Institutional Zones: Opening & Closing Trend HighlightsDescription / Content:

Track key institutional trading periods on Nifty/Bank Nifty charts with dynamic session zones:

Opening Volatility Zone: 9:15 AM – 9:45 AM IST (Green)

Closing Institutional Zone: 1:30 PM – 3:30 PM IST (Orange)

Both zones are bounded by the day’s high and low to help visualize institutional activity and price behavior.

Key Observations:

Breakout in both closing trend and opening trends often occurs on uptrending days.

Breakdown in both closing range and opening range usually happens on downside trending days.

Price opening above the previous closing trend is often a sign of a strong opening.

This script helps traders identify trend strength, breakout/breakdown zones, and institutional participation during critical market hours.

Disclaimer:

This indicator is for educational and informational purposes only. It is not a financial advice or recommendation to buy or sell any instrument. Always confirm with your own analysis before taking any trade.

Pine Script Features:

Dynamic boxes for opening and closing sessions

Boxes adjust to the day’s high and low

Optional labels at session start

Works on intraday charts (1m, 5m, 15m, etc.)

Usage Tip:

Use this indicator in combination with trend analysis and volume data to spot strong breakout/breakdown opportunities in Nifty and Bank Nifty.

Cicli

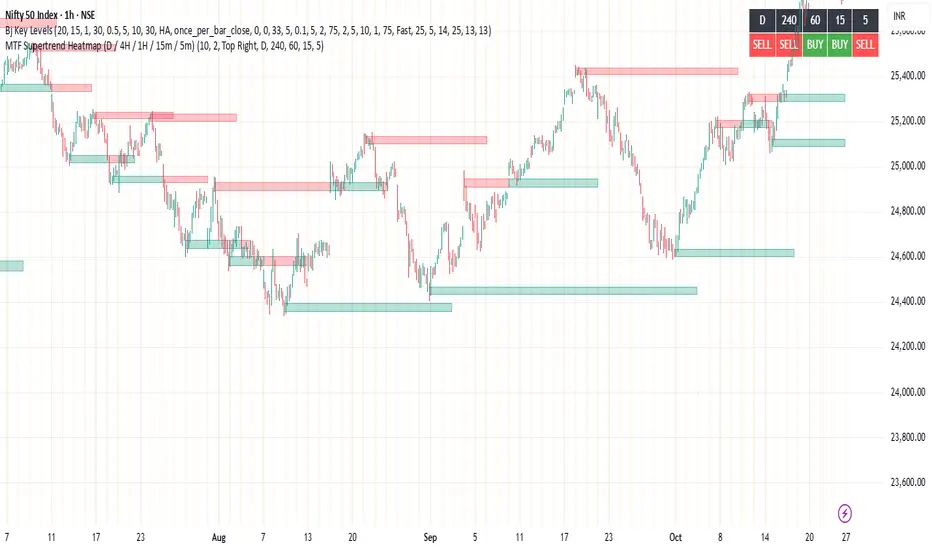

MTF Supertrend Heatmap (D / 4H / 1H / 15m / 5m)MTF Supertrend Heatmap (D / 4H / 1H / 15m / 5m)

A clean dashboard that tells you whether the same Supertrend (ATR Length, Multiplier) is BUY or SELL across five timeframes—all on one chart. Higher-TF values are fetched with request.security() and, when Confirm HTF bar close is ON, they do not repaint after that bar closes.

Optional toggles let you plot the current-TF Supertrend line and show bar-anchored flip markers (BUY/SELL) for each timeframe. Includes alerts for ALL-TF alignment and MAJORITY (≥3/5) agreement. Timeframes and Supertrend parameters are fully configurable. Use the heatmap for quick confirmation, reduce noise by keeping markers off unless needed.

Sonic R+EMA PYTAGOYou must determine the supply and demand zone as ema34, ema89, ema200, ema610. Then open the long position or the short position with SL and TP.

