Average Daily Range TrackerAverage Daily Range Tracker

This indicator helps you measure volatility in real time by tracking the Average Daily Range (ADR) and comparing it to the current day’s price action.

🔑 Features

Calculates the ADR over a user-defined lookback period (default = 14 days).

Displays today’s developing range (High–Low) as the session unfolds.

Shows what % of the ADR has already been consumed intraday.

Visual progress bar makes it easy to see how close today is to its historical average range.

Optional ADR plot available in a separate pane.

📈 How traders use it

Spot when a market has already made its “typical” daily move.

Adjust intraday trade expectations: avoid chasing after the bulk of the move is done.

Use % of ADR consumed as a volatility filter for setups.

Combine with support/resistance to identify exhaustion zones.

⚙️ Customization

Lookback length for ADR calculation.

Progress bar size and color.

Optional toggle to plot ADR in its own panel.

Cerca negli script per "range"

Renko Open Range delta

Delta Renko-Style Indicator Guide (NQ Focus)

This indicator takes inspiration from the Renko Chart concept and is optimized for the RTH session (New York time zone), specifically applied to the Nasdaq futures (NQ) product.

If you’re unfamiliar with Renko charts, it may help to review their basics first, as this indicator borrows their clean, block-based perspective to simplify price interpretation.

⸻

🔧 How the Indicator Works

• At market open (9:30 AM EST), the indicator plots a horizontal open price line, referred to as 0 delta.

• From this anchor, it plots 10 incremental levels (deltas) both above and below the open, each spaced by 62.5 NQ points.

Why 62.5?

• With NQ currently trading in the 23,000–24,000 range, a 62.5-point move represents roughly 0.26% of the daily average range.

• This makes each delta step significant enough to capture movement while filtering out smaller noise.

A mini table (location adjustable) displays:

• Current delta zone

• Last touched delta level

This gives you a quick snapshot of where price sits relative to the open.

⸻

📈 How to Read the Market

• At the open, price typically oscillates between 0 and +1 / -1 delta.

• A break beyond this zone often signals stronger directional intent:

• Trending day: price can push into +2, +3, +4, +5 (or the inverse for downside).

• Range day: expect price to bounce between +1, 0, -1 deltas.

⚠️ Note: This is a visualization tool, not a trading system. Its purpose is to help you quickly recognize range vs. trend conditions.

⸻

📊 Example

• In this case, NQ reached +1 delta shortly after open.

• A retest of 0 delta followed, and price later surged to +5/+6 deltas (helped by Fed news).

⸻

🛠️ Practical Uses

This indicator can help you:

• Define profit targets

• Place hard stop levels

• Gauge whether a counter-trend trade is worth the risk

⚠️ Caution: Avoid counter-trend trades if price is aggressively pushing toward +5/+6 or -5/-6 deltas, as trend exhaustion usually hasn’t set in yet.

⸻

🔄 Adapting for ES (S&P Futures)

• On NQ, 62.5 points ≈ $1,250 per contract.

• For ES, this translates to 25 points.

• Since 1 NQ contract ≈ 2 ES contracts in dollar terms, an optimized ES delta step would be 12.5 points.

You may also experiment with different delta values (e.g., 50 or 31.25 for NQ) to align with your risk profile and trading style.

⸻

🧪 Extending Beyond NQ

You can experiment with applying this indicator to ES or even stocks, but non-futures assets may require additional calibration and testing.

⸻

✅ Bottom line: This tool provides a clean, Renko-inspired framework for quickly gauging trend vs. range conditions, setting realistic profit targets, and avoiding poor counter-trend setups.

Major Lows OscillatorDescription

The Major Lows Oscillator is a custom technical indicator designed to identify significant low-price areas by normalizing the current closing price relative to recent lowest lows and highest highs. The oscillator calculates a normalized price percentage over a configurable lookback period, applies exponential moving averages for smoothing, and inverts the result to highlight potential market bottoms.

Calculation Details

Lowest Low Lookback : Finds the lowest low over a user-defined period (default 100 bars).

Highest High Lookback : Calculates the highest high over a short period (default 1 bar), providing a dynamic normalization range.

Normalization : Normalizes the current close within the range defined by the lowest low and highest high, scaled to 0-100.

Smoothing : Applies a 10-period EMA, inversion, and weighted smoothing combining the last valid value and current oscillator reading.

Final Output : Applies a final EMA (period 1) and inverts the oscillator (100 - value) to emphasize major lows.

Features

Customizable midline level for signal alerts (default 50).

Visual midline reference line.

Alerts trigger on oscillator crossing below midline for automated monitoring.

Usage

Useful for complementing existing setups or integration in algorithmic trading strategies.

Changing the input parameters opens new ways to leverage the asymmetric range concept, allowing adaptation to different market regimes and enhancing the oscillator’s sensitivity and utility.

