SharelineCore_LibraryLibrary "SharelineCore_Library"

funding_premium(premiumSym, funding_period, plot_type, interest_rate, fundScale)

Parameters:

premiumSym (string)

funding_period (string)

plot_type (string)

interest_rate (float)

fundScale (float)

cvd_vwap_delta(spotSym, perpSym, normLen, resetCVD)

Parameters:

spotSym (string)

perpSym (string)

normLen (int)

resetCVD (bool)

cvd_trend_norm(spotSymbol, perpSymbol, normLen, resetOnSession)

Parameters:

spotSymbol (string)

perpSymbol (string)

normLen (int)

resetOnSession (bool)

trend_strength_engine(cvdSpot, cvdPerp)

Parameters:

cvdSpot (float)

cvdPerp (float)

bias_engine(plot_value, spotTrendVal, perpTrendVal, spotStrength, perpStrength)

Parameters:

plot_value (float)

spotTrendVal (float)

perpTrendVal (float)

spotStrength (float)

perpStrength (float)

smc_engine(h, l, c, v, ms_len, bos_len, vol_filter, scale_factor, smooth_len, signal_len)

Parameters:

h (float)

l (float)

c (float)

v (float)

ms_len (int)

bos_len (int)

vol_filter (bool)

scale_factor (float)

smooth_len (simple int)

signal_len (simple int)

momentum_engine(o, c, v, fast, slow, signal, rsiLen, normLen, smaShort, smaLong, wMacd, wRsi, wCvd, wVpi)

Parameters:

o (float)

c (float)

v (float)

fast (simple int)

slow (simple int)

signal (simple int)

rsiLen (simple int)

normLen (int)

smaShort (int)

smaLong (int)

wMacd (float)

wRsi (float)

wCvd (float)

wVpi (float)

oi_engine(quotecur, useBinance, useBinance2, useBinance3, useBitmex, useBitmex2, useKraken, d_mult, strength1_mult, strength2_mult)

Parameters:

quotecur (string)

useBinance (bool)

useBinance2 (bool)

useBinance3 (bool)

useBitmex (bool)

useBitmex2 (bool)

useKraken (bool)

d_mult (float)

strength1_mult (float)

strength2_mult (float)

Strategies

LuxyEnergyIndexThe Luxy Energy Index (LEI) library provides functions to measure price movement exhaustion by analyzing three dimensions: Extension (distance from fair value), Velocity (speed of movement), and Volume (confirmation level).

LEI answers a different question than traditional momentum indicators: instead of "how far has price gone?" (like RSI), LEI asks "how tired is this move?"

This library allows Pine Script developers to integrate LEI calculations into their own indicators and strategies.

How to Import

//@version=6

indicator("My Indicator")

import OrenLuxy/LuxyEnergyIndex/1 as LEI

Main Functions

`lei(src)` → float

Returns the LEI value on a 0-100 scale.

src (optional): Price source, default is `close`

Returns : LEI value (0-100) or `na` if insufficient data (first 50 bars)

leiValue = LEI.lei()

leiValue = LEI.lei(hlc3) // custom source

`leiDetailed(src)` → tuple

Returns LEI with all component values for detailed analysis.

= LEI.leiDetailed()

Returns:

`lei` - Final LEI value (0-100)

`extension` - Distance from VWAP in ATR units

`velocity` - 5-bar price change in ATR units

`volumeZ` - Volume Z-Score

`volumeModifier` - Applied modifier (1.0 = neutral)

`vwap` - VWAP value used

Component Functions

| Function | Description | Returns |

|-----------------------------------|---------------------------------|---------------|

| `calcExtension(src, vwap)` | Distance from VWAP / ATR | float |

| `calcVelocity(src)` | 5-bar price change / ATR | float |

| `calcVolumeZ()` | Volume Z-Score | float |

| `calcVolumeModifier(volZ)` | Volume modifier | float (≥1.0) |

| `getVWAP()` | Auto-detects asset type | float |

Signal Functions

| Function | Description | Returns |

|---------------------------------------------|----------------------------------|-----------|

| `isExhausted(lei, threshold)` | LEI ≥ threshold (default 70) | bool |

| `isSafe(lei, threshold)` | LEI ≤ threshold (default 30) | bool |

| `crossedExhaustion(lei, threshold)` | Crossed into exhaustion | bool |

| `crossedSafe(lei, threshold)` | Crossed into safe zone | bool |

Utility Functions

| Function | Description | Returns |

|----------------------------|-------------------------|-----------|

| `getZone(lei)` | Zone name | string |

| `getColor(lei)` | Recommended color | color |

| `hasEnoughHistory()` | Data check | bool |

| `minBarsRequired()` | Required bars | int (50) |

| `version()` | Library version | string |

Interpretation Guide

| LEI Range | Zone | Meaning |

|-------------|--------------|--------------------------------------------------|

| 0-30 | Safe | Low exhaustion, move may continue |

| 30-50 | Caution | Moderate exhaustion |

| 50-70 | Warning | Elevated exhaustion |

| 70-100 | Exhaustion | High exhaustion, increased reversal risk |

Example: Basic Usage

//@version=6

indicator("LEI Example", overlay=false)

import OrenLuxy/LuxyEnergyIndex/1 as LEI

// Get LEI value

leiValue = LEI.lei()

// Plot with dynamic color

plot(leiValue, "LEI", LEI.getColor(leiValue), 2)

// Reference lines

hline(70, "High", color.red)

hline(30, "Low", color.green)

// Alert on exhaustion

if LEI.crossedExhaustion(leiValue) and barstate.isconfirmed

alert("LEI crossed into exhaustion zone")

Technical Details

Fixed Parameters (by design):

Velocity Period: 5 bars

Volume Period: 20 bars

Z-Score Period: 50 bars

ATR Period: 14

Extension/Velocity Weights: 50/50

Asset Support:

Stocks/Forex: Uses Session VWAP (daily reset)

Crypto: Uses Rolling VWAP (50-bar window) - auto-detected

Edge Cases:

Returns `na` until 50 bars of history

Zero volume: Volume modifier defaults to 1.0 (neutral)

Credits and Acknowledgments

This library builds upon established technical analysis concepts:

VWAP - Industry standard volume-weighted price measure

ATR by J. Welles Wilder Jr. (1978) - Volatility normalization

Z-Score - Statistical normalization method

Volume analysis principles from Volume Spread Analysis (VSA) methodology

Disclaimer

This library is provided for **educational and informational purposes only**. It does not constitute financial advice. Past performance does not guarantee future results. The exhaustion readings are probabilistic indicators, not guarantees of price reversal. Always conduct your own research and use proper risk management when trading.

CEDEARDataLibrary "CEDEARData"

getUnderlying(cedearTicker)

Parameters:

cedearTicker (simple string)

getRatio(cedearTicker)

Parameters:

cedearTicker (simple string)

getCurrency(cedearTicker)

Parameters:

cedearTicker (simple string)

isValidCedear(cedearTicker)

Parameters:

cedearTicker (simple string)

BybitMinOrderSizeBybit Order Quantity Compliance Library

This library provides all utility functions required for TradingView strategies

that execute orders on Bybit via webhooks.

Problem:

Bybit enforces two strict rules on every order submitted:

Minimum Order Size – each symbol has its own minimum quantity.

Quantity Precision – each symbol requires rounding to the correct number of decimals.

TradingView does not expose this metadata, so strategies can easily submit

quantities that Bybit rejects as invalid.

Solution (This Library):

This library embeds full Bybit contract metadata, including:

A complete mapping of Bybit symbols → minimum order size

A complete mapping of Bybit symbols → allowed precision (decimal places)

A helper to normalize tickers (removing `.P` suffix for Bybit perpetuals)

It also exposes utility functions to automatically make your quantities valid:

`normalizeTicker()` — removes `.P` for consistent lookup

`getMinOrderSize()` — returns the correct minimum order size

`getPrecisionForTicker()` — returns required quantity precision

`floorQty()` — floors quantities to valid minimum increments

`roundQty()` — rounds quantities to valid decimal precision

Use Cases:

Ensuring webhook strategies never send too-small orders

Rounding limit/market orders correctly before execution

Making Pine strategies execution-accurate for Bybit

Avoiding "order rejected: qty too small / invalid precision" errors

This library is recommended for:

Live trading via TradingView → Bybit webhooks

Backtesting strategies that simulate real Bybit constraints

Source: www.bybit.com

Updated: 2025-11-25 — Bybit contract metadata

normalizeTicker(symbol)

Normalizes Bybit perpetual tickers by removing the ".P" suffix.

precisionFromMinOrder(minOrder)

Derives precision (decimal places) from minimum order size.

getMinOrderSize(symbol)

Retrieves the minimum order size for the current or given symbol.

getPrecisionForTicker(symbol)

Retrieves the required quantity precision (decimal places) for a given Bybit symbol.

floorQty(qty, symbol)

Rounds a quantity down to the nearest valid minimum order size for a given symbol.

roundQty(qty, symbol)

Rounds a quantity to the valid precision for the specified symbol.

