MG Universal model🚀 Summary🚀

The MG univerasal model is a composite of various items such as RSI, price Z-Score, Sharpe Ratio, Sortino Ratio, Omega Ratio, etc

Each component is normalized and then equally wheighted out to perform a global metric.

At the end, an Exponential Moving Average is added on the global metric.

You can easily find a description of each component on the internet, for the Crosby Ratio, it's a metric that comes from bitcoinmagazinepro.com.

✨ Key Features ✨

🗡 Smoothed Global Metric

Using a Moving average to smooth out the whole aggregated metric.

🗡 Bands Zone at extreme levels

Automatically displaying bands at top and bottom levels of the oscillator.

🗡 Normalizing components

Each component is normalized.

🗡 DataTable

Optional DataTable is available to check the score for each components and their related Z-Score.

📊 How I use it 📊

When catching up with 0 line (midline), crossing it :

if it goes above 0.2:

get out when it crosses 0.2 again

else:

get out when it crosses 0 again

That's the way I use it, may be there is a better way, FAFO :)

❓ Seeing a bug or an issue ❓

Feel free to DM me if you see a component that seems badly calculated.

I will be happy to fix it.

❗❗ Disclaimer ❗❗

This is a single indicator, even though it's aggregating many, do not use it as a standalone.

Past performance is not indicative of future results.

Always backtest, check, and align parameters before live trading.

Statistics

Prop Firm Business SimulatorThe prop firm business simulator is exactly what it sounds like. It's a plug and play tool to test out any tradingview strategy and simulate hypothetical performance on CFD Prop Firms.

Now what is a modern day CFD Prop Firm?

These companies sell simulated trading challenges for a challenge fee. If you complete the challenge you get access to simulated capital and you get a portion of the profits you make on those accounts payed out.

I've included some popular firms in the code as presets so it's easy to simulate them. Take into account that this info will likely be out of date soon as these prices and challenge conditions change.

Also, this tool will never be able to 100% simulate prop firm conditions and all their rules. All I aim to do with this tool is provide estimations.

Now why is this tool helpful?

Most traders on here want to turn their passion into their full-time career, prop firms have lately been the buzz in the trading community and market themselves as a faster way to reach that goal.

While this all sounds great on paper, it is sometimes hard to estimate how much money you will have to burn on challenge fees and set realistic monthly payout expectations for yourself and your trading. This is where this tool comes in.

I've specifically developed this for traders that want to treat prop firms as a business. And as a business you want to know your monthly costs and income depending on the trading strategy and prop firm challenge you are using.

How to use this tool

It's quite simple you remove the top part of the script and replace it with your own strategy. Make sure it's written in same version of pinescript before you do that.

//--$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$--//--------------------------------------------------------------------------------------------------------------------------$$$$$$

//--$$$$$--Strategy-- --$$$$$$--// ******************************************************************************************************************************

//--$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$--//--------------------------------------------------------------------------------------------------------------------------$$$$$$

length = input.int(20, minval=1, group="Keltner Channel Breakout")

mult = input(2.0, "Multiplier", group="Keltner Channel Breakout")

src = input(close, title="Source", group="Keltner Channel Breakout")

exp = input(true, "Use Exponential MA", display = display.data_window, group="Keltner Channel Breakout")

BandsStyle = input.string("Average True Range", options = , title="Bands Style", display = display.data_window, group="Keltner Channel Breakout")

atrlength = input(10, "ATR Length", display = display.data_window, group="Keltner Channel Breakout")

esma(source, length)=>

s = ta.sma(source, length)

e = ta.ema(source, length)

exp ? e : s

ma = esma(src, length)

rangema = BandsStyle == "True Range" ? ta.tr(true) : BandsStyle == "Average True Range" ? ta.atr(atrlength) : ta.rma(high - low, length)

upper = ma + rangema * mult

lower = ma - rangema * mult

//--Graphical Display--// *-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-$$$$$$

u = plot(upper, color=#2962FF, title="Upper", force_overlay=true)

plot(ma, color=#2962FF, title="Basis", force_overlay=true)

l = plot(lower, color=#2962FF, title="Lower", force_overlay=true)

fill(u, l, color=color.rgb(33, 150, 243, 95), title="Background")

//--Risk Management--// *-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-$$$$$$

riskPerTradePerc = input.float(1, title="Risk per trade (%)", group="Keltner Channel Breakout")

le = high>upper ? false : true

se = lowlower

strategy.entry('PivRevLE', strategy.long, comment = 'PivRevLE', stop = upper, qty=riskToLots)

if se and upper>lower

strategy.entry('PivRevSE', strategy.short, comment = 'PivRevSE', stop = lower, qty=riskToLots)

The tool will then use the strategy equity of your own strategy and use this to simulat prop firms. Since these CFD prop firms work with different phases and payouts the indicator will simulate the gains until target or max drawdown / daily drawdown limit gets reached. If it reaches target it will go to the next phase and keep on doing that until it fails a challenge.

If in one of the phases there is a reward for completing, like a payout, refund, extra it will add this to the gains.

If you fail the challenge by reaching max drawdown or daily drawdown limit it will substract the challenge fee from the gains.

These gains are then visualised in the calendar so you can get an idea of yearly / monthly gains of the backtest. Remember, it is just a backtest so no guarantees of future income.

The bottom pane (non-overlay) is visualising the performance of the backtest during the phases. This way u can check if it is realistic. For instance if it only takes 1 bar on chart to reach target you are probably risking more than the firm wants you to risk. Also, it becomes much less clear if daily drawdown got hit in those high risk strategies, the results will be less accurate.

The daily drawdown limit get's reset every time there is a new dayofweek on chart.

If you set your prop firm preset setting to "'custom" the settings below that are applied as your prop firm settings. Otherwise it will use one of the template by default it's FTMO 100K.

The strategy I'm using as an example in this script is a simple Keltner Channel breakout strategy. I'm using a 0.05% commission per trade as that is what I found most common on crypto exchanges and it's close to the commissions+spread you get on a cfd prop firm. I'm targeting a 1% risk per trade in the backtest to try and stay within prop firm boundaries of max 1% risk per trade.

Lastly, the original yearly and monthly performance table was developed by Quantnomad and I've build ontop of that code. Here's a link to the original publication:

That's everything for now, hope this indicator helps people visualise the potential of prop firms better or to understand that they are not a good fit for their current financial situation.

CVD (Cumulative Volume Delta)

Cumulative Volume Delta

Use a moving average with three different

I thought about determining the volatility and direction of the price of the stock price and finding a place to break through.

I made some Mistake coz I'm new corder

I'm reposting this simple script due to house rule violation. (Whatever can haha) 😁

I'm erasing all the comments in my native language that I had in my script... I thought it would make the User uncomfortable, so I locked the code, and I thought maybe that's the problem

Anyway, I'm sorry 😅

[Kpt-Ahab] PnL-calculatorThe PnL-Cal shows how much you’re up or down in your own currency, based on the current exchange rate.

