PROFIT + V2We are glad to introduce you our new strategy PROFIT +.

The strategy PROFIT + is based on price and volume correlation analysis.

The entries are quick with tight stop loss. Best suits fot those who like

to get quick profit in the beginning of the price move.

It was tested on BTC , Bitmex exchange on 1 hour timeframe,

but it can also be used on 30, 15 and 10 minutes tf.

There is also ALERT INDICATOR for the strategy to receive notification

when there is a buy/sell signal.

To get acces to the strategy pm me.

-------------------------------------------------------------------------

Рады представить нашу новую торговую стратегию PROFIT+.

Стратегия PROFIT + основана на анализе корреляции цены и объёма.

Входы в стратегии быстрые с коротким стопом. Больше подходит для

тех кто любит забирать быстрый профит в самом начале движения.

Стратегия была тестирована на инструменте BTC биржа BITMEX

на 1 часовом таймфрейме, но она также работает на 30, 15 и 10 минутных тф.

Для стратегии также доступен ИНДИКАТОР АЛЕРТ для получения оповещения

при появлении buy/sell сигналов.

Для получения доступа к стратегии пишите мне в личные сообщения.

Cerca negli script per "profit"

Profit Runner Strategy v2.0This is the strategy version of the recently posted Profit Runner v2.0 study. We include both together so that users can use the strategy for backtesting and figuring out the optimal settings for their specific usage and then implement those settings in the study version(which includes alerts for automated trading).

Green background highlights are buy signals and red background highlights are sell signals. Red and green filled area show the user's stop loss .

QuantBuilder | FractalystWhat's the strategy's purpose and functionality?

QuantBuilder is designed for both traders and investors who want to utilize mathematical techniques to develop profitable strategies through backtesting on historical data.

The primary goal is to develop profitable quantitive strategies that not only outperform the underlying asset in terms of returns but also minimize drawdown.

For instance, consider Bitcoin (BTC), which has experienced significant volatility, averaging an estimated 200% annual return over the past decade, with maximum drawdowns exceeding -80%. By employing this strategy with diverse entry and exit techniques, users can potentially seek to enhance their Compound Annual Growth Rate (CAGR) while managing risk to maintain a lower maximum drawdown.

While this strategy employs quantitative techniques, including mathematical methods such as probabilities and positive expected values, it demonstrates exceptional efficacy across all markets. It particularly excels in futures, indices, stocks, cryptocurrencies, and commodities, leveraging their inherent trending behaviors for optimized performance.

In both trending and consolidating market conditions, QuantBuilder employs a combination of multi-timeframe probabilities, expected values, directional biases, moving averages and diverse entry models to identify and capitalize on bullish market movements.

How does the strategy perform for both investors and traders?

The strategy has two main modes, tailored for different market participants: Traders and Investors.

1. Trading:

- Designed for traders looking to capitalize on bullish markets.

- Utilizes a percentage risk per trade to manage risk and optimize returns.

- Suitable for both swing and intraday trading with a focus on probabilities and risk per trade approach.

2. Investing:

- Geared towards investors who aim to capitalize on bullish trending markets without using leverage while mitigating the asset's maximum drawdown.

- Utilizes pre-define percentage of the equity to buy, hold, and manage the asset.

- Focuses on long-term growth and capital appreciation by fully/partially investing in the asset during bullish conditions.

How does the strategy identify market structure? What are the underlying calculations?

The strategy utilizes an efficient logic with for loops to pinpoint the first swing candle featuring a pivot of 2, establishing the point at which the break of structure begins.

What entry criteria are used in this script? What are the underlying calculations?

The script utilizes two entry models: BreakOut and fractal.

Underlying Calculations:

Breakout: The script assigns the most recent swing high to a variable. When the price closes above this level and all other conditions are met, the script executes a breakout entry (conservative approach).

Fractal: The script identifies a swing low with a period of 2. Once this condition is met, the script executes the trade (aggressive approach).

How does the script calculate probabilities? What are the underlying calculations?

The script calculates probabilities by monitoring price interactions with liquidity levels. Here’s how the underlying calculations work:

Tracking Price Hits: The script counts the number of times the price taps into each liquidity side after the EQM level is activated. This data is stored in an array for further analysis.

Sample Size Consideration: The total number of price interactions serves as the sample size for calculating probabilities.

Probability Calculation: For each liquidity side, the script calculates the probability by taking the average of the recorded hits. This allows for a dynamic assessment of the likelihood that a particular side will be hit next, based on historical performance.

Dynamic Adjustment: As new price data comes in, the probabilities are recalculated, providing real-time aduptive insights into market behavior.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

How does the script calculate expected values? What are the underlying calculations?

The script calculates expected values by leveraging the probabilities of winning and losing trades, along with their respective returns. The process involves the following steps:

This quantitative methodology provides a robust framework for assessing the expected performance of trading strategies based on historical data and backtesting results.

How is the contextual bias calculated? What are the underlying calculations?

The contextual bias in the QuantBuilder script is calculated through a structured approach that assesses market structure based on swing highs and lows. Here’s how it works:

Identification of Swing Points: The script identifies significant swing points using a defined pivot logic, focusing on the first swing high and swing low. This helps establish critical levels for determining market structure.

Break of Structure (BOS) Assessment:

Bullish BOS: The script recognizes a bullish break of structure when a candle closes above the first swing high, followed by at least one swing low.

Bearish BOS: Conversely, a bearish break of structure is identified when a candle closes below the first swing low, followed by at least one swing high.

Bias Assignment: Based on the identified break of structure, the script assigns directional biases:

A bullish bias is assigned if a bullish BOS is confirmed.

A bearish bias is assigned if a bearish BOS is confirmed.

Quantitative Evaluation: Each identified bias is quantitatively evaluated, allowing the script to assign numerical values representing the strength of each bias. This quantification aids in assessing the reliability of market sentiment across multiple timeframes.

What's the purpose of using moving averages in this strategy? What are the underlying calculations?

Using moving averages is a widely-used technique to trade with the trend.

The main purpose of using moving averages in this strategy is to filter out bearish price action and to only take trades when the price is trading ABOVE specified moving averages.

The script uses different types of moving averages with user-adjustable timeframes and periods/lengths, allowing traders to try out different variations to maximize strategy performance and minimize drawdowns.

By applying these calculations, the strategy effectively identifies bullish trends and avoids market conditions that are not conducive to profitable trades.

The MA filter allows traders to choose whether they want a specific moving average above or below another one as their entry condition.

What type of stop-loss identification method are used in this strategy? What are the underlying calculations?

- Initial Stop-loss:

1. ATR Based:

The Average True Range (ATR) is a method used in technical analysis to measure volatility. It is not used to indicate the direction of price but to measure volatility, especially volatility caused by price gaps or limit moves.

Calculation:

- To calculate the ATR, the True Range (TR) first needs to be identified. The TR takes into account the most current period high/low range as well as the previous period close.

The True Range is the largest of the following:

- Current Period High minus Current Period Low

- Absolute Value of Current Period High minus Previous Period Close

- Absolute Value of Current Period Low minus Previous Period Close

- The ATR is then calculated as the moving average of the TR over a specified period. (The default period is 14)

2. ADR Based:

The Average Day Range (ADR) is an indicator that measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

Calculation:

- To calculate the ADR for a particular day:

- Calculate the average of the high prices over a specified number of days.

- Calculate the average of the low prices over the same number of days.

- Find the difference between these average values.

- The default period for calculating the ADR is 14 days. A shorter period may introduce more noise, while a longer period may be slower to react to new market movements.

