Fair Value Lead-Lag Model [BackQuant]Fair Value Lead-Lag Model

A cross-asset model that estimates where price "should" be relative to a chosen reference series, then tracks the deviation as a normalized oscillator. It helps you answer two questions: 1) is the asset rich or cheap vs its driver, and 2) is the driver leading or lagging price over the next N bars.

Concept in one paragraph

Many assets co-move with a macro or sector driver. Think BTC vs DXY, gold vs real yields, a stock vs its sector ETF. This tool builds a rolling fair value of the charted asset from a reference series and shows how far price is above or below that fair value in standard deviation units. You can shift the reference forward or backward to test who leads whom, then use the deviation and its bands to structure mean-reversion or trend-following ideas.

What the model does

Reference mapping : Pulls a reference symbol at a chosen timeframe, with an optional lead or lag in bars to test causality.

Fair value engine : Converts the reference into a synthetic fair value of the chart using one of four methods:

Ratio : price/ref with a rolling average ratio. Good when the relationship is proportional.

Spread : price minus ref with a rolling average spread. Good when the relationship is additive.

Z-Score : normalizes both series, aligns on standardized units, then re-projects to price space. Good when scale drifts.

Beta-Adjusted : rolling regression style. Uses covariance and variance to compute beta, then builds a fair value = mean(price) + beta * (ref − mean(ref)).

Deviation and bands : Computes a z-scored deviation of price vs fair value and plots sigma bands (±1, ±2, ±3) around the fair value line on the chart.

Correlation context : Shows rolling correlation so you can judge if deviations are meaningful or just noise when co-movement is weak.

Visuals :

Fair value line on price chart with sigma envelopes.

Deviation as a column oscillator and optional line.

Threshold shading beyond user-set upper and lower levels.

Summary table with reference, deviation, status, correlation, and method.

Why this is useful

Mean reversion framework : When correlation is healthy and deviation stretches beyond your sigma threshold, probability favors reversion toward fair value. This is classic pairs logic adapted to a driver and a target.

Trend confirmation : If price rides the fair value line and deviation stays modest while correlation is positive, it supports trend persistence. Pullbacks to negative deviation in an uptrend can be buyable.

Lead-lag discovery : Shift the reference forward by +N bars. If correlation improves, the reference tends to lead. Shift backward for the reverse. Use the best setting for planning early entries or hedges.

Regime detection : Large persistent deviations with falling correlation hint at regime change. The relationship you relied on may be breaking down, so reduce confidence or switch methods.

How to use it step by step

Pick a sensible reference : Choose a macro, index, currency, or sector driver that logically explains the asset’s moves. Example: gold with DXY, a semiconductor stock with SOXX.

Test lead-lag : Nudge Lead/Lag Periods to small positive values like +1 to +5 to see if the reference leads. If correlation improves, keep that offset. If correlation worsens, try a small negative value or zero.

Select a method :

Start with Beta-Adjusted when the relationship is approximately linear with drift.

Use Ratio if the assets usually move in proportional terms.

Use Spread when they trade around a level difference.

Use Z-Score when scales wander or volatility regimes shift.

Tune windows :

Rolling Window controls how quickly fair value adapts. Shorter equals faster but noisier.

Normalization Period controls how deviations are standardized. Longer equals stabler sigma sizing.

Correlation Length controls how co-movement is measured. Keep it near the fair value window.

Trade the edges :

Mean reversion idea : Wait for deviation beyond your Upper or Lower Threshold with positive correlation. Fade back toward fair value. Exit at the fair value line or the next inner sigma band.

Trend idea : In an uptrend, buy pullbacks when deviation dips negative but correlation remains healthy. In a downtrend, sell bounces when deviation spikes positive.

Read the table : Deviation shows how many sigmas you are from fair value. Status tells you overvalued or undervalued. Correlation color hints confidence. Method tells you the projection style used.

Reading the display

Fair value line on price chart: the model’s estimate of where price should trade given the reference, updated each bar.

Sigma bands around fair value: a quick sense of residual volatility. Reversions often target inner bands first.

Deviation oscillator : above zero means rich vs fair value, below zero means cheap. Color bins intensify with distance.

Correlation line (optional): scale is folded to match thresholds. Higher values increase trust in deviations.

Parameter tips

Start with Rolling Window 20 to 30, Normalization Period 100, Correlation Length 50.

Upper and Lower Threshold at ±2.0 are classic. Tighten to ±1.5 for more signals or widen to ±2.5 to focus on outliers.

When correlation drifts below about 0.3, treat deviations with caution. Consider switching method or reference.

If the fair value line whipsaws, increase Rolling Window or move to Beta-Adjusted which tends to be smoother.

Playbook examples

Pairs-style reversion : Asset is +2.3 sigma rich vs reference, correlation 0.65, trend flat. Short the deviation back toward fair value. Cover near the fair value line or +1 sigma.

Pro-trend pullback : Uptrend with correlation 0.7. Deviation dips to −1.2 sigma while price sits near the −1 sigma band. Buy the dip, target the fair value line, trail if the line is rising.

Lead-lag timing : Reference leads by +3 bars with improved correlation. Use reference swings as early cues to anticipate deviation turns on the target.

Caveats

The model assumes a stable relationship over the chosen windows. Structural breaks, policy shocks, and index rebalances can invalidate recent history.

Correlation is descriptive, not causal. A strong correlation does not guarantee future convergence.

Do not force trades when the reference has low liquidity or mismatched hours. Use a reference timeframe that captures real overlap.

Bottom line

This tool turns a loose cross-asset intuition into a quantified, visual fair value map. It gives you a consistent way to find rich or cheap conditions, time mean-reversion toward a statistically grounded target, and confirm or fade trends when the driver agrees.

Correlation

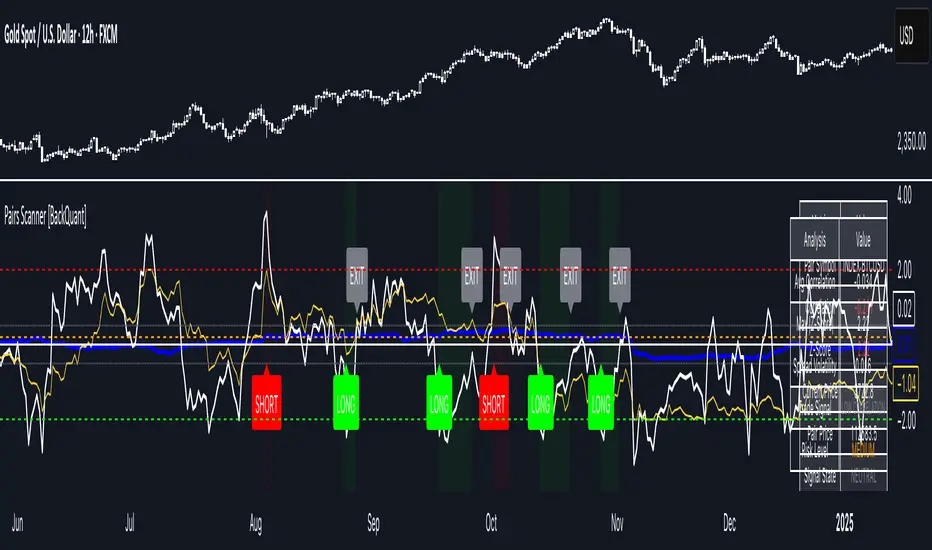

Pairs Trading Scanner [BackQuant]Pairs Trading Scanner

What it is

This scanner analyzes the relationship between your chart symbol and a chosen pair symbol in real time. It builds a normalized “spread” between them, tracks how tightly they move together (correlation), converts the spread into a Z-Score (how far from typical it is), and then prints clear LONG / SHORT / EXIT prompts plus an at-a-glance dashboard with the numbers that matter.

Why pairs at all?

Markets co-move. When two assets are statistically related, their relationship (the spread) tends to oscillate around a mean.

Pairs trading doesn’t require calling overall market direction you trade the relative mispricing between two instruments.

This scanner gives you a robust, visual way to find those dislocations, size their significance, and structure the trade.

How it works (plain English)

Step 1 Pick a partner: Select the Pair Symbol to compare against your chart symbol. The tool fetches synchronized prices for both.

Step 2 Build a spread: Choose a Spread Method that defines “relative value” (e.g., Log Spread, Price Ratio, Return Difference, Price Difference). Each lens highlights a different flavor of divergence.

Step 3 Validate relationship: A rolling Correlation checks if the pair is moving together enough to be tradable. If correlation is weak, the scanner stands down.

Step 4 Standardize & score: The spread is normalized (mean & variability over a lookback) to form a Z-Score . Large absolute Z means “stretched,” small means “near fair.”

Step 5 Signals: When the Z-Score crosses user-defined thresholds with sufficient correlation , entries print:

LONG = long chart symbol / short pair symbol,

SHORT = short chart symbol / long pair symbol,

EXIT = mean reversion into the exit zone or correlation failure.

Core concepts (the three pillars)

Spread Method Your definition of “distance” between the two series.

Guidance:

Log Spread: Focuses on proportional differences; robust when prices live on different scales.

