PhantomFlow TrendDetectorThe TrendDetector calculates waves on the chart using the built-in ZigZag indicator and detects a trend change after the last high/low update occurs in a minimum sequence of non-updated highs/lows. This assumes a continuation of the trend for the subsequent update of the remaining high/low.

For trend determination:

When you see a pink or light yellow trend color, it means that a new trend may potentially be emerging right now, and you can join it almost at the beginning. So, if you see patterns from your trading system aligning with the TrendDetector indicator and they have the same direction, it further increases the likelihood of your plan working out.

In the case where the trend phase has a red or green color, it may indicate that the primary market impulse has already occurred, and therefore, joining the trend at this time may not be advisable.

For trade entry:

Additionally, you can use the indicator specifically for entering the market using market orders. Depending on the timeframe (the smaller the timeframe, the more confirmation candles are needed), you can open a trade when one trend replaces another at the close, for example, the second candle in the case of a 10-minute timeframe. Stop-loss can be placed under the signal candle, a local peak, or a reversal trend valley, a global peak, or a reversal trend valley. In the example above, the second option was used.

Settings

You cannot technically adjust anything in this indicator because all the logic is hardcoded. However, for a better chart visualization, after adding it to the chart, click on the three dots next to the indicator name, select "Visual order," and then "Bring to front".

Cerca negli script per "wave"

[AIO] Multi Collection Moving Averages 140 MA TypesAll In One Multi Collection Moving Averages.

Since signing up 2 years ago, I have been collecting various Сollections.

I decided to get it into a decent shape and make it one of the biggest collections on TV, and maybe the entire internet.

And now I'm sharing my collection with you.

140 Different Types of Moving Averages are waiting for you.

Specifically :

"

AARMA | Adaptive Autonomous Recursive Moving Average

ADMA | Adjusted Moving Average

ADXMA | Average Directional Moving Average

ADXVMA | Average Directional Volatility Moving Average

AHMA | Ahrens Moving Average

ALF | Ehler Adaptive Laguerre Filter

ALMA | Arnaud Legoux Moving Average

ALSMA | Adaptive Least Squares

ALXMA | Alexander Moving Average

AMA | Adaptive Moving Average

ARI | Unknown

ARSI | Adaptive RSI Moving Average

AUF | Auto Filter

AUTL | Auto-Line

BAMA | Bryant Adaptive Moving Average

BFMA | Blackman Filter Moving Average

CMA | Corrected Moving Average

CORMA | Correlation Moving Average

COVEMA | Coefficient of Variation Weighted Exponential Moving Average

COVNA | Coefficient of Variation Weighted Moving Average

CTI | Coral Trend Indicator

DEC | Ehlers Simple Decycler

DEMA | Double EMA Moving Average

DEVS | Ehlers - Deviation Scaled Moving Average

DONEMA | Donchian Extremum Moving Average

DONMA | Donchian Moving Average

DSEMA | Double Smoothed Exponential Moving Average

DSWF | Damped Sine Wave Weighted Filter

DWMA | Double Weighted Moving Average

E2PBF | Ehlers 2-Pole Butterworth Filter

E2SSF | Ehlers 2-Pole Super Smoother Filter

E3PBF | Ehlers 3-Pole Butterworth Filter

E3SSF | Ehlers 3-Pole Super Smoother Filter

EDMA | Exponentially Deviating Moving Average (MZ EDMA)

EDSMA | Ehlers Dynamic Smoothed Moving Average

EEO | Ehlers Modified Elliptic Filter Optimum

EFRAMA | Ehlers Modified Fractal Adaptive Moving Average

EHMA | Exponential Hull Moving Average

EIT | Ehlers Instantaneous Trendline

ELF | Ehler Laguerre filter

EMA | Exponential Moving Average

EMARSI | EMARSI

EPF | Edge Preserving Filter

EPMA | End Point Moving Average

EREA | Ehlers Reverse Exponential Moving Average

ESSF | Ehlers Super Smoother Filter 2-pole

ETMA | Exponential Triangular Moving Average

EVMA | Elastic Volume Weighted Moving Average

FAMA | Following Adaptive Moving Average

FEMA | Fast Exponential Moving Average

FIBWMA | Fibonacci Weighted Moving Average

FLSMA | Fisher Least Squares Moving Average

FRAMA | Ehlers - Fractal Adaptive Moving Average

FX | Fibonacci X Level

GAUS | Ehlers - Gaussian Filter

GHL | Gann High Low

GMA | Gaussian Moving Average

GMMA | Geometric Mean Moving Average

HCF | Hybrid Convolution Filter

HEMA | Holt Exponential Moving Average

HKAMA | Hilbert based Kaufman Adaptive Moving Average

HMA | Harmonic Moving Average

HSMA | Hirashima Sugita Moving Average

HULL | Hull Moving Average

HULLT | Hull Triple Moving Average

HWMA | Henderson Weighted Moving Average

IE2 | Early T3 by Tim Tilson

IIRF | Infinite Impulse Response Filter

ILRS | Integral of Linear Regression Slope

JMA | Jurik Moving Average

KA | Unknown

KAMA | Kaufman Adaptive Moving Average & Apirine Adaptive MA

KIJUN | KIJUN

KIJUN2 | Kijun v2

LAG | Ehlers - Laguerre Filter

LCLSMA | 1LC-LSMA (1 line code lsma with 3 functions)

LEMA | Leader Exponential Moving Average

LLMA | Low-Lag Moving Average

LMA | Leo Moving Average

LP | Unknown

LRL | Linear Regression Line

LSMA | Least Squares Moving Average / Linear Regression Curve

LTB | Unknown

LWMA | Linear Weighted Moving Average

MAMA | MAMA - MESA Adaptive Moving Average

MAVW | Mavilim Weighted Moving Average

MCGD | McGinley Dynamic Moving Average

MF | Modular Filter

MID | Median Moving Average / Percentile Nearest Rank

MNMA | McNicholl Moving Average

MTMA | Unknown

MVSMA | Minimum Variance SMA

NLMA | Non-lag Moving Average

NWMA | Dürschner 3rd Generation Moving Average (New WMA)

PKF | Parametric Kalman Filter

PWMA | Parabolic Weighted Moving Average

QEMA | Quadruple Exponential Moving Average

QMA | Quick Moving Average

REMA | Regularized Exponential Moving Average

REPMA | Repulsion Moving Average

RGEMA | Range Exponential Moving Average

RMA | Welles Wilders Smoothing Moving Average

RMF | Recursive Median Filter

RMTA | Recursive Moving Trend Average

RSMA | Relative Strength Moving Average - based on RSI

RSRMA | Right Sided Ricker MA

RWMA | Regressively Weighted Moving Average

SAMA | Slope Adaptive Moving Average

SFMA | Smoother Filter Moving Average

SMA | Simple Moving Average

SSB | Senkou Span B

SSF | Ehlers - Super Smoother Filter P2

SSMA | Super Smooth Moving Average

STMA | Unknown

SWMA | Self-Weighted Moving Average

SW_MA | Sine-Weighted Moving Average

TEMA | Triple Exponential Moving Average

THMA | Triple Exponential Hull Moving Average

TL | Unknown

TMA | Triangular Moving Average

TPBF | Three-pole Ehlers Butterworth

TRAMA | Trend Regularity Adaptive Moving Average

TSF | True Strength Force

TT3 | Tilson (3rd Degree) Moving Average

VAMA | Volatility Adjusted Moving Average

VAMAF | Volume Adjusted Moving Average Function

VAR | Vector Autoregression Moving Average

VBMA | Variable Moving Average

VHMA | Vertical Horizontal Moving Average

VIDYA | Variable Index Dynamic Average

VMA | Volume Moving Average

VSO | Unknown

VWMA | Volume Weighted Moving Average

WCD | Unknown

WMA | Weighted Moving Average

XEMA | Optimized Exponential Moving Average

ZEMA | Zero Lag Moving Average

ZLDEMA | Zero-Lag Double Exponential Moving Average

ZLEMA | Ehlers - Zero Lag Exponential Moving Average

ZLTEMA | Zero-Lag Triple Exponential Moving Average

ZSMA | Zero-Lag Simple Moving Average

"

Don't forget that you can use any Moving Average not only for the chart but also for any of your indicators without affecting the code as in my example.

But remember that some MAs are not designed to work with anything other than a chart.

All MA and Code lists are sorted strictly alphabetically by short name (A-Z).

Each MA has its own number (ID) by which you can display the Moving Average you need.