Examples of input combinations and their potential purposes include:

Extremely Asymmetric Setting: Lowest Low Lookback = 200, Highest High Lookback = 1

Focuses on deep long-term lows contrasted with immediate highs, ideal for spotting strong oversold levels within an otherwise bullish short-term momentum.

Symmetric Lookbacks: Lowest Low Lookback = Highest High Lookback = 50

Balances the range equally, creating a normalized oscillator that treats recent lows and highs with the same weight — useful for markets with balanced volatility.

Short but Equal Lookbacks: Lowest Low Lookback = Highest High Lookback = 10

Highly sensitive to recent price swings, this setting can detect rapid shifts and is suited for intraday or very short-term trading.

Inverted Extreme: Lowest Low Lookback = 1, Highest High Lookback = 100

Highlights very recent lows against a long-term high range, possibly signaling quick dips in a generally overextended market.

Inputs

Midline Level : Threshold for alerts (default 50).

Lowest Low Lookback Period : Bars evaluated for lowest low (default 100).

Highest High Lookback Period : Bars evaluated for highest high (default 1).

Alerts

Configured to trigger once per bar close when the oscillator crosses below the midline level.

---

Disclaimer

This indicator is for educational and analytical use only.

Dr. Fib - FGBAB - Open Range Breakout for Stocks V1.0This Open Range Breakout Indicator (ORB) helps your discretionary trading when looking for breakouts on the 15 mins range.

This indicator helps your discretionary trading by allowing visual settings that helps discretionary trades to make faster decisions.

It will provide you will the following on-screen information:

- ORB HIGH and LOW: The Open Range Breakout set by the input parameters, for example the first 15 mins RTH Open from 9:30 to 6:45.-

- ORB MID: The ORB mid point for reference, generally the price tends to return and bounce from the 50% ORB.

Reward to Risk posible targets for LONG and SHORT trades: This will provide target value references, it is based on the ORB Risk from high to low, you have 1:1, 2:1, 3:1 and 4:1 possible targets in both directions.

Reference table:

The reference table is a visual setting for you to have at first sight important information before considering getting into the trade:

- ORB HIGH and LOW.

- Risk in points.

- Risk in USD.

- Amount of shares considering the MaxRisk input parameter you select.

- The current LIVE R:R based on the entry, if price is abobe ORB High it will simulate a LONG position is price is below the ORB Low it will simulate a SHORT position,

- The LIVE profit simulation based on the above.

- MaxRunUP, the highest equity the trade simulation has produced.

Direction: The current trade direction simulation based on the ORB HIGH or ORB LOW.

Keep in mind this indicator is a "gauge" a visual help for discretionary traders that like to trade Open Range Breakout strategy.

It will reset the ORB at RTH Close and build a new ORB at next calendar day based in the ORB time you have selected by the input parameters.

Please feel free to use in your own trading at your discretion.

Price Range Tracker by smaPrice Range Tracker by sma helps traders quickly visualize the current price’s position within a custom price range.

It calculates and displays the highest, lowest, and average price levels over a user-defined period (default: 50 bars).

What it does:

Draws dynamic horizontal lines for the maximum, average, and minimum price levels within the chosen period.

Shows labels next to each level, indicating how far they are from the current price in percentage terms.

Helps traders spot overbought/oversold conditions and potential range breakouts.

How to use:

Adjust the period to fit your timeframe and asset volatility.

Use the percentage distances to assess potential upside/downside from the current price.

Combine with your existing trend or reversal strategies for clearer decisions.

Colors and label distance can be customized to match your chart style.

Opening Range Breakout🧭 Overview

The Open Range Breakout (ORB) indicator is designed to capture and display the initial price range of the trading day (typically the first 15 minutes), and help traders identify breakout opportunities beyond this range. This is a popular strategy among intraday and momentum traders.

🔧 Features

📊 ORB High/Low Lines

Plots horizontal lines for the session’s high and low

🟩 Breakout Zones

Background highlights when price breaks above or below the range

🏷️ Breakout Labels

Text labels marking breakout events

🧭 Session Control

Customizable session input (default: 09:15–09:30 IST)

📍 ORB Line Labels

Text labels anchored to the ORB high and low lines (aligned right)

🔔 Alerts

Configurable alerts for breakout events

⚙️ Adjustable Settings

Show/hide background, labels, session window, etc.

⏱️ Session Logic

• The ORB range is calculated during a defined session window (default: 09:15–09:30).

• During this window, the highest high and lowest low are recorded as ORB High and ORB Low.

📈 Breakout Detection

• Breakout Above: Triggered when price crosses above the ORB High.

• Breakout Below: Triggered when price crosses below the ORB Low.