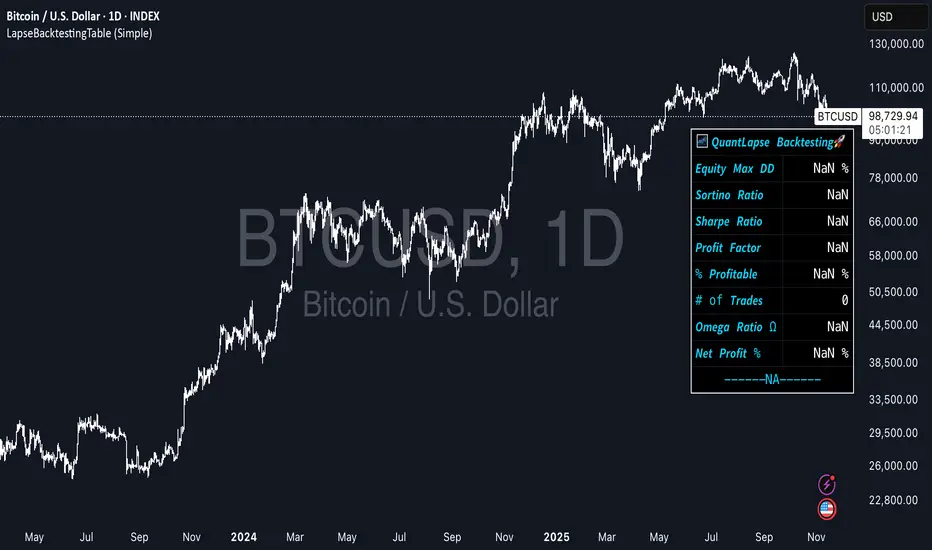

LapseBacktestingTableLibrary "LapseBacktestingMetrics"

This library provides a robust set of quantitative backtesting and performance evaluation functions for Pine Script strategies. It’s designed to help traders, quants, and developers assess risk, return, and robustness through detailed statistical metrics — including Sharpe, Sortino, Omega, drawdowns, and trade efficiency.

Built to enhance any trading strategy’s evaluation framework, this library allows you to visualize performance with the quantlapseTable() function, producing an interactive on-chart performance table.

Credit to EliCobra and BikeLife76 for original concept inspiration.

curve(disp_ind)

Retrieves a selected performance curve of your strategy.

Parameters:

disp_ind (simple string): Type of curve to plot. Options include "Equity", "Open Profit", "Net Profit", "Gross Profit".

Returns: (float) Corresponding performance curve value.

cleaner(disp_ind, plot)

Filters and displays selected strategy plots for clean visualization.

Parameters:

disp_ind (simple string): Type of display.

plot (simple float): Strategy plot variable.

Returns: (float) Filtered plot value.

maxEquityDrawDown()

Calculates the maximum equity drawdown during the strategy’s lifecycle.

Returns: (float) Maximum equity drawdown percentage.

maxTradeDrawDown()

Computes the worst intra-trade drawdown among all closed trades.

Returns: (float) Maximum intra-trade drawdown percentage.

consecutive_wins()

Finds the highest number of consecutive winning trades.

Returns: (int) Maximum consecutive wins.

consecutive_losses()

Finds the highest number of consecutive losing trades.

Returns: (int) Maximum consecutive losses.

no_position()

Counts the maximum consecutive bars where no position was held.

Returns: (int) Maximum flat days count.

long_profit()

Calculates total profit generated by long positions as a percentage of initial capital.

Returns: (float) Total long profit %.

short_profit()

Calculates total profit generated by short positions as a percentage of initial capital.

Returns: (float) Total short profit %.

prev_month()

Measures the previous month’s profit or loss based on equity change.

Returns: (float) Monthly equity delta.

w_months()

Counts the number of profitable months in the backtest.

Returns: (int) Total winning months.

l_months()

Counts the number of losing months in the backtest.

Returns: (int) Total losing months.

checktf()

Returns the time-adjusted scaling factor used in Sharpe and Sortino ratio calculations based on chart timeframe.

Returns: (float) Annualization multiplier.

stat_calc()

Performs complete statistical computation including drawdowns, Sharpe, Sortino, Omega, trade stats, and profit ratios.

Returns: (array)

.

f_colors(x, nv)

Generates a color gradient for performance values, supporting dynamic table visualization.

Parameters:

x (simple string): Metric label name.

nv (simple float): Metric numerical value.

Returns: (color) Gradient color value for table background.

quantlapseTable(option, position)

Displays an interactive Performance Table summarizing all major backtesting metrics.

Includes Sharpe, Sortino, Omega, Profit Factor, drawdowns, profitability %, and trade statistics.

Parameters:

option (simple string): Table type — "Full", "Simple", or "None".

position (simple string): Table position — "Top Left", "Middle Right", "Bottom Left", etc.

Returns: (table) On-chart performance visualization table.

This library empowers advanced quantitative evaluation directly within Pine Script®, ideal for strategy developers seeking deeper performance diagnostics and intuitive on-chart metrics.

UTBotLibrary "UTBot"

is a powerful and flexible trading toolkit implemented in Pine Script. Based on the widely recognized UT Bot strategy originally developed by Yo_adriiiiaan with important enhancements by HPotter, this library provides users with customizable functions for dynamic trailing stop calculations using ATR (Average True Range), trend detection, and signal generation. It enables developers and traders to seamlessly integrate UT Bot logic into their own indicators and strategies without duplicating code.

Key features include:

Accurate ATR-based trailing stop and reversal detection

Multi-timeframe support for enhanced signal reliability

Clean and efficient API for easy integration and customization

Detailed documentation and examples for quick adoption

Open-source and community-friendly, encouraging collaboration and improvements

We sincerely thank Yo_adriiiiaan for the original UT Bot concept and HPotter for valuable improvements that have made this strategy even more robust. This library aims to honor their work by making the UT Bot methodology accessible to Pine Script developers worldwide.

This library is designed for Pine Script programmers looking to leverage the proven UT Bot methodology to build robust trading systems with minimal effort and maximum maintainability.

UTBot(h, l, c, multi, leng)

Parameters:

h (float) - high

l (float) - low

c (float)-close

multi (float)- multi for ATR

leng (int)-length for ATR

Returns:

xATRTS - ATR Based TrailingStop Value

pos - pos==1, long position, pos==-1, shot position

signal - 0 no signal, 1 buy, -1 sell

AlertSenderLibrary_TradingFinderLibrary "AlertSenderLibrary_TradingFinder"

TODO: add library description here

AlertSender(Condition, Alert, AlertName, AlertType, DetectionType, SetupData, Frequncy, UTC, MoreInfo, Message, o, h, l, c, Entry, TP, SL, Distal, Proximal)

Parameters:

Condition (bool)

Alert (string)

AlertName (string)

AlertType (string)

DetectionType (string)

SetupData (string)

Frequncy (string)

UTC (string)

MoreInfo (string)

Message (string)

o (float)

h (float)

l (float)

c (float)

Entry (float)

TP (float)

SL (float)

Distal (float)

Proximal (float)

ApicodeLibrary "Apicode"

percentToTicks(percent, from)

Converts a percentage of the average entry price or a specified price to ticks when the

strategy has an open position.

Parameters:

percent (float) : (series int/float) The percentage of the `from` price to express in ticks, e.g.,

a value of 50 represents 50% (half) of the price.

from (float) : (series int/float) Optional. The price from which to calculate a percentage and convert

to ticks. The default is `strategy.position_avg_price`.

Returns: (float) The number of ticks within the specified percentage of the `from` price if

the strategy has an open position. Otherwise, it returns `na`.

percentToPrice(percent, from)

Calculates the price value that is a specific percentage distance away from the average

entry price or a specified price when the strategy has an open position.

Parameters:

percent (float) : (series int/float) The percentage of the `from` price to use as the distance. If the value

is positive, the calculated price is above the `from` price. If negative, the result is

below the `from` price. For example, a value of 10 calculates the price 10% higher than

the `from` price.

from (float) : (series int/float) Optional. The price from which to calculate a percentage distance.

