I have combined multiple concepts in this indicator to display information regarding the daily price range & its volatility.

A trading period's range is simply the difference between its high and the low. This script shows the daily high-to-low range of the price as a column chart. It has 3 main components:

1. Narrow-range days (NR7) & Wide-range Days (WR20) - as plot columns

Original concept from Thomas Bulkowski

Modified from "NR4 & NR7 Indicator" script by theapextrader7

Modified from "WR - BC Identifier" script by wrpteam2020

Narrow range days mark price contractions that often precede price expansions. This script uses NR7 (narrow range 7) as a narrow-range day. This value can be changed by the user if, instead of an NR7, he or she wishes to use NR4 or NR21, or any other interval of his or her choice. NR7 is an indecisive trading day in which the range is narrower than any of the previous six days (a total of 7 days). This is a popular concept given by Thomas Bulkowski. A breakout is said to occur when price closes above the top or below the bottom of the NR7. Upside breakout of an NR 7 candle with high volumes indicates bullishness.

Similarly, highs & lows of wide-range bars (on big volumes) are also significant reference levels for price. Wide-range candle are identified by size of the body candle (open - close). The script compares the size of previous 20 candles to identify WR20 candles. This value can also be changed by the user.

The script shows NR7 & WR20 as orange & blue bars, respectively.

The user can also turn on the option to identify a big high-to-low range candle greater than a pre-defined threshold (default is 5%). These show up as green or red bars.

2. TTM Squeeze - as background

Original concept from John Carter's book "Mastering the Trade"

Based on "Squeeze Momentum Indicator" script by LazyBear

John Carter’s TTM Squeeze indicator looks at the relationship between Bollinger Bands and Keltner's Channels to help identify period of volatility contractions. Bollinger Bands being completely enclosed within the Keltner Channels is indicative of a very low volatility. This is a state of volatility contraction known as squeeze. Using different ATR lengths (1.0, 1.5 and 2.0) for Keltner Channels, we can differentiate between levels of squeeze (High, Mid & Low compression, respectively). Greater the compression, higher the potential for explosive moves.

In the script, the High, Mid & Low compression squeezes are depicted via the background color being red, orange, or yellow, respectively.

3. Average Daily Range - as table

Original idea by alpine_trader

Modified from "ADR% - Average Daily Range % by MikeC" script by TheScrutiniser

Average Day Range (ADR) tells how much the price moves between the high and low on a given day. This is the day Range, which is then averaged to create ADR. The script uses an average of the last 20 days to calculate the ADR. Unlike ATR (Average True Range), this excludes Gaps.

The script displays the ADR as a % value in a table.

If you want to find stocks that move a lot on an average on most days, then look for stocks that have ADR% of 5% or more.

If you prefer lower volatility stocks, focus on stocks with lower ADR% values, such as 2% or less.

How it comes together

For a bullish "momentum burst", or a velocity trade:

Select stocks with Average Day Range % (ADR) greater than 5

Identify significant reference price levels via highs & lows of WR20 bars (on big volumes)

Wait for a decent mid-to-high compression squeeze

Look for clusters of NR7 candles in the consolidation

Any breakout from this consolidation should be accompanied by more than average (preferably pocket pivot) volumes