3. PL Based:

This method places the stop-loss at the low of the previous candle.

If the current entry is based on the hunt entry strategy, the stop-loss will be placed at the low of the candle that wicks through the lower FRMA band.

Example:

If the previous candle's low is 100, then the stop-loss will be set at 100.

This method ensures the stop-loss is placed just below the most recent significant low, providing a logical and immediate level for risk management.

- Trailing Stop-Loss:

One of the key elements of this strategy is its ability to detect structural liquidity and structural invalidation levels across multiple timeframes to trail the stop-loss once the trade is in running profits.

By utilizing this approach, the strategy allows enough room for price to run.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop.

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance.

What type of break-even and take profit identification methods are used in this strategy? What are the underlying calculations?

For Break-Even:

Percentage (%) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain percentage above the entry.

Calculation:

Break-even level = Entry Price * (1 + Percentage / 100)

Example:

If the entry price is $100 and the break-even percentage is 5%, the break-even level is $100 * 1.05 = $105.

Risk-to-Reward (RR) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain RR ratio.

Calculation:

Break-even level = Entry Price + (Initial Risk * RR Ratio)

For TP1 (Take Profit 1):

- You can choose to set a take profit level at which your position gets fully closed or 50% if the TP2 boolean is enabled.

- Similar to break-even, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP1 level as a percentage amount above the entry price or based on RR.

For TP2 (Take Profit 2):

- You can choose to set a take profit level at which your position gets fully closed.

- As with break-even and TP1, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP2 level as a percentage amount above the entry price or based on RR.

What's the day filter Filter, what does it do?

The day filter allows users to customize the session time and choose the specific days they want to include in the strategy session. This helps traders tailor their strategies to particular trading sessions or days of the week when they believe the market conditions are more favorable for their trading style.

Customize Session Time:

Users can define the start and end times for the trading session.

This allows the strategy to only consider trades within the specified time window, focusing on periods of higher market activity or preferred trading hours.

Select Days:

Users can select which days of the week to include in the strategy.

This feature is useful for excluding days with historically lower volatility or unfavorable trading conditions (e.g., Mondays or Fridays).

Benefits:

Focus on Optimal Trading Periods:

By customizing session times and days, traders can focus on periods when the market is more likely to present profitable opportunities.

Avoid Unfavorable Conditions:

Excluding specific days or times can help avoid trading during periods of low liquidity or high unpredictability, such as major news events or holidays.

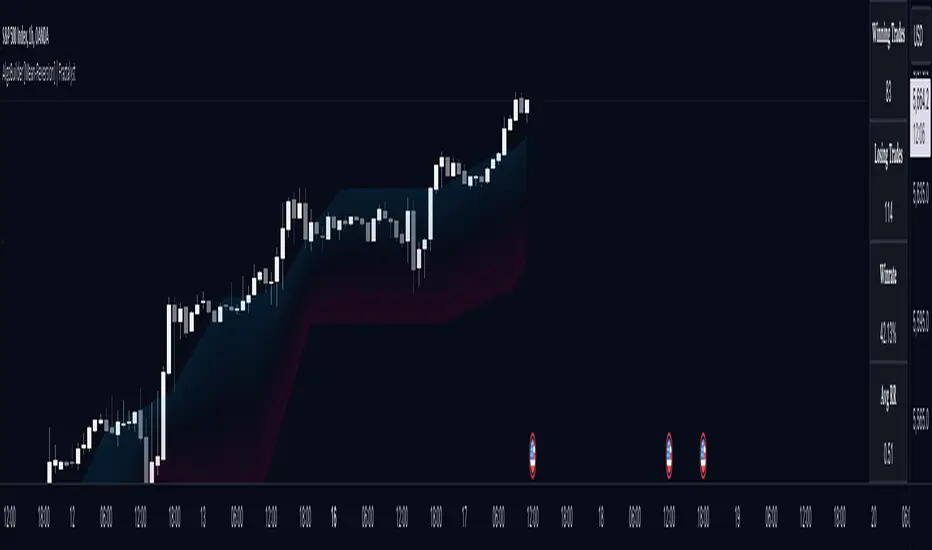

What tables are available in this script?

- Summary: Provides a general overview, displaying key performance parameters such as Net Profit, Profit Factor, Max Drawdown, Average Trade, Closed Trades and more.

Total Commission: Displays the cumulative commissions incurred from all trades executed within the selected backtesting window. This value is derived by summing the commission fees for each trade on your chart.

Average Commission: Represents the average commission per trade, calculated by dividing the Total Commission by the total number of closed trades. This metric is crucial for assessing the impact of trading costs on overall profitability.

Avg Trade: The sum of money gained or lost by the average trade generated by a strategy. Calculated by dividing the Net Profit by the overall number of closed trades. An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.

MaxDD: Displays the largest drawdown of losses, i.e., the maximum possible loss that the strategy could have incurred among all of the trades it has made. This value is calculated separately for every bar that the strategy spends with an open position.

Profit Factor: The amount of money a trading strategy made for every unit of money it lost (in the selected currency). This value is calculated by dividing gross profits by gross losses.

Avg RR: This is calculated by dividing the average winning trade by the average losing trade. This field is not a very meaningful value by itself because it does not take into account the ratio of the number of winning vs losing trades, and strategies can have different approaches to profitability. A strategy may trade at every possibility in order to capture many small profits, yet have an average losing trade greater than the average winning trade. The higher this value is, the better, but it should be considered together with the percentage of winning trades and the net profit.

Winrate: The percentage of winning trades generated by a strategy. Calculated by dividing the number of winning trades by the total number of closed trades generated by a strategy. Percent profitable is not a very reliable measure by itself. A strategy could have many small winning trades, making the percent profitable high with a small average winning trade, or a few big winning trades accounting for a low percent profitable and a big average winning trade. Most mean-reversion successful strategies have a percent profitability of 40-80% but are profitable due to risk management control.

BE Trades: Number of break-even trades, excluding commission/slippage.

Losing Trades: The total number of losing trades generated by the strategy.

Winning Trades: The total number of winning trades generated by the strategy.

Total Trades: Total number of taken traders visible your charts.

Net Profit: The overall profit or loss (in the selected currency) achieved by the trading strategy in the test period. The value is the sum of all values from the Profit column (on the List of Trades tab), taking into account the sign.

- Monthly: Displays performance data on a month-by-month basis, allowing users to analyze performance trends over each month and year.

- Weekly: Displays performance data on a week-by-week basis, helping users to understand weekly performance variations.

- UI Table: A user-friendly table that allows users to view and save the selected strategy parameters from user inputs. This table enables easy access to key settings and configurations, providing a straightforward solution for saving strategy parameters by simply taking a screenshot with Alt + S or ⌥ + S.

User-input styles and customizations:

To facilitate studying historical data, all conditions and filters can be applied to your charts. By plotting background colors on your charts, you'll be able to identify what worked and what didn't in certain market conditions.

Please note that all background colors in the style are disabled by default to enhance visualization.

How to Use This Quantitive Strategy Builder to Create a Profitable Edge and System?

Choose Your Strategy mode:

- Decide whether you are creating an investing strategy or a trading strategy.

Select a Market:

- Choose a one-sided market such as stocks, indices, or cryptocurrencies.

Historical Data:

- Ensure the historical data covers at least 10 years of price action for robust backtesting.

Timeframe Selection:

- Choose the timeframe you are comfortable trading with. It is strongly recommended to use a timeframe above 15 minutes to minimize the impact of commissions/slippage on your profits.

Set Commission and Slippage:

- Properly set the commission and slippage in the strategy properties according to your broker/prop firm specifications.