Price Ratio: Classic relative value; good when you care about “X per Y.”

Return Difference: Emphasizes recent performance gaps; nimble for momentum-to-mean plays.

Price Difference: Straight subtraction; intuitive for similar-scale assets (e.g., two ETFs).

Correlation A rolling score of co-movement. The scanner requires it to be above your Min Correlation before acting, so you’re not trading random divergence.

Z-Score “How abnormal is today’s spread?” Positive = chart richer than pair; negative = cheaper. Thresholds define entries/exits with transparent, statistical context.

What you’ll see on the chart

Correlation plot (blue line) with a dashed Min Correlation guide. Above the line = green zone for signals; below = hands off.

Z-Score plot (white line) with colored, dashed Entry bands and dotted Exit bands. Zero line for mean.

Normalized spread (yellow) for a quick “shape read” of recent divergence swings.

Signal markers :

LONG (green label) when Z < –Entry and corr OK,

SHORT (red label) when Z > +Entry and corr OK,

EXIT (gray label) when Z returns inside the Exit band or correlation drops below the floor.

Background tint for active state (faint green for long-spread stance, faint red for short-spread stance).

The two built-in dashboards

Statistics Table (top-right)

Pair Symbol Your chosen partner.

Correlation Live value vs. your minimum.

Z-Score How stretched the spread is now.

Current / Pair Prices Real-time anchors.

Signal State NEUTRAL / LONG / SHORT.

Price Ratio Context for ratio-style setups.

Analysis Table (bottom-right)

Avg Correlation Typical co-movement level over your window.

Max |Z| The recent extremes of dislocation.

Spread Volatility How “lively” the spread has been.

Trade Signal A human-readable prompt (e.g., “LONG A / SHORT B” or “NO TRADE” / “LOW CORRELATION”).

Risk Level LOW / MEDIUM / HIGH based on current stretch (absolute Z).

Signals logic (plain English)

Entry (LONG): The spread is unusually negative (chart cheaper vs pair) and correlation is healthy. Expect mean reversion upward in the spread: long chart, short pair.

Entry (SHORT): The spread is unusually positive (chart richer vs pair) and correlation is healthy. Expect mean reversion downward in the spread: short chart, long pair.

Exit: The spread relaxes back toward normal (inside your exit band), or correlation deteriorates (relationship no longer trusted).

A quick, repeatable workflow

1) Choose your pair in context (same sector/theme or known macro link). Think: “Do these two plausibly co-move?”

2) Pick a spread lens that matches your narrative (ratio for relative value, returns for short-term performance gaps, etc.).

3) Confirm correlation is above your floor no corr, no trade.

4) Wait for a stretch (Z beyond Entry band) and a printed LONG / SHORT .

5) Manage to the mean (EXIT band) or correlation failure; let the scanners’ state/labels keep you honest.

Settings that matter (and why)

Spread Method Defines the “mispricing” you care about.

Correlation Period Longer = steadier regime read, shorter = snappier to regime change.

Z-Score Period The window that defines “normal” for the spread; it sets the yardstick.

Use Percentage Returns Normalizes series when using return-based logic; keep on for mixed-scale assets.

Entry / Exit Thresholds Set your stretch and your target reversion zone. Wider entries = rarer but stronger signals.

Minimum Correlation The gatekeeper. Raising it favors quality over quantity.

Choosing pairs (practical cheat sheet)

Same family: two index ETFs, two oil-linked names, two gold miners, two L1 tokens.

Hedge & proxy: stock vs. sector ETF, BTC vs. BTC index, WTI vs. energy ETF.

Cross-venue or cross-listing: instruments that are functionally the same exposure but price differently intraday.

Reading the cues like a pro

Divergence shape: The yellow normalized spread helps you see rhythm fast spike and snap-back versus slow grind.

Corr-first discipline: Don’t fight the “Min Correlation” line. Good pairs trading starts with a relationship you can trust.

Exit humility: When Z re-centers, let the EXIT do its job. The edge is the journey to the mean, not overstaying it.

Frequently asked (quick answers)

“Long/Short means what exactly?”

LONG = long the chart symbol and short the pair symbol.

SHORT = short the chart symbol and long the pair symbol.

“Do I need same price scales?” No. The spread methods normalize in different ways; choose the one that fits your use case (log/ratio are great for mixed scales).

“What if correlation falls mid-trade?” The scanner will neutralize the state and print EXIT . Relationship first; trade second.

Field notes & patterns

Snap-back days: After a one-sided session, return-difference spreads often flag cleaner intraday mean reversions.

Macro rotations: Ratio spreads shine during sector re-weights (e.g., value vs. growth ETFs); look for steady corr + elevated |Z|.

Event bleed-through: If one symbol reacts to news and its partner lags, Z often flags a high-quality, short-horizon re-centering.

Display controls at a glance

Show Statistics Table Live state & key numbers, top-right.

Show Analysis Table Context/risk read, bottom-right.

Show Correlation / Spread / Z-Score Toggle the sub-charts you want visible.

Show Entry/Exit Signals Turn markers on/off as needed.

Coloring Adjust Long/Short/Neutral and correlation line colors to match your theme.

Alerts (ready to route to your workflow)

Pairs Long Entry Z falls through the long threshold with correlation above minimum.

Pairs Short Entry Z rises through the short threshold with correlation above minimum.

Pairs Trade Exit Z returns to neutral or the relationship fails your correlation floor.

Correlation Breakdown Rolling correlation crosses your minimum; relationship caution.

Final notes

The scanner is designed to keep you systematic: require relationship (correlation), quantify dislocation (Z-Score), act when stretched, stand down when it normalizes or the relationship degrades. It’s a full, visual loop for relative-value trading that stays out of your way when it should and gets loud only when the numbers line up.

Bitcoin vs. Gold correlation with lagBTC vs Gold (Lag) + Correlation — multi-timeframe, publication notes

What it does

Plots Gold on the same chart as Bitcoin, with a configurable lead/lag.

Lets you choose how the series is displayed:

Gold shifted forward (+lag on chart) — shows gold ahead of BTC on the time axis (visual offset).

Gold aligned to BTC (gold lag) — standard alignment; gold is lagged for calculation and plotted in place.

BTC 200D Lag (BTC shifted forward) — visualizes BTC shifted forward (like popular “BTC 200D Lag” charts).

Computes Pearson correlations between BTC (no lag) and Gold (with lag) over multiple lookback windows equivalent to:

30d, 60d, 90d, 180d, 365d, 2y (730d), 3y (1095d), 5y (1825d).

Shows a table with the correlation values, automatically scaled to the current timeframe.

Why this is useful

A common macro claim is that BTC tends to follow Gold with a delay (e.g., ~200 trading days). This tool lets you:

Visually advance Gold (or BTC) to see that lead-lag relationship on the chart.

Quantify the relationship with rolling correlations.

Switch timeframes (D/W/M/…): everything automatically stays in sync.

Quick start

Open a BTC chart (any exchange).

Add the indicator.

Set Gold symbol (default TVC:GOLD; alternatives: OANDA:XAUUSD, COMEX:GC1!, etc.).

Choose Lag value and Lag unit (Days/Weeks/Months/Years/Bars).

Pick Visual Mode:

To mirror those “BTC 200D Lag” posts: choose “BTC 200D Lag (BTC shifted forward)” with 200 Days.

To view Gold 200D ahead of BTC: select “Gold shifted forward (+lag on chart)” with 200 Days.

Keep Rebase to 100 ON for an apples-to-apples visual scale. (You can move the study to the left price scale if needed.)

Inputs

Gold symbol: external series to pair with BTC.

Lag value: numeric value.

Lag unit: Days, Weeks, Months (≈30d), Years (≈365d), or direct Bars.

Visual mode:

Gold shifted forward (+lag on chart) → gold is offset to the right by the lag (visual only).

Gold aligned to BTC (gold lag) → standard plot (no visual offset); correlations still use lagged gold.

BTC 200D Lag (BTC shifted forward) → BTC is offset to the right by the lag (visual only).

Rebase to 100 (visual): rescales each series to 100 on its first valid bar for clearer comparison.

Show gold without lag (debug): optional reference line.

Show price tag for gold (lag): toggles the track price label.

Timeframe handling

The study uses the current chart timeframe for both BTC and Gold (timeframe.period).

Lag in time units (Days/Weeks/Months/Years) is internally converted to an integer number of bars of the active timeframe (using timeframe.in_seconds).

Example: on W (weekly), 200 days ≈ 29 bars.

On intraday timeframes, days are converted proportionally.

Correlation math

Correlation = ta.correlation(BTC, Gold_lagged, length_in_bars)

Lookback lengths are the bar-equivalents of 30/60/90/180/365/730/1095/1825 days in the active timeframe.

Important: correlations are computed on prices (not returns). If you prefer returns-based correlation (often more statistically robust), duplicate the script and replace price inputs with change(close) or ta.roc(close, 1).

Reading the table

Window: nominal day label (e.g., 30d, 1y, 5y).

Bars (TF): how many bars that window equals on the current timeframe.

Correlation: Pearson coefficient . Background tint shows intensity and sign.

Tips & caveats

Visual offsets (offset=) move series on screen only; they don’t affect the math. The math always uses BTC (no lag) × Gold (lagged).