The default is `strategy.position_avg_price`.

Returns: (float) The price value at the specified `percentage` distance away from the `from` price

if the strategy has an open position. Otherwise, it returns `na`.

percentToCurrency(price, percent)

Parameters:

price (float) : (series int/float) The price from which to calculate the percentage.

percent (float) : (series int/float) The percentage of the `price` to calculate.

Returns: (float) The amount of the symbol's currency represented by the percentage of the specified

`price`.

percentProfit(exitPrice)

Calculates the expected profit/loss of the open position if it were to close at the

specified `exitPrice`, expressed as a percentage of the average entry price.

NOTE: This function may not return precise values for positions with multiple open trades

because it only uses the average entry price.

Parameters:

exitPrice (float) : (series int/float) The position's hypothetical closing price.

Returns: (float) The expected profit percentage from exiting the position at the `exitPrice`. If

there is no open position, it returns `na`.

priceToTicks(price)

Converts a price value to ticks.

Parameters:

price (float) : (series int/float) The price to convert.

Returns: (float) The value of the `price`, expressed in ticks.

ticksToPrice(ticks, from)

Calculates the price value at the specified number of ticks away from the average entry

price or a specified price when the strategy has an open position.

Parameters:

ticks (float) : (series int/float) The number of ticks away from the `from` price. If the value is positive,

the calculated price is above the `from` price. If negative, the result is below the `from`

price.

from (float) : (series int/float) Optional. The price to evaluate the tick distance from. The default is

`strategy.position_avg_price`.

Returns: (float) The price value at the specified number of ticks away from the `from` price if

the strategy has an open position. Otherwise, it returns `na`.

ticksToCurrency(ticks)

Converts a specified number of ticks to an amount of the symbol's currency.

Parameters:

ticks (float) : (series int/float) The number of ticks to convert.

Returns: (float) The amount of the symbol's currency represented by the tick distance.

ticksToStopLevel(ticks)

Calculates a stop-loss level using a specified tick distance from the position's average

entry price. A script can plot the returned value and use it as the `stop` argument in a

`strategy.exit()` call.

Parameters:

ticks (float) : (series int/float) The number of ticks from the position's average entry price to the

stop-loss level. If the position is long, the value represents the number of ticks *below*

the average entry price. If short, it represents the number of ticks *above* the price.

Returns: (float) The calculated stop-loss value for the open position. If there is no open position,

it returns `na`.

ticksToTpLevel(ticks)

Calculates a take-profit level using a specified tick distance from the position's average

entry price. A script can plot the returned value and use it as the `limit` argument in a

`strategy.exit()` call.

Parameters:

ticks (float) : (series int/float) The number of ticks from the position's average entry price to the

take-profit level. If the position is long, the value represents the number of ticks *above*

the average entry price. If short, it represents the number of ticks *below* the price.

Returns: (float) The calculated take-profit value for the open position. If there is no open

position, it returns `na`.

calcPositionSizeByStopLossTicks(stopLossTicks, riskPercent)

Calculates the entry quantity required to risk a specified percentage of the strategy's

current equity at a tick-based stop-loss level.

Parameters:

stopLossTicks (float) : (series int/float) The number of ticks in the stop-loss distance.

riskPercent (float) : (series int/float) The percentage of the strategy's equity to risk if a trade moves

`stopLossTicks` away from the entry price in the unfavorable direction.

Returns: (int) The number of contracts/shares/lots/units to use as the entry quantity to risk the

specified percentage of equity at the stop-loss level.

calcPositionSizeByStopLossPercent(stopLossPercent, riskPercent, entryPrice)

Calculates the entry quantity required to risk a specified percentage of the strategy's

current equity at a percent-based stop-loss level.

Parameters:

stopLossPercent (float) : (series int/float) The percentage of the `entryPrice` to use as the stop-loss distance.

riskPercent (float) : (series int/float) The percentage of the strategy's equity to risk if a trade moves

`stopLossPercent` of the `entryPrice` in the unfavorable direction.

entryPrice (float) : (series int/float) Optional. The entry price to use in the calculation. The default is

`close`.

Returns: (int) The number of contracts/shares/lots/units to use as the entry quantity to risk the

specified percentage of equity at the stop-loss level.

exitPercent(id, lossPercent, profitPercent, qty, qtyPercent, comment, alertMessage)

A wrapper for the `strategy.exit()` function designed for creating stop-loss and

take-profit orders at percentage distances away from the position's average entry price.

NOTE: This function calls `strategy.exit()` without a `from_entry` ID, so it creates exit

orders for *every* entry in an open position until the position closes. Therefore, using

this function when the strategy has a pyramiding value greater than 1 can lead to

unexpected results. See the "Exits for multiple entries" section of our User Manual's

"Strategies" page to learn more about this behavior.

Parameters:

id (string) : (series string) Optional. The identifier of the stop-loss/take-profit orders, which

corresponds to an exit ID in the strategy's trades after an order fills. The default is

`"Exit"`.

lossPercent (float) : (series int/float) The percentage of the position's average entry price to use as the

stop-loss distance. The function does not create a stop-loss order if the value is `na`.

profitPercent (float) : (series int/float) The percentage of the position's average entry price to use as the

take-profit distance. The function does not create a take-profit order if the value is `na`.

qty (float) : (series int/float) Optional. The number of contracts/lots/shares/units to close when an

exit order fills. If specified, the call uses this value instead of `qtyPercent` to

determine the order size. The exit orders reserve this quantity from the position, meaning

other orders from `strategy.exit()` cannot close this portion until the strategy fills or

cancels those orders. The default is `na`, which means the order size depends on the

`qtyPercent` value.

qtyPercent (float) : (series int/float) Optional. A value between 0 and 100 representing the percentage of the

open trade quantity to close when an exit order fills. The exit orders reserve this

percentage from the open trades, meaning other calls to this command cannot close this

portion until the strategy fills or cancels those orders. The percentage calculation

depends on the total size of the applicable open trades without considering the reserved

amount from other `strategy.exit()` calls. The call ignores this parameter if the `qty`

value is not `na`. The default is 100.

comment (string) : (series string) Optional. Additional notes on the filled order. If the value is specified

and not an empty "string", the Strategy Tester and the chart show this text for the order

instead of the specified `id`. The default is `na`.

alertMessage (string) : (series string) Optional. Custom text for the alert that fires when an order fills. If the

value is specified and not an empty "string", and the "Message" field of the "Create Alert"

dialog box contains the `{{strategy.order.alert_message}}` placeholder, the alert message

replaces the placeholder with this text. The default is `na`.

Returns: (void) The function does not return a usable value.

closeAllAtEndOfSession(comment, alertMessage)

A wrapper for the `strategy.close_all()` function designed to close all open trades with a

market order when the last bar in the current day's session closes. It uses the command's

`immediately` parameter to exit all trades at the last bar's `close` instead of the `open`

of the next session's first bar.

Parameters:

comment (string) : (series string) Optional. Additional notes on the filled order. If the value is specified

and not an empty "string", the Strategy Tester and the chart show this text for the order

instead of the automatically generated exit identifier. The default is `na`.

alertMessage (string) : (series string) Optional. Custom text for the alert that fires when an order fills. If the

value is specified and not an empty "string", and the "Message" field of the "Create Alert"

dialog box contains the `{{strategy.order.alert_message}}` placeholder, the alert message

replaces the placeholder with this text. The default is `na`.

Returns: (void) The function does not return a usable value.

closeAtEndOfSession(entryId, comment, alertMessage)

A wrapper for the `strategy.close()` function designed to close specific open trades with a

market order when the last bar in the current day's session closes. It uses the command's

`immediately` parameter to exit the trades at the last bar's `close` instead of the `open`

of the next session's first bar.

Parameters:

entryId (string)

comment (string) : (series string) Optional. Additional notes on the filled order. If the value is specified

and not an empty "string", the Strategy Tester and the chart show this text for the order

instead of the automatically generated exit identifier. The default is `na`.

alertMessage (string) : (series string) Optional. Custom text for the alert that fires when an order fills. If the

value is specified and not an empty "string", and the "Message" field of the "Create Alert"

dialog box contains the `{{strategy.order.alert_message}}` placeholder, the alert message

replaces the placeholder with this text. The default is `na`.

Returns: (void) The function does not return a usable value.

sortinoRatio(interestRate, forceCalc)

Calculates the Sortino ratio of the strategy based on realized monthly returns.