Let’s say your home currency is EUR.

On October 10, 2022, you bought 10 Tesla stocks at $219 apiece.

Back then, with an exchange rate of 0.9701, you spent €2,257.40.

If you sold the 10 Tesla shares on April 17, 2025 for $241.37 each, that’s around a 10% gain in USD.

But if you converted the USD back to EUR on the same day at an exchange rate of 1.1398, you’d actually end up with an overall loss of about 6.2%.

Right now, only a single entry point is supported.

If you bought shares on different days with different exchange rates, you’ll unfortunately have to enter an average for now.

For viewing on a phone, the table can be simplified.

Institutional MACD (Z-Score Edition) [VolumeVigilante]📈 Institutional MACD (Z-Score Edition) — Professional-Grade Momentum Signal

This is not your average MACD .

The Institutional MACD (Z-Score Edition) is a statistically enhanced momentum tool, purpose-built for serious traders and breakout hunters . By applying Z-Score normalization to the classic MACD structure, this indicator uncovers statistically significant momentum shifts , enabling cleaner reads on price extremes, trend continuation, and potential reversals.

💡 Why It Matters

The classic MACD is powerful — but raw momentum values can be noisy and relative , especially on volatile assets like BTC/USD . By transforming the MACD line, signal line, and histogram into Z-scores , we anchor these signals in statistical context . This makes the Institutional MACD:

✔️ Timeframe-agnostic and asset-normalized

✔️ Ideal for spotting true breakouts , not false flags

✔️ A reliable tool for detecting momentum divergence and exhaustion

🧪 Key Features

✅ Full Z-Score normalization (MACD, Signal, Histogram)

✅ Highlighted ±Z threshold bands for overbought/oversold zones

✅ Customizable histogram coloring for visual momentum shifts

✅ Built-in alerts for zero-crosses and Z-threshold breaks

✅ Clean overlay with optional display toggles

🔁 Strategy Tip: Mean Reversion Signals with Statistical Confidence

This indicator isn't just for spotting breakouts — it also shines as a mean reversion tool , thanks to its Z-Score normalization .

When the Z-Score histogram crosses beyond ±2, it marks a statistically significant deviation from the mean — often signaling that momentum is overstretched and the asset may be due for a pullback or reversal .

📌 How to use it:

Z > +2 → Price action is in overbought territory. Watch for exhaustion or short setups.

Z < -2 → Momentum is deeply oversold. Look for reversal confirmation or long opportunities.

These zones often precede snap-back moves , especially in range-bound or corrective markets .

🎯 Combine Z-Score extremes with:

Candlestick confirmation

Support/resistance zones

Volume or price divergence

Other mean reversion tools (e.g., RSI, Bollinger Bands)

Unlike the raw MACD, this version delivers statistical thresholds , not guesswork — helping traders make decisions rooted in probability, not emotion.

📢 Trade Smart. Trade Vigilantly.

Published by VolumeVigilante

Vietnamese Stocks: Multi-Ticker Fibonacci AlertThis Pine Script™ indicator is designed specifically for traders monitoring the Vietnamese stock market (HOSE, HNX). Its primary goal is to automate the tracking of Fibonacci retracement levels across a large list of stocks, alerting you when prices breach key support zones.

Core Functionality:

The script calculates Fibonacci retracement levels (23.6%, 38.2%, 50%, 61.8%, 78.6%) for up to 40 tickers simultaneously. The calculation is based on the highest high and lowest low identified since a user-defined Start Time. This allows you to anchor the Fibonacci analysis to a specific market event, trend start, or time period relevant to your strategy.

What it Does For You:

Automated Watchlist Scanning: Instead of drawing Fib levels on dozens of charts, select one of the two pre-configured watchlists (up to 40 symbols each, customizable in settings) populated with popular Vietnamese stocks.

Time-Based Fibonacci: Define a Start Time in the settings. The script uses this date to find the subsequent highest high and lowest low for each symbol in your chosen watchlist, forming the basis for the Fib calculation.

Intelligent Alerts: Get notified via TradingView's alerts when the candle closing price of any stock in your active watchlist falls below the critical 38.2%, 50%, 61.8%, or 78.6% levels relative to its own high/low range since the start time. Alerts are consolidated for efficiency.

Visual Aids:

- Plots the same time-based Fibonacci levels directly on your current chart symbol for quick reference.

- Includes an optional on-chart table showing which monitored stocks are currently below key Fib levels (enable "Show Debug Info").

- Features experimental background coloring to highlight potential bullish signals on the current chart.

Configuration:

Start Time: Crucial input – sets the anchor point for Fib calculations.

WatchList Selection: Choose between WatchList #1 (Bluechip/Midcap focus) or WatchList #2 (Defensive/Other focus) using the boolean toggles.

Symbol Customization: Easily replace the default symbols with your preferred Vietnamese stocks directly in the indicator settings.

Notification Prefix: Add custom text to the beginning of your alert messages.

Alert Setup: Remember to create an alert in TradingView, selecting this indicator and the alert() condition, usually with "Once Per Bar Close" frequency.

This tool is open-source under the MPL 2.0 license. Feel free to use, modify, and learn from it.

tafirstlibGeneral Purpose: Starts by stating it's a collection of utility functions for technical analysis.

Core Functionality Areas: Mentions key categories like:

Extrema detection (isMin, isMax, etc.)

Condition checking over time (isMachedInRange, isContinuous, etc.)

Rate of change analysis (isSlowDown)

Moving average calculation (getMA)

Advanced Features: Highlights the more complex functions:

Visualization helpers (getColorNew)

Moving Regression (mr) for smoothing/trend

Cycle analysis (bpDom)

Overall Goal: Concludes by stating the library's aim – simplifying development and enabling complex analysis.

