Moving Average Adaptive QThe Moving Average Adaptive Q (MAAQ) was authored by Perry Kaufman in the Stocks and Commodities Magazine 06/1995

This is similar to his Kaufman Adaptive Moving Average with a few changes. This is a pretty close moving average which I like quite a bit. Try it and let me know what you think.

Send me a message and let me know what other indicators you would like to see!

Media mobile adattiva di Kaufman (KAMA)

AMA_L/S_Sig- Fast EMA, Slow EMA Cross Strategy

- Use AMA for Slow

- Fast is expressed in some smoothing ways

- Hyper parameters not tuned

- For reference purposes

KAMA-ST BotExperimental supertrend model using KAMA (Kaufman Adaptive Moving Average) instead of RMA /SMA.

Good for scalping, NOT trend trading.

DO NOT USE THIS AS A STOPLOSS... you will get stopped!

Signals as what they are, no repaint, use other indicators as confirmation.

...have a play, good luck & stay safe!

MBY_Jet QunatHi, This is Yong From MBY_LAB

As I wish, I am happy to finally be able to publish this strategy.

This strategy is based on the previously published MBY_TMA RSI.

This strategy only works for 45-minute rods and is only applicable to Bitcoin / Bitfinex.

Thanks.

**Since this strategy is based on the starting price, there is no repainting and the backtest results are not false.**

Backtest info

10,000$

slippage 0.2%

trade fee 0.2%

Slow Heiken Ashi and Exponential Moving average Strategy 2.2Strategy using Slow Heiken Ashi by Glaz and Exponential moving averages. Looking for someone to help me turn the strategy into non-reoccuring alerts as I am having trouble doing so.

Uber Baseline [UTS]Fixed Trend Visualization

The trend is assumed UP while candle closes are above baseline. The baseline is then colored green.

The trend is assumed DOWN while candle closes are below baseline. The baseline is painted red in this case.

Uber Moving Averages [UTS]Uber Moving Averages are four highly customisable moving averages to complement your technical analysis.

The optional trend direction visualisation makes it a powerful tool for trend weighted analysis.

Moving Averages

16 different Moving Averages are at your disposal.

Trend Visualisation

If the predominant trend direction is DOWN the moving average is painted red. If the trend direction is UP the moving average is painted in green.

Kaufman Adaptive Moving Average Ribbon [ChuckBanger]Kaufman Adaptive Moving Average is one of the best moving averages in my opinion. So I made a ribbon script out of it. Good luck traders :)

Kaufman AMA Binary Wave [ChuckBanger]This is Kaufman AMA Binary Wave with buy and sell zones. It’s pretty simple: when the line is over zero = buy zone, below zero = sell, at zero = neutral. You can experiment with the filter and length settings to suit your environment.

Ifish KAMA Kaufman’s Adaptive Moving Average (KAMA) was developed by American quantitative financial theorist, Perry J. Kaufman, in 1998. The technique began in 1972 but Kaufman officially presented it to the public much later, through his book, “Trading Systems and Methods.” Unlike other moving averages, Kaufman’s Adaptive Moving Average accounts not only for price action but also for Market Volatility.

When market volatility is low, Kaufman’s Adaptive Moving Average remains near the current market price, but when volatility increases, it will lag behind. What the KAMA indicator aims to do is filter out “market noise” – insignificant, temporary surges in price action. One of the primary weaknesses of traditional moving averages is that when used for trading signals, they tend to generate many false signals. The KAMA indicator seeks to lessen this tendency – generate fewer false signals – by not responding to short-term, insignificant price movements.

Traders generally use the moving average indicator to identify market trend and reversals.

When calculating Kaufman’s Adaptive Moving Average, the following standard settings are used:

10 – Number of periods for the Efficiency Ratio

2 – Number of periods for the fastest exponential moving average

30 – Number of periods for the slowest exponential moving average

One of the uses of Kaufman’s Adaptive Moving Average is to identify the general trend of current market price action. Basically, when the KAMA indicator line is moving lower, it indicates the existence of a downtrend. On the other hand, when the KAMA line is moving higher, it shows an uptrend. As compared to the regular MA.

the KAMA indicator is less likely to generate false signals that may cause a trader to incur losses.

Kaufman’s Adaptive Moving Average can also be used to spot the beginning of new trends and pinpoint trend reversal points. One way to do this is by plotting two KAMA lines on a chart – one with a more short-term moving average and another with a longer-term moving average. When a faster KAMA line crosses above a slower KAMA line, this indicates a change from a downtrend to an uptrend. The trader can take a long position and close the trade when the faster MA line crosses back to beneath the slower MA line. Trading signals can also be derived by the movement of market price in relation to Kaufman’s Adaptive Moving Average. If price crosses from below to above the KAMA line, that is a bullish (buy) signal. Conversely, price falling from above the KAMA line to below it is a bearish (sell) signal.

