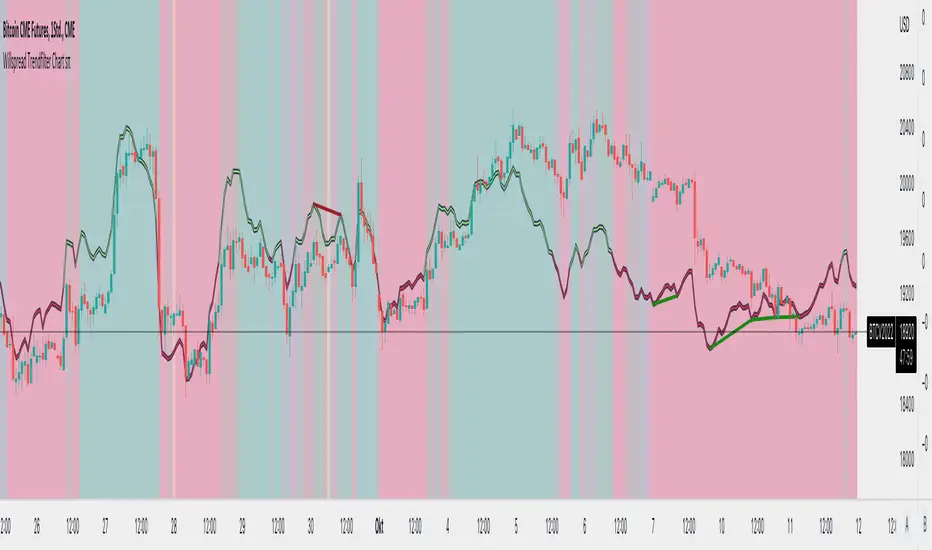

Willspread Chart + POIV & ADVolumen TrendColor sπThe Indicator is a combination of different types of measurements to the Price Action.

1. Spread: The Spread is set to measure your Symbol to another chosen Market like Dollar as Contra . But you can switch also between different markets.

2. Accumulation/Distribution with True Range of High or Low including OpenInterest. This only works with Futures .

--Energies, Metals, Bonds, Softs, Currencies, Livestock, live cattle , feeder cattle, lean hogs , index--

Open Interest for:

ZW, ZC, ZS, ZM, ZL, ZO, ZR, CL, RB, HO, NG, GC, SI, HG, PA, PL, ZN, ZB, ZT, ZF, CC, CT, KC, SB, JO, LB, AUDUSD, GBPUSD, USDCAD, EURUSD, USDJPY, USDCHF, USDMXN, NZDUSD, USDRUB, DX, BTC, ETH, LE, GF, HE, NQ, NDX, ES, SPX, RTY, VIX,

3. Accumulation/Distribution with True Range of High or Low including Volume .

4. The color shows if the Market has positive or negative (Willspread, Volume or Open Interest)

5. The Indicator also shows Divergences to Price and Willspread Movements.

If you want to have more information just give me a message.

Linea di accumulazione/distribuzione (ADL)