• Each breakout can trigger:

• A background highlight (green/red)

• A text label (“Breakout ↑” / “Breakout ↓”)

• An optional alert

🔔 Alerts

Two built-in alert conditions:

1. Breakout Above ORB High

• Message: "🔼 Price broke above ORB High: {{close}}"

2. Breakout Below ORB Low

• Message: "🔽 Price broke below ORB Low: {{close}}"

You can create alerts in TradingView by selecting these from the Add Alert window.

📌 Best Use Cases

• Intraday momentum trading

• Breakout and scalping strategies

• First 15-minute range traders (NSE, BSE markets)

Weekly Range PlotterThe Weekly Range Plotter is a dynamic market structure tool designed to help traders visualize critical high and low levels from specific days of the week and the previous week's range. It provides key visual anchors to support analysis of market behavior, including range compression/expansion and directional bias.

Candle Range % vs 8-Candle AvgCandle % Indicator – Measure Candle Strength by Range %

**Overview:**

The *Candle % Indicator* helps traders visually and analytically gauge the strength or significance of a price candle relative to its recent historical context. This is particularly useful for detecting breakout moves, volatility shifts, or overextended candles that may signal exhaustion.

**What It Does:**

* Calculates the **percentage range** of the current candle compared to the **average range of the past N candles**.

* Highlights candles that exceed a user-defined threshold (e.g., 150% of the average range).

* Useful for **filtering out extreme candles** that might represent anomalies or unsustainable moves.

* Can be combined with other strategies (like EMA crossovers, support/resistance breaks, etc.) to improve signal quality.

**Use Case Examples:**

***Filter out fakeouts** in breakout strategies by ignoring candles that are overly large and may revert.

***Volatility control**: Avoid entries when market conditions are erratic.

**Confluence**: Combine with EMA or RSI signals for refined entries.

**How to Read:**

* If a candle is larger than the average range by more than the set percentage (default 150%), it's flagged (e.g., no entry signal or optional visual marker).

* Ideal for intraday, swing, or algorithmic trading setups.

**Customizable Inputs:**

**Lookback Period**: Number of previous candles to calculate the average range.

**% Threshold**: Maximum percentage a candle can exceed the average before being filtered or marked.

Oculus Quantum RangeOculus Quantum Range

The Oculus Quantum Range is a sophisticated indicator designed to track dynamic support and resistance levels, based on market volatility and price action. It uses the Average True Range (ATR) to define a dynamic range, giving traders powerful breakout and breakdown targets for more informed decision-making.

Key Features:

Dynamic Support & Resistance Levels: The indicator calculates key dynamic levels using the highest high and lowest low over a user-defined period (default: 20 bars). These levels adjust according to market volatility, helping to reflect current market conditions.

Breakout & Breakdown Targets: The system calculates breakout and breakdown targets based on the ATR, adding flexibility to the classic support and resistance levels. The targets are plotted above and below the dynamic range.

Volume Confirmation: The breakout and breakdown targets are confirmed when there is a spike in volume, enhancing the reliability of these trade signals.

Pivot Levels: The middle level (pivot) is plotted as the average of the highest high and the lowest low over the range period, offering an additional reference point for traders.

How to Use:

Breakout Entry:

When the price crosses above the Dynamic Top Line (Resistance), a breakout is considered. The breakout target is calculated and plotted above the resistance level.

A confirmed breakout is when the price crosses the resistance with volume higher than the 20-period volume average.

Breakdown Entry:

When the price crosses below the Dynamic Bottom Line (Support), a breakdown is considered. The breakdown target is calculated and plotted below the support level.

A confirmed breakdown is when the price crosses the support with volume higher than the 20-period volume average.

Pivot Zone:

The middle level (pivot) acts as a reference zone, showing potential areas where price action may pause or reverse before continuing toward breakout or breakdown targets.

Alert Conditions:

Breakout Alert: Triggered when the price crosses above the dynamic top line (resistance).

Breakdown Alert: Triggered when the price crosses below the dynamic bottom line (support).

Visualization:

The Dynamic Top Line (Resistance) is plotted in red.

The Middle Level (Pivot) is plotted in blue.

The Dynamic Bottom Line (Support) is plotted in green.

Breakout Targets are plotted in purple above the resistance, and Breakdown Targets are plotted in orange below the support.

Confirmed Breakout/Breakdown are marked with green and red lines respectively, and the background will change to green or red for a visual cue.

This indicator is perfect for traders looking to make timely decisions based on price action, volatility, and volume. It’s ideal for identifying potential breakout and breakdown opportunities with clear, dynamic targets.

Average Daily Range [Dova Lazarus]Title: Average Daily Range

Description:

The Average Daily Range (ADR) indicator by Mantique Capital is designed to help traders assess the potential volatility of a trading day. It calculates the average range between daily highs and lows over a user-defined period and plots projected high/low zones based on that range.