Parameter Optimization:

- Use trial and error to test different parameters until you find the performance results you are looking for in the summary table or, preferably, through deep backtesting using the strategy tester.

Trade Count:

- Ensure the number of trades is 200 or more; the higher, the better for statistical significance.

Positive Average Trade:

- Make sure the average trade is above zero.

(An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.)

Performance Metrics:

- Look for a high profit factor, and net profit with minimum drawdown.

- Ideally, aim for a drawdown under 20-30%, depending on your risk tolerance.

Refinement and Optimization:

- Try out different markets and timeframes.

- Continue working on refining your edge using the available filters and components to further optimize your strategy.

What makes this strategy original?

QuantBuilder stands out due to its unique combination of quantitative techniques and innovative algorithms that leverage historical data for real-time trading decisions. Unlike most algorithmic strategies that work based on predefined rules, this strategy adapts to real-time market probabilities and expected values, enhancing its reliability. Key features include:

Mathematical Framework: The strategy integrates advanced mathematical concepts, such as probabilities and expected values, to assess trade viability and optimize decision-making.

Multi-Timeframe Analysis: By utilizing multi-timeframe probabilities, QuantBuilder provides a comprehensive view of market conditions, enhancing the accuracy of entry and exit points.

Dynamic Market Structure Identification: The script employs a systematic approach to identify market structure changes, utilizing a blend of swing highs and lows to detect contextual/direction bias of the market.

Built-in Trailing Stop Loss: The strategy features a dynamic trailing stop loss based on multi-timeframe analysis of market structure. This allows traders to lock in profits while adapting to changing market conditions, ensuring that exits are executed at optimal levels without prematurely closing positions.

Robust Performance Metrics: With detailed performance tables and visualizations, users can easily evaluate strategy effectiveness and adjust parameters based on historical performance.

Adaptability: The strategy is designed to work across various markets and timeframes, making it versatile for different trading styles and objectives.

Suitability for Investors and Traders: QuantBuilder is ideal for both investors and traders looking to rely on mathematically proven data to create profitable strategies, ensuring that decisions are grounded in quantitative analysis.

These original elements combine to create a powerful tool that can help both traders and investors to build and refine profitable strategies based on algorithmic quantitative analysis.

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

AlgoBuilder [Mean-Reversion] | FractalystWhat's the strategy's purpose and functionality?

This strategy is designed for both traders and investors looking to rely and trade based on historical and backtested data using automation.

The main goal is to build profitable mean-reversion strategies that outperform the underlying asset in terms of returns while minimizing drawdown.

For example, as for a benchmark, if the S&P 500 (SPX) has achieved an estimated 10% annual return with a maximum drawdown of -57% over the past 20 years, using this strategy with different entry and exit techniques, users can potentially seek ways to achieve a higher Compound Annual Growth Rate (CAGR) while maintaining a lower maximum drawdown.

Although the strategy can be applied to all markets and timeframes, it is most effective on stocks, indices, future markets, cryptocurrencies, and commodities and JPY currency pairs given their trending behaviors.

In trending market conditions, the strategy employs a combination of moving averages and diverse entry models to identify and capitalize on upward market movements. It integrates market structure-based moving averages and bands mechanisms across different timeframes and provides exit techniques, including percentage-based and risk-reward (RR) based take profit levels.

Additionally, the strategy has also a feature that includes a built-in probability function for traders who want to implement probabilities right into their trading strategies.

Performance summary, weekly, and monthly tables enable quick visualization of performance metrics like net profit, maximum drawdown, profit factor, average trade, average risk-reward ratio (RR), and more.

This aids optimization to meet specific goals and risk tolerance levels effectively.

-----

How does the strategy perform for both investors and traders?

The strategy has two main modes, tailored for different market participants: Traders and Investors.

Trading:

1. Trading:

- Designed for traders looking to capitalize on bullish trending markets.

- Utilizes a percentage risk per trade to manage risk and optimize returns.

- Suitable for active trading with a focus on mean-reversion and risk per trade approach.

◓: Mode | %: Risk percentage per trade

3. Investing:

- Geared towards investors who aim to capitalize on bullish trending markets without using leverage while mitigating the asset's maximum drawdown.

- Utilizes pre-define percentage of the equity to buy, hold, and manage the asset.

- Focuses on long-term growth and capital appreciation by fully investing in the asset during bullish conditions.

- ◓: Mode | %: Risk not applied (In investing mode, the strategy uses 10% of equity to buy the asset)

-----

What's is FRMA? How does the triple bands work? What are the underlying calculations?

Middle Band (FRMA):

The middle band is the core of the FRMA system. It represents the Fractalyst Moving Average, calculated by identifying the most recent external swing highs and lows in the market structure.

By determining these external swing pivot points, which act as significant highs and lows within the market range, the FRMA provides a unique moving average that adapts to market structure changes.

Upper Band:

The upper band shows the average price of the most recent external swing highs.

External swing highs are identified as the highest points between pivot points in the market structure.

This band helps traders identify potential overbought conditions when prices approach or exceed this upper band.

Lower Band:

The lower band shows the average price of the most recent external swing lows.

External swing lows are identified as the lowest points between pivot points in the market structure.

The script utilizes this band to identify potential oversold conditions, triggering entry signals as prices approach or drop below the lower band.

Adjustments Based on User Inputs:

Users can adjust how the upper and lower bands are calculated based on their preferences:

Upper/Lower: This method calculates the average bands using the prices of external swing highs and lows identified in the market.

Percentage Deviation from FRMA: Alternatively, users can opt to calculate the bands based on a percentage deviation from the middle FRMA. This approach provides flexibility to adjust the width of the bands relative to market conditions and volatility.

-----

What's the purpose of using moving averages in this strategy? What are the underlying calculations?

Using moving averages is a widely-used technique to trade with the trend.

The main purpose of using moving averages in this strategy is to filter out bearish price action and to only take trades when the price is trading ABOVE specified moving averages.

The script uses different types of moving averages with user-adjustable timeframes and periods/lengths, allowing traders to try out different variations to maximize strategy performance and minimize drawdowns.

By applying these calculations, the strategy effectively identifies bullish trends and avoids market conditions that are not conducive to profitable trades.

The MA filter allows traders to choose whether they want a specific moving average above or below another one as their entry condition.

This comparison filter can be turned on (>) or off.

For example, you can set the filter so that MA#1 > MA#2, meaning the first moving average must be above the second one before the script looks for entry conditions. This adds an extra layer of trend confirmation, ensuring that trades are only taken in more favorable market conditions.

⍺: MA Period | Σ: MA Timeframe

-----

What entry modes are used in this strategy? What are the underlying calculations?

The strategy by default uses two different techniques for the entry criteria with user-adjustable left and right bars: Breakout and Fractal.

1. Breakout Entries :

- The strategy looks for pivot high points with a default period of 3.

- It stores the most recent high level in a variable.

- When the price crosses above this most recent level, the strategy checks if all conditions are met and the bar is closed before taking the buy entry.

◧: Pivot high left bars period | ◨: Pivot high right bars period

2. Fractal Entries :

- The strategy looks for pivot low points with a default period of 3.

- When a pivot low is detected, the strategy checks if all conditions are met and the bar is closed before taking the buy entry.

◧: Pivot low left bars period | ◨: Pivot low right bars period

2. Hunt Entries :

- The strategy identifies a candle that wicks through the lower FRMA band.

- It waits for the next candle to close above the low of the wick candle.

- When this condition is met and the bar is closed, the strategy takes the buy entry.

