GARCH Adaptive Volatility & Momentum Predictor

💡 I. Indicator Concept: GARCH Adaptive Volatility & Momentum Predictor

-----------------------------------------------------------------------------

The GARCH Adaptive Momentum Speed indicator provides a powerful, forward-looking

view on market risk and momentum. Unlike standard moving averages or static

volatility indicators (like ATR), GARCH forecasts the Conditional Volatility (σ_t)

for the next bar, based on the principle of volatility clustering.

The indicator consists of two essential components:

1. GARCH Volatility (Level): The primary forecast of the expected magnitude of

price movement (risk).

2. Vol. Speed (Momentum): The first derivative of the GARCH forecast, showing

whether market risk is accelerating or decelerating. This component is the

main visual signal, displayed as a dynamic histogram.

⚙️ II. Key Features and Adaptive Logic

-----------------------------------------------------------------------------

* Dynamic Coefficient Adaptation: The indicator automatically adjusts the GARCH

coefficients (α and β) based on the chart's timeframe (TF):

- Intraday TFs (M1-H4): Uses higher α and lower β for quicker reaction

to recent shocks.

- Daily/Weekly TFs (D, W): Uses lower α and higher β for a smoother,

more persistent long-term forecast.

* Momentum Visualization: The Vol. Speed component is plotted as a dynamic

histogram (fill) that automatically changes color based on the direction of

acceleration (Green for up, Red for down).

📊 III. Interpretation Guide

-----------------------------------------------------------------------------

- GARCH Volatility (Blue Line): The predicted level of market risk. Use this to

gauge overall position sizing and stop loss width.

- Vol. Speed (Green Histogram): Momentum is ACCELERATING (Risk is increasing rapidly).

A strong signal that momentum is building, often preceding a breakout.

- Vol. Speed (Red Histogram): Momentum is DECELERATING (Risk is contracting).

Indicates momentum is fading, often associated with market consolidation.

🎯 IV. Trading Application

-----------------------------------------------------------------------------

- Breakout Timing: Look for a strong, high GREEN histogram bar. This suggests

the volatility pressure is increasing rapidly, and a breakout may be imminent.

- Consolidation: Small, shrinking RED histogram bars signal that market energy

is draining, ideal for tight consolidation patterns.

Volatilità

Tailwind.(BTC)Imagine the price of Bitcoin is like a person climbing a staircase.

The Steps (Grid): Instead of watching every single price movement, the strategy divides the market into fixed steps. In your configuration, each step measures **3,000 points**. (Examples: 60,000, 63,000, 66,000...).

The Signal: We buy only when the price climbs a full step decisively.

The "Expensive Price" Filter: If the price jumps the step but lands too far away (the candle closes too high), we do not buy. It is like trying to board a train that has already started moving too fast; the risk is too high.

Rigid Exits: The Take Profit (TP) and Stop Loss (SL) are calculated from the edge of the step, not from the specific price where you managed to buy. This preserves the geometric structure of the market.

The Code Logic (Step-by-Step)

A. The Math of the Grid (`math.floor`)

pinescript

level_base = math.floor(close / step_size) * step_size

This is the most important line.

What does it do? It rounds the price down to the nearest multiple of 3,000.

Example: If BTC is at 64,500 and the step size is 3,000:

1. Divide: $64,500 / 3,000 = 21.5$

2. `math.floor` (Floor): Removes the decimals $\rightarrow$ remains $21$.

3. Multiply: $21 * 3,000 = 63,000$.

Result: The code knows that the current "floor" is **63,000**, regardless of whether the price is at 63,001 or 65,999.

B. The Strict Breakout (`strict_cross`)

pinescript

strict_cross = (open < level_base) and (close > level_base)

Most strategies only check if `close > level`. We do things slightly differently:

`open < level_base`: Requires the candle to have "born" *below* the line (e.g., opened at 62,900).

`close > level_base`: Requires the candle to have *finished* above the line (e.g., closed at 63,200).

Why? This avoids entering on gaps (price jumps where the market opens already very high) and confirms that there was real buying power crossing the line.

C. The "Expensive Price" Filter (`max_dist_pct`)

pinescript

limit_price_entry = level_base + (step_size * (max_dist_pct / 100.0))

price_is_valid = close <= limit_price_entry

Here you apply the percentage rule:

-If the level is 63,000 and the next is 66,000 (a difference of 3,000).

-If `max_dist_pct` is **60%**, the limit is $63,000 + (60\% \text{ of } 3,000) = 64,800$.

-If the breakout candle closes at **65,000**, the variable `price_is_valid` will be **false** and it will not enter the trade. This avoids buying at the ceiling.

D. TP and SL Calculation (Anchored to the Level)

pinescript

take_profit = level_base + (step_size * tp_mult)

stop_loss = level_base - (step_size * sl_mult)

Note that we use `level_base` and not `close`.

-If you entered because the price broke 63,000, your SL is calculated starting from 63,000.

-If your SL is 1.0x, your stop will be exactly at 60,000.

This is crucial: If you bought "expensive" (e.g., at 63,500), your real stop is wider (3,500 points) than if you bought cheap (63,100). Because you filter out expensive entries, you protect your Risk/Reward ratio.

E. Visual Management (`var line`)

The code uses `var` variables to remember the TP and SL lines and the `line.set_x2` function to stretch them to the right while the operation remains open, providing that visual reference on the chart until the trade ends.

Workflow Summary

Strategy Parameters:

Total Capital: $20,000

We will use 10% of total capital per trade.

Commissions: 0.1% per trade.

TP: 1.4

SL: 1

Step Size (Grid): 3,000

We use the 200 EMA as a trend filter.

Feel free to experiment with the parameters to your liking. Cheers.

CT Market Fragility & Systemic Risk Monitor v1.0CT ⊕ Market Fragility & Systemic Risk Monitor v1.0

Systemic Stress & Market Regime Monitor

OVERVIEW

Wall Street-grade structural monitoring now open-source.

CT ⊕ Market Fragility & Systemic Risk Monitor v1.0 is a real-time systemic risk tool designed to detect fragility before it hits price. Built by former institutional traders, it delivers structural insight typically reserved for desks inside hedge funds and global macro desks.

This isn’t about finding entries or exits, it’s about understanding the environment you're trading in, and recognizing when it's shifting.

WHAT IT DOES

• Monitors six key market domains: Equities, Rates/Credit, FX (USD stress), Commodities, Crypto, and Macro

• Detects volatility stress, cross-domain coupling, and regime synchronization

• Classifies market structure into Normal → Fragile → Critical

• Shows a live dashboard with scores, coupling levels, and structural state

• Plots event markers (T1, T2, T3) for structural transitions

• Implements hysteresis logic to model post-stress 'memory

• Supports both single-domain ("Local Mode") and system-wide monitoring

HOW IT WORKS

This engine does not rely on traditional TA. No moving averages. No MACD. No patterns. No guesswork.

Instead, it measures how markets are behaving beneath price detecting when stress is:

• Building internally

• Spreading across domains

• Synchronizing into systemic fragility

T1 (🟠) — Early instability: acceleration in market coupling

T2 (🔵) — Fragile regime: multiple domains simultaneously stressed

T3 (🔴) — Critical regime: synchronized, system-wide stress

These are not buy/sell signals. They are structural regime alerts, the same kind used by institutions to cut risk before stress cascades.

WHY IT MATTERS

Most retail tools are reactive. They interpret surface-level patterns after the move.

This tool is different. It’s proactive – measuring pressure before it breaks structure.

Institutions have used structural fragility models like this for years. This script helps close that gap, giving everyday traders the same early warnings that pros use to reduce exposure and sidestep systemic blowups.

It’s not about finding the edge.

It’s about not getting crushed when the system breaks.

Whether you trade crypto, stocks, FX, or macro, this engine helps answer:

• Is the system stable right now?

• Are stress levels rising across markets?

• Is it time to tighten risk?

Institutions don’t wait for breakouts. They monitor structure.

Now, you can too.

KEY FEATURES

• Works on any asset class and any timeframe

• Fully customizable domain selection

• Three-tier structural alert system (T1–T3)

• Real-time dashboard: stress scores, states, and coupling levels

• Hysteresis modeling: post-stress “memory” detection

• Supports single-domain (local) or multi-domain (systemic) monitoring

• PineScript alerts built-in

RECOMMENDED USE

Active traders - all asset classes

Use the dashboard and T1–T3 alerts to stay aware of structural risk in real time.