Parameters:

interestRate (simple float) : (simple int/float) Optional. The *annual* "risk-free" return percentage to compare against

strategy returns. The default is 2, meaning it uses an annual benchmark of 2%.

forceCalc (bool) : (series bool) Optional. A value of `true` forces the function to calculate the ratio on the

current bar. If the value is `false`, the function calculates the ratio only on the latest

available bar for efficiency. The default is `false`.

Returns: (float) The Sortino ratio, which estimates the strategy's excess return per unit of

downside volatility.

sharpeRatio(interestRate, forceCalc)

Calculates the Sharpe ratio of the strategy based on realized monthly returns.

Parameters:

interestRate (simple float) : (simple int/float) Optional. The *annual* "risk-free" return percentage to compare against

strategy returns. The default is 2, meaning it uses an annual benchmark of 2%.

forceCalc (bool) : (series bool) Optional. A value of `true` forces the function to calculate the ratio on the

current bar. If the value is `false`, the function calculates the ratio only on the latest

available bar for efficiency. The default is `false`.

Returns: (float) The Sortino ratio, which estimates the strategy's excess return per unit of

total volatility.

WCWebLibLibrary "WCWebLib"

method buildWebhookJson(msg, constants)

Builds the final JSON payload from a webhookMessage type.

Namespace types: webhookMessage

Parameters:

msg (webhookMessage) : (webhookMessage) A prepared webhookMessage.

constants (CONSTANTS)

Returns: A JSON Payload.

method buildTakeProfitJson(msg)

Builds the takeProfit JSON message to be used in a webhook message.

Namespace types: takeProfitMessage

Parameters:

msg (takeProfitMessage)

method buildStopLossJson(msg, constants)

Builds the stopLoss JSON message to be used in a webhook message.

Namespace types: stopLossMessage

Parameters:

msg (stopLossMessage)

constants (CONSTANTS)

CONSTANTS

Constants for payload values.

Fields:

ACTION_BUY (series string)

ACTION_SELL (series string)

ACTION_EXIT (series string)

ACTION_CANCEL (series string)

ACTION_ADD (series string)

SENTIMENT_BULLISH (series string)

SENTIMENT_BEARISH (series string)

SENTIMENT_LONG (series string)

SENTIMENT_SHORT (series string)

SENTIMENT_FLAT (series string)

STOP_LOSS_TYPE_STOP (series string)

STOP_LOSS_TYPE_STOP_LIMIT (series string)

STOP_LOSS_TYPE_TRAILING_STOP (series string)

EXTENDEDHOURS (series bool)

ORDER_TYPE_LIMIT (series string)

ORDER_TYPE_MARKET (series string)

TIF_DAY (series string)

webhookMessage

Final webhook message.

Fields:

ticker (series string)

action (series string)

sentiment (series string)

price (series float)

quantity (series int)

takeProfit (series string)

stopLoss (series string)

extendedHours (series bool)

type (series string)

timeInForce (series string)

takeProfitMessage

Take profit message.

Fields:

limitPrice (series float)

percent (series float)

amount (series float)

stopLossMessage

Stop loss message.

Fields:

type (series string)

percent (series float)

amount (series float)

stopPrice (series float)

limitPrice (series float)

trailPrice (series float)

trailPercent (series float)

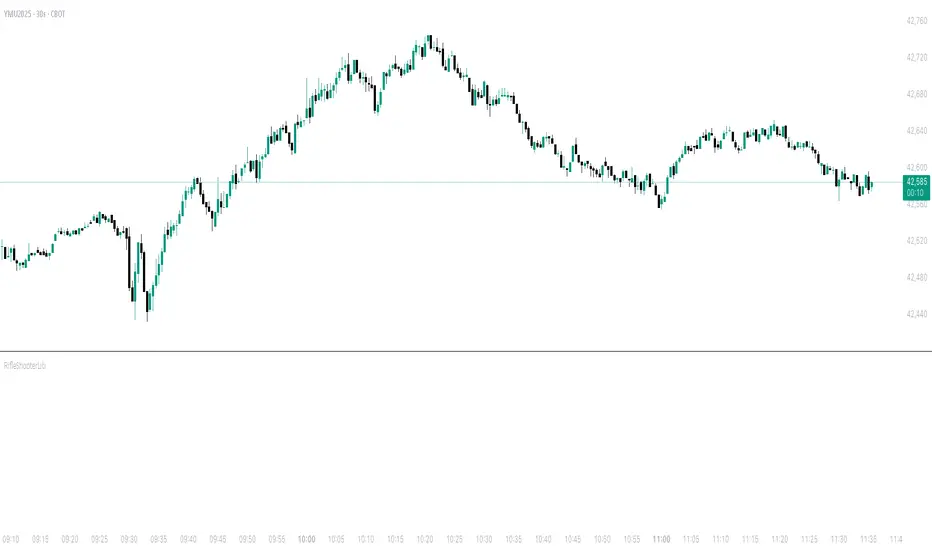

RifleShooterLibLibrary "RifleShooterLib"

Provides a collection of helper functions in support of the Rifle Shooter Indicators.

Functions support the key components of the Rifle Trade algorithm including

* measuring momentum

* identifying paraboloic price action (to disable the algorthim during such time)

* determine the lookback criteria of X point movement in last N minutes

* processing and navigating between the 23/43/73 levels

* maintaining a status table of algorithm progress

toStrRnd(val, digits)

Parameters:

val (float)

digits (int)

_isValidTimeRange(startTimeInput, endTimeInput)

Parameters:

startTimeInput (string)

endTimeInput (string)

_normalize(_src, _min, _max)

_normalize Normalizes series with unknown min/max using historical min/max.

Parameters:

_src (float) : Source series to normalize

_min (float) : minimum value of the rescaled series

_max (float) : maximum value of the rescaled series

Returns: The series scaled with values between min and max

arrayToSeries(arrayInput)

arrayToSeries Return an array from the provided series.

Parameters:

arrayInput (array) : Source array to convert to a series

Returns: The array as a series datatype

f_parabolicFiltering(_activeCount, long, shooterRsi, shooterRsiLongThreshold, shooterRsiShortThreshold, fiveMinuteRsi, fiveMinRsiLongThreshold, fiveMinRsiShortThreshold, shooterRsiRoc, shooterRsiRocLongThreshold, shooterRsiRocShortThreshold, quickChangeLookbackBars, quckChangeThreshold, curBarChangeThreshold, changeFromPrevBarThreshold, maxBarsToholdParabolicMoveActive, generateLabels)

f_parabolicFiltering Return true when price action indicates a parabolic active movement based on the provided inputs and thresholds.

Parameters:

_activeCount (int)

long (bool)

shooterRsi (float)

shooterRsiLongThreshold (float)

shooterRsiShortThreshold (float)

fiveMinuteRsi (float)

fiveMinRsiLongThreshold (float)

fiveMinRsiShortThreshold (float)

shooterRsiRoc (float)

shooterRsiRocLongThreshold (float)

shooterRsiRocShortThreshold (float)

quickChangeLookbackBars (int)

quckChangeThreshold (int)

curBarChangeThreshold (int)

changeFromPrevBarThreshold (int)

maxBarsToholdParabolicMoveActive (int)

generateLabels (bool)

rsiValid(rsi, buyThreshold, sellThreshold)

rsiValid Returns true if the provided RSI value is withing the associated threshold. For the unused threshold set it to na

Parameters:

rsi (float)

buyThreshold (float)

sellThreshold (float)

squezeBands(source, length)

squezeBands Returns the squeeze bands momentum color of current source series input

Parameters:

source (float)

length (int)

f_momentumOscilator(source, length, transperency)

f_momentumOscilator Returns the squeeze pro momentum value and bar color states of the series input

Parameters:

source (float)

length (int)

transperency (int)

f_getLookbackExtreme(lowSeries, highSeries, lbBars, long)

f_getLookbackExtreme Return the highest high or lowest low over the look back window

Parameters:

lowSeries (float)

highSeries (float)

lbBars (int)

long (bool)

f_getInitialMoveTarget(lbExtreme, priveMoveOffset, long)

f_getInitialMoveTarget Return the point delta required to achieve an initial rifle move (X points over Y lookback)

Parameters:

lbExtreme (float)

priveMoveOffset (int)

long (bool)

isSymbolSupported(sym)

isSymbolSupported Return true if provided symbol is one of the supported DOW Rifle Indicator symbols

