Strategy Builder Pro [ChartPrime]ChartPrime Strategy Creator Overview

The ChartPrime Strategy Builder offers traders an innovative, structured approach to building and testing strategies. The Strategy Creator allows users to combine, test, and automate complex strategies with many parameters.

Key Features of the ChartPrime Strategy Builder

1. Customizable Buy and Sell Conditions

The Strategy Creator provides flexibility in establishing entry and exit rules, with separate sections for long and short strategies. Traders can combine multiple conditions in each section to fine-tune when positions are opened or closed. For instance, they might choose to only buy when the indicator signals a buy and the Dynamic Reactor (a low lag filter) indicator shows a bullish trend. Users are able to pick, mix and match the following list of features:

Signal Mode: Select the type of assistive signals you are requiring. Provided are both trend following signals with self optimization using backtest results as well as reversal signals, aiming to provide real time tops and bottoms in markets. Both these signal modes can be fine tuned using the tuning input to refine signals to a trader's liking. ChartPrime Trend Signals leverage audio engineering inspired techniques and low-pass filters in order to achieve and attempt to produce lower lag response times and therefore are designed to have a uniqueness when compared to more classical trend following approaches.

The Dynamic Reactor: provides a simple band passing through the chart. This can provide assistance in support and resistance locations as well as identifying the trend direction expressed via green and red colors. Taking a moving average and applying unique adaptivity calculations gives this plot a unique and fast behavior.

Candlestick structures: analyze candlestick formation putting a spin on classical candlestick patterns and provide the most relevant formations on the chart. These are not classical and are filtered by further analyzing market activity. A trader's classic with a spin.

The Prime Trend Assistant: provides a trend following dynamic support and resistance level. This makes it perfect to use in confluence or as a filter for other supporting indicators. This is an adaptive trend following system designed to handle volatility leveraging filter kernels as opposed to low pass filters.

Money Flow: with further filters applied for early response to money flow changes in the market. This can be a great filter in trends.

Oscillator reversals: are built in leveraging an oscillator focusing on market momentum allowing users to enter based on market shifts and trends along with reversals.

Volume-Inspired Signals: determine overbought and oversold conditions, adding another layer of analysis to the oscillator. These appear as orange labels, providing a simple reading into a possible reversal.

The Volume Matrix: is a volume oscillator that shows whether money is flowing into or out of the market. Green suggests an uptrend with buyers in control, while red indicates a majority of sellers. By incorporating smoothed volume analysis, it distinguishes between bullish and bearish volumes, offering an early indication of potential trend reversals.

The True 7: is a middle-ranking system that evaluates the strength of a move and the overall trend, offering a numeric or visual representation of trend strength. It can also indicate when a trend is starting to reverse, providing leading signals for potential market shifts. Rather than using an oscillator, this offers the unique edge of falling into set categories, making understanding it simple. This can be a great confluence point when designing a strategy.

Take profits: These offer real-time suggestions from our algorithm on when it might be a good time to take profit. Using these as part of a strategy allows for great entries at bottoms and tops of trends.

Using features such as the Dynamic reactor have dual purposes. Traders can use this as both a filter and an entry condition. This allows for true interoperability when using the Strategy Builder. The above conditions are duplicated for short entries too allowing for symmetrical trading systems. By disabling all of the entry conditions on either long or short areas of the settings will create a strategy that only takes a single type of position. For example; a trader that just wants to take longs can disable all short options.

2. Layered Entries

Layered entries, a feature to enhance the uniqueness in the tool. It allows traders to average into positions as the market moves, rather than committing all capital at once. This feature is particularly useful for volatile markets where prices may fluctuate substantially. The Strategy Builder lets users adjust the number of layered entries, which can help in managing risk and optimizing entry points as well as the aggressiveness of the safety orders. With each safety order placed the system will automatically and dynamically scale into positions reducing the average entry price and hence dynamically adjust the potential take profits. Due to the potential complexities of exiting during multiple orders, a smart system is employed to automatically take profits on the layered system aiming to take profits at peaks of trends.

Users are able to override this smart TP system at the bottom of the settings instead targeting percentage profits for both short and long positions.

Entries lowering average buy price

The ability to adjust how quickly the system layers into positions can also be adjusted via the layered entries drop down between fast and slow mode where the slow mode will be more cautious when producing new orders.

3. Flexible Take Profit (TP) and Stop Loss (SL) Options

Traders can set their TP and SL levels according to various parameters, including ATR (Average True Range), risk-reward ratio, trailing stops, or specific price changes. If layered entries are active, an automatic TP method is applied by default, though traders can manually specify TP values if they prefer. This setup allows for precise control over trade exits, tailored to the strategy’s risk profile.

Provided options

The ability to use external take profits and stop losses is also provided. By loading an indicator of your choice the plots will be added to the chart. By navigating to the external sources area of the settings, users can select this plot and use it as part of a wider trading system.

Example: Let’s say a user has entries based on the inbuilt trend signals and wishes to exit whenever the RSI crosses above 70, they can add RSI to the chart, select crossing up and enter the value of 70.

4. Integrated Reinvestment for Compounding Gains

The reinvestment option allows traders to reinvest a portion of their gains into future trades, increasing trade size over time and benefiting from compounding. For example, a user might set 30% of each trade's profit to reinvest, with the remaining 70% allocated for risk management or additional safety orders. This approach can enhance long-term growth while balancing risk.

Generally in trading it can be a good approach to take profits so we suggest a healthy balance. This setting is generally best used for slow steady strategies with the long term aim of accumulating as much of the asset as possible.

5. Leverage and Position Sizing

Users can configure leverage and position sizing to simulate varying risk levels and capital allocations. A dashboard on the interface displays margin requirements based on the selected leverage, allowing traders to estimate trade sizes relative to their available capital. Whenever using leverage especially with layered entries it’s important to keep a close eye on the position sizes to avoid potential liquidations.

6. Pre-Configured Strategies for Immediate Testing

For users seeking a starting point, ChartPrime includes a range of preset strategies. These were developed and backtested by ChartPrime’s team. This allows traders to start with a stable base and adapt it to their own preferences. It is vital to understand that historical performance doesn't guarantee future success, and traders should be mindful of overfitting. These pre-built configurations offer a structured way and base to design strategies off of. These are also subject to changing results as new price action arrives and they become outdated. They serve the purpose of simply being example use cases.

7. In-Depth Specific Backtesting Ranges

The Strategy Builder includes backtesting capabilities, providing a clear view of how different setups would have performed over specified time periods. Traders can select date ranges to target specific market conditions, then review results on TradingView to see how their strategies perform across different market trends.

Example Use Case: Developing a Strategy

Consider a trader who is focused on long positions only and prefers a lower-risk strategy (note these tools can be used for all assets; we are using an undisclosed asset as an example). Using the Strategy Builder, they could:

- Disable short conditions.

- Set long entry rules to trigger when both the ChartPrime oscillator and Quantum Reactor indicators show bullish signals.

- Enable layered entries to improve average entry prices by adding to positions during market dips.

- Run a backtest over a two-year period to see historical performance trends, making adjustments as needed.

The backtest will show where entries and exits would have occurred and how layered entries may have impacted profitability.

8. Iterative design

Strategy builders and creating a strategy is often an iterative process. By experimenting and using logic; a trader can arrive at a more sustainable system. Analyzing the shortcomings of your strategy and iteratively designing and filtering them out is the goal. For example; let’s say a strategy has high drawdown, a user would want to tighten stop losses for example to reduce this and find a balance point between optimizing winning trades and reducing the drawdown. When designing a strategy there are generally tradeoffs and optimizing taking into consideration a wide range of factors is key. This also applies to filtering techniques, entries and exits and every variable in the strategy.

Let’s say a strategy was taking too many long positions in a downtrend and after you’ve analyzed the data, you come to the conclusion this needs to be solved. Filtering these using built in trend following tools can be a great approach and refining with logic is a great approach.

The Strategy Builder also takes into consideration those who seek to automate especially via reinvesting and leverage features.

Considerations

The ChartPrime Strategy Builder aims to help traders build clear, rule-based strategies without excessive complexity. As with all backtesting tools, it's crucial to understand that historical performance doesn't guarantee future success, and traders should be mindful of overfitting. This tool offers a structured way to test strategies against various market conditions, helping traders refine their approaches with data-driven insights. Traders should also ensure they enter the correct fees when designing strategies and ensure usage on standard candle types.

Cerca negli script per "profit"

Titan Investments|Quantitative THEMIS|Pro|BINANCE:BTCUSDTP:4hInvestment Strategy (Quantitative Trading)

| 🛑 | Watch "LIVE" and 'COPY' this strategy in real time:

🔗 Link: www.tradingview.com

Hello, welcome, feel free 🌹💐

Since the stone age to the most technological age, one thing has not changed, that which continues impress human beings the most, is the other human being!

Deep down, it's all very simple or very complicated, depends on how you look at it.

I believe that everyone was born to do something very well in life.

But few are those who have, let's use the word 'luck' .

Few are those who have the 'luck' to discover this thing.

That is why few are happy and successful in their jobs and professions.

Thank God I had this 'luck' , and discovered what I was born to do well.

