EMA+RSI Pump & Drop Swing Sniper (SL+TP) - StrategyThis is the strategy version of the 'EMA-RSI-Pump-Drop-Swing-Sniper-With-Alerts':

Some additions with this strategy:

~Added Stop loss & Take profit control. In Settings > Inputs if the Stop Loss is at .051 that means it's 5.1% and the Take Profit at .096 is 9.6%. If you wish to remove the TP and SL just change the value to 1.00 and it would be the same as it being 100% TP and SL which is likely to never be hit.

~Added Backtesting by changing the month/date/year in Settings > Inputs

~Added a 2nd EMA line to assist with the long entry signals. I only use this for long entry & exits, though you could use the long exits as Short entries too. I just personally don't do short trading on Bitcoin.

This is using an EMA and RSI with slightly modified settings to give good entry and exit points while looking at Bitcoin. I use this on a 1-hour and 4-hour chart and with other indicators to find good positions to enter a trade or exit if things are turning red.

It's important to know this strategy was made as a request by another user that was using the indicator version. I don't use this as a trading strategy by itself, I use the visuals it gives as a confirmation with other indicators to find the best possible entry and exit positions.

If you click on the EMA line it will color the bars of the chart based on if they are above or below the EMA - This is just visually helpful for me to see the active trend.

Make sure you hover over or click on the EMA line to see the colors of the candles change - it's not visible by default or without doing this.

Strategy!

MACD/RVSI/Stoch/RSI/EXP(Drawdown)I have been trying for several months to get a script to work on the 1min and this one gives some good backtest results. This script will also work on higher timeframes however, I've not extensively tested on higher timeframes. My aim was to get results on about 20 crypto coins then run the 1min bots in parallel looking for small frequent profits across all the coins. If you would like me to try and fit backtest results to any coin or pair on any timeframe please do get in touch anytime.

It's based on several indicators which are combined and then a newish way for the stop loss to implement based on an exponential rising which limits the time in each trade unless the price moves in the direction of the trade. The other useful feature is drawdown minimization which previously made all of my 1minute bot attempts non-practical due to differences between backtesting and actually running the bot(s) live.

Its possible at the top to paste in strategy comments which can be used through web-hooks for auto trading bots. Leaving these blank just defaults to the pre-programmed comments that provide some indication of why a trade was exited.

It is possible to select for Short and/or Long trades. Note however, that there are exponential markers on the charts for both long and short trades in any setting. I found that this way the bot worked well with regards to timing.

The next part of the user interface settings gets a bit tricky so try and use the sample parameters provided below. For example, select a crypto coin then try some of the options below until a reasonable backtest result in obtained (or select the best from the parameter groups tested) then move down the settings interface to optimise with the remaining settings.

So 'Use MACD/RVSI', 'RSI clause' and 'Use Stochastic' are set to true for the below sample settings (1min timeframe).

MACD/RVSI Confluence Resolution (1min, 2min, 5min, 10min, 1hour)

Timeframe RSI (1min, 2min, 3min, 15min, 1hour)

FastStoch, SlowStoch (1min, 45min: 5min, 30min: 1min, 1hour: 5min, 1hour)

Eg. for FTX:ETHPERP (MACD/RVSI Confluence Resolution=1hour, Timeframe RSI= 1min, FastStoch = 1min, SlowStoch = 45min)

Setting the timings is tricky - there is a lot going on. Have a look at the chart and select/deselect the options. The MACD/RVSI Confluence Resolution shows red and green vertical regions on the chart background. The Timeframe RSI colors the candle bodies red and green. These go green if the RSI crossed over 31% or red in the RSI crossed under 69%. The MACD/RVSI Confluence Resolution is explained in more detail in one of my other scripts. Then the Slow Stoch colors above and below the price action with red or green lines depending if on an uptrend or downtrend (approximately). Where there is also an up/down trend on the faster timeframe stoch there are vertical shaded fill regions between the slow stop above/below lines.

With all the above conditions selected to represent the data (looking at strategy backtest results whilst adjusting) there is a reasonable approximation to a credible trade.

So once an ok backtest result is obtained by selecting timing settings. Its ontot the Stop Ramp Settings. This is an exponential line which rises rapidly after a period of time thus exiting the trade or going upwards with the trade. It kind of limits the maximum time a trade will stay in position which forms part of the timing aspect of this bot. Look at the chart exponential red lines and adjust the settings, along with the backtest results to select a good timing.

Then its the Drawdown Catcher and the Take Profit Setting. Start with the drawdown catcher disabled i.e. set to zero. Put in a conservative Take Profit, for example if a Take Profit at 6% gives the best backtest results, go for 4% to account for differences between backtest results and actual live bot performance.

Then start to increase the Drawdown Catcher. This shades a lime region where the bot will not enter a trade. I found that with most trades using this bot, if the price action moved in the direction of the trade (long or short) at the onset - this gave most of the good results (high probability of positive trade). Also if a trade entered at the start price and when south, the accumilated drawdown from these failing trades made all previous 1min bot attempt non=profitable in practice (even with good backtest results). The exp timing and also this drawdown reduction strategies seem to be the thing which makes this approach credible.

Try to go for settings that give a very high change of positive trade. For example, an 85% profitable trades will probably provide say 55% positive trades in practice as its always highly possible to just fit the parameters to the exact position/trade timings - and in reality going forwards these don't play out the same. Also a Profit Factor of 2 is about the minimum I would accept - again this provides for example a Profit Factor of 1.2 in practive.

However all being said - I think its possible with this bot on the 1min across lots of coins - with regularly updating settings - to make profits. (Not financial advice)

Please do get in touch if you would like me to fit this bot to anytimeframe to any trade.