VWAP Balance HeatmapVWAP Balance Heatmap visually highlights where price stands relative to the dynamic equilibrium of bullish and bearish VWAP averages. The indicator builds two running VWAP arrays — one for bullish candles, one for bearish — then plots their averages and the midpoint between them. It fills the space between price and this midpoint, coloring it green when price is above balance and red when below. The result is a smooth heatmap that reveals whether the market is trading in premium or discount zones, helping you see shifts in momentum and balance without clutter or lag.

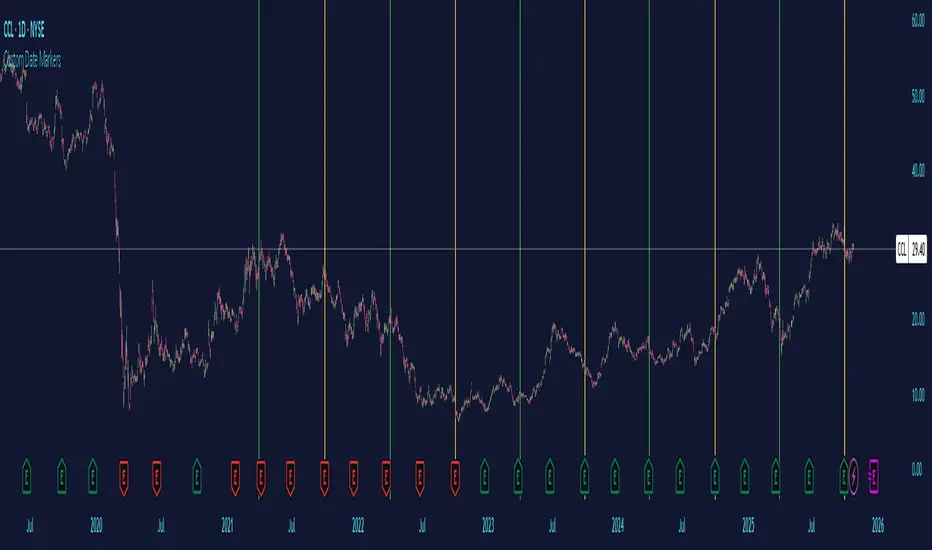

Custom Date MarkersCustom Date Markers - Pine Script Indicator

This indicator provides a powerful visual tool for technical and pattern analysis by allowing traders to mark up to 10 specific historical dates with customizable vertical lines on any chart. Each date can be assigned its own unique color, making it easy to categorize and distinguish between different types of events or market catalysts.

Primary Use Cases:

The indicator excels at identifying cyclical patterns and recurring market behavior. By marking significant dates such as earnings announcements, Federal Reserve meetings, dividend ex-dates, or seasonal events, traders can quickly visualize whether stocks consistently react in similar ways around these recurring dates. This is particularly valuable for discovering hidden patterns that might not be obvious from price action alone.

Practical Applications:

Earnings Analysis: Mark historical earnings dates to see if a stock tends to rally or sell-off before/after announcements

Macro Events: Identify how assets respond to FOMC meetings, CPI releases, or other economic data

Seasonal Patterns: Track dates that show recurring volatility or directional moves (like tax deadline periods, end-of-quarter re balancing, etc.)

Event Studies: Analyze the impact of company-specific events like product launches, FDA approvals, or leadership changes

Advanced Insights:

What makes this tool particularly interesting is its ability to reveal non-obvious correlations. For example, you might discover that a retail stock consistently experiences volume spikes 2-3 weeks before Black Friday across multiple years, or that certain tech stocks show weakness during specific conference dates. The color-coding feature allows you to layer multiple event types simultaneously—perhaps using red for bearish catalysts and green for bullish ones—creating a visual heat map of historical market reactions.

The indicator's 6-month default spacing (covering 4.5 years) is strategically designed to capture multiple business cycles while maintaining clarity on the chart. This timeframe is long enough to identify genuine patterns rather than coincidences, yet focused enough to remain relevant to current market conditions.