Next to the ID selection there are tooltips with short names and their numbers. Use them.

The panel below will help you to read the Name of the selected MA.

Because of the size of the collection I think this is the optimal and most convenient use. Correct me if this is not the case.

Unknown - Some MAs I collected so long ago that I lost the full real name and couldn't find the authors. If you recognize them, please let me know.

I have deliberately simplified all MAs to input just Source and Length.

Because the collection is so large, it would be quite inconvenient and difficult to customize all MA functions (multipliers, offset, etc.).

If you need or like any MA you will still have to take it from my collection for your code.

I tried to leave the basic MA settings inside function in first strings.

I have tried to list most of the authors, but since the bulk of the collection was created a long time ago and was not intended for public publication I could not find all of them.

Some of the features were created from scratch or may have been slightly modified, so please be careful.

If you would like to improve this collection, please write to me in PM.

Also Credits, Likes, Awards, Loves and Thanks to :

@alexgrover

@allanster

@andre_007

@auroagwei

@blackcat1402

@bsharpe

@cheatcountry

@CrackingCryptocurrency

@Duyck

@ErwinBeckers

@everget

@glaz

@gotbeatz26107

@HPotter

@io72signals

@JacobAmos

@JoshuaMcGowan

@KivancOzbilgic

@LazyBear

@loxx

@LuxAlgo

@MightyZinger

@nemozny

@NGBaltic

@peacefulLizard50262

@RicardoSantos

@StalexBot

@ThiagoSchmitz

@TradingView

— 𝐀𝐧𝐝 𝐎𝐭𝐡𝐞𝐫𝐬 !

So just a Big Thank You to everyone who has ever and anywhere shared their codes.

Zigzag Chart Points█ OVERVIEW

This indicator displays zigzag based on high and low using latest pine script version 5 , chart.point which using time, index and price as parameters.

Pretty much a strip down using latest pine script function, without any use of library .

This allow pine script user to have an idea of simplified and cleaner code for zigzag.

█ CREDITS

LonesomeTheBlue

█ FEATURES

1. Label can be show / hide including text can be resized.

2. Hover to label, can see tooltip will show price and time.

3. Tooltip will show date and time for hourly timeframe and below while show date only for day timeframe and above.

█ NOTES

1. I admit that chart.point just made the code much more cleaner and save more time. I previously using user-defined type(UDT) which quite hassle.

2. I have no plan to extend this indicator or include alert just I thinking to explore log.error() and runtime.error() , which I may probably release in other publications.

█ HOW TO USE'

Pretty much similar inside mentioned references, which previously I created.

█ REFERENCES

1. Zigzag Array Experimental

2. Simple Zigzag UDT

3. Zig Zag Ratio Simplified

4. Cyclic RSI High Low With Noise Filter

5. Auto AB=CD 1 to 1 Ratio Experimental

EphemerisLibrary "Ephemeris"

TODO: add library description here

mercuryElements()

mercuryRates()

venusElements()

venusRates()

earthElements()

earthRates()

marsElements()

marsRates()

jupiterElements()

jupiterRates()

saturnElements()

saturnRates()

uranusElements()

uranusRates()

neptuneElements()

neptuneRates()

rev360(x)

Normalize degrees to within [0, 360)

Parameters:

x (float) : degrees to be normalized

Returns: Normalized degrees

scaleAngle(longitude, magnitude, harmonic)

Scale angle in degrees

Parameters:

longitude (float)

magnitude (float)

harmonic (int)

Returns: Scaled angle in degrees

julianCenturyInJulianDays()

Constant Julian days per century

Returns: 36525

julianEpochJ2000()

Julian date on J2000 epoch start (2000-01-01)

Returns: 2451545.0

meanObliquityForJ2000()

Mean obliquity of the ecliptic on J2000 epoch start (2000-01-01)

Returns: 23.43928

getJulianDate(Year, Month, Day, Hour, Minute)

Convert calendar date to Julian date

Parameters:

Year (int) : calendar year as integer (e.g. 2018)

Month (int) : calendar month (January = 1, December = 12)

Day (int) : calendar day of month (e.g. January valid days are 1-31)

Hour (int) : valid values 0-23

Minute (int) : valid values 0-60

julianCenturies(date, epoch_start)

Centuries since Julian Epoch 2000-01-01

Parameters:

date (float) : Julian date to conver to Julian centuries

epoch_start (float) : Julian date of epoch start (e.g. J2000 epoch = 2451545)

Returns: Julian date converted to Julian centuries

julianCenturiesSinceEpochJ2000(julianDate)

Calculate Julian centuries since epoch J2000 (2000-01-01)

Parameters:

julianDate (float) : Julian Date in days

Returns: Julian centuries since epoch J2000 (2000-01-01)

atan2(y, x)

Specialized arctan function

Parameters:

y (float) : radians

x (float) : radians

Returns: special arctan of y/x

eccAnom(ec, m_param, dp)

Compute eccentricity of the anomaly

Parameters:

ec (float) : Eccentricity of Orbit

m_param (float) : Mean Anomaly ?

dp (int) : Decimal places to round to

Returns: Eccentricity of the Anomaly

planetEphemerisCalc(TGen, planetElementId, planetRatesId)

Compute planetary ephemeris (longtude relative to Earth or Sun) on a Julian date

Parameters:

TGen (float) : Julian Date

planetElementId (float ) : All planet orbital elements in an array. This index references a specific planet's elements.

planetRatesId (float ) : All planet orbital rates in an array. This index references a specific planet's rates.

Returns: X,Y,Z ecliptic rectangular coordinates and R radius from reference body.

calculateRightAscensionAndDeclination(earthX, earthY, earthZ, planetX, planetY, planetZ)

Calculate right ascension and declination for a planet relative to Earth

Parameters:

earthX (float) : Earth X ecliptic rectangular coordinate relative to Sun

earthY (float) : Earth Y ecliptic rectangular coordinate relative to Sun

earthZ (float) : Earth Z ecliptic rectangular coordinate relative to Sun

planetX (float) : Planet X ecliptic rectangular coordinate relative to Sun

planetY (float) : Planet Y ecliptic rectangular coordinate relative to Sun

planetZ (float) : Planet Z ecliptic rectangular coordinate relative to Sun

Returns: Planet geocentric orbital radius, geocentric right ascension, and geocentric declination

mercuryHelio(T)

Compute Mercury heliocentric longitude on date

Parameters:

T (float)

Returns: Mercury heliocentric longitude on date

venusHelio(T)

Compute Venus heliocentric longitude on date

Parameters:

T (float)

Returns: Venus heliocentric longitude on date

earthHelio(T)

Compute Earth heliocentric longitude on date

Parameters:

T (float)

Returns: Earth heliocentric longitude on date

marsHelio(T)

Compute Mars heliocentric longitude on date

Parameters:

T (float)

Returns: Mars heliocentric longitude on date

jupiterHelio(T)

Compute Jupiter heliocentric longitude on date

Parameters:

T (float)

Returns: Jupiter heliocentric longitude on date

saturnHelio(T)

Compute Saturn heliocentric longitude on date

Parameters:

T (float)

Returns: Saturn heliocentric longitude on date

neptuneHelio(T)

Compute Neptune heliocentric longitude on date

Parameters:

T (float)

Returns: Neptune heliocentric longitude on date

uranusHelio(T)

Compute Uranus heliocentric longitude on date

Parameters:

T (float)

Returns: Uranus heliocentric longitude on date

sunGeo(T)

Parameters:

T (float)

mercuryGeo(T)

Parameters:

T (float)

venusGeo(T)

Parameters:

T (float)

marsGeo(T)

Parameters:

T (float)

jupiterGeo(T)

Parameters:

T (float)

saturnGeo(T)

Parameters:

T (float)

neptuneGeo(T)

Parameters:

T (float)

uranusGeo(T)

Parameters:

T (float)

moonGeo(T_JD)

Parameters:

T_JD (float)

mercuryOrbitalPeriod()

Mercury orbital period in Earth days

Returns: 87.9691

venusOrbitalPeriod()

Venus orbital period in Earth days

Returns: 224.701

earthOrbitalPeriod()

Earth orbital period in Earth days

Returns: 365.256363004

marsOrbitalPeriod()

Mars orbital period in Earth days

Returns: 686.980

jupiterOrbitalPeriod()

Jupiter orbital period in Earth days

Returns: 4332.59

saturnOrbitalPeriod()

Saturn orbital period in Earth days

Returns: 10759.22

uranusOrbitalPeriod()

Uranus orbital period in Earth days

Returns: 30688.5

neptuneOrbitalPeriod()

Neptune orbital period in Earth days

Returns: 60195.0

jupiterSaturnCompositePeriod()

jupiterNeptuneCompositePeriod()

jupiterUranusCompositePeriod()

saturnNeptuneCompositePeriod()

saturnUranusCompositePeriod()

planetSineWave(julianDateInCenturies, planetOrbitalPeriod, planetHelio)

Convert heliocentric longitude of planet into a sine wave

Parameters:

julianDateInCenturies (float)

planetOrbitalPeriod (float) : Orbital period of planet in Earth days

planetHelio (float) : Heliocentric longitude of planet in degrees

Returns: Sine of heliocentric longitude on a Julian date

Ehlers SuperSmootherJohn F. Ehlers has provided the SuperSmoother filter in several of his works, including his book "Cyclical Analytics for Traders", Chapter 3.