MoonFlag PhD

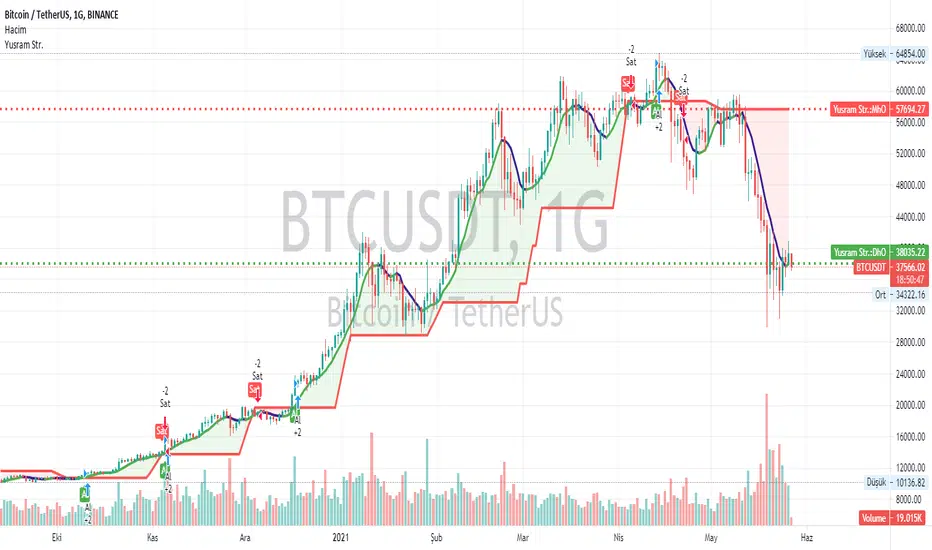

Yusram Mount MaV - Day MaV CrossOver Strgty

This indicator shows the comparison between the 7-day fast simple average and the monthly slow average of 5 bars. The red line indicates the monthly green and blue lines the daily average. If the Green-Blue line crosses the red upwards, it is a buy signal and the opposite is a sell signal. As soon as it turns green blue without waiting for the sell signal, a sell signal is created. If you are trading fast, you can consider turning green to blue as an opportunity. In the long run, the red intersection can be interpreted as a Stop point.

I hope it will be useful to everyone.

You can also find the strategy indicator with the same name.

I got the name of this indicator from my daughter's name. The meaning of the name Yüsra means "convenience". I hope this indicator will help you.Yüsram Mount HO - Day HO

Intrangle - Straddle / StrangleIntrangle is an indicator to assist Nifty / Bank Nifty Option Writers / Sellers to identify the PE / CE legs to Sell for Straddle and Strangle positions for Intraday.

Basic Idea : (My Conclusion for making this Indicator)

1) Last 10 Years data says Nifty / Bank Nifty More than 66% of times Index are sideways or rangebound (within 1% day) .

2) Mostly, First one hour high and low working as good support and resistance.

Once First one hour complete, this indicator will show Strangle High (CE), Strangle Low (PE) and Straddle (CE/PE).

Straddle:

If you want to do straddle strategy, sell at the money strike (CE/PE) when price comes near to the straddle line (black line),

Strangle:

If you want to do Strangle strategy, sell Strangle High (CE) and Strangle Low (PE) when price comes near to the straddle line (black line). Both Strangle High and Low will be out of the money when price near to the straddle line (black line).

Adjustment: option adjustment to be done based on the price movement. Adjustment purely up to the user / trader.

Note1: If price not comes to near straddle line after first hour, better to stay light…

Note2: If first hour not giving wide High / Low, don’t use strangle strike based on this indicator. Straddle can be done any day with require adjustment / hedge. This Indicator is purely for education purpose, user / trader has to be back-tested before their start using it.

This indicator will work in Nifty / Bank Nifty only. Best Time frames are 3/5/15 Mins. This is purely made for Intraday

Happy Trading 😊

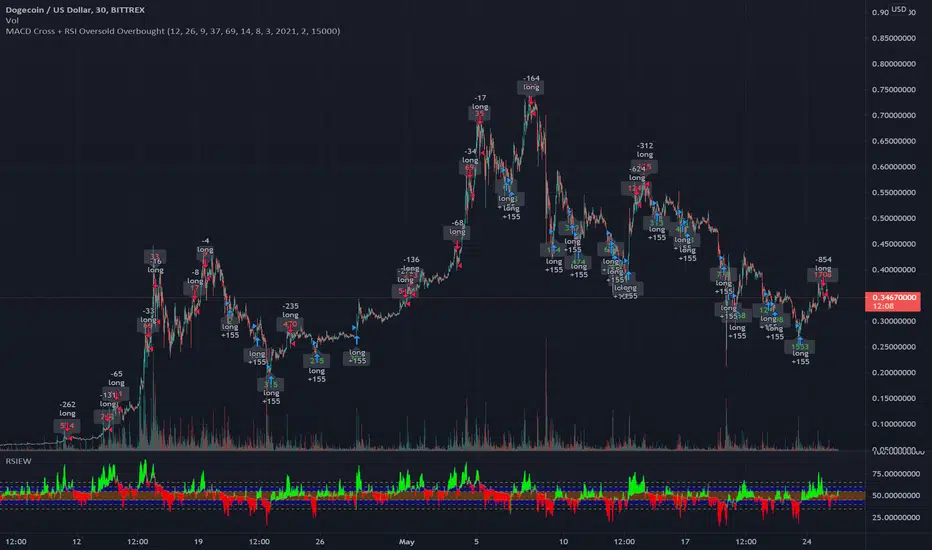

MACD Signal with RSI Indicating StrategyThis strategy looks for MACD signal crossover and RSI confirmation of oversold/overbought condition.

Tune to your crypto/stock for best results using the strategy and sent an alert. Currently set up to use 25% of equity at each buy signal and will sell 1/3 of position at each sell signal. Initial investment is $1000, but adjust as necessary.

Currently tuned to DOGEUSD on 30min chart.