Track multi-timeframe alignment to detect where risk originates and how it spreads across markets.

Crypto trader s

Monitor upstream domains (Equities, FX, Rates, Macro) to detect pressure before it reaches crypto.

Identify reflexive stress before Bitcoin reacts — and stay ahead of contagion events.

Macro & systematic traders

Use T1–T3 transitions as volatility filters, exposure governors, or dynamic risk overlays.

Build regime-aware models that adapt to shifting systemic conditions.

Examples & Visuals

Question: Would it have helped to know that at 9:30 on October 9th and again at 10:00 on October 10th that critical states were detected in the structural behavior of Bitcoin? Take a look:

30 min chart BTC shows two distinct T3 (critical) regime detections October 9th and 10:30 October 10th

5m BTC chart reveals high frequency instability for the same period, identifying instability, fragility, criticality

The 30minute BTC chart at 16:30 Friday October 10th,, a few hours after first detecting critical systemic risk

RISK DISCLAIMER

This is a structural analysis tool, not a predictive signal. It does not provide financial advice, trade entries, or forecasts. Use at your own risk. Full disclaimer embedded in the script.

Complexity Trading - From Wall St to Main St

No patterns. No repainting. No mysticism. Just logic, math, science and market structure - now made accessible to everyone.

Developer of LPPL Critical Pulse (LPPLCP), the Temporal Phase Model (TPM) and other

other advanced structural and attractor based systems inspired by Sornette’s LPPL framework and other differentiated thinkers.

Note on Methodology

This tool is not predictive, and not designed for academic publication.

It is a real-time structural monitoring system inspired by academically established concepts,

including LPPL attractor dynamics, cross-asset coupling, reflexivity, and phase regime transitions, implemented within the real-time constraints of PineScript, and intended for visual, exploratory, and diagnostic use.

Hybrid Strategy: Trend/ORB/MTFHybrid Strategy: Trend + ORB + Multi-Timeframe Matrix

This script is a comprehensive "Trading Manager" designed to filter out noise and identify high-probability breakout setups. It combines three powerful concepts into a single, clean chart interface: Trend Alignment, Opening Range Breakout (ORB), and Multi-Timeframe (MTF) Analysis.

It is designed to prevent "analysis paralysis" by providing a unified Dashboard that confirms if the trend is aligned across 5 different timeframes before you take a trade.

How it Works

The strategy relies on the "Golden Trio" of confluence:

1. Trend Definition (The Setup) Before looking for entries, the script analyzes the immediate trend. A bullish trend is defined as:

Price is above the Session VWAP.

The fast EMA (9) is above the slow EMA (21). (The inverse applies for bearish trends).

2. The Signal (The Trigger) The script draws the Opening Range (default: first 15 minutes of the session).

Buy Signal: Price breaks above the Opening Range High while the Trend is Bullish.

Sell Signal: Price breaks below the Opening Range Low while the Trend is Bearish.

3. The Confirmation (The Filter) A signal is only valid if the Higher Timeframe (default: 60m) agrees with the direction. If the 1m chart says "Buy" but the 60m chart is bearish, the signal is filtered out to prevent false breakouts.

Key Features

The Matrix Dashboard A zero-lag, real-time table in the corner of your screen that monitors 5 user-defined timeframes (e.g., 5m, 15m, 30m, 60m, 4H).

Trend: Checks if Price > EMA 21.

VWAP: Checks if Price > VWAP.

ORB: Checks if Price is currently above/below the Opening Range of that session.

D H/L: Warns if price is near the Daily High or Low.

PD H/L: Warns if price is near the Previous Daily High or Low.

Visual Order Blocks The script automatically identifies valid Order Blocks (sequences of consecutive candles followed by a strong explosive move).

Chart: Draws Green/Red zones extending to the right, showing where price may react.

Dashboard: Displays the exact High, Low, and Average price of the most recent Order Blocks for precision planning.

Risk Management (Trailing Stop) Once a trade is active, the script plots Chandelier Exit dots (ATR-based trailing stop) to help you manage the trade and lock in profits during trend runs.

Visual Guide (Chart Legend)

⬜ Gray Box: Represents the Opening Range (first 15 minutes). This is your "No Trade Zone." Wait for price to break out of this box.

🟢 Green Line: The Opening Range High. A break above this line signals potential Bullish momentum.

🔴 Red Line: The Opening Range Low. A break below this line signals potential Bearish momentum.

🟢 Green / 🔴 Red Zones (Boxes): These are Order Blocks.

🟢 Green Zone: A Bullish Order Block (Demand). Expect price to potentially bounce up from here.

🔴 Red Zone: A Bearish Order Block (Supply). Expect price to potentially reject down from here.

⚪ Dots (Trailing Stop):

🟢 Green Dots: These appear below price during a Bullish trend. They represent your suggested Stop Loss.

🔴 Red Dots: These appear above price during a Bearish trend.

🏷️ Buy / Sell Labels:

BUY: Triggers when Price breaks the Green Line + Trend is Bullish + HTF is Bullish.

SELL: Triggers when Price breaks the Red Line + Trend is Bearish + HTF is Bearish.

Settings

Session: Customizable RTH (Regular Trading Hours) to filter out pre-market noise.

Matrix Timeframes: 5 fixed slots to choose which timeframes you want to monitor.

Order Blocks: Adjust the sensitivity and lookback period for Order Block detection.

Risk: Customize the ATR multiplier for the trailing stop.

Disclaimer

This tool is for educational purposes only. Past performance does not guarantee future results. Always manage your risk properly.

Session HeatmapIntraday Seasonality

Overview

Analyzes historical patterns by time of day. Identifies when volatility, volume, and open interest changes tend to be highest or lowest.

Features

Multiple Metrics: TR (volatility), Volume, and Open Interest changes

Flexible Grouping: View patterns by weekday or month to spot day-of-week or seasonal effects

Heatmap Visualization: Blue (low) to Red (high) color scale for quick pattern recognition

Percentile Mode: Reduces outlier impact by using 5th-95th percentile range

Timezone Support: Display in UTC alongside your local time

Metrics Explained

TR: Volatility - when markets move most

Volume: Liquidity - when participation is highest

OI Increase: When new positions are opened

OI Decrease: When positions are closed

OI Net: Net open interest change

Usage

Set your timezone and preferred slot size (30min/1H)

Choose a date range (relative or custom)

Select a metric to analyze

Use "Group By" to see weekday or monthly patterns

Switch to Percentile color scale if outliers dominate

Notes

Chart timeframe should be equal to or smaller than Slot Size

OI metrics require Binance Perpetual symbols

DST is not automatically adjusted; consider seasonal shifts for US/EU sessions

Session ATR Progression Tracker📊 Session ATR Progression Tracker - SIYL Regression Trading Tool

Track how much of your instrument's 7-day Average True Range (ATR) has been covered during the current trading session. This indicator is specifically designed for regression traders who follow the "Stay In Your Lane" (SIYL) methodology, helping you identify when the probability of mean reversion significantly increases. If you are interested in more on that check out Rod Casselli and tradersdevgroup.com.

🎯 Key Features:

• Real-time ATR Coverage Percentage - See at a glance what percentage of the 7-day ATR has been covered in the current session

• SIYL-Optimized Thresholds - See at a glance when the instrument has achieved 80% and 100% ATR coverage, the proven thresholds where mean reversion probability increases (customizable)

• Flexible Session Modes:

- Daily: Resets at calendar day change

- Session: Uses exchange-defined trading sessions

- Custom Session: Set your exact session start/end times (perfect for futures traders and international markets)

• Visual Alerts - Color-coded display (gray → orange → red) and optional background highlighting

• Repositionable Display - Choose from 9 screen positions to avoid chart clutter

• Session Markers - Green triangles mark the start of each new session

• Detailed Stats - View current range, ATR value, session high/low, and session status

💡 Why Use This Indicator?

This tool is built around a proven concept: regression trading becomes significantly more effective once a session has achieved at least 80% of its 7-day ATR. At this threshold, the probability of price reverting to mean increases substantially, creating higher-probability trade setups for SIYL practitioners.