By utilizing these entry modes, the strategy aims to capitalize on bullish price movements while ensuring that the necessary conditions are met to validate the entry points.

-----

What type of stop-loss identification method are used in this strategy? What are the underlying calculations?

Initial Stop-Loss:

1. ATR Based:

The Average True Range (ATR) is a method used in technical analysis to measure volatility. It is not used to indicate the direction of price but to measure volatility, especially volatility caused by price gaps or limit moves.

Calculation:

- To calculate the ATR, the True Range (TR) first needs to be identified. The TR takes into account the most current period high/low range as well as the previous period close.

The True Range is the largest of the following:

- Current Period High minus Current Period Low

- Absolute Value of Current Period High minus Previous Period Close

- Absolute Value of Current Period Low minus Previous Period Close

- The ATR is then calculated as the moving average of the TR over a specified period. (The default period is 14).

Example - ATR (14) * 2

⍺: ATR period | Σ: ATR Multiplier

2. ADR Based:

The Average Day Range (ADR) is an indicator that measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

Calculation:

- To calculate the ADR for a particular day:

- Calculate the average of the high prices over a specified number of days.

- Calculate the average of the low prices over the same number of days.

- Find the difference between these average values.

- The default period for calculating the ADR is 14 days. A shorter period may introduce more noise, while a longer period may be slower to react to new market movements.

Example - ADR (20) * 2

⍺: ADR period | Σ: ADR Multiplier

3. PL Based:

This method places the stop-loss at the low of the previous candle.

If the current entry is based on the hunt entry strategy, the stop-loss will be placed at the low of the candle that wicks through the lower FRMA band.

Example:

If the previous candle's low is 100, then the stop-loss will be set at 100.

This method ensures the stop-loss is placed just below the most recent significant low, providing a logical and immediate level for risk management.

Application in Strategy (ATR/ADR):

- The strategy calculates the current bar's ADR/ATR with a user-defined period.

- It then multiplies the ADR/ATR by a user-defined multiplier to determine the initial stop-loss level.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop.

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance.

-----

What type of break-even and take profit identification methods are used in this strategy? What are the underlying calculations?

For Break-Even:

Percentage (%) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain percentage above the entry.

Calculation:

Break-even level = Entry Price * (1 + Percentage / 100)

Example:

If the entry price is $100 and the break-even percentage is 5%, the break-even level is $100 * 1.05 = $105.

Risk-to-Reward (RR) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain RR ratio.

Calculation:

Break-even level = Entry Price + (Initial Risk * RR Ratio)

Example:

If the entry price is $100, the initial risk is $10, and the RR ratio is 2, the break-even level is $100 + ($10 * 2) = $120.

FRMA Based:

Moves the stop-loss to break-even when the price hits the FRMA level at which the entry was taken.

Calculation:

Break-even level = FRMA level at the entry

Example:

If the FRMA level at entry is $102, the break-even level is set to $102 when the price reaches $102.

For TP1 (Take Profit 1):

- You can choose to set a take profit level at which your position gets fully closed or 50% if the TP2 boolean is enabled.

- Similar to break-even, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP1 level as a percentage amount above the entry price or based on RR.

For TP2 (Take Profit 2):

- You can choose to set a take profit level at which your position gets fully closed.

- As with break-even and TP1, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP2 level as a percentage amount above the entry price or based on RR.

When Both Percentage (%) Based and RR Based Take Profit Levels Are Off:

The script will adjust the take profit level to the higher FRMA band set within user inputs.

Calculation:

Take profit level = Higher FRMA band length/timeframe specified by the user.

This ensures that when neither percentage-based nor risk-to-reward-based take profit methods are enabled, the strategy defaults to using the higher FRMA band as the take profit level, providing a consistent and structured approach to profit-taking.

For TP1 and TP2, it's specifying the price levels at which the position is partially or fully closed based on the chosen method (percentage or RR) above the entry price.

These calculations are crucial for managing risk and optimizing profitability in the strategy.

⍺: BE/TP type (%/RR) | Σ: how many RR/% above the current price

-----

What's the ADR filter? What does it do? What are the underlying calculations?

The Average Day Range (ADR) measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

The period of the ADR filter used in this strategy is tied to the same period you've used for your initial stop-loss.

Users can define the minimum ADR they want to be met before the script looks for entry conditions.

ADR Bias Filter:

- Compares the current bar ADR with the ADR (Defined by user):

- If the current ADR is higher, it indicates that volatility has increased compared to ADR (DbU).(⬆)

- If the current ADR is lower, it indicates that volatility has decreased compared to ADR (DbU).(⬇)

Calculations:

1. Calculate ADR:

- Average the high prices over the specified period.

- Average the low prices over the same period.

- Find the difference between these average values in %.

2. Current ADR vs. ADR (DbU):

- Calculate the ADR for the current bar.

- Calculate the ADR (DbU).

- Compare the two values to determine if volatility has increased or decreased.

By using the ADR filter, the strategy ensures that trades are only taken in favorable market conditions where volatility meets the user's defined threshold, thus optimizing entry conditions and potentially improving the overall performance of the strategy.

>: Minimum required ADR for entry | %: Current ADR comparison to ADR of 14 days ago.

-----

What's the probability filter? What are the underlying calculations?

The probability filter is designed to enhance trade entries by using buyside liquidity and probability analysis to filter out unfavorable conditions.

This filter helps in identifying optimal entry points where the likelihood of a profitable trade is higher.

Calculations:

1. Understanding Swing highs and Swing Lows

Swing High: A Swing High is formed when there is a high with 2 lower highs to the left and right.

Swing Low: A Swing Low is formed when there is a low with 2 higher lows to the left and right.

2. Understanding the purpose and the underlying calculations behind Buyside, Sellside and Equilibrium levels.

3. Understanding probability calculations

1. Upon the formation of a new range, the script waits for the price to reach and tap into equilibrium or the 50% level. Status: "⏸" - Inactive

2. Once equilibrium is tapped into, the equilibrium status becomes activated and it waits for either liquidity side to be hit. Status: "▶" - Active

3. If the buyside liquidity is hit, the script adds to the count of successful buyside liquidity occurrences. Similarly, if the sellside is tapped, it records successful sellside liquidity occurrences.

5. Finally, the number of successful occurrences for each side is divided by the overall count individually to calculate the range probabilities.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

Example - BSL > 55%

-----

What's the range length Filter? What are the underlying calculations?

The range length filter identifies the price distance between buyside and sellside liquidity levels in percentage terms. When enabled, the script only looks for entries when the minimum range length is met. This helps ensure that trades are taken in markets with sufficient price movement.

Calculations:

Range Length (%) = ( ( Buyside Level − Sellside Level ) / Current Price ) ×100

Range Bias Identification:

Bullish Bias: The current range price has broken above the previous external swing high.

Bearish Bias: The current range price has broken below the previous external swing low.

Example - Range length filter is enabled | Range must be above 1%

>: Minimum required range length for entry | %: Current range length percentage in a (Bullish/Bearish) range

-----

What's the day filter Filter, what does it do?

The day filter allows users to customize the session time and choose the specific days they want to include in the strategy session. This helps traders tailor their strategies to particular trading sessions or days of the week when they believe the market conditions are more favorable for their trading style.

Customize Session Time:

Users can define the start and end times for the trading session.

This allows the strategy to only consider trades within the specified time window, focusing on periods of higher market activity or preferred trading hours.

Select Days:

Users can select which days of the week to include in the strategy.

This feature is useful for excluding days with historically lower volatility or unfavorable trading conditions (e.g., Mondays or Fridays).