Parameters:

sym (string)

getBasePrice(price)

getBasePrice Returns integer portion of provided float

Parameters:

price (float)

getLastTwoDigitsOfPrice(price)

getBasePrice Returns last two integer numerals of provided float value

Parameters:

price (float)

getNextLevelDown(price, lowestLevel, middleLevel, highestLevel)

getNextLevelDown Returns the next level above the provided price value

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

getNextLevelUp(price, lowestLevel, middleLevel, highestLevel)

getNextLevelUp Returns the next level below the provided price value

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

isALevel(price, lowestLevel, middleLevel, highestLevel)

isALevel Returns true if the provided price is onve of the specified levels

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

getClosestLevel(price, lowestLevel, middleLevel, highestLevel)

getClosestLevel Returns the level closest to the price value provided

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

f_fillSetupTableCell(_table, _col, _row, _text, _bgcolor, _txtcolor, _text_size)

f_fillSetupTableCell Helper function to fill a setup table celll

Parameters:

_table (table)

_col (int)

_row (int)

_text (string)

_bgcolor (color)

_txtcolor (color)

_text_size (string)

f_fillSetupTableRow(_table, _row, _col0Str, _col1Str, _col2Str, _bgcolor, _textColor, _textSize)

f_fillSetupTableRow Helper function to fill a setup table row

Parameters:

_table (table)

_row (int)

_col0Str (string)

_col1Str (string)

_col2Str (string)

_bgcolor (color)

_textColor (color)

_textSize (string)

f_addBlankRow(_table, _row)

f_addBlankRow Helper function to fill a setup table row with empty values

Parameters:

_table (table)

_row (int)

f_updateVersionTable(versionTable, versionStr, versionDateStr)

f_updateVersionTable Helper function to fill the version table with provided values

Parameters:

versionTable (table)

versionStr (string)

versionDateStr (string)

f_updateSetupTable(_table, parabolicMoveActive, initialMoveTargetOffset, initialMoveAchieved, shooterRsi, shooterRsiValid, rsiRocEnterThreshold, shooterRsiRoc, fiveMinuteRsi, fiveMinuteRsiValid, requireValid5MinuteRsiForEntry, stallLevelOffset, stallLevelExceeded, stallTargetOffset, recoverStallLevelValid, curBarChangeValid, volumeRoc, volumeRocThreshold, enableVolumeRocForTrigger, tradeActive, entryPrice, curCloseOffset, curSymCashDelta, djiCashDelta, showDjiDelta, longIndicator, fontSize)

f_updateSetupTable Manages writing current data to the setup table

Parameters:

_table (table)

parabolicMoveActive (bool)

initialMoveTargetOffset (float)

initialMoveAchieved (bool)

shooterRsi (float)

shooterRsiValid (bool)

rsiRocEnterThreshold (float)

shooterRsiRoc (float)

fiveMinuteRsi (float)

fiveMinuteRsiValid (bool)

requireValid5MinuteRsiForEntry (bool)

stallLevelOffset (float)

stallLevelExceeded (bool)

stallTargetOffset (float)

recoverStallLevelValid (bool)

curBarChangeValid (bool)

volumeRoc (float)

volumeRocThreshold (float)

enableVolumeRocForTrigger (bool)

tradeActive (bool)

entryPrice (float)

curCloseOffset (float)

curSymCashDelta (float)

djiCashDelta (float)

showDjiDelta (bool)

longIndicator (bool)

fontSize (string)

BackTestLibLibrary "BackTestLib"

Allows backtesting indicator performance. Tracks typical metrics such as won/loss, profit factor, draw down, etc. Trading View strategy library provides similar (and more comprehensive)

functionality but only works with strategies. This libary was created to address performance tracking within indicators.

Two primary outputs are generated:

1. Summary Table: Displays overall performance metrics for the indicator over the chart's loaded timeframe and history

2. Details Table: Displays a table of individual trade entries and exits. This table can grow larger than the available chart space. It does have a max number of rows supported. I haven't

found a way to add scroll bars or scroll bar equivalents yet.

f_init(data, _defaultStopLoss, _defaultTakeProfit, _useTrailingStop, _useTraingStopToBreakEven, _trailingStopActivation, _trailingStopOffset)

f_init Initialize the backtest data type. Called prior to using the backtester functions

Parameters:

data (backtesterData) : backtesterData to initialize

_defaultStopLoss (float) : Default trade stop loss to apply

_defaultTakeProfit (float) : Default trade take profit to apply

_useTrailingStop (bool) : Trailing stop enabled

_useTraingStopToBreakEven (bool) : When trailing stop active, trailing stop will increase no further than the entry price

_trailingStopActivation (int) : When trailing stop active, trailing will begin once price exceeds base stop loss by this number of points

_trailingStopOffset (int) : When trailing stop active, it will trail the max price achieved by this number of points

Returns: Initialized data set

f_buildResultStr(_resultType, _price, _resultPoints, _numWins, _pointsWon, _numLoss, _pointsLost)

f_buildResultStr Helper function to construct a string of resutling data for exit tooltip labels

Parameters:

_resultType (string)

_price (float)

_resultPoints (float)

_numWins (int)

_pointsWon (float)

_numLoss (int)

_pointsLost (float)

f_buildResultLabel(data, labelVertical, labelOffset, long)

f_buildResultLabel Helper function to construct an Exit label for display on the chart

Parameters:

data (backtesterData)

labelVertical (bool)

labelOffset (int)

long (bool)

f_updateTrailingStop(_entryPrice, _curPrice, _sl, _tp, trailingStopActivationInput, trailingStopOffsetInput, useTrailingStopToBreakEven)

f_updateTrailingStop Helper function to advance the trailing stop as price action dictates

Parameters:

_entryPrice (float)

_curPrice (float)

_sl (float)

_tp (float)

trailingStopActivationInput (float)

trailingStopOffsetInput (float)

useTrailingStopToBreakEven (bool)

Returns: Updated stop loss for current price action

f_enterShort(data, entryPrice, fixedStopLoss)

f_enterShort Helper function to enter a short and collect data necessary for tracking the trade entry

Parameters:

data (backtesterData)

entryPrice (float)

fixedStopLoss (float)

Returns: Updated backtest data

f_enterLong(data, entryPrice, fixedStopLoss)

f_enterLong Helper function to enter a long and collect data necessary for tracking the trade entry

Parameters:

data (backtesterData)

entryPrice (float)

fixedStopLoss (float)

Returns: Updated backtest data

f_exitTrade(data)

f_enterLong Helper function to exit a trade and update/reset tracking data

Parameters:

data (backtesterData)

Returns: Updated backtest data

f_checkTradeConditionForExit(data, condition, curPrice, enableRealTime)

f_checkTradeConditionForExit Helper function to determine if provided condition indicates an exit

Parameters:

data (backtesterData)

condition (bool) : When true trade will exit

curPrice (float)

enableRealTime (bool) : When true trade will evaluate if barstate is relatime or barstate is confirmed; otherwise just checks on is confirmed

Returns: Updated backtest data

f_checkTrade(data, curPrice, curLow, curHigh, enableRealTime)

f_checkTrade Helper function to determine if current price action dictates stop loss or take profit exit

Parameters:

data (backtesterData)

curPrice (float)

curLow (float)

curHigh (float)

enableRealTime (bool) : When true trade will evaluate if barstate is relatime or barstate is confirmed; otherwise just checks on is confirmed

Returns: Updated backtest data

f_fillCell(_table, _column, _row, _title, _value, _bgcolor, _txtcolor, _text_size)

f_fillCell Helper function to construct result table cells

Parameters:

_table (table)

_column (int)

_row (int)

_title (string)

_value (string)

_bgcolor (color)

_txtcolor (color)

_text_size (string)

Returns: Table cell

f_prepareStatsTable(data, drawTesterSummary, drawTesterDetails, summaryTableTextSize, detailsTableTextSize, displayRowZero, summaryTableLocation, detailsTableLocation)

f_fillCell Helper function to populate result table

Parameters:

data (backtesterData)

drawTesterSummary (bool)

drawTesterDetails (bool)

summaryTableTextSize (string)

detailsTableTextSize (string)

displayRowZero (bool)

summaryTableLocation (string)

detailsTableLocation (string)