Benefits for regression traders:

- Identify optimal entry points when mean reversion probability is highest (≥80% ATR coverage)

- Avoid premature regression entries before adequate range has been established

- Recognize when daily moves have "earned their range" and are ripe for reversal

- Time fade-the-move and counter-trend strategies with statistical backing

- Improve win rates by trading only after proven probability thresholds are met

⚙️ Setup Instructions:

1. Add the indicator to your chart

2. Select your preferred "Reset Mode" (recommend "Custom Session" for futures/international markets)

3. If using Custom Session, enter your session times in 24-hour format (e.g., 0930-1600 for US stocks, 1700-1600 for CME futures)

4. Adjust alert thresholds if desired (default: 80% and 100% - proven SIYL thresholds)

5. Position the display where it's most visible on your chart

📈 Works Across All Markets:

Stocks • Futures • Forex • Indices • Crypto • Commodities

Perfect for regression traders, mean reversion specialists, and SIYL practitioners who want to trade with probability on their side by entering only after the session has "earned its range."

---

Tip: For futures contracts with overnight sessions that span calendar days (like MES, MNQ, MYM), use "Custom Session" mode with your exchange's official session times for accurate tracking.

Bollinger Bands Forecast with Signals (Zeiierman)█ Overview

Bollinger Bands Forecast with Signals (Zeiierman) extends classic Bollinger Bands into a forward-looking framework. Instead of only showing where volatility has been, it projects where the basis (midline) and band width are likely to drift next, based on recent trend and volatility behavior.

The projection is built from the measured slopes of the Bollinger basis, the standard deviation (or ATR, depending on the mode), and a volatility “breathing” component. On top of that, the script includes an optional projected price path that can be blended with a deterministic random walk, plus rejection signals to highlight failed band breaks.

█ How It Works

⚪ Bollinger Core

The script first computes standard Bollinger Bands using the selected Source, Length, and Multiplier:

Basis = SMA(Source, Length)

Band width = Multiplier × StDev(Source, Length)

Upper/Lower = Basis ± Width

This remains the “live” (non-forecast) structure on the chart.

⚪ Trend & Volatility Slope Estimation

To project forward, the indicator measures directional drift and volatility drift using linear regression differences:

Basis slope from the Bollinger basis

StDev slope from the Bollinger deviation

ATR slope for ATR-based projection mode

These slopes drive the forecast bands forward, reflecting the market’s recent directional and volatility regime.

⚪ Projection Engine (Forecast Bands)

At the last bar, the indicator draws projected basis, upper, and lower lines out to Forecast Bars. The projected basis can be:

Trend (straight linear projection)

Curved (ease-in/out transition toward projected endpoints)

Smoothed (extra smoothing on projected basis/width)

⚪ Price Path Projection + Optional Random Walk

In addition to projecting the bands, the script can draw a price forecast path made of a small number of zigzag swings.

Each swing targets a point offset from the projected basis by a multiple of the projected half-width (“width units”).

Decay gradually reduces swing size as the forecast deepens.

The Optional Random Walk Blend adds a deterministic drift component to the zigzag path. It’s not true randomness; it’s a stable pseudo-random sequence, so the drawing doesn’t jump around on refresh, while still adding “natural” variation.

⚪ Rejection Signals

Signals are based on failed attempts to break a band:

Bear Signal (Down): price tries to push above the upper band, then falls back inside, while still closing above the basis.

Bull Signal (Up): price tries to push below the lower band, then returns back inside, while still closing below the basis.

█ How to Use

⚪ Forward Support/Resistance Corridors

Treat the projected upper/lower bands as a future volatility envelope, not a guarantee:

The upper projection ≈ is likely a resistance level if the regime persists

The lower projection ≈ is likely a support level if the regime persists

Best used for trade planning, targets, and “where price could travel” under similar conditions.

⚪ Regime Read: Trend + Volatility

The projection shape is informative:

Rising basis + expanding width → trend with increasing volatility (needs wider stops / more caution)

Flat basis + compressing width → contraction regime (often precedes expansion)

⚪ Signals for Mean-Reversion / Failed Breakouts

The rejection markers are useful for fade-style setups:

A Down signal near/after upper-band failure can imply rotation back toward the basis.

An Up signal near/after lower-band failure can imply snap-back toward the basis.

With MA filtering enabled, signals are constrained to align with the broader bias, helping reduce chop-driven noise.

█ Related Publications

Donchian Predictive Channel (Zeiierman)

█ Settings

⚪ Bollinger Band

Controls the live Bollinger Bands on the chart.

Source – Price used for calculations.

Length – Lookback period; higher = smoother, lower = more reactive.

Multiplier – Bandwidth; higher = wider bands, lower = tighter bands.

⚪ Forecast

Controls the forward projection of the Bollinger Bands.

Forecast Bars – How far into the future the bands are projected.

Trend Length – Lookback used to estimate trend and volatility slopes.

Forecast Band Mode – Defines projection behavior (linear, curved, breathing, ATR-based, or smoothed).

⚪ Price Forecast

Controls the projected price path inside the bands.

ZigZag Swings – Number of projected oscillations.

Amplitude – Distance from basis, measured in bandwidth units.

Decay – Shrinks swings further into the forecast.

⚪ Random-Walk

Adds controlled randomness to the price path.

Enable – Toggle random-walk influence.

Blend – Strength of randomness vs. zigzag.

Step Size – Size of random steps (band-width units).

Decay – Reduces randomness as the forecast deepens.

Seed – Changes the (stable) random sequence.

⚪ Signals

Controls rejection/mean-reversion signals.

Show Signals – Enable/disable signal markers.

MA Filter (Type/Length) – Filters signals by trend direction.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

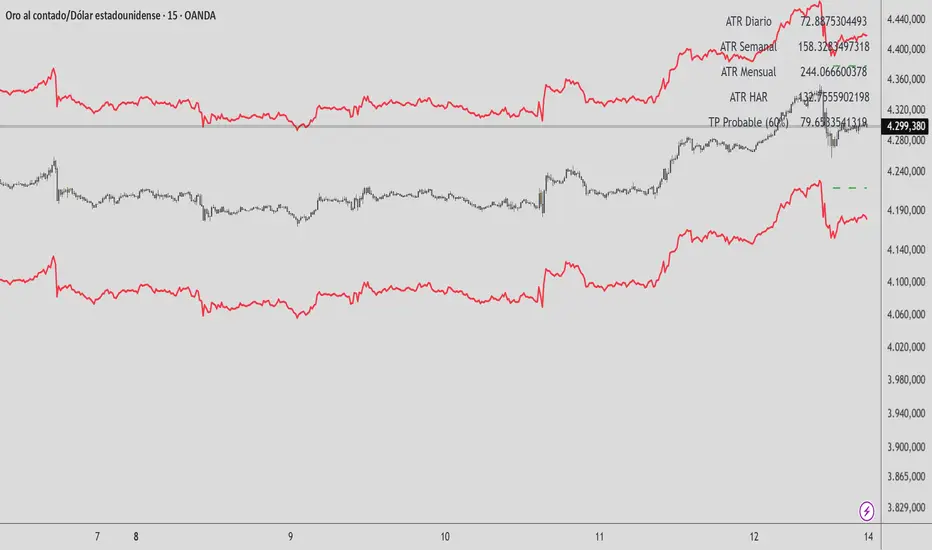

HAR Volatility ATR (Multi-Asset) - Andreus VillalobosIndicator based on the HAR (Hyper-Realized Volatility) model.

Combines daily, weekly, and monthly ATRs to project:

– Most probable price range (90%)

– Most probable take profit (60%)

Does not generate entry signals.

Designed for use in conjunction with:

market structure, liquidity, and price action.

Works on Forex, Indices, Gold, and Cryptocurrencies.

HAR Volatility ATR v1.0 (Andreus Villalobos)

Indicator based on the HAR (Hyper-Realized Volatility) model.

Combines daily, weekly, and monthly ATRs to project:

– Most probable price range (90%)

– Most probable take profit (60%)

Does not generate entry signals.

Designed for use in conjunction with:

market structure, liquidity, and price action.

Works on Forex, Indices, Gold, and Cryptocurrencies.