Library "tafirstlib"

TODO: add library description here

isSlowDown(data)

isSlowDown

Parameters:

data (float) : array of numbers

Returns: boolean

isMin(data, maeLength)

isMin

Parameters:

data (float) : array of numbers

maeLength (int) : number

Returns: boolean

isMax(data, maeLength)

isMax

Parameters:

data (float) : array of numbers

maeLength (int) : number

Returns: boolean

isMinStopped(data, maeLength)

isMinStopped

Parameters:

data (float) : array of numbers

maeLength (int) : number

Returns: boolean

isMaxStopped(data, maeLength)

isMaxStopped

Parameters:

data (float) : array of numbers

maeLength (int) : number

Returns: boolean

isLongMinStopped(data, maeLength, distance)

isLongMinStopped

Parameters:

data (float) : array of numbers

maeLength (int) : number

distance (int) : number

Returns: boolean

isLongMaxStopped(data, maeLength, distance)

isLongMaxStopped

Parameters:

data (float) : array of numbers

maeLength (int) : number

distance (int) : number

Returns: boolean

isMachedInRangeSkipCurrent(data, findRange, findValue)

isMachedInRangeSkipCurrent

Parameters:

data (bool) : array of numbers

findRange (int) : number

findValue (bool) : number

Returns: boolean

isMachedInRange(data, findRange, findValue)

isMachedInRange

Parameters:

data (bool) : array of numbers

findRange (int) : number

findValue (bool) : number

Returns: boolean

isMachedColorInRange(data, findRange, findValue)

isMachedColorInRange isMachedColorInRange(series color data, int findRange, color findValue)

Parameters:

data (color) : series of color

findRange (int) : int

findValue (color) : color

Returns: boolean

countMachedInRange(data, findRange, findValue)

countMachedInRange

Parameters:

data (bool) : array of numbers

findRange (int) : number

findValue (bool) : number

Returns: number

getColor(data)

getColor

Parameters:

data (float) : array of numbers

Returns: color

getColorNew(data)

getColorNew

Parameters:

data (float) : array of numbers

Returns: color

isColorBetter(color_data)

isColorBetter

Parameters:

color_data (color) : array of colors

Returns: boolean

isColorWorst(color_data)

isColorWorst

Parameters:

color_data (color) : array of colors

Returns: boolean

isColorBetter2(color_data)

isColorBetter2

Parameters:

color_data (color) : array of colors

Returns: boolean

isColorWorst2(color_data)

isColorWorst2

Parameters:

color_data (color) : array of colors

Returns: boolean

isDecreased2Bar(data)

isDecreased2Bar

Parameters:

data (float) : array of numbers

Returns: boolean

isContinuousAdvance(targetSeries, range2Find, howManyException)

isContinuousAdvance

Parameters:

targetSeries (bool) : array of booleans

range2Find (int) : number

howManyException (int) : number

Returns: boolean

isContinuous(targetSeries, range2Find, truefalse)

isContinuous

Parameters:

targetSeries (bool) : array of booleans

range2Find (int) : number

truefalse (bool) : boolean

Returns: boolean

isContinuousNotNow(targetSeries, range2Find, truefalse)

isContinuousNotNow

Parameters:

targetSeries (bool) : array of booleans

range2Find (int) : number

truefalse (bool) : boolean

Returns: boolean

isContinuousTwoFactors(targetSeries, range2Find, truefalse)

isContinuousTwoFactors

Parameters:

targetSeries (bool) : array of booleans

range2Find (int) : number

truefalse (bool) : boolean

Returns: boolean

findEventInRange(startDataBarIndex, neededDataBarIndex, currentBarIndex)

findEventInRange

Parameters:

startDataBarIndex (int) : number

neededDataBarIndex (int) : number

currentBarIndex (int) : number

Returns: boolean

findMin(firstdata, secondata, thirddata, forthdata)

findMin

Parameters:

firstdata (float) : number

secondata (float) : number

thirddata (float) : number

forthdata (float) : number

Returns: number

findMax(firstdata, secondata, thirddata, forthdata)

findMax

Parameters:

firstdata (float) : number

secondata (float) : number

thirddata (float) : number

forthdata (float) : number

Returns: number

getMA(src, length, mav)

getMA

Parameters:

src (float) : number

length (simple int) : number

mav (string) : string

Returns: number

mr(mrb_src, mrb_window, mrb_degree)

Parameters:

mrb_src (float)

mrb_window (int)

mrb_degree (int)

bpDom(maeLength, bpw, mult)

Parameters:

maeLength (int)

bpw (float)

mult (float)

FunctionSurvivalEstimationLibrary "FunctionSurvivalEstimation"

The Survival Estimation function, also known as Kaplan-Meier estimation or product-limit method, is a statistical technique used to estimate the survival probability of an individual over time. It's commonly used in medical research and epidemiology to analyze the survival rates of patients with different treatments, diseases, or risk factors.

What does it do?

The Survival Estimation function takes into account censored observations (i.e., individuals who are still alive at a certain point) and calculates the probability that an individual will survive beyond a specific time period. It's particularly useful when dealing with right-censoring, where some subjects are lost to follow-up or have not experienced the event of interest by the end of the study.

Interpretation

The Survival Estimation function provides a plot of the estimated survival probability over time, which can be used to:

1. Compare survival rates between different groups (e.g., treatment arms)

2. Identify patterns in the data that may indicate differences in mortality or disease progression

3. Make predictions about future outcomes based on historical data

4. In a trading context it may be used to ascertain the survival ratios of trading under specific conditions.

Reference:

www.global-developments.org

"Beyond GDP" ~ www.aeaweb.org

en.wikipedia.org

www.kdnuggets.com

survival_probability(alive_at_age, initial_alive)

Kaplan-Meier Survival Estimator.

Parameters:

alive_at_age (int) : The number of subjects still alive at a age.

initial_alive (int) : The Total number of initial subjects.

Returns: The probability that a subject lives longer than a certain age.

utility(c, l)

Captures the utility value from consumption and leisure.

Parameters:

c (float) : Consumption.

l (float) : Leisure.

Returns: Utility value from consumption and leisure.

welfare_utility(age, b, u, s)

Calculate the welfare utility value based age, basic needs and social interaction.

Parameters:

age (int) : Age of the subject.

b (float) : Value representing basic needs (food, shelter..).

u (float) : Value representing overall well-being and happiness.

s (float) : Value representing social interaction and connection with others.

Returns: Welfare utility value.

expected_lifetime_welfare(beta, consumption, leisure, alive_data, expectation)

Calculates the expected lifetime welfare of an individual based on their consumption, leisure, and survival probability over time.

Parameters:

beta (float) : Discount factor.

consumption (array) : List of consumption values at each step of the subjects life.

leisure (array) : List of leisure values at each step of the subjects life.

alive_data (array) : List of subjects alive at each age, the first element is the total or initial number of subjects.

expectation (float) : Optional, `defaut=1.0`. Expectation or weight given to this calculation.

Returns: Expected lifetime welfare value.

Statistical Trailing Stop [LuxAlgo]The Statistical Trailing Stop tool offers traders a way to lock in profits in trending markets with four statistical levels based on the log-normal distribution of volatility.

The indicator also features a dashboard with statistics of all detected signals.

🔶 USAGE

The tool works out of the box, traders can adjust the data used with two parameters: data & distribution length.

By default, the tool takes volatility measures of groups of 10 candles, and statistical measures of the last 100 of these groups then traders can adjust the base level to use as trailing, the larger the level, the more resistant the tool will be to moves against the trend.

🔹 Base Levels

Traders can choose up to 4 different levels of trailing, all based on the statistical distribution of volatility.

As we can see in the chart above, each higher level is more resistant to market movements, so level 0 is the most reactive and level 3 the least.

