RTH & ETH VWAPs (Unified Style)AVWAP indicator showing only the current session. Shows ETH VWAP even when RTH is turned on. Has standard deviation and fills for settings.

Vwaps

SuperLazyTradeSuperLazyTrade transforms SuperTrend into a professional day-trading system with intelligent quality filtering.

Instead of showing every signal, it rates each setup on a 100-point scale analyzing:

- Signal Freshness - Catch moves early

- Volume Strength - Confirm momentum

- VWAP Alignment - Trade with institutions

- Volatility Regime - Optimal market conditions

- RSI Confirmation - Momentum validation

The system blocks 35-40% of low-quality signals automatically, enforcing discipline with clear verdicts:

✅ JUMP (80+) - Best setups

⚡ TRADE (65-79) - Strong entries

⚠️ CAUTION (55-64) - Proceed carefully

🟡 TREND (45-54) - Mid-trend opportunities

🔴 AVOID (0-44) - Skip it

Features live P&L tracking, professional 11-row dashboard, and anti-repainting architecture. Perfect for traders who value quality over quantity.

⚠️ DISCLAIMER

This indicator does not guarantee profits. Trading involves substantial risk of loss. Past performance is not indicative of future results. Use at your own risk.

Bollinger Bands + VWAP + 4-State MACD BackgroundBollinger Bands + VWAP + 4-State MACD Background

An all-in-one technical analysis indicator combining three proven tools with an intelligent momentum-based background visualization system.

📊 FEATURES

Bollinger Bands

Standard Bollinger Bands implementation with full customization options:

Adjustable period length (default: 20)

Multiple moving average types: SMA, EMA, SMMA (RMA), WMA, VWMA

Configurable standard deviation multiplier (default: 2.0)

Visual fill between bands to highlight volatility zones

Offset capability for forward/backward display

Session VWAP (Volume Weighted Average Price)

Automatically resets at the start of each trading session:

Calculates true volume-weighted average price

Resets daily to provide fresh reference levels

Customizable source input (default: HLC3)

Adjustable line appearance (color and width)

Can be toggled on/off as needed

4-State MACD Background System

This is the unique feature of this indicator. The chart background dynamically changes based on MACD momentum analysis, providing instant visual feedback on trend strength and direction:

🟢 Strong Bullish (Bright Green)

MACD line is above signal line

Histogram is growing (momentum accelerating upward)

Indicates strong upward momentum

🟢 Weak Bullish (Pale Green)

MACD line is above signal line

Histogram is shrinking (momentum decelerating)

Early warning signal that uptrend may be weakening

🔴 Strong Bearish (Bright Red)

MACD line is below signal line

Histogram is falling (momentum accelerating downward)

Indicates strong downward momentum

🔴 Weak Bearish (Pale Red)

MACD line is below signal line

Histogram is rising (momentum decelerating)

Early warning signal that downtrend may be weakening

🎯 HOW TO USE

For Trend Trading:

Strong colored backgrounds indicate confirmed momentum in that direction - consider staying with the trend

Weak colored backgrounds signal potential momentum exhaustion - watch for possible reversals

Use VWAP as a dynamic support/resistance level

Bollinger Band breakouts combined with strong MACD backgrounds can confirm trend strength

Price above VWAP + strong bullish background = bullish bias

Price below VWAP + strong bearish background = bearish bias

For Mean Reversion:

Price touching upper/lower Bollinger Bands with weak MACD background may suggest potential reversal

VWAP acts as a mean reversion anchor during range-bound sessions

Background color shifts from strong to weak often precede price direction changes

Look for price return to VWAP when extended beyond bands with weakening momentum

Signal Confirmation:

Strongest signals occur when multiple indicators align:

BB breakout + MACD strong color + price above/below VWAP

Price rejection at BB bands + MACD color weakening

VWAP support/resistance hold + MACD color change

⚙️ SETTINGS

All components are fully customizable through organized input groups:

Bollinger Bands Group:

Period length

Moving average type (SMA/EMA/SMMA/WMA/VWMA)

Source (close/open/high/low/etc.)

Standard deviation multiplier

Offset

VWAP Group:

Toggle show/hide

Source calculation method

Line color

Line width

MACD Group:

Toggle background on/off

Fast length (default: 12)

Slow length (default: 26)

Signal length (default: 9)

Source

Four separate color settings for each momentum state

All colors include transparency controls

💡 EDUCATIONAL VALUE

This indicator teaches important concepts:

How volatility (Bollinger Bands) relates to price movement

The importance of volume-weighted pricing (VWAP)

Momentum analysis through MACD

How combining multiple timeframes and indicators can provide confluence

The difference between trend strength and trend direction

⚠️ IMPORTANT NOTES

This indicator is for educational and informational purposes only

No indicator is perfect - always use proper risk management

Past performance does not guarantee future results

Combine with your own analysis and risk tolerance

Test thoroughly on historical data before live trading

This is not financial advice - use at your own risk

🔧 TECHNICAL DETAILS

Pine Script Version 6

Overlay indicator (displays on price chart)

All calculations use standard, well-documented formulas

Minimal lag due to efficient coding

Compatible with all timeframes and instruments

No repainting - all signals are confirmed on bar close

📝 CHANGELOG

Version 1.0

Initial release

Bollinger Bands with multiple MA types

Session VWAP with daily reset

4-state MACD background system

Full customization options

Developed for traders who want multiple confirmation signals in a clean, organized format without cluttering their charts with separate indicator panels.

VOLX+ VWAP Range BandsVOLX+ plots multiple VWAP-weighted high/low channels across different lookback periods to show how price behaves relative to short-term and long-term value zones.

Instead of using a single VWAP line, this tool creates four rolling VWAP envelopes:

Short-term range (fast reaction)

Mid-term range

Mid-mid range (transitional layer)

Long-term range (macro context)

Each band is computed as:

VWAP-High = SMA(high × volume, length) ÷ SMA(volume, length)

VWAP-Low = SMA(low × volume, length) ÷ SMA(volume, length)

This produces dynamic price channels that account for both price and traded volume, offering a clearer sense of where the market is accepting or rejecting value.

What It Shows

Four VWAP-weighted high/low bands

A short-term VWAP midline

Price line

Three SMAs for trend context

Optional visibility switches for each VWAP band

The filled regions between VWAP highs and lows create a layered “value map,” helping you interpret:

Trend continuation (price hugging outer VWAP bands)

Mean reversion (price returning toward inner bands)

Volatility contraction/expansion

Shifts in short-term vs long-term balance

🧠 How to Use

Use the short-term band for day-trading context or detecting short-term excess.

Use mid-term and mid-mid bands to confirm developing structure.

Use the long-term VWAP band to understand broader value zones.

Combine VWAP bands with SMAs and structure analysis for confluence.

This indicator is intended for price interpretation and analytical support.

✔ Does Not Repaint

The script uses rolling VWAP formulas and standard MAs; everything is stable and non-repainting.

Session VWAPs [cryptalent]This indicator provides a more granular and timely analysis of market structure compared to traditional daily Volume Weighted Average Price (VWAP). It splits the 24-hour trading day into four distinct, customizable sessions (T1, T2, T3, T4), calculating an independent Session VWAP and Standard Deviation Bands for each segment.

🌟 Key Features and Functionality

1. Segmented VWAP Calculation

Purpose: To track the true Volume Weighted Average Price (Fair Value) specific to the participants and trading activities within different global market sessions (e.g., Asian, European, US sessions).

Design: By default, the 24 hours (based on UTC time) are divided into T1 (00:00-06:00), T2 (06:00-12:00), T3 (12:00-20:00), and T4 (20:00-00:00).

Mechanism: The VWAP calculation resets at the start of each designated session, offering a clearer, segment-specific view of market consensus and volume absorption.

2. Standard Deviation Bands

Calculation: Each Session VWAP line is accompanied by upper and lower standard deviation bands.

Control: The width of these bands is controlled by the user input "Band Multiplier" (default is 1.0, representing one standard deviation).

Application: These bands measure the Volume-Weighted Volatility and define the expected "normal" trading range for the current session.

- Price within the bands suggests consolidation or a normal auction process.

- Price breaking out of the bands indicates strong directional momentum or an extreme/overbought/oversold condition for that specific session.

3. High Customization (User Inputs)

Session Timing: All four session start and end times (in UTC) are customizable, allowing traders to align the indicator with specific market hours or individual trading strategies.

Price Source: The source price used for the VWAP calculation is selectable (default is close).

💡 Trading Applications

1. Fair Value Identification: The VWAP line serves as the "Fair Value" or "Volume-Weighted Consensus Cost" for the active session.

Price above VWAP: Buyers are in control during that session.

Price below VWAP: Sellers are in control during that session.

2. Dynamic Support & Resistance: Both the VWAP and the Standard Deviation Bands often act as reliable dynamic support and resistance levels.

3. Volatility Assessment: The width of the bands reflects the volume-weighted volatility of the current session. Narrow bands suggest range-bound trading; wide bands imply strong directional activity.

