AI Volume-KNN SuperTrend - by Trading Pine Lab🇬🇧 English

The AI Volume-KNN SuperTrend is an advanced trading strategy that combines the robustness of the SuperTrend indicator with a machine-learning inspired KNN (K-Nearest Neighbors) model. The baseline is built from a volume-weighted moving average with ATR-based bands, while the KNN classifier validates trend direction in real time. This dual-layer approach reduces false signals and improves trend confirmation.

Entries are triggered when the SuperTrend flips direction and the KNN classifier confirms the move as bullish or bearish. Exits are managed with a dynamic trailing stop, automatically adjusting to SuperTrend ± ATR × factor. The strategy includes visual markers for AI start/continuation signals, as well as customizable coloring for bullish, bearish, and neutral phases.

All parameters are fully configurable:

-Trading direction filter: Long / Short / Both.

-KNN settings: number of neighbors (K), dataset size (N).

-Label smoothing: price and SuperTrend smoothing lengths (WMAs).

-SuperTrend settings: length, ATR factor, and moving average source.

-Visualization: trend markers and per-trend coloring.

Volume

EMA inFusion Pro - Multiple SourcesEMA Fusion Pro: Dynamic Trend & Momentum Strategy with Three Exit Modes

EMA Fusion Pro is a highly customizable, multi-exit trend-following strategy designed for traders who value both precision and flexibility. By leveraging exponential moving averages (EMA), average directional index (ADX), and volume analysis, this strategy aims to capture trending market moves while offering three distinct exit modes for optimal risk management across varying market conditions.

Strategy Overview

This strategy systematically identifies potential entry points using a moving average crossover with highly configurable data sources (including price, volume, rate of change, or their Heikin Ashi versions) and filters signal quality with ADX trend strength and volume spikes. Each trade is managed with one of three advanced exit methodologies—reverse signal, ATR-based stop/take profit, or fixed percentage—giving you the control to adapt your risk profile to different market regimes.

Key Features

Customizable EMA Source: Calculate the core trend-filtering EMA from price (default), volume, rate of change, or their Heikin Ashi counterparts for unique market perspectives.

Trend Filter with ADX: Confirm entries only when the trend is strong, as measured by the user-adjustable ADX threshold.

Volume Spike Confirmation: Optional filter to only take trades with above-average volume activity, reducing false signals.

Three Exit Modes:

Reverse Signal: Exit trades when a new, opposite entry signal occurs.

ATR-Based Stop/Take Profit: Dynamic risk management using multiples of the average true range (ATR) for both take profit and stop loss.

Percent-Based Stop/Take Profit: Fixed-percentage risk management with user-defined thresholds.

Visual Annotations: Signal markers, EMA line color-coded by source, trend background coloring, and optional ATR/percent-based TP/SL levels.

Info Panel: Real-time display of all core indicators, current trading mode, exit parameters, and position status for quick oversight.

How It Works

Entry Logic: A crossover signal (above/below the EMA) triggers a new entry, but only if both ADX trend strength and (optionally) volume spike conditions are met.

Exit Logic: Three selectable modes allow you to exit trades on reverse signals, at a dynamic ATR-based profit or loss, or at a fixed percentage gain/loss.

Flexible Data Analysis: The EMA source can be chosen from six options—standard price, volume, rate of change, or their Heikin Ashi variants—allowing experimentation with different market dimensions.

Risk Management: All exits are precisely controlled, either by the next opposing signal, by volatility-adjusted levels, or by fixed risk/reward ratios.

Backtest & Optimization: The strategy is fully backtestable within TradingView’s Strategy Tester, with adjustable parameters for optimization.

Customization & Usage

Indicator Source: Select your preferred data type for EMA calculation, opening the door to creative strategy variations (e.g., volume momentum, pure price trend, rate of change divergence).

Filter Toggles: Enable/disable ADX and volume filters as desired—useful for different market environments.

Exit Mode Selection: Switch between reverse, ATR, or percent-based exits with a single parameter—ideal for adapting to ranging vs. trending markets.

Visual Clarity: The EMA line color reflects its underlying source, and the info panel summarizes all critical values for easy monitoring.

Who Should Use This Strategy?

Trend Followers seeking to ride strong moves with multiple exit options.

Experienced Traders who want to experiment with different data types (volume, momentum, Heikin Ashi) for trend analysis.

Algorithmic Traders looking for a robust, flexible base to build upon with their own ideas.

Getting Started

Apply the script to your chart and review default settings.

Customize parameters—EMA length, ADX threshold, volume settings, exit type—as desired.

Backtest on multiple instruments and timeframes to evaluate performance.

Optimize filters, exit rules, and risk parameters for your preferred trading style.

Monitor with the real-time info panel and trade alerts.

Disclaimer

This script is for educational and entertainment purposes only. It is not financial advice. Past performance is not indicative of future results. Always conduct thorough testing and consider your risk tolerance before trading real capital.

— Happy Trading —

Feel free to adapt, share, and contribute to this open-source strategy!

Breakout + Volume + HH/LL (Clean labels TP1-3)Breakout + Volume + HH/LL Strategy (Clean Labels)

This strategy combines breakout confirmation, volume strength, and market structure (Higher Highs / Lower Lows) to identify high-probability trade setups.

Breakout Filter: Uses a Donchian channel to detect price breakouts above resistance or below support.

Volume Confirmation: Requires volume to exceed the moving average of volume by a chosen multiplier, filtering out weak or false breakouts.

Market Structure: Long trades are only allowed if a Higher High (HH) has formed, and short trades only if a Lower Low (LL) has formed.

Trade Execution Rules:

For BUY trades: Entry at breakout, stop loss (SL) below the last pivot low, and three take profits (TP1–TP3) based on configurable risk-reward ratios.

For SELL trades: Entry at breakout, stop loss above the last pivot high, with TP1–TP3 levels set symmetrically below the entry.

Labels on Chart:

Each signal is marked with a clean label showing only:

Trade direction (BUY or SELL)

Entry price

Stop Loss

TP1, TP2, TP3

This makes the chart uncluttered while still providing all key trade information for execution or backtesting.

EMA and BB Analysis for US100 V250829This TradingView strategy generates buy and sell signals based on exponential moving average (EMA) crossovers, limited by other factors such as Bollinger Bands, volume, and EMA distance.