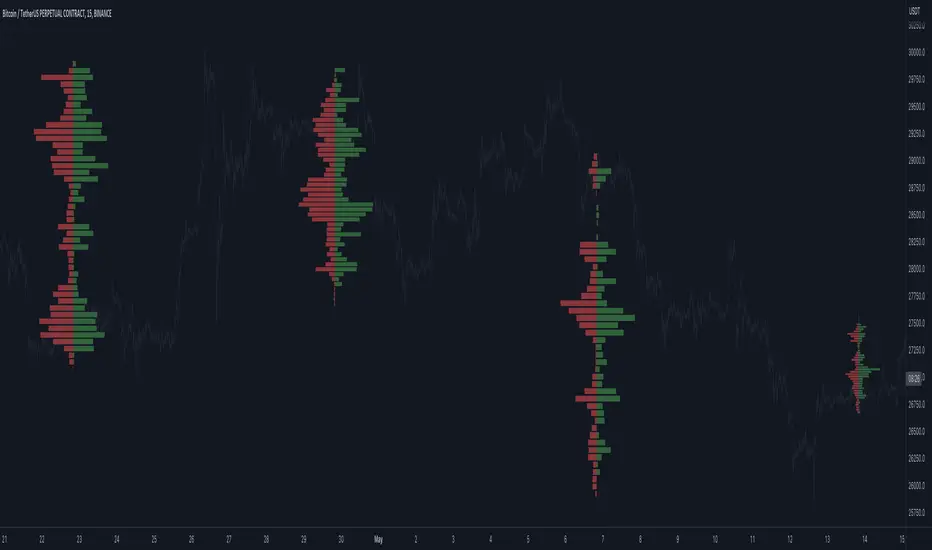

Open Interest Profile (OI)- By LeviathanThis script implements the concept of Open Interest Profile, which can help you analyze the activity of traders and identify the price levels where they are opening/closing their positions. This data can serve as a confluence for finding the areas of support and resistance , targets and placing stop losses. OI profiles can be viewed in the ranges of days, weeks, months, Tokyo sessions, London sessions and New York sessions.

A short introduction to Open Interest

Open Interest is a metric that measures the total amount of open derivatives contracts in a specific market at a given time. A valid contract is formed by both a buyer who opens a long position and a seller who opens a short position. This means that OI represents the total value of all open longs and all open shorts, divided by two. For example, if Open Interest is showing a value of $1B, it means that there is $1B worth of long and $1B worth of short contracts currently open/unsettled in a given market.

OI increasing = new long and short contracts are entering the market

OI decreasing = long and short contracts are exiting the market

OI unchanged = the net amount of positions remains the same (no new entries/exits or just a transfer of contracts occurring)

About this indicator

*This script is basically a modified version of my previous "Market Sessions and Volume Profile by @LeviathanCapital" indicator but this time, profiles are generated from Tradingview Open Interest data instead of volume (+ some other changes).

The usual representation of OI shows Open Interest value and its change based on time (for a particular day, time frame or each given candle). This indicator takes the data and plots it in a way where you can see the OI activity (change in OI) based on price levels. To put it simply, instead of observing WHEN (time) positions are entering/exiting the market, you can now see WHERE (price) positions are entering/exiting the market. This is the same concept as when it comes to Volume and Volume profile and therefore, similar strategies and ways of understanding the given data can be applied here. You can even combine the two to gain an edge (eg. high OI increase + Volume Profile showing dominant market selling = possible aggressive shorts taking place)

Green nodes = OI increase

Red nodes = OI decrease

A cluster of large green nodes can be used for support and resistance levels (*trapped traders theory) or targets (lots of liquidations and stop losses above/below), OI Profile gaps can present an objective for the price to fill them (liquidity gaps, imbalances, inefficiencies, etc), and more.

Indicator settings

1. Session/Lookback - Choose the range from where the OI Profile will be generated

2. OI Profile Mode - Mode 1 (shows only OI increase), Mode 2 (shows both OI increase and decrease), Mode 3 (shows OI decrease on left side and OI increase on the right side).

3. Show OI Value Area - Shows the area where most OI activity took place (useful as a range or S/R level )

4. Show Session Box - Shows the box around chosen sessions/lookback

5. Show Profile - Show/hide OI Profile

6. Show Current Session - Show/hide the ongoing session

7. Show Session Labels - Show/hide the text labels for each session

8. Resolution - The higher the value, the more refined a profile is, but fewer profiles are shown on the chart

9. OI Value Area % - Choose the percentage of VA (same as in Volume Profile's VA)

10. Smooth OI Data - Useful for assets that have very large spikes in OI over large bars, helps create better profiles

11. OI Increase - Pick the color of OI increase nodes in the profile

12. OI Decrease - Pick the color of OI decrease nodes in the profile

13. Value Area Box - Pick the color of the Value Area Box

14. Session Box Thickness - Pick the thickness of the lines surrounding the chosen sessions

Advice

The indicator calculates the profile based on candles - the more candles you can show, the better profile will be formed. This means that it's best to view most sessions on timeframes like 15min or lower. The only exception is the Monthly profile, where timeframes above 15min should be used. Just take a few minutes and switch between timeframes and sessions and you will figure out the optimal settings.