The SuperSmoother filter is utilized whenever one might typically apply a moving average of any kind. The outcome is that the output signal from the SuperSmoother filter displays significantly less lag compared to an equivalent amount of smoothing from a moving average. The lag difference between a moving average and the SuperSmoother filter becomes even more pronounced when critical periods are extended.

Market data contains noise, and the purpose of smoothing filters is to mitigate this noise. In fact, there are various types of noise inherent in market data. One type of noise is systemic, originating from random trading activities. Another type is aliasing noise, which arises due to the use of discrete data. Aliasing noise dominates the data when considering shorter cycle durations.

It's tempting to perceive market data as a continuous wave, but that's a misconception. Taking the closing price as representative of a bar provides just a single data point. Whether you opt for the midpoint between the high and low instead of the closing price, you're still limited to one sample per bar. Given the discrete nature of this data, certain spectral implications must be considered. For instance, the shortest feasible analysis period (without aliasing) is a two-bar cycle. This is referred to as the Nyquist frequency, at 0.5 cycles per sample.

An ideally sampled two-beat sinusoidal cycle becomes rectified when discretized. However, peak sampling for the cycle isn't always guaranteed, and interference between the sampling rate and the data frequency results in aliasing noise. This noise decreases as the data period lengthens. For example, a four-beat cycle implies four samples per cycle. With more samples, the sampled data provides a better representation of the sinusoidal component. The replica becomes even more accurate for an eight-bar data component. The increased precision of discrete data signifies that aliasing noise decreases as cycle durations expand.

A smoothing filter should possess the selectivity to reduce the aliasing noise below systemic noise levels. Given that aliasing noise increases by 6 dB per octave above the filter's selected cutoff frequency and the SuperSmoother's attenuation rate is 12 dB per octave, the SuperSmoother filter emerges as an effective tool to virtually eliminate aliasing noise in its output signal.

There are already several SuperSmoother indicators on Tradingview, but I like to structure the code and highlight the main components as functions rather than hiding them in the code. I hope this is useful for those who are starting to learn Pine Script.

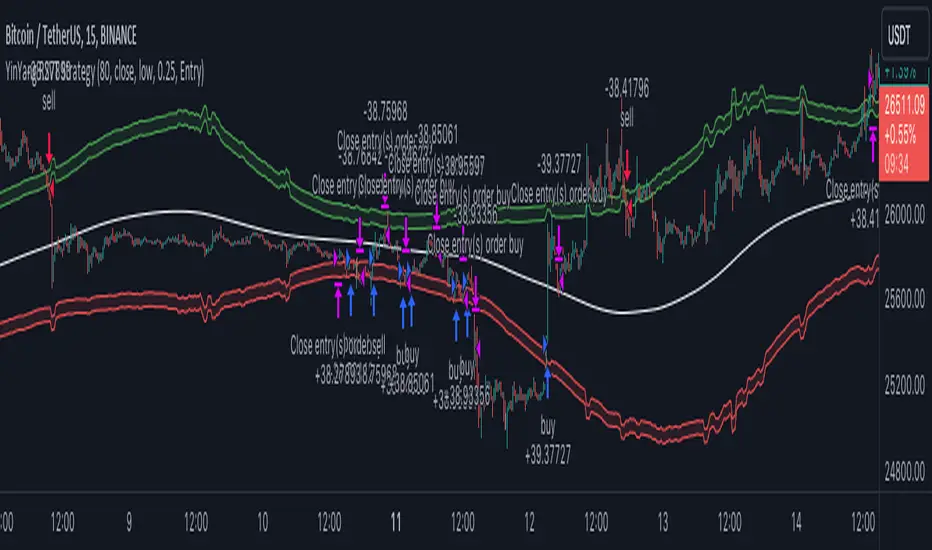

YinYang RSI Volume Trend StrategyThere are many strategies that use RSI or Volume but very few that take advantage of how useful and important the two of them combined are. This strategy uses the Highs and Lows with Volume and RSI weighted calculations on top of them. You may be wondering how much of an impact Volume and RSI can have on the prices; the answer is a lot and we will discuss those with plenty of examples below, but first…

How does this strategy work?

It’s simple really, when the purchase source crosses above the inner low band (red) it creates a Buy or Long. This long has a Trailing Stop Loss band (the outer low band that's also red) that can be adjusted in the Settings. The Stop Loss is based on a % of the inner low band’s price and by default it is 0.1% lower than the inner band’s price. This Stop Loss is not only a stop loss but it can also act as a Purchase Available location.

You can get back into a trade after a stop loss / take profit has been hit when your Reset Purchase Availability After condition has been met. This can either be at Stop Loss, Entry or None.

It is advised to allow it to reset in case the stop loss was a fake out but the call was right. Sometimes it may trigger stop loss multiple times in a row, but you don’t lose much on stop loss and you gain lots when the call is right.

The Take Profit location is the basis line (white). Take Profit occurs when the Exit Source (close, open, high, low or other) crosses the basis line and then on a different bar the Exit Source crosses back over the basis line. For example, if it was a Long and the bar’s Exit Source closed above the basis line, and then 2 bars later its Exit Source closed below the basis line, Take Profit would occur. You can disable Take Profit in Settings, but it is very useful as many times the price will cross the Basis and then correct back rather than making it all the way to the opposing zone.

Longs:

If for instance your Long doesn’t need to Take Profit and instead reaches the top zone, it will close the position when it crosses above the inner top line (green).

Please note you can change the Exit Source too which is what source (close, open, high, low) it uses to end the trades.

The Shorts work the same way as the Long but just opposite, they start when the purchase source crosses under the inner upper band (green).

Shorts:

Shorts take profit when it crosses under the basis line and then crosses back.

Shorts will Stop loss when their outer upper band (green) is crossed with the Exit Source.

Short trades are completed and closed when its Exit Source crosses under the inner low red band.

So, now that you understand how the strategy works, let’s discuss why this strategy works and how it is profitable.

First we will discuss Volume as we deem it plays a much bigger role overall and in our strategy:

As I’m sure many of you know, Volume plays a huge factor in how much something moves, but it also plays a role in the strength of the movement. For instance, let’s look at two scenarios:

Bitcoin’s price goes up $1000 in 1 Day but the Volume was only 10 million

Bitcoin’s price goes up $200 in 1 Day but the Volume was 40 million

If you were to only look at the price, you’d say #1 was more important because the price moved x5 the amount as #2, but once you factor in the volume, you know this is not true. The reason why Volume plays such a huge role in Price movement is because it shows there is a large Limit Order battle going on. It means that both Bears and Bulls believe that price is a good time to Buy and Sell. This creates a strong Support and Resistance price point in this location. If we look at scenario #2, when there is high volume, especially if it is drastically larger than the average volume Bitcoin was displaying recently, what can we decipher from this? Well, the biggest take away is that the Bull’s won the battle, and that likely when that happens we will see bullish movement continuing to happen as most of the Bears Limit Orders have been fulfilled. Whereas with #2, when large price movement happens and Bitcoin goes up $1000 with low volume what can we deduce? The main takeaway is that Bull’s pressured the price up with Market Orders where they purchased the best available price, also what this means is there were very few people who were wanting to sell. This generally dictates that Whale Limit orders for Sells/Shorts are much higher up and theres room for movement, but it also means there is likely a whale that is ready to dump and crash it back down.