If you like/use/profit, follow me or shoot me a donation. If you are looking for a script design, I can help.

SignalCAVE Strategy BuilderYou can create strategies without writing single line of Pine Script code!

Do backtesting, set alerts and explore algorithmic trading with using SignalCAVE Strategy Builder on TradingView.

SignalCAVE Strategy Builder for TradingView

SignalCAVE is a tool that help you to create strategies in TradingView. SignalCAVE offers flexible strategy builder panel enabling users to backtest and set alerts with custom conditions (selected indicators and parameters).

CAPABILITIES

You can define rules and conditions for “Long” and “Short” signals.

“Stop Loss” or “Take Profit” functions can be activated with providing percentage values.

“Only Long”, “Only Short” or both “Long and Short” signals can be used at the same time.

Available Indicators

EMA, SMA, WMA, HMA, RSI, MACD, Stochastic, Bollinger Bands, SuperTrend, Parabolic SAR, DMI, ATR, CCI, CMF, ROC, Ichimoku, OHLC Prices

How to Set Strategy Rules?

On SignalCAVE strategy settings screen, there are four types of input groups. You can populate these input boxes based on your strategy.

A: First indicator’s parameter and index value selection area

First Input: First indicator selection.

Second Input: First indicator’s parameter selection. If you want to use default parameters, select “Default Parameters”. If you want to use custom parameters, select “Custom Parameters”. If your selection was custom, then you need to fill “P:A” input boxes to assign your custom parameter.

Third Input: First indicator’s index selection. Default parameter is “0”, If you want to get previous value of indicator/price, you can type positive numbers.

?: Condition and Interval selection area.

You can select “Upper (>), Lower (<), Upper or Equal (>=), Lower or Equal (<=), CrossOver (⬆), CrossUnder (⬇)” conditions and time frame interval for calculation both first (A:) and second (B:) indicator.

B: Second indicator’s parameter and index value selection area

First Input: Second indicator selection.

Second Input: Second indicator’s parameter selection. You may use either default parameters, or custom parameters. If your selection was custom, then you need to fill “P:B” input boxes to assign your custom parameter.

Third Input: Second indicator’s index selection. Default parameter is “0”, If you want to get previous values of indicator/price, you can type positive numbers.

P:A First indicator’s custom parameter settings. If selected indicator has less then four parameters, you can fill unnecessary fields with “0” value.

P:B Second indicator’s custom parameter settings. If selected indicator has less then four parameters, you can fill unnecessary fields with “0” value.

DASHBOARD

After you build the strategy with SignalCAVE, you can see rules and conditions on dashboard with chart view screen.

Hint: By adding multiple times of SignalCAVE strategy on your chart screen, you can build more then one strategy.

STRATEGY TESTER / BACKTEST RESULTS

You can see strategy backtest results from “Strategy Tester” panel.

By changing parameters or strategy rules (strategy optimization), you may get better results. These results does not guarantee a success for future trades.

ALERT SETTINGS

If you want to get notify about your strategy outputs (Long Entry, Long Exit, Short Entry, Short Exit, Stop, Take Profit) you can set an “Alert”.

You can click “Alert” button to create a new alert. Make sure on “Conditions” selection must be “SignalCAVE” strategy.

Paste to “Message” field exactly the text below.

{{strategy.order.alert_message}}

Hint: By setting a single alarm, you can get notifications for all outputs.

Do your alerts modifies when you change the strategy conditions or parameters?

While the strategy got updated, its alerts still use the strategy’s state from the time when we made the alert (TradingView Wiki, 2018b).

This has the advantage that, once we made a script alert, we can change the script’s input options, change chart settings, or remove the script from to the chart. All of that won’t affect our existing alert. That gives a lot of flexibility to keep interacting with the chart and script.

But there’s also a disadvantage: if we do want our script’s alerts to change, we first need to remove the existing alerts. Then we have to create and configure new alerts based on the indicator’s updated code or settings.

Triple EMA Cross with Pivot PointsYou can change various options from the settings, a few things to bear in mind:

Always make sure the EMA timeframe is larger than the chart timeframe for it to be usable.

The timeframe for Pivot Points is still playing up so I'll be looking into that soon!

This indicator doesn't always work, use it in conjunction with other indicators to manage your risk

Trading Strategy

TEMA 2 & 16 Cross

Long Entry

TEMA cross & Higher Low

Close Long

TEMA cross

Short Entry

TEMA cross and Lower High

Close Short

TEMA cross

MACD Trendprediction Strategy V1A trend following indicator based on the MACD and EMA. In this case, signals are not generated by crossing the signal lines as with the MACD, but as soon as the distance between the signal lines increases or decreases. A profit factor of 1.6-3.5 is achieved.

Ein Trendfolge-Indikator, auf der Basis des MACD und EMA. Dabei werden Signale nicht wie bei dem MACD per Kreuzung der Signallinien generiert, sondern sobald ein der Abstand der Signallinien zu oder abnimmt.

MATR 4H Strategy - UpTradingEN // MATR 4H Strategy - UpTradin

Use 1:

This script is effective for all assets. Find out how to get the best performance. This indicator offers several possibilities:

- Only in TimeFrame 4H.

- The gray curve shows you the trend. You should not trade against it.

- Once the trend is established you can buy or sell according to the Buy and Sell sign.

- When the orange point (warning) appears you must remain attentive to a continuation of the movement or a reversal.

Use 2:

You can program limit orders using the green or red stripe. These are two bands that anticipate the high or low point of the price.

Legend:

- The gray line is an Ema 20 based on a Daily TimeFrame.

- The orange point means a continuation or a reversal.

- Buy means a buy zone.

- Sell means a sales area.

- The green curve allows you to program a limit order to buy.

- The red curve allows you to program a limited order to sell.

Operation:

This script works from an ATR programmable according to your needs and correlated according to an Ema. It also shows you the trend in a single one thanks to an Ema 20 based on Daily data.