Kama will color flip automatically when cross happens.

green = bullish flip

red = bearish flip

Ma line by its self just great to find s/r levels.

the periods that I like to use as input, I prefer fib sequence numbers

ea: 3,13, 21, 34 etc.

For more info or trading concept check my profile.

Kaufman Adaptive Least Squares Moving AverageIntroduction

It is possible to use a wide variety of filters for the estimation of a least squares moving average, one of the them being the Kaufman adaptive moving average (KAMA) which adapt to the market trend strength, by using KAMA in an lsma we therefore allow for an adaptive low lag filter which might provide a smarter way to remove noise while preserving reactivity.

The Indicator

The lsma aim to minimize the sum of the squared residuals, paired with KAMA we obtain a great adaptive solution for smoothing while conserving reactivity. Length control the period of the efficiency ratio used in KAMA, higher values of length allow for overall smoother results. The pre-filtering option allow for even smoother results by using KAMA as input instead of the raw price.

The proposed indicator without pre-filtering in green, a simple moving average in orange, and a lsma with all of them length = 200. The proposed filter allow for fast and precise crosses with the moving average while eliminating major whipsaws.

Same setup with the pre-filtering option, the result are overall smoother.

Conclusion

The provided code allow for the implementation of any filter instead of KAMA, try using your own filters. Thanks for reading :)

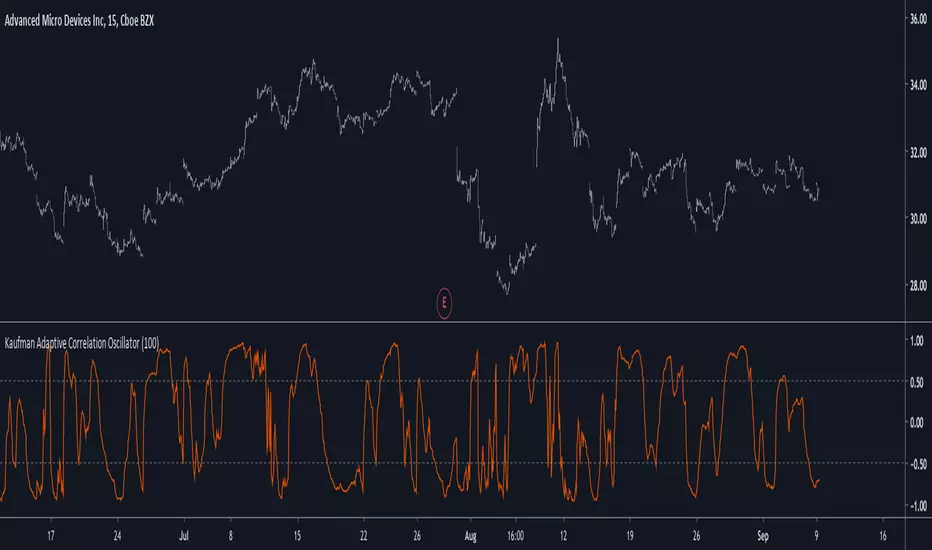

Kaufman Adaptive Correlation OscillatorIntroduction

The correlation oscillator is a technical indicator that measure the linear relationship between the market closing price and a simple increasing line, the indicator is in a (-1,1) range and rise when price is up-trending and fall when price is down-trending. Another characteristic of the indicator is its inherent smoothing which provide a noise free (to some extent) oscillator.

Such indicator use simple moving averages as well as estimates of the standard deviation for its calculation, but we can easily make it adaptive, this is why i propose this new technical indicator that create an adaptive correlation oscillator based on the Kaufman adaptive moving average.

The Indicator

The length parameter control the period window of the moving average, larger periods return smoother results while having a low kurtosis, which mean that values will remain around 1 or -1 a longer period of time. Pre-filtering apply a Kaufman adaptive moving average to the input, which allow for a smoother output.

No pre-filtering in orange, pre-filtering in yellow, period = 100 for both oscillators.

If you are not aware of the Kaufman adaptive moving average, such moving average return more reactive results when price is trending and smoother results when price is ranging, this also apply for the proposed indicator.

Conclusion

Classical correlation coefficients could use this approach, therefore the linear relationships between any variables could be measured. The fact that the indicator is adaptive add a certain potential, however such combination make the indicator have the drawback of kama + the correlation oscillator, which might appear at certain points.

Thanks for reading !

Adaptive ChannelThis indicator uses KAMA to adjust the length of a channel according to volatility.

A set up is generated when a candle closes below/above the mid point line; this is indicated via the background color.

Buy/sell on the break of the high/low of the signal candle.