And I was born to program. 👨💻

📋 Summary : Project Titan

0️⃣ : 🦄 Project Titan

1️⃣ : ⚖️ Quantitative THEMIS

2️⃣ : 🏛️ Titan Community

3️⃣ : 👨💻 Who am I ❔

4️⃣ : ❓ What is Statistical/Probabilistic Trading ❓

5️⃣ : ❓ How Statistical/Probabilistic Trading works ❓

6️⃣ : ❓ Why use a Statistical/Probabilistic system ❓

7️⃣ : ❓ Why the human brain is not prepared to do Trading ❓

8️⃣ : ❓ What is Backtest ❓

9️⃣ : ❓ How to build a Consistent system ❓

🔟 : ❓ What is a Quantitative Trading system ❓

1️⃣1️⃣ : ❓ How to build a Quantitative Trading system ❓

1️⃣2️⃣ : ❓ How to Exploit Market Anomalies ❓

1️⃣3️⃣ : ❓ What Defines a Robust, Profitable and Consistent System ❓

1️⃣4️⃣ : 🔧 Fixed Technical

1️⃣5️⃣ : ❌ Fixed Outputs : 🎯 TP(%) & 🛑SL(%)

1️⃣6️⃣ : ⚠️ Risk Profile

1️⃣7️⃣ : ⭕ Moving Exits : (Indicators)

1️⃣8️⃣ : 💸 Initial Capital

1️⃣9️⃣ : ⚙️ Entry Options

2️⃣0️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Third-Party Services'

2️⃣1️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Exchanges

2️⃣2️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Messaging Services'

2️⃣3️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : '🧲🤖Copy-Trading'

2️⃣4️⃣ : ❔ Why be a Titan Pro 👽❔

2️⃣5️⃣ : ❔ Why be a Titan Aff 🛸❔

2️⃣6️⃣ : 📋 Summary : ⚖️ Strategy: Titan Investments|Quantitative THEMIS|Pro|BINANCE:BTCUSDTP:4h

2️⃣7️⃣ : 📊 PERFORMANCE : 🆑 Conservative

2️⃣8️⃣ : 📊 PERFORMANCE : Ⓜ️ Moderate

2️⃣9️⃣ : 📊 PERFORMANCE : 🅰 Aggressive

3️⃣0️⃣ : 🛠️ Roadmap

3️⃣1️⃣ : 🧻 Notes ❕

3️⃣2️⃣ : 🚨 Disclaimer ❕❗

3️⃣3️⃣ : ♻️ ® No Repaint

3️⃣4️⃣ : 🔒 Copyright ©️

3️⃣5️⃣ : 👏 Acknowledgments

3️⃣6️⃣ : 👮 House Rules : 📺 TradingView

3️⃣7️⃣ : 🏛️ Become a Titan Pro member 👽

3️⃣8️⃣ : 🏛️ Be a member Titan Aff 🛸

0️⃣ : 🦄 Project Titan

This is the first real, 100% automated Quantitative Strategy made available to the public and the pinescript community for TradingView.

You will be able to automate all signals of this strategy for your broker , centralized or decentralized and also for messaging services : Discord, Telegram or Twitter .

This is the first strategy of a larger project, in 2023, I will provide a total of 6 100% automated 'Quantitative' strategies to the pinescript community for TradingView.

The future strategies to be shared here will also be unique , never before seen, real 'Quantitative' bots with real, validated results in real operation.

Just like the 'Quantitative THEMIS' strategy, it will be something out of the loop throughout the pinescript/tradingview community, truly unique tools for building mutual wealth consistently and continuously for our community.

1️⃣ : ⚖️ Quantitative THEMIS : Titan Investments|Quantitative THEMIS|Pro|BINANCE:BTCUSDTP:4h

This is a truly unique and out of the curve strategy for BTC /USD .

A truly real strategy, with real, validated results and in real operation.

A unique tool for building mutual wealth, consistently and continuously for the members of the Titan community.

Initially we will operate on a monthly, quarterly, annual or biennial subscription service.

Our goal here is to build a great community, in exchange for an extremely fair value for the use of our truly unique tools, which bring and will bring real results to our community members.

With this business model it will be possible to provide all Titan users and community members with the purest and highest degree of sophistication in the market with pinescript for tradingview, providing unique and truly profitable strategies.

My goal here is to offer the best to our members!

The best 'pinescript' tradingview service in the world!

We are the only Start-Up in the world that will decentralize real and full access to truly real 'quantitative' tools that bring and will bring real results for mutual and ongoing wealth building for our community.

2️⃣ : 🏛️ Titan Community : 👽 Pro 🔁 Aff 🛸

Become a Titan Pro 👽

To get access to the strategy: "Quantitative THEMIS" , and future Titan strategies in a 100% automated way, along with all tutorials for automation.

Pro Plans: 30 Days, 90 Days, 12 Months, 24 Months.

👽 Pro 🅼 Monthly

👽 Pro 🆀 Quarterly

👽 Pro🅰 Annual

👽 Pro👾Two Years

You will have access to a truly unique system that is out of the curve .

A 100% real, 100% automated, tested, validated, profitable, and in real operation strategy.

Become a Titan Affiliate 🛸

By becoming a Titan Affiliate 🛸, you will automatically receive 50% of the value of each new subscription you refer .

You will receive 50% for any of the above plans that you refer .

This way we will encourage our community to grow in a fair and healthy way, because we know what we have in our hands and what we deliver real value to our users.

We are at the highest level of sophistication in the market, the consistency here and the results here speak for themselves.

So growing our community means growing mutual wealth and raising collective conscience.

Wealth must be created not divided.

And here we are creating mutual wealth on all ends and in all ways.

A non-zero sum system, where everybody wins.

3️⃣ : 👨💻 Who am I ❔

My name is FilipeSoh I am 26 years old, Technical Analyst, Trader, Computer Engineer, pinescript Specialist, with extensive experience in several languages and technologies.

For the last 4 years I have been focusing on developing, editing and creating pinescript indicators and strategies for Tradingview for people and myself.

Full-time passionate workaholic pinescript developer with over 10,000 hours of pinescript development.

• Pinescript expert ▬Tradingview.

• Specialist in Automated Trading

• Specialist in Quantitative Trading.

• Statistical/Probabilistic Trading Specialist - Mark Douglas Scholl.

• Inventor of the 'Classic Forecast' Indicators.

• Inventor of the 'Backtest Table'.

4️⃣ : ❓ What is Statistical/Probabilistic Trading ❓

Statistical/probabilistic trading is the only way to get a positive mathematical expectation regarding the market and consequently that is the only way to make money consistently from it.

I will present below some more details about the Quantitative THEMIS strategy, it is a real strategy, tested, validated and in real operation, 'Skin in the Game' , a consistent way to make money with statistical/probabilistic trading in a 100% automated.

I am a Technical Analyst , I used to be a Discretionary Trader , today I am 100% a Statistical Trader .

I've gotten rich and made a lot of money, and I've also lost a lot with 'leverage'.

That was a few years ago.

The book that changed everything for me was "Trading in The Zone" by Mark Douglas.

That's when I understood that the market is just a game of statistics and probability, like a casino!

It was then that I understood that the human brain is not prepared for trading, because it involves triggers and mental emotions.

And emotions in trading and in making trading decisions do not go well together, not in the long run, because you always have the burden of being wrong with the outcome of that particular position.

But remembering that the market is just a statistical game!

5️⃣ : ❓ How Statistical/Probabilistic Trading works ❓

Let's use a 'coin' as an example:

If we toss a 'coin' up 10 times.

Do you agree that it is impossible for us to know exactly the result of the 'plays' before they actually happen?

As in the example above, would you agree, that we cannot "guess" the outcome of a position before it actually happens?

As much as we cannot "guess" whether the coin will drop heads or tails on each flip.

We can analyze the "backtest" of the 10 moves made with that coin:

If we analyze the 10 moves and count the number of times the coin fell heads or tails in a specific sequence, we then have a percentage of times the coin fell heads or tails, so we have a 'backtest' of those moves.

Then on the next flip we can now assume a point or a favorable position for one side, the side with the highest probability .

In a nutshell, this is more or less how probabilistic statistical trading works.

As Statistical Traders we can never say whether such a Trader/Position we take will be a winner or a loser.

But still we can have a positive and consistent result in a "sequence" of trades, because before we even open a position, backtests have already been performed so we identify an anomaly and build a system that will have a positive statistical advantage in our favor over the market.

The advantage will not be in one trade itself, but in the "sequence" of trades as a whole!

Because our system will work like a casino, having a positive mathematical expectation relative to the players/market.

Design, develop, test models and systems that can take advantage of market anomalies, until they change.

Be the casino! - Mark Douglas

6️⃣ : ❓ Why use a Statistical/Probabilistic system ❓

In recent years I have focused and specialized in developing 100% automated trading systems, essentially for the cryptocurrency market.

I have developed many extremely robust and efficient systems, with positive mathematical expectation towards the market.

These are not complex systems per se , because here we want to avoid 'over-optimization' as much as possible.

As Da Vinci said: "Simplicity is the highest degree of sophistication".

I say this because I have tested, tried and developed hundreds of systems/strategies.

I believe I have programmed more than 10,000 unique indicators/strategies, because this is my passion and purpose in life.

I am passionate about what I do, completely!

I love statistical trading because it is the only way to get consistency in the long run!

This is why I have studied, applied, developed, and specialized in 100% automated cryptocurrency trading systems.

The reason why our systems are extremely "simple" is because, as I mentioned before, in statistical trading we want to exploit the market anomaly to the maximum, that is, this anomaly will change from time to time, usually we can exploit a trading system efficiently for about 6 to 12 months, or for a few years, that is; for fixed 'scalpers' systems.

Because at some point these anomalies will be identified , and from the moment they are identified they will be exploited and will stop being anomalies .

With the system presented here; you can even copy the indicators and input values shared here;

However; what I have to offer you is: it is me , our team , and our community !

That is, we will constantly monitor this system, for life , because our goal here is to create a unique , perpetual , profitable , and consistent system for our community.

Myself , our team and our community will keep this script periodically updated , to ensure the positive mathematical expectation of it.

So we don't mind sharing the current parameters and values , because the real value is also in the future updates that this system will receive from me and our team , guided by our culture and our community of real users !