It uses EMAs of 16, 24, 32, and 64 periods, as well as the angles of each of these EMAs.

Entry Conditions:

EMA Crossover Entry:

When EMA16 crosses EMA64 and the following conditions are met:

EMA16, EMA24, EMA32 are aligned — for a buy signal:

EMA16 > EMA24

EMA24 > EMA32

EMA32 > EMA48

(and the opposite for a sell signal)

EMA Angles:

The angles of the EMAs must also follow the same alignment.

Divergence Entry:

When the distance between EMAs 16, 24, 32, and 48 increases.

Entry Limitations:

Once an entry is detected, it is filtered by several conditions:

When the distance between the entry candle and EMA96 is more than two candles of the maximum size over three periods.

The stop loss is set as two candles of the maximum size over three periods. If this stop loss exceeds 6,000 points (adjustable parameter), the entry is invalid.

When the price is at the edge of the Bollinger Band with a 1200-period setting (equivalent to a 1-hour Bollinger Band).

When the Bollinger Band's middle line is descending and a buy signal is triggered (and vice versa).

When volume drops below a certain threshold.

When a sideways market movement is detected.

All these entry limitations are configurable parameters and can be enabled or disabled.

Golden Cross + Support/Resistance + SL/TP + SignalsGolden Cross + Support/Resistance + SL/TP + Signals

Golden Cross + Support/Resistance + SL/TP + Signals

The Barking Rat PROThe Barking Rat PRO is designed around high/low pivot structure to capture meaningful market reversals. It intelligently identifies turning points by combining higher high/lower low (HH/LL) pivot detection, Fair Value Gap (FVG) confirmation, volatility-aware filters, and momentum checks. Unique features, such as a one-bar flip handler and a contextual ribbon overlay, provide traders with both clarity and precision. These tools help isolate high-probability setups while filtering out low-conviction signals, making trade opportunities easier to spot and act upon.

🧠 Core Logic: Structure-First, Filtered Reversals

The strategy takes a methodical, disciplined approach, prioritizing structural pivots over random signals. By layering multiple validation checks—structural pivots, gap confirmation, volatility filters, and momentum alignment—it highlights trades with high conviction while reducing exposure to noisy market conditions. The result is a clear, repeatable framework for reversal trading that can be applied across timeframes.

HH/LL Pivot Framework

Trades are triggered based on simple structural pivots: higher highs (HH) and lower lows (LL). When a structure flip occurs, the strategy either opens a new position or executes a one-bar delayed flip if an opposing position already exists. This ensures smooth transitions and avoids premature entries on minor market swings, keeping trading decisions focused on meaningful trend shifts.

Volatility & Distance Filters

To avoid low-quality trades, entries are validated against relative volatility, ensuring that pivots represent significant market movement. Trades must also be sufficiently spaced from previous entries and separated by a minimum number of bars, which prevents overtrading and clustered signals that can dilute performance.

Momentum Filter (RSI)

The strategy optionally aligns entries with momentum conditions using RSI. Long trades are favored when RSI is relatively low, suggesting potential exhaustion on the downside, while short trades are favored when RSI is relatively high, indicating potential overextension on the upside. This additional layer improves timing, helping traders avoid entering against strong, ongoing momentum.

Background Ribbon (Contextual Visuals)

A translucent ribbon overlays the chart to provide visual context of active trades. The ribbon displays volatility envelopes and position direction: green for long trades, red for short trades. It enhances clarity by giving traders a quick visual reference of the market environment without cluttering the chart.

Why These Parameters Were Chosen

The strategy focuses only on structurally meaningful pivots to ensure high-conviction trades.

Volatility filters confirm that trade signals are significant relative to recent price action, while FVG confirmation captures institutional-style imbalances.

Momentum and spacing rules prevent low-quality entries and overtrading, while the one-bar flip handler ensures seamless transitions when the structure reverses.

Ribbon overlays provide intuitive, real-time visualization of active trades and market context.

📈 Chart Visuals: Clear & Intuitive

- Green “▲” below a candle: Long entry triggered on LL → HH structure flip

- Red “▼” above a candle: Short entry triggered on HH → LL structure flip

- Translucent Ribbon: Green when long, Red when short

🔔 Alerts: Stay Notified Without Watching

The strategy supports real-time alerts on candle close, ensuring that only fully confirmed signals trigger notifications.

You must manually configure alerts within your TradingView account. Once set up, a single alert per instrument covers all relevant entries and exits, making hands-free monitoring simple and efficient.

⚙️ Strategy Report Properties

Position size: 25% of equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 25 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Aug 11, 2025 — Aug 28, 2025

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods

The strategy generates a sizeable number of trades, reducing reliance on a single outcome

Combined with conservative filters, the 25% setting offers a balance between aggression and control

Users are strongly encouraged to customize this to suit their risk profile.

🔍 What Makes This Strategy Unique?

HH/LL Pivot Focus: Trades pivot structure flips instead of relying on generic indicators.

Fair Value Gap Confirmation: Only pivots supported by FVGs are acted upon, reducing noise.

One-Bar Flip Handler: Ensures clean transitions when the structure reverses, avoiding same-bar conflicts.

Volatility & Spacing Filters: Trades require sufficient movement from prior entries and minimum bar spacing to maintain quality.

Momentum-Aware Entries: RSI alignment favors entries near potential exhaustion points, improving signal reliability.

Contextual Ribbon Overlay: Visualizes volatility and active positions clearly, without cluttering the chart.

Signalgo Strategy ISignalgo Strategy I: Technical Overview

Signalgo Strategy I is a systematically engineered TradingView strategy script designed to automate, test, and manage trend-following trades using multi-timeframe price/volume logic, volatility-based targets, and multi-layered exit management. This summary covers its operational structure, user inputs, entry and exit methodology, unique technical features, and practical application.

Core Logic and Workflow

Multi-Timeframe Data Synthesis

User-Defined Timeframe: The user chooses a timeframe (e.g., 1H, 4H, 1D, etc.), on which all strategy signals are based.

Cross-Timeframe Inputs: The strategy imports closing price, volume, and Average True Range (ATR) for the selected interval, independently from the chart’s native timeframe, enabling robust multi-timeframe analysis.

Price Change & Volume Ratio: It calculates the percent change of price per bar and computes a volume ratio by comparing current volume to its 20-bar moving average—enabling detection of true “event” moves vs. normal market noise.