Returns: Updated backtest data

backtesterData

backtesterData - container for backtest performance metrics

Fields:

tradesArray (array) : Array of strings with entries for each individual trade and its results

pointsBalance (series float) : Running sum of backtest points won/loss results

drawDown (series float) : Running sum of backtest total draw down points

maxDrawDown (series float) : Running sum of backtest total draw down points

maxRunup (series float) : Running sum of max points won over the backtest

numWins (series int) : Number of wins of current backtes set

numLoss (series int) : Number of losses of current backtes set

pointsWon (series float) : Running sum of points won to date

pointsLost (series float) : Running sum of points lost to date

entrySide (series string) : Current entry long/short

tradeActive (series bool) : Indicates if a trade is currently active

tradeComplete (series bool) : Indicates if a trade just exited (due to stop loss or take profit)

entryPrice (series float) : Current trade entry price

entryTime (series int) : Current trade entry time

sl (series float) : Current trade stop loss

tp (series float) : Current trade take profit

defaultStopLoss (series float) : Default trade stop loss to apply

defaultTakeProfit (series float) : Default trade take profit to apply

useTrailingStop (series bool) : Trailing stop enabled

useTrailingStopToBreakEven (series bool) : When trailing stop active, trailing stop will increase no further than the entry price

trailingStopActivation (series int) : When trailing stop active, trailing will begin once price exceeds base stop loss by this number of points

trailingStopOffset (series int) : When trailing stop active, it will trail the max price achieved by this number of points

resultType (series string) : Current trade won/lost

exitPrice (series float) : Current trade exit price

resultPoints (series float) : Current trade points won/lost

summaryTable (series table) : Table to deisplay summary info

tradesTable (series table) : Table to display per trade info

TradersPostDeluxeLibrary "TradersPostDeluxe"

TradersPost integration. It's currently not very deluxe

SendEntryAlert(ticker, action, quantity, orderType, takeProfit, stopLoss, id, price, timestamp, timezone)

Sends an alert to TradersPost to trigger an Entry

Parameters:

ticker (string) : Symbol to trade. Default is syminfo.ticker

action (series Action) : TradersPostAction (.buy, .sell) default = buy

quantity (float) : Amount to trade, default = 1

orderType (series OrderType) : TradersPostOrderType, default =e TradersPostOrderType.market

takeProfit (float) : Take profit limit price

stopLoss (float) : Stop loss price

id (string) : id for the trade

price (float) : Expected price

timestamp (int) : Time of the trade for reporting, defaults to timenow

timezone (string) : associated with the time, defaults to syminfo.timezone

Returns: Nothing

SendExitAlert(ticker, price, timestamp, timezone)

Sends an alert to TradersPost to trigger an Exit

Parameters:

ticker (string) : Symbol to flatten

price (float) : Documented planned price

timestamp (int) : Time of the trade for reporting, defaults to timenow

timezone (string) : associated with the time, defaults to syminfo.timezone

Returns: Nothing

WeightedVolumeUtilsLibrary "WeightedVolumeUtils"

fun(x)

Returns the input value (placeholder function).

Parameters:

x (float) : A float value.

Returns: The same float value passed as input.

weightedBSEVolume()

Calculates the weighted volume for BSE index based on top constituent stocks.

Returns: Weighted volume value based on fixed weights for BSE SENSEX stocks.

getAdjustedVolume()

Returns the adjusted volume for SENSEX or regular volume otherwise.

Returns: Weighted BSE volume if current symbol is SENSEX, else raw volume.

StrategyUtilsLibrary "StrategyUtils"

getHeikinAshi(open, high, low, close)

getHeikinAshi

Parameters:

open (float) : float: Raw open price

high (float) : float: Raw high price

low (float) : float: Raw low price

close (float) : float: Raw close price

Returns: tuple of haOpen, haClose, haHigh, haLow

getFibExtensions(high, low)

getFibExtensions

Parameters:

high (float) : float: Highest point before trade

low (float) : float: Lowest point before trade

Returns: tuple of extension levels

inBacktestWindow(time, start, end)

inBacktestWindow

Parameters:

time (int) : int: Current bar time

start (int) : int: Start timestamp

end (int) : int: End timestamp

Returns: bool: true if within Fbrange

getCurrentState(buy, sell)

getCurrentState

Parameters:

buy (bool) : bool: Buy signal condition

sell (bool) : bool: Sell signal condition

Returns: string: "Buy", "Sell", or "None"

formatPrice(price)

formatPrice

Parameters:

price (float) : float: Input price value

Returns: string: Formatted price string

getColorByProfit(netprofit, initial, green, red)

getColorByProfit

Parameters:

netprofit (float) : float: Strategy net profit

initial (float) : float: Initial capital

green (color) : color: Positive color

red (color) : color: Negative color

Returns: color: Display color based on PnL

UTSStrategyHelperLibrary "UTSStrategyHelper"

TODO: add library description here

stopLossPrice(sig, atr, factor, isLong)

Calculates the stop loss price using a distance determined by ATR multiplied by a factor. Example for Long trade SL: PRICE - (ATR * factor).

Parameters:

sig (float)

atr (float) : (float): The value of the atr.

factor (float)

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

takeProfitPrice(sig, atr, factor, isLong)

Calculates the take profit price using a distance determined by ATR multiplied by a factor. Example for Long trade TP: PRICE + (ATR * factor). When take profit price is reached usually 50 % of the position is closed and the other 50 % get a trailing stop assigned.

Parameters:

sig (float)

atr (float) : (float): The value of the atr.

factor (float)

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

trailingStopPrice(initialStopPrice, atr, factor, priceSource, isLong)

Calculates a trailing stop price using a distance determined by ATR multiplied by a factor. It takes an initial price and follows the price closely if it changes in a favourable way.

Parameters:

initialStopPrice (float) : (float): The initial stop price which, for consistency also should be ATR * factor behind price: e.g. Long trade: PRICE - (ATR * factor)

atr (float) : (float): The value of the atr. Ideally the ATR value at trade open is taken and used for subsequent calculations.

factor (float)

priceSource (float) : (float): The current price.

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

hasGreaterPositionSize(positionSize)

Determines if the strategy's position size has grown since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasSmallerPositionSize(positionSize)

Determines if the strategy's position size has decreased since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasUnchangedPositionSize(positionSize)

Determines if the strategy's position size has changed since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

exporthasLongPosition(positionSize)

Determines if the strategy has an open long position.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasShortPosition(positionSize)

Determines if the strategy has an open short position.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasAnyPosition(positionSize)

Determines if the strategy has any open position, regardless of short or long.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasSignal(value)

Determines if the given argument contains a valid value (means not 'na').

Parameters:

value (float) : (float): The actual value.

Returns: (bool): A boolean value.

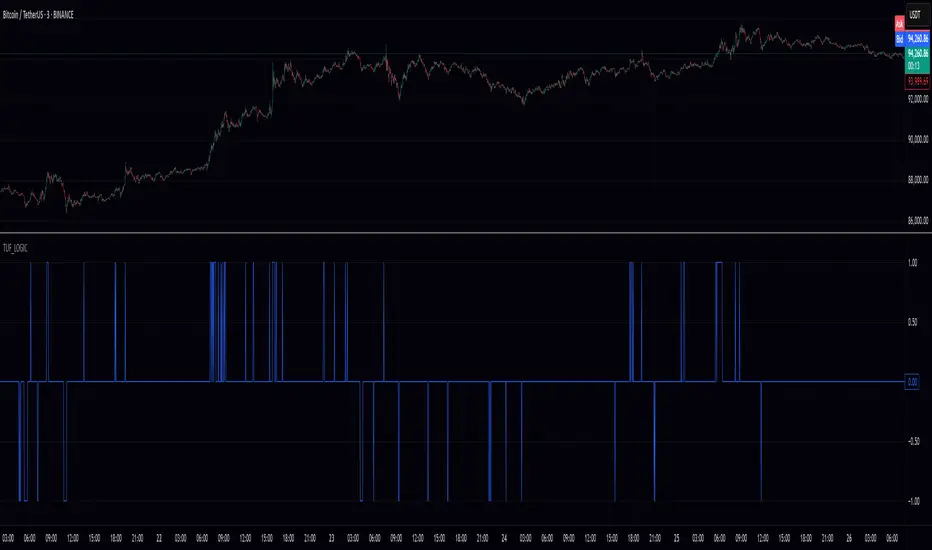

TUF_LOGICTUF_LOGIC: Three-Value Logic for Pine Script v6

The TUF_LOGIC library implements a robust three-valued logic system (trilean logic) for Pine Script v6, providing a formal framework for reasoning about uncertain or incomplete information in financial markets. By extending beyond binary True/False states to include an explicit "Uncertain" state, this library enables more nuanced algorithmic decision-making, particularly valuable in environments characterized by imperfect information.

Core Architecture

TUF_LOGIC offers two complementary interfaces for working with trilean values:

Enum-Based API (Recommended): Leverages Pine Script v6's enum capabilities with Trilean.True , Trilean.Uncertain , and Trilean.False for improved type safety and performance.

Integer-Based API (Legacy Support): Maintains compatibility with existing code using integer values 1 (True), 0 (Uncertain), and -1 (False).