FR // MATR 4H Strategy - UpTrading

Utilisation 1 :

Ce script est efficace pour la totalité des actifs. Découvrez comment obtenir le fonctionnement idéal. Cet indicateur offre plusieurs possibilités :

- Uniquement en TimeFrame 4H.

- La courbe grise vous indique la tendance. Il ne faut pas trader contre celle-ci.

- Une fois la tendance établie vous pouvez acheter ou vendre selon le signe Buy et Sell.

- Lorsque le point orange (warning) apparaît vous devez rester attentif à une continuation du mouvement ou d’un retournement.

Utilisation 2 :

Vous pouvez programmer des ordres limites grâce à la bande verte ou rouge. Il s’agit de deux bandes qui anticipent le point haut ou bas du prix.

Légende:

- La courbe grisée est une Ema 20 basée sur un TimeFrame Daily.

- Le point orange signifie une continuation ou un retournement.

- Buy signifie une zone d’achat.

- Sell signifie une zone de vente.

- La courbe verte vous permet de programmer un ordre limite à l’achat.

- La courbe rouge vous permet de programmer un ordre limité à la vente.

Fonctionnement:

Ce script fonctionne à partir d’un ATR programmable suivant vos besoins et corrélé suivant une Ema. Il vous indique également en une seule la tendance grâce à une Ema 20 basée sur des données en Daily.

Dankland Playground Moneymaker - V2“version 2” of my playground bot script. Its essentially a powerhouse suite of strategies. Although it is similar to the previous script, it nets different results as sections have been changed. Such as the somewhat reluctant removal of the Chande Momentum... The RSIs have also been updated, this was one of the main changes. RSIS now include a Moving Average cross of RSI to generate signals above and below the given thresholds instead of simply on crossing a threshold. This should give greater functionality overall. Most functions including Moving Averages have been updated to include a wider range of kinds of moving averages. This includes not just the moving average cross, but MACD and RSIs as well. I tried to perform the same upgrade on the %B, Stochastics and SMI, but hit the unpacked code limit of 60,000 lines... So, more “versions” will have to come for future “upgrades”, with the recognition that there will be cases where the old, “downgraded” versions may perform better and that some people (like myself) may continue to use them on some markets until I/we devise superior settings on the new ones for said markets. For instance, instead of replacing my 1 hr BTCUSD bot (where I used the now deleted Chande to pretty pleasing affect...) I made a new one for LINKUSD 10 min so I can have both running for now and work on replacing the BTCUSD later.

How it works basically is this... you have 16 oscillators which can all be used as independently as you wish. They can be split up into different groups or ran all together.

When in separate groups they should not be able to sell eachothers positions without triggering a full stop loss by turning the Independence/Stop All switches on. Every single oscillator has its own entry and exit position sizing which can be stated as either a percent of balance or a flat amount of contracts (or both combined). Each oscillator has a minimum amount of profit you can tell it to sell it, which is calculated from the average cost of your current position, which does include all groups. This works out to help you average out better entry and exit prices, essentially a method of DCAing.

You can set the minimum sale amount, which is to keep it from placing orders below your exchanges minimum dollar trade cost.

All this functionality combined also ensures more accurate back tests by ensuring that the script simply cannot spend money it doesn't see as in the balance, whereas other scripts will use a percentage of equity, and once 100% of your equity is in BTC for instance, it will keep buying more BTC for free and thus spoof up backtest numbers. If you look through the strategies here, many people claim to have amazing scripts and then you look into it and this is happening and skewing their numbers. These people are either very ignorant or what they made or scam artists and trolls in my opinion.

This version also includes On Bar Close switches for each oscillator. When switched on, signals are only allowed to generate on Bar Close. This helps to prevent retriggering from live signals, which when you are running this many oscillators, will become a problem! However, in most cases, you do not need to generate signals intrabar, as backtests will show, ignoring intrabar buys and sells (intrabar stop losses can still be very important though!) won't exactly keep you from high profitability strategies, but rather, allowing elements of chaos from live indicators moving up and down intrabar will, in fact, drift your actual results further and further from the backtest. You want an accurate backtest though. So choose wisely when you turn these off and you will do better.

The included oscillators are as follows:

NO MORE Chande Momentum cross – REMOVED – I was hitting PINE code limits here so I had to make choices and this one simply had to go. Begone!

Moving Average Cross

MACD cross

%B Bollinger cross

Stochastic cross + region filter

Stochastic RSI cross + region filter

SMII cross and region filter

Three RMIs

Know-Sure-Thing line-cross

Coppock Curve line-cross

TRIX line-cross

RSI of MA w/ MA cross

RSI of MA of KST w/ MA cross

RSI of MA of Coppock Curve w/ MA cross

RSI of MA of Trix w/ MA cross

So the idea is that this is essentially multiple strategies combined into one backtestable house. Balance is calculated for all position sizes in order to try to prevent false entries that plague so many scripts (IE, you set pyramiding to 2, each buy $1000, initial balance $1000, and yet it buys two orders off the bat for $2000 total and nets 400% profit because the second was considered free, happens on 90+% of scripts on Tradingview if you aren't very very careful!)

You tune each indicator and position size them so that they work together as well as you can and in doing so you are able to create a single backtest that is capable of running a bot, essentially, between multiple strategies - you can run a slower Moving Average cross, a faster SMI cross or MACD , or Bollinger that grabs big moves only, all the while having MACD trade small bonuses along the way. This way you can weight the Risk to Reward of each against eachother.

I will not try to claim this is something you can open and with no work have the best bot on the planet. This scripts intention is to take a lot of relatively common trading strategies and combine them under on roof with some risk management and the ability to weigh each against eachother.