As we are hosted on 'tradingview', all future updates for this strategy, will be implemented and updated automatically on your tradingview account.

What we want here is: to make sure you get gains from our system, because if you get gains , our ecosystem will grow as a whole in a healthy and scalable way, so we will be generating continuous mutual wealth and raising the collective consciousness .

People Need People: 3️⃣🅿

7️⃣ : ❓ Why the human brain is not prepared to do Trading ❓

Today my greatest skill is to develop statistically profitable and 100% automated strategies for 'pinescript' tradingview.

Note that I said: 'profitable' because in fact statistical trading is the only way to make money in a 'consistent' way from the market.

And consequently have a positive wealth curve every cycle, because we will be based on mathematics, not on feelings and news.

Because the human brain is not prepared to do trading.

Because trading is connected to the decision making of the cerebral cortex.

And the decision making is automatically linked to emotions, and emotions don't match with trading decision making, because in those moments, we can feel the best and also the worst sensations and emotions, and this certainly affects us and makes us commit grotesque mistakes!

That's why the human brain is not prepared to do trading.

If you want to participate in a fully automated, profitable and consistent trading system; be a Titan Pro 👽

I believe we are walking an extremely enriching path here, not only in terms of financial returns for our community, but also in terms of knowledge about probabilistic and automated statistical trading.

You will have access to an extremely robust system, which was built upon very strong concepts and foundations, and upon the world's main asset in a few years: Bitcoin .

We are the tip of the best that exists in the cryptocurrency market when it comes to probabilistic and automated statistical trading.

Result is result! Me being dressed or naked.

This is just the beginning!

But there is a way to consistently make money from the market.

Being the Casino! - Mark Douglas

8️⃣ : ❓ What is Backtest ❓

Imagine the market as a purely random system, but even in 'randomness' there are patterns.

So now imagine the market and statistical trading as follows:

Repeating the above 'coin' example, let's think of it as follows:

If we toss a coin up 10 times again.

It is impossible to know which flips will have heads or tails, correct?

But if we analyze these 10 tosses, then we will have a mathematical statistic of the past result, for example, 70 % of the tosses fell 'heads'.

That is:

7 moves fell on "heads" .

3 moves fell on "tails" .

So based on these conditions and on the generic backtest presented here, we could adopt " heads " as our system of moves, to have a statistical and probabilistic advantage in relation to the next move to be performed.

That is, if you define a system, based on backtests , that has a robust positive mathematical expectation in relation to the market you will have a profitable system.

For every move you make you will have a positive statistical advantage in your favor over the market before you even make the move.

Like a casino in relation to all its players!

The casino does not have an advantage over one specific player, but over all players, because it has a positive mathematical expectation about all the moves that night.

The casino will always have a positive statistical advantage over its players.

Note that there will always be real players who will make real, million-dollar bankrolls that night, but this condition is already built into the casino's 'strategy', which has a pre-determined positive statistical advantage of that night as a whole.

Statistical trading is the same thing, as long as you don't understand this you will keep losing money and consistently.

9️⃣ : ❓ How to build a Consistent system ❓

See most traders around the world perform trades believing that that specific position taken will make them filthy rich, because they simply believe faithfully that the position taken will be an undoubted winner, based on a trader's methodology: 'trading a trade' without analyzing the whole context, just using 'empirical' aspects in their system.

But if you think of trading, as a sequence of moves.

You see, 'a sequence' !

When we think statistically, it doesn't matter your result for this , or for the next specific trade , but the final sequence of trades as a whole.

As the market has a random system of results distribution , if your system has a positive statistical advantage in relation to the market, at the end of that sequence you'll have the biggest probability of having a winning bank.

That's how you do real trading!

And with consistency!

Trading is a long term game, but when you change the key you realize that it is a simple game to make money in a consistent way from the market, all you need is patience.

Even more when we are based on Bitcoin, which has its 'Halving' effect where, in theory, we will never lose money in 3 to 4 years intervals, due to its scarcity and the fact that Bitcoin is the 'discovery of digital scarcity' which makes it the digital gold, we believe in this thesis and we follow Satoshi's legacy.

So align Bitcoin with a probabilistic statistical trading system with a positive mathematical expectation of the market and 100% automated with the long term, and all you need is patience, and you will become rich.

In fact Bitcoin by itself is already a path, buy, wait for each halving and your wealth will be maintained.

No inflation, unlike fiat currencies.

This is a complete and extremely robust strategy, with the most current possible and 'not possible' techniques involved and applied here.

Today I am at another level in developing 100% automated 'quantitative' strategies.

I was born for this!

🔟 : ❓ What is a Quantitative Trading system ❓

In addition to having access to a revolutionary strategy you will have access to disruptive 100% multifunctional tables with the ability to perform 'backtests' for better tracking and monitoring of your system on a customized basis.

I would like to emphasize one thing, and that is that you keep this in mind.

Today my greatest skill in 'pinescript' is to build indicators, but mainly strategies, based on statistical and probabilistic trading, with a postive mathematical expectation in relation to the market, in a 100% automated way.

This with the goal of building a consistent and continuous positive equity curve through mathematics using data, converting it into statistical / probabilistic parameters and applying them to a Quantitative model.

Before becoming a Quantitative Trader , I was a Technical Analyst and a Discretionary Trader .

First as a position trader and then as a day trader.

Before becoming a Trader, I trained myself as a Technical Analyst , to masterly understand the shape and workings of the market in theory.

But everything changed when I met 'Mark Douglas' , when I got to know his works, that's when my head exploded 🤯, and I started to understand the market for good!

The market is nothing more than a 'random' system of distributing results.

See that I said: 'random' .

Do yourself a mental exercise.

Is there really such a thing as random ?

I believe not, as far as we know maybe the 'singularity'.

So thinking this way, to translate, the market is nothing more than a game of probability, statistics and pure mathematics.

Like a casino!

What happens is that most traders, whenever they take a position, take it with all the empirical certainty that such position will win or lose, and do not take into consideration the total sequence of results to understand their place in the market.

Understanding your place in the market gives you the ability to create and design systems that can exploit the present market anomaly, and thus make money statistically, consistently, and 100% automated.

Thinking of it this way, it is easy to make money from the market.

There are many ways to make money from the market, but the only consistent way I know of is through 'probabilistic and automated statistical trading'.

1️⃣1️⃣ : ❓ How to build a Quantitative Trading system ❓

There are some fundamental points that must be addressed here in order to understand what makes up a system based on statistics and probability applied to a quantitative model.

When we talk about 'discretionary' trading, it is a trading system based on human decisions after the defined 'empirical' conditions are met.

It is quite another thing to build a fully automated system without any human interference/interaction .

That said:

Building a statistically profitable system is perfectly possible, but this is a high level task , but with possible high rewards and consistent gains.

Here you will find a real "Skin In The Game" strategy.

With all due respect, but the vast majority of traders who post strategies on TradingView do not understand what they are doing.

Most of them do not understand the minimum complexity involved in the main variable for the construction of a real strategy, the mother variable: "strategy".

I say this by my own experience, because I have analyzed practically all the existing publications of TradingView + 200,000 indicators and strategies.

I breathe pinescript, I eat pinescript, I sleep pinescript, I bathe pinescript, I live TradingView.

But the main advantage for the TradingView users, is that all entry and exit orders made by this strategy can be checked and analyzed thoroughly, to validate and prove the veracity of this strategy, because this is a 100% real strategy.

Here there is a huge world of possibilities, but only one way to build a 'pinescript strategy' that will work correctly aligned to the real world with real results .

There are some fundamental points to take into consideration when building a profitable trading system:

The most important of these for me is: 'DrawDown' .

Followed by: 'Hit Rate' .

And only after that we use the parameter: 'Profit'.

See, this is because here, we are dealing with the 'imponderable' , and anything can happen in this scenario.

But there is one thing that makes us sleep peacefully at night, and that is: controlling losses .

That is, in other words: controlling the DrawDown .

The amateur is concerned with 'winning', the professional is concerned with conserving capital.

If we have the losses under control, then we can move on to the other two parameters: hit rate and profit.

See, the second most important factor in building a system is the hit rate.

I say this from my own experience.

I have worked with many systems with a 'low hit rate', but extremely profitable.

For example: systems with hit rates of 40 to 50%.

But as much as statistically and mathematically the profit is rewarding, operating systems with a low hit rate is always very stressful psychologically.

That's why there are two big reasons why when I build an automated trading system, I focus on the high hit rate of the system, they are

1 - To reduce psychological damage as much as possible .

2 - And more important , when we create a system with a 'high hit rate' , there is a huge intrinsic advantage here, that most statistic traders don't take in consideration.

That is: knowing more quickly when the system stops being functional.

The main advantage of a system with a high hit rate is: to identify when the system stops being functional and stop exploiting the market's anomaly.

Look: When we are talking about trading and random distribution of results on the market, do you agree that when we create a trading system, we are focused on exploring some anomaly of that market?

When that anomaly is verified by the market, it will stop being functional with time.

That's why trading systems, 'scalpers', especially for cryptocurrencies, need constant monitoring, quarterly, semi-annually or annually.

Because market movements change from time to time.

Because we go through different cycles from time to time, such as congestion cycles, accumulation , distribution , volatility , uptrends and downtrends .

1️⃣2️⃣ : ❓ How to Exploit Market Anomalies ❓

You see there is a very important point that must be stressed here.

As we are always trying to exploit an 'anomaly' in the market.

So the 'number' of indicators/tools that will integrate the system is of paramount importance.

But most traders do not take this into consideration.

To build a professional, robust, consistent, and profitable system, you don't need to use hundreds of indicators to build your setup.

This will actually make it harder to read when the setup stops working and needs some adjustment.