Key Features:

📊 Plots ADR-based high and low levels for the current day

🎯 Choose between bullish and bearish bias for level calculation

📈 Optional 30% to 90% intermediate levels with customizable style and color

🏷️ Display percentage labels showing distance in pips

🔁 Adjustable ADR period length and number of days displayed

This indicator is useful for determining how much price movement (volatility) to expect in a given trading day, making it an excellent tool for setting targets, managing risk, and identifying overextension zones.

Inspired by the popular "Best ADR Indicator for MT4"

Math by Thomas Swing RangeMath by Thomas Swing Range is a simple yet powerful tool designed to visually highlight key swing levels in the market based on a user-defined lookback period. It identifies the highest high, lowest low, and calculates the midpoint between them — creating a clear range for swing trading strategies.

These levels can help traders:

Spot potential support and resistance zones

Analyze price rejection near range boundaries

Frame mean-reversion or breakout setups

The indicator continuously updates and extends these lines into the future, making it easier to plan and manage trades with visual clarity.

🛠️ How to Use

Add to Chart:

Apply the indicator on any timeframe and asset (works best on higher timeframes like 1H, 4H, or Daily).

Configure Parameters:

Lookback Period: Number of candles used to detect the highest high and lowest low. Default is 20.

Extend Lines by N Bars: Number of future bars the levels should be projected to the right.

Interpret Lines:

🔴 Red Line: Swing High (Resistance)

🟢 Green Line: Swing Low (Support)

🔵 Blue Line: Midpoint (Mean level — useful for equilibrium-based strategies)

Trade Ideas:

Bounce trades from swing high/low zones.

Breakout confirmation if price closes strongly outside the range.

Reversion trades if price moves toward the midpoint after extreme moves.

Compression Patterns (w/ Trend + Proximity Filter)🧠 Description:

This indicator identifies high-probability price compression patterns within trending environments — a setup prized by experienced swing and day traders alike. It combines the classic NR4, NR7, 2-Bar NR, 3-Bar NR, and Inside Day formations with a powerful trend filter and proximity logic to deliver clear, focused signals.

🔍 What's Inside:

▪️ Compression Patterns

The core of this tool lies in the logic of price compression. These patterns signal the market taking a breath — volatility contracts, volume dries up, and price coils like a spring.

When this happens in the right context, the next move is often explosive.

NR4 / NR7: Narrowest range in 4 or 7 bars — excellent for spotting the quiet before the storm.

2-Bar NR / 3-Bar NR: These identify the tightest consecutive 2 or 3-day ranges over the past 20 days — contextually rare and powerful.

Inside Day: A simple but highly effective consolidation pattern, especially when it clusters around key moving averages.

▪️ Trend Filter (EMA Stack)

You could say this is where most indicators fall apart — no context.

This one doesn’t make that mistake.

Signals only fire when the 10 EMA > 20 EMA > 50 EMA, and price is above the 20 EMA. That’s a strong, established uptrend — the only environment where breakouts are statistically favourable.

Why?

Because trend following works.

It may not give you fixed daily returns, but it’s the only strategy with theoretically infinite profit potential. You risk little, trade less, and position yourself for rare but massive moves. That’s the edge.

▪️ Proximity Filter (1 ATR to EMA)

We’ve added another layer of discipline. Signals only fire when price is:

Within 1 ATR of the 10 EMA (if price is above it), or

Within 1 ATR of the 20 EMA (if price is below the 10 EMA)

This ensures you’re not chasing. You’re waiting for tight, controlled pullbacks into dynamic support — exactly where institutions add size, not exit.

⚙️ Fully Customisable:

Toggle visibility of each pattern

Custom colours and transparency for label & background

Adjustable ATR length and multiplier

Change label text if needed (useful for translations or tweaks)

🎯 Ideal Use Case:

Swing trading off the daily chart

Day trading with VWAP/MACD filters (in alternate versions)

Supplementing price action strategies

🔚 Final Word:

This isn’t an “everything scanner.”

It’s a discerning sniper scope for traders who wait patiently for clean trends, tight consolidations, and perfect proximity — then strike.

Max Price Range DeviationThis indicator measures how far a stock has moved in recent days relative to its typical movement over a longer period.

🧠 What it does:

Calculates the absolute price range (highest high − lowest low) over a recent number of days.

Compares this recent range to the average max range from rolling windows of the same size over a longer lookback period.

Plots:

✅ Recent Range (blue line)

✅ Average Historical Range (orange line)

✅ Ratio of Recent to Average (green line)

Highlights when recent movement is significantly higher than normal using a configurable threshold.

⚙️ Inputs:

Recent Period (days): Number of days to calculate the current price move.

Lookback Period (days): Number of days used to calculate the average historical range.

High Move Threshold (x avg): If the recent move exceeds this multiple of average, it's flagged.

🛠️ Use Cases:

Spot unusually large price swings.

Identify good opportunities to sell out-of-the-money options (e.g., covered calls or credit spreads) when moves are extended.

Avoid chasing late-stage breakouts.

