Deadband Hysteresis Supertrend [BackQuant]Deadband Hysteresis Supertrend

A two-stage trend tool that first filters price with a deadband baseline, then runs a Supertrend around that baseline with optional flip hysteresis and ATR-based adverse exits.

What this is

A hybrid of two ideas:

Deadband Hysteresis Baseline that only advances when price pulls far enough from the baseline to matter. This suppresses micro noise and gives you a stable centerline.

Supertrend bands wrapped around that baseline instead of raw price. Flips are further gated by an extra margin so side changes are more deliberate.

The goal is fewer whipsaws in chop and clearer regime identification during trends.

How it works (high level)

Deadband step — compute a per-bar “deadband” size from one of four modes: ATR, Percent of price, Ticks, or Points. If price deviates from the baseline by more than this amount, move the baseline forward by a fraction of the excess. If not, hold the line.

Centered Supertrend — build upper and lower bands around the baseline using ATR and a user factor. Track the usual trailing logic that tightens a band while price moves in its favor.

Flip hysteresis — require price to exceed the active band by an extra flip offset × ATR before switching sides. This adds stickiness at the boundary.

Adverse exit — once a side is taken, trigger an exit if price moves against the entry by K × ATR .

If you would like to check out the filter by itself:

What it plots

DBHF baseline (optional) as a smooth centerline.

DBHF Supertrend as the active trailing band.

Candle coloring by trend side for quick read.

Signal markers 𝕃 and 𝕊 at flips plus ✖ on adverse exits.

Inputs that matter

Price Source — series being filtered. Close is typical. HL2 or HLC3 can be steadier.

Deadband mode — ATR, Percent, Ticks, or Points. This defines the “it’s big enough to matter” zone.

ATR Length / Mult (DBHF) — only used when mode = ATR. Larger values widen the do-nothing zone.

Percent / Ticks / Points — alternatives to ATR; pick what fits your market’s convention.

Enter Mult — scales the deadband you must clear before the baseline moves. Increase to filter more noise.

Response — fraction of the excess applied to baseline movement. Higher responds faster; lower is smoother.

Supertrend ATR Period & Factor — traditional band size controls; higher factor widens and flips less often.

Flip Offset ATR — extra ATR buffer required to flip. Useful in choppy regimes.

Adverse Stop K·ATR — per-trade danger brake that forces an exit if price moves K×ATR against entry.

UI — toggle baseline, supertrend, signals, and bar painting; choose long and short colors.

How to read it

Green regime — candles painted long and the Supertrend running below price. Pullbacks toward the baseline that fail to breach the opposite band often resume higher.

Red regime — candles painted short and the Supertrend running above price. Rallies that cannot reclaim the band may roll over.

Frequent side swaps — reduce sensitivity by increasing Enter Mult, using ATR mode, raising the Supertrend factor, or adding Flip Offset ATR.

Use cases

Bias filter — allow entries only in the direction of the current side. Use your preferred triggers inside that bias.

Trailing logic — treat the active band as a dynamic stop. If the side flips or an adverse K·ATR exit prints, reduce or close exposure.

Regime map — on higher timeframes, the combination baseline + band produces a clean up vs down template for allocation decisions.

Tuning guidance

Fast markets — ATR deadband, modest Enter Mult (0.8–1.2), response 0.2–0.35, Supertrend factor 1.7–2.2, small Flip Offset (0.2–0.5 ATR).

Choppy ranges — widen deadband or raise Enter Mult, lower response, and add more Flip Offset so flips require stronger evidence.

Slow trends — longer ATR periods and higher Supertrend factor to keep you on side longer; use a conservative adverse K.

Included alerts

DBHF ST Long — side flips to long.

DBHF ST Short — side flips to short.

Adverse Exit Long / Short — K·ATR stop triggers against the current side.

Strengths

Deadbanded baseline reduces micro whipsaws before Supertrend logic even begins.

Flip hysteresis adds a second layer of confirmation at the boundary.

Optional adverse ATR stop provides a uniform risk cut across assets and regimes.

Clear visuals and minimal parameters to adjust for symbol behavior.

Putting it together

Think of this tool as two decisions layered into one view. The deadband baseline answers “does this move even count,” then the Supertrend wrapped around that baseline answers “if it counts, which side should I be on and where do I flip.” When both parts agree you tend to stay on the correct side of a trend for longer, and when they disagree you get an early warning that conditions are changing.

When the baseline bends and price cannot reclaim the opposite band , momentum is usually continuing. Pullbacks into the baseline that stall before the far band often resolve in trend.

When the baseline flattens and the bands compress , expect indecision. Use the Flip Offset ATR to avoid reacting to the first feint. Wait for a clean band breach with follow through.

When an adverse K·ATR exit prints while the side has not flipped , treat it as a risk event rather than a full regime change. Many users cut size, re-enter only if the side reasserts, and let the next flip confirm a new trend.

Final thoughts

Deadband Hysteresis Supertrend is best read as a regime lens. The baseline defines your tolerance for noise, the bands define your trailing structure, and the flip offset plus adverse ATR stop define how forgiving or strict you want to be at the boundary. On strong trends it helps you hold through shallow shakeouts. In choppy conditions it encourages patience until price does something meaningful. Start with settings that reflect the cadence of your market, observe how often flips occur, then nudge the deadband and flip offset until the tool spends most of its time describing the move you care about rather than the noise in between.

Statistics

Fixed Range Volume Profile"Distribution of transaction volume by price group (transaction volume by price block)"

Instructions for use (Professional Manual)

1. a basic concept

By vertical axis (price), shows the cumulative trading volume traded in the segment.

The longer the block, the more transactions took place in that price range.

Colors distinguish between buying/selling strength (green = buying advantage, red = selling advantage).

2. Key components

POC (Point of Control)

→ Longest block (most traded price segment, "key selling point").

VAH / VAL (Value Area High/Low)

→ Top/bottom segments where approximately 70% of the total volume is formed.

→ Role of "Major Support/Resistance".

High Capacity Node (HVN)

→ Significantly higher trading volumes → strong support/resistance.

Low Volume Node (LVN)

→ Low volume section → areas where prices are easily passed.

3. practical application

Find Support/Resistance

The thickest block (POC) is used as a place where prices often rebound/resist.

a trading entry/liquidation strategy

Buy if the price is supported near HVN,

When breaking through the LVN, fast movement (gap movement) can be expected.

break/goal setting

Finger = Under the LVN,

Target = Next HVN.