You may be wondering, what did this example have to do with YinYang RSI Volume Trend Strategy? Well the reason we’ve discussed this is because we use Volume multiple times to apply multiplications in our calculations to add large weight to the price when there is lots of volume (this is applied both positively and negatively). For instance, if the price drops a little and there is high volume, our strategy will move its bounds MUCH lower than the price actually dropped, and if there was low volume but the price dropped A LOT, our strategy will only move its bounds a little. We believe this reflects higher levels of price accuracy than just price alone based on the examples described above.

Don’t believe us?

Here is with Volume NOT factored in (VWMA = SMA and we remove our Volume Filter calculation):

Which produced -$2880 Profit

Here is with our Volume factored in:

Which produced $553,000 (55.3%)

As you can see, we wen’t from $-2800 profit with volume not factored to $553,000 with volume factored. That's quite a big difference! (Please note previous success does not predict future success we are simply displaying the $ amounts as example).

Now how about RSI and why does it matter in this strategy?

As I’m sure most of you are aware, RSI is one of the leading indicators used in trading. For this reason we figured it would only make sense to incorporate it into our calculations. We fiddled with RSI for quite awhile and sometimes what logically seems to be the right way to use it isn’t. Now, because of this, our RSI calculation is a little odd, but basically what we’re doing is we calculate the RSI, then turn it into a percentage (between 0-1) that can easily be multiplied to the price point we need. The price point we use is the difference between our high purchase zone and our low purchase zone. This allows us to see how much price movement there is between zones. We multiply our zone size with our RSI multiplication and we get the amount we will add +/- to our basis line (white line). This officially creates the NEW high and low purchase zones that we are actually using and displaying in our trades.

If you found that confusing, here are some examples to why it is an important calculation for this strategy:

Before RSI factored in:

Which produced 27.8% Profit

After RSI factored in:

Which produced 553% Profit

As you can see, the RSI makes not only the purchase zones more accurate, but it also greatly increases the profit the strategy is able to make. It also helps ensure an relatively linear profit slope so you know it is reliable with its trades.

This strategy can work on pretty much anything, but you should tweak the values a bit for each pair you are trading it with for best results.

We hope you can find some use out of this simple but effective strategy, if you have any questions, comments or concerns please let us know.

HAPPY TRADING!

[MAD] MindreaderHi,

This is a multiband indicator that shows you liquid support and resistance ranges based on growing offsets and growing ATR channels.

In the end, when setup well, you can make, based on historical observations, estimates of how traders will react, maybe identical again.

How to use:

Setup:

Activate the two checkboxes for centerline and All_Lines

Start with the middle line to establish the general direction of the asset.

With the 6 following options, you try to match the trends in the outer bands as good as possible.

Small changes can be made by till you have best fitting overall bands. I tried to make small steppingsize to visual setup very easy. Change a bit... wait look,... change a bit, wait look...

Deactivate the two setup boxes and continue with setting up the colors.

Have fun figuring out the perfect wave !!

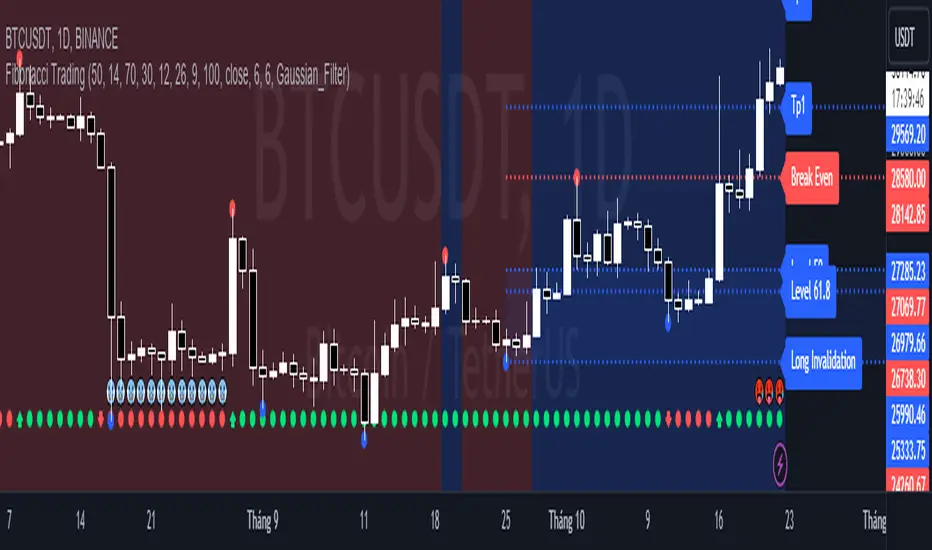

Fibonacci TradingFibonacci Trading

This simple script draw Fibonacci Retracement to define pullback level and draw Fibonacci Extension to define target level of a upward wave or doward wave

1. Upward wave

1.1 Fibonacci Retracement

+ Fibonacci Retracement measuare from support to nearest resistance on the right.

+ Retracement Level 0 named as "Breake Even"

+ Retracement Level 100 named as "Long Invalidation"

+ Retracement Level 50 and 61.8 is ploted as blue line

+ The zone between Retracement Level 50 and 100 is filled by blue color and named as "Buy zone"

1.2 Fibonacci Extension

+ Fibonacci Extension measuare from Retracement Level 61.8 to Retracement Level 0

+ Fibonacci Extension Level 161.8 named as "Tp1 (Target point 1)"

+ Fibonacci Extension Level 261.8 named as "Tp2 (Target point 2)"

2. Doward wave

2.1 Fibonacci Retracement

+ Fibonacci Retracement measuare from resistance to nearest support on the right.

+ Retracement Level 0 named as "Breake Even"

+ Retracement Level 100 named as "Short Invalidation"

+ Retracement Level 50 and 61.8 is ploted as red line

+ The zone between Retracement Level 50 and 100 is filled by red color and named as "Sell zone"

2.2 Fibonacci Extension

+ Fibonacci Extension measuare from Retracement Level 61.8 to Retracement Level 0

+ Fibonacci Extension Level 161.8 named as "Tp1 (Target point 1)"

+ Fibonacci Extension Level 261.8 named as "Tp2 (Target point 2)"

3. Trading Setup

3.1 Long Only: Only display Fibonacci of Upward wave

3.2 Short Only: Only display Fibonacci of Doward wave

3.3 Both: Display both Fibonacci of Upward wave and Doward wave

Random Market «NoaTrader»This is a simple script for generating random data shown as candles. The purpose of it is the following:

1- To see what works here. If everything is random and something is working, is there really any reason behind it?

2- To see what NOT works here! this is probably the most interesting part. Human behaviors are more likely to generate bubbles so theories like Elliot waves don't work here but do work on real charts! that is an interesting thing!

3- To find out the exact parameters defining a market which is a bit more complicated and deeper. If you look closely to candles you can say that it is not natural like other candle charts. If you have watched different timeframes enough, you have a sense of the difference between them. Why? What is natural? The volume? The wicks? The seasonality? The amount of randomness? The cycle of momentum change? ... If you can generate candles more similar to real ones it means you know the details of market much better!

P.S: the random function of trading view works differently on different symbols and timeframes..

Price Depth Analysis to the MAHello Traders! Today, I bring you an indicator that can greatly assist you in your trading. This indicator aims to analyze the Expansion and Contraction process of the price in relation to a moving average. We refer to "Expansion" when the price moves away from the moving average; a significant expansion could signal that the asset is in a strong trend. On the other hand, when we refer to "Contraction", it's when the price approaches or returns to the moving average. A contraction could signal that the asset is losing momentum and might be preparing for a trend change or consolidation.

To use the indicator, the first thing you need to do is define the type of analysis you want to perform (from the indicator settings) whether you want to evaluate prices above the moving average or below. You should also select the type of moving average and its period.

The indicator will search for the maximum distance in all the chart bars, which will be represented with a yellow label.

From that value, the indicator will generate a certain number of proportional levels (configurable up to 20) and will count all the bars that reached each level. This will be represented in a table showing both the number of bars that reached each range and the percentage in relation to the total bars of all ranges.

Additionally, there's the possibility to view the ranges directly for the current price, providing a good reference.

>> Alerts:

The indicator comes with alerts that notify traders about specific price movements in relation to a moving average (MA). These alerts are triggered when the price enters different ranges, either above or below the MA.

>> Settings:

- Type of Analysis: Users can choose to analyze the price either above or below the MA.

- Length of the moving average: Length of the MA.

- Source of the moving average: Source to calculate the MA (e.g., close, open).

- Type of moving average: Type of MA (SMA, EMA, WMA, VWMA, HMA).