Fundamental Operations

The library provides type conversion methods for seamless interaction between integer representation and enum types ( to_trilean() , to_int() ), along with validation functions to maintain trilean invariants.

Logical Operators

TUF_LOGIC extends traditional boolean operators to the trilean domain with NOT , AND , OR , XOR , and EQUALITY functions that properly handle the Uncertain state according to the principles of three-valued logic.

The library implements three different implication operators providing flexibility for different logical requirements: IMP_K (Kleene's approach), IMP_L (Łukasiewicz's approach), and IMP_RM3 (Relevant implication under RM3 logic).

Inspired by Tarski-Łukasiewicz's modal logic formulations, TUF_LOGIC includes modal operators: MA (Modal Assertion) evaluates whether a state is possibly true; LA (Logical Assertion) determines if a state is necessarily true; and IA (Indeterminacy Assertion) identifies explicitly uncertain states.

The UNANIMOUS operator evaluates trilean values for complete agreement, returning the consensus value if one exists or Uncertain otherwise. This function is available for both pairs of values and arrays of trilean values.

Practical Applications

TUF_LOGIC excels in financial market scenarios where decision-making must account for uncertainty. It enables technical indicator consensus by combining signals with different confidence levels, supports multi-timeframe analysis by reconciling potentially contradictory signals, enhances risk management by explicitly modeling uncertainty, and handles partial information systems where some data sources may be unreliable.

By providing a mathematically sound framework for reasoning about uncertainty, TUF_LOGIC elevates trading system design beyond simplistic binary logic, allowing for more sophisticated decision-making that better reflects real-world market complexity.

Library "TUF_LOGIC"

Three-Value Logic (TUF: True, Uncertain, False) implementation for Pine Script.

This library provides a comprehensive set of logical operations supporting trilean logic systems,

including Kleene, Łukasiewicz, and RM3 implications. Compatible with Pine v6 enums.

method validate(self)

Ensures a valid trilean integer value by clamping to the appropriate range .

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The integer value to validate.

Returns: An integer value guaranteed to be within the valid trilean range.

method to_trilean(self)

Converts an integer value to a Trilean enum value.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The integer to convert (typically -1, 0, or 1).

Returns: A Trilean enum value: True (1), Uncertain (0), or False (-1).

method to_int(self)

Converts a Trilean enum value to its corresponding integer representation.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The Trilean enum value to convert.

Returns: Integer value: 1 (True), 0 (Uncertain), or -1 (False).

method NOT(self)

Negates a trilean integer value (NOT operation).

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The integer value to negate.

Returns: Negated integer value: 1 -> -1, 0 -> 0, -1 -> 1.

method NOT(self)

Negates a Trilean enum value (NOT operation).

Namespace types: series Trilean

Parameters:

self (series Trilean) : The Trilean enum value to negate.

Returns: Negated Trilean: True -> False, Uncertain -> Uncertain, False -> True.

method AND(self, comparator)

Logical AND operation for trilean integer values.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The first integer value.

comparator (int) : The second integer value to compare with.

Returns: Integer result of the AND operation (minimum value).

method AND(self, comparator)

Logical AND operation for Trilean enum values following three-valued logic.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The first Trilean enum value.

comparator (series Trilean) : The second Trilean enum value to compare with.

Returns: Trilean result of the AND operation.

method OR(self, comparator)

Logical OR operation for trilean integer values.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The first integer value.

comparator (int) : The second integer value to compare with.

Returns: Integer result of the OR operation (maximum value).

method OR(self, comparator)

Logical OR operation for Trilean enum values following three-valued logic.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The first Trilean enum value.

comparator (series Trilean) : The second Trilean enum value to compare with.

Returns: Trilean result of the OR operation.

method EQUALITY(self, comparator)

Logical EQUALITY operation for trilean integer values.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The first integer value.

comparator (int) : The second integer value to compare with.

Returns: Integer representation (1/-1) indicating if values are equal.

method EQUALITY(self, comparator)

Logical EQUALITY operation for Trilean enum values.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The first Trilean enum value.

comparator (series Trilean) : The second Trilean enum value to compare with.

Returns: Trilean.True if both values are equal, Trilean.False otherwise.

method XOR(self, comparator)

Logical XOR (Exclusive OR) operation for trilean integer values.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The first integer value.

comparator (int) : The second integer value to compare with.

Returns: Integer result of the XOR operation.

method XOR(self, comparator)

Logical XOR (Exclusive OR) operation for Trilean enum values.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The first Trilean enum value.

comparator (series Trilean) : The second Trilean enum value to compare with.

Returns: Trilean result of the XOR operation.

method IMP_K(self, comparator)

Material implication using Kleene's logic for trilean integer values.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The antecedent integer value.

comparator (int) : The consequent integer value.

Returns: Integer result of Kleene's implication operation.

method IMP_K(self, comparator)

Material implication using Kleene's logic for Trilean enum values.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The antecedent Trilean enum value.

comparator (series Trilean) : The consequent Trilean enum value.

Returns: Trilean result of Kleene's implication operation.

method IMP_L(self, comparator)

Logical implication using Łukasiewicz's logic for trilean integer values.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The antecedent integer value.

comparator (int) : The consequent integer value.

Returns: Integer result of Łukasiewicz's implication operation.

method IMP_L(self, comparator)

Logical implication using Łukasiewicz's logic for Trilean enum values.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The antecedent Trilean enum value.

comparator (series Trilean) : The consequent Trilean enum value.

Returns: Trilean result of Łukasiewicz's implication operation.

method IMP_RM3(self, comparator)

Logical implication using RM3 logic for trilean integer values.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The antecedent integer value.

comparator (int) : The consequent integer value.

Returns: Integer result of the RM3 implication operation.

method IMP_RM3(self, comparator)

Logical implication using RM3 logic for Trilean enum values.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The antecedent Trilean enum value.

comparator (series Trilean) : The consequent Trilean enum value.

Returns: Trilean result of the RM3 implication operation.

method MA(self)

Modal Assertion (MA) operation for trilean integer values.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The integer value to evaluate.

Returns: 1 if the value is 1 or 0, -1 if the value is -1.

method MA(self)

Modal Assertion (MA) operation for Trilean enum values.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The Trilean enum value to evaluate.

Returns: Trilean.True if value is True or Uncertain, Trilean.False if value is False.

method LA(self)

Logical Assertion (LA) operation for trilean integer values.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The integer value to evaluate.

Returns: 1 if the value is 1, -1 otherwise.

method LA(self)

Logical Assertion (LA) operation for Trilean enum values.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The Trilean enum value to evaluate.

Returns: Trilean.True if value is True, Trilean.False otherwise.

method IA(self)

Indeterminacy Assertion (IA) operation for trilean integer values.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The integer value to evaluate.

Returns: 1 if the value is 0, -1 otherwise.

method IA(self)

Indeterminacy Assertion (IA) operation for Trilean enum values.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The Trilean enum value to evaluate.

Returns: Trilean.True if value is Uncertain, Trilean.False otherwise.

method UNANIMOUS(self, comparator)

Evaluates the unanimity between two trilean integer values.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The first integer value.

comparator (int) : The second integer value.

Returns: Integer value of self if both values are equal, 0 (Uncertain) otherwise.

method UNANIMOUS(self, comparator)

Evaluates the unanimity between two Trilean enum values.

Namespace types: series Trilean

Parameters:

self (series Trilean) : The first Trilean enum value.

comparator (series Trilean) : The second Trilean enum value.

Returns: Value of self if both values are equal, Trilean.Uncertain otherwise.

method UNANIMOUS(self)

Evaluates the unanimity among an array of trilean integer values.

Namespace types: array

Parameters:

self (array) : The array of integer values.

Returns: First value if all values are identical, 0 (Uncertain) otherwise.

method UNANIMOUS(self)

Evaluates the unanimity among an array of Trilean enum values.

Namespace types: array

Parameters:

self (array) : The array of Trilean enum values.

Returns: First value if all values are identical, Trilean.Uncertain otherwise.

UtilLibrary "Util"

defines commonly used utility functions and constants

calc_shares(entry_price, stop, fund, riskPerc)

Calculate number of shares for a trade

Parameters:

entry_price (float)

stop (float) : stop loss price

fund (float) : amount of fund to put in this trade

riskPerc (float) : percentage of fund to be risked in this trade. Default is 5%

Returns: number of shares

trade_exist(trade_id)

Returns if a trade with the specific ID is already open

Parameters:

trade_id (string)

Returns: true/false

trade

Fields:

id (series string)

direction (series TradeDir)

entry_price (series float)

shares (series float)

bars_open (series int)

Cometreon_Public📚 Cometreon Public Library – Advanced Functions for Pine Script

This library contains advanced functions used in my public indicators on TradingView. The goal is to make the code more modular and efficient, allowing users to call pre-built functions for complex calculations without rewriting them from scratch.