Benefits:

Focus on Optimal Trading Periods:

By customizing session times and days, traders can focus on periods when the market is more likely to present profitable opportunities.

Avoid Unfavorable Conditions:

Excluding specific days or times can help avoid trading during periods of low liquidity or high unpredictability, such as major news events or holidays.

Increased Flexibility: The filter provides increased flexibility, allowing traders to adapt the strategy to their specific needs and preferences.

Example - Day filter | Session Filter

θ: Session time | Exchange time-zone

-----

What tables are available in this script?

Table Type:

- Summary: Provides a general overview, displaying key performance parameters such as Net Profit, Profit Factor, Max Drawdown, Average Trade, Closed Trades and more.

Avg Trade: The sum of money gained or lost by the average trade generated by a strategy. Calculated by dividing the Net Profit by the overall number of closed trades. An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.

MaxDD: Displays the largest drawdown of losses, i.e., the maximum possible loss that the strategy could have incurred among all of the trades it has made. This value is calculated separately for every bar that the strategy spends with an open position.

Profit Factor: The amount of money a trading strategy made for every unit of money it lost (in the selected currency). This value is calculated by dividing gross profits by gross losses.

Avg RR: This is calculated by dividing the average winning trade by the average losing trade. This field is not a very meaningful value by itself because it does not take into account the ratio of the number of winning vs losing trades, and strategies can have different approaches to profitability. A strategy may trade at every possibility in order to capture many small profits, yet have an average losing trade greater than the average winning trade. The higher this value is, the better, but it should be considered together with the percentage of winning trades and the net profit.

Winrate: The percentage of winning trades generated by a strategy. Calculated by dividing the number of winning trades by the total number of closed trades generated by a strategy. Percent profitable is not a very reliable measure by itself. A strategy could have many small winning trades, making the percent profitable high with a small average winning trade, or a few big winning trades accounting for a low percent profitable and a big average winning trade. Most mean-reversion successful strategies have a percent profitability of 40-80% but are profitable due to risk management control.

BE Trades: Number of break-even trades, excluding commission/slippage.

Losing Trades: The total number of losing trades generated by the strategy.

Winning Trades: The total number of winning trades generated by the strategy.

Total Trades: Total number of taken traders visible your charts.

Net Profit: The overall profit or loss (in the selected currency) achieved by the trading strategy in the test period. The value is the sum of all values from the Profit column (on the List of Trades tab), taking into account the sign.

- Monthly: Displays performance data on a month-by-month basis, allowing users to analyze performance trends over each month.

- Weekly: Displays performance data on a week-by-week basis, helping users to understand weekly performance variations.

- OFF: Hides the performance table.

Profit Color:

- Allows users to set the color for representing profit in the performance table, helping to quickly distinguish profitable periods.

Loss Color:

- Allows users to set the color for representing loss in the performance table, helping to quickly identify loss-making periods.

These customizable tables provide traders with flexible and detailed performance analysis, aiding in better strategy evaluation and optimization.

-----

User-input styles and customizations:

To facilitate studying historical data, all conditions and rules can be applied to your charts. By plotting background colors on your charts, you'll be able to identify what worked and what didn't in certain market conditions.

Please note that all background colors in the style are disabled by default to enhance visualization.

-----

How to Use This Algobuilder to Create a Profitable Edge and System:

Choose Your Strategy mode:

- Decide whether you are creating an investing strategy or a trading strategy.

Select a Market:

- Choose a one-sided market such as stocks, indices, or cryptocurrencies.

Historical Data:

- Ensure the historical data covers at least 10 years of price action for robust backtesting.

Timeframe Selection:

- Choose the timeframe you are comfortable trading with. It is strongly recommended to use a timeframe above 15 minutes to minimize the impact of commissions/slippage on your profits.

Set Commission and Slippage:

- Properly set the commission and slippage in the strategy properties according to your broker or prop firm specifications.

Parameter Optimization:

- Use trial and error to test different parameters until you find the performance results you are looking for in the summary table or, preferably, through deep backtesting using the strategy tester.

Trade Count:

- Ensure the number of trades is 100 or more; the higher, the better for statistical significance.

Positive Average Trade:

- Make sure the average trade value is above zero.

(An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.)

Performance Metrics:

- Look for a high profit factor, and net profit with minimum drawdown.

- Ideally, aim for a drawdown under 20-30%, depending on your risk tolerance.

Refinement and Optimization:

- Try out different markets and timeframes.

- Continue working on refining your edge using the available filters and components to further optimize your strategy.

Automation:

- Once you’re confident in your strategy, you can use the automation section to connect the algorithm to your broker or prop firm.

- Trade a fully automated and backtested trading strategy, allowing for hands-free execution and management.

-----

What makes this strategy original?

1. Incorporating direct integration of probabilities into the strategy.

2. Utilizing built-in market structure-based moving averages across various timeframes.

4. Offering both investing and trading strategies, facilitating optimization from different perspectives.

5. Automation for efficient execution.

6. Providing a summary table for instant access to key parameters of the strategy.

-----

How to use automation?

For Traders:

1. Ensure the strategy parameters are properly set based on your optimized parameters.

2. Enter your PineConnector License ID in the designated field.

3. Specify the desired risk level.

4. Provide the Metatrader symbol.

5. Check for chart updates to ensure the automation table appears on the top right corner, displaying your License ID, risk, and symbol.

6. Set up an alert with the strategy selected as Condition and the Message as {{strategy.order.alert_message}}.

7. Activate the Webhook URL in the Notifications section, setting it as the official PineConnector webhook address.

8. Double-check all settings on PineConnector to ensure the connection is successful.

9. Create the alert for entry/exit automation.

For Investors:

1. Ensure the strategy parameters are properly set based on your optimized parameters.

2. Choose "Investing" in the user-input settings.

3. Create an alert with a specified name.

4. Customize the notifications tab to receive alerts via email.

5. Buying/selling alerts will be triggered instantly upon entry or exit order execution.

-----

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

Momentum Quality Index Strategyfiles.fm

Welcome to the Momentum Quality Index Strategy!

This is a fairly conservative strategy with a sharp criteria for entries and taking profits. This strategy has been tested amongst the top 50 stocks with volatility over 2%, and the verdict was that the profitability was often times over 85% profitability, often times reaching over 90% profitability. This strategy thrives in more volatile environments, often times beating the buying and holding strategy YTD performance by large margins.

This strategy is highly optimized for the 30 minute chart, giving insights into shorter term movements. It is based on cash trades of $1,000 per position, with a maximum of 4 trades being placed at once.

This strategy is optimized for common stock trading in more liquid markets, and not yet optimized for options trading (however I plan on developing highly profitable strategies for this purpose soon). The take profit is customizable.

I would refer to the image link I have posted at the top of this article for the strategy's effectiveness. The strategy report on this article isn't accurate, as this strategy is based on trading $1,000 per trade, therefore over longer term periods of time will not be as successful due to the fact that there is no compounding. However, over the course of smaller time frames (such as one year), it beats buying and holding of many assets.

This strategy is meant for day trading and short term swing trading, and is not meant to beat buying and holding of successful assets over the course of long periods of time.

DCA-Integrated Trend Continuation StrategyIntroducing the DCA-Integrated Trend Continuation Strategy 💼💰

The DCA-Integrated Trend Continuation Strategy represents a robust trading methodology that harnesses the potential of trend continuation opportunities while seamlessly incorporating the principles of Dollar Cost Averaging (DCA) as a risk management and backup mechanism. This strategy harmoniously blends these two concepts to potentially amplify profitability and optimize risk control across diverse market conditions.