So focusing on a high hit rate is very important here, this is a fundamental principle that is widely ignored , and with a high hit rate, we can know much more accurately when the system is no longer functional much faster.

As Darwin said: "It is not the strongest or the most intelligent that wins the game of life, it is the most adapted.

So simple systems, as contradictory as it may seem, are more efficient, because they help to identify inflection points in the market much more quickly.

1️⃣3️⃣ : ❓ What Defines a Robust, Profitable and Consistent System ❓

See I have built, hundreds of thousands of indicators and 'pinescript' strategies, hundreds of thousands.

This is an extremely professional, robust and profitable system.

Based on the currency pairs: BTC /USDT

There are many ways and avenues to build a profitable trading setup/system.

And actually this is not a difficult task, taking in consideration, as the main factor here, that our trading and investment plan is for the long term, so consequently we will face scenarios with less noise.

He who is in a hurry eats raw.

As mentioned before.

Defining trends in pinescript is technically a simple task, the hardest task is to determine congestion zones with low volume and volatility, it's in these moments that many false signals are generated, and consequently is where most setups face their maximum DrawDown.

That's why this strategy was strictly and thoroughly planned, built on a very solid foundation, to avoid as much noise as possible, for a positive and consistent equity curve in each market cycle, 'Consistency' is our 'Mantra' around here.

1️⃣4️⃣ : 🔧 Fixed Technical

• Strategy: Titan Investments|Quantitative THEMIS|Pro|BINANCE:BTCUSDTP:4h

• Pair: BTC/USDTP

• Time Frame: 4 hours

• Broker: Binance (Recommended)

For a more conservative scenario, we have built the Quantitative THEMIS for the 4h time frame, with the main focus on consistency.

So we can avoid noise as much as possible!

1️⃣5️⃣ : ❌ Fixed Outputs : 🎯 TP(%) & 🛑SL(%)

In order to build a 'perpetual' system specific to BTC/USDT, it took a lot of testing, and more testing, and a lot of investment and research.

There is one initial and fundamental point that we can address to justify the incredible consistency presented here.

That fundamental point is our exit via Take Profit or Stop Loss percentage (%).

🎯 Take Profit (%)

🛑 Stop Loss (%)

See, today I have been testing some more advanced backtesting models for some cryptocurrency systems.

In which I perform 'backtest of backtest', i.e. we use a set of strategies each focused on a principle, operating individually, but they are part of something unique, i.e. we do 'backtests' of 'backtests' together.

What I mean is that we do a lot of backtesting around here.

I can assure you, that always the best output for a trading system is to set fixed output values!

In other words:

🎯 Take Profit (%)

🛑 Stop Loss (%)

This happens because statistically setting fixed exit structures in the vast majority of times, presents a superior result on the capital/equity curve, throughout history and for the vast majority of setups compared to other exit methods.

This is due to a mathematical principle of simplicity, 'avoiding more noise'.

Thus whenever the Quantitative THEMIS strategy takes a position it has a target and a defined maximum stop percentage.

1️⃣6️⃣ : ⚠️ Risk Profile

The strategy, currently has 3 risk profiles ⚠️ patterns for 'fixed percentage exits': Take Profit (%) and Stop Loss (%) .

They are: ⚠️ Rich's Profiles

✔️🆑 Conservative: 🎯 TP=2.7 % 🛑 SL=2.7 %

❌Ⓜ️ Moderate: 🎯 TP=2.8 % 🛑 SL=2.7 %

❌🅰 Aggressive: 🎯 TP=1.6 % 🛑 SL=6.9 %

You will be able to select and switch between the above options and profiles through the 'input' menu of the strategy by navigating to the "⚠️ Risk Profile" menu.

You can then select, test and apply the Risk Profile above that best suits your risk management, expectations and reality , as well as customize all the 'fixed exit' values through the TP and SL menus below.

1️⃣7️⃣ : ⭕ Moving Exits : (Indicators)

The strategy currently also has 'Moving Exits' based on indicator signals.

These are Moving Exits (Indicators)

📈 LONG : (EXIT)

🧃 (MAO) Short : true

📉 SHORT : (EXIT)

🧃 (MAO) Long: false

You can select and toggle between the above options through the 'input' menu of the strategy by navigating to the "LONG : Exit" and "SHORT : Exit" menu.

1️⃣8️⃣ : 💸 Initial Capital

By default the "Initial Capital" set for entries and backtests of this strategy is: 10000 $

You can set another value for the 'Starting Capital' through the tradingview menu under "properties" , and edit the value of the "Initial Capital" field.

This way you can set and test other 'Entry Values' for your trades, tests and backtests.

1️⃣9️⃣ : ⚙️ Entry Options

By default the 'order size' set for this strategy is 100 % of the 'initial capital' on each new trade.

You can set and test other entry options like : contracts , cash , % of equity

You should make these changes directly in the input menu of the strategy by navigating to the menu "⚙️ Properties : TradingView" below.

⚙️ Properties : (TradingView)

📊 Strategy Type: strategy.position_size != 1

📝💲 % Order Type: % of equity

📝💲 % Order Size: 100

Leverage: 1

So you can define and test other 'Entry Options' for your trades, tests and backtests.

2️⃣0️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Third-Party Services'

It is possible to automate the signals of this strategy for any centralized or decentralized broker, as well as for messaging services: Discord, Telegram and Twitter.

All in an extremely simple and uncomplicated way through the tutorials available in PDF /VIDEO for our Titan Pro 👽 subscriber community.

With our tutorials in PDF and Video it will be possible to automate the signals of this strategy for the chosen service in an extremely simple way with less than 10 steps only.

Tradingview naturally doesn't count with native integration between brokers and tradingview.

But it is possible to use 'third party services' to do the integration and automation between Tradingview and your centralized or decentralized broker.

Here are the standard, available and recommended 'third party services' to automate the signals from the 'Quantitative THEMIS' strategy on the tradingview for your broker:

1) Wundertrading (Recommended):

2) 3commas:

3) Zignaly:

4) Aleeert.com (Recommended):

5) Alertatron:

Note! 'Third party services' cannot perform 'withdrawals' via their key 'API', they can only open positions, so your funds will always be 'safe' in your brokerage firm, being traded via the 'API', when they receive an entry and exit signal from this strategy.

2️⃣1️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Exchanges

You can automate this strategy for any of the brokers below, through your broker's 'API' by connecting it to the 'third party automation services' for tradingview available and mentioned in the menu above:

1) Binance (Recommended)

2) Bitmex

3) Bybit

4) KuCoin

5) Deribit

6) OKX

7) Coinbase

8) Huobi

9) Bitfinex

10) Bitget

11) Bittrex

12) Bitstamp

13) Gate. io

14) Kraken

15) Gemini

16) Ascendex

17) VCCE

2️⃣2️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Messaging Services'

You can also automate and monitor the signals of this strategy much more efficiently by sending them to the following popular messaging services:

1) Discord

2) Telegram

3) Twitter

2️⃣3️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : '🧲🤖Copy-Trading'

It will also be possible to copy/replicate the entries and exits of this strategy to your broker in an extremely simple and agile way, through the available copy-trader services.

This way it will be possible to replicate the signals of this strategy at each entry and exit to your broker through the API connecting it to the integrated copy-trader services available through the tradingview automation services below:

1) Wundetrading:

2) Zignaly:

2️⃣4️⃣ : ❔ Why be a Titan Pro 👽❔

I believe that today I am at another level in 'pinescript' development.

I consider myself today a true unicorn as a pinescript developer, someone unique and very rare.

If you choose another tool or another pinescript service, this tool will be just another one, with no real results.

But if you join our Titan community, you will have access to a unique tool! And you will get real results!

I already earn money consistently with statistical and automated trading and as an expert pinescript developer.

I am here to evolve my skills as much as possible, and one day become a pinescript 'Wizard'.

So excellence, quality and professionalism will always be my north here.

You will never find a developer like me, and who will take so seriously such a revolutionary project as this one. A Maverick! ▬ The man never stops!

Here you will find the highest degree of sophistication and development in the market for 'pinescript'.

You will get the best of me and the best of pinescript possible.

Let me show you how a professional in my field does it.

Become a Titan Pro Member 👽 and get Full Access to this strategy and all the Automation Tutorials.

Be the Titan in your life!

2️⃣5️⃣ : ❔ Why be a Titan Aff 🛸❔

Get financial return for your referrals, Decentralize the World, and raise the collective consciousness.