Judgment of trends

When the block distribution is concentrated above, "Increase to Collection Section"

If you're driven below, you're "in a downtrend to a variance section."

4. Precautions

The volume distribution is "past data based" and is not an indicator of the future.

Rather than using it alone, it is more effective to combine with Fibonacci, trend lines, and candle patterns.

In particular, in the volatile market, the LVN breakthrough → may signal a surge/fall.

In summary, this block indicator is "a map showing the most market participants at any price point".

In other words, it is useful for finding support/resistance as a tool for analyzing sales and establishing the basis for trading strategies.

Crypto OI AgregatedCrypto OI Aggregated — Open Interest Aggregator for Crypto Exchanges

General Description

The indicator is designed for comprehensive analysis of Open Interest (OI) across major cryptocurrency exchanges. It consolidates data from multiple platforms, visualizes it as candlestick charts or deltas, and builds tables with breakdowns by exchange and contract type. This allows traders to quickly understand where market interest is concentrated and how the market structure is shifting.

Unlike standard tools that only show data from a single exchange, this indicator provides a full market overview and makes it easy to compare dynamics across different platforms.

⸻

Key Features

• Aggregation of OI data from exchanges: Binance, Bybit, OKX, Bitget, Kraken, HTX, Deribit (feel free to leave a comment if you’d like me to add other exchanges that provide open interest data)

• Support for contract types: USDT.P, USD.P, USDC.P, USD.PM

• Automatic normalization of various OI data formats from different providers

• Display modes:

• OI candlestick chart (total aggregated OI)

• OI Delta (change in OI per bar)

• Full table with detailed data by exchange and contract type

• Short summary table with totals in USD and base assets

• Support for USD or COIN denomination

• Convenient formatting for large numbers

• Customizable colors

⸻

How to Use the Indicator

1. Select Exchanges

In the settings, enable or disable specific exchanges. It is recommended to activate only the ones you need for analysis — this will make the indicator faster.

2. Choose Data Type

• OI — aggregated open interest from selected exchanges.

• OI delta — delta (change in OI compared to the previous bar).

3. Denomination

• USD — values are converted into USD equivalents.

• COIN — values are shown in the base asset (BTC, ETH, etc.).

4. Reading the Chart

• OI candlesticks show the overall OI dynamics.

• Delta histogram highlights how much OI has grown or decreased per bar.

• Colors are fully customizable.

5. Tables

• Enabled via the Show table option.

• Full Table → Rows = exchanges, Columns = contract types. Cells contain OI values in either USD or the base asset, depending on settings. Quickly shows where the main interest is concentrated.

• Short Table → Displays only the total OI values in USD and the base asset.

⸻

Important Notes

• For better readability of large values, two custom formatting functions were implemented. They work similarly to format.volume, but with improved digit grouping and adjustable decimal precision. In the tables, the top row is formatted using format.volume, while the bottom row uses the improved formatting functions for clearer representation.

str(d, n, s) =>

str.substring(d, 0, str.length(d) - n) + '.' + str.substring(d, str.length(d) - n, str.length(d) - (n - 2)) + s

format(_r) =>

d = str.tostring(math.round(_r))

str.length(d) > 9 ? str(d, 9, " B") : str.length(d) > 6 ? str(d, 6, " M") : str.length(d) > 3 ? str(d, 3, " K") : d

⸻

Conclusion: Crypto OI Aggregated is a convenient and powerful tool for cryptocurrency derivatives traders. It enables tracking of OI dynamics across multiple exchanges simultaneously, detecting imbalances between contracts, and identifying signals that are not visible when analyzing a single exchange.

Adaptive FoS LibraryThis library provides Adaptive Functions that I use in my scripts. For calculations, I use the max_bars_back function with a fixed length of 200 bars to prevent errors when a script tries to access data beyond its available history. This is a key difference from most other adaptive libraries — if you don’t need it, you don’t have to use it.

Some of the adaptive length functions are normalized. In addition to the adaptive length functions, this library includes various methods for calculating moving averages, normalized differences between fast and slow MA's, as well as several normalized oscillators.

High Probability Order Blocks [AlgoAlpha]🟠 OVERVIEW

This script detects and visualizes high-probability order blocks by combining a volatility-based z-score trigger with a statistical survival model inspired by Kaplan-Meier estimation. It builds and manages bullish and bearish order blocks dynamically on the chart, displays live survival probabilities per block, and plots optional rejection signals. What makes this tool unique is its use of historical mitigation behavior to estimate and plot how likely each zone is to persist, offering traders a probabilistic perspective on order block strength—something rarely seen in retail indicators.

🟠 CONCEPTS

Order blocks are regions of strong institutional interest, often marked by large imbalances between buying and selling. This script identifies those areas using z-score thresholds on directional distance (up or down candles), detecting statistically significant moves that signal potential smart money footprints. A bullish block is drawn when a strong up-move (zUp > 4) follows a down candle, and vice versa for bearish blocks. Over time, each block is evaluated: if price “mitigates” it (i.e., closes cleanly past the opposite side and confirmed with a 1 bar delay), it’s considered resolved and logged. These resolved blocks then inform a Kaplan-Meier-like survival curve, estimating the likelihood that future blocks of a given age will remain unbroken. The indicator then draws a probability curve for each side (bull/bear), updating it in real time.

🟠 FEATURES

Live label inside each block showing survival probability or “N.E.D.” if insufficient data.

Kaplan-Meier survival curves drawn directly on the chart to show estimated strength decay.

Rejection markers (▲ ▼) if price bounces cleanly off an active order block.

Alerts for zone creation and rejection signals, supporting rule-based trading workflows.

🟠 USAGE

Read the label inside each block for Age | Survival% (or N.E.D. if there aren’t enough samples yet); higher survival % suggests blocks of that age have historically lasted longer.

Use the right-side survival curves to gauge how probability decays with age for bull vs bear blocks, and align entries with the side showing stronger survival at current age.

Treat ▲ (bullish rejection) and ▼ (bearish rejection) as optional confluence when price tests a boundary and fails to break.

Turn on alerts for “Bullish Zone Created,” “Bearish Zone Created,” and rejection signals so you don’t need to watch constantly.

If your chart gets crowded, enable Prevent Overlap ; tune Max Box Age to your timeframe; and adjust KM Training Window / Minimum Samples to trade off responsiveness vs stability.

Stop Loss vs Take Profit Probability and EVThis stop loss and take profit calculator uses a Monte Carlo simulation to calculate the probability of hitting your Stop Loss or Take Profit levels across different time horizons (expressed in bars).