This strategy is well-suited for both trending and ranging markets. During trending markets, it aims to capture and ride the momentum of the trend while optimizing entry points. In ranging markets or pullbacks, the DCA feature comes into play, allowing users to accumulate more assets at potentially lower prices and potentially increase profits when the market resumes its upward trend. This cohesive approach not only enhances the overall effectiveness of the strategy but also fosters a more resilient and adaptable trading approach in ever-changing market dynamics.

💎 How it Works:

▶️ The strategy incorporates a customizable entry signal based on candlestick patterns, enabling the identification of potential trend continuation opportunities. By focusing on consecutive bullish candles, it detects the presence of bullish momentum, indicating an optimal time to enter a long position.

To refine the precision of the signals, traders can set a specific percentage threshold for the closing price of the candle, ensuring it is above a certain percentage of its body. This condition verifies strong bullish momentum and confirms significant upward movement within the candle, thereby increasing the reliability of the signal.

In addition, the strategy offers further confirmation by examining the relationship between the closing price of the signal candle and its previous candles. If the closing price of the signal candle is higher than its preceding candles, it provides an additional layer of assurance before entering a position. This approach is particularly effective in detecting sharp movements and capturing significant price shifts, as it focuses on identifying instances where the closing price shows clear strength and outperforms the previous candle's price action. By prioritizing such occurrences, the strategy aims to capture robust trends and capitalize on notable market movements.

▶️ During market downturns, the strategy incorporates intelligent management of price drops, offering flexibility through fixed or customizable price drop percentages. This unique feature allows for additional entries at specified drop percentages, enabling traders to accumulate positions at more favorable prices.

By strategically adjusting the custom price drop percentages, you can optimize your entry points to potentially maximize profitability. Utilizing lower percentages for initial entries takes advantage of price fluctuations, potentially yielding higher returns. On the other hand, employing higher percentages for final entries adopts a more cautious approach during significant market downturns, emphasizing enhanced risk management. This adaptive approach ensures that the strategy effectively navigates challenging market conditions while seeking to optimize overall performance.

▶️ To enhance performance and mitigate risks, the strategy integrates average purchase price management. This feature dynamically adjusts the average buy price percentage decrease after each price drop, expediting the achievement of the target point even in challenging market conditions. By reducing recovery times and ensuring investment safety, this strategy optimizes outcomes for traders.

▶️ Risk management is at the core of this strategy, prioritizing the protection of capital. It incorporates an account balance validation mechanism that conducts automatic checks prior to each entry, ensuring alignment with available funds. This essential feature provides real-time insights into the affordability of price drops and the number of entries, enabling traders to make informed decisions and maintain optimal risk control.

▶️ Furthermore, the strategy offers take profit options, allowing traders to secure gains by setting fixed percentage profits from the average buy price or using a trailing target. Stop loss protection is also available, enabling traders to set a fixed percentage from the average purchase price to limit potential losses and preserve capital.

▶️ This strategy is fully compatible with third-party trading bots, allowing for easy connectivity to popular trading platforms. By leveraging the TradingView webhook functionality, you can effortlessly link the strategy to your preferred bot and receive accurate signals for position entry and exit. The strategy provides all the necessary alert message fields, ensuring a smooth and user-friendly trading experience. With this integration, you can automate the execution of trades, saving time and effort while enjoying the benefits of this powerful strategy.

🚀 How to Use:

To effectively utilize the DCA-Integrated Trend Continuation Strategy, follow these steps:

1. Choose your preferred DCA Mode - whether by quantity or by value - to determine how you want to size your positions.

2. Customize the entry conditions of the strategy to align with your trading preferences. Specify the number of consecutive bullish candles, set a desired percentage threshold for the close of the signal candle relative to its body, and determine the number of previous candles to compare with.

3. Adjust the pyramiding parameter to suit your risk tolerance and desired returns. Whether you prefer a more conservative approach with fewer pyramids or a more aggressive stance with multiple pyramids, this strategy offers flexibility.

4. Personalize the price drop percentages based on your risk appetite and trading strategy. Choose between fixed or custom percentages to optimize your entries in different market scenarios.

5. Configure the average purchase price management settings to control the percentage decrease in the average buy price after each price drop, ensuring it aligns with your risk tolerance and strategy.

6. Utilize the account balance validation feature to ensure the strategy's actions align with your available funds, enhancing risk management and preventing overexposure.

7. Set take profit options to secure your gains and implement stop loss protection to limit potential losses, providing an additional layer of risk management.

8. Use the date and time filtering feature to define the duration during which the strategy operates, allowing for specific backtesting periods or integration with a trading bot.

9. For automated trading, take advantage of the compatibility with third-party trading bots to seamlessly integrate the strategy with popular trading platforms.

By following these steps, traders can harness the power of the DCA-Integrated Trend Continuation Strategy to potentially maximize profitability and optimize their trading outcomes in both trending and ranging markets.

⚙️ User Settings:

To ensure the backtest result is representative of real-world trading conditions, particularly in the highly volatile Crypto market, the default strategy parameters have been carefully selected to produce realistic results with a conservative approach. However, you have the flexibility to customize these settings based on your risk tolerance and strategy preferences, whether you're focusing on short-term or long-term trading, allowing you to potentially achieve higher profits. The backtesting was conducted using the BTCUSDT pair in 15-minute timeframe on the Binance exchange. Users can configure the following options:

General Settings:

- Initial Capital (Default: $10,000)

- Currency (Default: USDT)

- Commission (Default: 0.1%)

- Slippage (Default: 5 ticks)

Order Size Management:

- DCA Mode (Default: Quantity)

- Order Size in Quantity (Default: 0.01)

- Order Size in Value (Default: $300)

Strategy's Entry Conditions:

- Number of Consecutive Bullish Candles (Default: 3)

- Close Over Candle Body % (Default: 50% - Disabled)

- Close Over Previous Candles Lookback (Default: 14 - Disabled)

- Pyramiding Number (Default: 30)

Price Drop Management:

- Enable Price Drop Calculations (Default: Enabled)

- Enable Current Balance Check (Default: Enabled)

- Price Drop Percentage Type (Default: Custom)

- Average Price Move Down Percentage % (Default: 50%)

- Fixed Price Drop Percentage % (Default: 0.5%)

- Custom Price Drop Percentage % (Defaults: 0.5, 0.5, 0.5, 1, 3, 5, 5, 10, 10, 10)

TP/SL:

- Take Profit % (Default: 3%)

- Stop Loss % (Default: 100%)

- Enable Trailing Target (Default: Enabled)

- Trailing Offset % (Default: 0.1%)

Backtest Table (Default: Enabled)

Date & Time:

- Date Range Filtering (Default: Disabled)

- Start Time

- End Time

Alert Message:

- Alert Message for Enter Long

- Alert Message for Exit Long

By providing these customizable settings, the strategy allows you to tailor it to your specific needs, enhancing the adaptability and effectiveness of your trading approach.

🔐 Source Code Protection:

The source code of the DCA-Integrated Trend Continuation Strategy is designed to be robust, reliable, and highly efficient. Its original and innovative implementation merits protecting the source code and limiting access, ensuring the exclusivity of this strategy. By safeguarding the code, the integrity and uniqueness of the strategy are preserved, giving users a competitive edge in their trading activities.

Crypto Scalping Strategy by SAIFOverview

An optimized scalping strategy designed for cryptocurrency markets, focusing on breakout opportunities with strict risk controls and optional safe compounding features. This strategy combines price action, volume analysis, and multi-timeframe trend confirmation.