4. Trend Strength: Sustained price action outside of the standard deviation bands is a key measure of the strength and commitment behind a current trend.

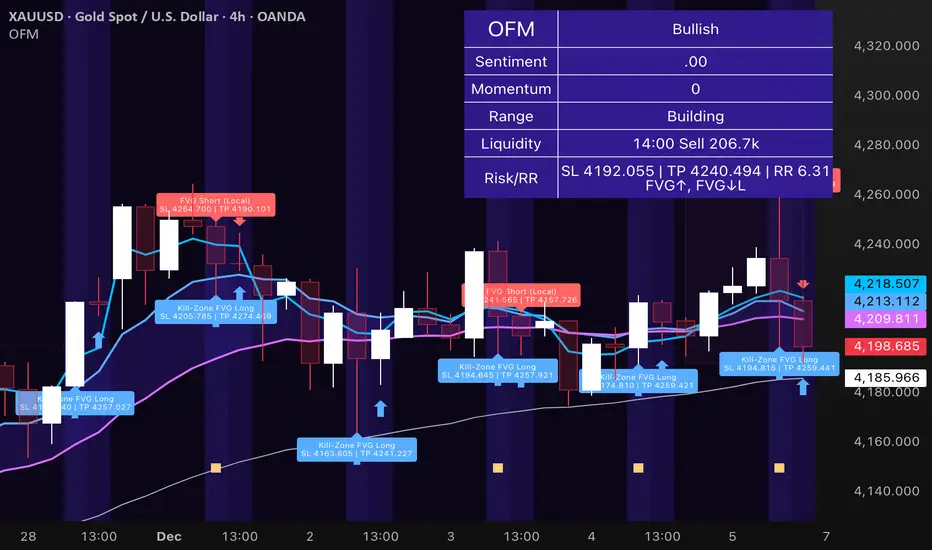

Obsidian Flux Matrix# Obsidian Flux Matrix | JackOfAllTrades

Made with my Senior Level AI Pine Script v6 coding bot for the community!

Narrative Overview

Obsidian Flux Matrix (OFM) is an open-source Pine Script v6 study that fuses social sentiment, higher timeframe trend bias, fair-value-gap detection, liquidity raids, VWAP gravitation, session profiling, and a diagnostic HUD. The layout keeps the obsidian palette so critical overlays stay readable without overwhelming a price chart.

Purpose & Scope

OFM focuses on actionable structure rather than marketing claims. It documents every driver that powers its confluence engine so reviewers understand what triggers each visual.

Core Analytical Pillars

1. Social Pulse Engine

Sentiment Webhook Feed: Accepts normalized scores (-1 to +1). Signals only arm when the EMA-smoothed value exceeds the `sentimentMin` input (0.35 by default).

Volume Confirmation: Requires local volume > 30-bar average × `volSpikeMult` (default 2.0) before sentiment flags.

EMA Cross Validation: Fast EMA 8 crossing above/below slow EMA 21 keeps momentum aligned with flow.

Momentum Alignment: Multi-timeframe momentum composite must agree (positive for longs, negative for shorts).

2. Peer Momentum Heatmap

Multi-Timeframe Blend: RSI + Stoch RSI fetched via request.security() on 1H/4H/1D by default.

Composite Scoring: Each timeframe votes +1/-1/0; totals are clamped between -3 and +3.

Intraday Readability: Configurable band thickness (1-5) so scalpers see context without losing space.

Dynamic Opacity: Stronger agreement boosts column opacity for quick bias checks.

3. Trend & Displacement Framework

Dual EMA Ribbon: Cyan/magenta ribbon highlights immediate posture.

HTF Bias: A higher-timeframe EMA (default 55 on 4H) sets macro direction.

Displacement Score: Body-to-ATR ratio (>1.4 default) detects impulses that seed FVGs or VWAP raids.

ATR Normalization: All thresholds float with volatility so the study adapts to assets and regimes.

4. Intelligent Fair Value Gap (FVG) System

Gap Detection: Three-candle logic (bullish: low > high ; bearish: high < low ) with ATR-sized minimums (0.15 × ATR default).

Overlap Prevention: Price-range checks stop redundant boxes.

Spacing Control: `fvgMinSpacing` (default 5) avoids stacking from the same impulse.

Storage Caps: Max three FVGs per side unless the user widens the limit.

Session Awareness: Kill zone filters keep taps focused on London/NY if desired.

Auto Cleanup: Boxes delete when price closes beyond their invalidation level.

5. VWAP Magnet + Liquidity Raid Engine

Session or Rolling VWAP: Toggle resets to match intraday or rolling preferences.

Equal High/Low Scanner: Looks back 20 bars by default for liquidity pools.

Displacement Filter: ATR multiplier ensures raids represent genuine liquidity sweeps.

Mean Reversion Focus: Signals fire when price displaces back toward VWAP following a raid.

6. Session Range Breakout System

Initial Balance Tracking: First N bars (15 default) define the session box.

Breakout Logic: Requires simultaneous liquidity spikes, nearby FVG activity, and supportive momentum.

Z-Score Volume Filter: >1.5σ by default to filter noisy moves.

7. Lifestyle Liquidity Scanner

Volume Z-Scores: 50-bar baseline highlights statistically significant spikes.

Smart Money Footprints: Bottom-of-chart squares color-code buy vs sell participation.

Panel Memory: HUD logs the last five raid timestamps, direction, and normalized size.

8. Risk Matrix & Diagnostic HUD

HUD Structure: Table in the top-right summarizes HTF bias, sentiment, momentum, range state, liquidity memory, and current risk references.

Signal Tags: Aggregates SPS, FVG, VWAP, Range, and Liquidity states into a compact string.

Risk Metrics: Swing-based stops (5-bar lookback) + ATR targets (1.5× default) keep risk transparent.

Signal Families & Alerts

Social Pulse (SPS): Volume-confirmed sentiment alignment; triangle markers with “SPS”.

Kill-Zone FVG: Session + HTF alignment + FVG tap; arrow markers plus SL/TP labels.

Local FVG: Captures local reversals when HTF bias has not flipped yet.

VWAP Raid: Equal-high/low raids that snap toward VWAP; “VWAP” label markers.

Range Breakout: Initial balance violations with liquidity and imbalance confirmation; circle markers.

Liquidity Spike: Z-score spikes ≥ threshold; square markers along the baseline.

Visual Design & Customization

Theme Palette: Primary background RGB (12,6,24). Accent shading RGB (26,10,48). Long accents RGB (88,174,255). Short accents RGB (219,109,255).

Stylized Candles: Optional overlay using theme colors.

Signal Toggles: Independently enable markers, heatmap, and diagnostics.

Label Spacing: Auto-spacing enforces ≥4-bar gaps to prevent text overlap.

Customization & Workflow Notes

Adjust ATR/FVG thresholds when volatility shifts.

Re-anchor sentiment to your webhook cadence; EMA smoothing (default 5) dampens noise.

Reposition the HUD by editing the `table.new` coordinates.

Use multiples of the chart timeframe for HTF requests to minimize load.

Session inputs accept exchange-local time; align them to your market.

Performance & Compliance

Pure Pine v6: Single-line statements, no `lookahead_on`.

Resource Safe: Arrays trimmed, boxes limited, `request.security` cached.

Repaint Awareness: Signals confirm on close; alerts mirror on-chart logic.

Runtime Safety: Arrays/loops guard against `na`.

Use Cases

Measure when social sentiment aligns with structure.

Plan ICT-style intraday rebalances around session-specific FVG taps.

Fade VWAP raids when displacement shows exhaustion.

Watch initial balance breaks backed by statistical volume.

Keep risk/target references anchored in ATR logic.

Signal Logic Snapshot

Social Pulse Long/Short: `sentimentEMA` gated by `sentimentMin`, `volSpike`, EMA 8/21 cross, and `momoComposite` sign agreement. Keeps hype tied to structural follow-through.

Kill-Zone FVG Long/Short: Requires session filter, HTF EMA bias alignment, and an active FVG tap (`bullFvgTap` / `bearFvgTap`). Labels include swing stops + ATR targets pulled from `swingLookback` and `liqTargetMultiple`.

Local FVG Long/Short: Uses `localBullish` / `localBearish` heuristics (EMA slope, displacement, sequential closes) to surface intraday reversals even when HTF bias has not flipped.

VWAP Raids: Detect equal-high/equal-low sweeps (`raidHigh`, `raidLow`) that revert toward `sessionVwap` or rolling VWAP when displacement exceeds `vwapAlertDisplace`.

Range Breakouts: Combine `rangeComplete`, breakout confirmation, liquidity spikes, and nearby FVG activity for statistically backed initial balance breaks.

Liquidity Spikes: Volume Z-score > `zScoreThreshold` logs direction, size, and timestamp for the HUD and optional review workflows.