With large lags on high timeframes, early bars will be na (normal). Scroll forward / reduce lag.

If your Gold feed doesn’t load, try an alternative symbol that your plan supports.

Rebase to 100 helps visibility when BTC ($100k) and Gold ($2k) share a scale.

Months/Years use 30/365-day approximations. For exact control, use Days or Bars.

Correlations on very short lengths or sparse data can be unstable; consider the longer windows for sturdier signals.

This is a visual/analytical tool, not a trading signal. Always apply independent risk management.

Suggested setups

Replicate “BTC 200D Lag” charts:

Visual Mode: BTC 200D Lag (BTC shifted forward)

Lag: 200 Days

Rebase: ON

Gold leads BTC (Gold ahead):

Visual Mode: Gold shifted forward (+lag on chart)

Lag: 200 Days

Rebase: ON

Compatibility: Pine v6, overlay study.

Best with: BTCUSD (any exchange) + a reliable Gold feed.

Author’s note: Lead-lag relationships are not stable over time; treat correlations as descriptive, not predictive.

AI-Weighted RSI (Zeiierman)█ Overview

AI-Weighted RSI (Zeiierman) is an adaptive oscillator that enhances classic RSI by applying a correlation-weighted prediction layer. Instead of looking only at RSI values directly, this indicator continuously evaluates how other price- and volume-based features (returns, volatility, volume shifts) correlate with RSI, and then weights them accordingly to project the next RSI state.

The result is a smoother, forward-looking RSI framework that adapts to market conditions in real time.

By leveraging feature correlation instead of static formulas, AI-Weighted RSI behaves like a lightweight learning model, adjusting its emphasis depending on which features are most aligned with RSI behavior during the current regime.

█ How It Works

⚪ Feature Extraction

Each bar, the script computes features: log returns, RSI itself, ATR% (volatility), volume, and volume log-change.

⚪ Correlation Screening

Over a rolling learning window, it measures the correlation of each feature against RSI. The strongest relationships are ranked and selected.

⚪ Adaptive Weighting

Features are standardized (z-scored), then combined using their signed correlations as weights, building a rolling, adaptive prediction of RSI.

⚪ Prediction to RSI Weight

The predicted RSI is mapped back into a “weight” scale (±2 by default). Above 0 = bullish bias, below 0 = bearish bias, with color-graded fills to visualize overbought/oversold pressure.

⚪ Signal Line

A smoothing option (signal length) overlays a moving average of the AI-Weighted RSI for clearer trend confirmation.

█ Why AI-Weighted RSI

⚪ Adaptive to Market Regime

Because the model re-evaluates correlations continuously, it naturally shifts which features dominate, sometimes volatility explains RSI best, sometimes volume, sometimes returns.

⚪ Forward-Looking Bias

Instead of simply reflecting RSI, the model provides a projection, helping anticipate shifts in momentum before RSI itself flips.

█ How to Use

⚪ Directional Bias

Read the RSI relative to 0. Above = bullish momentum bias, below = bearish.

⚪ Overbought / Oversold Zones

Shaded fills beyond +0.5 or -0.5 highlight extremes where RSI pressure often exhausts.

⚪ Divergences

When price makes new highs/lows but AI-Weighted RSI fails to confirm, it often signals weakening momentum.

█ Settings

RSI Length: Lookback for the core RSI calculation.

Signal Length: Smoothing applied to the AI-Weighted RSI output.

Learning Window: Bars used for correlation learning and z-scoring.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

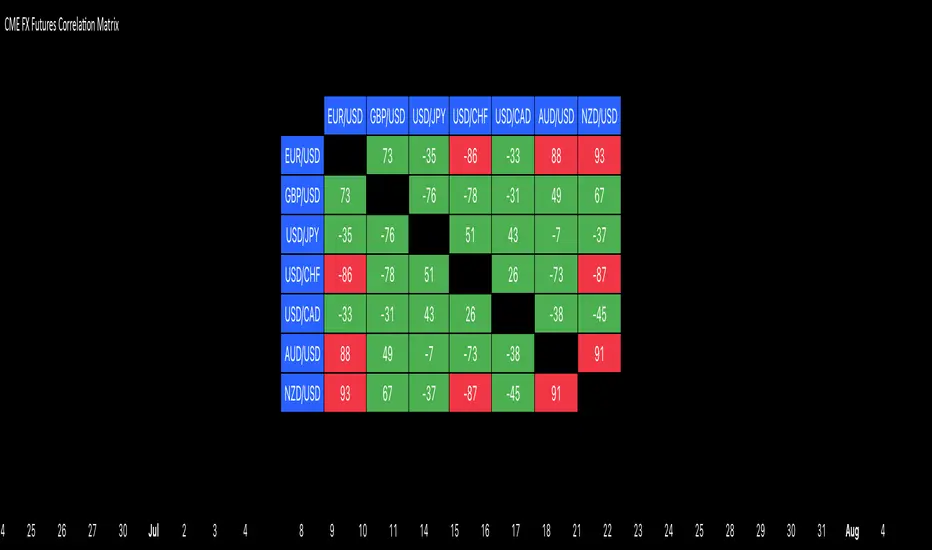

CME FX Futures Correlation MatrixThis indicator calculates the correlation between major CME FX futures and displays it in a visual table. It shows how closely pairs like EUR/USD, GBP/USD, USD/JPY, USD/CHF, USD/CAD, AUD/USD, and NZD/USD move together or in opposite directions.

The indicator inherits the timeframe of the chart it’s applied to.

Color coding:

Red: strong correlation (absolute value > 80%), both positive and negative

Green: moderate/low correlation

How to launch it

Apply the indicator to a CME chart (e.g., EUR/USD futures).

Set Numbers of Bars Back to the desired lookback period (default 100).

The table appears in the center of the chart, showing correlation percentages between all major FX futures.

PPP – Info Table (Anchor + Corr/Alpha/Beta) v3PPP – Info Table (Anchor + Corr/Alpha/Beta)

- By P3 Analytics, run by Puranam Pradeep Picasso Sharma

🔎 Overview

This indicator creates a clean, dynamic information table on your chart that lets you quickly analyze how your chosen asset is performing relative to BTC, ETH, or any other benchmarks.

With a single glance, you can see:

% change from today’s open (for the anchor asset, BTC, and ETH)

Previous day % change (self + benchmarks)

Correlation, Beta, and Alpha statistics for the selected window (1W, 1M, 1Y)

Anchor values at any bar you choose (via Bars Back or Anchor Time)

Perfect for traders who want to measure coin strength vs benchmarks and make better rotation, risk, or hedging decisions.

📊 Key Metrics

Correlation (Corr): How closely the asset moves with the benchmark.

+1 = moves together, 0 = no relation, -1 = moves opposite.

Beta (β): Sensitivity of returns vs the benchmark.

β = 1 → moves 1:1 with BTC.

β > 1 → more volatile (amplifies BTC moves).

β < 1 → less volatile (defensive).

Alpha (α): Excess return beyond what Beta predicts.

Positive α = outperforming benchmark-adjusted expectation.

Negative α = underperforming.

⚙️ Features

Flexible Anchor Mode:

Bars Back → quickly step through bars.

Time → pin analysis to a specific historical candle.

Customizable Benchmarks: Default BTC & ETH (futures), but replaceable with any ticker.

Adjustable Stats Window:

1 Week, 1 Month, 1 Year (auto-scales if using chart timeframe).

Compact Mode for a smaller table layout.

Dark/Light Theme, font size, corner placement, transparency, and decimal control.

Runs efficiently with minimal chart clutter.

🧑💻 About P3 Analytics

This indicator is developed under P3 Analytics, a research & trading technology initiative led by Puranam Pradeep Picasso Sharma.

P3 Analytics builds tools that merge machine learning, statistics, and trading strategy into accessible products for traders across crypto, equities, forex, and commodities.

✅ How to Use

Add indicator to your chart.

In settings:

Pick your benchmarks (default = BTCUSDT.P, ETHUSDT.P).

Choose your anchor (Bars Back or Time).

Set window length for correlation/alpha/beta.

Read the table:

Left side = your asset.

Right side = benchmarks.

Colors: Green = positive % change, Red = negative.

🚀 Why Use This?

Quickly compare your asset vs BTC/ETH without juggling multiple charts.

Spot whether a coin is truly leading or just following BTC.

Identify outperformance (alpha) coins for rotation or trend plays.

Manage risk by knowing which assets are high beta (high leverage-like moves).

✦ Indicator by P3 Analytics

✦ Created & published by Puranam Pradeep Picasso Sharma

Rolling Performance Toolkit (Returns, Correlation and Sharpe)This script provides a flexible toolkit for evaluating rolling performance metrics between any asset and a benchmark.

Features:

Library-based: Built on a custom utilities library for consistent return and statistics calculations.

Rolling Window Control: Choose the lookback period (in days) to calculate metrics.

Multiple Modes: Toggle between Rolling Returns, Rolling Correlation, and Rolling Sharpe Ratio.

Benchmark Comparison: Compare your selected ticker against a benchmark (default: S&P 500 / SPX), but you can easily switch to any symbol.