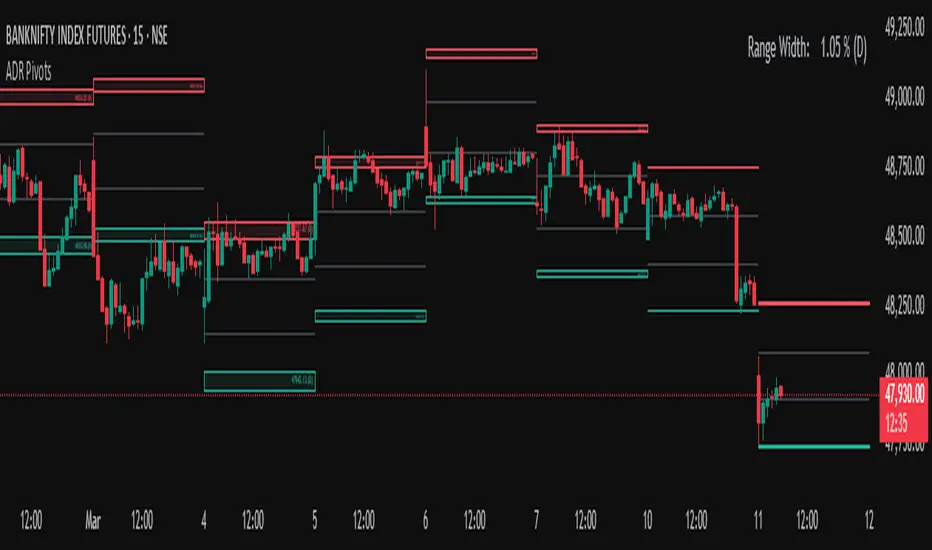

Average Daily Range (ADR) (Multi Timeframe, Multi Period)Average Daily Range (ADR)

(Multi Timeframe, Multi Period, Extended Levels)

Tips

• Narrow Zones are an indication of breakouts. It can be a very tight range as well.

• Wider Zones can be Sideways or Volatile.

What is this Indicator?

• This is Average Daily Range (ADR) Zones or Pivots.

• This have Multi Timeframe, Multi Period (Up to 3 Levels) and Extended Target Levels.

Advantages of this Indicator

• This is a Leading indicator, not Dynamic or Repaint.

• Helps to identify the reversal points.

• The levels are more accurate and not like the old formulas.

• Can practically follow the Buy Low and Sell High principle.

• Helps to keep minimum Stop Loss.

Who to use?

• Highly beneficial for Day Traders

• It can be used for Swing and Positions as well.

What timeframe to use?

• Any timeframe.

When to use?

• Any market conditions.

How to use?

Entry

• Long entry when the Price reach at or closer to the Green Support zone.

• Long entry when the Price retrace to the Red Resistance zone.

• Short entry when the Price reach at or closer to the Red Resistance zone.

• Short entry when the Price retrace to the Green Support zone.

• Long or Short at the Pivot line.

Exit

• Use past ADR levels as targets.

• Or use the Target levels in the indicator for breakouts.

• Use the Pivot line as target.

• Use Support or Resistance Zones as targets in reversal method.

What are the Lines?

Gray Line:

• It the day Open or can be considered as Pivot.

Red & Green ADR Zones:

• Red Zone is Resistance.

• Green Zone is Support.

• Mostly price can reverse from this Zones.

• Multiple Red and Green Lines forms a Zone.

• These lines are average levels of past days which helps to figure out the maximum and minimum price range that can be moved in that day.

• The default number of days are 5, 7 and 14. This can be customized.

Red & Green Target Lines:

• These are Target levels.

What are the Labels?

• First Number: Price of that level.

• Numbers in (): Percentage change and Change of price from LTP (Last Traded Price) to that Level.

General Tips

• It is good if Stock trend is same as that of the Index trend.

• Lots of indicators creates lots of confusion.

• Keep the chart simple and clean.

• Buy Low and Sell High.

• Master averages or 50%.

Volume Risk Avoidance IndicatorPrice Pattern Analysis is the core of trading. But price patterns often fails.

VRAI (Volume Risk Avoidance Indicator) shows Volume Pressure, so that you can avoid volume-based risks.

For example, never short when you see green (buying pressure). Never long when you see red (selling pressure).

You still need to pick good price patterns, because the crossover of volume pressure is not reliable.

Enjoy!

Break of structure indicatorThis indicator allows you to set a range of price which you want to get an alert about if price breaks that structure.

Breakout Accumulation/DistributionBasic modification of my SFP Momentum Indicator showing accumulation/distribution patterns based on breakouts above previous anchor points.

Candles are colored based on whether accumulation or distribution was last.

Best if used at HTF then confirmed at LTF.