Session Logic & VWAP Handling

Kill zone + NY session inputs use TradingView’s session strings; `f_inSession()` drives both visual shading and whether FVG taps are tradeable when `killZoneOnly` is true.

Session VWAP resets using cumulative price × volume sums that restart when the daily timestamp changes; rolling VWAP falls back to `ta.vwap(hlc3)` for instruments where daily resets are less relevant.

Initial balance box (`rangeBars` input) locks once complete, extends forward, and stays on chart to contextualize later liquidity raids or breakouts.

Parameter Reference

Trend: `emaFastLen`, `emaSlowLen`, `htfResolution`, `htfEmaLen`, `showEmaRibbon`, `showHtfBiasLine`.

Momentum: `tf1`, `tf2`, `tf3`, `rsiLen`, `stochLen`, `stochSmooth`, `heatmapHeight`.

Volume/Liquidity: `volLookback`, `volSpikeMult`, `zScoreLen`, `zScoreThreshold`, `equalLookback`.

VWAP & Sessions: `vwapMode`, `showVwapLine`, `vwapAlertDisplace`, `killSession`, `nySession`, `showSessionShade`, `rangeBars`.

FVG/Risk: `fvgMinTicks`, `fvgLookback`, `fvgMinSpacing`, `killZoneOnly`, `liqTargetMultiple`, `swingLookback`.

Visualization Toggles: `showSignalMarkers`, `showHeatmapBand`, `showInfoPanel`, `showStylizedCandles`.

Workflow Recipes

Kill-Zone Continuation: During the defined kill session, look for `killFvgLong` or `killFvgShort` arrows that line up with `sentimentValid` and positive `momoComposite`. Use the HUD’s risk readout to confirm SL/TP distances before entering.

VWAP Raid Fade: Outside kill zone, track `raidToVwapLong/Short`. Confirm the candle body exceeds the displacement multiplier, and price crosses back toward VWAP before considering reversions.

Range Break Monitor: After the initial balance locks, mark `rangeBreakLong/Short` circles only when the momentum band is >0 or <0 respectively and a fresh FVG box sits near price.

Liquidity Spike Review: When the HUD shows “Liquidity” timestamps, hover the plotted squares at chart bottom to see whether spikes were buy/sell oriented and if local FVGs formed immediately after.

Metadata

Author: officialjackofalltrades

Platform: TradingView (Pine Script v6)

Category: Sentiment + Liquidity Intelligence

Hope you Enjoy!

AMS Adaptive Supertrend Lite – ORB + VWAP 1.0AMS Adaptive Supertrend Lite – ORB + VWAP

This indicator focuses on providing a clean read of trend, structure, and opening range context without unnecessary complexity. It’s designed for traders who prefer straightforward visual tools that support their own decision-making process.

Consider this a small multi-tool for your basic ORB needs.

Included:

-Supertrend

A simple ATR-based Supertrend for directional context.

You can edit colors, line width, ATR settings, etc.

No signals or automation, just a clear trend reference.

-EMAs

Optional fast and slow EMAs for structural context.

Useful for gauging short-term momentum and slope.

-VWAP

A standard session VWAP.

You can style it however you like (solid, dashed, colored) in the Style tab.

-Opening Range (ORB)

Configurable ORB band including:

ORB duration (in minutes)

Optional RTH-only logic

Adjustable session window

Choice of timeframe used to build the ORB

Automatic hiding on higher timeframes (optional)

The ORB high/low are built on the selected lower timeframe and then displayed on the active chart.

-HTF Bias Shading (Optional)

A simple background tint based on EMA structure on a higher timeframe.

Meant to give gentle context, not trading signals.

Alerts

Two alerts are included:

Supertrend flipping bullish

Supertrend flipping bearish

These are notifications, not calls to action.

Intended Use

This is a visual tool for traders who want clear structure and context on their chart.

It does not provide entries, exits, strategies, or automated logic.

Disclaimer

This script is for educational and informational purposes only.

It is not financial advice, and no performance is guaranteed.

Always test tools for yourself and use proper risk management.

Range Lattice## RangeLattice

RangeLattice constructs a higher-timeframe scaffolding on any intraday chart, locking in structural highs/lows, mid/quarter grids, VWAP confluence, and live acceptance/break analytics. It provides a non-repainting overlay that turns range management into a disciplined process.

HOW IT WORKS

Structure Harvesting – Using request.security() , the script samples highs/lows from a user-selected timeframe (default 240 minutes) over a configurable lookback to establish the dominant range.

Grid Construction – Midpoint and quarter levels are derived mathematically, mirroring how institutional traders map distribution/accumulation zones.

Acceptance Detection – Consecutive closes inside the range flip an acceptance flag and darken the cloud, signaling balanced auction conditions.

Break Confirmation – Multi-bar closes outside the structure raise break labels and alerts, filtering the countless fake-outs that plague breakout traders.

VWAP Fan Overlay – Session VWAP plus ATR-based bands provide a live measure of flow centering relative to the lattice.

HOW TO USE IT

Range Plays : Fade taps of the outer rails only when acceptance is active and VWAP sits inside the grid—this is where mean-reversion works best.

Breakout Plays : Wait for confirmed break labels before entering expansion trades; the dashboard's Width/ATR metric tells you if the expansion has enough fuel.

Market Prep : Carry the same lattice from pre-market into regular trading hours by keeping the structure timeframe fixed; alerts keep you notified even when managing multiple tickers.

VISUAL FEATURES

Range Tap and Mid Pivot markers provide a tape-reading breadcrumb trail for journaling.

Cloud fill opacity tightens when acceptance persists, visually signaling balance compressions ready to break.

Dashboard displays absolute width, ATR-normalized width, and current state (Balanced vs Transitional) so you can glance across charts quickly.

Acceptance Flag toggle: Keep the repeated acceptance squares hidden until you need to audit balance.

PARAMETERS

Structure Timeframe (default: 240): Choose the timeframe whose ranges matter most (4H for indices, Daily for stocks).

Structure Lookback (default: 60): Bars sampled on the structure timeframe.

Acceptance Bars (default: 8): How many consecutive bars inside the range confirm balance.

Break Confirmation Bars (default: 3): Bars required outside the range to validate a breakout.

ATR Reference (default: 14): ATR period for width normalization.

Show Midpoint Grid (default: enabled): Display the midpoint and quarter levels.

Show Adaptive VWAP Fan (default: enabled): Toggle the VWAP channel for assets where volume distribution matters most.

Show Acceptance Flags (default: disabled): Turn the acceptance markers on/off for maximum visual control.

Show Range Dashboard (default: enabled): Disable if screen space is limited, re-enable during prep sessions.

ALERTS

The indicator includes five alert conditions:

Range High Tap: Price interacted with the RangeLattice high

Range Low Tap: Price interacted with the RangeLattice low

Range Mid Tap: Price interacted with the RangeLattice mid

Range Break Up: Confirmed upside breakout

Range Break Down: Confirmed downside breakout

Where it works best

This indicator works best on liquid instruments with clear structural levels. On very low timeframes (1-minute and below), the structure may update too frequently to be useful. The acceptance/break confirmation system requires patience—faster traders may find the multi-bar confirmation too slow for scalping. The VWAP fan is session-based and resets daily, which may not suit all trading styles.

FluxPulse Beacon## FluxPulse Beacon

FluxPulse Beacon applies a microstructure lens to every bar, combining directional thrust, realized volatility, and multi-timeframe liquidity checks to decide whether the tape is being pushed by real sponsorship or just noise. The oscillator's color-coded columns and adaptive burst thresholds transform complex flow dynamics into a single actionable flux score for futures and equities traders.

HOW IT WORKS

Momentum Extraction – Price differentials over a configurable pulse distance are smoothed using exponential moving averages to isolate directional thrust without reacting to single prints.

Volatility + Liquidity Normalization – The momentum stream is divided by realized volatility and multiplied by both local and higher-timeframe EMA volume ratios, ensuring pulses only appear when volatility and liquidity align.

Adaptive Thresholding – A volatility-derived standard deviation of flux is blended with the base threshold so bursts scale automatically between low-volatility and high-volatility market conditions.

Divergence Engine – Linear regression slopes compare price vs. flux to tag bullish/bearish divergences, highlighting stealth accumulation or distribution zones.

HOW TO USE IT

Continuation Entries : Go with the trend when histogram bars stay above the adaptive threshold, the signal line confirms, and trend bias agrees—this is where liquidity-backed follow-through lives.

Fade Plays : Watch for divergence alerts and shrinking compression values; when flux prints below zero yet price grinds higher, hidden selling pressure often precedes rollovers.

Session Filter : Compression percentage in the diagnostics table instantly tells you whether to trade thin overnight sessions—low compression means stand down.

VISUAL FEATURES

Dynamic background heat maps flux magnitude, while threshold lines provide a quick read on whether a pulse is statistically significant.

Diagnostics table displays live flux, signal, adaptive threshold, and compression for quick reference.

Alert-first workflow: The surface is intentionally clean—bursts and divergences are delivered via alerts instead of on-chart clutter.