Hype Filtering

Anti-Hype Mechanism: An entry is automatically filtered out if abnormal high volume occurs without corresponding price movement, commonly observed during manipulation or announcement periods. This helps isolate genuine market-driven momentum.

User Inputs

Select Timeframe: Choose which interval drives signal generation.

Backtest Start Date: Specify from which date historical signals are included in the strategy (for precise backtests).

Take-Profit/Stop-Loss Configuration: Internally, risk levels are set as multiples of ATR and allow for three discrete profit targets.

Entry Logic

Trade Signal Criteria:

Price change magnitude in the current bar must exceed a fixed sensitivity threshold.

Volume for the bar must be significantly elevated compared to average, indicating meaningful participation.

Anti-hype check must not be triggered.

Bullish/Bearish Determination: If all conditions are met and price change direction is positive, a long signal triggers. If negative, a short signal triggers.

Signal Debouncing: Ensures a signal triggers only when a new condition emerges, avoiding duplicate entries on flat or choppy bars.

State Management: The script tracks whether an active long or short is open to avoid overlapping entries and to facilitate clean reversals.

Exit Strategy

Take-Profits: Three distinct profit targets (TP1, TP2, TP3) are calculated as fixed multiples of the ATR-based stop loss, adapting dynamically to volatility.

Reversals: If a buy signal appears while a short is open (or vice versa), the existing trade is closed and reversed in a single step.

Time-Based Exit: If, 49 bars after entry, the trade is in-profit but hasn’t reached TP1, it exits to avoid stagnation risk.

Adverse Move Exit: The position is force-closed if it suffers a 10% reversal from entry, acting as a catastrophic stop.

Visual Feedback: Each TP/SL/exit is plotted as a clear, color-coded line on the chart; no hidden logic is used.

Alerts: Built-in TradingView alert conditions allow automated notification for both entries and strategic exits.

Distinguishing Features vs. Traditional MA Strategies

Event-Based, Not Just Slope-Based: While classic moving average strategies enter trades on MA crossovers or slope changes, Signalgo Strategy I demands high-magnitude price and volume confirmation on the chosen timeframe.

Volume Filtering: Very few MA strategies independently filter for meaningful volume spikes.

Real Market Event Focus: The anti-hype filter differentiates organic market trends from manipulated “high-volume, no-move” sessions.

Three-Layer Exit Logic: Instead of a single trailing stop or fixed RR, this script manages three profit targets, time-based closures, and hard adverse thresholds.

Multi-Timeframe, Not Chart-Dependent: The “main” analytical interval can be set independently from the current chart, allowing for in-depth cross-timeframe backtests and system runs.

Reversal Handling: Automatic handling of signal reversals closes and flips positions precisely, reducing slippage and manual error.

Persistent State Tracking: Maintains variables tracking entry price, trade status, and target/stop levels independently of chart context.

Trading Application

Strategy Sandbox: Designed for robust backtesting, allowing users to simulate performance across historical data for any major asset or interval.

Active Risk Management: Trades are consistently managed for both fixed interval “stall” and significant loss, not just via trailing stops or fixed-day closes.

Alert Driven: Can power algorithmic trading bots or notify discretionary traders the moment a qualifying market event occurs.

Script_Algo - ORB Strategy with Filters🔍 Core Concept: This strategy combines three powerful technical analysis tools: Range Breakout, the SuperTrend indicator, and a volume filter. Additionally, it features precise customization of the number of candles used to construct the breakout range, enabling optimized performance for specific assets.

🎯 How It Works:

The strategy defines a trading range at the beginning of the trading session based on a selected number of candles.

It waits for a breakout above the upper or below the lower boundary of this range, requiring a candle close.

It filters signals using the SuperTrend indicator for trend confirmation.

It utilizes trading volume to filter out false breakouts.

⚡ Strategy Features

📈 Entry Points:

Long: Candle close above the upper range boundary + SuperTrend confirmation

Short: Candle close below the lower range boundary + SuperTrend confirmation

🛡️ Risk Management:

Stop-Loss: Set at the opposite range boundary.

Take-Profit: Calculated based on a risk/reward ratio (3:1 by default).

Position Size: 10 contracts (configurable).

⚠️ IMPORTANT SETTINGS

🕐 Time Parameters:

Set the correct time and time zone!

❕ATTENTION: The strategy works ONLY with correct time settings! Set the time corresponding to your location and trading session.

📊 This strategy is optimized for trading TESLA stock!

Parameters are tailored to TESLA's volatility, and trading volumes are adequate for signal filtering. Trading time corresponds to the American session.

📈 If you look at the backtesting results, you can see that the strategy could potentially have generated about 70 percent profit on Tesla stock over six months on 5m timeframe. However, this does not guarantee that results will be repeated in the future; remain vigilant.

⚠️ For other assets, the following is required:

Testing and parameter optimization

Adjustment of time intervals and the number of candles forming the range

Calibration of stop-loss and take-profit levels

⚠️ Limitations and Drawbacks

🔗 Automation Constraints:

❌ Cannot be directly connected via Webhook to CFD brokers!

Additional IT solutions are required for automation, thus only manual trading based on signals is possible.

📉 Risk Management:

Do not risk more than 2-3% of your account per trade.

Test on historical data before live use.

Start with a demo account.

💪 Strategy Advantages

✅ Combined approach – multiple signal filters

✅ Clear entry and exit rules

✅ Visual signals on the chart

✅ Volume-based false breakout filtering

✅ Automatic position management

🎯 Usage Recommendations

Always test the strategy on historical data.

Start with small trading volumes.

Ensure time settings are correct.

Adapt parameters to current market volatility.

Use only for stocks – futures and Forex require adaptation.

📚 Suitable Timeframes - M1-M15

Only highly liquid stocks

🍀 I wish all subscribers good luck in trading and steady profits!

📈 May your charts move in the right direction!

⚠️ Remember: Trading involves risk. Do not invest money you cannot afford to lose!

Pump & Dump Strategy (seconds) w/ Candle Confirmation + ReverseStrategy for pump and dump. Look for > 1% price increment in seconds.