Risk-Free Rate Options: Choose from zero, a constant annual % rate, or a proxy symbol (default: US03M – 3-Month Treasury Yield).

Annualized Sharpe: Sharpe ratios are annualized by default (×√252) for intuitive interpretation.

This tool is useful for traders and investors who want to monitor relative performance, diversification benefits, or risk-adjusted returns over time.

utilitiesLibrary for commonly used utilities, for visualizing rolling returns, correlations and sharpe

Crypto Strength MatrixOverview

The "Crypto Strength Matrix" is a custom Pine Script v5 indicator designed for cryptocurrency traders to assess the relative strength of major crypto market segments against traditional markets (e.g., the U.S. Dollar Index) and Bitcoin dominance. This indicator plots the strength of Altcoins (excluding ETH and SOL), Ethereum (ETH), Solana (SOL), the Dollar Index (DXY) versus Altcoins, and Bitcoin Dominance (DOM) on a 0-100 scale, using the Relative Strength Index (RSI) methodology. It provides a visual and intuitive way to identify overbought (>70) or oversold (<30) conditions across these assets, helping traders spot potential entry or exit points in the crypto market.

How It Works

The indicator fetches real-time data from various crypto and forex symbols available on TradingView, including:

CRYPTOCAP:TOTAL2 (total altcoin market cap),

CRYPTOCAP:ETH and CRYPTOCAP:SOL (market caps of ETH and SOL),

CRYPTO:ETHUSD and CRYPTO:SOLUSD (ETH and SOL prices),

CRYPTOCAP:BTC.D (Bitcoin dominance),

TVC:DXY (U.S. Dollar Index).

Calculations:

Altcoin Strength (OTH): Measures the RSI of the normalized market cap of all altcoins excluding ETH and SOL (calculated as TOTAL2 - ETH - SOL), relative to the total altcoin market cap. This reflects the strength of smaller altcoins.

ETH Strength: Computes the RSI of ETH/USD price adjusted by the DXY, isolating ETH's performance against the dollar.

SOL Strength: Similar to ETH, calculates the RSI of SOL/USD price adjusted by the DXY, focusing on Solana's strength.

DXY vs Altcoins: Uses the RSI of the DXY divided by the normalized total altcoin market cap, indicating the dollar's strength relative to altcoins.

Bitcoin Dominance (DOM): Directly applies RSI to Bitcoin dominance data, showing BTC's market control.

Each metric is plotted as a line with a unique color (OTH in aqua, ETH in teal, SOL in purple, DXY in green, DOM in orange) and labeled at the end of the chart for easy identification. Horizontal lines at 70 (overbought), 50 (neutral), and 30 (oversold) provide reference levels.

How to Use

Add the Indicator: Apply the "Crypto Strength Matrix" to a cryptocurrency chart (e.g., BTC/USD or ETH/USD) on a daily or 4-hour timeframe for optimal results.

Interpret the Lines:

OTH (Altcoins excluding ETH and SOL): A value above 70 suggests strong momentum in smaller altcoins, while below 30 indicates weakness. Monitor for divergence with ETH and SOL.

ETH and SOL: High values (>70) signal potential overbought conditions for these assets, while low values (<30) may indicate oversold opportunities.

DXY: Rising above 70 may suggest a stronger dollar, potentially pressuring crypto prices, while below 30 could indicate a weakening dollar, favoring crypto.

DOM: A value above 70 reflects strong Bitcoin dominance, often leading to altcoin underperformance, while below 30 may signal altcoin season.

Combine with Price Action: Use the indicator alongside candlestick patterns or volume analysis to confirm trade signals.

Adjust RSI Length: The default RSI length is 14, but you can tweak this input in the indicator settings to suit your trading style (e.g., 7 for shorter-term, 21 for longer-term trends).

Monitor Trends: Look for crossovers between lines (e.g., OTH rising above DXY) or alignment with the 50 neutral line to gauge market shifts.

Tips

Timeframe Selection: Daily charts provide a broad market view, while 4-hour charts offer more frequent signals. Avoid very short timeframes (e.g., 5m) due to noise.

Contextual Awareness: Combine with macroeconomic news (e.g., U.S. dollar strength) and Bitcoin price movements for better decision-making.

Risk Management: Use the indicator as a supplementary tool, not a standalone signal, and always set stop-losses based on your risk tolerance.

This indicator is ideal for crypto traders seeking a comprehensive view of market dynamics without the complexity of multiple charts. Enjoy trading with the "Crypto Strength Matrix"!

Correlation Heatmap Matrix [TradingFinder] 20 Assets Variable🔵 Introduction

Correlation is one of the most important statistical and analytical metrics in financial markets, data mining, and data science. It measures the strength and direction of the relationship between two variables.

The correlation coefficient always ranges between +1 and -1 : a perfect positive correlation (+1) means that two assets or currency pairs move together in the same direction and at a constant ratio, a correlation of zero (0) indicates no clear linear relationship, and a perfect negative correlation (-1) means they move in exactly opposite directions.

While the Pearson Correlation Coefficient is the most common method for calculation, other statistical methods like Spearman and Kendall are also used depending on the context.

In financial market analysis, correlation is a key tool for Forex, the Stock Market, and the Cryptocurrency Market because it allows traders to assess the price relationship between currency pairs, stocks, or coins. For example, in Forex, EUR/USD and GBP/USD often have a high positive correlation; in stocks, companies from the same sector such as Apple and Microsoft tend to move similarly; and in crypto, most altcoins show a strong positive correlation with Bitcoin.

Using a Correlation Heatmap in these markets visually displays the strength and direction of these relationships, helping traders make more accurate decisions for risk management and strategy optimization.

🟣 Correlation in Financial Markets

In finance, correlation refers to measuring how closely two assets move together over time. These assets can be stocks, currency pairs, commodities, indices, or cryptocurrencies. The main goal of correlation analysis in trading is to understand these movement patterns and use them for risk management, trend forecasting, and developing trading strategies.

🟣 Correlation Heatmap

A correlation heatmap is a visual tool that presents the correlation between multiple assets in a color-coded table. Each cell shows the correlation coefficient between two assets, with colors indicating its strength and direction. Warm colors (such as red or orange) represent strong negative correlation, cool colors (such as blue or cyan) represent strong positive correlation, and mid-range tones (such as yellow or green) indicate correlations that are close to neutral.

🟣 Practical Applications in Markets

Forex : Identify currency pairs that move together or in opposite directions, avoid overexposure to similar trades, and spot unusual divergences.

Crypto : Examine the dependency of altcoins on Bitcoin and find independent movers for portfolio diversification.

Stocks : Detect relationships between stocks in the same industry or find outliers that move differently from their sector.

🟣 Key Uses of Correlation in Trading

Risk management and diversification: Select assets with low or negative correlation to reduce portfolio volatility.

Avoiding overexposure: Prevent opening multiple positions on highly correlated assets.

Pairs trading: Exploit temporary deviations between historically correlated assets for arbitrage opportunities.

Intermarket analysis: Study the relationships between different markets like stocks, currencies, commodities, and bonds.

Divergence detection: Spot when two typically correlated assets move apart as a possible trend change signal.

Market forecasting: Use correlated asset movements to anticipate others’ behavior.

Event reaction analysis: Evaluate how groups of assets respond to economic or political events.

❗ Important Note

It’s important to note that correlation does not imply causation — it only reflects co-movement between assets. Correlation is also dynamic and can change over time, which is why analyzing it across multiple timeframes provides a more accurate picture. Combining correlation heatmaps with other analytical tools can significantly improve the precision of trading decisions.

🔵 How to Use

The Correlation Heatmap Matrix indicator is designed to analyze and manage the relationships between multiple assets at once. After adding the tool to your chart, start by selecting the assets you want to compare (up to 20).

Then, choose the Correlation Period that fits your trading strategy. Shorter periods (e.g., 20 bars) are more sensitive to recent price movements, making them suitable for short-term trading, while longer periods (e.g., 100 or 200 bars) provide a broader view of correlation trends over time.

The indicator outputs a color-coded matrix where each cell represents the correlation between two assets. Warm colors like red and orange signal strong negative correlation, while cool colors like blue and cyan indicate strong positive correlation. Mid-range tones such as yellow or green suggest correlations that are close to neutral. This visual representation makes it easy to spot market patterns at a glance.

One of the most valuable uses of this tool is in portfolio risk management. Portfolios with highly correlated assets are more vulnerable to market swings. By using the heatmap, traders can find assets with low or negative correlation to reduce overall risk.

Another key benefit is preventing overexposure. For example, if EUR/USD and GBP/USD have a high positive correlation, opening trades on both is almost like doubling the position size on one asset, increasing risk unnecessarily. The heatmap makes such relationships clear, helping you avoid them.

The indicator is also useful for pairs trading, where a trader identifies assets that are usually correlated but have temporarily diverged — a potential arbitrage or mean-reversion opportunity.

Additionally, the tool supports intermarket analysis, allowing traders to see how movements in one market (e.g., crude oil) may impact others (e.g., the Canadian dollar). Divergence detection is another advantage: if two typically aligned assets suddenly move in opposite directions, it could signal a major trend shift or a news-driven move.