Key Features

Breakout Detection System

Identifies significant price breakouts using dynamic channel analysis

Confirms breakouts with volume surge validation

Filters trades based on multi-timeframe trend alignment

Multi-Timeframe Trend Confirmation

Analyzes 1-hour and 4-hour timeframes for trend direction

Only takes trades aligned with higher timeframe trends

Uses long-term moving averages for trend validation

Advanced Risk Management

Conservative default risk: 1% per trade

ATR-based stop-loss placement (2x ATR)

Trailing stop mechanism to protect profits

Minimum profit target before trailing activates

Built-in position sizing based on account equity

Safe Capital Management Options

Fixed Capital Mode: Trade with consistent position sizes

Safe Compounding Mode: Gradually scales position size based on realized profits only

Drawdown Protection: 80% equity floor prevents excessive capital erosion

Leverage Control: 10x leverage factored into position calculations

Technical Filters

Momentum confirmation via oscillator conditions

Directional movement analysis

Volume threshold requirements

Trend strength validation

Position Sizing

The strategy automatically calculates position sizes based on:

Your specified risk percentage

Current ATR volatility

Available leverage

Account equity (with optional compounding)

Trade Management

Entry: Executes on confirmed breakouts with volume and trend alignment

Stop Loss: Placed at 2x ATR from entry

Take Profit: Uses trailing stops that activate after minimum profit threshold

Exit: Automatically managed through strategy exits

Customization Options

Adjustable channel length for breakout detection

Configurable volume multiplier for surge detection

Customizable oscillator thresholds

Flexible ATR period for volatility measurement

Optional compounding vs. fixed capital modes

Adjustable trailing stop parameters

Visual Features

Channel boundaries plotted on chart

Entry signals marked with arrows

Background coloring indicates trend direction

Real-time info table shows:

Current risk level

Compounding status

Capital values

Drawdown protection status

Alert Capabilities

Built-in alert conditions for:

Buy signals (breakout opportunities)

Sell signals (breakdown opportunities)

Important Disclaimers

⚠️ Educational Purpose Only: This strategy is provided for educational and research purposes. It is not investment advice.

⚠️ High-Risk Trading: Scalping and leverage trading carry substantial risk of loss. Cryptocurrency markets are highly volatile.

⚠️ Not Financial Advice: This tool does not constitute financial, investment, or trading advice. Always conduct your own research and consult qualified professionals.

⚠️ Leverage Warning: This strategy uses 10x leverage, which can amplify both gains and losses significantly.

⚠️ Backtesting Limitations: Past performance does not guarantee future results. Real trading involves slippage, execution delays, and emotional factors not present in backtesting.

⚠️ Capital at Risk: Only trade with capital you can afford to lose completely. Never trade with borrowed money or funds needed for living expenses.

Commission & Fees

Commission: 0.13% per trade

Initial capital: $100 (default)

Commission costs are factored into backtest results

Best Practices

Start Small: Begin with minimum capital and conservative risk settings

Test Thoroughly: Backtest across different market conditions and timeframes

Monitor Performance: Track win rate, profit factor, and maximum drawdown

Adjust Parameters: Optimize settings for your specific trading pairs

Use Alerts: Set up notifications to avoid missing opportunities

Manage Emotions: Follow the strategy rules consistently without override

Recommended Markets

High liquidity cryptocurrency pairs (BTC, ETH major pairs)

Assets with clear trending behavior

Markets with sufficient volume for scalping

Timeframes: 1H to 4H charts recommended

Risk Reminder

Scalping requires:

Quick decision-making

Tight risk management

Consistent discipline

Understanding of market microstructure

Proper capitalization

Always practice proper risk management. The strategy includes safety features, but no system can eliminate trading risk entirely. Trade responsibly.

Long Term Profitable Swing | AbbasA Story of a Profitable Swing Trading Strategy

Imagine you're sailing across the ocean, looking for the perfect wave to ride. Swing trading is quite similar—you're navigating the stock market, searching for the ideal moments to enter and exit trades. This strategy, created by Abbas, helps you find those waves and ride them effectively to profitable outcomes.

🌊 Finding the Perfect Wave (Entry)

Our journey begins with two simple signs that tell us a great trading opportunity is forming:

- Moving Averages: We use two lines that follow price trends—the faster one (EMA 16) reacts quickly to recent price moves, and the slower one (EMA 30) gives us a longer-term perspective. When the faster line crosses above the slower line, it's like a clear signal saying, "Hey! The wave is rising, and prices might move higher!"

- RSI Momentum: Next, we check a tool called the RSI, which measures momentum (how strongly prices are moving). If the RSI number is above 50, it means there's enough strength behind this rising wave to carry us forward.

When both signals appear together, that's our green light. It's time to jump on our surfboard and start riding this promising wave.

⚓ Safely Riding the Wave (Risk Management)

While we're riding this wave, we want to ensure we're safe from sudden surprises. To do this, we use something called the Average True Range (ATR), which measures how volatile (or bumpy) the price movements are:

- Stop-Loss: To avoid falling too hard, we set a safety line (stop-loss) 8 times the ATR below our entry price. This helps ensure we exit if the wave suddenly turns against us, protecting us from heavy losses.

- Take Profit: We also set a goal to exit the trade at 11 times the ATR above our entry. This way, we capture significant profits when the wave reaches a nice high point.

🌟 Multiple Rides, Bigger Adventures

This strategy allows us to take multiple positions simultaneously—like riding several waves at once, up to 5. Each trade we make uses only 10% of our trading capital, keeping risks manageable and giving us multiple opportunities to win big.

🗺️ Easy to Follow Settings

Here are the basic settings we use:

- Fast EMA**: 16

- Slow EMA**: 30

- RSI Length**: 9

- RSI Threshold**: 50

- ATR Length**: 21

- ATR Stop-Loss Multiplier**: 8

- ATR Take-Profit Multiplier**: 11

These settings are flexible—you can adjust them to better suit different markets or your personal trading style.

🎉 Riding the Waves of Success

This simple yet powerful swing trading approach helps you confidently enter trades, clearly know when to exit, and effectively manage your risk. It’s a reliable way to ride market waves, capture profits, and minimize losses.

Happy trading, and may you find many profitable waves to ride! 🌊✨

Please test, and take into account that it depends on taking multiple longs within the swing, and you only get to invest 25/30% of your equity.

Trend Follower Intraday [ Adjustable TF ]Trend Follower Intraday for 3 minute Time-Frame (Adjustable) , that has the time condition for Indian Markets as well.

Unlike the Free Scripts - Risk Management , Position Sizing , Partial Exit etc. are also included .

Send us a Message to know more about the strategy.

// ══════════════════════════════════════════════════════════════════════════ //

The Timing can be changed to fit other markets, scroll down to "TIME CONDITION" to know more.

The commission is also included in the strategy .

The basic idea is when ,

1) EMA1 crosses above EMA2 , is a Long condition .

2) EMA1 crosses below EMA2 , is a Short condition .

3) Green Section indicates Long position.

4) Red Section indicates Short position.

5) Allowed hours specifies the trade entry timing.

6) ATR STOP is the stop-loss value on chart , can be adjusted in INPUTS.

7) Target 1 is the 1st target value on chart , can be adjusted in INPUTS.

8) RISK is Maximum Risk per trade for the intraday trade can be changed .

9) Total Capital used can be adjusted under INPUTS.

10) ATR TRAIL is used for trailing after entry, as mentioned in the inputs below.

11) Check trades under the list of trades .

12) Trade only in liquid stocks .