It is up to the trader to determine the best level for each underlying, time frame and market conditions.

🔹 Dashboard

The tool provides a dashboard with the statistics of all trades, making it very easy to assess the performance of the parameters used for any given market.

As we can see on the chart, all Daily BTC signals with default parameters but different base levels, level 2 is the best performing of all four, giving a positive expectation of $2435 per trade, taking into account all long and short trades.

Of note are the long trades with a win rate of 76.47% and a risk-to-reward of 3.34, giving a positive expectation of $4839 per trade, with winners having an average duration of 210 days and losers 32 days.

This, compared to short trades with negative expectation, speaks to the uptrend bias of this particular market.

🔶 SETTINGS

Data Length: Select how many bars to use per data point

Distribution Length: Select how many data points the distribution will have

Base Level: Choose between 4 different trailing levels

🔹 Dashboard

Show Statistics: Enable/disable dashboard

Position: Select dashboard position

Size: Select dashboard size

Composite Scaled EMA LevelsComposite Scaled EMA Levels Indicator

This TradingView Pine Script indicator calculates a “composite EMA” that compares the closing price of the current asset with that of the XU100 index and scales the EMA values to the XU100 level. It then visualizes these computed levels as horizontal lines on the chart with corresponding labels.

Key Components:

Inputs and Data Retrieval:

Length Input: The user defines a parameter length (default is 10) which determines over how many bars the horizontal line is drawn.

Data Collection:

The daily closing price of the current symbol (current_close) is retrieved using request.security().

The daily closing price of the XU100 index (xu100) is also retrieved.

A ratio is computed as current_close / xu100. This ratio serves as the basis for calculating the composite EMAs.

EMA Calculations:

The indicator computes Exponential Moving Averages (EMAs) on the ratio for specific periods.

In the provided version, the script calculates EMAs for three periods (34, 55, and 233), though you can easily expand this to other periods if needed.

Each computed EMA (for instance, EMA34, EMA55, EMA233) is then scaled by multiplying it with the XU100 index’s close, converting it to a price level that is meaningful on the chart.

Drawing Horizontal Lines:

Instead of using the standard plot() function, the script uses line.new() to draw horizontal lines representing the scaled EMA values over the last “length” bars.

Before drawing new lines, any existing lines and labels are deleted to ensure that only the most current values are shown.

Adding Labels to Lines:

The script creates a label for each EMA using label.new(), placing the label at the current bar (i.e., the rightmost position on the chart) using label.style_label_left so that the text appears to the right of the line.

The label displays the name of the composite EMA (e.g., "Composite EMA 34") along with its current scaled value.

Visualization:

The horizontal lines and labels provide a visual reference for the composite EMA levels. These lines help traders see critical support/resistance levels derived from the relationship between the current asset and the XU100 index.

Colors are assigned for clarity (for example, the EMA lines in this version use green).

Summary:

The Composite Scaled EMA Levels indicator is designed to help traders analyze the relationship between an asset’s price and the broader market index (XU100) by calculating a ratio and then applying EMAs on that ratio. By scaling these EMAs back to price levels and displaying them as horizontal lines with clear labels on the chart, the indicator offers a visual tool to assess trend direction and potential support or resistance levels. This can assist in making informed trading decisions based on composite trend analysis.

Average Body RangeThe Average Body Range (ABR) indicator calculates the average size of a candle's real body over a specified period. Unlike the traditional Average Daily Range (ADR), which measures the full range from high to low, the ABR focuses solely on the absolute difference between the open and close of each bar. This provides insight into market momentum and trading activity by reflecting how much price is actually moving from open to close , not just in total.

This indicator is especially useful for identifying:

Periods of strong directional movement (larger body sizes)

Low-volatility or indecisive markets (smaller body sizes)

Changes in trend conviction or momentum

Customization:

Length: Number of bars used to compute the average (default: 14)

Use ABR to enhance your understanding of price behavior and better time entries or exits based on market strength.

RTH and ETH RangesKey Functions :

Visualizes Regular Trading Hours (RTH) and Extended Trading Hours (ETH) price ranges

Tracks session highs, lows, and 50% levels where significant market reactions occur

Detects breakouts beyond previous session extremes

Trading Applications :

Exposes potential liquidity raids at session boundaries where smart money targets stop orders

Identifies critical price thresholds where institutional activity concentrates

Highlights divergences between RTH and ETH behavior that precede directional moves

Provides measurement of session volatility differences

Maps key price levels for objective entry and exit parameters

Reveals market dynamics at session transitions where institutional positioning changes

Dirty Market IndexThis indicator is designed to out an index displaying the level of dirtiness in market.

This level is defined by:

Sum of shadow lengths of last n candles (n is input and user can change it, it's 100 by default)

divided by

Sum of full candle bodies of last n candles (high - low)

This factor indicates how many percents of the market movement has been placed in shadows of candles, the higher this number, the dirtier market would be.

3 Candles Gap3 Candle Gap Indicator is made to detect these types of patterns:

1. 3 consecutive bullish or bearish candles

2. the middle candle true body (body excluding shadows) has a part that is not covered by previous and next candle shadows (gap)

This pattern helps traders to detect candles where price has moved in a direction and gap has formed (price is not covered by previous or next candles shadows), this is a signal showing price momentum where one side (bulls/bears) is so powerful at moving the price that the other side (bears/bulls) can't get price back to cover the gap.

This indicator has "repainting" by 1 candle which means, it uses the data from future to work, however this future data does not go further than 1 candle.

Leavitt Convolution ProbabilityTechnical Analysis of Markets with Leavitt Market Projections and Associated Convolution Probability

The aim of this study is to present an innovative approach to market analysis based on the research "Leavitt Market Projections." This technical tool combines one indicator and a probability function to enhance the accuracy and speed of market forecasts.

Key Features

Advanced Indicators : the script includes the Convolution line and a probability oscillator, designed to anticipate market changes. These indicators provide timely signals and offer a clear view of price dynamics.

Convolution Probability Function : The Convolution Probability (CP) is a key element of the script. A significant increase in this probability often precedes a market decline, while a decrease in probability can signal a bullish move. The Convolution Probability Function:

At each bar, i, the linear regression routine finds the two parameters for the straight line: y=mix+bi.

Standard deviations can be calculated from the sequence of slopes, {mi}, and intercepts, {bi}.

Each standard deviation has a corresponding probability.

Their adjusted product is the Convolution Probability, CP. The construction of the Convolution Probability is straightforward. The adjusted product is the probability of one times 1− the probability of the other.

Customizable Settings : Users can define oversold and overbought levels, as well as set an offset for the linear regression calculation. These options allow for tailoring the script to individual trading strategies and market conditions.

Statistical Analysis : Each analyzed bar generates regression parameters that allow for the calculation of standard deviations and associated probabilities, providing an in-depth view of market dynamics.