Pro Tip: Combine this indicator with volume analysis or other technical indicators to validate whether the patterns you observe are accompanied by meaningful market participation or if they're statistical noise.

Midnight Lines for Tokyo, London, New Yorkممتاز 👌 إليك **تعريفًا محدثًا وكاملًا للمؤشر باللغتين العربية والإنجليزية**، مع إدراج توضيح دقيق لتعامل المؤشر مع **تغيّر التوقيت الصيفي والشتوي (DST)** في لندن ونيويورك:

---

## 🇬🇧 **English Description (with DST behavior)**

**Indicator name:** *Midnight Lines for Tokyo, London, and New York*

**Purpose:**

This indicator automatically draws **vertical lines** on the chart at **midnight (00:00)** for the three major global trading sessions:

* **Tokyo**

* **London**

* **New York**

### 🔹 How it works:

1. The script checks each candle’s time using the built-in TradingView time zone function:

* `"Asia/Tokyo"`

* `"Europe/London"`

* `"America/New_York"`

2. When it detects **00:00** in any of these zones, it draws:

* A **vertical dotted line** that extends from the top to the bottom of the chart.

* A **label** at the top with the session name (e.g., “Tokyo Midnight”).

3. Each session has its own color for clarity:

* **Blue** → Tokyo Midnight

* **Green** → London Midnight

* **Red** → New York Midnight

### 🕒 Automatic Daylight Saving Time (DST) Adjustment:

The indicator automatically adapts to **Daylight Saving Time changes** in both **London** and **New York**:

* When London switches between **GMT and GMT+1**, the midnight line shifts automatically to remain accurate.

* When New York switches between **EST and EDT**, the script also updates accordingly.

* Tokyo does **not** observe DST, so its timing stays constant year-round.

### 🎯 Purpose:

Helps traders visually track the start of each new trading day in the major sessions and analyze:

* Session overlaps (e.g., London–New York overlap)

* Session-based trading strategies

* Price movement behavior at each new day open

---

## 🇸🇦 **الوصف بالعربية (مع إدراج تغير التوقيت)**

**اسم المؤشر:** خطوط منتصف الليل لجلسات طوكيو، لندن، ونيويورك

**الهدف:**

يقوم هذا المؤشر تلقائيًا برسم **خطوط عمودية** على الرسم البياني عند **منتصف الليل (00:00)** لكل من الجلسات الثلاث الرئيسية:

* **جلسة طوكيو**

* **جلسة لندن**

* **جلسة نيويورك**

### 🔹 كيفية العمل:

1. يستخدم المؤشر دوال TradingView لحساب الوقت الفعلي لكل مدينة:

* `"Asia/Tokyo"` لطوكيو

* `"Europe/London"` للندن

* `"America/New_York"` لنيويورك

2. عند وصول الساعة إلى **00:00** بتوقيت أي مدينة، يرسم المؤشر:

* **خطًا عموديًا متقطعًا** يمتد من أعلى إلى أسفل الرسم البياني.

* **تسمية (Label)** أعلى الخط باسم الجلسة (مثل “Tokyo Midnight”).

3. كل جلسة لها لون مختلف:

* **أزرق** → منتصف طوكيو

* **أخضر** → منتصف لندن

* **أحمر** → منتصف نيويورك

### 🕒 التعامل مع تغيّر التوقيت الصيفي والشتوي (DST):

يتكيّف المؤشر تلقائيًا مع تغيّر التوقيت في لندن ونيويورك:

* عندما تنتقل لندن بين **التوقيت الشتوي (GMT)** و**التوقيت الصيفي (GMT+1)**، يتحرك الخط تلقائيًا ليبقى في الساعة 00:00 المحلية.

* وعندما تنتقل نيويورك بين **EST** و**EDT**، يتم تعديل الخط كذلك تلقائيًا.