Body Percentage of Range (Colored)Short Description:

This indicator measures the dominance of the candle's body relative to its total range (High - Low), providing a visual gauge of intra-candle strength versus indecision. Columns are colored based on whether the body constitutes more or less than a defined percentage (default 50%) of the candle's total height.

Detailed Description:

What it Does:

The "Body Percentage of Range" indicator calculates, for each candle, what percentage of the total price range (High minus Low) is occupied by the candle's body (absolute difference between Open and Close).

A value of 100% means the candle has no wicks (a Marubozu), indicating strong conviction during that period.

A value of 0% means the candle has no body (a Doji), indicating perfect indecision.

Values in between show the relative balance between the directional move (body) and the price exploration/rejection (wicks).

How to Interpret:

The indicator plots this percentage as columns:

Column Height: Represents the percentage of the body relative to the total range. Higher columns indicate a larger body dominance.

Column Color:

Green Columns: Appear when the body percentage is above the user-defined threshold (default 50%). This suggests that the directional move within the candle was stronger than the indecision (wicks). Often seen during trending moves or strong momentum candles.

Red Columns: Appear when the body percentage is at or below the user-defined threshold (default 50%). This suggests that wicks dominate the candle (body is 50% or less of the range), indicating significant indecision, struggle between buyers and sellers, or potential reversals. These are common in choppy, consolidating, or reversal market conditions.

Orange Line (Optional MA): A Simple Moving Average (SMA) of the body percentages is plotted to help smooth the readings and identify broader periods where candle structure indicates more trending (high MA) vs. ranging/indecisive (low MA) characteristics.

Potential Use Cases:

Identifying Choppy vs. Trending Markets: Sustained periods of low, predominantly red columns (and often a low/declining MA) can signal a choppy, range-bound market where trend-following strategies might underperform. Conversely, periods with frequent high, green columns suggest a more trending environment.

Confirming Breakouts/Momentum: High green columns appearing alongside increased volume during a breakout can add conviction to the move's strength.

Spotting Potential Exhaustion/Reversals: A very tall green column after a strong trend, followed immediately by a low red column (like a Doji or Spinning Top pattern appearing on the price chart), might signal potential exhaustion or a pending reversal, indicating indecision has suddenly entered the market.

Filtering Entries: Traders might avoid taking entries (especially trend-following ones) when the indicator shows a consistent pattern of low red columns, suggesting high market indecision.

Settings:

Color Threshold %: Allows you to set the percentage level above which columns turn green (default is 50%).

Smoothing MA Length: Adjusts the lookback period for the Simple Moving Average.

Disclaimer:

This indicator is a tool for technical analysis and should be used in conjunction with other methods (like price action, volume analysis, other indicators) and robust risk management. It does not provide direct buy/sell signals and past performance is not indicative of future results.

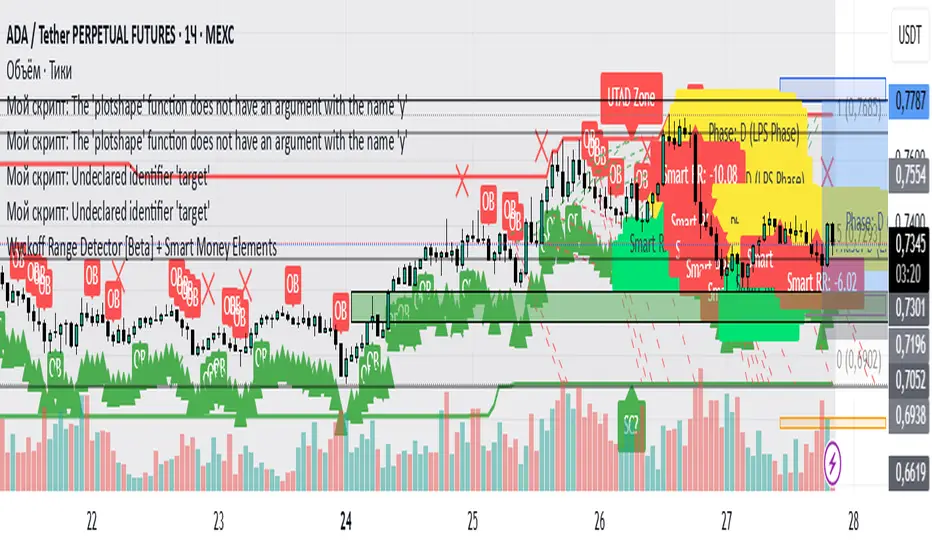

Wyckoff Range Detector [Beta] + Smart Money ElementsThis indicator detects the key phases of the Wyckoff market structure and integrates smart money elements, such as Order Blocks (OB), Fair Value Gaps (FVG), and Breaker Blocks. It also helps identify potential reversal zones (LPS, UTAD, Spring), breakout opportunities, and provides automatic Risk-Reward (R:R) calculations.