BDNS ORB Strategy v3BDNS Opening Range Breakout Strategy

What This Strategy Does This strategy implements an Opening Range Breakout (ORB) system that identifies the high and low prices during a customizable opening period, then trades breakouts above or below these levels with momentum confirmation. The strategy goes beyond basic ORB concepts by incorporating ADX momentum filtering, VWAP directional bias, dynamic position sizing, and sophisticated exit management including breakeven moves and trailing stops.

Core Strategy Logic

Opening Range Definition: The strategy tracks price action during a user-defined opening period (default: 9:30-9:35 AM ET for 5 minutes). During this time, blue horizontal lines appear marking the session high and low. A yellow background highlights this opening range period.

Breakout Detection: After the opening range completes, green and red horizontal lines appear showing the actual entry levels - these are offset from the range boundaries by a configurable number of ticks (default: 24 ticks) to filter out false breakouts and ensure committed moves.

Entry Conditions: Trades trigger when price breaks through these offset levels during the trading window (green background, default until 10:30 AM ET), but only when:

ADX momentum indicator exceeds threshold (default 24.0) in the breakout direction

Price relationship to VWAP confirms directional bias (when VWAP filter enabled)

Daily trade limits haven't been reached

Large range filtering conditions are met

Visual Elements and Usage

Range Lines: Blue lines show the actual opening range boundaries. These appear immediately when the opening session begins.

Entry Levels: Green (long) and red (short) lines show where trades will trigger, appearing after the opening range completes.

Information Table: A data table appears in the top-right showing real-time strategy status including range size in ticks, ADX readings, filter status, trade counts, and momentum conditions.

Position Management:

When in a trade, colored circles appear showing:

Lime circles: Long position targets (T1, T2, T3)

Orange circles: Short position targets

Red circles: Stop loss levels

Blue crosses: Breakeven levels (when that feature activates)

Purple lines: Trailing stop levels (when position 3 trailing activates)

Background Colors:

Yellow: Opening range session active

Green: Trading window active

Purple: Large range day detected

Gray: Large range day being skipped

Position Management System

The strategy uses a three-tier exit approach:

Position 1: Takes partial profits at first target (default 50% of range size)

Position 2: Exits at second target (default 100% of range size)

Position 3: Either exits at third target or uses trailing stop after Position 2 wins

Breakeven Feature: When enabled and price reaches the breakeven trigger level, all stop losses move to a more favorable breakeven level instead of the original stop, protecting against giving back profits.

Trailing Stop System: After Position 2 hits its target, Position 3 automatically switches to a trailing stop that moves in the trader's favor as price continues trending.

Customization for Different Instruments

The default settings are configured for MNQ (Micro NASDAQ futures) but the ORB concept is highly customizable for any futures instrument and timeframe. Range duration, breakout offsets, and filter thresholds should be adjusted based on the specific instrument's volatility characteristics and typical intraday patterns.

Filter Usage Guidelines

ADX Momentum Filter: Essential for avoiding breakouts during consolidation. Higher thresholds (30+) for trending markets, lower (20-25) for more opportunities.

VWAP Filter: Helpful in trending conditions but may reduce trade frequency. Better to disable during range-bound or mean-reverting periods.

Large Range Filter: Critical risk management tool. When the opening range exceeds your threshold:

Skip: Avoids trades when stops would be too large

Fade: Trades mean reversion back into the range

Trade: Takes breakouts regardless (higher risk)

Range Size Considerations: Setting a large range threshold (200-400 ticks) helps avoid days when both sides of the range get tested before any meaningful breakout occurs, which often leads to whipsaws.

Risk Management Features

Dynamic Stops and Targets: All exit levels scale with the opening range size, ensuring risk/reward remains consistent regardless of daily volatility. A 100-tick range day will have proportionally smaller stops than a 300-tick range day.

Position Sizing: Configure contract amounts for each position tier based on account size and risk tolerance.

Daily Trade Limits: Prevents overtrading by limiting trades per direction per day.

Breakout Offset: The tick offset from range boundaries is crucial - too small creates false signals, too large misses good moves. Test different values based on your instrument's typical noise levels.

Advanced Features

Large Third Target: Set Target 3 to 300-500% to essentially hold runners indefinitely, using the trailing stop as the primary exit method for capturing extended trends.

Fade Trading: On large range days, the strategy can trade mean reversion when initial breakouts fail, often providing good counter-trend opportunities.

Time-Based Exits: All positions close at the end of the trading window, preventing overnight risk.

Strategy Properties Used

Initial Capital: $5,000 (realistic for micro contract trading)

Commission: $0.50 per contract (realistic retail rates)

Position Size: 100% of equity (manages risk through contract quantities and stop placement)

Default quantities: 3/1/1 contracts across the three positions

The default settings assume larger account sizes or proprietary trading firm accounts where higher risk tolerance is acceptable. With MNQ at $0.50 per tick, a typical 200-tick opening range with 75% stop loss (150 ticks) would risk $375 on a 5-contract position. For smaller retail accounts, consider reducing position sizes significantly - using only Position 1 (3 contracts) would risk $225, or even reducing to 1-2 total contracts to maintain appropriate risk levels relative to account size.

Getting Started Apply the strategy to your preferred instrument

Adjust the opening range time and duration for your market

Set appropriate breakout offset based on typical noise levels

Configure large range threshold based on your risk tolerance

Test filter combinations to find what works best for your trading style

Adjust contract quantities based on your account size and risk management rules

The strategy works best on liquid instruments with clear opening sessions and sufficient volatility to generate meaningful ranges. Results will vary significantly based on market conditions, parameter settings, and the specific instrument traded.

I warrant that the information created and published by by me here on TradingView is not prohibited, doesn't constitute investment advice, and isn't created solely for qualified investors.

TTE Elite Market SignalsWelcome to TTE Elite Market Signals Your very own personal trading assistant

Trading today demands more than intuition—it requires exclusive access to elite-level market intelligence and the discipline to act on high-probability signals. Every professional trader seeks that decisive advantage: the clarity and confidence that separates consistent profitability from market uncertainty. The financial markets show no mercy, demanding precision, logic, and strategy grounded in institutional-grade analysis.

Human judgment, while powerful, can be compromised by fatigue and emotion, leading to costly trading errors. This is precisely where TTE Elite Market Signals excels. Our sophisticated platform combines proven trading methodologies with advanced signal generation technology, delivering market intelligence that empowers you to identify optimal entry and exit opportunities while maintaining complete control over your trading decisions.