It provides data-driven insights to optimize your risk management and position sizing by showing Expected Value for each scenario.

As a quant, I love using statistical data to help my decisions and get better EV from my trades.

🔬 How It's Calculated

Monte Carlo Simulation: Runs 1,000-10,000 price simulations using a random walk model

Volatility Analysis: Combines ATR-based and Historical Volatility for accurate price movement modeling

Expected Value: Calculates profit/loss expectation using formula: (TP_Probability × Reward) - (SL_Probability × Risk)

Time Horizons: Tests multiple timeframes (1, 5, 10, 20, 50 bars) to find optimal holding periods

Risk/Reward Ratios: Automatically calculates and displays R:R ratios for quick assessment

💡 Use Cases

Position Sizing - Determine optimal risk per trade based on Expected Value

Time Horizon Optimization - Find the best holding period for your strategy

Stop Loss Placement - Validate SL levels using probability analysis

Take Profit Optimization - Set TP levels with statistical backing

Strategy Backtesting - Compare different R:R setups before entering trades

Risk Management - Avoid trades with negative Expected Value

Swing vs Day Trading - Choose timeframes with highest success probability

🎯 How to Use

Setup Trade: Enter your entry price, stop loss, and take profit levels

You can add or remove time horizons denominated in bars. Say you are looking at 1h candles, adding a 24-bar time horizon means you are looking into 24 hours

Choose Direction: Select Long or Short position

Review Table

Analyze Expected Value: Focus on positive EV scenarios (green background)

Optimize Timing: Select time horizons with best risk/reward profile

Adjust Parameters: Modify volatility calculation method and simulation count if needed

Examples

Here's how you can read the tables.

Example 1:

In this chart, we are analyzing the TP and SL probabilities as well as the EV (expected value) for a stock. I want to check what the likelihood is that my SL and TP get triggered over the next 5 days. The stock market is open for 6.5 hours per day, which is 13 bars in this 30-minute bar chart. 26 bars is 2 days, 39 bars is 3 days and so on.

Although this trade is more likely to trigger my SL than my TP, in some of the time horizons we have a positive expected value because of the risk/reward of our trade (i.e. distance of the SL and TP from the price) and the probability of hitting SL and TP.

Example 2:

In this example, we have applied the indicator to gold. Because the TP is much closer to the price, the probability of hitting the TP is much higher.

We can also observe that the expected Value in the shorter time frames is better than in the longer ones. This can give us some clues to set up our trade. If we know that the EV is positive, we can allocate more to that specific trade.

Enjoy, and please let me know your feedback! 😊🥂

ETFs Sector PerformanceDisplays a table of the Top 8 performing ETFs over a selected period (1M / 2M / 3M / 6M) to quickly identify industry strength.

Pre-Set Universe (39 ETFs)

ITA — iShares U.S. Aerospace & Defense ETF

DBA — Invesco DB Agriculture Fund

BOTZ — Global X Robotics & Artificial Intelligence ETF

JETS — U.S. Global Jets ETF

XLB — Materials Select Sector SPDR Fund

XBI — SPDR S&P Biotech ETF

PKB — Invesco Dynamic Building & Construction ETF

ICLN — iShares Global Clean Energy ETF

SKYY — First Trust Cloud Computing ETF

DBC — Invesco DB Commodity Index Tracking Fund

XLY — Consumer Discretionary Select Sector SPDR Fund

XLP — Consumer Staples Select Sector SPDR Fund

BLOK — Amplify Transformational Data Sharing ETF

KARS — KraneShares Electric Vehicles & Future Mobility ETF

XLE — Energy Select Sector SPDR Fund

ESPO — VanEck Video Gaming and eSports ETF

XLF — Financial Select Sector SPDR Fund

PBJ — Invesco Dynamic Food & Beverage ETF

ITB — iShares U.S. Home Construction ETF

XLI — Industrial Select Sector SPDR Fund

PAVE — Global X U.S. Infrastructure Development ETF

PEJ — Invesco Dynamic Leisure & Entertainment ETF

LIT — Global X Lithium & Battery Tech ETF

IHI — iShares U.S. Medical Devices ETF

XME — SPDR S&P Metals & Mining ETF

FCG — First Trust Natural Gas ETF

URA — Global X Uranium ETF

PPH — VanEck Pharmaceutical ETF

QTUM — Defiance Quantum Computing & Machine Learning ETF

IYR — iShares U.S. Real Estate ETF

XRT — SPDR S&P Retail ETF

SOXX — iShares Semiconductor ETF

BOAT — SonicShares Global Shipping ETF

IGV — iShares Expanded Tech-Software Sector ETF

TAN — Invesco Solar ETF

SLX — VanEck Steel ETF

IYZ — iShares U.S. Telecommunications ETF

IYT — iShares U.S. Transportation ETF

XLU — Utilities Select Sector SPDR Fund

Theil-Sen Line Filter [BackQuant]Theil-Sen Line Filter

A robust, median-slope baseline that tracks price while resisting outliers. Designed for the chart pane as a clean, adaptive reference line with optional candle coloring and slope-flip alerts.

What this is

A trend filter that estimates the underlying slope of price using a Theil-Sen style median of past slopes, then advances a baseline by a controlled fraction of that slope each bar. The result is a smooth line that reacts to real directional change while staying calm through noise, gaps, and single-bar shocks.

Why Theil-Sen

Classical moving averages are sensitive to outliers and shape changes. Ordinary least squares is sensitive to large residuals. The Theil-Sen idea replaces a single fragile estimate with the median of many simple slopes, which is statistically robust and less influenced by a few extreme bars. That makes the baseline steadier in choppy conditions and cleaner around regime turns.

What it plots

Filtered baseline that advances by a fraction of the robust slope each bar.

Optional candle coloring by baseline slope sign for quick trend read.

Alerts when the baseline slope turns up or down.

How it behaves (high level)

Looks back over a fixed window and forms many “current vs past” bar-to-bar slopes.

Takes the median of those slopes to get a robust estimate for the bar.

Optionally caps the magnitude of that per-bar slope so a single volatile bar cannot yank the line.

Moves the baseline forward by a user-controlled fraction of the estimated slope. Lower fractions are smoother. Higher fractions are more responsive.

Inputs and what they do

Price Source — the series the filter tracks. Typical is close; HL2 or HLC3 can be smoother.

Window Length — how many bars to consider for slopes. Larger windows are steadier and slower. Smaller windows are quicker and noisier.