Key Features:

Wyckoff Phases Detection:

Automatically detects key phases of Wyckoff's market structure:

B (Range) – The initial range of accumulation.

C (Spring Phase) – Accumulation phase with a potential breakout.

C (UTAD Phase) – Upthrust After Distribution, indicating a potential reversal.

D (LPS Phase) – Last Point of Support, signaling accumulation before a breakout.

E (Breakout) – Phase marking breakout from range.

Re-Accumulation – Possible continuation in the range after a breakout.

Re-Distribution – Possible breakdown of a distribution phase.

Smart Money Elements:

Order Blocks (OB): Identifies Bullish and Bearish OBs to anticipate market entries.

Fair Value Gap (FVG): Highlights imbalance areas where price is likely to return.

Breaker Blocks: Marks areas where the price has previously broken a structure, indicating strong supply/demand zones.

Automatic Risk-Reward Calculation:

Smart RR: Automatically calculates Risk-Reward (R:R) ratios from LPS phases and Order Blocks. It draws lines to indicate target and stop levels with green for the target and red for the stop.

Visual representation of the entry signal with target and stop levels displayed.

Alerts:

Set alerts for phase changes, breakout, re-accumulation, or re-distribution to stay updated on the market’s movements.

Visual Tools:

Labels are used to indicate key zones such as AR, SC, LPS, and Spring Zones.

Draw boxes for the Spring and LPS phases to highlight areas where price action is likely to reverse.

Lines to represent potential breakouts, with customizable risk-reward indicators.

How to Use:

Apply the Indicator on any chart.

Identify Wyckoff phases to understand market trends.

Monitor Smart Money Elements (OB, FVG, Breaker) for entry and exit points.

Use automatic Risk-Reward levels for managing trades.

Set alerts for various Wyckoff phases and smart money signals to stay updated.

Custom Opening Range FillThis TradingView indicator visualizes a customizable opening range. Users define the start hour, minute (UTC), and range duration. It calculates the high and low prices within this period and fills the area between them on the chart. The range resets daily. This highlights a specific trading window, aiding in identifying potential breakout or breakdown levels. Traders can adjust the time parameters to analyze various market sessions or strategies. It's useful for those focusing on price action within a defined timeframe, simplifying the observation of key price levels.

PriceCatch - Previous Hour RangeHi Tradingview community,

Recently I stumbled upon a video on Youtube where the Youtuber was talking about Intraday trading based on 1 hour price range.

Anyone requesting the code was asked to contact over email for the code. So, I thought, this is such a simple script and has no special complex coding involved and why such a show off instead of just sharing it.

So, I decided to write the code myself and it took me under 10 minutes to do it. So, here's the PriceCatch - Previous Hour Range script. It is open source, so you can check it and apply it in your trading strategy.

Remember, this is just a simple range plotter and does not give any signals.

If you want 2 hours range, then simply change 60 to 120. Simple.

So, all the best with your trades.

PriceCatch

Weekend RangeWeekend Range Indicator – Customizable High/Low Zones

🔹 Overview

The Weekend Range Indicator marks the last 20 weekends on your chart, highlighting their highs and lows with fully customizable colors, transparency, and time settings. This tool helps traders identify key support and resistance levels from weekend price action.

🛠️ Features

✅ Custom Weekend Start & End – Choose the weekend days and time (UTC)

✅ Automatically Tracks the Last 20 Weekends (configurable up to 50)

✅ Custom Box Colors & Transparency – Adjust the fill and border colors easily

✅ Works on All Timeframes – Best viewed on 1H, 4H, or higher

✅ Efficient & Optimized Code – No lag, smooth performance

🎯 How to Use

1️⃣ Add the indicator to your chart.

2️⃣ Adjust the weekend start & end time in the settings.

3️⃣ Customize the box colors and transparency to match your style.

4️⃣ Watch how price reacts around the weekend high/low zones for trade opportunities.

💡 Trading Strategies

🔹 Breakout Trading – Look for price breaking above or below the weekend range.

🔹 Reversal Zones – Watch for rejections at weekend highs/lows.

🔹 Liquidity & Stop Hunts – Large players often target these levels.

📈 Recommended Markets

✔ Works best on Forex, Crypto, Indices, and Commodities

✔ Ideal for swing traders and intraday traders

🚀 Enjoy using the indicator! Let me know if you’d like any new features added! 🎯🔥

Dynamic 50% Indicator of the selected range!This is a indicator which shows you the 50% level of the selected timeframe range. This is a good tool because price tends to bounce of of 50% levels.

Introducing the 50% Range Level Indicator, designed for traders who seek accuracy and strategic insights in their market analysis. This tool calculates and visually displays the midpoint (50% level) of any selected price range, helping you identify key equilibrium zones where price action often reacts.

Why Use This Indicator?

Key Market Equilibrium – The 50% level is a crucial reference point where price often consolidates, reverses, or gathers momentum.