2️⃣6️⃣ : 📋 Summary : ⚖️ Strategy: Titan Investments|Quantitative THEMIS|Pro|BINANCE:BTCUSDTP:4h

® Titan Investimentos | Quantitative THEMIS ⚖️ | Pro 👽 2.6 | Dev: © FilipeSoh 🧙 | 🤖 100% Automated : Discord, Telegram, Twitter, Wundertrading, 3commas, Zignaly, Aleeert, Alertatron, Uniswap-v3 | BINANCE:BTCUSDTPERP 4h

🛒 Subscribe this strategy ❗️ Be a Titan Member 🏛️

🛒 Titan Pro 👽 🏛️ Titan Pro 👽 Version with ✔️100% Integrated Automation 🤖 and 📚 Automation Tutorials ✔️100% available at: (PDF/VIDEO)

🛒 Titan Affiliate 🛸 🏛️ Titan Affiliate 🛸 (Subscription Sale) 🔥 Receive 50% commission

📋 Summary : QT THEMIS ⚖️

🕵️♂️ Check This Strategy..................................................................0

🦄 ® Titan Investimentos...............................................................1

👨💻 © Developer..........................................................................2

📚 Signal Automation Tutorials : (PDF/VIDEO).......................................3

👨🔧 Revision...............................................................................4

📊 Table : (BACKTEST)..................................................................5

📊 Table : (INFORMATIONS).............................................................6

⚙️ Properties : (TRADINGVIEW)........................................................7

📆 Backtest : (TRADINGVIEW)..........................................................8

⚠️ Risk Profile...........................................................................9

🟢 On 🔴 Off : (LONG/SHORT).......................................................10

📈 LONG : (ENTRY)....................................................................11

📉 SHORT : (ENTRY)...................................................................12

📈 LONG : (EXIT).......................................................................13

📉 SHORT : (EXIT)......................................................................14

🧩 (EI) External Indicator.............................................................15

📡 (QT) Quantitative...................................................................16

🎠 (FF) Forecast......................................................................17

🅱 (BB) Bollinger Bands................................................................18

🧃 (MAP) Moving Average Primary......................................................19

🧃 (MAP) Labels.........................................................................20

🍔 (MAQ) Moving Average Quaternary.................................................21

🍟 (MACD) Moving Average Convergence Divergence...............................22

📣 (VWAP) Volume Weighted Average Price........................................23

🪀 (HL) HILO..........................................................................24

🅾 (OBV) On Balance Volume.........................................................25

🥊 (SAR) Stop and Reverse...........................................................26

🛡️ (DSR) Dynamic Support and Resistance..........................................27

🔊 (VD) Volume Directional..........................................................28

🧰 (RSI) Relative Momentum Index.................................................29

🎯 (TP) Take Profit %..................................................................30

🛑 (SL) Stop Loss %....................................................................31

🤖 Automation Selected...............................................................32

📱💻 Discord............................................................................33

📱💻 Telegram..........................................................................34

📱💻 Twitter...........................................................................35

🤖 Wundertrading......................................................................36

🤖 3commas............................................................................37

🤖 Zignaly...............................................................................38

🤖 Aleeert...............................................................................39

🤖 Alertatron...........................................................................40

🤖 Uniswap-v3..........................................................................41

🧲🤖 Copy-Trading....................................................................42

♻️ ® No Repaint........................................................................43

🔒 Copyright ©️..........................................................................44

🏛️ Be a Titan Member..................................................................45

Nº Active Users..........................................................................46

⏱ Time Left............................................................................47

| 0 | 🕵️♂️ Check This Strategy

🕵️♂️ Version Demo: 🐄 Version with ❌non-integrated automation 🤖 and 📚 Tutorials for automation ❌not available

🕵️♂️ Version Pro: 👽 Version with ✔️100% Integrated Automation 🤖 and 📚 Automation Tutorials ✔️100% available at: (PDF/VIDEO)

| 1 | 🦄 ® Titan Investimentos

Decentralizing the World 🗺

Raising the Collective Conscience 🗺

🦄Site:

🦄TradingView: www.tradingview.com

🦄Discord:

🦄Telegram:

🦄Youtube:

🦄Twitter:

🦄Instagram:

🦄TikTok:

🦄Linkedin:

🦄E-mail:

| 2 | 👨💻 © Developer

🧠 Developer: @FilipeSoh🧙

📺 TradingView: www.tradingview.com

☑️ Linkedin:

✅ Fiverr:

✅ Upwork:

🎥 YouTube:

🐤 Twitter:

🤳 Instagram:

| 3 | 📚 Signal Automation Tutorials : (PDF/VIDEO)

📚 Discord: 🔗 Link: 🔒Titan Pro👽

📚 Telegram: 🔗 Link: 🔒Titan Pro👽

📚 Twitter: 🔗 Link: 🔒Titan Pro👽

📚 Wundertrading: 🔗 Link: 🔒Titan Pro👽

📚 3comnas: 🔗 Link: 🔒Titan Pro👽

📚 Zignaly: 🔗 Link: 🔒Titan Pro👽

📚 Aleeert: 🔗 Link: 🔒Titan Pro👽

📚 Alertatron: 🔗 Link: 🔒Titan Pro👽

📚 Uniswap-v3: 🔗 Link: 🔒Titan Pro👽

📚 Copy-Trading: 🔗 Link: 🔒Titan Pro👽

| 4 | 👨🔧 Revision

👨🔧 Start Of Operations: 01 Jan 2019 21:00 -0300 💡 Start Of Operations (Skin in the game) : Revision 1.0

👨🔧 Previous Review: 01 Jan 2022 21:00 -0300 💡 Previous Review : Revision 2.0

👨🔧 Current Revision: 01 Jan 2023 21:00 -0300 💡 Current Revision : Revision 2.6

👨🔧 Next Revision: 28 May 2023 21:00 -0300 💡 Next Revision : Revision 2.7

| 5 | 📊 Table : (BACKTEST)

📊 Table: true

🖌️ Style: label.style_label_left

📐 Size: size_small

📏 Line: defval

🎨 Color: #131722

| 6 | 📊 Table : (INFORMATIONS)

📊 Table: false

🖌️ Style: label.style_label_right

📐 Size: size_small

📏 Line: defval

🎨 Color: #131722

| 7 | ⚙️ Properties : (TradingView)

📊 Strategy Type: strategy.position_size != 1

📝💲 % Order Type: % of equity

📝💲 % Order Size: 100 %

🚀 Leverage: 1

| 8 | 📆 Backtest : (TradingView)

🗓️ Mon: true

🗓️ Tue: true

🗓️ Wed: true

🗓️ Thu: true

🗓️ Fri: true

🗓️ Sat: true

🗓️ Sun: true

📆 Range: custom

📆 Start: UTC 31 Oct 2008 00:00

📆 End: UTC 31 Oct 2030 23:45

📆 Session: 0000-0000

📆 UTC: UTC

| 9 | ⚠️ Risk Profile

✔️🆑 Conservative: 🎯 TP=2.7 % 🛑 SL=2.7 %

❌Ⓜ️ Moderate: 🎯 TP=2.8 % 🛑 SL=2.7 %

❌🅰 Aggressive: 🎯 TP=1.6 % 🛑 SL=6.9 %

| 10 | 🟢 On 🔴 Off : (LONG/SHORT)

🟢📈 LONG: true

🟢📉 SHORT: true

| 11 | 📈 LONG : (ENTRY)

📡 (QT) Long: true

🧃 (MAP) Long: false

🅱 (BB) Long: false

🍟 (MACD) Long: false

🅾 (OBV) Long: false

| 12 | 📉 SHORT : (ENTRY)

📡 (QT) Short: true

🧃 (MAP) Short: false

🅱 (BB) Short: false

🍟 (MACD) Short: false

🅾 (OBV) Short: false

| 13 | 📈 LONG : (EXIT)

🧃 (MAP) Short: true

| 14 | 📉 SHORT : (EXIT)