SFP MomentumCustom swing fail detector with levels and breakouts both major and minor plus colored candles based on SFP momentum.

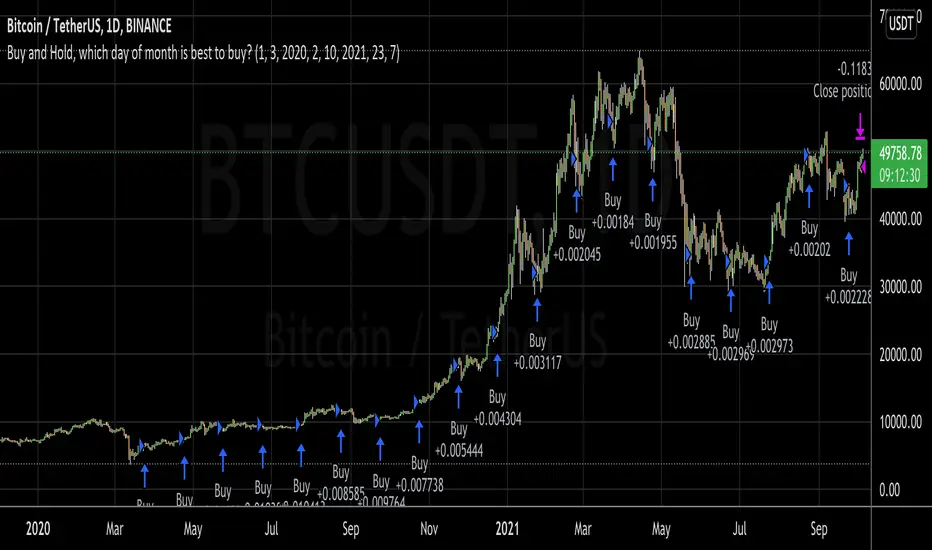

Buy and Hold, which day of month is best to buy?I wanted to invest a certain fiat amount each month and was wondering which day would be best to do this.

So, with this script, you can set your entry day. On the last day of the date range, it will close all positions. You can then see what amount of the asset you have accumulated to date. If you try all the days of the month and see when you can sell the most amount of the asset, you've found the best buy date of the month for that asset.

A second option is to set an exit day. This is good for a strategy where you would go long (buy) on the entry date and short (sell) on the exit day.

This was inspired by people running out of money by the end of the month and selling their asset, which could make the price fall. Then when they receive the wages by the 5th or so, they would rebuy, causing the price to go up.

Accumulation/Distribution %This script takes the signal from the Accumulation Distribution indicator invented by Larry Williams and normalizes it such that it becomes an oscillator about a zero line as described by John Bollinger in his book Bollinger on Bollinger Bands . The purpose of the indicator is to serve as a volume-based confirmation of signals given by other indicators, typically Bollinger Bands paired with a momentum indicator . In the example shown, Bollinger Bands are paired with Bollinger Bands %B and the Bollinger Bands %B indicator is interpreted similar to the Relative Strength Index ( RSI ) which is a momentum indicator .

The AD% indicator is colorized such that positive readings are green and negative readings are red. The readings become darker when approaching the zero line. The colorization is also displayed on the price chart. The chart type needs to be set to "bars" for price colorization to work properly.

The formula for this indicator is presented in the John Bollinger book as follows:

10-day sum of /10-sum of volume

How to use (my take on a strategy from the book):

1. Look for %B readings that are oversold or overbought (less than 0.00 or greater than 1.00)

2. Check for bearish divergence or bullish convergence of price and %B as shown on the chart

3. Verify divergence or convergence with AD%

4. Note previous trending/crossover behavior of AD% and %B and compare to situation being analyzed

5. A conservative trader may consider buying/selling on a close beyond the 20-day moving average and an AD% zero line crossover (color change)

6. An aggressive trader may consider buying/selling on a color change alone, on a breakdown of %B, or some other signal(s).