- Show Moving Average: Option to display or hide the MA on the chart.

- Number of levels: Number of levels or ranges to categorize the distance between the price and the MA.

- Number of decimals: Number of decimals to display in labels and tables.

- Show Ranges: Option to display or hide the ranges on the chart.

- Extend Range: Extension of the ranges into future bars.

- Range Fill Transparency: Transparency of the range fill.

>> Potential Utility of the Indicator:

- Entry and Exit Optimization:

By understanding the percentages of each range, traders can identify optimal levels to enter or exit a trade, maximizing profits and minimizing losses.

- Risk Management:

Range percentages can help determine market volatility. A range with a high percentage indicates greater volatility, which can be useful for setting wider stop losses or adjusting position size.

- Overbought and Oversold Zone Identification:

If a price is at the upper or lower extreme of its percentage range, it may indicate overbought or oversold conditions, respectively. These zones can be opportunities for counter-trend trades.

- Momentum Assessment:

A rapid change in range percentages can indicate strong momentum in a particular direction. Traders can use this information to ride the momentum wave or prepare for a potential reversal.

- False Signal Filtering:

By combining range percentage knowledge with other indicators, traders can filter out signals that might be less reliable, thus improving trade accuracy.

- Strategic Planning:

Knowing range percentages allows traders to adapt their strategies according to market conditions. For instance, in a market with narrow ranges and low percentages, they might opt for range strategies. In markets with wide ranges and high percentages, they might look for trend strategies.

- Trend Strength Evaluation:

If range percentages show that the price consistently stays at one end of the range, this may signal a strong and sustained trend.

- Improved Trading Discipline:

By basing trading decisions on quantitative data like range percentages, traders can trade more objectively and disciplined, avoiding impulsive or emotion-based decisions.

>> Future Indicator Update:

- In future versions, we plan to incorporate a detailed analysis based on the historical behavior of candles after the price enters a specific range. For instance, if after an upward movement the price enters a certain range and historically, the next candle tends to be bearish in a high percentage of occasions, this information will be highlighted and presented clearly to the user. The idea behind this addition is to provide traders with a statistical edge, allowing them to anticipate potential market movements with greater accuracy. Moreover, this information could be used to seek trading opportunities in smaller timeframes, aligning the trade direction based on the probability of this mentioned candle.

>> Conclusions:

- In summary, a detailed understanding of each range's percentages in an indicator provides traders with a valuable tool to analyze the market, make informed decisions, and enhance their trading. By grasping the significance of these percentages, traders can adapt their strategies and techniques to fully leverage the opportunities the market presents.

Indicator Based Market Exposure (IBME)The Indicator Based Market Exposure (IBME) system was created by Big Wave Chartist as a way to navigate the markets using a confluence of three different signals to determine when the "internals" of the market are in your favor and how heavily invested to be at any point. The idea of the system is also to flash warning signs when the market internals are beginning to deteriorate so as to take a defensive stance. Of course this system can be strictly adhered to, or it can be incorporated into a more discretionary style of trading, and be combined with progressive exposure into (and out of) the market as positions gain (or lose) traction.

The IBME displays a straightforward action signal based on the combination of the 3 separate signals:

Green 🟢 Full size-longs permitted

Yellow 🟡 Pilot positions permitted

Red 🔴 No longs allowed

So let's get into the signals used:

McClellan Summation Index

Net New Highs/Lows

Net New Highs Crossover

McClellan Summation Index (MSI)

The McClellan Summation Index is a long-term version of the McClellan Oscillator, which is a market breadth indicator based on stock advances and declines. Interpretation is similar to that of the McClellan Oscillator, except that it is more suited to intermediate to major trends and related reversals. The McClellan Summation Index can be calculated as the sum of all the daily values of the McClellan Oscillator. This is used along with the 10-sma to watch for a crossover indicating an uptrend or downtrend beginning.

Net New Highs/Lows

This is the net number of stocks making 52-week highs or lows. For instance, if there are 60 new 52-week highs and 20 new 52-week lows, the net number will be 40 net new 52 week highs. This signal is particularly useful in gauging breadth.

Net New Highs Crossover

This is the description of NNHC from the original separate version of this indicator created by HikoStory: "Net New Highs can guide you to increase or decrease your exposure based on the current market health. They are calculated by subtracting the new highs from the new lows, based on all stocks of the...NASDAQ. A positive value shows that the market is doing good, since more stocks are making new highs compared to new lows. A negative value shows that the market is doing bad, since more stocks are making new lows compared to new highs. Combined with a moving average you can see crossovers that can warn you early when there is a change in the current market health."

The default index for the IBME is the Nasdaq.

The IBME is meant to be used on a daily time frame chart, therefore the signal will only show on a daily time frame chart.

Display options include:

Show/hide individual signals

Table background/font color

Table size/placement

Recursive Micro Zigzag🎲 Overview

Zigzag is basic building block for any pattern recognition algorithm. This indicator is a research-oriented tool that combines the concepts of Micro Zigzag and Recursive Zigzag to facilitate a comprehensive analysis of price patterns. This indicator focuses on deriving zigzag on multiple levels in more efficient and enhanced manner in order to support enhanced pattern recognition.

The Recursive Micro Zigzag Indicator utilises the Micro Zigzag as the foundation and applies the Recursive Zigzag technique to derive higher-level zigzags. By integrating these techniques, this indicator enables researchers to analyse price patterns at multiple levels and gain a deeper understanding of market behaviour.

🎲 Concept:

Micro Zigzag Base : The indicator utilises the Micro Zigzag concept to capture detailed price movements within each candle. It allows for the visualisation of the sequential price action within the candle, aiding in pattern recognition at a micro level.

Basic implementation of micro zigzag can be found in this link - Micro-Zigzag

Recursive Zigzag Expansion : Building upon the Micro Zigzag base, the indicator applies the Recursive Zigzag concept to derive higher-level zigzags. Through recursive analysis of the Micro Zigzag's pivots, the indicator uncovers intricate patterns and trends that may not be evident in single-level zigzags.

Earlier implementations of recursive zigzag can be found here:

Recursive Zigzag

Recursive Zigzag - Trendoscope

And the libraries

rZigzag

ZigzagMethods

The major differences in this implementation are

Micro Zigzag Base - Earlier implementation made use of standard zigzag as base whereas this implementation uses Micro Zigzag as base

Not cap on Pivot depth - Earlier implementation was limited by the depth of level 0 zigzag. In this implementation, we are trying to build the recursive algorithm progressively so that there is no cap on the depth of level 0 zigzag. But, if we go for higher levels, there is chance of program timing out due to pine limitations.

These algorithms are useful in automatically spotting patterns on the chart including Harmonic Patterns, Chart Patterns, Elliot Waves and many more.

@tk · fractal rsi levels█ OVERVIEW

This script is an indicator that helps traders to identify the RSI Levels for multiple fractals wherever the current timeframe is. This script was based on RSI Levels, 20-30 & 70-80 by abdomi indicator, that calculates the Relative Strenght Index levels based on the asset's price and plots it into the chart, creating a "wave" style indicator. The core feature of this indicator is the fractal rays, so trader can visualize each of the oversold and overbought levels of multiple timeframe on the current timeframe that he is on. The indicator will plots multiple rays after the chart bars. indicating where is the oversold and overbought levels for others fractals.

█ MOTIVATION

Since the RSI Levels, 20-30 & 70-80 by abdomi indicator helps a lot to identify the possible price levels when the asset is oversold or overbought, I saw myself drawing multiple horizontal lines on these levels in lower timeframes so, in an uptrend or downtrend, I can try to get a pullback of these trends when the asset reaches oversold or overboght levels. So, I get the idea to make those lines visible in multiple timeframes so I don't need to draw it myself manually anymore.

█ CONCEPT

The trading concept to use this indicator is the concept to make entries on uptrend or downtrend pullbacks when the asset price reaches oversold or overbought levels. But this strategy don't works alone. It needs to be aligned together with others indicators like Exponential Moving Averages, Chart Patterns, Support and Resistance, and so on... Even more confluences that you have, bigger are your chances to increase the probability for a successful trade. So, don't use this indicator alone. Compose a trading strategy and use it to improve your analysis.

█ CUSTOMIZATION

This indicator allows the trader to customize the following settings:

GENERAL

Text size

Changes the font size of the labels to improve accessibility.

Type: string

Options: `tiny`, `small`, `normal`, `large`.