The results from applying this technical tool show increased accuracy and speed in market forecasts. The combination of Convolution indicator and the probability function enables the identification of turning points and the anticipation of market changes.

Additional information:

Leavitt, in his study, considers the SPY chart.

When the Convolution Probability (CP) is high, it indicates that the probability P1 (related to the slope) is high, and conversely, when CP is low, P1 is low and P2 is high.

For the calculation of probability, an approximate formula of the Cumulative Distribution Function (CDF) has been used, which is given by: CDF(x)=21(1+erf(σ2x−μ)) where μ is the mean and σ is the standard deviation.

For the calculation of probability, the formula used in this script is: 0.5 * (1 + (math.sign(zSlope) * math.sqrt(1 - math.exp(-0.5 * zSlope * zSlope))))

Conclusions

This study presents the approach to market analysis based on the research "Leavitt Market Projections." The script combines Convolution indicator and a Probability function to provide more precise trading signals. The results demonstrate greater accuracy and speed in market forecasts, making this technical tool a valuable asset for market participants.

Drawdown Visualizer v1.0Drawdown Visualizer

The Drawdown Visualizer tracks the percentage decline from all-time highs, providing valuable insights into market corrections and potential buying opportunities.

Key Features:

1) Real-Time Drawdown Tracking: The indicator continuously calculates and displays the current percentage drawdown from the all-time high price, color-coded from green (minimal drawdown) to red (severe drawdown) for instant visual feedback.

2) Maximum Drawdown Detection: Permanently tracks and displays the maximum historical drawdown encountered during the analyzed period, helping traders understand worst-case scenarios.

3) Statistical Analysis: Calculates and displays three important statistical measures:

* Average Drawdown: The mean value of all drawdowns recorded

* Median Drawdown: The middle value in the sorted list of all drawdowns, providing insight

into typical decline patterns

* Normal Drawdown Range: Visualizes the expected range of typical drawdowns based on

statistical standard deviation

Practical Applications:

1) Risk Management: Understand typical and extreme drawdowns to set appropriate stop-loss levels

2) Market Context: Gain perspective on whether current corrections are normal or exceptional

3) Entry Point Analysis: Identify potential buying opportunities when drawdowns reach statistical extremes

Daily LevelsOverview:

The Daily Levels indicator plots key price levels from the previous trading day, including the high, low, median (pivot), and projected extensions. These levels help traders identify potential support/resistance zones and anticipate breakout or reversal opportunities.

Key Features:

✅ Previous Day High & Low – Visualizes the prior day’s high and low as dynamic support/resistance levels.

✅ Median (Pivot) Line – Calculates the midpoint between the previous day’s high and low, acting as a key intraday reference.

✅ Projected Levels – Extends the high/low range symmetrically above and below the median, highlighting potential breakout zones.

✅ Customizable Display – Toggle visibility, adjust colors, and modify line styles (solid, dotted, dashed).

✅ Price Labels – Clear on-chart labels showing exact price values for quick reference.

✅ Built-in Alerts – Get notified when price crosses any of the key levels.

How to Use:

Trend Identification: If price holds above the median, the bias is bullish; below suggests bearish momentum.

Breakout Trading: Watch for moves beyond the projected levels for potential continuation.

Mean Reversion: Fade moves toward the previous day’s high/low if the median holds as support/resistance.

Ideal For:

Day Traders – Intraday support/resistance levels.

Swing Traders – Context for multi-day trends.

Breakout/Reversal Strategies – Clear levels for trade triggers.

Settings Recommendations:

High/Low Lines: Use semi-transparent colors (e.g., green/red) for clarity.

Projections: Helpful for anticipating extended moves (e.g., teal for upper, orange for lower).

Alerts: Enable notifications for key crosses (e.g., median or high/low breaks).

Day’s Open ForecastOverview

This Pine Script indicator combines two primary components:

1. Day’s Open Forecast:

o Tracks historical daily moves (up and down) from the day’s open.

o Calculates average up and down moves over a user-defined lookback period.

o Optionally includes standard deviation adjustments to forecast potential intraday levels.

o Plots lines on the chart for the forecasted up and down moves from the current day's open.

2. Session VWAP:

o Allows you to specify a custom trading session (by time range and UTC offset).

o Calculates and plots a Volume-Weighted Average Price (VWAP) during that session.

By combining these two features, you can gauge potential intraday moves relative to historical behavior from the open, while also tracking a session-specific VWAP that can act as a dynamic support/resistance reference.

How the Code Works

1. Collect Daily Moves

o The script detects when a new day starts using time("D").

o Once a new day is detected, it stores the previous day’s up-move (dayHigh - dayOpen) and down-move (dayOpen - dayLow) into arrays.

o These arrays keep track of the last N days (default: 126) of up/down move data.

2. Compute Statistics

o The script computes the average (f_average()) of up-moves and down-moves over the stored period.

o It also computes the standard deviation (f_stddev()) of up/down moves for optional “forecast bands.”

3. Forecast Lines

o Plots the current day’s open.

o Plots the average forecast lines above and below the open (Avg Up Move Level and Avg Down Move Level).

o If standard deviation is enabled, plots additional lines (Avg+StdDev Up and Avg+StdDev Down).

4. Session VWAP

o The script detects the start of a user-defined session (via input.session) and resets accumulation of volume and the numerator for VWAP.

o As each bar in the session updates, it accumulates volume (vwapCumulativeVolume) and a price-volume product (vwapCumulativeNumerator).

o The session VWAP is then calculated as (vwapCumulativeNumerator / vwapCumulativeVolume) and plotted.

5. Visualization Options

o Users can toggle standard deviation usage, historical up/down moves plotting, and whether to show the forecast “bands.”

o The vwapSession and vwapUtc inputs let you adjust which session (and time zone offset) the VWAP is calculated for.

________________________________________

How to Use This Indicator on TradingView

1. Create a New Script

o Open TradingView, then navigate to Pine Editor (usually found at the bottom of the chart).

o Copy and paste the entire code into the editor.

2. Save and Add to Chart

o Click Save (give it a relevant title if you wish), then click Add to chart.

o The indicator will appear on your chart with the forecast lines and VWAP.

o By default, it is overlayed on the price chart (because of overlay=true).

3. Customize Inputs

o In the indicator’s settings, you can:

Change lookback days (default: 126).

Enable or disable standard deviation (Include Standard Deviation in Forecast?).

Adjust the standard deviation multiplier.

Choose whether to plot bands (Plot Bands with Averages/StdDev?).

Plot historical moves if desired (Plot Historical Up/Down Moves for Reference?).

Set your custom session and UTC offset for the VWAP calculation.

4. Interpretation

o “Current Day Open” is simply today’s open price on your chart.

o Up/Down Move Lines: Indicate a potential forecast based on historical averages.

