Adaptive

Variable Index Dynamic Average (VIDYA)Variable Index Dynamic Average indicator script based on the original version by Tushar Chande.

Adaptive Donchian ChannelThis indicator adds a level of adaptivity to the simple Donchian Channel by adjusting the sensitivity (lookback periods) of the channel's upper and lower bounds based on the amount of time that has elapsed since the price has hit/expanded the channel boundaries. Comparing the results of this indicator to the standard Donchian Channel, the readier level of responsiveness may prove self-evident.

METHODOLOGY:

Specifically, the more recently the channel was expanded in one direction, the longer the lookback period grows in that direction. Conversely, if the channel has not been expanded in a given direction, the lookback period will contract so as to allow for a tighter channel.

For example, let the initial lookback period be 20 bars and let the factor argument be 0.1 (or 2 bars to start, as 20*0.1 = 2). Now say the current bar sets a new 20-period high. Then the lookback period for the upper bound is expanded by 2 bars to 22, and the lookback period for the lower bound is contracted by 2 bars to 18, thereby making it simultaneously harder to set new highs and easier to set new lows (and vice versa for hitting new lows). If neither a new high nor a new low is formed, both periods contract by the given factor.

Kaufman Adaptive Moving Average (day)The KAMA will not change when the interval changes from day to something like 5 minutes or 30 minutes. Allows for more precise trading with the same indicator on a different interval.

Kaufman Adaptive Moving AverageFrom Stockcharts.com:

"Developed by Perry Kaufman, Kaufman's Adaptive Moving Average (KAMA) is a moving average designed to account for market noise or volatility. KAMA will closely follow prices when the price swings are relatively small and the noise is low. KAMA will adjust when the price swings widen and follow prices from a greater distance. This trend-following indicator can be used to identify the overall trend, time turning points and filter price movements."

This is different from other users' KAMA's because it allows the user to adjust more parameters that can adjust the indicator in more precise ways without needing to change the source code.

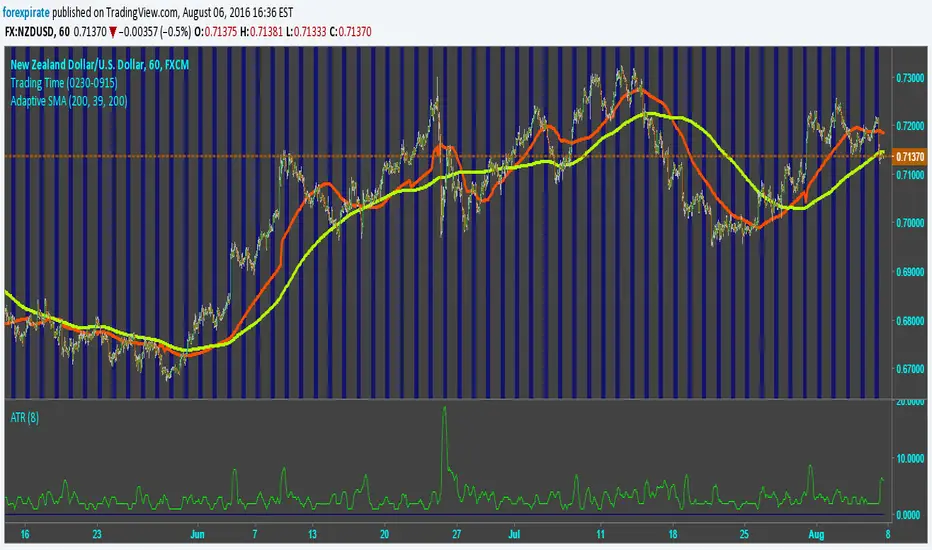

Adaptive SMACoders,

I am working on this adaptive SMA. It has its pros and cons. It is a work in progress and I welcome any one that wants to add or change it. If you add or make positive changes please let me know. It is based off of daily range. Currently it is set to the open three days prior to the current open.

Fractal Adaptive Moving AverageSettings:

FRAMA: blue line, SC = 252, FC = 40, length = 252

EMA: orange line, length = 50

FRAMA seems to be the evolution of the current and much-used EMA. The basic strategy is simple: long if the price crosses up the line, short or exit if vice versa.

The main difference between EMA and FRAMA is that the first one seems to lag much more than the first one, as we can see from the chart below (crude oil daily chart)

FYI

etfhq.com

quantstrattrader.wordpress.com

Adaptive Ergodic Candlestick Oscillator [LazyBear]This updates Blau's excellent Candlestick oscillator to be adaptive by using the length of a scaled stochastic indicator and an exponent (for calculating the smoothing coefficient) to obtain the moving average.