🧃 (MAP) Long: false

| 15 | 🧩 (EI) External Indicator

🧩 (EI) Connect your external indicator/filter: false

🧩 (EI) Connect your indicator here (Study mode only): close

🧩 (EI) Connect your indicator here (Study mode only): close

| 16 | 📡 (QT) Quantitative

📡 (QT) Quantitative: true

📡 (QT) Market: BINANCE:BTCUSDTPERP

📡 (QT) Dice: openai

| 17 | 🎠 (FF) Forecast

🎠 (FF) Include current unclosed current candle: true

🎠 (FF) Forecast Type: flat

🎠 (FF) Nº of candles to use in linear regression: 3

| 18 | 🅱 (BB) Bollinger Bands

🅱 (BB) Bollinger Bands: true

🅱 (BB) Type: EMA

🅱 (BB) Period: 20

🅱 (BB) Source: close

🅱 (BB) Multiplier: 2

🅱 (BB) Linewidth: 0

🅱 (BB) Color: #131722

| 19 | 🧃 (MAP) Moving Average Primary

🧃 (MAP) Moving Average Primary: true

🧃 (MAP) BarColor: false

🧃 (MAP) Background: false

🧃 (MAP) Type: SMA

🧃 (MAP) Source: open

🧃 (MAP) Period: 100

🧃 (MAP) Multiplier: 2.0

🧃 (MAP) Linewidth: 2

🧃 (MAP) Color P: #42bda8

🧃 (MAP) Color N: #801922

| 20 | 🧃 (MAP) Labels

🧃 (MAP) Labels: true

🧃 (MAP) Style BUY ZONE: shape.labelup

🧃 (MAP) Color BUY ZONE: #42bda8

🧃 (MAP) Style SELL ZONE: shape.labeldown

🧃 (MAP) Color SELL ZONE: #801922

| 21 | 🍔 (MAQ) Moving Average Quaternary

🍔 (MAQ) Moving Average Quaternary: true

🍔 (MAQ) BarColor: false

🍔 (MAQ) Background: false

🍔 (MAQ) Type: SMA

🍔 (MAQ) Source: close

🍔 (MAQ) Primary: 14

🍔 (MAQ) Secondary: 22

🍔 (MAQ) Tertiary: 44

🍔 (MAQ) Quaternary: 16

🍔 (MAQ) Linewidth: 0

🍔 (MAQ) Color P: #42bda8

🍔 (MAQ) Color N: #801922

| 22 | 🍟 (MACD) Moving Average Convergence Divergence

🍟 (MACD) Macd Type: EMA

🍟 (MACD) Signal Type: EMA

🍟 (MACD) Source: close

🍟 (MACD) Fast: 12

🍟 (MACD) Slow: 26

🍟 (MACD) Smoothing: 9

| 23 | 📣 (VWAP) Volume Weighted Average Price

📣 (VWAP) Source: close

📣 (VWAP) Period: 340

📣 (VWAP) Momentum A: 84

📣 (VWAP) Momentum B: 150

📣 (VWAP) Average Volume: 1

📣 (VWAP) Multiplier: 1

📣 (VWAP) Diviser: 2

| 24 | 🪀 (HL) HILO

🪀 (HL) Type: SMA

🪀 (HL) Function: Maverick🧙

🪀 (HL) Source H: high

🪀 (HL) Source L: low

🪀 (HL) Period: 20

🪀 (HL) Momentum: 26

🪀 (HL) Diviser: 2

🪀 (HL) Multiplier: 1

| 25 | 🅾 (OBV) On Balance Volume

🅾 (OBV) Type: EMA

🅾 (OBV) Source: close

🅾 (OBV) Period: 16

🅾 (OBV) Diviser: 2

🅾 (OBV) Multiplier: 1

| 26 | 🥊 (SAR) Stop and Reverse

🥊 (SAR) Source: close

🥊 (SAR) High: 1.8

🥊 (SAR) Mid: 1.6

🥊 (SAR) Low: 1.6

🥊 (SAR) Diviser: 2

🥊 (SAR) Multiplier: 1

| 27 | 🛡️ (DSR) Dynamic Support and Resistance

🛡️ (DSR) Source D: close

🛡️ (DSR) Source R: high

🛡️ (DSR) Source S: low

🛡️ (DSR) Momentum R: 0

🛡️ (DSR) Momentum S: 2

🛡️ (DSR) Diviser: 2

🛡️ (DSR) Multiplier: 1

| 28 | 🔊 (VD) Volume Directional

🔊 (VD) Type: SMA

🔊 (VD) Period: 68

🔊 (VD) Momentum: 3.8

🔊 (VD) Diviser: 2

🔊 (VD) Multiplier: 1

| 29 | 🧰 (RSI) Relative Momentum Index

🧰 (RSI) Type UP: EMA

🧰 (RSI) Type DOWN: EMA

🧰 (RSI) Source: close

🧰 (RSI) Period: 29

🧰 (RSI) Smoothing: 22

🧰 (RSI) Momentum R: 64

🧰 (RSI) Momentum S: 142

🧰 (RSI) Diviser: 2

🧰 (RSI) Multiplier: 1

| 30 | 🎯 (TP) Take Profit %

🎯 (TP) Take Profit: false

🎯 (TP) %: 2.2

🎯 (TP) Color: #42bda8

🎯 (TP) Linewidth: 1

| 31 | 🛑 (SL) Stop Loss %

🛑 (SL) Stop Loss: false

🛑 (SL) %: 2.7

🛑 (SL) Color: #801922

🛑 (SL) Linewidth: 1

| 32 | 🤖 Automation : Discord | Telegram | Twitter | Wundertrading | 3commas | Zignaly | Aleeert | Alertatron | Uniswap-v3

🤖 Automation Selected : Discord

| 33 | 🤖 Discord

🔗 Link Discord: discord.com

🔗 Link 📚 Automation: 🔒Titan Pro👽

📱💻 Discord ▬ Enter Long: 🔒Titan Pro👽

📱💻 Discord ▬ Exit Long: 🔒Titan Pro👽

📱💻 Discord ▬ Enter Short: 🔒Titan Pro👽

📱💻 Discord ▬ Exit Short: 🔒Titan Pro👽

| 34 | 🤖 Telegram

🔗 Link Telegram: telegram.org

🔗 Link 📚 Automation: 🔒Titan Pro👽

📱💻 Telegram ▬ Enter Long: 🔒Titan Pro👽

📱💻 Telegram ▬ Exit Long: 🔒Titan Pro👽

📱💻 Telegram ▬ Enter Short: 🔒Titan Pro👽

📱💻 Telegram ▬ Exit Short: 🔒Titan Pro👽

| 35 | 🤖 Twitter

🔗 Link Twitter: twitter.com

🔗 Link 📚 Automation: 🔒Titan Pro👽

📱💻 Twitter ▬ Enter Long: 🔒Titan Pro👽

📱💻 Twitter ▬ Exit Long: 🔒Titan Pro👽

📱💻 Twitter ▬ Enter Short: 🔒Titan Pro👽

📱💻 Twitter ▬ Exit Short: 🔒Titan Pro👽

| 36 | 🤖 Wundertrading : Binance | Bitmex | Bybit | KuCoin | Deribit | OKX | Coinbase | Huobi | Bitfinex | Bitget

🔗 Link Wundertrading: wundertrading.com

🔗 Link 📚 Automation: 🔒Titan Pro👽

📱💻 Wundertrading ▬ Enter Long: 🔒Titan Pro👽

📱💻 Wundertrading ▬ Exit Long: 🔒Titan Pro👽

📱💻 Wundertrading ▬ Enter Short: 🔒Titan Pro👽

📱💻 Wundertrading ▬ Exit Short: 🔒Titan Pro👽

| 37 | 🤖 3commas : Binance | Bybit | OKX | Bitfinex | Coinbase | Deribit | Bitmex | Bittrex | Bitstamp | Gate.io | Kraken | Gemini | Huobi | KuCoin

🔗 Link 3commas: 3commas.io

🔗 Link 📚 Automation: 🔒Titan Pro👽

📱💻 3commas ▬ Enter Long: 🔒Titan Pro👽

📱💻 3commas ▬ Exit Long: 🔒Titan Pro👽

📱💻 3commas ▬ Enter Short: 🔒Titan Pro👽

📱💻 3commas ▬ Exit Short: 🔒Titan Pro👽

| 38 | 🤖 Zignaly : Binance | Ascendex | Bitmex | Kucoin | VCCE

🔗 Link Zignaly: zignaly.com

🔗 Link 📚 Automation: 🔒Titan Pro👽

🤖 Type Automation: Profit Sharing

🤖 Type Provider: Webook

🔑 Key: 🔒Titan Pro👽

🤖 pair: BTCUSDTP

🤖 exchange: binance

🤖 exchangeAccountType: futures

🤖 orderType: market

🚀 leverage: 1x

% positionSizePercentage: 100 %

💸 positionSizeQuote: 10000 $

🆔 signalId: @Signal1234

| 39 | 🤖 Aleeert : Binance

🔗 Link Aleeert: aleeert.com

🔗 Link 📚 Automation: 🔒Titan Pro👽

📱💻 Aleeert ▬ Enter Long: 🔒Titan Pro👽

📱💻 Aleeert ▬ Exit Long: 🔒Titan Pro👽

📱💻 Aleeert ▬ Enter Short: 🔒Titan Pro👽

📱💻 Aleeert ▬ Exit Short: 🔒Titan Pro👽

| 40 | 🤖 Alertatron : Binance | Bybit | Deribit | Bitmex

🔗 Link Alertatron: alertatron.com

🔗 Link 📚 Automation: 🔒Titan Pro👽

📱💻 Alertatron ▬ Enter Long: 🔒Titan Pro👽

📱💻 Alertatron ▬ Exit Long: 🔒Titan Pro👽

📱💻 Alertatron ▬ Enter Short: 🔒Titan Pro👽

📱💻 Alertatron ▬ Exit Short: 🔒Titan Pro👽

| 41 | 🤖 Uniswap-v3

🔗 Link Alertatron: uniswap.org

🔗 Link 📚 Automation: 🔒Titan Pro👽

📱💻 Uniswap-v3 ▬ Enter Long: 🔒Titan Pro👽

📱💻 Uniswap-v3 ▬ Exit Long: 🔒Titan Pro👽

📱💻 Uniswap-v3 ▬ Enter Short: 🔒Titan Pro👽

📱💻 Uniswap-v3 ▬ Exit Short: 🔒Titan Pro👽

| 42 | 🧲🤖 Copy-Trading : Zignaly | Wundertrading

🔗 Link 📚 Copy-Trading: 🔒Titan Pro👽

🧲🤖 Copy-Trading ▬ Zignaly: 🔒Titan Pro👽

🧲🤖 Copy-Trading ▬ Wundertrading: 🔒Titan Pro👽

| 43 | ♻️ ® Don't Repaint!

♻️ This Strategy does not Repaint!: ® Signs Do not repaint❕

♻️ This is a Real Strategy!: Quality : ® Titan Investimentos

📋️️ Get more information about Repainting here:

| 44 | 🔒 Copyright ©️

🔒 Copyright ©️: Copyright © 2023-2024 All rights reserved, ® Titan Investimentos

🔒 Copyright ©️: ® Titan Investimentos

🔒 Copyright ©️: Unique and Exclusive Strategy. All rights reserved

| 45 | 🏛️ Be a Titan Members

🏛️ Titan Pro 👽 Version with ✔️100% Integrated Automation 🤖 and 📚 Automation Tutorials ✔️100% available at: (PDF/VIDEO)

🏛️ Titan Affiliate 🛸 (Subscription Sale) 🔥 Receive 50% commission

| 46 | ⏱ Time Left

Time Left Titan Demo 🐄: ⏱♾ | ⏱ : ♾ Titan Demo 🐄 Version with ❌non-integrated automation 🤖 and 📚 Tutorials for automation ❌not available

Time Left Titan Pro 👽: 🔒Titan Pro👽 | ⏱ : Pro Plans: 30 Days, 90 Days, 12 Months, 24 Months. (👽 Pro 🅼 Monthly, 👽 Pro 🆀 Quarterly, 👽 Pro🅰 Annual, 👽 Pro👾Two Years)

| 47 | Nº Active Users

Nº Active Subscribers Titan Pro 👽: 5️⃣6️⃣ | 1✔️ 5✔️ 10✔️ 100❌ 1K❌ 10K❌ 50K❌ 100K❌ 1M❌ 10M❌ 100M❌ : ⏱ Active Users is updated every 24 hours (Check on indicator)

Nº Active Affiliates Titan Aff 🛸: 6️⃣ | 1✔️ 5✔️ 10❌ 100❌ 1K❌ 10K❌ 50K❌ 100K❌ 1M❌ 10M❌ 100M❌ : ⏱ Active Users is updated every 24 hours (Check on indicator)