If you are looking for a super advanced singular algorithm that tries to capture every peak and valley exactly on the dot, this is not for you. If you are looking for a tool with a high level of customizability, with a publisher who intends to update it to the best of his ability in accordance to seeking to make the best product that I personally can make for both myself and the community (because I will be using this myself of course!) that was specifically designed with the intention of performing well in spot markets by averaging low entry costs and high exit costs, this is for you! That is the exact intention here. It can certainly work with margin, but you will have to take extra care in setting your stop losses. I intend to make a version capable of going short which will be included as part of the package. It may take some work to keep all of the risk management working as well for shorts though. There will be more scripts added to the “package” as I hit the limit on this one a few times and have had to keep some ideas out already.

The current backtest shown is hand-optimized by myself for Link /USD 10min market (Binance US – shouldn't need much work to fit to other exchange markets) with multiple stop losses.

Bear & Bull Zone Signal StrategySince I love to mix and match, here is something fresh and that actually works on the breakout of Ethereum without losing your ass on lagging indicators.

It blends some of the nice parts of my previous scripts while moving to big boy pants with a twist on the Fibonacci retracement using SMA and EMA at multiple levels to do a sanity check.

Is it too good to be true? Nope, just what happens when a Solution Architect starts messing around with crypto and applies engineering and mathematics to the mix. You get a strategy that really doesn't have high profit losses when you tweak it just the right way.

What's the right tweak you ask?

1. Start with a 30 minute timeframe and set your window start date to the date the market began the bear or bull run

2. Make sure you can see your strategy performance window (not the graph one)

3. Set Stop Loss and Target Profit to 50%

4. Use your mouse wheel or up and down arrows and mess around with the RSI, go down one at a time but no lower than 7. Whichever value displayed the highest long or short gain is the one to pick.

5. Now select long or short only based on whichever one shows the highest gain.

6. Now go to K and D, leave K as 3 and check what happens when D is 4 or 5. Leave D at the value that gives you the highest gain.

7. Now go to EMA Fast and Slow Lengths. Leave Fast at 5 and check what happens when the Slow is moved up to 11 or 12, do the gains go up. If not, check what happens when Slow is moved down to 9, 8, or 7. Whichever gives you the highest gain, leave it there. Now go mess with the fast length, keep in mind that fast must always be less than slow. So check values down to 3 and up to 6. Same concept, mo money...leave it be.

8. Now go mess with the Target Profit, I start at 5, hit enter, then go to 7, hit enter, then 9...up by 2 until I get to 21 to make sure I don't hastily pick a low one and always keep in mind between which values the gain switched from high to low. For example, in this example I published at 11 it was $5k and at 13 it was $3700 for the gains. So after I got up to 21 I went back to 11 and started going up by 0.01 steps until the value dropped, which was at 11.19 so I set it at 11.18.

9. Now stop loss is trickier, you've maximized the gains, which means if you set the stop loss at a low value you will sacrifice gains. Typically by this point your loss is less than 10% with this script. So, my approach is to find the value where the stop loss doesn't change what I've tweaked already. In this example, I did the same start at 5 and go up by 2 and saw that when I went to 17 it stopped changing. So I started going back down by 0.5 and saw at 15.5 the gains went lower again. Now I started going back up in steps of 0.01 and at 15.98 it went back to the high gain I already tweaked for. I kept stop loss there and unleashed the strategy on ETH.

So far so good, no bad trades and it's been behaving pretty well.

EMA Strategy - VaibhavRules are simple:

For CE only

1) Wait until the candle closes above the green line and a cross appears below the candle.

2) Enter on the next candle and keep your Sl at the previous candle low.

3) You can get multiple confirmation by add the pin bars from the settings.

Jaws Mean Reversion [Strategy]This very simple strategy is an implementation of PJ Sutherlands' Jaws Mean reversion algorithm. It simply buys when a small moving average period (e.g. 2) is below

a longer moving average period (e.g. 5) by a certain percentage and closes when the small period average crosses over the longer moving average.

If you are going to use this, you may wish to apply this to a range of investment assets using a screener for setups, as the amount signals are low. Alternatively, you may wish to tweak the settings to provide more signals.

Context can be found here:

LINK

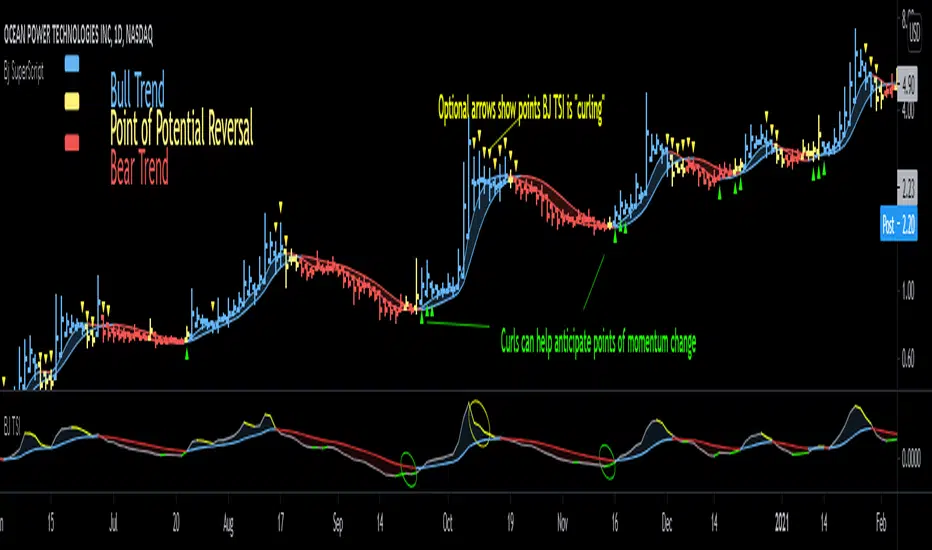

Bjorgum SuperScript

Bjorgum Reversal

Bj Reversal uses Tilson moving averages to identify trend changes

Bars change to yellow as bar close crosses the Tilson moving averages. Blue or red is confirmed as the two Tilson averages themselves cross.