Securities behave differently from one another and this strategy doesn't work for all of them. As with any strategy, check past performance to make sure this approach is a good fit. Bandwidth ( volatility ) squeeze is another strategy which seems to work well for this security. For that reason, it was used to demonstrate buy signals, but squeezes aren't always so predictable. AD% may be useful for determining which direction a squeeze will resolve itself, as was the case here. Further information on volatility squeeze trading can be found in the John Bollinger book Bollinger on Bollinger Bands or online.

The default TradingView Accumulation Distribution indicator does not incorporate opening price. The formula used for this indicator does, so there are multiple versions of the A/D formula.

Despite the buy signal indicated, I'm not going long Hecla Mining here and I don't recommend it. I'd need to do further DD before doing so.

Please feel free to ask questions.

+ Accumulation/DistributionThis is an updated version (with lots of extras added) of the Accumulation/Distribution indicator coded by @Cl8DH.

You can read about what he says about his indicator, and how to use it, here:

So, from that, what have I done?

I added a moving average (of which there are many types to choose from) so that you can use this as a "two lines cross" indicator, as well as a "mid-line cross" indicator.

I added Bollinger Bands (primarily for when "range" is turned off, but if you want to use the Bands with it in fixed range mode too, that's fine. You do you.).

I added candle coloring for both ways of using this indicator:

In rangebound mode there is overbought and oversold coloring, as well as bullish (ADP above the MA and median) and bearish (ADP below the MA and median), and neutral (ADP is above the MA but below the median, or below the MA and above the median). With range turned off there is no overbought or oversold of course. Above the MA and median is bullish, below both is bearish, and neutral covers that grey area where it's neither one nor the other.

The indicator itself is also colored in the same way the candles are. The MA and BBands are biased colored as well (green/red).

Alerts for pretty much every condition imaginable.

Please note in the image above the indicator is pretty gaudy. I don't use it like that, and you can turn a lot of that stuff off (lines, shading, etc.). That is just the default settings.

Like I said, I think Bollinger Bands make most sense if you have it set to range off, but they could be useful either way. Depends on you, the trader.

The candle color is 100% based on the moving average, so if you are using the BBands, set your MA to the default 20 SMA because that's what BBands use for the basis. If you just turn off the MA, whatever it is set to the indicator will still see that and use it (unless you turn off candle colors) to color the candles.

Above is the same image, but just with range turned off, and the Bollinger Bands turned off.

That's all. Hope you like this! It's becoming a favorite of mine, and a lot of what I've implemented here will be added to my previously released indicators, as well as any new ones.

Volume using Candle RangeAnother way of finding out a rough estimate of the volume or how much bulls or bears were in control using only the range of the candlesticks in relation to the closing price. If the close is in the higher range zone then the volume is said to have been positive, if the close is in the lower range zone then the volume is said to have been negative. The close is compared to the midpoint of the candle to see how far from the midpoint the close was.

The columns bars show how far each candlestick's close price is to the midpoint of its high and low. It's possible for the column bar to be a different color than the candlestick itself if the close was above or below the midpoint. An average line is shown that takes the average of a given length amount of column bars. There is an option to show the absolute value only of the columns and the average line.

This is based on an idea I found about candlestick range bars implying volume. This is an attempt to put that theory into practice and to see if there's any truth to it. It's not exactly volume and may not always look like it, and it does not show how many trades took place but instead tries to use price in relation to the high and low range.

OBV Accumulation / Distribution Strategy CryptoThis version its made for 8-12h and works amazingly on the ETH pairs. Can be adapted to others as well

For this example, I used an initial 1$ account, using always full capital on each trade(without using any leverage), together with a 0.1% commission/fees for each deal, on Coinbase broker.

This is a long only strategy

The components for the inside of the strategy are the next one :

1. OBV Accumulation/Distribution

3. EMA

The rules here are simple : we check for cross up or above on OBV and EMAmoving average and after that we check for the trend direction based on ascending/descending OBV. Based on this we enter long or exit long.