Default: `small`

RSI LEVELS · SETTINGS

Pre-oversold Level

Changes the RSI Level to calculate the "pre-oversold" price level on the chart.

Type: int

Min: 1

Max: 49

Default: 33

Pre-overbought Level

Changes the RSI Level to calculate the "pre-overbought" price level on the chart.

Type: int

Min: 51

Max: 100

Default: 67

Show "Pre-over" Levels

Enables / Disables the pre-oversold and pre-overbought levels on the chart.

Type: bool

Default: true

FRACTAL RAYS · SETTINGS

Length

Changes the base length for the RSI calculation.

Type: int

Min: 1

Default: 14

Source

Changes the base source for the RSI calculation.

Type: float

Default: close

FRACTAL RAYS · STYLE

Ray Color

Changes the color of all fractal rays and its label.

Type: color

Default: color.rgb(187, 74, 207)

Ray Style

Changes the style of all fractal rays.

Type: string

Options: `line.style_solid`, `line.style_dashed`, `line.style_dotted`

Default: line.style_dotted

Ray Length

Changes the length of all fractal rays.

Type: int

Default: 15

FRACTAL RAYS · OVERSOLD

Oversold Level

Changes the base RSI Level for fractal rays calculation.

Type: int

Min: 1

Default: 30

Oversold Prefix

Customizes the fractal ray label with a prefix text.

Type: string

Default: 🚀

Oversold Suffix

Customizes the fractal ray label with a suffix text.

Type: string

Default: (empty)

FRACTAL RAYS · OVERBOUGHT

Overbought Level

Changes the base RSI Level for fractal rays calculation.

Type: int

Min: 1

Default: 70

Overbought Prefix

Customizes the fractal ray label with a prefix text.

Type: string

Default: 🐻

Overbought Suffix

Customizes the fractal ray label with a suffix text.

Type: string

Default: (empty)

FRACTAL RAYS · VISIBILITY RULES

These rules are applied for each of fractal rays so, the traders can choose what timeframes they wants to show the fractal rays for each of it. The rule will be applied as the following condition: `if timeframe != CURRENT_TIMEFRAME and timeframe <= CHOSEN_OPTION`. Actually, the fractal rays are on the chart but, isn't visible because it was applied a transparent color, so it is visually not on the chart to prevent chart's over polution.

LABELS

Show Labels on Price Scale

Shows labels on price scale.

Type: bool

Default: false

Show Price on Fractal Rays

Shows the RSI Level price on each of fractal rays respectively.

Type: bool

Default: false

█ EXTERNAL LIBRARIES

This script uses the `tk` library to calculate RSI Levels. It is a library that contains various functions that helps pine script developers to calculate RSI Levels.

█ FUNCTIONS

The library contains the following functions:

fn_fractalVisibilityRule(string visibilityRule)

Converts the fractal rays timeframe visibility rule label to timestamp int.

Parameters:

visibilityRule: (string) Fractal ray visibility rule label.

Returns: (int) Fractal ray visibility rule timestamp.

fn_requestFractal(string period, expression)

Converts the fractal rays timeframe visibility rule label to timestamp int.

Parameters:

period: (string) Timeframe period for the desired fractal.

expression: (mixed) Security expression that will be applied for calculation.

Returns: (mixed) A result determined by expression.

fn_plotRay(float y, string label, color color, int length)

Plots ray after chart bars for the current time.

Parameters:

period: (string) Timeframe period for the desired fractal.

expression: (mixed) Security expression that will be applied for calculation.

Returns: (void) This function only plots the elements into the chart

fn_plotRsiLevelRay(simple string period, simple int level, color color)

Plots RSI Levels ray after chart bars for the current time.

Parameters:

period: (simple string) Timeframe period.

level: (simple int) Relative Strength Index level.

color: (color) The color of both, ray and label text.

Returns: (void) This function only plots the elements into the chart

Market Time Cycle (Expo)█ Time Cycles Overview

Time cycles are a fascinating and powerful concept in the world of trading and investing. They are all about understanding and predicting the timing of market moves based on the premise that market events and price movements are not random, but instead occur in repeatable, cyclical patterns.

The Concept of Time Cycles: The foundation of time cycles lies in the belief that historical market patterns tend to repeat themselves over specific periods. These periods or cycles could be influenced by a myriad of factors like economic data releases, earnings reports, geopolitical events, or even natural human behavior. For example, some traders observe increased market activity around the start and end of a trading day, which is a form of intraday time cycle.

Understanding time cycles can provide traders with a roadmap, helping them anticipate potential trend shifts and make more informed decisions about when to buy or sell.

█ Indicator Overview

The Market Time Cycle (Expo) is designed to help traders track and analyze market cycles and generate signals for potential trading opportunities. It uses mathematical techniques to analyze market cycles and detect possible turning points. It does this by projecting the estimated cycle timeline and providing visual indications of cyclical phases through the use of color-coded lines and sine wave cycles.

Time cycles offer a compelling way to forecast market trends and time your trades better. By adding time cycles to your trading toolbox, you could potentially gain a new perspective on market movements and refine your trading strategy further. The indicator generates trading signals based on the sine wave's behavior. When the sine wave crosses certain thresholds, the indicator generates a signal suggesting a potential trading opportunity based on cycle behavior.

█ How to use

This indicator can be a valuable tool to help traders understand and predict market trends and time their trades more accurately. By visualizing the cyclic nature of markets, traders can better anticipate potential turning points and adjust their trading strategies accordingly. It helps traders to spot ideal entry and exit points based on the cyclical nature of financial markets.

█ Settings

You can customize the number of bars (NumbOfBars) that are taken into consideration for the cycle. Including a higher number of bars will provide more data, which can be helpful for analyzing long-term trends.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

BankNifty targets using VIX Version 2Original Idea Credit: Verified Market Waves

Hi,

After watching different videos online on how to get targets of BankNifty & Nifty decided to write this small script using VIX.

Nothing great but I really like the concept of getting high and low targets for the day or weekly or monthly or yearly.

What does the script do

1. We get closing of India Vix & BankNifty and Nifty

2. We get square root of Daily (365 days) | Weekly (52) | Monthly (12) & Yearly (1)

3. We divide India Vix closing with different square root to get a decimal value.

4. We use the derived value from step 3 which is used as % to calculate high and low values on BankNifty close price.

Small explanation via below screen shot to understand how to use it.

As always it comes with source code so you can modify as per your requirement.

Hope it helps 👍

Quinn-Fernandes Fourier Transform of Filtered Price [Loxx]Down the Rabbit Hole We Go: A Deep Dive into the Mysteries of Quinn-Fernandes Fast Fourier Transform and Hodrick-Prescott Filtering

In the ever-evolving landscape of financial markets, the ability to accurately identify and exploit underlying market patterns is of paramount importance. As market participants continuously search for innovative tools to gain an edge in their trading and investment strategies, advanced mathematical techniques, such as the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter, have emerged as powerful analytical tools. This comprehensive analysis aims to delve into the rich history and theoretical foundations of these techniques, exploring their applications in financial time series analysis, particularly in the context of a sophisticated trading indicator. Furthermore, we will critically assess the limitations and challenges associated with these transformative tools, while offering practical insights and recommendations for overcoming these hurdles to maximize their potential in the financial domain.

Our investigation will begin with a comprehensive examination of the origins and development of both the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter. We will trace their roots from classical Fourier analysis and time series smoothing to their modern-day adaptive iterations. We will elucidate the key concepts and mathematical underpinnings of these techniques and demonstrate how they are synergistically used in the context of the trading indicator under study.

As we progress, we will carefully consider the potential drawbacks and challenges associated with using the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter as integral components of a trading indicator. By providing a critical evaluation of their computational complexity, sensitivity to input parameters, assumptions about data stationarity, performance in noisy environments, and their nature as lagging indicators, we aim to offer a balanced and comprehensive understanding of these powerful analytical tools.

In conclusion, this in-depth analysis of the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter aims to provide a solid foundation for financial market participants seeking to harness the potential of these advanced techniques in their trading and investment strategies. By shedding light on their history, applications, and limitations, we hope to equip traders and investors with the knowledge and insights necessary to make informed decisions and, ultimately, achieve greater success in the highly competitive world of finance.

█ Fourier Transform and Hodrick-Prescott Filter in Financial Time Series Analysis

Financial time series analysis plays a crucial role in making informed decisions about investments and trading strategies. Among the various methods used in this domain, the Fourier Transform and the Hodrick-Prescott (HP) Filter have emerged as powerful techniques for processing and analyzing financial data. This section aims to provide a comprehensive understanding of these two methodologies, their significance in financial time series analysis, and their combined application to enhance trading strategies.