This is the first version of Open Interest Profile script so please understand that it will be improved in future updates.

Thank you for your support.

** Some profile generation elements are inspired by @LonesomeTheBlue's volume profile script

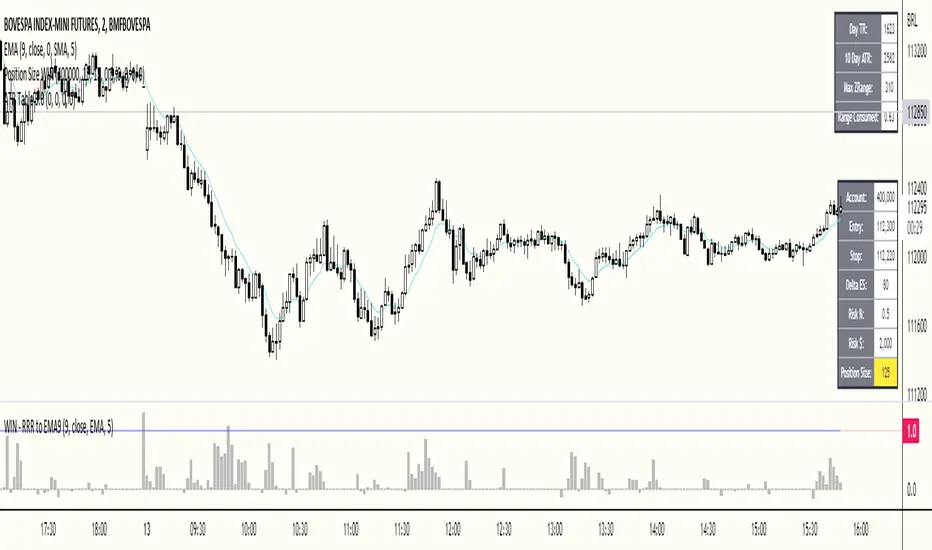

ATR Table 2.0ATR Table 2.0

This script was created in order to display a table that "calculates" how far the price can go on the current day .

The script is a table with 3 lines that calculates:

First Line - Day TR: The True Range of the current day ( - , including an Opening GAP if it exists);

Second Line - 10 Day ATR: The Average True Range of the asset (including Opening GAPs) for the last 10 days;

Third LIne - Range Consumed: How much of the 10 Day ATR it was consumed on the current day.

Example of how to use the information on the table and the understanding of it's purpose:

1) Supose you are day trading an asset that, during the last 10 days, have moved around $1.00 a day - This is the 10 Day ATR.

2) On this day, after 2 hours of the opening market, the price have already moved $0.50 (supose that it has moved $0.30 up and $0.35 down from the close of the prior day and the price is now near the close of the prior day).

3) In this situation, knowing that the price often moves around $1.00 a day, and knowing that it already moved $0.65 ($0.30 up and $0.35 down based on the close of the prior day), you may pay attention when the price breaksthrough the max or the min of the day, cause it can still move $0.35 in that direction ($1.00 - $0.65).

----------------------------------------------

ATR Table 2.0

Esse script foi criado para disponibilizar uma tabela que "calcula" quanto o preço pode andar ainda no dia em questão .

O script é uma tabela com 3 linhas que calcula:

Primeira Linha - TR do Dia: O Range Verdadeira do dia em questão ( - , incluindo GAP de Abertura se for o caso);

Segunda Linha - ATR de 10 Dias: A média do Range Verdadeira do ativo (incluindo GAPs de abertura) dos últimos 10 dias;

Terceira Linha - Range Consumido: O quanto do ATR de 10dias já foi consumido no dia em questão.

Exemplo de como usar essa informação na tabela e o entendimento do seu propósito:

1) Suponha que você está realizando day trade de um ativo que, durante os últimos 10 dias, se move em torno de $1.00 por dia. Esse é o ATR de 10 dias.