PARAMETERS

Trend EMA Length (default: 34): Defines the macro bias anchor; increase for higher-timeframe confirmation.

Pulse Distance (default: 8): Controls how sensitive momentum extraction becomes.

Volatility Window (default: 21): Sample window for realized volatility normalization.

Liquidity Window (default: 55): Volume smoothing window that proxies liquidity expansion.

Liquidity Reference TF (default: 60): Select a higher timeframe to cross-check whether current volume matches institutional flows.

Adaptive Threshold (default: enabled): Disable for fixed thresholds on slower markets; enable for high-volatility assets.

Base Burst Threshold (default: 1.25): Minimum flux magnitude that qualifies as an actionable pulse.

ALERTS

The indicator includes four alert conditions:

Bull Burst: Detects upside liquidity pulses

Bear Burst: Detects downside liquidity pulses

Bull Divergence: Flags bullish delta divergence

Bear Divergence: Flags bearish delta divergence

LIMITATIONS

This indicator is designed for liquid futures and equity markets. Performance may degrade in low-volume or highly illiquid instruments. The adaptive threshold system works best on timeframes where sufficient volatility history exists (typically 15-minute charts and above). Divergence signals are probabilistic and should be confirmed with price action.

INSERT_CHART_SNAPSHOT_URL_HERE

---

## RangeLattice Mapper

RangeLattice Mapper constructs a higher-timeframe scaffolding on any intraday chart, locking in structural highs/lows, mid/quarter grids, VWAP confluence, and live acceptance/break analytics. It provides a non-repainting overlay that turns range management into a disciplined process.

HOW IT WORKS

Structure Harvesting – Using request.security() , the script samples highs/lows from a user-selected timeframe (default 240 minutes) over a configurable lookback to establish the dominant range.

Grid Construction – Midpoint and quarter levels are derived mathematically, mirroring how institutional traders map distribution/accumulation zones.

Acceptance Detection – Consecutive closes inside the range flip an acceptance flag and darken the cloud, signaling balanced auction conditions.

Break Confirmation – Multi-bar closes outside the structure raise break labels and alerts, filtering the countless fake-outs that plague breakout traders.

VWAP Fan Overlay – Session VWAP plus ATR-based bands provide a live measure of flow centering relative to the lattice.

HOW TO USE IT

Range Plays : Fade taps of the outer rails only when acceptance is active and VWAP sits inside the grid—this is where mean-reversion works best.

Breakout Plays : Wait for confirmed break labels before entering expansion trades; the dashboard's Width/ATR metric tells you if the expansion has enough fuel.

Market Prep : Carry the same lattice from pre-market into regular trading hours by keeping the structure timeframe fixed; alerts keep you notified even when managing multiple tickers.

VISUAL FEATURES

Range Tap and Mid Pivot markers provide a tape-reading breadcrumb trail for journaling.

Cloud fill opacity tightens when acceptance persists, visually signaling balance compressions ready to break.

Dashboard displays absolute width, ATR-normalized width, and current state (Balanced vs Transitional) so you can glance across charts quickly.

Acceptance Flag toggle: Keep the repeated acceptance squares hidden until you need to audit balance.

PARAMETERS

Structure Timeframe (default: 240): Choose the timeframe whose ranges matter most (4H for indices, Daily for stocks).

Structure Lookback (default: 60): Bars sampled on the structure timeframe.

Acceptance Bars (default: 8): How many consecutive bars inside the range confirm balance.

Break Confirmation Bars (default: 3): Bars required outside the range to validate a breakout.

ATR Reference (default: 14): ATR period for width normalization.

Show Midpoint Grid (default: enabled): Display the midpoint and quarter levels.

Show Adaptive VWAP Fan (default: enabled): Toggle the VWAP channel for assets where volume distribution matters most.

Show Acceptance Flags (default: disabled): Turn the acceptance markers on/off for maximum visual control.

Show Range Dashboard (default: enabled): Disable if screen space is limited, re-enable during prep sessions.

ALERTS

The indicator includes five alert conditions:

Range High Tap: Price interacted with the RangeLattice high

Range Low Tap: Price interacted with the RangeLattice low

Range Mid Tap: Price interacted with the RangeLattice mid

Range Break Up: Confirmed upside breakout

Range Break Down: Confirmed downside breakout

LIMITATIONS

This indicator works best on liquid instruments with clear structural levels. On very low timeframes (1-minute and below), the structure may update too frequently to be useful. The acceptance/break confirmation system requires patience—faster traders may find the multi-bar confirmation too slow for scalping. The VWAP fan is session-based and resets daily, which may not suit all trading styles.

---

AMS Adaptive Supertrend - v1.0The ATMOS MARKET SUITE (AMS) Adaptive Supertrend is a volatility-responsive trend framework designed to keep structural context clear across changing market conditions. It expands on the traditional Supertrend by incorporating ATR percentiles, regime detection, and optional higher-timeframe and VWAP overlays.

Instead of issuing buy/sell signals, this tool helps traders understand trend direction, structural stability, volatility environment, and potential transitions. Its adaptive architecture allows the Supertrend to remain steady during chop while responding more dynamically during strong expansions.

Best Uses

• Identifying clear structural trend during intraday trading

• Filtering for aligned conditions before trend continuation setups

• Understanding volatility regimes (compressed vs expanding)

• Monitoring HTF structural influence on lower-timeframe trades

• Using as a standalone trend backbone or as part of the full ATMOS MARKET SUITE suite

This indicator provides context, not predictions. It is fully functional on its own and also integrates naturally with the Momentum Engine, Consensus Strip, and Cx3 ORB system.

ZynIQ VWAP Master v2 - (Lite Pack)Overview

ZynIQ VWAP Master v2 (Lite) provides a clean, structured view of volume-weighted price action using configurable VWAP bands and session-aware logic. It is designed to help traders identify value zones, mean-reversion conditions and directional bias around the VWAP.

Key Features

• Main VWAP with optional upper and lower bands

• Configurable multipliers for custom deviation levels

• Session-aware VWAP anchoring (daily or continuous, depending on settings)

• Lightweight visual style suitable for intraday and swing charts

• Optional HUD panel for quick context

• Highlights value areas and stretched conditions relative to VWAP

Use Cases

• Identifying when price returns to or deviates from value

• Tracking mean-reversion setups

• Assessing directional bias relative to VWAP

• Combining VWAP context with breakout or momentum analysis

Notes

This tool provides VWAP-based structure and value context. It is not a standalone trading system. Use it with your own confirmation and risk management.

OG INDICATORTrade Legacy All-in-One Institutional Indicator

Unlock institutional-grade trading with this comprehensive Pine Script indicator. Seamlessly integrates multiple EMAs, SMAs, VWAPs, and ORB displays into one effortless panel—mimicking pro standards for quick, intuitive analysis.

Per Trade Legacy (Jackie): "This is the only indicator you need for profitability." Pair it with your strategy for powerful confluence, boosting edge and profits.

Simple setup, zero clutter. Premium access via invite-only.

Sniper Entry 🚀🚀 {_AU_} EMA 9 + EMA 15 + VWAP BY = AU AYUSH

This indicator combines EMA 9, EMA 15, and VWAP to identify trend direction and intraday strength. EMA 9 and EMA 15 show short-term momentum and crossover signals, while VWAP acts as an institutional reference point for fair value. Together, they help traders spot trend continuation, pullbacks, and high-quality entry zones during intraday sessions.

VWAP SESSION BUY SELL STRATEGY (INDICATOR) (PDK1977)VWAP SESSION BUY SELL STRATEGY (INDICATOR) (PDK1977)

This indicator combines the proven UT Bot breakout engine but with VWAP directional filtering and ATR-based take profit levels.

It delivers clean, high-probability trend entries and automatic volatility-calibrated exits.

How it works:

Buy only when price is above VWAP

Sell only when price is below VWAP

UT Bot confirms momentum with ATR-based trailing logic

ATR Take Profit gives consistent exits based on volatility

Bars turn green/red only while in a trade, back to normal after TP

Best For:

Intraday and swing trading

Indices, FX, crypto, and high-volume stocks but also for Forex with right TF and settings

Traders who want clean signals and minimal noise

2. Trade Checklist:

Use this before every entry. Quick, simple, reliable.

BUY Checklist:

Price confirmed above VWAP

Label prints BUY

Enter on Buy label (on bar close)

→ Hold until ATR TP hits

SELL Checklist:

Price below VWAP

Label prints SELL

Enter on Sell label

→ Hold until ATR TP hits

Avoid Entries When:

Price is chopping tightly around VWAP

Major news events are about to release

Volume is extremely low

ATR is shrinking rapidly (market compression)

3. Risk-Management Guide

This is tailored to how your system actually behaves.

1. Use ATR TP as Primary Exit:

The system automatically calculates a TP based on volatility:

High volatility → larger TP

Low volatility → smaller TP

This keeps trades consistent and avoids lingering too long.