13) Risk only 1-5% of total capital.

14) Inputs can be changed for better back-test results, but also manually check the trades before setting alerts

15) SQUARE OFF TIME - As you change the time frame , also change the square-off time to the candle's closing time.

Eg: For 3min Time-frame , Hour = 2Hrs | Minute = 57min

16) Strategy stops for the day if you have a loss .

17) COMMISSION value is set to 20Rs and SLIPPAGE value is set to 2 . Go to properties to change it .

*The input values and the results are mentioned under "BACKTEST RESULTS" below*

// ══════════════════════════════ //

// ————————> RISK MANAGEMENT <——————— //

// ══════════════════════════════ //

Risk management is done based on max loss per trade and can be adjusted in the INPUTS.

// ═══════════════════════════ //

// ————————> POSITION SIZE <——————— //

// ═══════════════════════════ //

Quantity of each trade is different based on the loss

// ═════════════════════════ //

// ————————> PROPERTIES <——————— //

// ═════════════════════════ //

COMMISSION , SLIPPAGE ,RECALCULATE is already mentioned in the code.

COMMISSION can be charges , based on the broker charges.

// ═══════════════════════════════//

// ————————> TIME CONDITION <————————— //

// ═══════════════════════════════//

The time can be changed in the INPUT.

The Indian Markets open at 9:15am and closes at 3:30pm.

The 'Allowed hours' under Inputs specifies the time at which Entries should happen .

"Close All" function closes all the trades before 3pm , at the open of the next candle.

To change the time to close all trades , check INPUT.

All open trades get closed by 3pm , because some brokers don't allow you to place fresh intraday orders after 3pm .

// ═══════════════════════════════════════════════ //

// ————————> BACKTEST RESULTS ( 123 CLOSED TRADES ) <————————— //

// ═══════════════════════════════════════════════ //

INPUTS can be changed for better Back-Test results.

The strategy applied to NSE:JSWENERGY (3 min Time-Frame and with a capital of 3,00,000 ) gives us 81% profitability , as shown below

It was tested for a period a 6 months with a Profit Factor of 1.957 ,net Profit of 43,000Rs .

Sharpe Ratio = 0.745

Sortino Ratio = 2.091

No strategy in the world promises 100% profits in all market conditions , so always define your risk before trading.

Also check Back-Test results manually ,before setting Alerts

The Graph has a Linear Curve with Consistent Profits.

The INPUTS are as follows,

1) EMA1 ————————————————> 38

2) EMA2 ————————————————> 118

3) ALLOWED HRS ———————————> 9:35 TO 14:30

4) ATR STOP ——————————————> 3.2

5) RISK ——————————————————> 3000

6) ATR TRAIL ———————————————> 2.6

7) TARGET 1 ————————————————> 2.4

8) MAX POSITION VALUE ——————————> 3,00,000

8) MAX DRAWDOWN —————————————> 9,000

8) SQUARE-OFF ————————————————> 14:57

NSE:JSWENERGY

Apply it to your charts Now !

NSE:JSWENERGY

Send us a message for FREE TRIALS | Instant Access

Thank You ☺

CONSOLIDATION BAND BREAKOUT [5MIN TF]CONSOLIDTION BREAKOUT STRATEGY for 5 minute Time-Frame , that has the time condition adjustable for Indian Markets.

// ══════════════════════════════════════════════════════════════════════════ //

Unlike the Free Scripts - Risk Management , Position Sizing , Partial Exit etc. are also included .

Message to know more about the strategy.

// ══════════════════════════════════════════════════════════════════════════ //

The Timing can be changed to fit other markets, scroll down to "TIME CONDITION" to know more.

The commission is also included in the strategy .

The basic idea is when ,

1) Price crosses above upper Level ,indicated by Red Line, is a Long condition .

2) Price crosses below lower Level ,indicated by Green Line , is a Short condition .

3) Candle close crosses above ema1 , is a part of the Long condition .

4) Candle close crosses below ema1 , is a part of the Short condition .

5) Allowed hours specifies the trade entry timing.

6) ATR STOP is the stop-loss value on chart , can be adjusted in INPUTS.

7) Target 1 is the 1st target value on chart , can be adjusted in INPUTS.

8) RISK is Maximum Risk per trade for the intraday trade can be changed .

9) Total Capital used can be adjusted under INPUTS.

10) ATR TRAIL is used for trailing after entry, as mentioned in the inputs below.

11) Check trades under the list of trades .

12) Trade only in liquid stocks .

13) Risk only 1-5% of total capital.

14) Inputs can be changed for better back-test results, but also manually check the trades before setting alerts

15) SQUARE OFF TIME - As you change the time frame , also change the square-off time to that candle's closing time.

Eg: For 3min Time-frame , Hour = 2Hrs | Minute = 57min

16) Strategy stops for the day if you have a loss .

*The input values and the results are mentioned under "BACKTEST RESULTS" below*

// ══════════════════════════════ //

// ————————> RISK MANAGEMENT <——————— //

// ══════════════════════════════ //

Risk management is done based on max loss per trade and can be adjusted in the INPUTS.

// ═══════════════════════════ //

// ————————> POSITION SIZE <——————— //

// ═══════════════════════════ //

Quantity of each trade is different based on the loss

// ═════════════════════════ //

// ————————> PROPERTIES <——————— //

// ═════════════════════════ //

COMMISSION , SLIPPAGE ,RECALCULATE is already mentioned .

COMMISSION can be charges , based on the broker charges.

// ═══════════════════════════════//

// ————————> TIME CONDITION <————————— //

// ═══════════════════════════════//

The time can be changed in the INPUT.

The Indian Markets open at 9:15am and closes at 3:30pm.

The 'Allowed hours' under Inputs specifies the time at which Entries should happen .

"Close All" function closes all the trades before 3pm , at the open of the next candle.

To change the time to close all trades , check INPUT.

All open trades get closed at 3pm , because some brokers don't allow you to place fresh intraday orders after 3pm .

// ═══════════════════════════════════════════════ //

// ————————> BACKTEST RESULTS ( 123 CLOSED TRADES )<————————— //

// ═══════════════════════════════════════════════ //

INPUTS can be changed for better Back-Test results.

The strategy applied to NSE:TCS (5 min Time-Frame and with a capital of 1,00,000 ) gives us 77% profitability , as shown below

It was tested for a period a 1 year with a Profit Factor of 2.143 ,net Profit of 10,886 Rs .

The Initial Capital and Risk can be increased for better results.

The graph has a Linear Curve with Consistent Profits.

The INPUTS are as follows,

1) LENGTH ——————————————> 79

2) MUT_STDEV ————————————> 2.3

3) ALLOWED HRS ———————————> 9:25 TO 14:30

4) ATR STOP ——————————————> 2.2

5) RISK ——————————————————> 400

6) ATR TRAIL ———————————————> 2.6

7) TARGET 1 ————————————————> 2.1

8) MAX POSITION VALUE ——————————> 1,00,000

8) MAX DRAWDOWN —————————————> 2,000

8) SQUARE-OFF ————————————————> 14:55

NSE:TCS

Apply it to your charts Now !!

Send us a message to know more about this strategy

Thank You ☺ NSE:TCS

Omni Trader Accompanying Backtesting StrategyVersion 1.0

Purpose

This backtesting strategy indicator is a accompanying tool for use with my popular trading and alert indicator: Omni Trader | RMI EMA RSI VOL | Margin Focused Indicator

Reference Indicator Link:

Features

This strategy has been programmed to act exactly how the accompanying indicator would be used with an automated strategy such as Autoview or through manual trading