Custom Range Selection – Simply select your desired price range, and the indicator will dynamically plot the midpoint.

Enhance Your Trading Strategy – Use it for support & resistance confirmation, retracement analysis, or confluence with other indicators.

Works on All Timeframes & Assets – Suitable for stocks, forex, crypto, and indices.

Gain an Edge in the Market

Whether you’re a day trader, swing trader, or long-term investor, the 50% Range Level Indicator can enhance your technical analysis and decision-making.

CandelaCharts - Balanced Price Range (BPR) 📝 Overview

ICT Balanced Price Range (BPR) is the area on the price chart where two opposite Fair Value Gaps overlap.

To identify a Balanced Price Range (BPR), mark a fair value gap (FVG) on the sell side of the price and another on the buy side. These FVGs should be directly opposite each other horizontally. The overlapping area between the two is the Balanced Price Range.

The significance of the ICT Balanced Price Range lies in its sensitivity to price movements. When the market approaches a BPR, it often triggers a rapid and notable price reaction.

This reaction occurs because the two opposing FVGs attract the attention of smart money traders—those with substantial capital capable of influencing market trends. As a key concept in the Inner Circle Trader (ICT) methodology, the BPR serves as an ideal entry point, frequently driving considerable market activity.

📦 Features

MTF

Mitigation

Consequent Encroachment (CE)

Threshold

Hide Overlap

Advanced Styling

⚙️ Settings

Show: Controls whether BPRs are displayed on the chart.

Show Last: Sets the number of BPRs you want to display.

Length: Determines the length of each BPR.

Mitigation: Highlights when an BPR has been touched, using a different color without marking it as invalid.

Timeframe: Specifies the timeframe used to detect BPRs.

Threshold: Sets the minimum gap size required for BPR detection on the chart.

Show Mid-Line: Configures the midpoint line's width and style within the BPR. (Consequent Encroachment - CE)

Show Border: Defines the border width and line style of the BPR.

Hide Overlap: Removes overlapping BPRs from view.

Extend: Extends the BPR length to the current candle.

Elongate: Fully extends the BPR length to the right side of the chart.

⚡️ Showcase

Simple

Mitigated

Bordered

Consequent Encroachment

Extended

🚨 Alerts

This script offers alert options for all signal types.

Bearish Signal

A bearish signal is generated when the price re-enters a bearish inversion zone and then reverses downward.

Bullish Signal

A bullish signal is generated when the price revisits a bullish inversion zone and then breaks upward through the top.

⚠️ Disclaimer

Trading involves significant risk, and many participants may incur losses. The content on this site is not intended as financial advice and should not be interpreted as such. Decisions to buy, sell, hold, or trade securities, commodities, or other financial instruments carry inherent risks and are best made with guidance from qualified financial professionals. Past performance is not indicative of future results.

Daily Range Position Sizer// ENGLISH, GERMAN BELOW

Daily Range Position Sizer

A versatile indicator that helps traders calculate position sizes based on daily high/low levels with flexible session handling.

Features:

- Displays daily high and low levels with broken line style for clear visibility

- Calculates position sizes for both long and short setups based on your defined risk amount

- Flexible session dealing with optional pre-market inclusion

- Real-time position size updates based on current price

- Clearly visible info box showing position sizes

Settings:

- Risk Amount ($): Define your desired risk amount in dollars

- Include Pre-market: Toggle between regular session only (9:30-16:00 ET) or full day including pre-market

- X-Offset: Adjust the horizontal position of the info box

Usage:

1. Set your desired risk amount

2. Choose whether to include pre-market data

3. Monitor daily ranges and corresponding position sizes

4. Use the automatically calculated position sizes for your trades

Note: This indicator is for educational and informational purposes only. Always verify calculations and manage your risk appropriately.

Contributions and feedback are welcome!

// GERMAN

Tageshoch/-Tief & Positionsgröße

Ein vielseitiger Indikator, der Tradern bei der Berechnung von Positionsgrößen auf der Basis von Tageshochs und -tiefs hilft und eine flexible Handhabung der Sitzungen ermöglicht.

Eigenschaften:

- Zeigt tägliche Höchst- und Tiefststände mit gestrichelten Linien für eine klare Sichtbarkeit an

- Berechnet Positionsgrößen für Long- und Short-Setups auf der Grundlage des von Ihnen definierten Risikobetrags

- Flexibles Session-Handling mit optionaler Einbeziehung des vorbörslichen Handels

- Aktualisierung der Positionsgröße in Echtzeit auf Basis des aktuellen Kurses

- Deutlich sichtbare Infobox mit Positionsgrößen

Einstellungen:

- Risikobetrag ($): Definieren Sie Ihren gewünschten Risikobetrag in Dollar

- Vorbörslich einbeziehen: Schalten Sie um zwischen nur regulärer Sitzung (9:30-16:00 ET) oder ganztägig einschließlich Vormarkt

- X-Absatz: Passen Sie die horizontale Position der Infobox an

Verwendung:

1. Legen Sie den gewünschten Risikobetrag fest

2. Wählen Sie, ob vorbörsliche Daten einbezogen werden sollen

3. Überwachen Sie die täglichen Bandbreiten und die entsprechenden Positionsgrößen

4. Verwenden Sie die automatisch berechneten Positionsgrößen für Ihre Trades

Hinweis: Dieser Indikator ist nur für Lehr- und Informationszwecke gedacht. Überprüfen Sie stets die Berechnungen und steuern Sie Ihr Risiko angemessen.