2. Stop-Loss Recommendation

This strategy is designed for TP-only exits, but if you want a SL:

Recommended Stop-Loss:

Use ATR’s opposite trail, OR

Use 1 × ATR behind your entry candle

This matches the system's internal logic.

3. Position Sizing

Since this system enters during momentum expansions, use:

1–2% max risk per trade

Reduce risk during high-impact news sessions

4. Understand VWAP Environment

Different VWAP conditions require different expectations:

Strong Trend (price far from VWAP)

Higher TP probability

Fewer whipsaws

Excellent continuation setups

Chop Zone (price flips above/below VWAP)

Do NOT trade

Signals lose edge

Wait for a clean break + UT confirmation

5. Choose Correct VWAP Reset for your trading and session

This dramatically improves results.

Market Recommended VWAP Reset

US Stocks New York Session

Indices Daily

Forex London or New York

Crypto Daily or None

4. Final Tips for Best Performance

✔ Enter only in the direction of VWAP

✔ Don’t chase signals far away from entry candle

✔ Avoid trading right into major support/resistance

✔ ATR TP will handle exits mostly

Disclaimer

This script is provided for educational and informational purposes only.

It does not constitute financial advice, investment advice, trading advice, or any form of recommendation to buy or sell any financial instrument. The auto take no responsibility for loss or error in the script.

Tactical Deviation🎯 TACTICAL DEVIATION - Volume-Backed VWAP Deviation Analysis

What Makes This Different?

Unlike basic VWAP indicators, Tactical Deviation combines:

• Multi-timeframe VWAP deviation bands (Daily/Weekly/Monthly)

• Volume spike intelligence - signals only appear with volume confirmation

• Pivot reversal detection at deviation extremes

• Optional multi-VWAP confluence system

• Smart defaults for quality over quantity

This unique combination filters weak setups and identifies high-probability entries at extreme price deviations from fair value.

📊 DEFAULT SETTINGS (Ready to Use)

✅ Daily VWAP with ±2σ deviation bands

✅ Volume spike detection (1.5x average required)

✅ 2σ minimum deviation for signals

❌ Weekly/Monthly VWAPs (enable for multi-timeframe)

❌ Pivot reversal requirement (enable for stronger signals)

❌ Fill zones (optional visual enhancement)

Why: Daily VWAP is most relevant for intraday trading. 2σ bands catch meaningful moves. Volume spikes ensure conviction. Clean chart focuses on what matters.

🚀 HOW TO USE

BASIC USAGE:

• Green triangles (below bars) = Long signals at oversold deviations

• Red triangles (above bars) = Short signals at overbought deviations

SIGNAL QUALITY:

• Normal size, bright colors = Volume spike (best quality)

• Small size, lighter colors = Volume momentum

• Tiny size = No volume confirmation

DEVIATION ZONES:

• ±2σ = Extreme deviation (signals appear here)

• ±1σ to ±2σ = Extended but not extreme

• Within ±1σ = Normal range

TRADING APPROACHES:

Mean Reversion:

→ Enter when price reaches ±2σ with volume spike

→ Target: Return to VWAP or opposite band

→ Stop: Beyond extreme deviation

Trend Continuation:

→ Use bands to identify pullbacks

→ Enter pullback to VWAP in trending market

→ Volume confirms continuation

Reversal Trading:

→ Enable "Require Pivot Reversal" for stronger signals

→ Signals only when deviation + pivot reversal occur

→ Higher probability, fewer signals

⚙️ EXPLORE SETTINGS FOR FULL USE

VWAP SETTINGS:

• Show Weekly/Monthly VWAP = Multi-timeframe context

• Show ±1σ Bands = Normal deviation range

• Show ±3σ Bands = Extreme extremes (rare but powerful)

SIGNAL SETTINGS:

• Min Deviation: 1σ (more signals) | 2σ (default) | 3σ (fewer, extreme only)

• Require Pivot Reversal: OFF (default) | ON (stronger but fewer)

• Volume Spike Threshold: 1.5x (default) | 2.0x+ (major spikes) | 1.2x (more signals)

CONFLUENCE SETTINGS:

• Require Multi-VWAP Confluence: OFF (default) | ON (2+ VWAPs must agree)

• Min VWAPs: 2 (Daily + Weekly/Monthly) | 3 (all must agree)

VISUAL SETTINGS:

• Show Fill Zones = Shaded areas between bands

• Fill Opacity = Transparency adjustment

• Line Widths = Customize thickness

💡 PRO TIPS

1. Start with defaults, then enable features as you learn

2. Volume spike requirement filters weak moves - keep it enabled

3. Enable Weekly/Monthly VWAPs for higher timeframe context

4. Enable confluence for swing trading setups

5. Pivot reversals: ON for reversals, OFF for continuations

6. Check top-right info table for current deviation levels

🎨 VISUAL GUIDE

• Cyan Line = Daily VWAP (fair value)

• Cyan Bands = Daily deviation zones

• Orange Line = Weekly VWAP (if enabled)

• Purple Line = Monthly VWAP (if enabled)

• Green Triangle = Long signal (oversold)

• Red Triangle = Short signal (overbought)

⚠️ IMPORTANT

Educational purposes only. Always use proper risk management. Signals are based on statistical deviation, not guarantees. Volume confirmation improves quality but doesn't guarantee outcomes. Combine with your own analysis.

The unique combination of VWAP deviation analysis, volume profile confirmation, pivot identification, and multi-timeframe confluence in a single clean interface makes Tactical Deviation different from basic VWAP indicators.

Happy Trading! 📈

Volume Weighted Average Price AdvancedVWAP (Advanced) with Multi‑Venue Aggregation and Historical Value Areas

Core: Anchored VWAP with configurable anchor (session/week/month/quarter/year/decade/century or corporate events), offset, and up to three standard-deviation bands.

Multi‑Venue Aggregation: Optionally pull price/volume from up to 5 additional exchanges/symbols (pair-matched by default). VWAP/σ are computed on the aggregated price*volume.

Value Area Blocks: Each completed anchor draws a block from the chosen basis (±1σ or ±2σ) or an optional percentile-based range (default 20–80%). Blocks project to the exact next anchor boundary, or you can extend them to the latest bar. Prior-period VWAP lines are shown inside the blocks.

Volume Gate: Optionally skip drawing prior blocks when the anchor’s aggregated volume is below a median/mean baseline times a multiplier.

HTF Context: Optional higher-timeframe VWAP overlay; can filter the current VWAP/bands so they only show when aligned with the HTF VWAP.

Venue Health: Label shows how many extra venues were included (non‑na) and median venue volume; flags divergence when primary volume is below venue median × threshold.

Alerts: Price in current value area (VWAP ±1σ) and price crossing the most recent prior VWAP.

Styling: Bands and fills are minimal; HTF VWAP is a distinct line; value-area blocks are shaded with prior VWAP lines inside.

Configure via the grouped inputs: VWAP Settings, Additional Exchange Sources, Historical Value Areas, HTF Context, and Bands Settings.

Quantum Market Analyzer X7Quantum Market Analyzer X7 - Complete Study Guide

Table of Contents

1. Overview

2. Indicator Components

3. Signal Interpretation

4. Live Market Analysis Guide

5. Best Practices

6. Limitations and Considerations

7. Risk Disclaimer

________________________________________

Overview

The Quantum Market Analyzer X7 is a comprehensive multi-timeframe technical analysis indicator that combines traditional and modern analytical methods. It aggregates signals from multiple technical indicators across seven key analysis categories to provide traders with a consolidated view of market sentiment and potential trading opportunities.

Key Features:

• Multi-Indicator Analysis: Combines 20+ technical indicators

• Real-Time Dashboard: Professional interface with customizable display

• Signal Aggregation: Weighted scoring system for overall market sentiment

• Advanced Analytics: Includes Order Block detection, Supertrend, and Volume analysis

• Visual Progress Indicators: Easy-to-read progress bars for signal strength

________________________________________

Indicator Components

1. Oscillators Section

Purpose: Identifies overbought/oversold conditions and momentum changes

Included Indicators:

• RSI (14): Relative Strength Index - momentum oscillator

• Stochastic (14): Compares closing price to price range

• CCI (20): Commodity Channel Index - cycle identification

• Williams %R (14): Momentum indicator similar to Stochastic

• MACD (12,26,9): Moving Average Convergence Divergence

• Momentum (10): Rate of price change

• ROC (9): Rate of Change

• Bollinger Bands (20,2): Volatility-based indicator

Signal Interpretation:

• Strong Buy (6+ points): Multiple oscillators indicate oversold conditions

• Buy (2-5 points): Moderate bullish momentum

• Neutral (-1 to 1 points): Balanced conditions

• Sell (-2 to -5 points): Moderate bearish momentum

• Strong Sell (-6+ points): Multiple oscillators indicate overbought conditions

2. Moving Averages Section

Purpose: Determines trend direction and strength

Included Indicators:

• SMA: 10, 20, 50, 100, 200 periods

• EMA: 10, 20, 50 periods

Signal Logic:

• Price >2% above MA = Strong Buy (+2)

• Price above MA = Buy (+1)

• Price below MA = Sell (-1)

• Price >2% below MA = Strong Sell (-2)

Signal Interpretation:

• Strong Buy (6+ points): Price well above multiple MAs, strong uptrend

• Buy (2-5 points): Price above most MAs, bullish trend

• Neutral (-1 to 1 points): Mixed MA signals, consolidation

• Sell (-2 to -5 points): Price below most MAs, bearish trend

• Strong Sell (-6+ points): Price well below multiple MAs, strong downtrend

3. Order Block Analysis

Purpose: Identifies institutional support/resistance levels and breakouts

How It Works:

• Detects historical levels where large orders were placed

• Monitors price behavior around these levels

• Identifies breakouts from established order blocks

Signal Types:

• BULLISH BRK (+2): Breakout above resistance order block

• BEARISH BRK (-2): Breakdown below support order block

• ABOVE SUP (+1): Price holding above support

• BELOW RES (-1): Price rejected at resistance

• NEUTRAL (0): No significant order block interaction

4. Supertrend Analysis

Purpose: Trend following indicator based on Average True Range

Parameters:

• ATR Period: 10 (default)

• ATR Multiplier: 6.0 (default)

Signal Types:

• BULLISH (+2): Price above Supertrend line

• BEARISH (-2): Price below Supertrend line

• NEUTRAL (0): Transition period

5. Trendline/Channel Analysis

Purpose: Identifies trend channels and breakout patterns

Components:

• Dynamic trendline calculation using pivot points

• Channel width based on historical volatility

• Breakout detection algorithm

Signal Types:

• UPPER BRK (+2): Breakout above upper channel

• LOWER BRK (-2): Breakdown below lower channel

• ABOVE MID (+1): Price above channel midline

• BELOW MID (-1): Price below channel midline

6. Volume Analysis

Purpose: Confirms price movements with volume data

Components:

• Volume spikes detection

• On Balance Volume (OBV)

• Volume Price Trend (VPT)

• Money Flow Index (MFI)

• Accumulation/Distribution Line

Signal Calculation: Multiple volume indicators are combined to determine institutional activity and confirm price movements.

________________________________________

Signal Interpretation

Overall Summary Signals

The indicator aggregates all component signals into an overall market sentiment:

Signal Score Range Interpretation Action

STRONG BUY 10+ Overwhelming bullish consensus Consider long positions

BUY 4-9 Moderate to strong bullish bias Look for long opportunities

NEUTRAL -3 to 3 Mixed signals, consolidation Wait for clearer direction

SELL -4 to -9 Moderate to strong bearish bias Look for short opportunities

STRONG SELL -10+ Overwhelming bearish consensus Consider short positions

Progress Bar Interpretation

• Filled bars indicate signal strength

• Green bars: Bullish signals

• Red bars: Bearish signals

• More filled bars = stronger conviction

________________________________________

Live Market Analysis Guide

Step 1: Initial Assessment

1. Check Overall Summary: Start with the main signal

2. Verify with Component Analysis: Ensure signals align

3. Look for Divergences: Identify conflicting signals

Step 2: Timeframe Analysis

1. Set Appropriate Timeframe: Use 1H for intraday, 4H/1D for swing trading

2. Multi-Timeframe Confirmation: Check higher timeframes for trend context

3. Entry Timing: Use lower timeframes for precise entry points

Step 3: Signal Confirmation Process.

For Buy Signals:

1. Oscillators: Look for oversold conditions (RSI <30, Stoch <20)

2. Moving Averages: Price should be above key MAs

3. Order Blocks: Confirm bounce from support levels

4. Volume: Check for accumulation patterns

5. Supertrend: Ensure bullish trend alignment.

For Sell Signals:

1. Oscillators: Look for overbought conditions (RSI >70, Stoch >80)

2. Moving Averages: Price should be below key MAs

3. Order Blocks: Confirm rejection at resistance levels

4. Volume: Check for distribution patterns

5. Supertrend: Ensure bearish trend alignment.

Step 4: Risk Management Integration

1. Signal Strength Assessment: Stronger signals = larger position size

2. Stop Loss Placement: Use Order Block levels for stops

3. Take Profit Targets: Based on channel analysis and resistance levels

4. Position Sizing: Adjust based on signal confidence

________________________________________

Best Practices

Entry Strategies

1. High Conviction Entries: Wait for STRONG BUY/SELL signals

2. Confluence Trading: Look for multiple components aligning

3. Breakout Trading: Use Order Block and Trendline breakouts

4. Trend Following: Align with Supertrend direction.

Risk Management

1. Never Risk More Than 2% Per Trade: Regardless of signal strength

2. Use Stop Losses: Place at invalidation levels

3. Scale Positions: Stronger signals warrant larger (but still controlled) positions

4. Diversification: Don't rely solely on one indicator.

Market Conditions

1. Trending Markets: Focus on Supertrend and MA signals

2. Range-Bound Markets: Emphasize Oscillator and Order Block signals

3. High Volatility: Reduce position sizes, widen stops

4. Low Volume: Be cautious of breakout signals.

Common Mistakes to Avoid

1. Signal Chasing: Don't enter after signals have already moved significantly

2. Ignoring Context: Consider overall market conditions

3. Overtrading: Wait for high-quality setups

4. Poor Risk Management: Always use appropriate position sizing

________________________________________

Limitations and Considerations

Technical Limitations

1. Lagging Nature: All technical indicators are based on historical data

2. False Signals: No indicator is 100% accurate

3. Market Regime Changes: Indicators may perform differently in various market conditions

4. Whipsaws: Possible in choppy, sideways markets.

Optimal Use Cases

1. Trending Markets: Performs best in clear trending environments

2. Medium to High Volatility: Requires sufficient price movement for signals

3. Liquid Markets: Works best with adequate volume and tight spreads

4. Multiple Timeframe Analysis: Most effective when used across different timeframes.

When to Use Caution

1. Major News Events: Fundamental analysis may override technical signals

2. Market Opens/Closes: Higher volatility can create false signals

3. Low Volume Periods: Signals may be less reliable

4. Holiday Trading: Reduced participation affects signal quality

________________________________________

Risk Disclaimer

IMPORTANT LEGAL DISCLAIMER FROM aiTrendview

WARNING: TRADING INVOLVES SUBSTANTIAL RISK OF LOSS

This Quantum Market Analyzer X7 indicator ("the Indicator") is provided for educational and informational purposes only. By using this indicator, you acknowledge and agree to the following terms:

No Investment Advice

• The Indicator does NOT constitute investment advice, financial advice, or trading recommendations

• All signals generated are based on historical price data and mathematical calculations

• Past performance does not guarantee future results

• No representation is made that any account will achieve profits or losses similar to those shown.

Risk Acknowledgment

• TRADING CARRIES SUBSTANTIAL RISK: You may lose some or all of your invested capital

• LEVERAGE AMPLIFIES RISK: Margin trading can result in losses exceeding your initial investment

• MARKET VOLATILITY: Financial markets are inherently unpredictable and volatile

• TECHNICAL ANALYSIS LIMITATIONS: No technical indicator is infallible or guarantees profitable trades.

User Responsibility

• YOU ARE SOLELY RESPONSIBLE for all trading decisions and their consequences

• CONDUCT YOUR OWN RESEARCH: Always perform independent analysis before making trading decisions

• CONSULT PROFESSIONALS: Seek advice from qualified financial advisors

• RISK MANAGEMENT: Implement appropriate risk management strategies

No Warranties

• The Indicator is provided "AS IS" without warranties of any kind

• aiTrendview makes no representations about the accuracy, reliability, or suitability of the Indicator

• Technical glitches, data feed issues, or calculation errors may occur

• The Indicator may not work as expected in all market conditions.

Limitation of Liability

• aiTrendview SHALL NOT BE LIABLE for any direct, indirect, incidental, or consequential damages

• This includes but is not limited to: trading losses, missed opportunities, data inaccuracies, or system failures

• MAXIMUM LIABILITY is limited to the amount paid for the indicator (if any)

Code Usage and Distribution

• This indicator is published on TradingView in accordance with TradingView's house rules

• UNAUTHORIZED MODIFICATION or redistribution of this code is prohibited

• Users may not claim ownership of this intellectual property

• Commercial use requires explicit written permission from aiTrendview.