2) Nesse dia, após 2 horas da abertura do pregão, o preço já se moveu $.050 (suponhamos que ele tenha se moveu $0.30 para cima e $0.35 para baixo a partir do fechamento do dia anterior e agora o preço está próximo do fechamento do dia anterior).

3) Nessa situação, sabendo que o preço se move por volta de $1.00 por dia, e sabendo que ele já se moveu $0.65 ($0.30 pra cima e $0.35 pra baixo a partir do fechamento do dia anterior), você deve se atentar para quando o preço romper a máxima ou a mínima do dia, pois ele pode se mover ainda $.035 na direção do rompimento ($1.00 - $0.65).

Improved Chaikin Money FlowChaikin Money Flow is a well-known Indicator for gauging buying/selling pressure. Marc Chaikin intended this to be used on the daily timeframe to capture the behavior of price action at or near the daily close when larger-scale actors influence the market. The calculation is straight forward as described within the built-in TradingView "CMF" indicator:

1. Period Money Flow Multiplier = ((Close - Low) - (High - Close)) /(High - Low)

2. Period Money Flow Volume = Period Money Flow Multiplier x Volume for the Period

3. Chaikin Money Flow = 21 Period Sum of Money Flow Volume / 21 Period Sum of Volume

There is, however, a problem with this algorithm: it does not account for daily gaps in price action. This leads to the indicator sometimes moving out-of-sync with price action and/or an under-emphasis of the magnitude change of the indicator relative to the change in price action. This is a significant problem for someone trying to read divergences against an underlying.

Note: I have never seen a published attempt to improve this indicator which is why I decided that there had to be a way to do it.

In order to mitigate this issue, I have taken the basic script provided by TradingView and made a key modification. If the open of a candle is outside the range of the previous candle, then the close of the previous candle is used as the "high" for the current candle (in the case of a gap down) or the "low" for the current candle (in the case of a gap up). However, if the close of the current candle exceeds the previous close, highs and lows for the current candle are calculated as normal. I believe this accounts for gaps in price action without significantly altering the original intent of the indicator.

I have made four other minor tweaks:

1. Default style is color coded area above and below the Zero Line

2. Range scaled to +/-100 instead of +/-1 (displays better on graph)

3. Set timeframe to Daily (as that is the timeframe for which this indicator was intended by Chaikin)

4. Length defaults to 21 (which is what Chaikin uses)

MA Cross ScreenerThis script lets you pick 20 symbols to check for ma crosses. The way it works is it scans all 20 of your symbols for moving average crosses and then it sends an both a regular alert and a visual alert inside of the indicator. I found that ma cross strategies are very popular right now so I thought it would be nice to have one indicator instead of 20 discord servers. The features include: 20 custom symbols, alerts, custom colors, ma select, and custom time frames. If you want to use the custom time frame option, use the lowest time frame possible. That way you wont have gaps. If you have any comments please voice them, that includes suggestions!

I hope you all find this useful!

Bodies X Wix Version of Smart Money Tools by makuchaku & eFeThis is the same Script as Super Fair Value Gaps / FVG /BoS / by makuchaku & eFe. Mine Should Default to Large Text instead of small. The Super Order Blocks I believe was meant to for you to find one of the many Smart Money tools such as turn on the Fair Value gap but leave the others off, or Turn on where the Break of Structure and leave the others off. The reason I believe this is because the default values for each of the structures were default colored (green for positive and red for negative) for all.

Mine has a different Color for every possible structure. As long as you can read with the larger text that I added, then you can create your own boxes positive for break of structure, rejection block, order blocks and fair value gaps for any time frame. The reason I did that is because There's only certain things I believe I will need to mark for myself in each time frame, and then from there You can stretch iyour own box out further in time because if price touches a fair value gap for example, the fair value gap should conyinue in time until at least 2 candles have filed the Fair valu gap going both directions. That's truly when the fair value gap should is mitigated and will from off the chart. However, If I knew How to add the code for that, I would.