█ The Quinn-Fernandes Fourier Transform: History, Applications, and Use in Financial Time Series Analysis

The Quinn-Fernandes Fourier Transform is an advanced spectral estimation technique developed by John J. Quinn and Mauricio A. Fernandes in the early 1990s. It builds upon the classical Fourier Transform by introducing an adaptive approach that improves the identification of dominant frequencies in noisy signals. This section will explore the history of the Quinn-Fernandes Fourier Transform, its applications in various domains, and its specific use in financial time series analysis.

History of the Quinn-Fernandes Fourier Transform

The Quinn-Fernandes Fourier Transform was introduced in a 1993 paper titled "The Application of Adaptive Estimation to the Interpolation of Missing Values in Noisy Signals." In this paper, Quinn and Fernandes developed an adaptive spectral estimation algorithm to address the limitations of the classical Fourier Transform when analyzing noisy signals.

The classical Fourier Transform is a powerful mathematical tool that decomposes a function or a time series into a sum of sinusoids, making it easier to identify underlying patterns and trends. However, its performance can be negatively impacted by noise and missing data points, leading to inaccurate frequency identification.

Quinn and Fernandes sought to address these issues by developing an adaptive algorithm that could more accurately identify the dominant frequencies in a noisy signal, even when data points were missing. This adaptive algorithm, now known as the Quinn-Fernandes Fourier Transform, employs an iterative approach to refine the frequency estimates, ultimately resulting in improved spectral estimation.

Applications of the Quinn-Fernandes Fourier Transform

The Quinn-Fernandes Fourier Transform has found applications in various fields, including signal processing, telecommunications, geophysics, and biomedical engineering. Its ability to accurately identify dominant frequencies in noisy signals makes it a valuable tool for analyzing and interpreting data in these domains.

For example, in telecommunications, the Quinn-Fernandes Fourier Transform can be used to analyze the performance of communication systems and identify interference patterns. In geophysics, it can help detect and analyze seismic signals and vibrations, leading to improved understanding of geological processes. In biomedical engineering, the technique can be employed to analyze physiological signals, such as electrocardiograms, leading to more accurate diagnoses and better patient care.

Use of the Quinn-Fernandes Fourier Transform in Financial Time Series Analysis

In financial time series analysis, the Quinn-Fernandes Fourier Transform can be a powerful tool for isolating the dominant cycles and frequencies in asset price data. By more accurately identifying these critical cycles, traders can better understand the underlying dynamics of financial markets and develop more effective trading strategies.

The Quinn-Fernandes Fourier Transform is used in conjunction with the Hodrick-Prescott Filter, a technique that separates the underlying trend from the cyclical component in a time series. By first applying the Hodrick-Prescott Filter to the financial data, short-term fluctuations and noise are removed, resulting in a smoothed representation of the underlying trend. This smoothed data is then subjected to the Quinn-Fernandes Fourier Transform, allowing for more accurate identification of the dominant cycles and frequencies in the asset price data.

By employing the Quinn-Fernandes Fourier Transform in this manner, traders can gain a deeper understanding of the underlying dynamics of financial time series and develop more effective trading strategies. The enhanced knowledge of market cycles and frequencies can lead to improved risk management and ultimately, better investment performance.

The Quinn-Fernandes Fourier Transform is an advanced spectral estimation technique that has proven valuable in various domains, including financial time series analysis. Its adaptive approach to frequency identification addresses the limitations of the classical Fourier Transform when analyzing noisy signals, leading to more accurate and reliable analysis. By employing the Quinn-Fernandes Fourier Transform in financial time series analysis, traders can gain a deeper understanding of the underlying financial instrument.

Drawbacks to the Quinn-Fernandes algorithm

While the Quinn-Fernandes Fourier Transform is an effective tool for identifying dominant cycles and frequencies in financial time series, it is not without its drawbacks. Some of the limitations and challenges associated with this indicator include:

1. Computational complexity: The adaptive nature of the Quinn-Fernandes Fourier Transform requires iterative calculations, which can lead to increased computational complexity. This can be particularly challenging when analyzing large datasets or when the indicator is used in real-time trading environments.

2. Sensitivity to input parameters: The performance of the Quinn-Fernandes Fourier Transform is dependent on the choice of input parameters, such as the number of harmonic periods, frequency tolerance, and Hodrick-Prescott filter settings. Choosing inappropriate parameter values can lead to inaccurate frequency identification or reduced performance. Finding the optimal parameter settings can be challenging, and may require trial and error or a more sophisticated optimization process.

3. Assumption of stationary data: The Quinn-Fernandes Fourier Transform assumes that the underlying data is stationary, meaning that its statistical properties do not change over time. However, financial time series data is often non-stationary, with changing trends and volatility. This can limit the effectiveness of the indicator and may require additional preprocessing steps, such as detrending or differencing, to ensure the data meets the assumptions of the algorithm.

4. Limitations in noisy environments: Although the Quinn-Fernandes Fourier Transform is designed to handle noisy signals, its performance may still be negatively impacted by significant noise levels. In such cases, the identification of dominant frequencies may become less reliable, leading to suboptimal trading signals or strategies.

5. Lagging indicator: As with many technical analysis tools, the Quinn-Fernandes Fourier Transform is a lagging indicator, meaning that it is based on past data. While it can provide valuable insights into historical market dynamics, its ability to predict future price movements may be limited. This can result in false signals or late entries and exits, potentially reducing the effectiveness of trading strategies based on this indicator.

Despite these drawbacks, the Quinn-Fernandes Fourier Transform remains a valuable tool for financial time series analysis when used appropriately. By being aware of its limitations and adjusting input parameters or preprocessing steps as needed, traders can still benefit from its ability to identify dominant cycles and frequencies in financial data, and use this information to inform their trading strategies.

█ Deep-dive into the Hodrick-Prescott Fitler

The Hodrick-Prescott (HP) filter is a statistical tool used in economics and finance to separate a time series into two components: a trend component and a cyclical component. It is a powerful tool for identifying long-term trends in economic and financial data and is widely used by economists, central banks, and financial institutions around the world.

The HP filter was first introduced in the 1990s by economists Robert Hodrick and Edward Prescott. It is a simple, two-parameter filter that separates a time series into a trend component and a cyclical component. The trend component represents the long-term behavior of the data, while the cyclical component captures the shorter-term fluctuations around the trend.

The HP filter works by minimizing the following objective function:

Minimize: (Sum of Squared Deviations) + λ (Sum of Squared Second Differences)

Where:

1. The first term represents the deviation of the data from the trend.

2. The second term represents the smoothness of the trend.

3. λ is a smoothing parameter that determines the degree of smoothness of the trend.

The smoothing parameter λ is typically set to a value between 100 and 1600, depending on the frequency of the data. Higher values of λ lead to a smoother trend, while lower values lead to a more volatile trend.

The HP filter has several advantages over other smoothing techniques. It is a non-parametric method, meaning that it does not make any assumptions about the underlying distribution of the data. It also allows for easy comparison of trends across different time series and can be used with data of any frequency.

Another significant advantage of the HP Filter is its ability to adapt to changes in the underlying trend. This feature makes it particularly well-suited for analyzing financial time series, which often exhibit non-stationary behavior. By employing the HP Filter to smooth financial data, traders can more accurately identify and analyze the long-term trends that drive asset prices, ultimately leading to better-informed investment decisions.

However, the HP filter also has some limitations. It assumes that the trend is a smooth function, which may not be the case in some situations. It can also be sensitive to changes in the smoothing parameter λ, which may result in different trends for the same data. Additionally, the filter may produce unrealistic trends for very short time series.

Despite these limitations, the HP filter remains a valuable tool for analyzing economic and financial data. It is widely used by central banks and financial institutions to monitor long-term trends in the economy, and it can be used to identify turning points in the business cycle. The filter can also be used to analyze asset prices, exchange rates, and other financial variables.

The Hodrick-Prescott filter is a powerful tool for analyzing economic and financial data. It separates a time series into a trend component and a cyclical component, allowing for easy identification of long-term trends and turning points in the business cycle. While it has some limitations, it remains a valuable tool for economists, central banks, and financial institutions around the world.