* أما طوكيو فلا تعتمد التوقيت الصيفي، لذا يبقى وقتها ثابتًا دائمًا على الساعة **00:00 JST**.

### 🎯 الفائدة:

يساعد المتداولين على تحديد **بداية كل جلسة تداول رئيسية**، ومراقبة:

* **تداخل الجلسات** مثل لندن ونيويورك

* **تحركات السعر عند بداية اليوم الجديد**

* **استراتيجيات التداول الزمنية حسب الجلسة**

---

BTC Confluence Score + Confirmed Signals (12m/1h)This script combines 7 different signals across multiple timeframes (12 min + 1 hour + BTC dominance), then only gives you a BUY or SELL when everything aligns.

It’s designed to filter out fake-outs and help you catch momentum reversals that stick.

WHAT IT’S DOING UNDER THE HOOD

Timeframes

12 min (fast) → short-term trigger (RSI, Stoch RSI, volatility)

1 hour (slow) → trend confirmation (EMA structure, RSI, MACD)

BTC Dominance (1 h) → strength/flow confirmation (is capital rotating into BTC or alts?)

This gives you a multi-timeframe confluence, which is what professional traders look for before entering a trade.

2. The 7 “Score” Ingredients

Each bar gets a “score” from –7 (super bearish) to +7 (super bullish) based on:

# Condition Bullish signal (+1) Bearish signal (–1)

1 RSI (12m) RSI > 50 RSI < 50

2 RSI (1h) RSI > 50 RSI < 50

3 MACD Histogram > 0 Histogram < 0

4 BTC Dominance level > 59.8 % < 59.8 %

5 BTC Dominance trend 3 EMA > 8 EMA 3 EMA < 8 EMA

6 1h EMAs trend 50 EMA > 200 EMA and price > 50 EMA 50 EMA < 200 EMA and price < 50 EMA

7 Volatility (ATR) Current ATR > average (momentum increasing) —

The Confluence Score bar at the bottom shows this numerically:

💚 +5 to +7 → Strong bullish conditions

❤️ –5 to –7 → Strong bearish conditions

🩶 Between –2 and +2 → Choppy / neutral

3️⃣ Confirmed Entry Logic (the clear triangles you see now)

You’ll now see only two real actionable markers:

✅ BUY (Green Triangle Up)

Triggered when:

Stoch RSI crosses upward on 12 min

RSI > 50 (momentum confirmation)

MACD histogram > 0 (trend shift)

Confluence score ≥ 4 (default threshold)

This means momentum + trend + structure + volume all agree on an upward move.

→ Ideal for going long or closing shorts.

🚨 SELL (Red Triangle Down)

Triggered when:

Stoch RSI crosses downward

RSI < 50

MACD histogram < 0

Confluence score ≥ 4 bearish

That’s your exit / short confirmation.

4️⃣ Color Bars (Score Strength)

At the bottom of the chart:

💚 Green Bars = full bullish confluence (+5 or more)

💛 Lime/Orange Bars = moderate bullish or early reversal

❤️ Red Bars = strong bearish confluence (–5 or less)

🩶 Gray Bars = chop/no edge

If you prefer visual simplicity, just use:

BUY = Green Triangle appears on green bars

SELL = Red Triangle appears on red bars

That’s your “double confirmation.”

🎯 HOW TO TRADE IT

⏱ Timeframes

Use 12 min for entries (fast scalps or 1–2 hr setups).

Confirm direction with the 1 hour timeframe — only trade in that direction.

💰 Entry Playbook

Signal What to Do

✅ Green Triangle appears Enter long or scale in. Set stop below recent swing low.

🚨 Red Triangle appears Exit long / enter short / scale out.

Bars gray or alternating Stay out — market is undecided.

🧮 Min Score Setting

Default = 4 (balanced).

Raise to 5 for cleaner, fewer signals.

Lower to 3 for more aggressive, frequent trades.

📲 Alerts

You can now create TradingView alerts using:

BUY Confirmed

SELL Confirmed

Set alert type:

“Once per bar close” — so you only get notified after confirmation, not mid-bar noise.