Overall, the Correlation Heatmap Matrix is not just an analytical indicator but also a fast, visual alert system for monitoring multiple markets at once. This is particularly valuable for traders in fast-moving environments like Forex and crypto.

🔵 Settings

🟣 Logic

Correlation Period : Number of bars used to calculate correlation between assets.

🟣 Display

Table on Chart : Enable/disable displaying the heatmap directly on the chart.

Table Size : Choose the table size (from very small to very large).

Table Position : Set the table location on the chart (top, middle, or bottom in various alignments).

🟣 Symbol Custom

Select Market : Choose the market type (Forex, Stocks, Crypto, or Custom).

Symbol 1 to Symbol 20: In custom mode, you can define up to 20 assets for correlation calculation.

🔵 Conclusion

The Correlation Heatmap Matrix is a powerful tool for analyzing correlations across multiple assets in Forex, crypto, and stock markets. By displaying a color-coded table, it visually conveys both the strength and direction of correlations — warm colors for strong negative correlation, cool colors for strong positive correlation, and mid-range tones such as yellow or green for near-zero or neutral correlation.

This helps traders select assets with low or negative correlation for diversification, avoid overexposure to similar trades, identify arbitrage and pairs trading opportunities, and detect unusual divergences between typically aligned assets. With support for custom mode and up to 20 symbols, it offers high flexibility for different trading strategies, making it a valuable complement to technical analysis and risk management.

Correlation HeatMap [TradingFinder] Sessions Data Science Stats🔵 Introduction

n financial markets, correlation describes the statistical relationship between the price movements of two assets and how they interact over time. It plays a key role in both trading and investing by helping analyze asset behavior, manage portfolio risk, and understand intermarket dynamics. The Correlation Heatmap is a visual tool that shows how the correlation between multiple assets and a central reference asset (the Main Symbol) changes over time.

It supports four market types forex, stocks, crypto, and a custom mode making it adaptable to different trading environments. The heatmap uses a color-coded grid where warmer tones represent stronger negative correlations and cooler tones indicate stronger positive ones. This intuitive color system allows traders to quickly identify when assets move together or diverge, offering real-time insights that go beyond traditional correlation tables.

🟣 How to Interpret the Heatmap Visually ?

Each cell represents the correlation between the main symbol and one compared asset at a specific time.

Warm colors (e.g. red, orange) suggest strong negative correlation as one asset rises, the other tends to fall.

Cool colors (e.g. blue, green) suggest strong positive correlation both assets tend to move in the same direction.

Lighter shades indicate weaker correlations, while darker shades indicate stronger correlations.

The heatmap updates over time, allowing users to detect changes in correlation during market events or trading sessions.

One of the standout features of this indicator is its ability to overlay global market sessions such as Tokyo, London, New York, or major equity opens directly onto the heatmap timeline. This alignment lets traders observe how correlation structures respond to real-world session changes. For example, they can spot when assets shift from being inversely correlated to moving together as a new session opens, potentially signaling new momentum or macro flow. The customizable symbol setup (including up to 20 compared assets) makes it ideal not only for forex and crypto traders but also for multi-asset and sector-based stock analysis.

🟣 Use Cases and Advantages

Analyze sector rotation in equities by tracking correlation to major indices like SPX or DJI.

Monitor altcoin behavior relative to Bitcoin to find early entry opportunities in crypto markets.

Detect changes in currency alignment with DXY across trading sessions in forex.

Identify correlation breakdowns during market volatility, signaling possible new trends.

Use correlation shifts as confirmation for trade setups or to hedge multi-asset exposure

🔵 How to Use

Correlation is one of the core concepts in financial analysis and allows traders to understand how assets behave in relation to one another. The Correlation Heatmap extends this idea by going beyond a simple number or static matrix. Instead, it presents a dynamic visual map of how correlations shift over time.

In this indicator, a Main Symbol is selected as the reference point for analysis. In standard modes such as forex, stocks, or crypto, the symbol currently shown on the main chart is automatically used as the main symbol. This allows users to begin correlation analysis right away without adjusting any settings.

The horizontal axis of the heatmap shows time, while the vertical axis lists the selected assets. Each cell on the heatmap shows the correlation between that asset and the main symbol at a given moment.

This approach is especially useful for intermarket analysis. In forex, for example, tracking how currency pairs like OANDA:EURUSD EURUSD, FX:GBPUSD GBPUSD, and PEPPERSTONE:AUDUSD AUDUSD correlate with TVC:DXY DXY can give insight into broader capital flow.

If these pairs start showing increasing positive correlation with DXY say, shifting from blue to light green it could signal the start of a new phase or reversal. Conversely, if negative correlation fades gradually, it may suggest weakening relationships and more independent or volatile movement.

In the crypto market, watching how altcoins correlate with Bitcoin can help identify ideal entry points in secondary assets. In the stock market, analyzing how companies within the same sector move in relation to a major index like SP:SPX SPX or DJ:DJI DJI is also a highly effective technique for both technical and fundamental analysts.

This indicator not only visualizes correlation but also displays major market sessions. When enabled, this feature helps traders observe how correlation behavior changes at the start of each session, whether it's Tokyo, London, New York, or the opening of stock exchanges. Many key shifts, breakouts, or reversals tend to happen around these times, and the heatmap makes them easy to spot.

Another important feature is the market selection mode. Users can switch between forex, crypto, stocks, or custom markets and see correlation behavior specific to each one. In custom mode, users can manually select any combination of symbols for more advanced or personalized analysis. This makes the heatmap valuable not only for forex traders but also for stock traders, crypto analysts, and multi-asset strategists.

Finally, the heatmap's color-coded design helps users make sense of the data quickly. Warm colors such as red and orange reflect stronger negative correlations, while cool colors like blue and green represent stronger positive relationships. This simplicity and clarity make the tool accessible to both beginners and experienced traders.

🔵 Settings

Correlation Period: Allows you to set how many historical bars are used for calculating correlation. A higher number means a smoother, slower-moving heatmap, while a lower number makes it more responsive to recent changes.

Select Market: Lets you choose between Forex, Stock, Crypto, or Custom. In the first three options, the chart’s active symbol is automatically used as the Main Symbol. In Custom mode, you can manually define the Main Symbol and up to 20 Compared Symbols.

Show Open Session: Enables the display of major trading sessions such as Tokyo, London, New York, or equity market opening hours directly on the timeline. This helps you connect correlation shifts with real-world market activity.

Market Mode: Lets you select whether the displayed sessions relate to the forex or stock market.

🔵 Conclusion

The Correlation Heatmap is a robust and flexible tool for analyzing the relationship between assets across different markets. By tracking how correlations change in real time, traders can better identify alignment or divergence between symbols and gain valuable insights into market structure.

Support for multiple asset classes, session overlays, and intuitive visual cues make this one of the most effective tools for intermarket analysis.

Whether you’re looking to manage portfolio risk, validate entry points, or simply understand capital flow across markets, this heatmap provides a clear and actionable perspective that you can rely on.

M2 Global Liquidity Index [Extended + Empirical BTC Offset]M2 Global Liquidity Index

This script visualizes global M2 liquidity based on major economic zones (USA, China, Eurozone, Japan, UK), with the option to include extended countries such as Switzerland, Canada, India, Russia, Brazil, South Korea, Mexico, and South Africa.

The indicator includes an empirically derived offset to reflect how Bitcoin historically reacts with a time lag—typically around 12 weeks—after shifts in global liquidity.

Features:

Predefined empirical offset options ranging from 12 to 120 days

Automatic offset adjustment when applied to the weekly chart

Optional inclusion of extended global M2 sources

Important:

This indicator is intended only for use on the weekly chart. It provides meaningful and accurate results exclusively in this time frame, due to the nature of the offset-based correlation logic.

Use cases:

Macro-level analysis of Bitcoin’s price movements

Identifying early signs of potential market tops or bottoms in relation to liquidity flows

Two assets correlation trackerHi, I made this simple script to see how two correlated assets are actually performing short-term. The idea comes from correlation between BTC and ETH that that usually stands 0.9 (Pearson's correlation). However Pearson's correlation doesn't indicate the relative price difference and cannot be used trading correlation when used alone.

My approach is simple - we can select the date/time from which we will start tracking the price change, and instead of tracking the price, we track 100 USD worth of BTC and ETH and how this investment perform. This gives us the price difference relative to a point in the near future, I would suggest using latest trend shift, for example.

On example of how this can be used: If we see that BTC is falling slower than ETH since trend shift, we can long BTC and short ETH in equal parts and expect to gain from the difference while hedging potential loss.