Renko Average Bricks This indicator calculates the average RENKO brick streaks. Streaks=consecutive bricks of the same color. EX. G= 1 streak of 1. GGG = 1 streak of 3. RR 1 streak of 2. Single bricks count. There is the option for look back period which can be changed but Defaults to 50. Calculates the last 50 completed green streaks and then averages them. Same with red streaks. Only closed bricks count.

Very Simple and can be used for targets, ect.

Cheers

TRV & nTRV - Trimmed Range VolatilityGrid bots require stable volatility measurement - ATR becomes misleading when gaps and sudden spikes distort the average. TRV (Trimmed Range Volatility) is an advanced version of ATR: it filters outliers at the extremes (highest and lowest ranges) and remains unaffected by gaps. This provides real-time, accurate volatility measurement for grid bot setup.Grid bots require stable volatility measurement - ATR becomes misleading when gaps and sudden spikes distort the average. TRV (Trimmed Range Volatility) is an advanced version of ATR: it filters outliers at the extremes (highest and lowest ranges) and remains unaffected by gaps. This provides real-time, accurate volatility measurement for grid bot setup.

Why We Developed TRV?

When a gap or sudden spike occurs in the morning, this extreme movement affects standard ATR calculations for an extended period. Even if the price moves sideways for the rest of the day, ATR remains elevated. This causes grid bots to operate with unnecessarily wide spacing and execute fewer trades.

TRV Advantages:

✅ Unaffected by Gaps: Opening gaps don't distort the calculation

✅ Extreme Point Elimination: Filters the largest and smallest outlier candles

✅ Real-Time Accuracy: Shows current market volatility

✅ Grid Bot Optimization: Enables tighter and more efficient grid spacing

✅ Comparison Capability: Compare different stocks and timeframes with nTRV

Grid Bot Usage:

The TRV value is used directly to calculate the number of grid lines:

(Resistance - Support) / TRV = Number of Grid Lines

Example:

Resistance: $110

Support: $90

TRV: $2

Grid Count: (110-90)/2 = 10 grid lines

Features:

Two Filtering Modes: Manual (enter number) or Percentage-Based (automatic ratio)

Four Indicators in One: nTRV, TRV, ATR, and nATR all displayed on the same panel

nTRV: Normalized value (percentage-based, for stock comparison)

TRV: Absolute value (currency-based, for grid calculation)

ATR & nATR Included: Standard ATR and nATR for direct comparison with TRV

Comprehensive Analysis: Compare filtered (TRV) vs unfiltered (ATR) volatility side-by-side

Default: 10% top, 10% bottom outlier elimination

Conclusion:

TRV is an advanced version of ATR specifically designed for grid bot traders. By filtering outlier movements, it provides more stable and reliable volatility measurement. The indicator includes both TRV (filtered) and ATR (unfiltered) on the same chart, giving traders a comprehensive view to make informed decisions. This dual-display approach enables more efficient grid strategies and increased trading frequency.

GARCH Volume Volatility [MarkitTick]Title: GARCH Volume Volatility

Description

Overview

The GARCH Volume Volatility (GV) indicator is a sophisticated quantitative tool designed to analyze the rate of change in market participation. While the vast majority of technical indicators focus on Price Volatility (how much price moves), this script focuses on Volume Volatility (how unstable the participation is).

Market volume is rarely distributed evenly; it tends to cluster. Periods of high activity are often followed by more high activity, and periods of calm tend to persist. This behavior is known as "heteroskedasticity." This script utilizes an Exponentially Weighted Moving Average (EWMA) model—a core component of Generalized Autoregressive Conditional Heteroskedasticity (GARCH) frameworks—to model these changing variance regimes.

By isolating volume volatility from raw volume data, this tool helps traders distinguish between sustainable liquidity flows and erratic, unsustainable volume shocks that often precede market reversals or breakouts.

Methodology and Calculations

1. Logarithmic vs. Percentage Returns

The foundation of this indicator is the calculation of "Volume Returns"—the period-over-period change in volume.

- The script defaults to Logarithmic Returns. In financial statistics, log returns are preferred because they normalize data that can vary wildly in magnitude (such as cryptocurrency volume spikes), providing a more symmetric view of changes.

- Users can opt for standard percentage changes if they prefer a linear approach.

2. Variance Proxy (Squared Returns)

To measure volatility, the direction of the volume change (up or down) matters less than the magnitude. The script squares the returns to create a "Variance Proxy." This ensures that a massive drop in volume is treated with the same statistical weight as a massive spike in volume—both represent a significant change in the volatility of participation.

3. GARCH-Style Smoothing (EWMA)

Standard Moving Averages (SMA) treat all data points in the lookback period equally. However, volatility is dynamic. This script uses an EWMA model with a tunable "Lambda" (Decay Factor).

- The Recursive Formula: The current calculation relies on a weighted average of the current variance and the previous period's smoothed variance.

- Memory Effect: This allows the indicator to "remember" recent volatility shocks while gradually letting their influence fade. This mimics the GARCH process of conditional variance.

4. Dynamic Statistical Thresholds

The final output is the Volatility (square root of variance). To make this data actionable, the script calculates a dynamic upper and lower limit based on the standard deviation (Z-Score) of the volatility itself over a user-defined lookback period.

How to Use

The indicator plots a histogram that categorizes the market into four distinct volatility regimes:

1. High Volatility (Red Histogram)

Trigger: Volatility > High Band (Upper Standard Deviation).

Interpretation: This signals an extreme anomaly in volume stability. This is not just "high volume," but "erratic volume behavior." This often occurs at:

- Capitulation bottoms (panic selling).

- Euphoric tops (blow-off tops).

- Major news events or earnings releases.

2. Elevated Volatility (Maroon Histogram)

Trigger: Volatility > Mean Average.

Interpretation: The market is in an active state. Participation is changing rapidly, but within statistically normal bounds. This is common during healthy, trending moves where new participants are entering the market steadily.

3. Normal/Low Volatility (Green Histogram)

Trigger: Volatility is within the lower bands.

Interpretation: The market volume is stable. There are no sudden shocks in participation. This is typical of consolidation phases or "creeping" trends where the price drifts without significant volume conviction.

4. Extremely Low Volatility (Bright Green/Transparent)

Trigger: Volatility < Low Band.

Interpretation: The "calm before the storm." When volume volatility collapses to near-zero, it implies that the market has reached a state of equilibrium or disinterest. Historically, volatility is cyclical; periods of extreme compression often lead to violent expansion.

Settings and Configuration

Core Settings

- Use EWMA: When checked (Default), uses the recursive GARCH-style calculation. If unchecked, it reverts to a simple SMA of variance, which is less sensitive to recent shocks but more stable.

- Log Returns: Uses natural log for calculations. Highly recommended for assets with exponential growth or large volume ranges.

- Length: The baseline period for the calculation.

- Threshold Lookback: The number of bars used to calculate the Mean and Standard Deviation bands.

- EWMA Lambda: The decay factor (0.0 to 1.0). A value of 0.94 is standard for risk metrics.

-- Higher Lambda (e.g., 0.98): The indicator reacts slower and is smoother (long memory).

-- Lower Lambda (e.g., 0.80): The indicator reacts very fast to new data (short memory).

Visuals

- Show Thresholds: Toggles the visibility of the statistical bands on the chart.

- High Band (StdDev): The multiplier for the upper warning zone. Default is 1.5 deviations. Increasing this to 2.0 or 3.0 will filter for only the most extreme events.

Disclaimer This tool is for educational and technical analysis purposes only. Breakouts can fail (fake-outs), and past geometric patterns do not guarantee future price action. Always manage risk and use this tool in conjunction with other forms of analysis.

RSI WMA Crossover Momentum w/ HighlightRSI WMA Crossover Momentum

This is a momentum indicator that tracks the RSI. Its principle is to use the WMA line to determine the trend of the RSI, and from the RSI, the price trend can be determined.

Volume-Gated Trend Ribbon [QuantAlgo]🟢 Overview

The Volume-Gated Trend Ribbon employs a selective price-updating mechanism that filters market noise through volume validation, creating a trend-following system that responds exclusively to significant price movements. The indicator gates price updates to moving average calculations based on volume threshold crossovers, ensuring that only bars with significant participation influence the trend direction. By interpolating between fast and slow moving averages to create a multi-layered visual ribbon, the indicator provides traders and investors with an adaptive trend identification framework that distinguishes between volume-backed directional shifts and low-conviction price fluctuations across multiple timeframes and asset classes.