If standard deviation is enabled, the second set of lines acts as an extended range.

o VWAP: Helpful for determining intraday price equilibrium over the specified session.

Important Notes / Best Practices

• The script only updates the historical up/down move data once per day (when a new day starts).

• The VWAP portion resets at the start of the specified session each day.

• Standard deviation multiplies the average up/down range, giving you a sense of “volatility range” around the day’s open.

• Adjust the lookback length (dayCount) to balance how many days of data you want to average. More days = smoother but possibly slower to adapt; fewer days = more reactive but potentially less reliable historically.

Educational & Liability Disclaimers

1. Educational Disclaimer

o The information provided by this indicator is for educational and informational purposes only. It is a technical analysis tool intended to demonstrate how to use historical data and basic statistics in Pine Script.

2. No Financial Advice

o This script does not constitute financial or investment advice. All examples and explanations are solely illustrative. You should always do your own analysis before making any investment decisions.

3. No Liability

o The author of this script is not liable for any losses or damages—monetary or otherwise—that may occur from the application of this script.

o Past performance does not guarantee future results, and you should never invest money you cannot afford to lose.

By adding this indicator to your TradingView chart, you acknowledge and accept that you alone are responsible for your own trading decisions.

Enjoy using the “Day’s Open Forecast” and Session VWAP for better market insights!

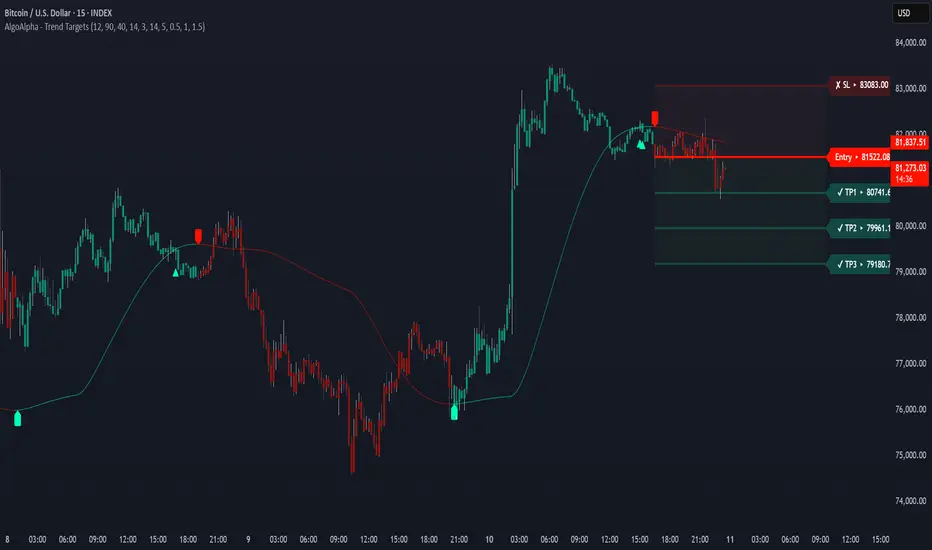

Trend Targets [AlgoAlpha]OVERVIEW

This script combines a smoothed trend-following model with dynamic price rejection logic and ATR-based target projection to give traders a complete visual framework for trading trend continuations. It overlays on price and automatically detects potential trend shifts, confirms rejections near dynamic support/resistance, and displays calculated stop-loss and take-profit levels to support structured risk-reward management. Unlike traditional indicators that only show trend direction or signal entries, this tool brings together a unique mix of signal validation, volatility-aware positioning, and layered profit-taking to guide decision-making with more context.

CONCEPTS

The core trend logic is built on a custom Supertrend that uses an ATR-based band structure with long smoothing chains—first through a WMA, then an EMA—allowing the trend line to respond to major shifts while ignoring noise. A key addition is the use of rejection logic: the script looks for consolidation candles that "hug" the smoothed trend line and counts how many consecutive bars reject from it. This behavior often precedes significant moves. A user-defined threshold filters out weak tests and highlights only meaningful rejections.

FEATURES

Trend Detection : Automatically identifies trend direction using a smoothed Supertrend (WMA + EMA), with shape markers on trend shifts and color-coded bars for clarity.

Rejection Signals : Detects price rejections at the trend line after a user-defined number of consolidation bars; plots ▲/▼ icons to highlight strong continuation setups.

Target Projection : On trend confirmation, plots entry, stop-loss (ATR-based), and three dynamic take-profit levels based on customizable multiples.

Dynamic Updates : All levels (entry, SL, TP1–TP3) auto-adjust based on volatility and are labeled in real time on the chart.

Customization : Users can tweak trend parameters, rejection confirmation count, SL/TP ratios, smoothing lengths, and appearance settings.

Alerts : Built-in alerts for trend changes, rejection events, and when TP1, TP2, or TP3 are reached.

Chart Overlay : Plots directly on price chart with minimal clutter and clearly labeled levels for easy trading.

USAGE

Start by tuning the Supertrend factor and ATR period to fit your asset and timeframe—higher values will catch bigger swings, lower values catch faster moves. The confirmation count should match how tightly you want to filter rejection behavior—higher values make signals rarer but stronger. When the trend shifts, the indicator colors the bars and line accordingly, and if enabled, plots the full entry-TP-SL structure. Rejection markers appear only after enough qualifying bars confirm price pressure at the trend line. This is especially useful for continuation plays where price retests the trend but fails to break it. All calculations are based on volatility (ATR), so targets naturally adjust with market conditions. Add alerts to get notified of important signals even when away from the chart.

NR_VersatilitiesLibrary "NR_Versatilities"

Versatilities (aka, Versatile Utilities) includes:

- Seventeen Price Variants returned as a tuple,

- Eight Smoothing functions rolled into one,

- Pick any Past Value from any series with offset,

- Or just the previous value from any series.

pastVal(src, len)

Fetches past value from src that came len distance ago

Parameters:

src (float) : source series

len (int) : lookback distance - (optional) default is 1

Returns: latest src if len <= 0, else src

previous(src)

Fetches past value from src that came len distance ago

Parameters:

src (float) : source series

Returns: previous value in the series if found, else current value

price_variants()

Computes Several different averages using current and previous OHLC values

Returns: Seventeen Uncommon Average Price Combinations

dynamic_MA(matyp, masrc, malen, lsmaoff, almasgm, almaoff, almaflr)

Dynamically computes Eight different MAs on-demand individually, or an average of all taken together

Parameters:

matyp (string) : pick one of these MAs - ALMA, EMA, HMA, LSMA, RMA, SMA, SWMA, WMA, ALL

masrc (float) : source series to compute MA

malen (simple int) : lookback distance for MA

lsmaoff (simple int) : optional LSMA offset - default is 0

almasgm (simple float) : optional ALMA sigma - default is 5

almaoff (simple float) : optional ALMA offset - default is 0.5

almaflr (simple bool) : optional ALMA floor flag - default is false

Returns: MA series for chosen type or, an average of all of them, if chosen so

Multi-Timeframe Anchored VWAP Valuation# Multi-Timeframe Anchored VWAP Valuation

## Overview

This indicator provides a unique perspective on potential price valuation by comparing the current price to the Volume Weighted Average Price (VWAP) anchored to the start of multiple timeframes: Weekly, Monthly, Quarterly, and Yearly. It synthesizes these comparisons into a single oscillator value, helping traders gauge if the current price is potentially extended relative to significant volume-weighted levels.