RISK WARNING

Trading on any financial market involves a risk of loss. Please consider carefully if such trading is appropriate for you. Past performance is not indicative of future results.

If you have any questions or you are interested in trying it, private message me and I will give you as soon as I see the message a trial for it.

Divergence TemplateDivergence Template!

This public indicator helps you to find as many divergences with as many indicators you like, without the long hassle of knowing and coding the divergence yourself.

Just replace the "Divergence Condition" with your formula and give it a title in the second step, everything simply illustrated to someone without any coding experience!

This example is calculating A/D Divergences.

Let's make 2021 great!

With help of @madoqa.

A/D + 21/200EMASimple Accumulation & Distribution indicator with the 21 and 200EMA plotted on it. Might be a useful tool in your arsenal.

Whale Hunter [Gu5]Indicator to show a big change (Whale) in the same candle

The candles change color, until the Momentum returns to zero

After the movement of a whale, the market is usually on range, and there may be false entries

The default values (2.618% and 20 lenght), are optimized for BTCUSD 15m

---

Spanish

Este indicador muestrar un gran cambio porcentual (ballena) en la misma vela

Las velas cambian de color, hasta que el Momentum vuelve a cero

Luego de el movimiento de una ballena, el mercado suele quedar en lateral, y puede haber falsas entradas

Los valores por defecto (2.618% y 20 lenght), están optimizados para BTCUSD 15m

Accumulation/Distribution Open Interest Money Flow Hi, this script is the version of Accumulation / Distribution Money Flow (ADMF) that uses Open Interes ts in the required markets instead of Volume.

Can be set from the menu. (Futures/Others)

NOTE: I only modified this script.

The original script belongs to cl8DH.

Original of the script:

I think it will make a difference in the future and commodity markets.

Since the system uses CFTC data, use only for 1W timeframe.

With my best regards..

Whale Trading SystemThis script is an advanced version of the distributional blocks script.

In distributional buys and sells:

I used a high - low cloud filter, which makes it more prudent to sell the next sell higher for sells and to buy the next purchase lower for buys.

I also used the Stochastic Money Flow Index function because it also uses volume to separate regions.

The long period is 52 weeks, which is equal to one year,

The short period is one-fourth of its value, which is equal to a financial quarter.

Then the values calculated with these periods are calculated by stochastic - rsi logic within the function, giving us two averages and separating the regions according to crossovers and crossunders .

In buys and sales, the higher your next distributional position size makes your profit more .

In the old system, there was a confusion as it was not divided into zones.

Because we divide into zones here, zone changes are the last stop to free up existing positions, and you must reopen each time you change zones.

And I changed standard distribution days, depending on the price change and the histogram, as StochMFI also took into account the volume.

In this way, there is sustainability.

I am also sharing my educational idea that explains the logic of this system in more detail :

Now that we have been divided into regions, a maximum of 10 pieces will suffice us.

And the regional shifts will allow us to sell and buy all of our position size, and now we will feel much more comfortable.

The most timeframe I find most accurate are the weekly bars.

Even in the example, we see how we have benefited from the sharp drop in bitcoin, while the price is falling, and we have lowered the average with higher-weight purchases than the previous one.

In both buys and sales here, both the histogram intensities and the average of the purchases you have reduced with the transactions, or the earnings you have increased with the sales, guide you.

In areas with high volatility ,if we adjust our positions properly, even if we follow the changes in the region, we will get rid of those situations with few wounds and we will surely catch the trend!

NOTE : Crossover/crossunder and distributional buy/sell alerts added.

Best regards , Noldo.

Distribution Position Size Panel

This panel is an example position size panel that I prepared and I consider the rates reasonable.

I have prepared this panel so that the money allocated to the investment ends 14 consecutive signals.

The sum of the ratios is 100 units.

You can adjust your positions according to this panel.