Compliance and Regulations

• VERIFY LOCAL REGULATIONS: Ensure compliance with your jurisdiction's trading laws

• Some trading strategies may not be suitable for all investors

• Tax implications of trading are your responsibility

• Report trading activities as required by law

Specific Risk Factors

1. False Signals: The Indicator may generate incorrect buy/sell signals

2. Market Gaps: Overnight gaps can invalidate technical analysis

3. Fundamental Events: News and economic data can override technical signals

4. Liquidity Risk: Some markets may have insufficient liquidity

5. Technology Risk: Platform failures or connectivity issues may prevent order execution.

Professional Trading Warning

• THIS IS NOT PROFESSIONAL TRADING SOFTWARE: Not intended for institutional or professional trading

• NO REGULATORY APPROVAL: This indicator has not been approved by any financial regulatory authority

• EDUCATIONAL PURPOSE: Designed primarily for learning technical analysis concepts

FINAL WARNING

NEVER INVEST MONEY YOU CANNOT AFFORD TO LOSE

Trading financial instruments involves significant risk. The majority of retail traders lose money. Before using this indicator in live trading:

1. Practice on paper/demo accounts extensively

2. Start with small position sizes

3. Develop a comprehensive trading plan

4. Implement strict risk management rules

5. Continuously educate yourself about market dynamics

By using the Quantum Market Analyzer X7, you acknowledge that you have read, understood, and agree to this disclaimer. You assume full responsibility for all trading decisions and their outcomes.

Contact: For questions about this disclaimer or the indicator, contact aiTrendview through official TradingView channels only.

________________________________________

This study guide and indicator are published on TradingView in compliance with TradingView's community guidelines and house rules. All users must adhere to TradingView's terms of service when using this indicator.

Document Version: 1.0

Publisher: aiTrendview

________________________________________

Disclaimer

The content provided in this blog post is for educational and training purposes only. It is not intended to be, and should not be construed as, financial, investment, or trading advice. All charting and technical analysis examples are for illustrative purposes. Trading and investing in financial markets involve substantial risk of loss and are not suitable for every individual. Before making any financial decisions, you should consult with a qualified financial professional to assess your personal financial situation.

Multi Rolling VWAPMulti Rolling VWAP Indicator

Displays 4 volume-weighted average price (VWAP) levels on your chart:

7D VWAP - Weekly rolling average

30D VWAP - Monthly rolling average

90D VWAP - Quarterly rolling average

365D VWAP - Yearly rolling average

Each VWAP shows where the average price is, weighted by volume. Institutional traders often use these levels as support/resistance.

Optional Features:

Bands show volatility zones (Value Area High/Low)

Anchor modes: Reset weekly, monthly, quarterly, or yearly instead of rolling

Crypto volume aggregation from 15+ exchanges for accurate calculations

Clean, minimal design for white background charts.

Adaptive CE-VWAP Breakout Framework [KedArc Quant]Description

A structured framework that unites three complementary systems into one charting engine:

Chandelier Exit (CE) – ATR-based trailing logic that defines trend direction, stop placement, and risk/reward overlays.

Swing-Anchored VWAP (SWAV) – a dynamically anchored VWAP that re-starts from each confirmed swing and adapts its smoothness to volatility.

Pivot S/R with Volume Breaks – confirmed horizontal levels with alerts when broken on expanding volume.

This script builds a single workflow for bias → trigger → managementwithout mixing unrelated indicators. Each module is internally linked rather than layered cosmetically, making it a true analytical framework—not.

Acknowledgment

Special thanks to Dynamic Swing Anchored VWAP by Zeiierman, whose swing-anchoring concept inspired a part of the SWAV module’s implementation and adaptation logic.

Support and Resistance Levels with Breaks by LuxAlgo for S/R breakout logic.

How this helps traders

Trend clarity – CE color-codes direction and provides evolving stops.

Context value – SWAV traces adaptive mean paths so traders see where price is heavy or light.

Action filter – Pivot+volume logic highlights true structural breaks, filtering false moves.

Discipline tool – Optional R:R boxes visualize risk and target zones to enforce planning.

Entry / Exit guidelines (for study purposes only)

Bias Use CE direction: green = long bias red = short bias

Entry

1. Breakout method– Trade in CE direction when a pivot level breaks on valid volume.

2. VWAP confirmation– Prefer breaks occurring around the nearest SWAV path (fair-value cross or re-test).

Exit

Stop = CE line / recent swing HL / ATR × (multiplier)

Target = R-multiple × risk (default 2 R)

Optional live update keeps SL/TP aligned with current CE state.

Core formula concepts

ATR Stop: Stop = High/Low – ATR × multiplier

VWAP calc: Σ(price × vol) / Σ(vol) anchored at swing pivot, adapted by APT (Adaptive Price Tracking) ratio ∝ ATR volatility.

Volume oscillator: 100 × (EMA₅ – EMA₁₀)/EMA₁₀; valid break when threshold %.

Input configuration (high-level)

Master Controls

Show CE / SWAV modules Theme & Fill opacity

CE Section

ATR period & multiplier Use Close for extremums

Show buy/sell labels Await bar confirmation

Risk-Reward overlay: R-multiple, Stop basis (CE/Swing/ATR×), Live update toggle

SWAV Section

Swing period Adaptive Price Tracking length Volatility bias (ATR-based adaptation) Line width

Pivot & Volume Breaks

Left/Right bar windows Volume threshold % Show Break labels and alerts

Best timeframes

Intraday: 5 m – 30 m for breakout confirmation

Swing: 1 h – 4 h for trend context

Settings scale with instrument volatility—adjust ATR period and volume threshold to match liquidity.

Glossary

ATR: Average True Range (volatility metric)

CE: Chandelier Exit (trailing stop/trend filter)

SWAV: Swing-Anchored VWAP (anchored mean price path)

Pivot H/L: Confirmed local extrema using left/right bar windows

R-multiple: Profit target as a multiple of initial risk

FAQ

Q: Does it repaint? A: No—pivots wait for confirmation and VWAP updates forward-only.

Q: Can modules be disabled? A: Yes—each section has its own toggle.

Q: Can it trade automatically? A: This is an indicator/study, not an auto-strategy.

Q: Is this financial advice? A: No—educational use only.

Disclaimer

This script is for educational and analytical purposes only.

It is not financial advice. Trading involves risk of loss. Past performance does not guarantee future results. Always apply sound risk management.

ZenAlgo - BoxerThis indicator plots multi-period Volume-Weighted Average Price (VWAP) ranges and deviation bands across several timeframes — specifically weekly, monthly, quarterly, semi-annual, and yearly. It is designed to visualize how price evolves relative to statistically weighted value areas within each period, based on both traded price and volume distribution.

Each timeframe layer is drawn independently, using its own cumulative VWAP and standard deviation calculation, and displayed as horizontal ranges aligned precisely with calendar periods. This structure allows the chart to show where price currently trades relative to past value zones and how each higher-timeframe VWAP acts as a dynamic reference for mean reversion or continuation.

Calculation Logic

1. Source and Base Inputs

The indicator uses the average of high, low, and close as its price source.

Stocks reset daily at session open.

2. VWAP and Deviation Computation

For each active timeframe, it accumulates the product of price and volume and divides it by cumulative volume, forming a continuously updated VWAP within that period.

The dispersion of price around VWAP is measured through a volume-weighted variance, converted to standard deviation.

These values form symmetrical bands around the VWAP (±1σ, ±2σ, etc.), describing the statistically typical price spread.

3. Range Drawing and Persistence

When a new period begins (e.g., a new week or month), the script finalizes the previous VWAP and deviation values, fixes them to time coordinates representing the full duration of that completed period, and draws corresponding lines or boxes across the entire range.

The user can control how many historical periods remain visible, ensuring performance and clarity even on high-frequency charts.

Each band can be toggled independently (for example ±1, ±2, ±3 deviations), and colors are adjustable per timeframe.

4. Adaptive Time Anchors

The start of each timeframe is aligned with calendar boundaries.

For stocks, the start time aligns with 9:30 New York time to coincide with market open for NYSE.

Each new anchor triggers a reset of cumulative data and creation of a new VWAP range.

5. Visualization Structure

The weekly layer is drawn first and can optionally display live VWAP bands extending backward for a user-defined number of weeks.

Monthly, quarterly, semi-annual, and yearly layers use the same computation principle but with independent accumulation windows.

The central VWAP line is dashed, while outer deviation levels are drawn as dotted or solid lines depending on their multiplier.

Boxes are rendered for key deviation intervals (e.g., ±2σ) to highlight broader value zones.

Interpretation

The VWAP represents the mean price weighted by traded volume for the given period.

Deviation bands describe statistically typical distance from that mean; outer bands mark less frequent extremes.

When price remains within ±1σ or ±2σ, it suggests balance around fair value.

Repeated touches or breaks beyond outer deviations indicate expansion or compression of volatility relative to prior periods.

Overlaps of VWAPs from multiple timeframes reveal multi-period confluence zones, useful for observing where long-term and short-term value agree or diverge.

Recommended Timeframes by Range Type

Weekly Range

Recommended timeframe: 30m to 12h

Suggested options: 30m, 1h, 2h, 3h, 4h, 6h, 8h, 12h

Using lower timeframes (like 5m) is technically possible, but higher ones provide smoother visualization and better readability.