Reversal is great for pinpointing trend change often giving the absolute best entry or exit

Its sensitive nature can mean more false signals on some assets

Be sure to use other indicators from the Bjorgum Collection to confirm signals, or use another strategy that fits the asset or time frame being viewed

Bjorgum HEMA Strategy

Hema uses HA smoothed EMAs to identify trend direction

Default EMA lengths are 5,9, and 21 period

Bar Color will change Malibu or Ruby on a cross of BOTH 5 and 9 EMA

The lengths are customizable to whatever lengths the user desires

Rolando Santos True Relative Movement (TRM)

This underrated momentum strategy conceptualized by Rolando Santos uses 2 indicators to give a 3 color scheme

A leading indicator (RSI) is combined with a lagging indicator (TSI) to produce bar colors based on the condition of each indicator

Both indicators in positive territory produce blue bars

Both indicators in negative bias produce yellow bars

If signals are mixed (one up one down) bars become grey

Speed Selection

The Bjorgum speed selector optimizes the strategy based on the users desires or trading style at the touch of a button

Fast setting is better for swing trades - more timely signals, more whipsaw

Slow setting is better for longer holds or more volatile assets - slower signals, smooths out whipsaw

RSI Bar Color

RSI color changes bar color based on user defined RSI values

Buy/ sell signals are typically given on a cross of the 50 level

Speed selector (fast/Slow) automatically changes lengths between Bj RSI (5 period) and a standard RSI (14 period)

Additional capabilities can be mixed and matched from strategies in the "Strategy Override" section

Add-ons include:

Tilson - The moving average system from Bjorgum Reversal can be toggled to couple with another bar color strategy by clicking this button

PSAR - Parabolic Stop and Reverse indicator can help with trend direction, volatility, and stop losses

HEMA - The 3 moving average system from the HEMA strategy can be coupled with any of the other strategies by clicking "Show HEMA"

Bj Arrows - These arrows plot at the bar level to draw attention to when the BJ TSI is "curling" (See profile for Bjorgum TSI and download today)

-Optional "Plotbar Overlay" plots bars with Heikin-Ashi Inputs when toggled

-This allows for the benefits of price smoothing without sacrificing moving average and indicator performance as real close value is still used

-This can also help on short time frames and improve results with crypto! The user must "mute" the main series candles when in use to avoid candle overlap.

-Optional price line as muting main bars will disable the TradingView default price line. The horizontal plot will track the real closing price while in HA mode!

3 EMA Stochastik RSI ATR SL TP only LONGHey there!

Here i will show you the 3 EMA RSI Stochastic Crossover strategy with an ATR SL and TP.

The strategy works as follows:

For long positions, the EMA's must be in the following order:

The 8 E M A must be above the 14 E M A and the 14 E M A must be above the 50 E M A.

The buy signal is given to us by the Stochastic RSI indicators.

The K line must cross the D line above. The following candle must then close above all E M A's.

The stop loss is determined by three times the value of the ATR.

The take profit is determined by two times the value of the ATR.

In this strategy only long positions are traded.

3x SuperTrend Strategy (Mel0nTek) V1This is a triple SuperTrend based strategy for lower time frame trades such as day trades and scalping. I have not seen many strategies that combine multiple SuperTrends so I thought I would publish this one since I put it together and have been quite happy with the results. I have found through testing that the best results are on currency exchange markets such as Crypto or Forex on 1-15 min time frames.

The core idea was inspired by a youtube video put out by Trade Pro:

"Trade Pro - HIGHEST PROFIT Triple Supertrend Trading Strategy Proven 100 Trade Results"

I went ahead and set the defaults to the ones he uses in his video for anyone who wants to try a configuration similar to his. They work pretty well in general, however the EMA, SuperTrend ATR multipliers, and P/L ratio can be tuned/optimized to fit the timeframe/market desired. The video is quite good but not a required watch as I will explain below.

The 200EMA is used as a medium-term trend direction indicator.

- Price closing consistently above the 200EMA means that only long positions should be entered.

- Price closing consistently below 200EMA means that only short positions should be entered.

The 3 SuperTrend indicators should be used as direction confirmation for entries. Typically, price above SuperTrend indicates bullish movement, while price below SuperTrend indicates Bearish movement. However by itself, it is not a great indication to enter/exit positions in my experience. By combining 3 of them with slightly longer periods and increased ATR multipliers, we can get much stronger confirmation of trend direction/strength.

The way they are used in this strategy is such that:

- We only want to enter a position if at least 2 out of 3 SuperTrends are on our side.

- 3/3 SuperTrends on our side is the best case, since we are taking trades WITH momentum/price strength.

- The second farthest SuperTrend from entry price is used as a Stop Loss

SuperTrend being on our side is not the only requirement for an entry however. The probability of success is increased with SuperTrend, and a longer EMA on our side, but we want to be sure that we aren't getting in too late/after the movement has already happened.

So we use Stoch RSI to pick our entries where price is oversold/overbought and reversing. That means the Stoch RSI is above 80, or below 20, and our indication to enter the trade is when the 2 lines cross/begin reversing direction.

So with trend direction on our side, we can get really good entries at these oversold/overbought extremes, especially as it's reversing (Stoch RSI K and D are crossing). This allows us to use the SuperTrend as a support/stop loss on our entry since price should be above it.

Then we just target 1.5x our max loss so that even if we only win 50% of the time, we still make a profit.