Beiträge und Feedback sind willkommen!

Standard Deviation based Upper Lower RangeThis script makes use of historical data for finding the standard deviation on daily returns. Based on the mean and standard deviation, the upper and lower range for the stock is shown upto 2x standard deviation. These bounds can be treated as volatility range for the next n trading sessions. This volatility is based on historical data. Users can change the lookback historical period, and can also set the time period (days) for upcoming trading sessions.

This indicator can be useful in determining stoploss and target levels along with the traditional support/resistance levels. It can also be useful in option trading where one needs to determine a range beyond which it is safe to sell an option.

A range of 1 SD has around 65% to 68% probability that it will not be breached. A range of 2 SD has around 95% probability that it will not be breached.

The indicator is based on Normal distribution theory. In future editions, I envision to also calculate the skewness and kurtosis so that we can determine if a stock is properly following Normal Distribution theory. That may further favor the calculated range.

[Opening Range pre-Market Breakout Screener] with Alerts (TSO)=

with Alerts (TSO)

===========================================================================

===========================================================================

This Opening Range/pre-Market breakout screener lets you monitor up to 10 symbols/instruments simultaneously (9 plus the one currently displayed on the chart). It provides alerts when the price breaks out of the pre-market range, offering two options: 1) Immediate alerts as the breakout happens with the live bar, and 2) Alerts after the bar closes. The screener also labels breakouts on the chart and offers live status updates in the stats table. The Opening Range/pre-Market area is fully customizable, with a default setting optimized for US stock market pre-market hours (07:00 am-09:30 am ET). Additionally, you can set the Active Trading Session Schedule to define specific intraday periods when breakouts and alerts will be displayed.

What sets this indicator apart from other ORB indicators is its integrated screener for multiple symbols and an IMMEDIATE alert/status feature that notifies you the moment the price breaks through the pre-market range. Moreover, it can be used worldwide as it includes an active trading session schedule for every trading region globally!

===========================================================================

Explanation of all the Features/Inputs/Settings

---------------------------------------------------------------------------

>>> This is where the desired symbols can be turned on/checked to be screened for ORB breakout - the selected/checked symbols at creation of a 'Any alert() function call' alert will alert on any of the selected/checked symbols.

>>> Active Trading Session Hours, this is where Active Trading Session Hours can be setup during which breakouts will be shown on chart/table and alerts will trigger. Every trading region is included, by default it's set to a regular US trading session: 09:30am0-4:00pm ET.

>>> ORB Breakout Config is where the desired breakout approaches can be shown/alert turn on. Closed Bar Breakout: means that a breakout is considered as occurred only when a candle bar is fully closed. Live Breakouts: a breakout occurs immediately at price breakout thru pre-Market range, while candle bar is still open.

>>> Final section is simply the stats table location.

===========================================================================

Adding Alerts in TradngView

---------------------------------------------------------------------------

1) Consolidation alert(s) for the selected/checked symbols

- Select/check/find the desired symbols/instruments (when selecting symbols, make sure - they are from correct BROKER/SOURCE as pricing may differ between different brokers, causing confusion (under 1 broker/source, the symbol will be consolidated, under another it will not...))

-Right-click anywhere on any TradingView chart

-Click on Add alert

-Condition: Select this indicator by it’s name

-Immediately below, change it to "alert() function calls only"

-Expiration: Open-ended (that may require higher tier TradingView account, otherwise the alert will need to be occasionally re-triggered)

-Alert name: Anything

-Hit “Create”

-Note: If you change ANY Settings within the indicator – you must DELETE the current alert and create a new one per steps above, otherwise it will continue triggering alerts per old Settings!

* Once alert triggers, don't get confused, as it will show "Alert on SYMBOL", the SYMBOL will be where you created the major alert for all the symbols within the screener list! Within the alert, on the bottom, it will say: "SPY - LONG Breakout - Live" - this is where the correct symbol is for which the alert for consolidation was triggered!

===========================================================================

If you have any questions or issues with the indicator, please message me directly via TradingView.

---------------------------------------------------------------------------

Good Luck! (NOTE: Trading is very risky, past performance is not necessarily indicative of future results, so please trade responsibly!)