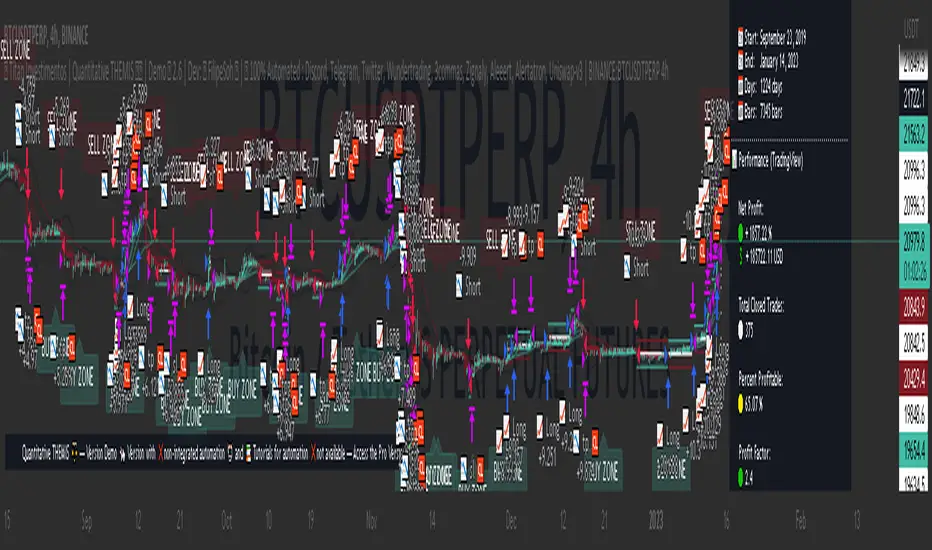

2️⃣7️⃣ : 📊 PERFORMANCE : 🆑 Conservative

📊 Exchange: Binance

📊 Pair: BINANCE: BTCUSDTPERP

📊 TimeFrame: 4h

📊 Initial Capital: 10000 $

📊 Order Type: % equity

📊 Size Per Order: 100 %

📊 Commission: 0.03 %

📊 Pyramid: 1

• ⚠️ Risk Profile: 🆑 Conservative: 🎯 TP=2.7 % | 🛑 SL=2.7 %

• 📆All years: 🆑 Conservative: 🚀 Leverage 1️⃣x

📆 Start: September 23, 2019

📆 End: January 11, 2023

📅 Days: 1221

📅 Bars: 7325

Net Profit:

🟢 + 1669.89 %

💲 + 166989.43 USD

Total Close Trades:

⚪️ 369

Percent Profitable:

🟡 64.77 %

Profit Factor:

🟢 2.314

DrawDrown Maximum:

🔴 -24.82 %

💲 -10221.43 USD

Avg Trade:

💲 + 452.55 USD

✔️ Trades Winning: 239

❌ Trades Losing: 130

✔️ Average Gross Win: + 12.31 %

❌ Average Gross Loss: - 9.78 %

✔️ Maximum Consecutive Wins: 9

❌ Maximum Consecutive Losses: 6

% Average Gain Annual: 499.33 %

% Average Gain Monthly: 41.61 %

% Average Gain Weekly: 9.6 %

% Average Gain Day: 1.37 %

💲 Average Gain Annual: 49933 $

💲 Average Gain Monthly: 4161 $

💲 Average Gain Weekly: 960 $

💲 Average Gain Day: 137 $

• 📆 Year: 2020: 🆑 Conservative: 🚀 Leverage 1️⃣x

• 📆 Year: 2021: 🆑 Conservative: 🚀 Leverage 1️⃣x

• 📆 Year: 2022: 🆑 Conservative: 🚀 Leverage 1️⃣x

2️⃣8️⃣ : 📊 PERFORMANCE : Ⓜ️ Moderate

📊 Exchange: Binance

📊 Pair: BINANCE: BTCUSDTPERP

📊 TimeFrame: 4h

📊 Initial Capital: 10000 $

📊 Order Type: % equity

📊 Size Per Order: 100 %

📊 Commission: 0.03 %

📊 Pyramid: 1

• ⚠️ Risk Profile: Ⓜ️ Moderate: 🎯 TP=2.8 % | 🛑 SL=2.7 %

• 📆 All years: Ⓜ️ Moderate: 🚀 Leverage 1️⃣x

📆 Start: September 23, 2019

📆 End: January 11, 2023

📅 Days: 1221

📅 Bars: 7325

Net Profit:

🟢 + 1472.04 %

💲 + 147199.89 USD

Total Close Trades:

⚪️ 362

Percent Profitable:

🟡 63.26 %

Profit Factor:

🟢 2.192

DrawDrown Maximum:

🔴 -22.69 %

💲 -9269.33 USD

Avg Trade:

💲 + 406.63 USD

✔️ Trades Winning: 229

❌ Trades Losing : 133

✔️ Average Gross Win: + 11.82 %

❌ Average Gross Loss: - 9.29 %

✔️ Maximum Consecutive Wins: 9

❌ Maximum Consecutive Losses: 8

% Average Gain Annual: 440.15 %

% Average Gain Monthly: 36.68 %

% Average Gain Weekly: 8.46 %

% Average Gain Day: 1.21 %

💲 Average Gain Annual: 44015 $

💲 Average Gain Monthly: 3668 $

💲 Average Gain Weekly: 846 $

💲 Average Gain Day: 121 $

• 📆 Year: 2020: Ⓜ️ Moderate: 🚀 Leverage 1️⃣x

• 📆 Year: 2021: Ⓜ️ Moderate: 🚀 Leverage 1️⃣x

• 📆 Year: 2022: Ⓜ️ Moderate: 🚀 Leverage 1️⃣x

2️⃣9️⃣ : 📊 PERFORMANCE : 🅰 Aggressive

📊 Exchange: Binance

📊 Pair: BINANCE: BTCUSDTPERP

📊 TimeFrame: 4h

📊 Initial Capital: 10000 $

📊 Order Type: % equity

📊 Size Per Order: 100 %

📊 Commission: 0.03 %

📊 Pyramid: 1

• ⚠️ Risk Profile: 🅰 Aggressive: 🎯 TP=1.6 % | 🛑 SL=6.9 %

• 📆 All years: 🅰 Aggressive: 🚀 Leverage 1️⃣x

📆 Start: September 23, 2019

📆 End: January 11, 2023

📅 Days: 1221

📅 Bars: 7325

Net Profit:

🟢 + 989.38 %

💲 + 98938.38 USD

Total Close Trades:

⚪️ 380

Percent Profitable:

🟢 84.47 %

Profit Factor:

🟢 2.156

DrawDrown Maximum:

🔴 -17.88 %

💲 -9182.84 USD

Avg Trade:

💲 + 260.36 USD

✔️ Trades Winning: 321

❌ Trades Losing: 59

✔️ Average Gross Win: + 5.75 %

❌ Average Gross Loss: - 14.51 %

✔️ Maximum Consecutive Wins: 21

❌ Maximum Consecutive Losses: 6

% Average Gain Annual: 295.84 %

% Average Gain Monthly: 24.65 %

% Average Gain Weekly: 5.69 %

% Average Gain Day: 0.81 %

💲 Average Gain Annual: 29584 $

💲 Average Gain Monthly: 2465 $

💲 Average Gain Weekly: 569 $

💲 Average Gain Day: 81 $

• 📆 Year: 2020: 🅰 Aggressive: 🚀 Leverage 1️⃣x

• 📆 Year: 2021: 🅰 Aggressive: 🚀 Leverage 1️⃣x

• 📆 Year: 2022: 🅰 Aggressive: 🚀 Leverage 1️⃣x

3️⃣0️⃣ : 🛠️ Roadmap

🛠️• 14/ 01 /2023 : Titan THEMIS Launch

🛠️• Updates January/2023 :

• 📚 Tutorials for Automation 🤖 already Available : ✔️

• ✔️ Discord

• ✔️ Wundertrading

• ✔️ Zignaly

• 📚 Tutorials for Automation 🤖 In Preparation : ⭕

• ⭕ Telegram

• ⭕ Twitter

• ⭕ 3comnas

• ⭕ Aleeert

• ⭕ Alertatron

• ⭕ Uniswap-v3

• ⭕ Copy-Trading

🛠️• Updates February/2023 :

• 📰 Launch of advertising material for Titan Affiliates 🛸

• 🛍️🎥🖼️📊 (Sales Page/VSL/Videos/Creative/Infographics)

🛠️• 28/05/2023 : Titan THEMIS update ▬ Version 2.7

🛠️• 28/05/2023 : BOT BOB release ▬ Version 1.0

• (Native Titan THEMIS Automation - Through BOT BOB, a bot for automation of signals, indicators and strategies of TradingView, of own code ▬ in validation.

• BOT BOB

Automation/Connection :

• API - For Centralized Brokers.

• Smart Contracts - Wallet Web - For Decentralized Brokers.

• This way users can automate any indicator or strategy of TradingView and Titan in a decentralized, secure and simplified way.

• Without having the need to use 'third party services' for automating TradingView indicators and strategies like the ones available above.

🛠️• 28/05/2023 : Release ▬ Titan Culture Guide 📝

3️⃣1️⃣ : 🧻 Notes ❕

🧻 • Note ❕ The "Demo 🐄" version, ❌does not have 'integrated automation', to automate the signals of this strategy and enjoy a fully automated system, you need to have access to the Pro version with '100% integrated automation' and all the tutorials for automation available. Become a Titan Pro 👽

🧻 • Note ❕ You will also need to be a "Pro User or higher on Tradingview", to be able to use the webhook feature available only for 'paid' profiles on the platform.