Response — fraction of the estimated slope applied each bar. 1.00 follows the robust slope closely; values below 1.00 dampen moves.

Slope Cap Mode — optional guardrail on each bar’s slope:

None — no cap.

ATR — cap scales with recent true range.

Percent — cap scales with price level.

Points — fixed absolute cap in price points.

ATR Length / Mult, Cap Percent, Cap Points — tune the chosen cap mode’s size.

UI Settings — show or hide the line, paint candles by slope, choose long and short colors.

How to read it

Up-slope baseline and green candles indicate a rising robust trend. Pullbacks that do not flip the slope often resolve in trend direction.

Down-slope baseline and red candles indicate a falling robust trend. Bounces against the slope are lower-probability until proven otherwise.

Flat or frequent flips suggest a range. Increase window length or decrease response if you want fewer whipsaws in sideways markets.

Use cases

Bias filter — only take longs when slope is up, shorts when slope is down. It is a simple way to gate faster setups.

Stop or trail reference — use the line as a trailing guide. If price closes beyond the line and the slope flips, consider reducing exposure.

Regime detector — widen the window on higher timeframes to define major up vs down regimes for asset rotation or risk toggles.

Noise control — enable a cap mode in very volatile symbols to retain the line’s continuity through event bars.

Tuning guidance

Quick swing trading — shorter window, higher response, optionally add a percent cap to keep it stable on large moves.

Position trading — longer window, moderate response. ATR cap tends to scale well across cycles.

Low-liquidity or gappy charts — prefer longer window and a points or ATR cap. That reduces jumpiness around discontinuities.

Alerts included

Theil-Sen Up Slope — baseline’s one-bar change crosses above zero.

Theil-Sen Down Slope — baseline’s one-bar change crosses below zero.

Strengths

Robust to outliers through median-based slope estimation.

Continuously advances with price rather than re-anchoring, which reduces lag at turns.

User-selectable slope caps to tame shock bars without over-smoothing everything.

Minimal visuals with optional candle painting for fast regime recognition.

Notes

This is a filter, not a trading system. It does not account for execution, spreads, or gaps. Pair it with entry logic, risk management, and higher-timeframe context if you plan to use it for decisions.

Supertrend [TradingConToto]Supertrend — ADX/DI + EMA Gap + Breakout (with Mobile UI)

What makes it original

Supertrend combines trend strength (ADX/DI), multi-timeframe bias (EMA63 and EMA 200D equivalent), a structural filter based on the distance between EMA2400 and EMA4800 expressed in ATR units, and a momentum confirmation through a previous high breakout.

This is not a random mashup — it’s a sequence of filters designed to reduce trades in ranging markets and prioritize mature trends:

Direction: +DI > -DI (trend led by buyers).

Strength: ADX > mean(ADX) (avoids weak, choppy phases).

Short-term bias: Close > EMA63.

Long-term bias: Close > EMA4800 ≈ EMA200 daily on H1.

Momentum: Close > High (immediate breakout).

Structure: (EMA2400 − EMA4800) > k·ATR (ensures separation in ATR units, filters out flat phases).

Entries & exits

Entry: when all six conditions are met and no open position exists.

Exit: if +DI < -DI or Close < EMA63.

Visuals: EMA63 is painted green while in position and red otherwise, with a supertrend-style band; “BUY” labels appear below the green band and “SELL” labels above the red band.

UI: includes a compact table (mobile-friendly) showing the state of each condition.

Default parameters used in this publication

Initial capital: 10,000

Position size: 10% of equity (≤10% per trade is considered sustainable).

Commission: 0.01% per side (adjust to your broker/market).

Slippage: 1 tick

Pyramiding: 0 (only one position at a time)

Adjust commission/slippage to match your market. For US equities, commissions are often per share; for spot crypto, 0.10–0.20% total is common. I publish with 0.01% per side as a conservative example to avoid overestimating results.

Recommended backtest dataset

Timeframe: H1

Multi-cycle window (e.g. 2015–today)

Symbols with high liquidity (e.g. NASDAQ-100 large caps, or BTC/ETH spot) to generate 100+ trades. Avoid cherry-picked short windows.

Why each filter matters

+DI > -DI + ADX > mean: reduce counter-trend trades and weak signals.

Close > EMA63 + Close > EMA4800: enforce trend alignment in short and long horizons.

Breakout High : requires immediate momentum, avoids early entries.

EMA gap in ATR units: blocks flat or compressed structures where EMA200D aligns with price.

Limitations

The breakout filter may skip healthy pullbacks; the design prioritizes continuation over perfect entry price.

No fixed trailing stop/TP; exits depend on trend degradation via DI/EMA63.

Results vary with real costs (commissions, slippage, funding). Adjust defaults to your broker.

How to use

Apply it on a clean chart (no other indicators when publishing).

Keep in mind the default parameters above; if you change them, mention it in your notes and use the same values in the Strategy Tester.

Ensure your dataset produces 100+ trades for statistical validity.

Retail Sentiment Indicator - Multi-Asset CFD & Fear/Greed IndexRetail Sentiment Indicator - Multi-Asset CFD & Fear/Greed Index

Overview

The Retail Sentiment Indicator provides real-time sentiment data for major financial instruments including stocks, forex, commodities, and cryptocurrencies. This indicator displays retail trader positioning and market sentiment using CFD data and fear/greed indices.

Methodology and Scale Calculation

This indicator operates on a **-50 to +50 scale** with zero representing perfect market equilibrium.

Scale Interpretation:

- **Zero (0)**: Market balance - exactly 50% of investors buying, 50% selling

- **Positive values**: Majority buying pressure

- Example: If 63% of investors are buying, the indicator shows +13 (63 - 50 = +13)

- **Negative values**: Majority selling pressure

- Example: If 92% of investors are selling, the indicator shows -42 (50 - 92 = -42)

BTC Fear & Greed Index Scaling:

The original `BTC FEAR&GREED` index is natively scaled from 0-100 by its creator. In our indicator, this data has been rescaled to also fit the -50 to +50 range for consistency with other sentiment data sources.

This unified scaling approach allows for direct comparison across all instruments and data sources within the indicator.

-Important Data Source Selection-

Bitcoin (BTC) Data Sources

When viewing Bitcoin charts, the indicator offers **two different data sources**:

1. **Default Auto-Mode**: `BTCUSD Retail CFD` - Retail CFD traders sentiment data (automatically loaded).