TFPS_EngineLibrary "TFPS_Engine"

f_calculate_lead_lag(series1, series2, length, max_lag)

Parameters:

series1 (float)

series2 (float)

length (int)

max_lag (int)

f_calculate_pressure_score(spx_ticker, vix_ticker, dxy_ticker, us10y_ticker, benchmark_source, trend_lookback, score_smoothing, use_dynamic_weights, corr_lookback, w_spx, w_vix, w_dxy, w_us10y, zscore_lookback, max_lag)

Parameters:

spx_ticker (string)

vix_ticker (string)

dxy_ticker (string)

us10y_ticker (string)

benchmark_source (float)

trend_lookback (int)

score_smoothing (simple int)

use_dynamic_weights (bool)

corr_lookback (int)

w_spx (float)

w_vix (float)

w_dxy (float)

w_us10y (float)

zscore_lookback (int)

max_lag (int)

LeadLagOutput

Fields:

best_lag (series int)

max_corr (series float)

TFPS_Output

Fields:

historical_score (series float)

smoothed_score (series float)

z_score (series float)

regime_signal (series int)

lead_lag_bars (series int)

lead_lag_corr (series float)

weight_spx (series float)

weight_vix (series float)

weight_dxy (series float)

weight_us10y (series float)

TFPS - TradFi-Pressure-Score (Adaptive)The data-driven answer to an irreversible market reality.

This indicator quantifies the combined pressure from the S&P 500, VIX, DXY, and US10Y, whose correlation to crypto has reached peak values of 0.87. Your decisive macro edge, in real-time.

This indicator is built on a fundamental analysis of market data from the last five years. The analysis proves an irreversible transformation: The crypto market has evolved into a high-beta risk asset, its fate inextricably linked to Traditional Finance (TradFi).

The empirical data is clear:

Bitcoin increasingly behaves like a leveraged version of the S&P 500.

The correlation to stock indices, with peak values of up to 0.87, is statistically highly significant.

The "digital gold" safe-haven narrative is refuted by the data; the correlation to gold (0.04) is virtually non-existent and statistically insignificant.

This means: Standard indicators like RSI or MACD are insufficient for today's market conditions. They only see price, ignoring the powerful external context that now dominates price action.

The TradFi Pressure Score (TFPS) is the answer to this data-driven reality. It's your institutional-grade macro dashboard, aggregating the four most dominant external forces into a single, actionable score:

S&P 500 (SPY): The pulse of global risk appetite. A rising S&P signals a "risk-on" environment, fueling capital flows into crypto.

VIX: The market's "Fear Gauge". A rising VIX signals a "risk-off" flight to safety, draining liquidity from crypto.

DXY (US-Dollar Index): The counter-pole to risk assets. A strong Dollar (rising DXY) tightens global liquidity, creating significant headwinds for Bitcoin.

US 10Y Yield: The opportunity cost of capital. Rising yields make risk-free assets more attractive, pulling capital away from non-yielding assets like crypto.

What makes TFPS truly unique?

Dynamic Weighting (its secret weapon): Which factor matters most today? The DXY or the VIX? TFPS continuously analyzes the correlation of all four factors to your chosen asset (e.g., Bitcoin) and automatically adjusts their weight in real-time. This ensures you're always focused on what's currently driving the market.

Adaptive Engine : What drives a 15-minute chart is different from a daily chart. The TFPS engine automatically adapts its lookback periods and calculations to your chosen timeframe for optimal relevance.

Clear, Actionable Signals Designed for Traders:

Pressure Line (>0 or <0): Instantly see if the world's largest financial forces are providing a tailwind or a headwind for your trade.

Z-Score (Extreme Readings) : Get early warnings of extreme macro "Greed" or "Fear". Readings above +2 or below -2 have historically pinpointed moments of market exhaustion that often precede major trend reversals.

Regime Change : A fundamental shift in the nature of TradFi pressure is visualized with a clear signal, providing unambiguous macro insights.

Lead/Lag Status : Gain a critical edge by knowing who's in the driver's seat. The dashboard tells you if TradFi is LEADING the price action or if crypto is moving independently, allowing you to focus on the right information source.

This is a private beta. I am granting exclusive access to a limited number of traders who understand this new market reality. In exchange for your valuable feedback, you will be among the first to leverage what I believe is the new standard for macro analysis in crypto trading.

Request access to trade with the full context.

Assets Correlation AnalyzerAssets Correlation Analyzer

---------------------------------------------

What is it?

The Assets Correlation Analyzer is a technical indicator that measures and visualizes the statistical relationship between any two financial assets (a 'Base Asset' vs. a 'Comparison Asset', example Gold vs. SPY or Nasdaq vs. Bitcoin). The indicator calculates dynamic correlation tracking using statistical methods, confidence intervals, and category-wide analysis capabilities.

---------------------------------------------

Why was it built? / Potential Benefits

This indicator was developed to help analyze inter-asset relationships in portfolio management and trading strategies. The indicator can be used for:

Risk Assessment: Identify when assets begin moving together

Diversification Analysis: Monitor portfolio component relationships

Pairs Trading: Identify when correlated assets diverge

Market Analysis: Recognize shifts in market conditions through correlation patterns

Asset Analysis: Support decision-making based on correlation dynamics

Hedging Analysis: Identify relationships between different instruments

---------------------------------------------

How it Works

The indicator employs established statistical methods to calculate rolling correlations between two selected assets:

Data Collection: Retrieves price data for both selected assets using TradingView's security function

Returns Calculation: Computes logarithmic or simple returns based on user preference

Outlier Filtering: Optionally removes extreme price movements (beyond 2.5 standard deviations) to improve accuracy

Correlation Computation: Calculates either Pearson or Spearman rank correlation over the specified period

Signal Generation: Applies smoothing and generates a signal line (EMA) for momentum detection

Confidence Assessment: Evaluates data quality and provides confidence metrics

---------------------------------------------

How to Read the Oscillator

Main Correlation Line

Values Range: -1.0 to +1.0

+1.0: Perfect positive correlation (assets move identically)

+0.7 to +0.99: Strong positive correlation

+0.3 to +0.69: Moderate positive correlation

-0.3 to +0.29: Weak/No significant correlation

-0.69 to -0.31: Moderate negative correlation

-0.99 to -0.7: Strong negative correlation

-1.0: Perfect negative correlation (assets move oppositely)

Color Coding System

Green shades: Positive correlation levels, with brighter green indicating stronger positive correlation

Red shades: Negative correlation levels, with brighter red indicating stronger negative correlation

Gray: Insufficient data or transitional periods

The color intensity reflects both correlation strength and momentum relative to the signal line.

Signal Line (Gray)

The EMA-based signal line helps identify momentum changes:

Correlation above signal: Positive momentum in correlation

Correlation below signal: Negative momentum in correlation

Crossovers: Potential turning points in the relationship

Background Fills

Gradient fills provide a quick visual assessment of correlation strength, with intensity indicating the degree of correlation.

---------------------------------------------

Correlation Calculation Methods and Options

Calculation Methods

Spearman Rank Correlation (Default)

Uses ranked values rather than raw prices

Less sensitive to outliers and non-linear relationships

Suitable for volatile or non-normally distributed assets

Pearson Correlation (Traditional)

Standard linear correlation method

More sensitive to outliers

Suitable for assets with normal distribution patterns

---------------------------------------------

Customization Options

Correlation Period (7-500 bars): Determines the lookback window for calculation

Signal Line Period (1-200 bars): Controls the smoothing of the signal line

Outlier Removal: Automatically filters extreme price movements

Return Type: Choose between logarithmic (recommended) or simple returns

Smoothing Period: Reduces noise in correlation readings

---------------------------------------------

Asset Categories

The indicator includes 80+ pre-configured assets across multiple categories:

Metals: Gold, Silver, Copper, Platinum, Palladium, Nickel, Zinc, Aluminum

Energy: WTI/Brent Crude, Natural Gas, Uranium

Agriculture: Corn, Soybeans, Wheat, Coffee

ETFs: Major indices, sector, geographic, and specialty ETFs

Bonds: Government and corporate bond instruments

Financial: Currency pairs, treasury yields, volatility indices

Cryptocurrencies: Major digital assets and market cap indices

Real Estate: REITs and real estate focused instruments

---------------------------------------------

For Whom This Indicator Is Designed

Intended Users

Portfolio Managers: Asset allocation and risk assessment

Quantitative Traders: Correlation-based strategy development

Risk Analysts: Correlation monitoring and analysis

Institutional Investors: Diversification analysis

Active Traders: Pairs trading and arbitrage analysis

Skill Level

Intermediate to Advanced: Requires understanding of correlation concepts and statistical interpretation

Experience with Statistics: Users should be familiar with correlation analysis concepts

---------------------------------------------

Information Tables

Main Analysis Table

Displays current correlation value, data confidence percentage, and selected asset information.

Category Correlation Table

Shows correlation strength between the selected 'Base Asset' (in the chart, Gold) and all assets in the comparison asset's category.

---------------------------------------------

Alert Conditions

Four built-in alert types:

Strong Stable Positive Correlation: Triggers when correlation exceeds +0.8 with low volatility

Strong Stable Negative Correlation: Triggers when correlation falls below -0.8 with low volatility

Bullish Correlation Momentum: Signals when correlation crosses above the signal line

Bearish Correlation Momentum: Signals when correlation crosses below the signal line

---------------------------------------------

Usage Notes

Longer periods (30-50 bars) provide more stable analysis

Shorter periods (10-20 bars) provide more responsive signals

Monitor confidence levels - correlations with <75% confidence should be interpreted cautiously

Correlations tend to increase during market stress periods

Should be used in conjunction with other analysis tools

---------------------------------------------

Important Disclaimer

This indicator is for educational and informational purposes only. It should not be considered as financial advice or a recommendation to buy, sell, or hold any financial instrument. Past correlation patterns do not guarantee future relationships between assets. Users should conduct their own research and consider consulting with a qualified financial advisor before making investment decisions. Trading and investing involve substantial risk of loss, and correlation analysis cannot eliminate these risks. The accuracy of correlation calculations depends on data quality and market conditions, which can change rapidly.