## Core Concept & Calculation

1. **Anchored VWAP:** The script calculates the VWAP separately for the current Week, Month, Quarter (3 Months), and Year (12 Months), starting the calculation from the first bar of each period.

2. **Price Deviation:** It measures how far the current `close` price is from each of these anchored VWAPs. This distance is measured in terms of standard deviations calculated *within* that specific anchor period (e.g., how many weekly standard deviations the price is away from the weekly VWAP).

3. **Deviation Score (Multiplier):** Based on this standard deviation distance, a score is assigned. The further the price is from the VWAP (in terms of standard deviations), the higher the absolute score. The indicator uses linear interpolation to determine scores between the standard deviation levels (defaulted at 1, 2, and 3 standard deviations corresponding to scores of +/-2, +/-3, +/-4, with a score of 1 at the VWAP).

4. **Timeframe Weighting:** Longer timeframes are considered more significant. The deviation scores are multiplied by fixed scalars: Weekly (x1), Monthly (x2), Quarterly (x3), Yearly (x4).

5. **Final Valuation Metric:** The weighted scores from all four timeframes are summed up to produce the final oscillator value plotted in the indicator pane.

## How to Interpret and Use

* **Histogram (Indicator Pane):**

* The main output is the histogram representing the `Final Valuation Metric`.

* **Positive Values:** Suggest the price is generally trading above its volume-weighted averages across the timeframes, potentially indicating strength or relative "overvaluation."

* **Negative Values:** Suggest the price is generally trading below its volume-weighted averages, potentially indicating weakness or relative "undervaluation."

* **Values Near Zero:** Indicate the price is relatively close to its volume-weighted averages.

* **Histogram Color:**

* The color of the histogram bars provides context based on the metric's *own recent history*.

* **Green (Positive Color):** The metric is currently *above* its recent average plus a standard deviation band (dynamic upper threshold). This highlights potentially significant "overvalued" readings relative to its normal range.

* **Red (Negative Color):** The metric is currently *below* its recent average minus a standard deviation band (dynamic lower threshold). This highlights potentially significant "undervalued" readings relative to its normal range.

* **Gray (Neutral Color):** The metric is within its typical recent range (between the dynamic upper and lower thresholds).

* **Orange Line:** Plots the moving average of the `Final Valuation Metric` itself (based on the "Threshold Lookback Period"), serving as the centerline for the dynamic thresholds.

* **On-Chart Table:**

* Provides a detailed breakdown for transparency.

* Shows the calculated VWAP, the raw deviation multiplier score, and the final weighted (adjusted) metric for each individual timeframe (W, M, Q, Y).

* Displays the current price, the final combined metric value, and a textual interpretation ("Overvalued", "Undervalued", "Neutral") based on the dynamic thresholds.

## Potential Use Cases

* Identifying potential exhaustion points when the indicator reaches statistically high (green) or low (red) levels relative to its recent history.

* Assessing whether price trends are supported by underlying volume-weighted average prices across multiple timeframes.

* Can be used alongside other technical analysis tools for confirmation.

## Settings

* **Calculation Settings:**

* `STDEV Level 1`: Adjusts the 1st standard deviation level (default 1.0).

* `STDEV Level 2`: Adjusts the 2nd standard deviation level (default 2.0).

* `STDEV Level 3`: Adjusts the 3rd standard deviation level (default 3.0).

* **Interpretation Settings:**

* `Threshold Lookback Period`: Defines the number of bars used to calculate the average and standard deviation of the final metric for dynamic thresholds (default 200).

* `Threshold StDev Multiplier`: Controls how many standard deviations above/below the metric's average are used to set the "Overvalued"/"Undervalued" thresholds (default 1.0).

* **Table Settings:** Customize the position and colors of the data table displayed on the chart.

## Important Considerations

* This indicator measures price deviation relative to *anchored* VWAPs and its *own historical range*. It is not a standalone trading system.

* The interpretation of "Overvalued" and "Undervalued" is relative to the indicator's logic and calculations; it does not guarantee future price movement.

* Like all indicators, past performance is not indicative of future results. Use this tool as part of a comprehensive analysis and risk management strategy.

* The anchored VWAP and Standard Deviation values reset at the beginning of each respective period (Week, Month, Quarter, Year).

HarmonicMapLibLibrary "HarmonicMapLib"

Harmonic Pattern Library implementation utilising maps

method tostring(this)

convert Range value to string

Namespace types: Range

Parameters:

this (Range) : Range value

Returns: converted string representation

method tostring(this)

convert array of Range value to string

Namespace types: array

Parameters:

this (array) : array object

Returns: converted string representation

method tostring(this)

convert map of string to Range value to string

Namespace types: map

Parameters:

this (map) : map object

Returns: converted string representation

method tostring(this)

convert RatioMap to string

Namespace types: RatioMap

Parameters:

this (RatioMap) : RatioMap object

Returns: converted string representation

method tostring(this)

convert array of RatioMap to string

Namespace types: array

Parameters:

this (array) : array object

Returns: converted string representation

method tostring(this)

convert map of string to RatioMap to string

Namespace types: map

Parameters:

this (map) : map object

Returns: converted string representation

method tostring(this)

convert map of string to bool to string

Namespace types: map

Parameters:

this (map) : map object

Returns: converted string representation

method tostring(this)

convert PrzRange to string

Namespace types: PrzRange

Parameters:

this (PrzRange) : PrzRange object

Returns: converted string representation

method tostring(this)

convert array of PrzRange to string

Namespace types: array

Parameters:

this (array) : array object

Returns: converted string representation

getHarmonicMap()

Creates the RatioMap for harmonic patterns

Returns: map haronic ratio rules for all patterns

method evaluate(patternsMap, pattern, ratioRange, properties, ratioValue)

evaluates harmonic ratio range

Namespace types: map

Parameters:

patternsMap (map) : parameter containing valid pattern names

pattern (string) : Pattern type to be evaluated

ratioRange (Range) : ratio range to be checked

properties (ScanProperties) : Scan Properties

ratioValue (float)

Returns: void

method evaluate(przRange, pattern, ratioRange, priceRange, properties)