Check out the options page for configurable variables.

More info on Ergodic Oscillator:

Book: "Momentum, Direction and Divergence" by William Blau

List of my public indicators: bit.ly

List of my app-store indicators: blog.tradingview.com

Ehlers Smoothed Adaptive Momentum [LazyBear]Bored of Ehlers yet? :) I still have plenty of Ehlers in my collection, was thinking of publishing one of his Fishers or Adaptive RVI next, but @ChartArt requested Smoothed Adaptive Momentum (SAM), so here we go...

This is my 200th script (not including the variations and other custom scripts I shared over PM). My complete list of indicators here - bit.ly

Now, about the indicator :)

This smoothed adaptive momentum is straightforward to use (per Ehlers original rules). If it crosses above zero buy the next open, if it crosses below zero sell the next open. Of course, I strongly suggest filtering the signals.

Finally, here's an Ehlers-only chart to help determine where BTC is heading :P

More info:

- Ehlers CG Oscillator:

- Cybernetic Analysis for Stocks and Futures (Ehlers)

List of my public indicators: bit.ly

List of my app-store indicators: blog.tradingview.com

--Updated chart--

Here's the chart with barcolors ON (forgot to turn it on in the published one)

Ehlers Adaptive CG Indicator [LazyBear]Lets go with another adaptive indicator today. BTW, this is my 199th script (1 more and I am planning to work on my other backlogs).

This is the adaptive version of Ehlers' Center Of Gravity (CG) (already published, check "More info" below). Idea behind making something "adaptive" is to calculate it using dynamic cycle period inputs instead of static setting. In adaptive CG, Ehlers uses the dominant cycle period as the length in computation of alpha.

According to Ehlers this should be more responsive than the non-adaptive version. Buy and sell signals should often occur one bar earlier than for the non-adaptive version.

I have the usual options in place. Check out plain CC for comparison.

Here's a quick comparison between CG and Adaptive CG:

More info:

- Ehlers CG Oscillator:

- Cybernetic Analysis for Stocks and Futures (Ehlers)

List of my public indicators: bit.ly

List of my app-store indicators: blog.tradingview.com

Ehlers Adaptive Cyber Cycle Indicator [LazyBear]Another famous Ehlers indicator.

This is the adaptive version of Ehlers' Cyber Cycle (CC) (already published, check "More info" below). Idea behind making something "adaptive" is to calculate it using dynamic cycle period inputs instead of static setting. In adaptive cyber cycle, Ehlers uses the dominant cycle period as the length in computation of alpha.

According to Ehlers this should be more responsive than the non-adaptive version. Buy and sell signals should often occur one bar earlier than for the non-adaptive version.

I have the usual options in place. Check out plain CC for comparison.

More info:

- Cyber Cycle Indicator:

- Cybernetic Analysis for Stocks and Futures (Ehlers)

List of my public indicators: bit.ly

List of my app-store indicators: blog.tradingview.com

Ehlers MESA Adaptive Moving Average [LazyBear]Another one to add to Ehlers collection.

The MESA Adaptive Moving Average (MAMA) adapts to price movement based on the rate of change of phase as measured by the Hilbert Transform Discriminator. This method features a fast attack average and a slow decay average so that composite average rapidly ratchets behind price changes and holds the average value until the next ratchet occurs. Consider FAMA (Following AMA) as the signal.

Here are some of the options:

Fill MAMA/FAMA region (ribbon mode):

Mark Crossovers:

The above options (along with the bar colors) allow this to be used as a standalone system.

BTW, John Ehlers calls MAMA, "Mother of all Adaptive Moving Averages", lemme know what you think :)

More info:

- MESA Adaptive Moving Average, Stocks and Commodities Magazine, August 2001

- MAMA: www.mesasoftware.com

List of my public indicators: bit.ly

List of my app-store indicators: blog.tradingview.com

Kaufman Moving Average Adaptive (KAMA) Everyone wants a short-term, fast trading trend that works without large

losses. That combination does not exist. But it is possible to have fast

trading trends in which one must get in or out of the market quickly, but

these have the distinct disadvantage of being whipsawed by market noise

when the market is volatile in a sideways trending market. During these

periods, the trader is jumping in and out of positions with no profit-making

trend in sight. In an attempt to overcome the problem of noise and still be

able to get closer to the actual change of the trend, Kaufman developed an

indicator that adapts to market movement. This indicator, an adaptive moving

average (AMA), moves very slowly when markets are moving sideways but moves

swiftly when the markets also move swiftly, change directions or break out of

a trading range.