The explicit rules of this strategy are as follows:

=== Rules ===

long only

- price above EMA200

short only

- price below EMA200

Stop Loss = 2nd SuperTrend line above (short) or below(long) entry candle

Profit = 1.5x SL/risk (Profit Ratio x Max Loss)

=== Entry Setup ===

LONG

- Stoch RSI below 20, cross up

- at least 2 SuperTrend lines below close

SHORT

- Stoch RSI above 80, cross down

- at least 2 SuperTrend lines above close

P.S. Special thanks to Trade Pro for producing so many quality videos, putting strategy claims to the test, and providing me with so many good ideas I apply to my own strategies.

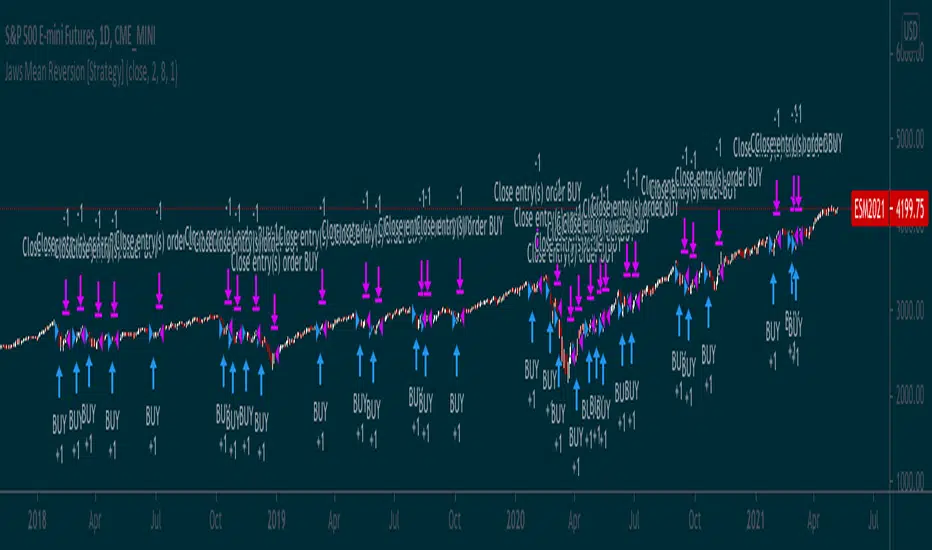

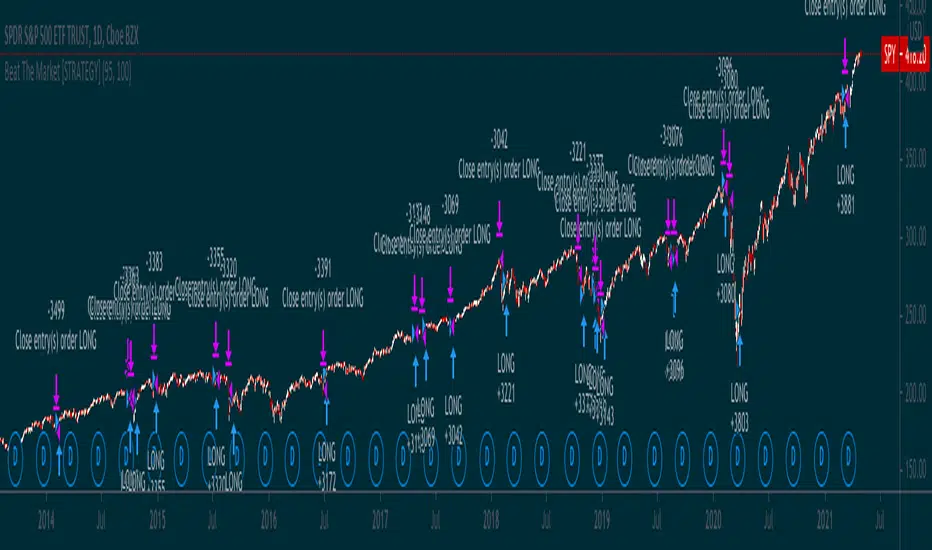

Simple way to BEAT the market [STRATEGY]This script has been created to demonstrate the effectiveness of using market regime filters in your trading strategy, and how they can improve your returns and lower your drawdowns

This strategy adds a simple filter (A historical volatility percentile filter, an implementation of which can be found on my trading profile) to a traditional buy and hold strategy of the index SPY.

Note, There are other filters that could also be added including a long-term moving average/percentile rank filter/ADX filter etc, to improve the returns further.

The filter closes our long position during periods of volatility that exceed the 95th percentile (or in the top 5% of volatile days) and buys back when the volatility is below 95% rank of the past 100 days

Have included the backtest results since 1993 which is 28 years of data at the time of writing. Comparison of traditional buy and hold with this modified strategy can be found below:

Traditional buy and hold:

Return per year: 7.95 % (ex Dividends)

Total return: 851.1 %

Max drawdown: 50.79 %

'Modified' buy and hold (this script):

Return per year: 9.92 % (ex Dividends)

Total return: 1412.2 %

Max drawdown: 31.57 %

Feel free to use some of the market filters in my trading profile to improve and refine your strategies further, or make a copy and play around with the code yourself. This is just a simple example for demo purposes.

All in One StrategyTrue improvement over my previous script. This script adds in all of the complementary indicators, makes it truly easy to adjust the inputs, and has produced a real world net gain using the TradingView bots paired with any broker's API that is supported.

It has a selection for which strategy you'd like to use and due to limitations in Pine I cannot program in logic to make sure you only pick one, so you need to make sure you are only picking one.

To tweak the Connors option - it only depends on the RSI length variable, everything else is hard coded and tweaked for Crypto.

To tweak the MACD - play around with the min and max values of the RSI for lookback and the amount of candles to lookback. Then tweak the fast and slow MA lengths. I have found that a fast length of 3 or 4 and a slow length between 6 and 10 will yield the highest gains.

Also, when I was a young Noob I thought using a chart timeframe of 5 minutes was the best...no...no it wasn't. I lost my ass. Don't lose yours. I highly suggest sticking with a 30 minute timeframe, you will minimize losses caused by false triggers, have less trades and higher profits. More is not always better, trades that may sell one day and then buy six days later are normal. Leave it do its magic and you'll be very happy in the end.