█ Combined Application of Fourier Transform and Hodrick-Prescott Filter

The integration of the Fourier Transform and the Hodrick-Prescott Filter in financial time series analysis can offer several benefits. By first applying the HP Filter to the financial data, traders can remove short-term fluctuations and noise, effectively isolating the underlying trend. This smoothed data can then be subjected to the Fourier Transform, allowing for the identification of dominant cycles and frequencies with greater precision.

By combining these two powerful techniques, traders can gain a more comprehensive understanding of the underlying dynamics of financial time series. This enhanced knowledge can lead to the development of more effective trading strategies, better risk management, and ultimately, improved investment performance.

The Fourier Transform and the Hodrick-Prescott Filter are powerful tools for financial time series analysis. Each technique offers unique benefits, with the Fourier Transform being adept at identifying dominant cycles and frequencies, and the HP Filter excelling at isolating long-term trends from short-term noise. By combining these methodologies, traders can develop a deeper understanding of the underlying dynamics of financial time series, leading to more informed investment decisions and improved trading strategies. As the financial markets continue to evolve, the combined application of these techniques will undoubtedly remain an essential aspect of modern financial analysis.

█ Features

Endpointed and Non-repainting

This is an endpointed and non-repainting indicator. These are crucial factors that contribute to its usefulness and reliability in trading and investment strategies. Let us break down these concepts and discuss why they matter in the context of a financial indicator.

1. Endpoint nature: An endpoint indicator uses the most recent data points to calculate its values, ensuring that the output is timely and reflective of the current market conditions. This is in contrast to non-endpoint indicators, which may use earlier data points in their calculations, potentially leading to less timely or less relevant results. By utilizing the most recent data available, the endpoint nature of this indicator ensures that it remains up-to-date and relevant, providing traders and investors with valuable and actionable insights into the market dynamics.

2. Non-repainting characteristic: A non-repainting indicator is one that does not change its values or signals after they have been generated. This means that once a signal or a value has been plotted on the chart, it will remain there, and future data will not affect it. This is crucial for traders and investors, as it offers a sense of consistency and certainty when making decisions based on the indicator's output.

Repainting indicators, on the other hand, can change their values or signals as new data comes in, effectively "repainting" the past. This can be problematic for several reasons:

a. Misleading results: Repainting indicators can create the illusion of a highly accurate or successful trading system when backtesting, as the indicator may adapt its past signals to fit the historical price data. This can lead to overly optimistic performance results that may not hold up in real-time trading.

b. Decision-making uncertainty: When an indicator repaints, it becomes challenging for traders and investors to trust its signals, as the signal that prompted a trade may change or disappear after the fact. This can create confusion and indecision, making it difficult to execute a consistent trading strategy.

The endpoint and non-repainting characteristics of this indicator contribute to its overall reliability and effectiveness as a tool for trading and investment decision-making. By providing timely and consistent information, this indicator helps traders and investors make well-informed decisions that are less likely to be influenced by misleading or shifting data.

Inputs

Source: This input determines the source of the price data to be used for the calculations. Users can select from options like closing price, opening price, high, low, etc., based on their preferences. Changing the source of the price data (e.g., from closing price to opening price) will alter the base data used for calculations, which may lead to different patterns and cycles being identified.

Calculation Bars: This input represents the number of past bars used for the calculation. A higher value will use more historical data for the analysis, while a lower value will focus on more recent price data. Increasing the number of past bars used for calculation will incorporate more historical data into the analysis. This may lead to a more comprehensive understanding of long-term trends but could also result in a slower response to recent price changes. Decreasing this value will focus more on recent data, potentially making the indicator more responsive to short-term fluctuations.

Harmonic Period: This input represents the harmonic period, which is the number of harmonics used in the Fourier Transform. A higher value will result in more harmonics being used, potentially capturing more complex cycles in the price data. Increasing the harmonic period will include more harmonics in the Fourier Transform, potentially capturing more complex cycles in the price data. However, this may also introduce more noise and make it harder to identify clear patterns. Decreasing this value will focus on simpler cycles and may make the analysis clearer, but it might miss out on more complex patterns.

Frequency Tolerance: This input represents the frequency tolerance, which determines how close the frequencies of the harmonics must be to be considered part of the same cycle. A higher value will allow for more variation between harmonics, while a lower value will require the frequencies to be more similar. Increasing the frequency tolerance will allow for more variation between harmonics, potentially capturing a broader range of cycles. However, this may also introduce noise and make it more difficult to identify clear patterns. Decreasing this value will require the frequencies to be more similar, potentially making the analysis clearer, but it might miss out on some cycles.

Number of Bars to Render: This input determines the number of bars to render on the chart. A higher value will result in more historical data being displayed, but it may also slow down the computation due to the increased amount of data being processed. Increasing the number of bars to render on the chart will display more historical data, providing a broader context for the analysis. However, this may also slow down the computation due to the increased amount of data being processed. Decreasing this value will speed up the computation, but it will provide less historical context for the analysis.

Smoothing Mode: This input allows the user to choose between two smoothing modes for the source price data: no smoothing or Hodrick-Prescott (HP) smoothing. The choice depends on the user's preference for how the price data should be processed before the Fourier Transform is applied. Choosing between no smoothing and Hodrick-Prescott (HP) smoothing will affect the preprocessing of the price data. Using HP smoothing will remove some of the short-term fluctuations from the data, potentially making the analysis clearer and more focused on longer-term trends. Not using smoothing will retain the original price fluctuations, which may provide more detail but also introduce noise into the analysis.

Hodrick-Prescott Filter Period: This input represents the Hodrick-Prescott filter period, which is used if the user chooses to apply HP smoothing to the price data. A higher value will result in a smoother curve, while a lower value will retain more of the original price fluctuations. Increasing the Hodrick-Prescott filter period will result in a smoother curve for the price data, emphasizing longer-term trends and minimizing short-term fluctuations. Decreasing this value will retain more of the original price fluctuations, potentially providing more detail but also introducing noise into the analysis.

Alets and signals

This indicator featues alerts, signals and bar coloring. You have to option to turn these on/off in the settings menu.

Maximum Bars Restriction

This indicator requires a large amount of processing power to render on the chart. To reduce overhead, the setting "Number of Bars to Render" is set to 500 bars. You can adjust this to you liking.

█ Related Indicators and Libraries

Goertzel Cycle Composite Wave

Goertzel Browser

Fourier Spectrometer of Price w/ Extrapolation Forecast

Fourier Extrapolator of 'Caterpillar' SSA of Price

Normalized, Variety, Fast Fourier Transform Explorer

Real-Fast Fourier Transform of Price Oscillator

Real-Fast Fourier Transform of Price w/ Linear Regression

Fourier Extrapolation of Variety Moving Averages

Fourier Extrapolator of Variety RSI w/ Bollinger Bands

Fourier Extrapolator of Price w/ Projection Forecast

Fourier Extrapolator of Price

STD-Stepped Fast Cosine Transform Moving Average

Variety RSI of Fast Discrete Cosine Transform

loxfft

Breaker Blocks with Signals [LuxAlgo]The Breaker Blocks with Signals indicator aims to highlight a complete methodology based on breaker blocks. Breakout signals between the price and breaker blocks are highlighted and premium/discount swing levels are included to provide potential take profit/stop loss levels.

This script also includes alerts for each signal highlighted.

🔶 SETTINGS

🔹 Breaker Blocks

Length: Sensitivity of the detected swings used to construct breaker blocks. Higher values will return longer term breaker blocks.

Use only candle body: Only use the candle body when determining the maximum/minimum extremities of the order blocks.

Use 2 candles instead of 1: Use two candles to confirm the occurrence of a breaker block.

Stop at first break of center line: Do not highlight breakout signals after invalidation until reset.

🔹 PD Array

Only when E is in premium/discount zone: Only set breaker block if point E of wave ABCDE is within the corresponding zone.

Show premium discount zone: Show premium/discount zone.

Highlight Swing Break: Highlight occurrences of price breaking a previous swing level.

Show Swings/PD Arrays: Show swing levels/labels and pd areas.

🔶 USAGE

The Breaker Blocks with Signals indicator aims to provide users with a minimalistic display alongside optimal signals to be aware of for finding trade setups as shown below.

Here we can see a MSS occurred allowing the indicator to detect a Breaker Block (-BB) & display a red arrow to confirm this signal.

The signal(s) that can be used for potential entries are only during retests of the breaker blocks.

A potential strategy traders could use with this indicator is to target the corresponding Discount PD Arrays detected (for a short position) and Premium PD Arrays (for a long position).