2. **Manual Selection**: `BTC FEAR&GREED` - Fear & Greed Index from website: alternative dot me

**To access BTC Fear & Greed Index**: Input settings -> disable checkbox "Auto-load Sentiment Data" -> manually select "BTC FEAR&GREED" from the dropdown menu.

US Stock Market Data Sources

For US stocks and indices (S&P 500, NASDAQ, Dow Jones), there are **two data source options**:

1. **Default Auto-Mode**: Individual retail CFD sentiment data for each instrument

2. **Manual Selection**: `SNN FEAR&GREED` - SNN's Fear & Greed Index covering the overall US market sentiment. SNN was used as the name to avoid any potential trademark infringement.

**To access SNN Fear & Greed Index**: When viewing US market charts, disable in input settings checkbox "Auto-load Sentiment Data" and manually select "SNN FEAR&GREED" from the dropdown menu.

This distinction allows traders to choose between **instrument-specific retail sentiment** (auto-mode) or **broader market sentiment indices** (manual selection).

Features

- **Auto-Detection**: Automatically loads sentiment data based on the current chart symbol

- **Manual Selection**: Choose from 40+ supported instruments when auto-detection is unavailable

- **Multiple Data Sources**: Combines retail CFD sentiment with Fear & Greed indices

- **Visual Zones**: Clear greed/fear zones with color-coded backgrounds

- **Real-time Updates**: Live sentiment data from merged data sources

Supported Instruments

Major Indices

- S&P 500, NASDAQ, Dow Jones 30, DAX

Forex Pairs

- Major pairs: EURUSD, GBPUSD, USDJPY, USDCHF, USDCAD

- Cross pairs: EURJPY, GBPJPY, AUDUSD, NZDUSD, and 20+ others

Commodities

- Precious metals: Gold (XAUUSD), Silver (XAGUSD)

- Energy: WTI Oil

- Agricultural: Wheat, Coffee

- Industrial: Copper

Cryptocurrencies

- Bitcoin (BTC) sentiment data

- BTC & SNN Fear & Greed indices

How to Use

1. **Auto Mode** (Default): Enable "Auto-load Sentiment Data" to automatically display sentiment for the current chart symbol

2. **Manual Mode**: Disable auto-load and select from the dropdown menu for specific instruments

3. **Interpretation**:

- Values above 0 (green) indicate retail greed/bullish sentiment

- Values below 0 (red) indicate retail fear/bearish sentiment

- Fear & Greed indices use 0-100 scale (50 is neutral)

Data Sources

This indicator uses curated sentiment data from retail CFD providers and established fear/greed indices. Data is updated regularly and sourced from reputable financial data providers.

Trading Strategy & Market Philosophy

Contrarian Trading Approach

The primary purpose of this indicator is based on the fundamental market principle that **the majority of retail investors are often wrong**, and markets typically move opposite to the positions held by the majority of market participants.

Key Strategy Guidelines:

- **Contrarian Signal**: When the majority of users are positioned on one side of the market, there is statistically greater market advantage in taking positions in the opposite direction

- **Trend Exhaustion Signal**: An interesting observed phenomenon occurs when, during a long-lasting trend where the majority of investors have consistently been on the wrong side, the Sentiment indicator suddenly shows that the majority has flipped and opened positions in the direction of that long-running trend. This is often a signal of fuel exhaustion for further movement in that direction

Interpretation Examples

- High greed readings (majority bullish) → Consider bearish opportunities

- High fear readings (majority bearish) → Consider bullish opportunities

- Sudden sentiment flip during established trends → Potential trend reversal signal

Technical Notes

- Built with PineScript v6

- Dynamic symbol detection with fallback options

- Optimized for performance with minimal resource usage

- Color-coded visualization with customizable zones

Data Sources & Expansion

Acknowledgments

We extend our gratitude to **TradingView** for enabling the use of custom data feeds based on GitHub repositories, making this comprehensive sentiment analysis possible.

Data Expansion Opportunities

As the operator of this indicator, I am **open to suggestions for new data sources** that could be integrated and published. If you have ideas for additional instruments or sentiment data:

How to Submit Suggestions:

1. Send a **private message** with your proposal

2. Include: **instrument/data type**, **source**, and **brief description**

3. If technically feasible, we will work to import and publish the data

Data Infrastructure Status

Current Data Upload Process:

Please note that sentiment data uploads may occasionally experience minor interruptions. However, this should not pose significant issues as sentiment data typically changes gradually rather than rapidly.

Infrastructure Development:

We are actively working on establishing permanent cloud-based infrastructure to ensure continuous, automated data collection and upload processes. This will provide more reliable and consistent data availability in the future.

Disclaimer

This indicator is for educational and informational purposes only. Sentiment data should be used as part of a comprehensive trading strategy and not as the sole basis for trading decisions. Past performance does not guarantee future results. The contrarian approach described is a market theory and may not always produce profitable results.

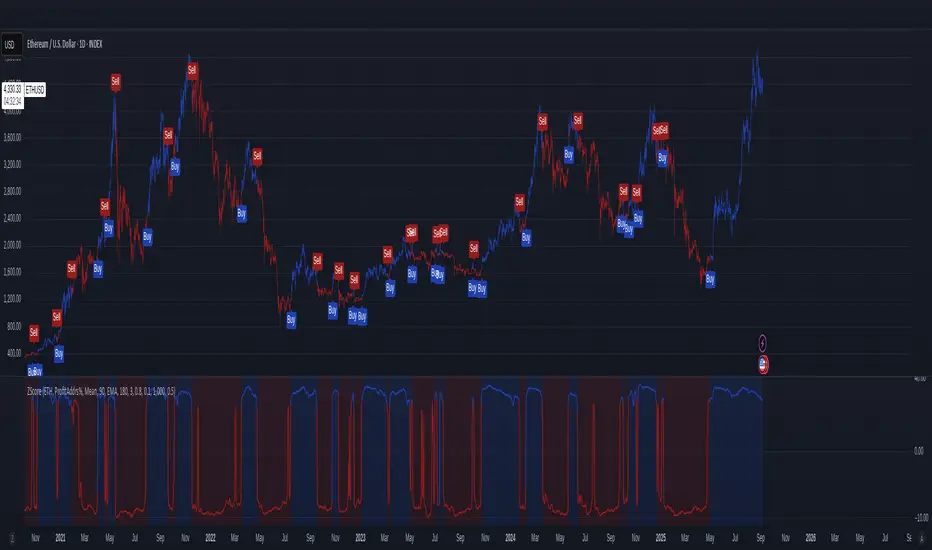

On-Chain Metrics & Z-Mode SelectionThis indicator provides an on-chain metric analysis framework for cryptocurrencies (currently limited to) BTC and ETH; allowing users to select from popular metrics such as SOPR, Profit Addresses %, NUPL, or MVRV.