OptionsMillionaire SPY Moving Averages and Signalsby ColeJustice

OptionsMillionaire's SPY Options trading system is based mainly on these indicators:

- 8 EMA*

- 21 EMA*

- 100 SMA*

- 200 SMA*

- MACD

- RSI

- Squeeze Momentum

(*provided by this indicator)

and follows these rules:

|

| 1) I never fight the trend. If its green, i buy calls. If its red, i buy puts. I will only buy puts on a green day if there is a overall change in market trend. Inversely, calls on a red day

| 2) Price action is my #1 indicator. I wait for it to confirm my thesis before i enter a trade

| 3) I only trade SPY Options

| 4) My baseline is to choose a call/put that has a DTE (Date To Expiration) 6-7 days out, with a strike $2-$3 away. I adjust that to fit my current appetite for volatility. i virtually never play same day DTE's.

| 5) I set a 10% stop, but usually exit at 8% before my stop triggers depending on current situation

| 6) I utilize about 10-20% of my Portfolio for one trade. Sometimes more. Rarely less.

| 7) I never hold overnight in these market conditions.

| 8) I shoot for 10-20% for gains. Depending on market conditions.

| 9) Always look for confirmations in your indicators.

| 10) I never force a trade. No trade is a good trade too if the entry just isn't there.

| 11) Patience always pays off. A great set-up can form in minutes or seconds. I never regret being patient to enter. I nearly always regret rushing into a trade.

|

This indicator combines the moving averages into a single unit to simplify one part of the indicator usage rules: the 8 EMA / 21 EMA Cross. . The 8 crossing over the 21 is a Bullish signal, while the 8 crossing under the 21 is a Bearish signal. This indicator places flags at these crossover/under points, as well as shading the area between the 8 and 21 EMAs to help visualize the strength of the trend; green during a Bullish cross, and red during a Bearish cross.

A new addition to this strategy is the Hull Moving Average, or HMA. This script defaults to an HMA of 20 and shows alerts when candles close above or below the plot in the form of green and red candle backgrounds. This alert is best used in conjunction with the main crossovers and should be considered an addition level of confidence rather than providing trade entry/exits directly. This indicator is more flexible and you should feel free to adjust the period if you find a different value works better within your own personal trading style.

Each individual element of this indicator can be modified or toggled, providing maximum customization. While you should strive to become comfortable with the default settings, these options are provided in case you feel the need to adjust for your own style (or if testing on tickers other than SPY, for example).

Goodluch, and happy trading!

CRYPTO 3EMA Strategy with Take Profit & Stop Loss based on ATRSimple 3 EMA Strategy with plotted Take Profit and Stop Loss

Entry condition:

- Middle EMA cross above the Slow EMA

- Set take profit and stop loss exit conditions based on ATR Indicator

Exit condition:

- Fast EMA cross below the Middle EMA

Linear RSIThis is an attempt to create a strategy based on the previous post. The strategy, as before, is based on the RSI, which is calculated using linear regression, but with the addition of EMA. The crossing of EMA and RSI is a buy and sell signal. There are also two functions to buy (because I haven't decided which is really better), so please use checkbox to order which one you would like to use.

BNBUSD 1 Minute Chart / 1 Hour BBand Day Trading 3Commas*** As always, this is provided for educational purposes only and I am not an investment advisor; I'm just a guy who likes to come up with novel ideas and share them with other traders so they can learn. ***

This strategy is a fun one. I took parts of 'Bollinger Awesome Alert R1 by JustUncleL' () and modified it to have enhanced day trading functionality. This version does not show source and that is by design - I want the alerts to be visible to the public and if you want to get set up with a version that integrates with 3commas, drop me a message - there's a lot more that goes into setting up automated 3commas trading but this script was written specifically with 3commas in mind.

It's possible this is one of the more interesting strategy indicators I've made. The setup I used for this is as such and you will need to set it up the same way:

One minute chart for the BNB/USD(T) pair on Binance.us (other exchanges will likely work, other coin pairs or other time frames will likely not)

This script watches the one minute chart and when price golden crosses the lower Bollinger band, a buy order is placed.

There are two sell conditions; one I set up to take profit and one I designed as a kind of stop loss. I went with a flat 7.5% for the take profit as this showed the best results in the backtester. I had planned for it to be closer to 3% but for this strategy to work it needs to be higher. According to the backtest it offers around double the return of buying and holding BNB over the sample timeframe.

The 'stop loss' condition is where the fun lies. I transposed Bollinger bands from a one hour BNBUSD Binance.us chart on top of the 1 minute chart and those are the blue lines you see. The stop loss condition happens when the current price death crosses the bottom one hour Bollinger band. Ironically, often this doesn't result in any losses as you will see in the chart and instead results in a small win. This definitely was not my intention when I created it but it's a lot better than the earlier version where I set up a variable percentage-based stop loss. Even with me optimizing the regular stop loss for this coin pair, my 1 hour bband method nets an extra 2% profit over the same two week time period, even with Binance fees factored in!

Have fun and like I said, hmu via message if you want access to the customizable indicator for 3commas!

MA Emperor insiliconot StrategyConverted EmperorBTC's EMA crossover indicator for easy backtesting and added ability to:

Specify time period for backtesting

Specify order quantity

Toggle original indicators (default off)

Quoting EmperorBTC:

Entry is to be made when the

1. Cross over gives a P(Positive Sign) and the candle completely closes above the cross-over

2. When the Heikin Ashi turns green and the next green HA candle goes above the previous green HA candle.

3. The price should be at-least above the 0.236 Level from the Swing high.

Kindly note that the strategy only attempts to do check number 1, where it ensures the entry opens above the cross-over.