🔹 Currently Available Functions:

1️⃣ Moving Average Function – Provides multiple types of moving averages to choose from, including:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

2️⃣ Custom RSI – Uses the Moving Average function to modify the calculation method, with an additional option for a dynamic version.

3️⃣ Custom MACD – Uses the Moving Average function to modify the calculation method, with an additional option for a dynamic version.

4️⃣ Custom Alligator – Uses the Moving Average function to modify generic calculations, allowing users to change the calculation method.

CapitalManagementLibrary "CapitalManagement"

TODO: Manage the capital

order_volume(percent_risk, order_entry_price, stop_loss_price)

: Function to calculate order volume according to give risk percent_risk

Parameters:

percent_risk (float)

order_entry_price (float)

stop_loss_price (float)

calculate_takeprofit_price(entry_price, stop_loss_price, risk_reward)

: Function to calculate take profit price according to given risk:reward ratio

Parameters:

entry_price (float)

stop_loss_price (float)

risk_reward (float)

Returns: Return take profit value according to given risk:reward ratio

capital_managementLibrary "capital_management"

TODO: add library description here

Volume_calculation(precent_risk, order_entry_price, stop_loss_price)

TODO: Volume calculation function by placing orders with fiven % risk

Parameters:

precent_risk (float)

order_entry_price (float)

stop_loss_price (float)

Returns: stop_loss_price: Price that place stop loss order

KalmanfilterLibrary "Kalmanfilter"

A sophisticated Kalman Filter implementation for financial time series analysis

@author Rocky-Studio

@version 1.0

initialize(initial_value, process_noise, measurement_noise)

Initializes Kalman Filter parameters

Parameters:

initial_value (float) : (float) The initial state estimate

process_noise (float) : (float) The process noise coefficient (Q)

measurement_noise (float) : (float) The measurement noise coefficient (R)

Returns: A tuple containing

update(prev_state, prev_covariance, measurement, process_noise, measurement_noise)

Update Kalman Filter state

Parameters:

prev_state (float)

prev_covariance (float)

measurement (float)

process_noise (float)

measurement_noise (float)

calculate_measurement_noise(price_series, length)

Adaptive measurement noise calculation

Parameters:

price_series (array)

length (int)

calculate_measurement_noise_simple(price_series)

Parameters:

price_series (array)

update_trading(prev_state, prev_velocity, prev_covariance, measurement, volatility_window)

Enhanced trading update with velocity

Parameters:

prev_state (float)

prev_velocity (float)

prev_covariance (float)

measurement (float)

volatility_window (int)

model4_update(prev_mean, prev_speed, prev_covariance, price, process_noise, measurement_noise)

Kalman Filter Model 4 implementation (Benhamou 2018)

Parameters:

prev_mean (float)

prev_speed (float)

prev_covariance (array)

price (float)

process_noise (array)

measurement_noise (float)

model4_initialize(initial_price)

Initialize Model 4 parameters

Parameters:

initial_price (float)

model4_default_process_noise()

Create default process noise matrix for Model 4

model4_calculate_measurement_noise(price_series, length)

Adaptive measurement noise calculation for Model 4

Parameters:

price_series (array)

length (int)

lib_statemachine_modifiedLibrary "lib_statemachine_modified"

Modified to fix bugs and create getState and priorState methods.

method step(this, before, after, condition)

Namespace types: StateMachine

Parameters:

this (StateMachine)

before (int) : (int): Current state before transition

after (int) : (int): State to transition to

condition (bool) : (bool): Condition to trigger the transition

Returns: (bool): True if the state changed, else False

method step(this, after, condition)

Namespace types: StateMachine

Parameters:

this (StateMachine)

after (int) : (int): State to transition to

condition (bool) : (bool): Condition to trigger the transition

Returns: (bool): True if the state changed, else False

method currentState(this)

Namespace types: StateMachine

Parameters:

this (StateMachine)

method previousState(this)

Namespace types: StateMachine

Parameters:

this (StateMachine)

method changed(this, within_bars)

Namespace types: StateMachine

Parameters:

this (StateMachine)

within_bars (int) : (int): Number of bars to look back for a state change

Returns: (bool): True if a state change occurred within the timeframe, else False

method reset(this, condition, min_occurrences)

Namespace types: StateMachine

Parameters:

this (StateMachine)

condition (bool) : (bool): Condition to trigger the reset

min_occurrences (int) : (int): Minimum number of times the condition must be true to reset

Returns: (bool): True if the state was reset, else False

StateMachine

Fields:

state (series int)

neutral (series int)

enabled (series bool)

reset_counter (series int)

prior_state (series int)

last_change_bar (series int)

Milvetti_Pineconnector_LibraryLibrary "Milvetti_Pineconnector_Library"

This library has methods that provide practical signal transmission for Pineconnector.Developed By Milvetti

buy(licenseId, symbol, risk, sl, tp, beTrigger, beOffset, trailTrig, trailDist, trailStep, atrTimeframe, atrTrigger, atrPeriod, atrMultiplier, atrShift, spread, accFilter, secret, comment)

Create a buy order message

Parameters:

licenseId (string) : License Id. This is a unique identifier found in the Pineconnector Licensing Dashboard.

symbol (string) : Symbol. Default is syminfo.ticker

risk (float) : Risk. Function depends on the “Volume Type” selected in the EA

sl (float) : StopLoss. Place stop-loss. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

tp (float) : TakeProfit. Place take-profit. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

beTrigger (float) : Breakeven will be activated after the position gains this number of pips. Ensure > 0

beOffset (float) : Offset from entry price. 0 means the SL will be placed exactly at entry price. 1 means 1 pip above the entry price for buy trades and 1 pip below for sell trades.

trailTrig (int) : Trailing stop-loss will be activated after a trade gains this number of pips. Default is 0(inactive)

trailDist (int) : SL will be opened at traildist after trailtrig is met, even if you do not have a SL placed.. Default is 0(inactive)

trailStep (int) : Moves trailing stop-loss once price moves to favourable by a specified number of pips. Default is 0(inactive)

atrTimeframe (string) : ATR Trailing Stop will be based on the specified timeframe in minutes and will only update once per bar close. Default is Timeframe.Period

atrTrigger (float) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default is 0(inactive)

atrPeriod (int) : ATR averaging period. Default is 0

atrMultiplier (float) : Multiple of ATR to utilise in the new SL computation. Default is 1

atrShift (float) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default is 0

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips. Default is 0(inactive)

accFilter (float) : Enter the position only if the account requirement is met. Default is 0(inactive)

secret (string)

comment (string) : Comment. Add a string into the order’s comment section. Default is "Symbol+Timeframe"

sell(licenseId, symbol, risk, sl, tp, beTrigger, beOffset, trailTrig, trailDist, trailStep, atrTimeframe, atrTrigger, atrPeriod, atrMultiplier, atrShift, spread, accFilter, secret, comment)

Create a buy order message

Parameters:

licenseId (string) : License Id. This is a unique identifier found in the Pineconnector Licensing Dashboard.

symbol (string) : Symbol. Default is syminfo.ticker

risk (float) : Risk. Function depends on the “Volume Type” selected in the EA

sl (float) : StopLoss. Place stop-loss. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

tp (float) : TakeProfit. Place take-profit. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

beTrigger (float) : Breakeven will be activated after the position gains this number of pips. Ensure > 0

beOffset (float) : Offset from entry price. 0 means the SL will be placed exactly at entry price. 1 means 1 pip above the entry price for buy trades and 1 pip below for sell trades.

trailTrig (int) : Trailing stop-loss will be activated after a trade gains this number of pips. Default is 0(inactive)

trailDist (int) : SL will be opened at traildist after trailtrig is met, even if you do not have a SL placed.. Default is 0(inactive)

trailStep (int) : Moves trailing stop-loss once price moves to favourable by a specified number of pips. Default is 0(inactive)

atrTimeframe (string) : ATR Trailing Stop will be based on the specified timeframe in minutes and will only update once per bar close. Default is Timeframe.Period

atrTrigger (float) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default is 0(inactive)

atrPeriod (int) : ATR averaging period. Default is 0

atrMultiplier (float) : Multiple of ATR to utilise in the new SL computation. Default is 1

atrShift (float) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default is 0