Revolutionary Signal Intelligence

TTE Elite Market Signals features adaptive learning technology that evolves with market conditions. It continuously refines its analysis, helping you identify higher-probability setups while providing the market intelligence needed for superior risk management.

Elite Analysis Modes

Our platform adapts its signal generation to match market personalities:

- Institutional Flow Mode (MM-hybrid): Identifies manipulation patterns and tracks smart money movement with exclusive institutional-grade precision

- Momentum Adaptive Mode: Rapidly adjusts analysis when volatility and momentum shift

- Conservative Precision Mode: Steady, risk-conscious signals for consistent performance

- Adaptive Intelligence Mode: Self-refining system that enhances signal quality over time from past trades (long term of use)

Comprehensive Signal Intelligence

TTE Elite Market Signals integrates multiple sophisticated analytical systems:

- Volume Profile analysis for exclusive institutional-level market insights

- Pattern recognition enhanced by machine learning algorithms

- Intelligent exit timing that identifies optimal profit-taking opportunities

- Protection against market manipulation tactics

- Position sizing guidance that scales with trading success

- Fibonacci based reversal logic

Perfect for Your Trading Evolution

Experienced traders appreciate our sophisticated market intelligence and institutional-grade analytics that provide genuine competitive advantages.

Developing traders benefit from intelligent signal analysis that handles complex market calculations while teaching professional-level market interpretation and risk management principles via visuals on chart and descriptive panel.

All timeframes supported—from scalping to swing trading, TTE Elite Market Signals adapts to your preferred trading style via several user input selections.

Two Elite Service Modes

1. Signal Intelligence Mode: Real-time market signals with AI-driven analysis and detailed trade rationale

2. Alert Precision Mode: High-probability setup notifications with comprehensive market context and risk parameters

The Exclusive Learning Advantage

What makes TTE Elite Market Signals exceptional: it maintains a comprehensive trade memory and identifies the highest-probability signals, adapts to changing volatility patterns, and continuously refines(does not repaint) its analysis to enhance your profit potential and trading accuracy.

Built-in Professional Protection

- Advanced manipulation detection safeguards against institutional market maker(MM) tactics

- Intelligent risk assessment adjusts signal confidence based on market conditions

- Progressive scaling guidance maximizes winners while minimizing losses(educational)

- Comprehensive oversight with customizable risk parameters

Experience the Elite Difference

TTE gives you visuals on the chart of past trades and live metrics results to see what actually work and what fails, to minimize unrealistic expectations. Just sit back and watch sophisticated algorithms work tirelessly on your behalf, identifying opportunities that others miss and alerting you as signals are generated. Transforming the stressful, emotional battlefield of trading into a systematic analytical approach.

Let the System Do the Heavy Lifting

While others struggle with analysis paralysis and emotional decision-making, you'll have access to signals that have already processed hundreds of data points, identified institutional patterns, and calculated optimal risk-reward scenarios for a far less stressful trading experience.

What Elite Traders Should Know

TTE Elite Market Signals represents cutting-edge signal generation technology designed for serious market education and skill development, but it is not a black box, nor perfect for all markets. It must be adjusted to yield optimal results. While our advanced capabilities and institutional-grade features provide significant analytical advantages, trading success requires discipline and proper execution. Markets evolve, and optimal results demand understanding of signal context.

Success with TTE Elite Market Signals comes from mastering our analytical modes and using the proper entry types such as breakout entry, machine learning(ML) entry etc, utilizing and selecting the most effective risk control to optimize it, and maintaining disciplined risk management.

Join the Elite Trading Revolution

This isn't just another signal service—it equips you with the tools to do proper market analysis displaying price movement and volume profile designed for serious traders who understand that consistent profitability comes from discipline, superior market intelligence and proper interpretation, not luck.

Trade smart, stay profitable, and achieve trading excellence.

Best TTE Settings

Trade Entry Types:

1st Best Breakout Entry(out perform all others when used alone)

2nd Best ML Entry by itself or + Pattern Entry Combined

Risk Management:

ATR Multiplier 2

Enable Master Size Control

Master Size Mode

Max Risk Per Trade % 2.5

Max Multiplier Cap 1.5

Enable Growth Scaling

Growth Scaling Mode-set to Time Based or Performance

Risk Management System- set to Hybrid

Enable ML System

ML Mode-set to Auto or Quantum Learning

ML Application Strategy-set to Universal All Entries

Enable Trend Continuation

Mode- Set to Standard

Independent Entry-stays unchecked(off)

Best Performing Instruments on TTE (will update list as more are adjusted and tested)

NVDA

AMD

AMZN

TSLA

SPY

QQQ

PLTR

FlowStateTrader FlowState Trader - Advanced Time-Filtered Strategy

## Overview

FlowState Trader is a sophisticated algorithmic trading strategy that combines precision entry signals with intelligent time-based filtering and adaptive risk management. Built for traders seeking to achieve their optimal performance state, FlowState identifies high-probability trading opportunities within user-defined time windows while employing dynamic trailing stops and partial position management.

## Core Strategy Philosophy

FlowState Trader operates on the principle that peak trading performance occurs when three elements align: **Focus** (precise entry signals), **Flow** (optimal time windows), and **State** (intelligent position management). This strategy excels at finding reversal opportunities at key support and resistance levels while filtering out suboptimal trading periods to keep traders in their optimal flow state.

## Key Features

### 🎯 Focus Entry System

**Support/Resistance Zone Trading**:

- Dynamic identification of key price levels using configurable lookback periods

- Entry signals triggered when price interacts with these critical zones

- Volume confirmation ensures genuine breakout/reversal momentum

- Trend filter alignment prevents counter-trend disasters

**Entry Conditions**:

- **Long Signals**: Price closes above support buffer, touches support level, with above-average volume

- **Short Signals**: Price closes below resistance buffer, touches resistance level, with above-average volume

- Optional trend filter using EMA or SMA for directional bias confirmation

### ⏰ FlowState Time Filtering System

**Comprehensive Time Controls**:

- **12-Hour Format Trading Windows**: User-friendly AM/PM time selection

- **Multi-Timezone Support**: UTC, EST, PST, CST with automatic conversion

- **Day-of-Week Filtering**: Trade only weekdays, weekends, or both

- **Lunch Hour Avoidance**: Automatically skips low-volume lunch periods (12-1 PM)

