Sigma Trinity ModelAbstract

Sigma Trinity Model is an educational framework that studies how three layers of market behavior interact within the same trend: (1) structural momentum (Rasta), (2) internal strength (RSI), and (3) continuation/compounding structure (Pyramid). The model deliberately combines bar-close momentum logic with intrabar, wick-aware strength checks to help users see how reversals form, confirm, and extend. It is not a signal service or automation tool; it is a transparent learning instrument for chart study and backtesting.

Why this is not “just a mashup”

Many scripts merge indicators without explaining the purpose. Sigma Trinity is a coordinated, three-engine study designed for a specific learning goal:

Rasta (structure): defines when momentum actually flips using a dual-line EMA vs smoothed EMA. It gives the entry/exit framework on bar close for clean historical study.

RSI (energy): measures internal strength with wick-aware triggers. It uses RSI of LOW (for bottom touches/reclaims) and RSI of HIGH (for top touches/exhaustion) so users can see intrabar strength/weakness that the close can hide.

Pyramid (progression): demonstrates how continuation behaves once momentum and strength align. It shows the logic of adds (compounding) as a didactic layer, also on bar close to keep historical alignment consistent.

These three roles are complementary, not redundant: structure → strength → progression.

Architecture Overview

Execution model

Rasta & Pyramid: bar close only by default (historically stable, easy to audit).

RSI: per tick (realtime) with bar-close backup by default, using RSI of LOW for entries and RSI of HIGH for exits. This makes the module sensitive to intra-bar wicks while still giving a close-based safety net for backtests.

Stops (optional in strategy builds): wick-accurate: trail arms/ratchets on HIGH; stop hit checks with LOW (or Close if selected) with a small undershoot buffer to avoid micro-noise hits.

Visual model

Dual lines (EMA vs smoothed EMA) for Rasta + color fog to see direction and compression/expansion.

Rungs (small vertical lines) drawn between the two Rasta lines to visualize wave spacing and rhythm.

Clean labels for Entry/Exit/Pyramid Add/RSI events. Everything is state-locked to avoid spamming.

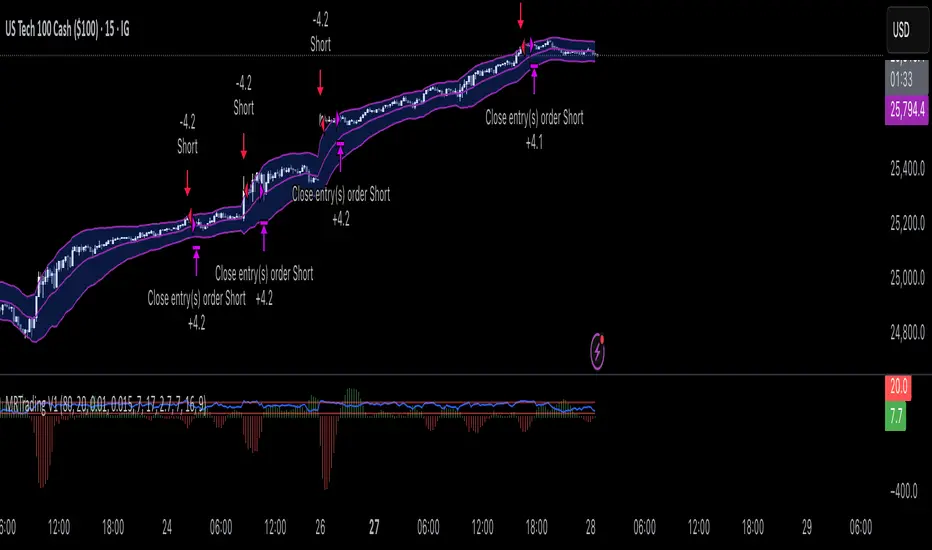

Module 1 — Rasta (Structural Momentum Layer)

Goal: Identify structural momentum reversals and maintain a consistent, replayable backbone for study.

Method:

Compute an EMA of a chosen price source (default Close), and a smoothed version (SMA/EMA/RMA/WMA/None selectable).

Flip points occur when the EMA line crosses the smoothed line.

Optional EMA 8/21 trend filter can gate entries (long-bias when EMA8 > EMA21). A small “adaptive on flip” option lets an entry fire when the filter itself flips to ON and the EMA is already above the smoothed line—useful for trend resumption.

Why bar close only?

Bar-close Rasta gives a stable, auditable timeline for the structure of the trend. It teaches users to separate “structure” (close-resolved) from “energy” (intrabar, via RSI).

Visuals:

Fog between the lines (green/red) to show regime.

Rungs between lines to show spread (compression vs expansion).

Optional plotting of EMA8/EMA21 so users can see the gating effect.

Module 2 — RSI (Internal Strength / Energy Layer)

Goal: Reveal the intrabar strength/weakness that often precedes or confirms structural flips.

Method:

Standard RSI with adjustable length and signal smoothing for the panel view.

Logic uses wick-aware sources:

Entry trigger: RSI of LOW (same RSI length) touching or below a lower band (default 15). Think of it as intraband reactivation from the bottom, using the candle’s deepest excursion.

Exit trigger: RSI of HIGH touching or above an upper band (default 85). Think of it as exhaustion at the top, using the candle’s highest excursion.