With the webhook feature it is possible to send the signals of this strategy to almost anywhere, in our case to centralized or decentralized brokerages, also to popular messaging services such as: Discord, Telegram or Twiter.

3️⃣2️⃣ : 🚨 Disclaimer ❕❗

🚨 • Disclaimer ❕❕ Past positive result and performance of a system does not guarantee its positive result and performance for the future!

🚨 • Disclaimer ❗❗❗ When using this strategy: Titan Investments is totally Exempt from any claim of liability for losses. The responsibility on the management of your funds is solely yours. This is a very high risk/volatility market! Understand your place in the market.

3️⃣3️⃣ : ♻️ ® No Repaint

This Strategy does not Repaint! This is a real strategy!

3️⃣4️⃣ : 🔒 Copyright ©️

Copyright © 2022-2023 All rights reserved, ® Titan Investimentos

3️⃣5️⃣ : 👏 Acknowledgments

I want to start this message in thanks to TradingView and all the Pinescript community for all the 'magic' created here, a unique ecosystem! rich and healthy, a fertile soil, a 'new world' of possibilities, for a complete deepening and improvement of our best personal skills.

I leave here my immense thanks to the whole community: Tradingview, Pinecoders, Wizards and Moderators.

I was not born Rich .

Thanks to TradingView and pinescript and all its transformation.

I could develop myself and the best of me and the best of my skills.

And consequently build wealth and patrimony.

Gratitude.

One more story for the infinite book !

If you were born poor you were born to be rich !

Raising🔼 the level and raising🔼 the ruler! 📏

My work is my 'debauchery'! Do better! 💐🌹

Soul of a first-timer! Creativity Exudes! 🦄

This is the manifestation of God's magic in me. This is the best of me. 🧙

You will copy me, I know. So you owe me. 💋

My mission here is to raise the consciousness and self-esteem of all Titans and Titanids! Welcome! 🧘 🏛️

The only way to accomplish great work is to do what you love ! Before I learned to program I was wasting my life!

Death is the best creation of life .

Now you are the new , but in the not so distant future you will gradually become the old . Here I stay forever!

Playing the game like an Athlete! 🖼️ Enjoy and Enjoy 🍷 🗿

In honor of: BOB ☆

1 name, 3 letters, 3 possibilities, and if read backwards it's the same thing, a palindrome. ☘

Gratitude to the oracles that have enabled me the 'luck' to get this far: Dal&Ni&Fer

3️⃣6️⃣ : 👮 House Rules : 📺 TradingView

House Rules : This publication and strategy follows all TradingView house guidelines and rules:

📺 TradingView House Rules: www.tradingview.com

📺 Script publication rules: www.tradingview.com

📺 Vendor requirements: www.tradingview.com

📺 Links/References rules: www.tradingview.com

3️⃣7️⃣ : 🏛️ Become a Titan Pro member 👽

🟩 Titan Pro 👽 🟩

3️⃣8️⃣ : 🏛️ Be a member Titan Aff 🛸

🟥 Titan Affiliate 🛸 🟥

Titan Investments|Quantitative THEMIS|Demo|BINANCE:BTCUSDTP:4hInvestment Strategy (Quantitative Trading)

| 🛑 | Watch "LIVE" and 'COPY' this strategy in real time:

🔗 Link: www.tradingview.com

Hello, welcome, feel free 🌹💐

Since the stone age to the most technological age, one thing has not changed, that which continues impress human beings the most, is the other human being!

Deep down, it's all very simple or very complicated, depends on how you look at it.

I believe that everyone was born to do something very well in life.

But few are those who have, let's use the word 'luck' .

Few are those who have the 'luck' to discover this thing.

That is why few are happy and successful in their jobs and professions.

Thank God I had this 'luck' , and discovered what I was born to do well.

And I was born to program. 👨💻

📋 Summary : Project Titan

0️⃣ : 🦄 Project Titan

1️⃣ : ⚖️ Quantitative THEMIS

2️⃣ : 🏛️ Titan Community

3️⃣ : 👨💻 Who am I ❔

4️⃣ : ❓ What is Statistical/Probabilistic Trading ❓

5️⃣ : ❓ How Statistical/Probabilistic Trading works ❓

6️⃣ : ❓ Why use a Statistical/Probabilistic system ❓

7️⃣ : ❓ Why the human brain is not prepared to do Trading ❓

8️⃣ : ❓ What is Backtest ❓

9️⃣ : ❓ How to build a Consistent system ❓

🔟 : ❓ What is a Quantitative Trading system ❓

1️⃣1️⃣ : ❓ How to build a Quantitative Trading system ❓

1️⃣2️⃣ : ❓ How to Exploit Market Anomalies ❓

1️⃣3️⃣ : ❓ What Defines a Robust, Profitable and Consistent System ❓

1️⃣4️⃣ : 🔧 Fixed Technical

1️⃣5️⃣ : ❌ Fixed Outputs : 🎯 TP(%) & 🛑SL(%)

1️⃣6️⃣ : ⚠️ Risk Profile

1️⃣7️⃣ : ⭕ Moving Exits : (Indicators)

1️⃣8️⃣ : 💸 Initial Capital

1️⃣9️⃣ : ⚙️ Entry Options

2️⃣0️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Third-Party Services'

2️⃣1️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Exchanges

2️⃣2️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Messaging Services'

2️⃣3️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : '🧲🤖Copy-Trading'

2️⃣4️⃣ : ❔ Why be a Titan Pro 👽❔

2️⃣5️⃣ : ❔ Why be a Titan Aff 🛸❔

2️⃣6️⃣ : 📋 Summary : ⚖️ Strategy: Titan Investments|Quantitative THEMIS|Demo|BINANCE:BTCUSDTP:4h

2️⃣7️⃣ : 📊 PERFORMANCE : 🆑 Conservative

2️⃣8️⃣ : 📊 PERFORMANCE : Ⓜ️ Moderate

2️⃣9️⃣ : 📊 PERFORMANCE : 🅰 Aggressive

3️⃣0️⃣ : 🛠️ Roadmap

3️⃣1️⃣ : 🧻 Notes ❕

3️⃣2️⃣ : 🚨 Disclaimer ❕❗

3️⃣3️⃣ : ♻️ ® No Repaint

3️⃣4️⃣ : 🔒 Copyright ©️

3️⃣5️⃣ : 👏 Acknowledgments

3️⃣6️⃣ : 👮 House Rules : 📺 TradingView

3️⃣7️⃣ : 🏛️ Become a Titan Pro member 👽

3️⃣8️⃣ : 🏛️ Be a member Titan Aff 🛸

0️⃣ : 🦄 Project Titan

This is the first real, 100% automated Quantitative Strategy made available to the public and the pinescript community for TradingView.

You will be able to automate all signals of this strategy for your broker , centralized or decentralized and also for messaging services : Discord, Telegram or Twitter .

This is the first strategy of a larger project, in 2023, I will provide a total of 6 100% automated 'Quantitative' strategies to the pinescript community for TradingView.

The future strategies to be shared here will also be unique , never before seen, real 'Quantitative' bots with real, validated results in real operation.

Just like the 'Quantitative THEMIS' strategy, it will be something out of the loop throughout the pinescript/tradingview community, truly unique tools for building mutual wealth consistently and continuously for our community.

1️⃣ : ⚖️ Quantitative THEMIS : Titan Investments|Quantitative THEMIS|Demo|BINANCE:BTCUSDTP:4h

This is a truly unique and out of the curve strategy for BTC /USD .

A truly real strategy, with real, validated results and in real operation.

A unique tool for building mutual wealth, consistently and continuously for the members of the Titan community.

Initially we will operate on a monthly, quarterly, annual or biennial subscription service.

Our goal here is to build a great community, in exchange for an extremely fair value for the use of our truly unique tools, which bring and will bring real results to our community members.

With this business model it will be possible to provide all Titan users and community members with the purest and highest degree of sophistication in the market with pinescript for tradingview, providing unique and truly profitable strategies.

My goal here is to offer the best to our members!

The best 'pinescript' tradingview service in the world!

We are the only Start-Up in the world that will decentralize real and full access to truly real 'quantitative' tools that bring and will bring real results for mutual and ongoing wealth building for our community.

2️⃣ : 🏛️ Titan Community : 👽 Pro 🔁 Aff 🛸

Become a Titan Pro 👽

To get access to the strategy: "Quantitative THEMIS" , and future Titan strategies in a 100% automated way, along with all tutorials for automation.

Pro Plans: 30 Days, 90 Days, 12 Months, 24 Months.

👽 Pro 🅼 Monthly

👽 Pro 🆀 Quarterly

👽 Pro🅰 Annual

👽 Pro👾Two Years

You will have access to a truly unique system that is out of the curve .

A 100% real, 100% automated, tested, validated, profitable, and in real operation strategy.

Become a Titan Affiliate 🛸

By becoming a Titan Affiliate 🛸, you will automatically receive 50% of the value of each new subscription you refer .

You will receive 50% for any of the above plans that you refer .

This way we will encourage our community to grow in a fair and healthy way, because we know what we have in our hands and what we deliver real value to our users.

We are at the highest level of sophistication in the market, the consistency here and the results here speak for themselves.

So growing our community means growing mutual wealth and raising collective conscience.

Wealth must be created not divided.

And here we are creating mutual wealth on all ends and in all ways.

A non-zero sum system, where everybody wins.

3️⃣ : 👨💻 Who am I ❔

My name is FilipeSoh I am 26 years old, Technical Analyst, Trader, Computer Engineer, pinescript Specialist, with extensive experience in several languages and technologies.

For the last 4 years I have been focusing on developing, editing and creating pinescript indicators and strategies for Tradingview for people and myself.