Additionally, I have the Max Boxes per chart, so you should have the ability to see every OB, FVG,RJB, & BoS on the chart

I tried my hardest to create a colored border that was different from the box. But the way the original was coded was almost impossible to do. Because they defined each of the structures (FVG, OB, BoS, RJB) outer levels, when the outer levels connect via math in the code, then it joins all the outside lines for a rectangle. When creating a box, the coloe will always be the same as the border unfortunately. (Unless I replan this from the beginning)

I also Changed the default labels for reach structure from a hard to read gray to a white that pops out.

Also, chart indicators are a little large as well. Such as the cross, sideways cross, The green Triangle, and the white Diamond. You'll get used to it or you can change it as well.

Creating videos for students, you need something they can see.

So, I just wanted to ensure everything was a little more unique and easily usable when showing this to my students when I send them private videos for our weekly lessons. I'm trying to learn how to use the IPFS for THAT, (which i see has invaded PineScript) Hope this indicator helps.

If you're to borrow this, Just make sure you keep the authors in the name makuchaku & efe

PivotsSimply plots pivots found on any timeframe based on length specified.

Supports other timeframes, you choose to display gaps or not, with gaps on the labels may disappear so keep that in mind.

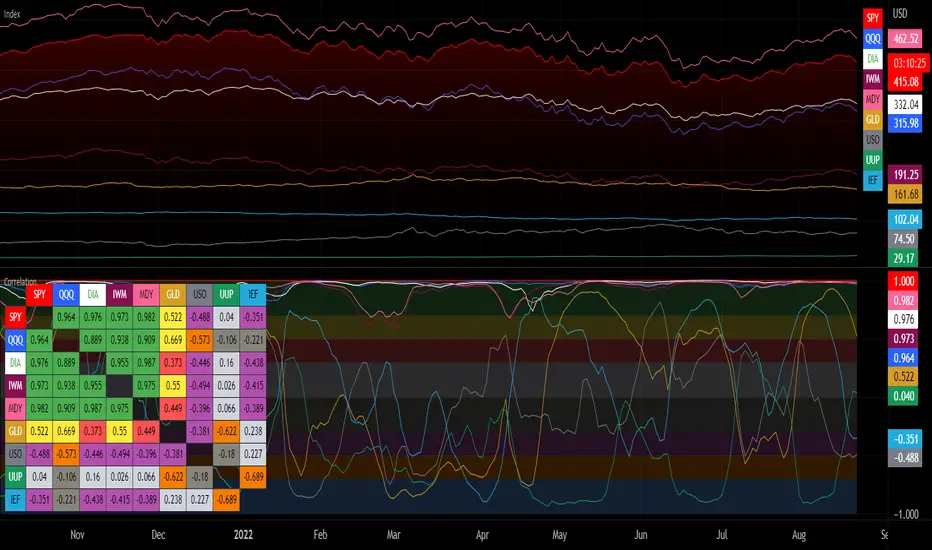

Correlation with Matrix TableCorrelation coefficient is a measure of the strength of the relationship between two values. It can be useful for market analysis, cryptocurrencies, forex and much more.

Since it "describes the degree to which two series tend to deviate from their moving average values" (1), first of all you have to set the length of these moving averages. You can also retrieve the values from another timeframe, and choose whether or not to ignore the gaps.

After selecting the reference ticker, which is not dependent from the chart you are on, you can choose up to eight other tickers to relate to it. The provided matrix table will then give you a deeper insight through all of the correlations between the chosen symbols.

Correlation values are scored on a scale from 1 to -1

A value of 1 means the correlation between the values is perfect.

A value of 0 means that there is no correlation at all.

A value of -1 indicates that the correlation is perfectly opposite.

For a better view at a glance, eight level colors are available and it is possible to modify them at will. You can even change level ranges by setting their threshold values. The background color of the matrix's cells will change accordingly to all of these choices.

The default threshold values, commonly used in statistics, are as follows:

None to weak correlation: 0 - 0.3

Weak to moderate correlation: 0.3 - 0.5

Moderate to high correlation: 0.5 - 0.7

High to perfect correlation: 0.7 - 1

Remember to be careful about spurious correlations, which are strong correlations without a real causal relationship.

(1) www.tradingview.com