🟢 How It Works

The indicator first establishes a dynamic baseline by calculating the simple moving average of volume over a configurable lookback period, then applies a user-defined multiplier to determine the significance threshold:

avgVol = ta.sma(volume, volPeriod)

highVol = volume >= avgVol * volMult

The gated price mechanism employs conditional updating where the close price is only captured and stored when volume exceeds the threshold. During low-volume periods, the indicator maintains the last qualified price level rather than tracking every minor fluctuation:

var float gatedClose = close

if highVol

gatedClose := close

Dual moving averages are calculated using the gated price input, with the indicator supporting various MA types. The fast and slow periods create the outer boundaries of the trend ribbon:

fastMA = volMA(gatedClose, close, fastPeriod)

slowMA = volMA(gatedClose, close, slowPeriod)

Ribbon interpolation creates intermediate layers by blending the fast and slow moving averages using weighted combinations, establishing a gradient effect that visually represents trend strength and momentum distribution:

midFastMA = fastMA * 0.67 + slowMA * 0.33

midSlowMA = fastMA * 0.33 + slowMA * 0.67

Trend state determination compares the fast MA against the slow MA, establishing bullish regimes when the faster average trades above the slower average and bearish regimes during the inverse relationship. Signal generation triggers on state transitions, producing alerts when the directional bias shifts:

bullish = fastMA > slowMA

longSignal = trendState == 1 and trendState != 1

shortSignal = trendState == -1 and trendState != -1

The visualization architecture constructs a three-tiered opacity gradient where the ribbon's core (between mid-slow and slow MAs) displays the highest opacity, the inner layer (between mid-fast and mid-slow) shows medium opacity, and the outer layer (between fast and mid-fast) presents the lightest fill, creating depth perception that emphasizes the trend center while acknowledging edge uncertainty.

🟢 How to Use This Indicator

▶ Long and Short Signals: The indicator generates long/buy signals when the trend state transitions to bullish (fast MA crosses above slow MA) and short/sell signals when transitioning to bearish (fast MA crosses below slow MA). Because these crossovers only reflect volume-validated price movements, they represent significant level of participation rather than random noise, providing higher-conviction entry signals that filter out false breakouts occurring on thin volume.

▶ Ribbon Width Dynamics: The spacing between the fast and slow moving averages creates the ribbon width, which serves as a visual proxy for trend strength and volatility. Expanding ribbons indicate accelerating directional movement with increasing separation between short-term and long-term momentum, suggesting robust trend development. Conversely, contracting ribbons signal momentum deceleration, potential trend exhaustion, or impending consolidation as the fast MA converges toward the slow MA.

▶ Preconfigured Presets: Three optimized parameter sets accommodate different trading styles and market conditions. Default provides balanced trend identification suitable for swing trading on daily timeframes with moderate volume filtering and responsiveness. Fast Response delivers aggressive signal generation optimized for intraday scalping on 1-15 minute charts, using lower volume thresholds and shorter moving average periods to capture rapid momentum shifts. Smooth Trend offers conservative trend confirmation ideal for position trading on 4-hour to weekly charts, employing stricter volume requirements and extended periods to filter noise and identify only the most robust directional moves.

▶ Built-in Alerts: Three alert conditions enable automated monitoring: Bullish Trend Signal triggers when the fast MA crosses above the slow MA confirming uptrend initiation, Bearish Trend Signal activates when the fast MA crosses below the slow MA confirming downtrend initiation, and Trend Change alerts on any directional transition regardless of direction. These notifications allow you to respond to volume-validated regime shifts without continuous chart monitoring.

▶ Color Customization: Six visual themes (Classic, Aqua, Cosmic, Ember, Neon, plus Custom) accommodate different chart backgrounds and display preferences, ensuring optimal contrast and visual clarity across trading environments. The adjustable fill opacity control (0-100%) allows fine-tuning of ribbon prominence, with lower opacity values create subtle background context while higher values produce bold trend emphasis. Optional bar coloring extends the trend indication directly to the price bars, providing immediate directional reference without requiring visual cross-reference to the ribbon itself.

PMax - Asymmetric MultipliersDescription: This script is an enhanced version of the popular PMax (Profit Maximizer) indicator, originally developed by KivancOzbilgic. It has been converted into a full strategy with advanced customization options for backtesting and trend following.

Key Features & Modifications:

Asymmetric ATR Multipliers: Unlike the standard version, this script allows you to set different ATR multipliers for Upper (Short/Resistance) and Lower (Long/Support) bands.

Default Upper: 1.5 (Tighter trailing for Short positions)

Default Lower: 3.0 (Wider trailing for Long positions to avoid whipsaws)

Expanded MA Types: Added HULL (HMA) and VAR (Variable Index Dynamic Average) options.

VAR is highly recommended for filtering out noise in ranging markets.

HULL is ideal for scalping and faster reactions.

Built-in Risk Management: A fixed 5% Stop Loss mechanism is integrated into the strategy. It protects your capital by closing positions if the price moves 5% against you, even if the trend hasn't reversed yet.

Visibility Fix: Solved the issue where the PMax line would disappear or start at zero in the initial bars.

How to Use:

Use the VAR MA type for trend following in volatile markets.

Adjust the "Stop Loss Percent" input to fit your risk appetite.

The strategy employs an "Always In" logic (Long/Short) but respects the hard Stop Loss.

Credits: Original PMax logic by KivancOzbilgic.

VEGA (Velocity of Efficient Gain Adaptation)VEGA (Velocity of Efficient Gain Adaptation)

VEGA is a momentum oscillator that measures the velocity of an efficiency-weighted adaptive moving average. Unlike traditional momentum indicators that react uniformly to all price movements, VEGA intelligently adapts its sensitivity based on market conditions—responding quickly during trending periods and filtering noise during consolidation.

--------------------------------

What Makes VEGA Different

Efficiency-Driven Adaptation

At its core, VEGA uses the Efficiency Ratio (ER) to distinguish between trending and choppy markets. When price moves efficiently in one direction, VEGA's underlying adaptive MA speeds up to capture the move. When price chops sideways, it slows down to avoid whipsaws. This creates a momentum reading that's inherently cleaner than fixed-period alternatives.

Linear Regression Smoothed Source

VEGA offers an optional LinReg-smoothed price source that blends regular candles with linear regression values. This pre-smoothing reduces noise before it ever enters the calculation, resulting in a histogram that's easier to read without sacrificing responsiveness. The mix ratio lets you dial in exactly how much smoothing you want.

Z-Score Normalization with Dead Zone

Rather than arbitrary oscillator bounds, VEGA normalizes output as standard deviations from the mean. This gives statistically meaningful levels: readings above +2σ or below -2σ represent genuinely extreme momentum. The configurable dead zone (with Snap, Soft Fade, or None modes) filters out insignificant movements near zero, keeping you focused on signals that matter.

--------------------------------

How It Works

1. Source Preparation — Price is smoothed via a LinReg/regular candle blend

2. Efficiency Ratio — Measures directional movement vs total movement over the lookback period

3. Adaptive MA — Applies variable smoothing based on efficiency (fast during trends, slow during chop)

4. Velocity — Calculates the rate of change of the adaptive MA

5. Normalization — Converts to Z-Score (standard deviations) or ATR-normalized percentage

6. Dead Zone — Optionally filters near-zero values to reduce noise

--------------------------------

How To Read VEGA

Signal and Interpretation

Histogram above zero | Bullish momentum

Histogram below zero | Bearish momentum

Bright color | Momentum accelerating

Faded color | Momentum decelerating

Beyond ±1σ bands | Above-average momentum

Beyond ±2σ bands | Extreme momentum (potential reversal zone)

Zero line cross*| Momentum shift

--------------------------------

Key Settings

ER Length — Lookback for efficiency ratio calculation. Higher = smoother, slower adaptation.

Fast/Slow Smoothing — Controls the adaptive MA's responsiveness range. The MA blends between these based on efficiency.

LinReg Settings — Enable smoothed candles and adjust the blend ratio (0 = regular candles, 1 = full LinReg, 0.5 = 50/50 mix).

Z-Score Lookback — Period for calculating mean and standard deviation. Shorter = more reactive normalization.