Monthly Range

Recommended timeframe: 1h to 1D

Suggested options: 1h, 2h, 3h, 4h, 6h, 8h, 12h, 1D

Lower timeframes such as 30m may not display the full monthly range due to TradingView’s bar limits, so use higher TFs for complete coverage.

Quarterly Range

Recommended timeframe: 4h to 1W

Suggested options: 4h, 6h, 8h, 12h, 1D, 1W

Quarterly ranges benefit from higher timeframes to ensure that enough historical data is visible without exceeding chart limits.

Semi-Annual Range

Recommended timeframe: 12h to 1M

Suggested options: 12h, 1D, 1W, 1M

Lower timeframes would require too many bars to load a full six-month range; higher TFs offer a clearer overview.

Yearly Range

Recommended timeframe: 1D to 1M or higher

Suggested options: 1D, 1W, 1M

Yearly ranges often cannot display correctly on low timeframes (e.g. 1h) because of TradingView’s maximum bar limits — for instance, five years of 1h data exceeds 40,000 bars. Use higher TFs for accurate rendering.

Added Value Compared to Common Free VWAP Indicators

Incorporates five independent timeframes simultaneously (week, month, quarter, half-year, year) with exact calendar anchoring and timezone handling.

Calculates volume-weighted deviation for each layer, maintaining consistent statistical scale across assets.

Provides historical box persistence , allowing comparison of completed VWAP structures instead of only current running lines.

Enables selective visibility, bandwidth control, and precise visual differentiation through adjustable colors and line weights.

Limitations and Notes

The indicator does not generate trading signals. It is purely analytical and descriptive.

On very low timeframes or illiquid assets, deviation values may fluctuate if volume data is inconsistent.

Historical boxes are approximate in length for months with fewer than 31 days; this simplification has negligible effect on interpretation.

High visual density may occur when enabling many deviations or timeframes at once; users should limit visible history for performance.

Best Usage Practices

Apply on intraday charts (5–240 min) to study how price interacts with weekly or higher-timeframe VWAP zones.

Observe convergence of VWAPs from multiple periods to locate significant equilibrium levels.

Use outer deviations to frame potential exhaustion or re-entry zones rather than directional predictions.

Combine with independent volume- or structure-based analysis for context.

Vwap Daily By SamsungTitle

Daily VWAP with Historical Lookback (Logic Fix)

Description

This script calculates and plots the daily Volume-Weighted Average Price (VWAP), an essential tool for intraday traders.

What makes this indicator special is its robust plotting logic. Unlike many simple VWAP scripts that struggle to show data for previous days, this version includes a crucial fix that allows you to reliably display historical VWAP lines for as many days back as you need. This allows for more comprehensive backtesting and analysis of how price has interacted with the VWAP on previous trading days.

This is an indispensable tool for traders who use VWAP as a dynamic level of support/resistance, a benchmark for trade execution quality, or a gauge of the day's trend.

Key Features

Historical VWAP Display: Easily plot VWAP for multiple past days on your chart. Simply set the number of lookback days in the settings.

Accurate Daily Calculation: The VWAP calculation correctly resets at the beginning of each new trading session (00:00 server time).

Fully Customizable: You have full control over the appearance of the VWAP line, including its color, width, and style (Solid or Stepped).

Robust Plotting Engine: This script solves the common Pine Script issue where conditionally plotted historical lines fail to render. It works reliably on all intraday timeframes.

Built-in Debug Mode: For advanced users or those curious about the inner workings, a comprehensive debug mode can be enabled to display raw VWAP values, cumulative volume, and timeframe warnings.

How to Use

Add the "Daily VWAP with Historical Lookback" indicator to your chart.

IMPORTANT: Make sure you are on an intraday timeframe (e.g., 1H, 30M, 15M, 5M, 1M). This indicator is designed for intraday analysis and will display a warning if used on a daily or higher timeframe.

Open the indicator's settings.

In the "VWAP Settings" tab, adjust the "Lookback Days to Display" to set how many previous days of VWAP you want to see. (e.g., 0 for today only, 1 for today and yesterday, 10 for the last 10 days).

Customize the line's appearance in the "Line Style" tab.

The "Logic Fix" Explained (For Developers)

A common challenge in Pine Script is conditionally plotting data for historical bars. Many scripts attempt this by dynamically changing the plot color to na (transparent) for bars that shouldn't be displayed. This method is often unreliable and can result in the entire plot failing to render.

This script employs a more robust and standard approach: manipulating the data series itself.

The Problem: plot(vwap, color = shouldPlot ? color.red : na) can be buggy.

The Solution: plot(shouldPlot ? vwap : na, color = color.red) is reliable.

Instead of changing the color, we create a new data series (plotVwap). This series contains the vwapValue only on the bars that meet our date criteria. On all other bars, its value is na (Not a Number). The plot() function is designed to handle na values by simply "lifting the pen," creating a clean break in the line. This ensures that the VWAP is drawn only for the selected days, with 100% reliability across all historical data.

Settings Explained

Lookback Days to Display: Sets the number of past days (from the last visible bar) for which to display the VWAP.

Line Color, Width, and Style: Standard cosmetic settings for the VWAP line.

Enable Debug Mode (Master Switch): Toggles all debugging features on or off. It is enabled by default to help new users.

Display Debug: Cumulative Volume: When enabled, it shows the daily cumulative volume in a gray area on a separate pane.

Display Debug: Raw VWAP Value: When enabled, it plots the raw, unfiltered VWAP calculation for all days on the chart, helping to verify the core logic.

This script is provided for educational and informational purposes. Trading involves significant risk. Always conduct your own research and analysis before making any trading decisions.

If you find this script useful, a 'Like' is always appreciated! Happy trading

Multi-Anchor VWAP Deviation Dashboard Overview

Multi-Anchor VWAP Deviation Dashboard (Optimized Global) is an overlay indicator that computes up to five user-defined Anchored Volume Weighted Average Prices (AVWAPs) from custom timestamps, plotting their lines and displaying real-time percentage deviations from the current close. It enables precise analysis of price positioning relative to key events (e.g., earnings, news) or periods (e.g., weekly opens), with a compact dashboard for quick scans. Optimized for performance, it uses manual iterative calculations to handle dynamic anchor changes without repainting.

Core Mechanics

The indicator focuses on efficient AVWAP computation and deviation tracking:

Anchor Configuration: Five independent anchors, each with a name, UTC timestamp (e.g., "01 Oct 2025 00:00" for monthly open), show toggle, and color. Timestamps define the calculation start—e.g., AVWAP1 from "20 Oct 2025" onward.

AVWAP Calculation: For each enabled anchor, it identifies the first bar at/after the timestamp as the reset point, then iteratively accumulates (price * volume) / total volume from there. Uses HLC3 source (customizable); handles input changes by resetting sums on new anchors.

Deviation Metric: For each AVWAP, computes % deviation = ((close - AVWAP) / AVWAP) * 100—positive = above (potential resistance), negative = below (support).

Visuals: Plots lines (linewidth 1–2, user colors); dashboard (2 columns, 6 rows) shows names (anchor-colored if enabled) and deviations (green >0%, red <0%, gray N/A), positioned user-selectable with text sizing. Updates on last bar for efficiency.

This setup scales deviations across volatilities, aiding multi-period bias assessment.

Why This Adds Value & Originality

Standard VWAPs limit to session anchors (daily/weekly); deviation tools often lack multiples. This isn't a simple mashup: Manual iterative AVWAP (no built-in ta.vwap reliance) ensures dynamic resets on timestamp tweaks—e.g., shift "Event" to FOMC date without recalc lag. The 5-anchor flexibility (arbitrary UTC times) + centralized dashboard (colored deviations at a glance) creates a "global timeline scanner" unique to event-driven trading, unlike rigid multi-VWAP scripts. It streamlines what requires 5 separate indicators, with % normalization for cross-asset comparison (e.g., SPY vs. BTC).

How to Use

Setup: Overlay on chart. Configure anchors (e.g., Anchor1: "Weekly Open" at next Monday 00:00 UTC; enable/show 2–3 for focus). Set source (HLC3 default), position (Top Right), text size (Small).

Interpret Dashboard:

Left Column: Anchor names (e.g., "Monthly Open" in orange).

Right Column: Deviations (e.g., "+1.25%" green = above, bullish exhaustion?).

Scan for confluence (e.g., all >+2% = overbought).

Trading:

Lines: Price near AVWAP = mean reversion; breaks = momentum.

Example: -0.8% below "Event" anchor post-earnings → potential bounce buy.

Use on 1H–D; adjust timestamps via calendar.

Tips: Enable 1–3 anchors to avoid clutter; test on historical events.

Limitations & Disclaimer

AVWAPs reset on anchor bars, potentially lagging mid-period; deviations are % only (add ATR for absolute). Table updates on close (no intrabar). Timestamps must be UTC/future-proof. No alerts/exits—integrate manually. Not advice; backtest deviations on your assets. Past ≠ future. Comments for ideas.

The VWAP OracleOverview