- **Visual Time Indicators**: Background coloring shows active/inactive trading periods

**Smart Time Features**:

- Handles overnight trading sessions seamlessly

- Prevents trades during historically poor performance periods

- Customizable trading hours for different market sessions

- Real-time trading window status in dashboard

### 🛡️ Adaptive Risk Management

**Multi-Level Take Profit System**:

- **TP1**: First profit target with optional partial position closure

- **TP2**: Final profit target for remaining position

- **Flexible Scaling**: Choose number of contracts to close at each level

**Dynamic Trailing Stop Technology**:

- **Three Operating Modes**:

- **Conservative**: Earlier activation, tighter trailing (protect profits)

- **Balanced**: Optimal risk/reward balance (recommended)

- **Aggressive**: Later activation, wider trailing (let winners run)

- **ATR-Based Calculations**: Adapts to current market volatility

- **Automatic Activation**: Engages when position reaches profitability threshold

### 📊 Intelligent Position Sizing

**Contract-Based Management**:

- Configurable entry quantity (1-1000 contracts)

- Partial close quantities for profit-taking

- Clear position tracking and P&L monitoring

- Real-time position status updates

### 🎨 Professional Visualization

**Enhanced Chart Elements**:

- **Entry Zone Highlighting**: Clear visual identification of trading opportunities

- **Dynamic Risk/Reward Lines**: Real-time TP and SL levels with price labels

- **Trailing Stop Visualization**: Live tracking of adaptive stop levels

- **Support/Resistance Lines**: Key level identification

- **Time Window Background**: Visual confirmation of active trading periods

**Dual Dashboard System**:

- **Strategy Dashboard**: Real-time position info, settings status, and current levels

- **Performance Scorecard**: Live P&L tracking, win rates, and trade statistics

- **Customizable Sizing**: Small, Medium, or Large display options

### ⚙️ Comprehensive Customization

**Core Strategy Settings**:

- **Lookback Period**: Support/resistance calculation period (5-100 bars)

- **ATR Configuration**: Period and multipliers for stops/targets

- **Reward-to-Risk Ratios**: Customizable profit target calculations

- **Trend Filter Options**: EMA/SMA selection with adjustable periods

**Time Filter Controls**:

- **Trading Hours**: Start/end times in 12-hour format

- **Timezone Selection**: Four major timezone options

- **Day Restrictions**: Weekend-only, weekday-only, or unrestricted

- **Session Management**: Lunch hour avoidance and custom periods

**Risk Management Options**:

- **Trailing Stop Modes**: Conservative/Balanced/Aggressive presets

- **Partial Close Settings**: Enable/disable with custom quantities

- **Alert System**: Comprehensive notifications for all trade events

### 📈 Performance Tracking

**Real-Time Metrics**:

- Net profit/loss calculation

- Win rate percentage

- Profit factor analysis

- Maximum drawdown tracking

- Total trade count and breakdown

- Current position P&L

**Trade Analytics**:

- Winner/loser ratio tracking

- Real-time performance scorecard

- Strategy effectiveness monitoring

- Risk-adjusted return metrics

### 🔔 Alert System

**Comprehensive Notifications**:

- Entry signal alerts with price and quantity

- Take profit level hits (TP1 and TP2)

- Stop loss activations

- Trailing stop engagements

- Position closure notifications

## Strategy Logic Deep Dive

### Entry Signal Generation

The strategy identifies high-probability reversal points by combining multiple confirmation factors:

1. **Price Action**: Looks for price interaction with key support/resistance levels

2. **Volume Confirmation**: Ensures sufficient market interest and liquidity

3. **Trend Alignment**: Optional filter prevents counter-trend positions

4. **Time Validation**: Only trades during user-defined optimal periods

5. **Zone Analysis**: Entry occurs within calculated buffer zones around key levels

### Risk Management Philosophy

FlowState Trader employs a three-tier risk management approach:

1. **Initial Protection**: ATR-based stop losses set at strategy entry

2. **Profit Preservation**: Trailing stops activate once position becomes profitable

3. **Scaled Exit**: Partial profit-taking allows for both security and potential

### Time-Based Edge

The time filtering system recognizes that not all trading hours are equal:

- Avoids low-volume, high-spread periods

- Focuses on optimal liquidity windows

- Prevents trading during news events (lunch hours)

- Allows customization for different market sessions

## Best Practices and Optimization

### Recommended Settings

**For Scalping (1-5 minute charts)**:

- Lookback Period: 10-20

- ATR Period: 14

- Trailing Stop: Conservative mode

- Time Filter: Major session hours only

**For Day Trading (15-60 minute charts)**:

- Lookback Period: 20-30

- ATR Period: 14-21

- Trailing Stop: Balanced mode

- Time Filter: Extended trading hours

**For Swing Trading (4H+ charts)**:

- Lookback Period: 30-50

- ATR Period: 21+

- Trailing Stop: Aggressive mode

- Time Filter: Disabled or very broad

### Market Compatibility

- **Forex**: Excellent for major pairs during active sessions

- **Stocks**: Ideal for liquid stocks during market hours

- **Futures**: Perfect for index and commodity futures

- **Crypto**: Effective on major cryptocurrencies (24/7 capability)

### Risk Considerations

- **Market Conditions**: Performance varies with volatility regimes

- **Timeframe Selection**: Lower timeframes require tighter risk management

- **Position Sizing**: Never risk more than 1-2% of account per trade

- **Backtesting**: Always test on historical data before live implementation

## Educational Value

FlowState serves as an excellent learning tool for:

- Understanding support/resistance trading

- Learning proper time-based filtering

- Mastering trailing stop techniques

- Developing systematic trading approaches

- Risk management best practices

## Disclaimer

This strategy is for educational and informational purposes only. Past performance does not guarantee future results. Trading involves substantial risk of loss and is not suitable for all investors. Users should thoroughly backtest the strategy and understand all risks before live trading. Always use proper position sizing and never risk more than you can afford to lose.

---

*FlowState Trader represents the evolution of systematic trading - combining classical technical analysis with modern risk management and intelligent time filtering to help traders achieve their optimal performance state through systematic, disciplined execution.*

Opening Range Breakout🚀 ORB – Optimized for Peak Performance 🚀

Catch the morning breakout moves with zero guesswork!

This plug-and-play Opening Range Breakout strategy is fully optimized ; no settings to tweak, no parameters to adjust.