Y ou now have your own BTC AI Confluence System:

Filters all noise from RSI, MACD, EMAs, volatility, and BTC dominance

Waits for perfect alignment across multiple timeframes

Gives you one simple green (BUY) or red (SELL) signal

Lets you scalp 1–2 % moves safely or swing trade confirmations

Relative Valuation OscillatorRelative Valuation Oscillator (RVO) Description

The Valuation_OTC.pine script is a Relative Valuation Oscillator for TradingView that compares the current asset against a reference asset (like Bitcoin, S&P 500, or Gold) to determine if it's relatively overvalued or undervalued.

Key Features:

1. Multiple Calculation Methods:

Simple Ratio - Compares price ratio deviation from average

Percentage Difference - Direct percentage comparison between assets

Ratio Z-Score - Statistical measure (standard deviations from mean)

Rate of Change Comparison - Compares momentum/performance

Normalized Ratio - 0-100 scale centered at zero

2. Customizable Settings:

Reference asset selection (default: BTC/USDT)

Adjustable lookback period (10-500 bars)

Optional smoothing with configurable period

Overbought/oversold level thresholds (default: ±1.5)

3. Trading Signals:

Overvalued - Oscillator above overbought level (red zone)

Undervalued - Oscillator below oversold level (green zone)

Neutral - Between thresholds

Crossover alerts for key levels

Divergence detection (bullish/bearish)

4. Visual Components:

Color-coded oscillator line (green when positive, red when negative)

Optional signal line for additional smoothing

Background shading for valuation zones

Information table showing current metrics and status

Shape markers for crossovers and divergences

5. Alert Conditions:

Overvalued/undervalued alerts

Zero-line crossovers

Divergence signals

This indicator is useful for pairs trading, relative strength analysis, and identifying when an asset is trading at extremes relative to a benchmark asset.

BTC Confluence Alert 1 Overall Purpose

This script is a custom TradingView indicator that scans for confluence (agreement) between:

BTC’s short-term and medium-term momentum (12-minute and 1-hour RSIs),

The MACD histogram (trend direction and momentum strength),

Bitcoin dominance (money flowing back into BTC).

When all three are bullish, it flashes green and triggers a single alert.

Session Anchor Lines (Asia, London, NY)it draws a line at each session open ( in relative to the 4 HR candle )

SPX / Silver (XAGUSD) RatioThis script visualizes the S&P 500 Index to Silver ratio (SPX/Silver) — a powerful tool for monitoring the relative strength of equities vs. precious metals over time.

📊 Use Case:

Helps traders assess macro sentiment shifts between risk-on (equities) and risk-off (commodities).

A rising ratio indicates equity outperformance vs Silver, often in growth-driven bull markets.

A falling ratio suggests Silver is outperforming — potentially due to inflation, geopolitical risk, or weakening equities.

⚙️ Data & Calculation:

SPX: SP:SPX (S&P 500 Index)

Silver: TVC:SILVER

Formula:

SPX / Silver

(Both are spot/index prices, updated on daily timeframe)

📈 Interpretation:

📈 Ratio Rising → SPX outperforming Silver → Risk-on sentiment

📉 Ratio Falling → Silver outperforming SPX → Possible flight to safety or inflation hedge

🧠 Ideal For:

Macro trend analysis

Intermarket strategy development

Asset rotation decision-making

Spotting Silver bottoms during SPX/Silver peak zones

Bitcoin Cycles Halvins/Tops/Bottoms By CrBeThis Script shows you the actual Bitcoin tops and bottoms dates.

London Open High/Low 9:00-9:15indicator marks out high and low of the first 15 minutes of the London session.

golden smart entrySmart Money Concepts (SMC) is a trading methodology that focuses on understanding and following the behavior of institutional investors—often referred to as "smart money." The goal is to identify high-probability trade setups by analyzing how these large players move the market.