It enables various analyses on the chosen metric to capture momentum and rate of change dynamics over time.

Analyses include:

Normalization techniques utilizing Mean or Median with standard deviation, as well as a 'Robust' method using interquartile range-based Z-scoring to accommodate skewed distributions, or raw values without normalization.

An optional differential calculation that highlights the rate of change (first derivative) of the metric.

Moving average smoothing with up to two passes, supporting EMA, SMA, or WMA types.

Optional sigmoid-based compression that scales and centers the indicator output, improving interpretability, mitigating extreme outliers, and allowing the user to scale the output so that the step size or increment of the long and short thresholds remains within a workable range.

Buy and sell signals are generated based on configurable long and short thresholds applied to the processed output.

Visual components such as trend colouring, threshold lines, background shading, and labels make it simple for traders to identify entry signals.

This indicator is suitable for those looking to integrate blockchain behavioral insights into their trading decisions.

Overall, this script transforms complex on-chain data into actionable trade signals by combining adaptive normalization and smoothing techniques. Its versatility and multi-metric support make it a valuable tool for both market monitoring and strategy development.

No financial decisions should be made based solely on this indicator. Always conduct your own research. .

Acknowledgements

Inspiration drawn from: CipherDecoded

Rolling Performance Toolkit (Returns, Correlation and Sharpe)This script provides a flexible toolkit for evaluating rolling performance metrics between any asset and a benchmark.

Features:

Library-based: Built on a custom utilities library for consistent return and statistics calculations.

Rolling Window Control: Choose the lookback period (in days) to calculate metrics.

Multiple Modes: Toggle between Rolling Returns, Rolling Correlation, and Rolling Sharpe Ratio.

Benchmark Comparison: Compare your selected ticker against a benchmark (default: S&P 500 / SPX), but you can easily switch to any symbol.

Risk-Free Rate Options: Choose from zero, a constant annual % rate, or a proxy symbol (default: US03M – 3-Month Treasury Yield).

Annualized Sharpe: Sharpe ratios are annualized by default (×√252) for intuitive interpretation.

This tool is useful for traders and investors who want to monitor relative performance, diversification benefits, or risk-adjusted returns over time.

utilitiesLibrary for commonly used utilities, for visualizing rolling returns, correlations and sharpe

Deadband Hysteresis Filter [BackQuant]Deadband Hysteresis Filter

What this is

This tool builds a “debounced” price baseline that ignores small fluctuations and only reacts when price meaningfully departs from its recent path. It uses a deadband to define how much deviation matters and a hysteresis scheme to avoid rapid flip-flops around the decision boundary. The baseline’s slope provides a simple trend cue, used to color candles and to trigger up and down alerts.

Why deadband and hysteresis help

They filter micro noise so the baseline does not react to every tiny tick.

They stabilize state changes. Hysteresis means the rule to start moving is stricter than the rule to keep holding, which reduces whipsaw.

They produce a stepped, readable path that advances during sustained moves and stays flat during chop.

How it works (conceptual)

At each bar the script maintains a running baseline dbhf and compares it to the input price p .

Compute a base threshold baseTau using the selected mode (ATR, Percent, Ticks, or Points).

Build an enter band tauEnter = baseTau × Enter Mult and an exit band tauExit = baseTau × Exit Mult where typically Exit Mult < Enter Mult .

Let diff = p − dbhf .

If diff > +tauEnter , raise the baseline by response × (diff − tauEnter) .

If diff < −tauEnter , lower the baseline by response × (diff + tauEnter) .

Otherwise, hold the prior value.

Trend state is derived from slope: dbhf > dbhf → up trend, dbhf < dbhf → down trend.

Inputs and what they control

Threshold mode

ATR — baseTau = ATR(atrLen) × atrMult . Adapts to volatility. Useful when regimes change.

Percent — baseTau = |price| × pctThresh% . Scale-free across symbols of different prices.

Ticks — baseTau = syminfo.mintick × tickThresh . Good for futures where tick size matters.

Points — baseTau = ptsThresh . Fixed distance in price units.

Band multipliers and response

Enter Mult — outer band. Price must travel at least this far from the baseline before an update occurs. Larger values reject more noise but increase lag.

Exit Mult — inner band for hysteresis. Keep this smaller than Enter Mult to create a hold zone that resists small re-entries.

Response — step size when outside the enter band. Higher response tracks faster; lower response is smoother.

UI settings

Show Filtered Price — plots the baseline on price.

Paint candles — colors bars by the filtered slope using your long/short colors.

How it can be used

Trend qualifier — take entries only in the direction of the baseline slope and skip trades against it.

Debounced crossovers — use the baseline as a stabilized surrogate for price in moving-average or channel crossover rules.

Trailing logic — trail stops a small distance beyond the baseline so small pullbacks do not eject the trade.

Session aware filtering — widen Enter Mult or switch to ATR mode for volatile sessions; tighten in quiet sessions.

Parameter interactions and tuning

Enter Mult vs Response — both govern sensitivity. If you see too many flips, increase Enter Mult or reduce Response. If turns feel late, do the opposite.

Exit Mult — widening the gap between Enter and Exit expands the hold zone and reduces oscillation around the threshold.

Mode choice — ATR adapts automatically; Percent keeps behavior consistent across instruments; Ticks or Points are useful when you think in fixed increments.

Timeframe coupling — on higher timeframes you can often lower Enter Mult or raise Response because raw noise is already reduced.

Concrete starter recipes

General purpose — ATR mode, atrLen=14 , atrMult=1.0–1.5 , Enter=1.0 , Exit=0.5 , Response=0.20 . Balanced noise rejection and lag.

Choppy range filter — ATR mode, increase atrMult to 2.0, keep Response≈0.15 . Stronger suppression of micro-moves.

Fast intraday — Percent mode, pctThresh=0.1–0.3 , Enter=1.0 , Exit=0.4–0.6 , Response=0.30–0.40 . Quicker turns for scalping.

Futures ticks — Ticks mode, set tickThresh to a few spreads beyond typical noise; start with Enter=1.0 , Exit=0.5 , Response=0.25 .

Strengths

Clear, explainable logic with an explicit noise budget.

Multiple threshold modes so the same tool fits equities, futures, and crypto.

Built-in hysteresis that reduces flip-flop near the boundary.