✅ Pre-tuned for U.S. market open on 5-minute charts.

✅ Built-in risk management with stop loss, take profit, and one trade per day.

✅ Auto exit before market close to lock in gains and avoid late-day whipsaws.

Perfect for day traders who want to focus on execution, not experimentation.

Just load it, trade it, and let the strategy do the heavy lifting.

⚠ Disclaimer : Educational use only. Always backtest and paper trade before using with real capital.

Key Features

• No Guesswork – Pre-set with the best-performing configuration.

• Opening Range Breakout Logic – Identifies the early range of the market and trades strong breakouts.

• Strict Risk Management – Stop loss and take profit levels are automatically calculated from the range size.

• One Trade Per Day – Prevents overtrading and keeps the focus on quality setups.

• End-of-Day Auto Exit – Closes all open trades at 3:30 PM EST to avoid late-session volatility.

How It Works

1. Opening Range Calculation: At market open (9:30 AM EST), the strategy monitors opening range.

2. Breakout Entry: Monitors the breakouts with moment.

3. Risk & Profit Targets: Stop loss and take profit are calculated automatically based on the range size. Risk-to-reward ratio is set for balanced performance.

4. Trade Control: Only one trade per day (either long or short). All trades are force-closed at 3:30 PM EST.

Nifty Power -> Nifty 50 chart + EMA of RSI + avg volume strategyThis strategy works in 1 hour candle in Nifty 50 chart. In this strategy, upward trade takes place when there is a crossover of RSI 15 on EMA50 of RSI 15 and volume is greater than volume based EMA21. On the other hand, lower trade takes place when RSI 15 is less than EMA50 of RSI 15. Please note that there is no stop loss given and also that the trade will reverse as per the trend. Sometimes on somedays, there will be no trades. Also please note that this is an Intraday strategy. The trade if taken closes on 15:15 in Nifty 50. This strategy can be used for swing trading. Some pine script code such as supertrend and ema21 of close is redundant. Try not to get confused as only EMA50 of RSI 15 is used and EMA21 of volume is used. I am using built-in pinescript indicators and there is no special calculation done in the pine script code. I have taken numbars variable to count number of candles. For example, if you have 30 minuite chart then numbars variable will count the intraday candles accordingly and the same for 1 hour candles.

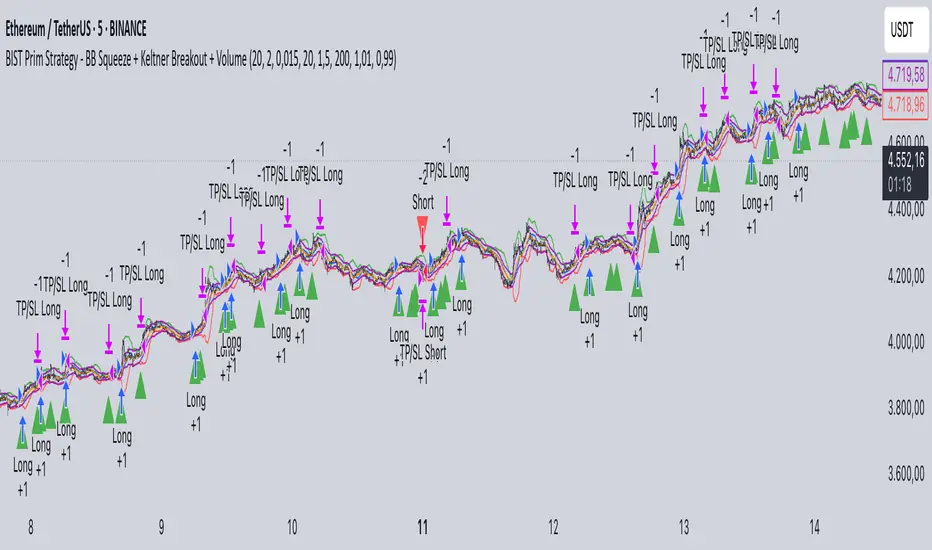

BB Squeeze + Keltner Breakout + VolumeHow the Strategy Works

Bollinger Bands Squeeze: The strategy first looks for a "squeeze" in the Bollinger Bands. This happens when the bands narrow significantly, indicating a period of low market volatility and potential consolidation. The bbSqueeze variable becomes true when the Bollinger Bandwidth falls below a set

AI Demand Strategy (Long Only) professionals.aiThe "AI Demand Strategy (Long Only) professionals.ai" is a TradingView strategy designed for USDT-based spot trading.

It focuses on long-only entries, incorporates optional trend filtering, and includes configurable risk-to-reward settings for exit targets.

It provides:

Customizable parameters for sensitivity, risk/reward ratio, and trend filtering

Automated entry and exit management

Stop-loss and take-profit level plotting on the chart

Visual buy/sell markers for trade signals

Optional SMA filter for trend confirmation

Built-in alert conditions to connect with external trading automation systems

This setup allows traders to visually monitor trade levels, backtest performance, and automate alerts without manually tracking market conditions.

MACD EMA 200 Strategy (Roche 5min Scalp)Free to use, stay blessed.

I don't believe charging for something that everyone can use.

Please enjoy it.

Intraday set up - RSI +MACDIntraday setup using RSI + MACD + Multi-Timeframe EMA 50 + Volume as confluence

Reversed Large Bars Strategy with Williams %RThis strategy script is ideal for volatile assets such as Natural Gas (NATGAS) or Crude Oil (WTI/Brent), which often exhibit strong price movements with high volume.

How It Works:

The strategy identifies short-term reversals after two consecutive large candles with significant volume, under specific conditions. It is based on the assumption that after strong directional moves, a temporary price exhaustion or reversal may occur.

Logic Breakdown:

Large Bar Detection:

A bar is considered “large” if its range (high – low) is significantly higher than the average (by a configurable percentage) and is accompanied by a spike in volume.

Two Consecutive Large Bars:

Entry is only considered when two large bars appear back-to-back — this strengthens the momentum signal.

Candle Type Filter:

For short entries: Two consecutive large bullish bars followed by a bullish candle → implies overextension upwards.

For long entries: Two consecutive large bearish bars followed by a bearish candle → implies overextension downwards.

Williams %R Filter:

The Williams %R oscillator adds confirmation based on overbought/oversold conditions:

Longs are allowed when %R is below the oversold level.