Dead Zone Type — How to handle near-zero values:

Snap — Hard cutoff to zero

Soft Fade — Gradual reduction toward zero

None — No filtering

Dead Zone Threshold — Values within this Z-Score range are affected by the dead zone setting.

VEGA works on any timeframe and any market. For best results, adjust the ER Length and LinReg settings to match your trading style and the volatility characteristics of your instrument.

Volatility Targeting: Single Asset [BackQuant]Volatility Targeting: Single Asset

An educational example that demonstrates how volatility targeting can scale exposure up or down on one symbol, then applies a simple EMA cross for long or short direction and a higher timeframe style regime filter to gate risk. It builds a synthetic equity curve and compares it to buy and hold and a benchmark.

Important disclaimer

This script is a concept and education example only . It is not a complete trading system and it is not meant for live execution. It does not model many real world constraints, and its equity curve is only a simplified simulation. If you want to trade any idea like this, you need a proper strategy() implementation, realistic execution assumptions, and robust backtesting with out of sample validation.

Single asset vs the full portfolio concept

This indicator is the single asset, long short version of the broader volatility targeted momentum portfolio concept. The original multi asset concept and full portfolio implementation is here:

That portfolio script is about allocating across multiple assets with a portfolio view. This script is intentionally simpler and focuses on one symbol so you can clearly see how volatility targeting behaves, how the scaling interacts with trend direction, and what an equity curve comparison looks like.

What this indicator is trying to demonstrate

Volatility targeting is a risk scaling framework. The core idea is simple:

If realized volatility is low relative to a target, you can scale position size up so the strategy behaves like it has a stable risk budget.

If realized volatility is high relative to a target, you scale down to avoid getting blown around by the market.

Instead of always being 1x long or 1x short, exposure becomes dynamic. This is often used in risk parity style systems, trend following overlays, and volatility controlled products.

This script combines that risk scaling with a simple trend direction model:

Fast and slow EMA cross determines whether the strategy is long or short.

A second, longer EMA cross acts as a regime filter that decides whether the system is ACTIVE or effectively in CASH.

An equity curve is built from the scaled returns so you can visualize how the framework behaves across regimes.

How the logic works step by step

1) Returns and simple momentum

The script uses log returns for the base return stream:

ret = log(price / price )

It also computes a simple momentum value:

mom = price / price - 1

In this version, momentum is mainly informational since the directional signal is the EMA cross. The lookback input is shared with volatility estimation to keep the concept compact.

2) Realized volatility estimation

Realized volatility is estimated as the standard deviation of returns over the lookback window, then annualized:

vol = stdev(ret, lookback) * sqrt(tradingdays)

The Trading Days/Year input controls annualization:

252 is typical for traditional markets.

365 is typical for crypto since it trades daily.

3) Volatility targeting multiplier

Once realized vol is estimated, the script computes a scaling factor that tries to push realized volatility toward the target:

volMult = targetVol / vol

This is then clamped into a reasonable range:

Minimum 0.1 so exposure never goes to zero just because vol spikes.

Maximum 5.0 so exposure is not allowed to lever infinitely during ultra low volatility periods.

This clamp is one of the most important “sanity rails” in any volatility targeted system. Without it, very low volatility regimes can create unrealistic leverage.

4) Scaled return stream

The per bar return used for the equity curve is the raw return multiplied by the volatility multiplier:

sr = ret * volMult

Think of this as the return you would have earned if you scaled exposure to match the volatility budget.

5) Long short direction via EMA cross

Direction is determined by a fast and slow EMA cross on price:

If fast EMA is above slow EMA, direction is long.

If fast EMA is below slow EMA, direction is short.

This produces dir as either +1 or -1. The scaled return stream is then signed by direction:

avgRet = dir * sr

So the strategy return is volatility targeted and directionally flipped depending on trend.

6) Regime filter: ACTIVE vs CASH

A second EMA pair acts as a top level regime filter:

If fast regime EMA is above slow regime EMA, the system is ACTIVE.

If fast regime EMA is below slow regime EMA, the system is considered CASH, meaning it does not compound equity.

This is designed to reduce participation in long bear phases or low quality environments, depending on how you set the regime lengths. By default it is a classic 50 and 200 EMA cross structure.

Important detail, the script applies regime_filter when compounding equity, meaning it uses the prior bar regime state to avoid ambiguous same bar updates.

7) Equity curve construction

The script builds a synthetic equity curve starting from Initial Capital after Start Date . Each bar:

If regime was ACTIVE on the previous bar, equity compounds by (1 + netRet).

If regime was CASH, equity stays flat.

Fees are modeled very simply as a per bar penalty on returns:

netRet = avgRet - (fee_rate * avgRet)

This is not realistic execution modeling, it is just a simple turnover penalty knob to show how friction can reduce compounded performance. Real backtesting should model trade based costs, spreads, funding, and slippage.

Benchmark and buy and hold comparison

The script pulls a benchmark symbol via request.security and builds a buy and hold equity curve starting from the same date and initial capital. The buy and hold curve is based on benchmark price appreciation, not the strategy’s asset price, so you can compare:

Strategy equity on the chart symbol.

Buy and hold equity for the selected benchmark instrument.

By default the benchmark is TVC:SPX, but you can set it to anything, for crypto you might set it to BTC, or a sector index, or a dominance proxy depending on your study.

What it plots

If enabled, the indicator plots:

Strategy Equity as a line, colored by recent direction of equity change, using Positive Equity Color and Negative Equity Color .

Buy and Hold Equity for the chosen benchmark as a line.

Optional labels that tag each curve on the right side of the chart.

This makes it easy to visually see when volatility targeting and regime gating change the shape of the equity curve relative to a simple passive hold.

Metrics table explained

If Show Metrics Table is enabled, a table is built and populated with common performance statistics based on the simulated daily returns of the strategy equity curve after the start date. These include:

Net Profit (%) total return relative to initial capital.

Max DD (%) maximum drawdown computed from equity peaks, stored over time.

Win Rate percent of positive return bars.

Annual Mean Returns (% p/y) mean daily return annualized.

Annual Stdev Returns (% p/y) volatility of daily returns annualized.

Variance of annualized returns.

Sortino Ratio annualized return divided by downside deviation, using negative return stdev.

Sharpe Ratio risk adjusted return using the risk free rate input.

Omega Ratio positive return sum divided by negative return sum.

Gain to Pain total return sum divided by absolute loss sum.

CAGR (% p/y) compounded annual growth rate based on time since start date.

Portfolio Alpha (% p/y) alpha versus benchmark using beta and the benchmark mean.

Portfolio Beta covariance of strategy returns with benchmark returns divided by benchmark variance.

Skewness of Returns actually the script computes a conditional value based on the lower 5 percent tail of returns, so it behaves more like a simple CVaR style tail loss estimate than classic skewness.

Important note, these are calculated from the synthetic equity stream in an indicator context. They are useful for concept exploration, but they are not a substitute for professional backtesting where trade timing, fills, funding, and leverage constraints are accurately represented.

How to interpret the system conceptually

Vol targeting effect

When volatility rises, volMult falls, so the strategy de risks and the equity curve typically becomes smoother. When volatility compresses, volMult rises, so the system takes more exposure and tries to maintain a stable risk budget.

This is why volatility targeting is often used as a “risk equalizer”, it can reduce the “biggest drawdowns happen only because vol expanded” problem, at the cost of potentially under participating in explosive upside if volatility rises during a trend.

Long short directional effect

Because direction is an EMA cross:

In strong trends, the direction stays stable and the scaled return stream compounds in that trend direction.

In choppy ranges, the EMA cross can flip and create whipsaws, which is where fees and regime filtering matter most.

Regime filter effect

The 50 and 200 style filter tries to:

Keep the system active in sustained up regimes.

Reduce exposure during long down regimes or extended weakness.

It will always be late at turning points, by design. It is a slow filter meant to reduce deep participation, not to catch bottoms.

Common applications

This script is mainly for understanding and research, but conceptually, volatility targeting overlays are used for:

Risk budgeting normalize risk so your exposure is not accidentally huge in high vol regimes.

System comparison see how a simple trend model behaves with and without vol scaling.

Parameter exploration test how target volatility, lookback length, and regime lengths change the shape of equity and drawdowns.