Slope-based coloring and alerts that make state changes obvious in real time.

Limitations and notes

All filters add lag. Larger thresholds and smaller response trade faster reaction for fewer false turns.

Fixed Points or Ticks can under- or over-filter when volatility regime shifts. ATR adapts, but will also expand bands during spikes.

On extremely choppy symbols, even a well tuned band will step frequently. Widen Enter Mult or reduce Response if needed.

This is a chart study. It does not include commissions, slippage, funding, or gap risks.

Alerts

DBHF Up Slope — baseline turns from down to up on the latest bar.

DBHF Down Slope — baseline turns from up to down on the latest bar.

Implementation details worth knowing

Initialization sets the baseline to the first observed price to avoid a cold-start jump.

Slope is evaluated bar-to-bar. The up and down alerts check for a change of slope rather than raw price crossings.

Candle colors and the baseline plot share the same long/short palette with transparency applied to the line.

Practical workflow

Pick a mode that matches how you think about distance. ATR for volatility aware, Percent for scale-free, Ticks or Points for fixed increments.

Tune Enter Mult until the number of flips feels appropriate for your timeframe.

Set Exit Mult clearly below Enter Mult to create a real hold zone.

Adjust Response last to control “how fast” the baseline chases price once it decides to move.

Final thoughts

Deadband plus hysteresis gives you a principled way to “only care when it matters.” With a sensible threshold and response, the filter yields a stable, low-chop trend cue you can use directly for bias or plug into your own entries, exits, and risk rules.

Logit Transform -EasyNeuro-Logit Transform

This script implements a novel indicator inspired by the Fisher Transform, replacing its core arctanh-based mapping with the logit transform. It is designed to highlight extreme values in bounded inputs from a probabilistic and statistical perspective.

Background: Fisher Transform

The Fisher Transform, introduced by John Ehlers , is a statistical technique that maps a bounded variable x (between a and b) to a variable approximately following a Gaussian distribution. The standard form for a normalized input y (between -1 and 1) is F(y) = 0.5 * ln((1 + y)/(1 - y)) = arctanh(y).

This transformation has the following properties:

Linearization of extremes:

Small deviations around the mean are smooth, while movements near the boundaries are sharply amplified.

Gaussian approximation:

After transformation, the variable approximates a normal distribution, enabling analytical techniques that assume normality.

Probabilistic interpretation:

The Fisher Transform can be linked to likelihood ratio tests, where the transform emphasizes deviations from median or expected values in a statistically meaningful way.

In technical analysis, this allows traders to detect turning points or extreme market conditions more clearly than raw oscillators alone.

Logit Transform as a Generalization

The logit function is defined for p between 0 and 1 as logit(p) = ln(p / (1 - p)).

Key properties of the logit transform:

Maps probabilities in (0, 1) to the entire real line, similar to the Fisher Transform.

Emphasizes values near 0 and 1, providing sharp differentiation of extreme states.

Directly interpretable in terms of odds and likelihood ratios: logit(p) = ln(odds).

From a statistical viewpoint, the logit transform corresponds to the canonical link function in binomial generalized linear models (GLMs). This provides a natural interpretation of the transformed variable as the logarithm of the likelihood ratio between success and failure states, giving a rigorous probabilistic framework for extreme value detection.

Theoretical Advantages

Distributional linearization:

For inputs that can be interpreted as probabilities, the logit transform creates a variable approximately linear in log-odds, similar to Fisher’s goal of Gaussianization but with a probabilistic foundation.

Extreme sensitivity:

By amplifying small differences near 0 or 1, it allows for sharper detection of market extremes or overbought/oversold conditions.

Statistical interpretability:

Provides a link to statistical hypothesis testing via likelihood ratios, enabling integration with probabilistic models or risk metrics.

Applications in Technical Analysis

Oscillator enhancement:

Apply to RSI, Stochastic Oscillators, or other bounded indicators to accentuate extreme values with a well-defined probabilistic interpretation.

Comparative study:

Use alongside the Fisher Transform to analyze the effect of different nonlinear mappings on market signals, helping to uncover subtle nonlinearity in price behavior.

Probabilistic risk assessment:

Transforming input series into log-odds allows incorporation into statistical risk models or volatility estimation frameworks.

Practical Considerations

The logit diverges near 0 and 1, requiring careful scaling or smoothing to avoid numerical instability. As with the Fisher Transform, this indicator is not a standalone trading signal and should be combined with complementary technical or statistical indicators.

In summary, the Logit Transform builds upon the Fisher Transform’s theoretical foundation while introducing a probabilistically rigorous mapping. By connecting extreme-value detection to odds ratios and likelihood principles, it provides traders and analysts with a mathematically grounded tool for examining market dynamics.

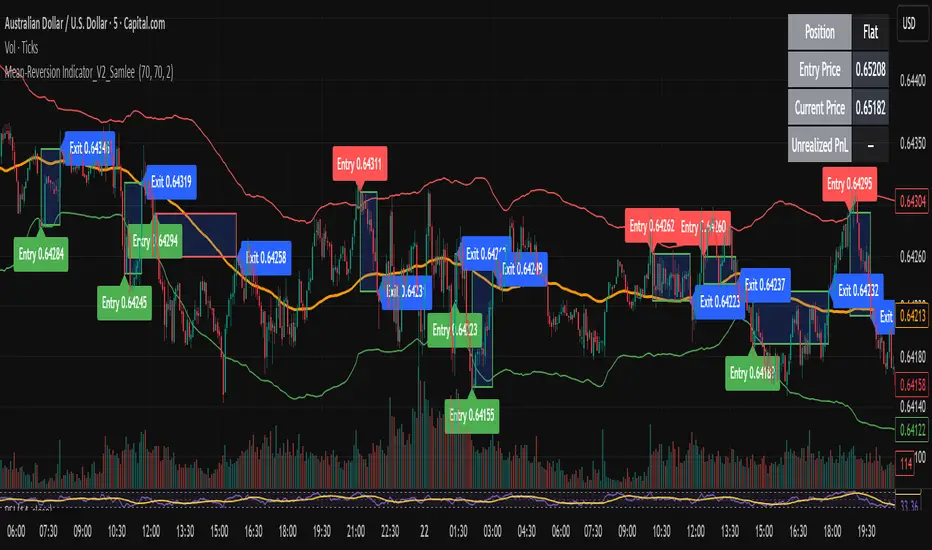

Mean-Reversion Indicator_V2_SamleeOverview

This is the second version of my mean reversion indicator. It combines a moving average with adaptive standard deviation bands to detect when the price deviates significantly from its mean. The script provides automatic entry/exit signals, real-time PnL tracking, and shaded trade zones to make mean reversion trading more intuitive.