Shorts are allowed when %R is above the overbought level.

Ratio Logic:

A running percentage of bullish vs bearish large bars is tracked over a rolling period. This ensures entries are filtered based on broader context and trend dominance.

Stop Loss / Take Profit / Breakeven:

Each trade includes configurable SL/TP, and optional breakeven logic:

If unrealized profit exceeds a set percentage, SL is moved to entry (optionally with a buffer).

[Stratégia] VWAP Mean Magnet v9 (Simple Alert)This strategy is specifically designed for a ranging (sideways-moving) Bitcoin market.

A trade is only opened and signaled on the chart if all three of the following conditions are met simultaneously at the close of a candle:

Zone Entry

The price must cross into the signal zone: the red band for a Short (sell) position, or the green band for a Long (buy) position.

RSI Confirmation

The RSI indicator must also confirm the signal. For a Short, it must go above 65 (overbought condition). For a Long, it must fall below 25 (oversold condition).

Volume Filter

The volume on the entry candle cannot be excessively high. This safety filter is designed to prevent trades during risky, high-momentum breakouts.

Estrategia VWAP + RSI + SuperTrend (15m) con AlertasEstrategia para trading de Futuros en temporalidad de 15 minutos

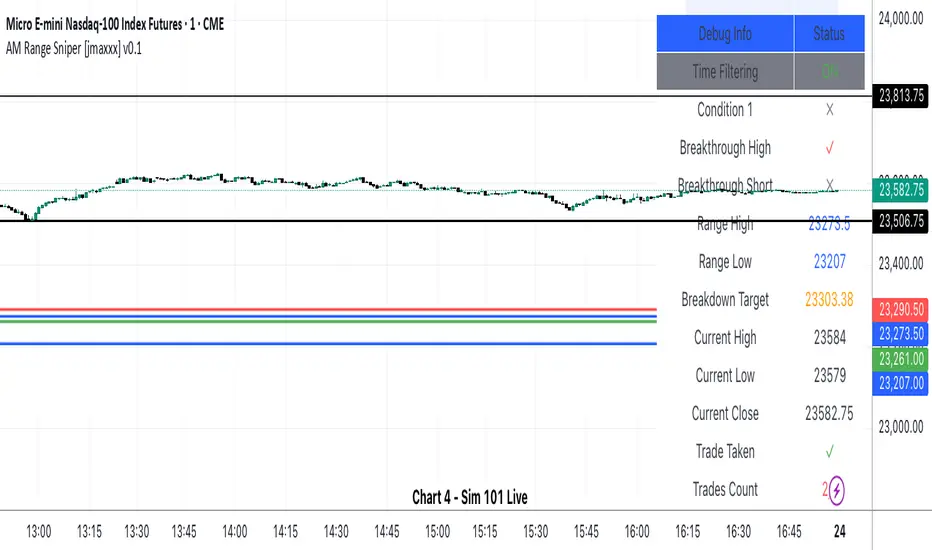

AM Range Sniper [jmaxxx]AM Range Sniper

Overview

AM Range Sniper is a sophisticated morning session trading strategy designed for Micro E-mini Nasdaq-100 Index Futures (MNQ). This strategy capitalizes on the critical 8:30-9:30 AM EST range formation period, implementing precise entry and exit mechanics with advanced risk management.

Key Features

🕐 Time-Based Range Analysis

Range Definition: Automatically identifies and tracks the 8:30-9:30 AM EST range

Trading Window: Active trading from 9:30 AM to 11:00 AM EST (extended for second chance trades)

Session Management: Daily reset ensures clean state for each trading session

🎯 Multiple Entry Patterns

Breakthrough/Retest: Captures price breakthroughs above range with retest opportunities

Long/Short Opportunities: Comprehensive coverage of both directional moves

Breakdown: Identifies bearish breakdowns below range support

Break Up: Detects bullish breakups above range resistance

Range Sweeps: Monitors for range high/low sweeps with reversal entries

⚡ Advanced Risk Management

Configurable Stop Losses: Tick-based stop losses for each trade type

Take Profit Targets: Automatic target calculations based on range size

Hard Close Protection: Automatic position closure at 4 PM EST

Second Chance Feature: Optional second trade opportunity if first trade loses

🔧 Professional Features

Visual Stop Loss Lines: Real-time stop loss visualization on chart

Debug Information Panel: Comprehensive status monitoring

Alert Integration: Customizable alert messages for entries/exits

Flexible Time Settings: Adjustable for different timezones

Strategy Logic

Range Formation (8:30-9:30 AM)

The strategy monitors the first hour of trading to establish the day's range. This range serves as the foundation for all subsequent trading decisions.

Entry Conditions

Breakthrough: Price breaks above range high with retest rejection

Breakdown: Price breaks below range low with confirmed bearish momentum

Break Up: Price breaks above range high with strong bullish confirmation

Sweep Entries: Range high/low sweeps followed by reversal signals

Risk Management

Stop Loss: Configurable tick-based stops for each trade type

Take Profit: 1.5x range size targets for breakdown/breakup trades

Position Sizing: Percentage-based position sizing

Session Limits: Maximum 2 trades per session (with second chance feature)

Settings & Customization

Core Parameters

Enable/disable individual entry patterns

Configurable stop loss levels (1-500 ticks)

Second chance feature toggle

Previous day level integration

Visual Customization

Customizable stop loss colors and widths

Debug panel visibility

Range line styling

Alert Configuration

Custom entry/exit alert messages

***** Automate With *****

APEX

NinjaTrader

Crosstrade.io ( promo code JMAXXX )

Performance & Reliability

Precision Focused: Waits for high-probability setups

Risk-Aware: Comprehensive stop loss and position management

Session-Based: Clean daily resets prevent carryover issues

Professional Grade: Designed for serious traders

Ideal For

Day Traders: Morning session specialists

Futures Traders: MNQ and similar instruments

Range Traders: Traders who capitalize on range breakouts

Risk-Conscious Traders: Those who prioritize risk management

Disclaimer

This strategy is for educational and informational purposes. Past performance does not guarantee future results. Always test thoroughly on historical data and paper trading before live implementation. Risk management is crucial - never risk more than you can afford to lose.

Created by jmaxxx - Professional trading strategy developer

For questions, feedback, or customization requests, please leave a comment below.