The first steps are low rates.

If the phrases are strong, you can specify a position size from the lower digits.

Likewise, when you make a big profit, you can empty your profits in the lower steps.

In the event of a color change, you can return to the beginning or lower limit.

NOTE: This script is an auxiliary command to the distribution blocks script,

if you want to use another script, you can add distribution days to yours.

14 th stake does not appear in the preview, you need to reduce the size of the distribution blocks indicator slightly.

Rafael Zioni's examples of the panels helped a lot, thanks to him.

Stay tuned ! Regards , Noldo.

Distribution BlocksThis idea has been created by the combination of the two existing systems as a result of my efforts to create a distributional buying and selling guide that has plagued my head for a long time.

1st idea is Accumulation / Distribution Line :

2nd idea is Distribution Day :

These two ideas, the intellectual assistance of professional brokers, and my observations of cot data played a role in the formation of this idea.

Let's start.

No matter how often we divide our risk, both our minds are not comfortable and our capital may end at any moment, and if we do not use professional systems, our chances of success are 50 percent.

If we take this system as an aid to our classic systems, we can determine the amount of risk with those predictions and gradually trade.

If we don't use leverage and we have a little predictive ability, our chances of success go above 50 percent.

But for the first time, we can keep our first lot very low and increase the number of positions in the same order of orders (example: buy and buy and buy).

If we keep the first amount low, the folds won't hurt us.

When we catch up with the trend, purchases with larger position sizes than lower prices lower our average price, so that we can make a good profit when the rising trend starts.

By accepting the zone changes as the reset point just like in the martingale system, we enter the folds in the new zone with our first lot weight.

Although we cannot catch the trend, we determine the stoploss level by adding the first point we entered or the first point we entered and the commission cost.

In fact, this method is the method of buying and selling very large traders and producers, banks, pro-brokers, hedge funds and in other words the new popular phrase "whales".

Because if he trades otherwise, he cannot find buyers because his goods are too big.

I like the comfort of mind in this way.

Finally, your methods separating the negative and positive regions (macd, rsi, interpretation observation etc.)

the stronger you are, the higher your success rate.

I think the Accumulation Distribution method is very successful, but it can be adjusted for the period.

I can't wait to integrate my relativity system on this.

And when my deep learning series is over, I will integrate them on ANN series and share them publicly.

To start with, I can say briefly.

If your capital is 100:

(first lot + (increase multiplier * first lot) + (increase multiplier * increase multiplier * first lot) + .....) = 100

I tell you that you can have the same position in this series 10 - 15 times,

this will help you decide how small a position size is to be used as the starting rate and choose a low increment multiplier!

I think that this idea cannot be converted into strategy, because when our expectations come true, we may want to free all positions and start again.And I think that's better.

And in sudden movements and developments we take action with different expectations.

I'm going to talk about this script's calculations and profits on educational ideas.

Regards , Noldo.

Volume Ticks - Increasing Volume Bar Count [LucF]Volume Ticks is a zero-lag market sentiment indicator. It works by providing a cumulative count of increasing volume columns.

A one count is added for each increasing volume column where close>open, and one is subtracted on an increasing volume column if close

Distribution Days-BuschiThis script is a simple extension of the script "Distribution Day" from user "kalle2017". Thanks to him!

As the name suggests, the idea is to recognize "distribution days", when the "firm hands sell to the shaky hands" (Kostolany). So, too many distribution days in a certain timeframe can be a sign for a coming correction / bear market.

A distribution day gets triggered when a loss compared on the day before exceeds 0.2 % and the trading volume is higher.

This indicator works on any daily chart symbol but should be primarily used on major indexes.

Possible inputs are "days back" to count how many trading should be examined(default: 25). Additionally, I implemented the possibility to draw a moving average (default: exponential, 50), to eliminate distribution days below, because it is more of an indicator for the upside. Perhaps a little bit too much / too complicated, therefore it is off by default.