Evaluate PRZ ranges

Namespace types: map

Parameters:

przRange (map)

pattern (string) : Pattern name

ratioRange (Range) : Range of ratio for the pattern

priceRange (Range) : Price range based on ratio

properties (ScanProperties) : ScanProperties object

Returns: void

method scanRatio(currentPatterns, rules, properties, ratioName, ratioValue)

Scan for particular named ratio of harmonic pattern to filter valid patterns

Namespace types: map

Parameters:

currentPatterns (map) : Current valid patterns map

rules (map) : map Harmonic ratio rules

properties (ScanProperties) : ScanProperties object

ratioName (string) : Specific ratio name

ratioValue (float) : ratio value to be checked

Returns: updated currentPatterns object

method scanPatterns(patterns, x, a, b, c, d, properties)

Scan for patterns based on X, A, B, C, D values

Namespace types: map

Parameters:

patterns (map) : List of allowed patterns

x (float) : X coordinate

a (float) : A coordinate

b (float) : B coordinate

c (float) : C coordinate

d (float) : D coordinate

properties (ScanProperties) : ScanProperties object. If na, default values are initialised

Returns: updated valid patterns map

method scanProjections(patterns, x, a, b, c, properties)

Scan for projections based on X, A, B, C values

Namespace types: map

Parameters:

patterns (map) : List of allowed patterns

x (float) : X coordinate

a (float) : A coordinate

b (float) : B coordinate

c (float) : C coordinate

properties (ScanProperties) : ScanProperties object. If na, default values are initialised

Returns: updated valid projections map

method merge(this, other)

merge two ranges into one

Namespace types: Range

Parameters:

this (Range) : first range

other (Range) : second range

Returns: combined range

method union(this, other)

union of two ranges into one

Namespace types: Range

Parameters:

this (Range) : first range

other (Range) : second range

Returns: union range

method overlaps(this, other)

checks if two ranges intersect

Namespace types: Range

Parameters:

this (Range) : first range

other (Range) : second range

Returns: true if intersects, false otherwise

method consolidate(this)

Consolidate ranges into PRZ

Namespace types: map

Parameters:

this (map) : map of Ranges

Returns: consolidated PRZ

method consolidateMany(this)

Consolidate ranges into multiple PRZ ranges

Namespace types: map

Parameters:

this (map) : map of Ranges

Returns: consolidated array of PRZ ranges

method getRange(currentPatterns, x, a, b, c, properties)

Get D range based on X, A, B, C coordinates for the current patterns

Namespace types: map

Parameters:

currentPatterns (map) : List of valid patterns

x (float) : X coordinate

a (float) : A coordinate

b (float) : B coordinate

c (float) : C coordinate

properties (ScanProperties) : ScanProperties object. If na, default values are initialised

Returns: map of D ranges

method getPrzRange(currentPatterns, x, a, b, c, properties)

Get PRZ range based on X, A, B, C coordinates for the current patterns

Namespace types: map

Parameters:

currentPatterns (map) : List of valid patterns

x (float) : X coordinate

a (float) : A coordinate

b (float) : B coordinate

c (float) : C coordinate

properties (ScanProperties) : ScanProperties object. If na, default values are initialised

Returns: PRZRange for the pattern

method getProjectionRanges(currentPatterns, x, a, b, c, properties)

Get projection range based on X, A, B, C coordinates for the current patterns

Namespace types: map

Parameters:

currentPatterns (map) : List of valid patterns

x (float) : X coordinate

a (float) : A coordinate

b (float) : B coordinate

c (float) : C coordinate

properties (ScanProperties) : ScanProperties object. If na, default values are initialised

Returns: array of projection ranges

Range

Collection of range values

Fields:

values (array) : array of float values

RatioMap

ratio map for pattern

Fields:

ratioMap (map) : map of string to Range (array of float)

ScanProperties

Pattern Scanning properties

Fields:

strictMode (series bool) : strict scanning mode will check for overflows

logScale (series bool) : scan ratios in log scale

errorMin (series float) : min error threshold

errorMax (series float)

mintick (series float) : minimum tick value of price

PrzRange

Potential reversal zone range

Fields:

patterns (array) : array of pattern names for the given XABCD combination

prz (Range) : PRZ range

Intrinsic Event (Multi DC OS)Overview

This indicator implements an event-based approach to analyze price movements in the foreign exchange market, inspired by the intrinsic time framework introduced in Fractals and Intrinsic Time - A Challenge to Econometricians by U. A. Müller et al. (1995). It identifies significant price events using an intrinsic time perspective and supports multi-agent analysis to reflect the heterogeneous nature of financial markets. The script plots these events as lines and labels on the chart, offering a visual tool for traders to understand market dynamics at different scales.

Key Features

Intrinsic Events : The indicator detects directional change (DC) and overshoot (OS) events based on user-defined thresholds (delta), aligning with the paper’s concept of intrinsic time (Section 6). Intrinsic time redefines time based on market activity, expanding during volatile periods and contracting during inactive ones, rather than relying on a physical clock.

Multi-Agent Analysis : Supports up to five agents, each with its own threshold and color settings, reflecting the heterogeneous market hypothesis (Section 5). This allows the indicator to capture the perspectives of market participants with different time horizons, such as short-term FX dealers and long-term central banks.

How It Works

Intrinsic Events Detection : The script identifies two types of events using intrinsic time principles:

Directional Change (DC) : Triggered when the price reverses by the threshold (delta) against the current trend (e.g., a drop by delta in an uptrend signals a "Down DC").

Overshoot (OS) : Occurs when the price continues in the trend direction by the threshold (e.g., a rise by delta in an uptrend signals an "Up OS").

DC events are plotted as solid lines, and OS events as dashed lines, with labels like "Up DC" or "OS Down" for clarity. The label style adjusts based on the trend to ensure visibility.

Multi-Agent Setup : Each agent operates independently with its own threshold, mimicking market participants with varying time horizons (Section 5). Smaller thresholds detect frequent, short-term events, while larger thresholds capture broader, long-term movements.

Settings

Each agent can be configured with:

Enable Agent : Toggle the agent on or off.

Threshold (%) : The percentage threshold (delta) for detecting DC and OS events (default values: 0.1%, 0.2%, 0.5%, 1%, 2% for agents 1–5).

Up Mode Color : Color for lines and labels in up mode (DC events).

Down Mode Color : Color for lines and labels in down mode (OS events).

Usage Notes

This indicator is designed for the foreign exchange market, leveraging its high liquidity, as noted in the paper (Section 1). Adjust the threshold values based on the instrument’s volatility—higher volatility leads to more intrinsic events (Section 4). It can be adapted to other markets where event-based analysis applies.

Reference

The methodology is based on:

Fractals and Intrinsic Time - A Challenge to Econometricians by U. A. Müller, M. M. Dacorogna, R. D. Davé, O. V. Pictet, R. B. Olsen, and J. R. Ward (June 28, 1995). Olsen & Associates Preprint.