Framework building as a reference blueprint before implementing a proper strategy() version with trade based execution logic.

Tuning guidance

Lookback lower values react faster to vol shifts but can create unstable scaling, higher values smooth scaling but react slower to regime changes.

Target volatility higher targets increase exposure and drawdown potential, lower targets reduce exposure and usually lower drawdowns, but can under perform in strong trends.

Signal EMAs tighter EMAs increase trade frequency, wider EMAs reduce churn but react slower.

Regime EMAs slower regime filters reduce false toggles but will miss early trend transitions.

Fees if you crank this up you will see how sensitive higher turnover parameter sets are to friction.

Final note

This is a compact educational demonstration of a volatility targeted, long short single asset framework with a regime gate and a synthetic equity curve. If you want a production ready implementation, the correct next step is to convert this concept into a strategy() script, add realistic execution and cost modeling, test across multiple timeframes and market regimes, and validate out of sample before making any decision based on the results.

Trinity Bollinger Bands Pro with BreakoutsTrinity Bollinger Bands Pro Indicator

The **Trinity Bollinger Bands Pro + Triple Bands & Expansion** is a highly customized, advanced volatility and breakout indicator built on the classic Bollinger Bands framework. It expands the standard single-pair bands into **three independent deviation levels** (typically 1σ, 2σ, and 3σ) around a user-selectable moving average basis (default EMA 20). This creates clear "zones" of volatility, with dynamic trend-based coloring, layered fills, fixed-style labels, and a statistical volatility expansion detector shown as a directional background highlight in a separate pane. The result is a visually intuitive tool that helps traders identify consolidation, building momentum, confirmed trends, and rare explosive moves with high-probability filtering.

### Why It's Good and Different from Standard Indicators

This indicator stands out by addressing common limitations of traditional Bollinger Bands and multi-deviation scripts:

- **Layered statistical significance**: Unlike single (2σ) or basic double-band setups, it provides three distinct levels—early momentum (1σ), standard confirmation (2σ), and extreme/rare breakouts (3σ)—making it easier to stage trades progressively rather than relying on one ambiguous cross.

- **Trend-aware visuals**: Bands, basis, and fills change color based on price position relative to a separate trend MA, giving immediate bullish/bearish bias without needing additional indicators.

- **Clean, fixed labels**: Tiny, arrow-pointing labels ("1/2/3 SD Above/Below", "BB Basis") with consistent colors (purple upper, blue lower, yellow basis) provide instant identification

- **Statistical expansion detection**: Uses percentile ranking of band width "bell curve" concept" to identify abnormally high volatility, triggering directional background highlights (green bullish, red bearish) earlier than raw width spikes.

- **Reduced noise and fakeouts**: Tiered breakouts + expansion filter focus alerts on high-probability moves, unlike most BB scripts that flood signals on every touch.

Compared to popular public scripts (e.g., standard Bollinger Bands, Triple BB variants, or separate BBW Percentile tools), this combines everything into one cohesive indicator with superior visual clarity and statistical rigor.

### Key Features

- **Triple customizable bands**: Enable/disable and adjust multipliers for 1σ (early), 2σ (confirmed), 3σ (extreme) deviations.

- **Trend-based dynamic coloring**: Separate editable colors for each band set (bullish/bearish).

- **Layered zone fills**: Colored between bands with transparency, reflecting current trend.

- **Fixed tiny labels**: All left-pointing arrows with purple (upper), blue (lower), yellow (basis) backgrounds for quick reference.

- **Statistical expansion overlay**: with directional background (green/red) during extreme volatility expansions (earlier trigger using 2σ width).

- **Tiered alerts**: Early (Band 1), Confirmed (Band 2), Extreme (Band 3), High-Probability (Extreme + expansion), and general expansion alerts.

- **Fully configurable basis**: Length, type (SMA/EMA/WMA/RMA), and thin fixed lines for minimal clutter.

### How Traders Can Use It

- **Spot squeezes and breakouts**: Watch for tight bands (low width) → expansion background → price closing outside Band 1 (early entry), Band 2 (add/confirm), Band 3 (strong trend conviction).

- **Filter fakeouts**: Only act on crosses accompanied by expansion background color matching trend direction—dramatically reduces whipsaws.

- **Trend riding**: Price "walking" colored bands (e.g., hugging upper purple-label bands in green background = strong bullish momentum).

- **Scalping/intraday**: On lower timeframes (e.g., 10min), use early Band 1 signals with expansion for quick moves.

- **Swing/position trading**: Wait for Band 3 extreme breakout + colored background for higher-probability, larger moves.

- **Risk management**: Place stops near basis or inner band; trail using outer bands during expansions.

Overall, this indicator excels at turning volatility into actionable, staged signals with visual simplicity—ideal for traders seeking an edge in identifying real explosive trends over noise. It's particularly powerful on volatile stocks like AMD/INTC or indices during news/events.

Trinity Real Move Detector DashboardRelease Notes (critical)

1. This code "will" require tweaks for different timeframes to the multiplier, do not assume the data in the table is accurate, cross check it with the Trinity Real Move Detector or another ATR tool, to validate the values in the table and ensure you have set the correct values.

2. I mention this below. But please understand that pine code has a limitation in the number of security calls (40 request.security() calls per script). This code is on the limit of that threshold and I would encourage developers to see if they can find a way around this to improve the script and release further updates.

What do we have...

The Trinity Real Move Detector Dashboard is a powerful TradingView indicator designed to scan multiple assets at once and show when each one has genuine short-term volatility "energy" — the kind that makes directional options trades (especially 0DTE or short-dated) have a high probability of follow-through, and can be used for swing trading as well. It combines a simple ATR-based volatility filter with a SuperTrend-style bias to tell you not only if the market is "awake" but also in which direction the momentum is leaning.

At its core, the indicator calculates the current ATR on your chosen timeframe and compares it to a user-defined percentage of the asset's daily ATR. When the short-term ATR spikes above that threshold, it signals "enough energy" — meaning the underlying is moving with real force rather than choppy noise. The SuperTrend logic then determines bullish or bearish bias, so the status shows "BULLISH ENERGY" (green) or "BEARISH ENERGY" (red) when energy is on, or "WAIT" when it's not. It also counts how many bars the energy has been active and shows the current ATR vs threshold for quick visual confirmation.

The dashboard displays all this in a clean table with columns for Symbol, Multiplier, Current ATR, Threshold, Status, Bars Active, and Bias (UP/DOWN). It's perfect for 3-minute charts but works on any timeframe — just adjust the multiplier based on the hints in the settings.

Editing symbols and multipliers is straightforward and user-friendly. In the indicator settings, you'll see numbered inputs like "1. Symbol - NVDA" and "1. Multiplier". To change an asset, simply type the new ticker in the symbol field (e.g., replace "NVDA" with "TSLA", "AVGO", or "ADAUSD"). You can also adjust the multiplier for each asset individually in the corresponding "Multiplier" field to make it more or less sensitive — lower numbers give more signals, higher numbers give stricter, higher-quality ones. This lets you customize the dashboard to your watchlist without any coding. For example, if you switch to a 4-hour chart or a slower-moving stock like AVGO, you may need to raise the multiplier (e.g., to 0.3–0.4) to avoid false "bullish" signals during minor bounces in a larger downtrend.

One important note about the multiplier and timeframes: the default values are optimized for fast intraday charts (like 3-minute or 5-minute). On higher timeframes (15-minute, 1-hour, 4-hour, or daily), the SuperTrend bias can be too sensitive with low multipliers (1.0 default in the code), leading to situations like the AVGO 4-hour example — where price is clearly downtrending, but the dashboard shows "BULLISH ENERGY" because the tight bands flip on small bounces. To fix this, you need to manually increase the multiplier for that asset (or all assets) in the settings. For 4-hour or daily charts, 0.25–0.35 is often better to match smoother SuperTrend indicators like Trinity. Always test on your timeframe and asset — crypto usually needs slightly lower multipliers than stocks due to higher volatility.