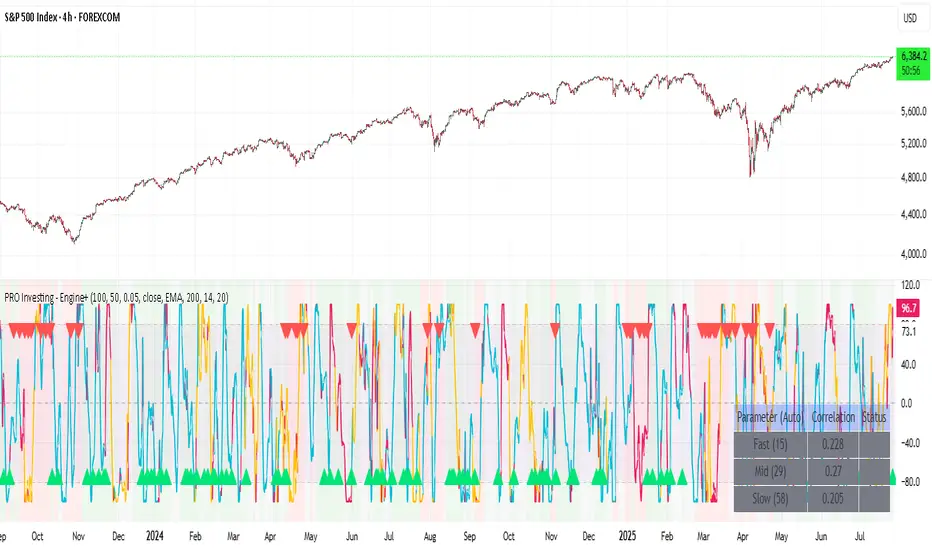

PRO Investing - Apex EnginePRO Investing - Apex Engine

1. Core Concept: Why Does This Indicator Exist?

Traditional momentum oscillators like RSI or Stochastic use a fixed "lookback period" (e.g., 14). This creates a fundamental problem: a 14-period setting that works well in a fast, trending market will generate constant false signals in a slow, choppy market, and vice-versa. The market's character is dynamic, but most tools are static.

The Apex Engine was built to solve this problem. Its primary innovation is a self-optimizing core that continuously adapts to changing market conditions. Instead of relying on one fixed setting, it actively tests three different momentum profiles (Fast, Mid, and Slow) in real-time and selects the one that is most synchronized with the current price action.

This is not just a random combination of indicators; it's a deliberate synthesis designed to create a more robust momentum tool. It combines:

Volatility analysis (ATR) to generate adaptive lookback periods.

Momentum measurement (ROC) to gauge the speed of price changes.

Statistical analysis (Correlation) to validate which momentum measurement is most effective right now.

Classic trend filters (Moving Average, ADX) to ensure signals are only taken in favorable market conditions.

The result is an oscillator that aims to be more responsive in volatile trends and more stable in quiet periods, providing a more intelligent and adaptive signal.

2. How It Works: The Engine's Three-Stage Process

To be transparent, it's important to understand the step-by-step logic the indicator follows on every bar. It's a process of Adapt -> Validate -> Signal.

Stage 1: Adapt (Dynamic Length Calculation)

The engine first measures market volatility using the Average True Range (ATR) relative to its own long-term average. This creates a volatility_factor. In high-volatility environments, this factor causes the base calculation lengths to shorten. In low-volatility, they lengthen. This produces three potential Rate of Change (ROC) lengths: dynamic_fast_len, dynamic_mid_len, and dynamic_slow_len.

Stage 2: Validate (Self-Optimizing Mode Selection)

This is the core of the engine. It calculates the ROC for all three dynamic lengths. To determine which is best, it uses the ta.correlation() function to measure how well each ROC's movement has correlated with the actual bar-to-bar price changes over the "Optimization Lookback" period. The ROC length with the highest correlation score is chosen as the most effective profile for the current moment. This "active" mode is reflected in the oscillator's color and the dashboard.

Stage 3: Signal (Normalized Velocity Oscillator)

The winning ROC series is then normalized into a consistent oscillator (the Velocity line) that ranges from -100 (extreme oversold) to +100 (extreme overbought). This ensures signals are comparable across any asset or timeframe. Signals are only generated when this Velocity line crosses its signal line and the trend filters (explained below) give a green light.

3. How to Use the Indicator: A Practical Guide

Reading the Visuals:

Velocity Line (Blue/Yellow/Pink): The main oscillator line. Its color indicates which mode is active (Fast, Mid, or Slow).

Signal Line (White): A moving average of the Velocity line. Crossovers generate potential signals.

Buy/Sell Triangles (▲ / ▼): These are your primary entry signals. They are intentionally strict and only appear when momentum, trend, and price action align.

Background Color (Green/Red/Gray): This is your trend context.

Green: Bullish trend confirmed (e.g., price above a rising 200 EMA and ADX > 20). Only Buy signals (▲) can appear.

Red: Bearish trend confirmed. Only Sell signals (▼) can appear.

Gray: No clear trend. The market is likely choppy or consolidating. No signals will appear; it is best to stay out.

Trading Strategy Example:

Wait for a colored background. A green or red background indicates the market is in a tradable trend.

Look for a signal. For a green background, wait for a lime Buy triangle (▲) to appear.

Confirm the trade. Before entering, confirm the signal aligns with your own analysis (e.g., support/resistance levels, chart patterns).

Manage the trade. Set a stop-loss according to your risk management rules. An exit can be considered on a fixed target, a trailing stop, or when an opposing signal appears.

4. Settings and Customization

This script is open-source, and its settings are transparent. You are encouraged to understand them.

Synaptic Engine Group:

Volatility Period: The master control for the adaptive engine. Higher values are slower and more stable.

Optimization Lookback: How many bars to use for the correlation check.

Switch Sensitivity: A buffer to prevent frantic switching between modes.

Advanced Configuration & Filters Group:

Price Source: The data source for momentum calculation (default close).

Trend Filter MA Type & Length: Define your long-term trend.

Filter by MA Slope: A key feature. If ON, allows for "buy the dip" entries below a rising MA. If OFF, it's stricter, requiring price to be above the MA.

ADX Length & Threshold: Filters out non-trending, choppy markets. Signals will not fire if the ADX is below this threshold.

5. Important Disclaimer

This indicator is a decision-support tool for discretionary traders, not an automated trading system or financial advice. Past performance is not indicative of future results. All trading involves substantial risk. You should always use proper risk management, including setting stop-losses, and never risk more than you are prepared to lose. The signals generated by this script should be used as one component of a broader trading plan.

Durdens Global M2 Liquidity Tracker🧠 Durdens Global M2 Liquidity Tracker | Bitcoin vs Liquidity, Visualized

If you’re not watching global liquidity, you’re not really trading macro.

This indicator tracks FX-adjusted M2 money supply across 20+ countries, aggregated into a single global liquidity signal. It can then be used to overlay against Bitcoin for timing macro shifts with precision.

🔍 Core Features:

🌐 USD-adjusted M2 from the US, China, Eurozone, UK, Japan, and more

📊 Normalization modes: None (raw), Index (Based to 100), Z-Score

⏳ Offset input to shift liquidity data forward — aligns with Bitcoin's delayed reaction (84–107 days common)

🧠 BTC correlation matrix: 30D, 90D, 365D correlation values

🧪 Top 3 M2 delta signals: Tracks 90-day % change for US, China, EU

🧮 Fibonacci SMAs: 13 / 34 / 89 for structural macro context

🟢🔴 Liquidity regime engine: EMA 89 defines "Risk-On" vs "Risk-Off" states

🧩 How It Works:

Each country’s M2 is multiplied by its FX rate (to USD) and summed into a single global M2 line. This ensures comparability across nations. The user can choose to:

Normalize the output (raw, indexed, or z-scored)

Shift the global M2 forward in time (offset), simulating the lag effect liquidity has on Bitcoin

Visualize macro risk conditions using EMA 89 as a liquidity regime filter

Analyze BTC correlation across 3 windows and track key regions’ M2 delta

❓ FAQ:

Why does this matter?

M2 is the monetary fuel behind asset bubbles. When liquidity rises, Bitcoin follows; with a delay. This tracker helps you front-run macro flows before they hit the chart.

Why use Index or Z-Score modes?

Raw values skew long-term visual analysis. Index mode rebases data for comparative trend tracking. Z-Score shows when liquidity is overheated or suppressed (mean reversion).

What does the offset input do?

Liquidity doesn’t hit Bitcoin instantly. Many traders use an 84–107 day forward shift to align M2 changes with BTC price action. The offset helps you visualize this.

Why track top 3 M2 regions?