Core Logic

Mean benchmark: Simple Moving Average (MA).

Volatility bands: Standard deviation of the spread (close − MA) defines upper and lower bands.

Trading rules:

Price breaks below the lower band → Enter Long

Price breaks above the upper band → Enter Short

Price reverts to MA → Exit position

What’s different vs. classic Bollinger/Keltner

Bandwidth is based on the standard deviation of the price–MA spread, not raw closing prices.

Entry signals use previous-bar confirmation to reduce intrabar noise.

Exit rule is a mean-touch condition, rather than fixed profit/loss targets.

Enhanced visualization:

A shaded box dynamically shows the distance between entry and current/exit price, making it easy to see profit/loss zones over the holding period.

Instant PnL labels display current position side (Long/Short/Flat) and live profit/loss in both pips and %.

Entry and exit points are clearly marked on the chart with labels and exact prices.

These visualization tools go beyond what most indicators provide, giving traders a clearer, more practical view of trade evolution.

Key Features

Automatic detection of position status (Long / Short / Flat).

Chart labels for entries (“Entry”) and exits (“Exit”).

Real-time floating PnL calculation in both pips and %.

Info panel (top-right) showing entry price, current price, position side, and PnL.

Dynamic shading between entry and current/exit price to visualize profit/loss zones.

Usage Notes & Risk

Mean reversion may underperform in strong trending markets; parameters (len_ma, len_std, mult) should be validated per instrument and timeframe.

Works best on relatively stable, mean-reverting pairs (e.g., AUDNZD).

Risk management is essential: use independent stop-loss rules (e.g., limit risk to 1–2% of equity per trade).

This script is provided for educational purposes only and is not financial advice.

Volatility % Bands (O→C)Volatility % Bands (O→C) is an indicator designed to visualize the percentage change from Open to Close of each candle, providing a clear view of short-term momentum and volatility.

**Histogram**: Displays bar-by-bar % change (Close vs Open). Green bars indicate positive changes, while red bars indicate negative ones, making momentum shifts easy to identify.

**Moving Average Line**: Plots the Simple Moving Average (SMA) of the absolute % change, helping traders track the average volatility over a chosen period.

**Background Bands**: Based on the user-defined Level Step, ±1 to ±5 zones are highlighted as shaded bands, allowing quick recognition of whether volatility is low, moderate, or extreme.

**Label**: Shows the latest candle’s % change and the current SMA value as a floating label on the right, making it convenient for real-time monitoring.

This tool can be useful for volatility breakout strategies, day trading, and short-term momentum analysis.

Machine Learning Z-Score Buy and Sell [SS]Hey everyone,

Releasing this Z-Score based buy and sell indicator.

What it does

This indicator:

Uses Z-score and trend to identify potential buy and sell areas.

Signals those buy and sell areas and provides a target price based on the mean.

Plots the target price for buy and sell signals as a red line (for sell signals) or green line (for buy signals).

Has some "machine learning" aspects, namely, it is able to auto select its lookback length based on its analysis of the trend using Pienscript's trend correlation function iterated over multiple lengths, in order for the indicator to identify:

a) The strongest trend; and

b) The correct target price

What is Z-Score

Z-Score is a measure of the mean. Thus, this is a mean reverting type strategy, as it uses z-score to determine price's distance from the mean (or a Z-Score of 0) and then it looks at historic deviations from the mean to signal the buy and sell signals (i.e. how far has price traditionally drifted from the mean before reverting).

Z-Score is a powerful tool in this sense, and if you folow my other indicators, you will know how much I love Z-score!

How to use the indicator

If you want to use the full Machine Learning capabilities of the indicator, its best to just leave all default settings. These default settings will automatically adjust the mean target price and buy and sell signals to align with the current price action.

If you want to be more aggressive in your

Target Price; and

Signals

Then you can opt to manually input a lookback length and mean reversion standard deviation. However, I generally suggest to avoid this as you are then making your own determination of trend by qualitative assessment. It can work, but its just not suggested.

In the input menu, you will see the option to "Manually select lookback" thus over-riding the auto-determination of trend and targets.

You will also see "manual pullback" enabler and "Pullback Standard Deviation". You can set your pullback standard deviation if you want to be more aggressive. The indicator will naturally shift to conservative target prices based on a neutral mean. However, if you want to increase the aggressiveness of the target price, you can increase or decrease the pullback standard deviation.

General Tips about Manually Adjusting Pullback Target

Here are some tips if you want to manually adjust the pullback targets:

The pullback target needs to be in a standard deviation value, this can be anywhere from 0 to 4 or 0 to -4 (you can theoretically go higher but its not really realistic). You can also do decimals, so 1.5 or 1.25 etc.

To determine whether you should be doing negative or positive standard deviation, you should determine the trend. If it is a downtrend and you are looking to short the rips, you will want to select a negative number, like -1.

If it is an uptrend and you want to buy the dips, you should be selecting a positive number, like 1 or 1.5.

Again, I do suggest leaving the indicator to decide for itself, but the options are there for those who wish.

Overall strategy

This is a mean reverting strategy. So if you are a mean reversion trader, this may be of particular interest to you.

Optional

Optionally, you can have the indicator plot the target prices or not, simply toggle this functionality off or on in the settings menu.

Concluding remarks

That is the indicator in a nutshell!

I hope you enjoy it and find it helpful.

Feel free to check out my other Z-Score based indicators if you find this interesting or want to learn more about the power of Z-Score in trading!

Thanks all and safe trades!

Simple MADSimple MAD is a lightweight and customizable indicator that calculates the Median Absolute Deviation (MAD) over a configurable period to measure market volatility. It dynamically displays Stop-Loss (SL) and Take-Profit (TP) levels based on MAD multipliers, both in absolute price and percentage terms.

The indicator includes a clean, watermark-style table with full layout controls — allowing you to adjust position, text size, alignment, and colors. It supports both manual entry price and automatic use of the latest close, making it ideal for traders who want to manage risk with precision and clarity.

Perfect for swing traders, volatility-based strategies, and anyone looking to integrate MAD into their decision-making.

Date Range Performance

Calculates total change and percentage change between two dates.

Computes average change per bar and per day.

Offers arithmetic and geometric daily %.

Supports auto mode (last N trading days) and manual date range.

Displays results as a watermark on the chart.