Realtime + Close Backup: fires intrabar on tick, but if the realtime event was missed, the close backup will note it at bar end.

Cooldown control: optional bars-between-signals to avoid rapid re-triggers on choppy sequences.

Why wick-aware RSI?

A close-only RSI can miss the true micro-extremes that cause reversals. Using LOW/HIGH for triggers captures the behavior that traders actually react to during the bar, while the bar-close backup preserves historical reproducibility.

Module 3 — Pyramid (Continuation / Compounding Layer)

Goal: Teach how continuation behaves once a trend is underway, and how adds can be structured.

Method:

Same dual-line logic as Rasta (EMA vs smoothed EMA), but only fires when already in a position (or after prior entry conditions).

Supports the same EMA 8/21 filter and optional adaptive-on-flip behavior.

Bar close only to maintain historical cohesion.

What it teaches:

Adds tend to cluster when momentum persists.

Students can experiment with add spacing and compare “one-shot entries” vs “laddered adds” during strong regimes.

How the Pieces Work Together

Rasta establishes the structural frame (when the wave flip is real enough to record at close).

RSI validates or challenges that structure by tracking intrabar energy at the extremes (low/high touches).

Pyramid shows what sustained continuation looks like once (1) and (2) align.

This produces a layered view: Structure → Energy → Progression. Users can see when all three line up (strongest phases) and when they diverge (riskier phases or transitions).

How to Use It (Step-by-Step)

Quick Start

Apply script to any symbol/timeframe.

In Strategy/Indicator Properties:

Enable On every tick (recommended).

If available, enable Using bar magnifier and choose a lower resolution (e.g., 1m) to simulate intrabar fills more realistically.

Keep On bar close unchecked if you want to observe realtime logic in live charts (strategies still place orders on close by platform design).

Default behavior: Rasta & Pyramid = bar close; RSI = per tick with close backup.

Reading the Chart

Watch for Rasta Entry/Exit labels: they define clean structural turns on close.

Watch RSI Entry (LOW touch at/below lower band) and RSI Exit (HIGH touch at/above upper band) to gauge internal energy extremes.

Pyramid Add labels reveal continuation phases once a move is already in progress.

Tuning

Rasta smoothing: choose SMA/EMA/RMA/WMA or None. Higher smoothing → later but cleaner flips; lower smoothing → earlier but choppier.

RSI bands: a common educational setting is 15/85 for strong extremes; 20/80 is a bit looser.

Cooldown: increase if you see too many RSI re-fires in chop.

EMA 8/21 filter: toggle ON to study “trend-gated” entries, OFF to study raw momentum flips.

Backtesting Notes (for Strategy Builds)

Stops (optional): trail is armed when price advances by a trigger (default D–F₀), ratchets only upward from HIGH, and hits from LOW (or Close if chosen) with a tiny undershoot buffer to avoid micro-wicks.

Order sequencing per bar (mirrors the script’s code comments):

Trail ratchet via HIGH

Intrabar stop hit via LOW/CLOSE → immediate close

If still in position at bar close: process exits (Rasta/RSI)

If still in position at bar close: process Pyramid Add

If flat at bar close: process entries (Rasta/RSI)

Platform reality: strategies place orders at bar close in historical testing; the intrabar logic improves realism for stops and event marking but final order timestamps are still close-resolved.

Inputs Reference (common)

Modules: enable/disable RSI and Pyramid learning layers.

Rasta: EMA length, smoothing type/length, EMA8/21 filter & adaptive flip, fog opacity, rungs on/off & limit.

RSI: RSI length, signal MA length (panel), Entry band (LOW), Exit band (HIGH), cooldown bars, labels.

Pyramid: EMA length, smoothing, EMA8/21 filter & adaptive adds.

Execution: toggle Bar Close Only for Rasta/Pyramid; toggle Realtime + Close Backup for RSI.

Stops (strategy): Fixed Stop % (first), Fixed Stop % (add), Trail Distance %, Trigger rule (auto D–F₀ or custom), undershoot buffer %, and hit source (LOW/CLOSE).

What to Study With It

Convergence: how often RSI-LOW entry touches precede the next Rasta flip.

Divergence: cases where RSI screams exhaustion (HIGH >= upper band) but Rasta hasn’t flipped yet—often transition zones.

Continuation: how Pyramid adds cluster in strong moves; how spacing changes with smoothing/filter choices.

Regime changes: use EMA8/21 filter toggles to see what happens at macro turns vs chop.

Limitations & Scope

This is a learning tool, not a trade copier. It does not provide financial advice or automated execution.

Intrabar results depend on data granularity; bar magnifier (when available) can help simulate lower-resolution ticks, but true tick-by-tick fills are a platform-level feature and not guaranteed across all symbols.

Suggested Publication Settings (Strategy)

Initial capital: 100

Order size: 100 USD (cash)

Pyramiding: 10

Commission: 0.25%

Slippage: 3 ticks

Recalculate: ✓ On every tick

Fill orders: ✓ Using bar magnifier (choose 1m or similar); leave On bar close unchecked for live viewing.

Educational License

Released under the Michael Culpepper Gratitude License (2025).

Use and modify freely for education and research with attribution. No resale. No promises of profitability. Purpose is understanding, not signals.

Strategia Pine Script®