TradingView has a hard limit of 40 request.security() calls per script. Each asset in the dashboard requires several calls (current ATR, daily ATR, SuperTrend components, etc.), so with the full ATR-based bias, you can safely monitor about 6–8 assets before hitting the limit. Adding more symbols increases the number of calls and will trigger the "too many securities" error. This is a platform restriction to prevent excessive server load, and there's no official way around it in a single script. Some advanced coders use tricks like caching or lower-timeframe requests to squeeze in a few more, but for reliability, sticking to 6–8 assets is recommended. If you need more, the common workaround is to create two separate indicators (e.g., one for stocks, one for crypto) and add both to the same chart.

Overall, this dashboard gives you a professional-grade multi-asset scanner that filters out low-energy noise and highlights real momentum opportunities across stocks and crypto — all in one glance. It's especially valuable for options traders who want to avoid theta decay on weak moves and only strike when the market has true fuel. By tweaking the per-symbol multipliers in the settings, you can perfectly adapt it to any timeframe or asset behavior, avoiding issues like the AVGO false bullish signal on higher timeframes.

ATR Trailing StopATR Trailing Stop (Dynamic Volatility Regimes)

==============================================

This indicator implements an adaptive ATR-based trailing stop for long positions. The stop automatically adjusts based on stock volatility, tightening during fast movements and widening during calm periods. It is designed as a trade management tool to help protect profits while staying aligned with strong trends.

How It Works

------------

* Tracks the highest high over a configurable lookback window and ensures this “top” never moves downward.

* Computes the trailing stop as:**Top – ATR × Dynamic Multiplier**

* The ATR multiplier changes depending on volatility:

* Low volatility → Wide stop (slower trailing)

* Medium volatility → Standard trailing

* High volatility → Tight stop (faster trailing)

* The trailing stop only moves upward; it never decreases.

* If price falls significantly below the stop (default: 5%), the system resets and begins trailing from a new top.

* An optional price-scale label displays:

* Current stop value

* Volatility regime (LOW / MID / HIGH)

* ATR percentage and active multiplier

Alerts

------

Two alert conditions are included:

### Trailing Stop – Near

Triggers when price moves within a user-defined percentage above the stop.

### Trailing Stop – Hit

Triggers when price touches or closes below the stop.

How to Use

----------

1. Add the indicator to any chart (daily timeframe recommended).

2. Configure:

* ATR length

* Lookback bars

* Volatility thresholds

* ATR multipliers

3. Set alerts for early warnings or stop-hit events.

4. Use the stop line as a dynamic risk-management tool to guide exit decisions and protect profits.

Notes

-----

* Designed for long-only trailing logic.

* This indicator does not generate entry signals; it is intended for stop management.

Golden Volume Lines📌 Golden Volume — Lines (Golden Team)

Golden Volume — Lines is an advanced volume-based indicator that detects Ultra High Volume candles using a statistical percentile model, then automatically draws and tracks key price levels derived from those candles.

The indicator highlights where real market interest and liquidity appear and shows how price reacts when those levels are broken.

🔍 How It Works

Volume Measurement

Choose between:

Units (raw volume)

Money (Volume × Average Price)

Average price can be calculated using HL2 or OHLC4.

Percentile-Based Classification

Volume is classified into:

Medium

High

Ultra High Volume

Thresholds are calculated using a rolling percentile window.

Ultra Volume candles are colored orange.

Dynamic High & Low Levels

For every Ultra Volume candle:

A High and Low dotted line is drawn.

Lines extend to the right until price breaks them.

Smart Line Break Detection (Wick-Based)

A line is considered broken when price wicks through it.

When a break occurs:

🟧 Orange line → broken by an Ultra Volume candle

⚪ White line → broken by a normal candle

The line stops exactly at the breaking candle.

🔔 Alerts

Alert on Ultra High Volume candles

Alert when a High or Low line is broken

Separate alerts for:

Break by Ultra Volume candle

Break by Normal candle

🎯 Use Cases

Breakout & continuation confirmation

Liquidity sweep detection

Volume-validated support & resistance

Market reaction after extreme participation

⚙️ Key Inputs

Volume display mode (Units / Money)

Percentile thresholds

Lookback window size

Maximum number of active Ultra levels

Optional dynamic alerts

⚠️ Disclaimer

This indicator is a volume and market structure tool, not a standalone trading system.

Always use proper risk management and additional confirmation.

Relative Volume Bollinger Band %

The Relative Volume Bollinger Band % indicator is a powerful tool designed for traders seeking insights into volume, Bollinger band and relative strength dynamics. This indicator assesses the deviation of a security's trading volume relative to the Bollinger band % indicator and the RSI moving average. Together, these shed light on potential zones of interests where market shifts have a high probability of occurring.

Key Features:

Period: Tailor the indicator's sensitivity by adjusting the period of the smooth moving average and/or the period of the Bollinger band.

How it Works:

Moving Average Calculation: The script computes the simple moving average (SMA) of the relative strength over a defined period. When the higher SMA (orange line) is in the top grey zone, the security is in a zone where it has a high probability of becoming bullish. When the higher SMA is in the lower grey zone, the security is in a zone where it has a high probability of becoming bearish.

-Bollinger Band %: The script also computes the BB% which is primarily used to confirm overbought and oversold areas. When overbought, it turns white and remains white until the overbuying pressure is released indicating that the security is about to become bearish. The script indicates a bearish reversal when the BB% and RVOL bars are both red or when there are no more yellow RVOL bars, if present. When the BB% is<0 and rising, it will also appear white with yellow RVOL bars above. This is a good indication that bulls are beginning to enter buying positions. Confirmation here is indicated when the yellow RVOL bars change to green.

Relative Volume: The indicator then also normalizes the difference volume to indicate areas of high and low volatility. This shows where higher than normal volumes are being traded and can be used as a good indication of when to enter or exit a trade when the above criterions are met.

Visual Representation: The result is visually represented on the chart using columns. Bright green columns signify bullish relative volume values that are much greater than normal. Green columns signify bullish relative volume values that are significant. Red columns represent bearish values that are significant. Blue columns on the BB% indicator represent significant bullish buying in overbought areas. Red columns on the BB% indicator that are < 0 represent a bearish trend that is in an oversold area. This is there to prevent early entry into the market.

Enhancements:

Areas of Interest: Optionally, Areas of interest are represented by red, yellow and green circles on the higher SMA line, aiding in the identification of significant deviations.

Range-Weighted Volatility (Comparable)I wrote an indicator to measure volatility inside a range. It’s extremely useful for choosing a trading pair for grid strategies, because it lets you quickly, easily, and fairly identify which asset is the volatility leader. It measures volatility “fairly” relative to the asset’s trading range, not just by absolute price changes.

For example: if an asset trades in a 50–100 range and over a week it moves many, many times between 52 and 98, then it’s highly volatile. But if another asset trades in a 50–1000 range and makes the same 52–98 moves, its volatility is actually low — because the “weight” of that movement relative to the full range is small. The indicator accounts for this “movement weight” relative to the range, then sums these weights into a single number. That number makes it easy to judge whether an asset is suitable for a grid strategy.

That’s exactly what grids need: not just high volatility, but high volatility within a narrow range.

Settings: the Window (bars) field defines how many bars are used to calculate volatility. On a 5-minute chart, one week is 2016 bars (2460/57). By default, the script calculates over 30 days on 5-minute charts. The script also allows you to set a second symbol for comparison, so you can see both results on the same chart.

Написал индикатор для определения волатильности в диапазоне, очень-очень полезно для выбора торговой пары на гриде, позволяет легко и быстро и честно определить лидера по волатильности, при этом определяет ее "честно", относительно торгового диапазона, а не просто изменения цены.

Например если актив торгуется в диапазоне 50-100 и за неделю много-много раз сходил 52-98, то это очень волатильный актив, и в то же время если актив торгуется в диапазоне 50-1000 и сходил так же 52-98, то это будет низко волатильный актив, т.е. учитывается "вес" движения относительно диапазона и данные "веса" суммируются в одну единую цифру по которой и можно оценивать насколько актив подходит под грид стратегию.

А ведь именно это для гридов и нужно, не просто высокая волатильность, а именно высокая волатильность в узком диапазоне.

Касательно настроек , в поле Windows (bars) задается количество баров по которым скрипт будет считать волатильность, на 5-ти минутки неделя это 2016 (24*60/5*7), стандартно скрипт считает за 30 дней на 5-ти минутки. + в самом скрипте можно указать вторую пару для сравнения чтоб на одном графике увидеть результат.