US, China, and Eurozone are the heavyweights in global liquidity. Tracking their offset-day % change gives immediate insight into capital expansion or contraction.

Can I use this to trade?

Absolutely; but it’s best used as a macro filter. Combine with price structure, funding, or on-chain data to optimize timing and conviction.

⚡ Use Cases:

Spot early pivots in liquidity regimes (Risk-Off to Risk-On)

Quantify macro backdrop for Bitcoin or altcoin cycles

Understand when the Fed or PBOC are tightening or easing

Ditch the hopium. Trade with context.

—

Built by: @DurdensBitcoinLedger

Follow for updates — future upgrades include:

• Regional toggles

• Custom M2 baskets

• Alert conditions

• Continued revisions & updates

Stay liquid, not wrecked.

Asset Premium/Discount Monitor📊 Overview

The Asset Premium/Discount Monitor is a tool for analyzing the relative value between two correlated assets. It measures when one asset is trading at a premium or discount compared to its historical relationship with another asset, helping traders identify potential mean reversion opportunities, or pairs trading opportunities.

🎯 Use Cases

Perfect for analyzing:

NASDAQ:MSTR vs CRYPTO:BTCUSD - MicroStrategy's premium/discount to Bitcoin

NASDAQ:COIN vs BITSTAMP:BTCUSD - Coinbase's relative value to Bitcoin

NASDAQ:TSLA vs NASDAQ:QQQ - Tesla's premium to tech sector

Regional banks AMEX:KRE vs AMEX:XLF - Individual bank stocks vs financial sector

Any two correlated assets where relative value matters

Example of a trade: MSTR vs BTC - When indicator shows MSTR at 95% percentile (extreme premium): Short MSTR, Buy BTC. Then exit when the spread reverts to the mean, say 40-60% percentile.

🔧 How It Works

Core Calculation

Ratio Analysis: Calculates the price ratio between your asset and the correlated asset

Historical Baseline: Establishes the "normal" relationship using a 252-day moving average. You can change this.

Premium Measurement: Measures current deviation from historical average as a percentage

Statistical Context: Provides percentile rankings and standard deviation bands

The Math

Premium % = (Current Ratio / Historical Average Ratio - 1) × 100

🎨 Customization Options

Correlated Asset: Choose any symbol for comparison

Lookback Period: Adjust historical baseline (50-1000 days)

Smoothing: Reduce noise with moving average (1-50 days)

Visual Toggles: Show/hide bands and percentile lines

Color Themes: Customize premium/discount colors

📊 Interpretation Guide

Premium/Discount Reading

Positive %: Asset trading above historical relationship (premium)

Negative %: Asset trading below historical relationship (discount)

Near 0%: Asset at fair value relative to correlation

Percentile Ranking

90%+: Near recent highs - potential selling opportunity

10% and below: Near recent lows - potential buying opportunity

25-75%: Normal trading range

Signal Classifications

🔴 SELL PREMIUM: Asset expensive relative to recent range

🟡 Premium Rich: Moderately expensive, monitor for reversal

⚪ NEUTRAL: Fair value territory

🟡 Discount Opportunity: Moderately cheap, potential accumulation zone

🟢 BUY DISCOUNT: Asset cheap relative to recent range

🚨 Built-in Alerts

Extreme Premium Alert: Triggers when percentile > 95%

Extreme Discount Alert: Triggers when percentile < 5%

⚠️ Important Notes

Works best with highly correlated assets

Historical relationships can change - monitor correlation strength

Not investment advice - use as one factor in your analysis

Backtest thoroughly before implementing any strategy

🔄 Updates & Future Features

This indicator will be continuously improved based on user feedback. So... please give me your feedback!

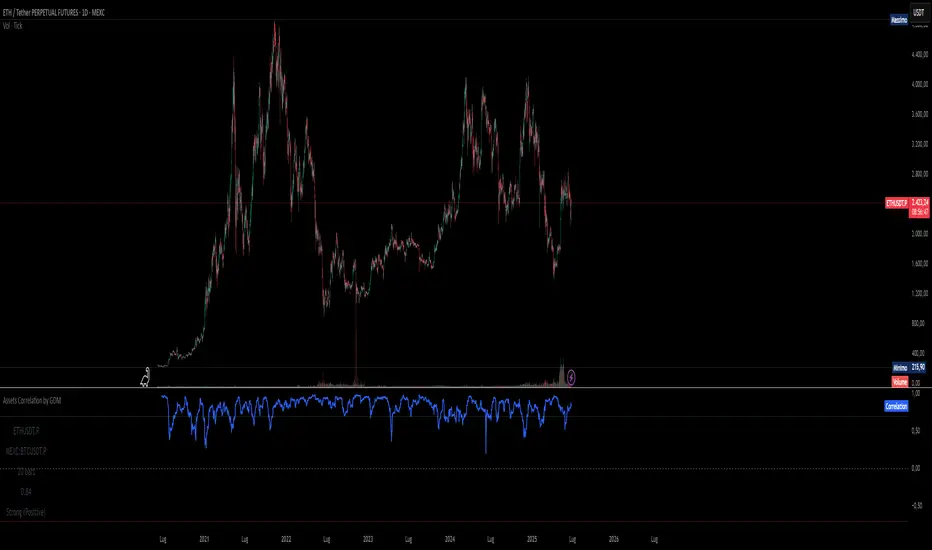

Assets Correlation by GDM📊 Correlation Matrix Table between Two Assets

This indicator calculates and displays the rolling correlation between the asset on your chart and a second asset of your choice. The correlation is computed based on log returns over a user-defined lookback period. A live summary table appears in the bottom left corner, providing a real-time snapshot of the current correlation and its context.

How it works:

Comparison Asset:

Select any symbol to compare with the chart asset (e.g., compare BTCUSD to ETHUSD).

Lookback Period:

Choose the rolling window (in bars) used to calculate the Pearson correlation coefficient.

Dynamic Table:

A table in the lower left corner summarizes:

Main asset symbol

Comparison symbol

Analysis period (bars)

Current correlation value (rounded to 2 decimals)

Correlation strength & direction (Strong, Moderate, Weak | Positive/Negative)

Visual Plot:

The indicator plots the correlation value over time so you can observe changes and trends.

Table Positioning:

Table location can be adjusted from settings (bottom left/right, top left/right).

How to use:

Risk Management & Diversification:

Quickly assess if two assets move together (positive correlation), in opposite directions (negative correlation), or independently.

Pairs Trading:

Identify opportunities when correlation diverges from historical norms.

Portfolio Construction:

Avoid overexposure to highly correlated assets, or use negative correlation for hedging.

Limitations & Tips:

Correlation values are based on historical returns and may change during periods of market stress or volatility.

Use multiple lookback periods (short, medium, long) for a more robust view.

Correlation does not imply causation—always complement with additional analysis.

Script Features:

User-selectable comparison asset and lookback window.

Real-time correlation calculation.

Clean summary table with correlation stats.

Optional alert logic and correlation plot for more advanced usage.

If you find this indicator useful, please leave a like and let me know your suggestions for improvements!

Intermarket Correlation Oscillator (ICO)The Intermarket Correlation Oscillator (ICO) is a TradingView indicator that helps traders analyze the relationship between two assets, such as stocks, indices, or cryptocurrencies, by measuring their price correlation. It displays this correlation as an oscillator ranging from -1 to +1, making it easy to spot whether the assets move together, oppositely, or independently. A value near +1 indicates strong positive correlation (assets move in the same direction), near -1 shows strong negative correlation (opposite movements), and near 0 suggests no correlation. This tool is ideal for confirming trends, spotting divergences, or identifying hedging opportunities across markets.

How It Works?

The ICO calculates the Pearson correlation coefficient between the chart’s primary asset (e.g., Apple stock) and a secondary asset you choose (e.g., SPY for the S&P 500) over a specified number of bars (default: 20). The oscillator is plotted in a separate pane below the chart, with key levels at +0.8 (overbought, strong positive correlation) and -0.8 (oversold, strong negative correlation). A midline at 0 helps gauge neutral correlation. When the oscillator crosses these levels or the midline, labels ("OB" for overbought, "OS" for oversold) and alerts notify you of significant shifts. Shaded zones highlight extreme correlations (red for overbought, green for oversold) if enabled.

Why Use the ICO?

Trend Confirmation: High positive correlation (e.g., SPY and QQQ both rising) confirms market trends.

Divergence Detection: Negative correlation (e.g., DXY rising while stocks fall) signals potential reversals.

Hedging: Identify negatively correlated assets to balance your portfolio.

Market Insights: Understand how assets like stocks, bonds, or crypto interact.

Easy Steps to Use the ICO in TradingView

Add the Indicator:

Open TradingView and load your chart (e.g., AAPL on a daily timeframe).

Go to the Pine Editor at the bottom of the TradingView window.

Copy and paste the ICO script provided earlier.

Click "Add to Chart" to display the oscillator below your price chart.

Configure Settings:

Click the gear icon next to the indicator’s name in the chart pane to open settings.

Secondary Symbol: Choose an asset to compare with your chart’s symbol (e.g., "SPY" for S&P 500, "DXY" for USD Index, or "BTCUSD" for Bitcoin). Default is SPY.