Use the channel top/bottom as a stop (or a close above/below the mid pint line)

Powered Kaufman Adaptive Moving AverageIntroduction

The ability the Kaufman adaptive moving average (KAMA) has to be flat during ranging markets and close to the price during trending markets is what make this moving average one of the most useful in technical analysis. KAMA is calculated by using exponential averaging using the efficiency ratio (ER) as smoothing variable where 1 > ER > 0 . An increasing efficiency ratio indicate a trending market. Based on one of my latest indicator (see Kaufman Adaptive Bands) i propose this modified KAMA that allow to emphasis the abilities of KAMA by powering the efficiency ratio. I also added a new option that allow for even more adaptivity.

The Indicator

The indicator is a simple KAMA of period length that use a powered ER with exponent factor .

When factor = 1 the indicator is a simple KAMA, however when factor > 1 there can be more emphasis on the flattening effect of KAMA.

You can also restrain this effect by using 1 > factor > 0

Note that when the exponent is lower than 1 and greater than 0 you are basically applying a nth square root to the value, for example pow(2,0.5) = sqrt(2) because 1/0.5 = 2, in our case :

pow(ER,factor > 1) < ER and pow(ER,1 > factor > 0) > ER

Self Powered P-KAMA

When the self powered option is checked you are basically powering ER with the reciprocal of ER as exponent, however factor does no longer change anything. This can give interesting results since the exponent depend on the market trend strength.

In orange the self powered KAMA of period length = 50 and in blue a basic powered KAMA with a factor of 3 and a period of length = 50.

Conclusion

Applying basic math to indicators is always fun and easy to do, if you have adaptive moving averages using exponential averaging try powering your smoothing variable in order to see interesting results. I hope you like this indicator. Thanks for reading !

Options - Kaufman / LEAST SQUARES Moving AverageThis is a combo of multiple indicators :

1- three kama moving averages

2- one lsma moving average

3- a kama upper and lower band that you can set to use any of the three kama moving averages in the indicator as source

4- upper, lower and center bollinger bands price for last candle

The horizontal dot line is the bollinger and the horizontal arrowed lines are the bands for kama indicator.

The parameters are available for KAMA, LSMA and BB settings, the default settings are prefabricated for options trading.

Highly Optimized (Aroon, DMI, RWI)It is a highly optimized script for H4, D1. Backtests from (2016 - 2019, depending on the currency pair). Optimization still

going on.

Following alerts can be activated:

-

Buy-Signal (Baseline-Cross)!

Sell-Signal (Baseline-Cross)!

Buy Signal (Aroon)!

Sell Signal (Aroon)!

Buy Signal (DMI)!

Sell Signal (DMI)!

Buy Signal (RWI)!

Sell Signal (RWI)!

Can be used by the following pairs:

AUDCAD

AUDCHF

AUDJPY

AUDNZD

AUDSGD

AUDUSD

CADCHF

CADJPY

CHFJPY

CHFSGD

EURAUD

EURCAD

EURCHF

EURGBP

EURJPY

EURNZD

EURSGD

EURTRY

EURUSD

GBPAUD

GBPCAD

GBPCHF

GBPJPY

GBPNZD

GBPSGD

GBPUSD

NZDCAD

NZDCHF

NZDJPY

NZDUSD

SEKJPY

SGDJPY

USDCAD

USDCHF

USDCNH

USDJPY

USDSGD

USDTRY

XRPUSD

Price is 5€ per Month or 75€ lifetime. One week free for testing.

Kaufman Adaptive BandsIntroduction

Bands are quite efficient in technical analysis, they can provide support and resistance levels, provide breakouts points, trailing stop loss/take profits positions and can show the current market volatility to the user. Most of the time bands are made from a central tendency estimator like a moving average plus/minus a volatility indicator. Therefore bands can be made out of pretty much everything thus allowing for any kind of flavors.

So i propose a band indicator made from a Kaufman adaptive moving average using an estimate of the standard deviation.

Construction

The Kaufman moving average is an exponential averager using the efficiency ratio as smoothing variable, length control the period of kama and in order to provide more smoothness a power parameter has been introduced, higher values of power will return smoother results.

The volatility indicator is made from a biased estimation of the standard deviation by using the square root of the mean of the square minus the square of the mean method, except that we use kama instead of a mean.

The bands are made by adding/subtracting this volatility indicator with kama.

How To Use

The ability of the indicator to adapt to the current market state is what makes him a great tool for avoiding major exposition during ranging market, therefore the indicator will have a greater motion during trending market, or more simply the bands will move during trending markets while staying "flat" during ranging ones. Therefore the indicator might be more suited to breakouts, even if some cases will return what where turning points, this is particularly true during ranging markets.

Of course the efficiency ratio is not an "unbiased" trend metric indicator, it can consider high volatility markets as trending markets. Its one of his downsides.

High values of power will create smoother bands.

When using a low power parameter use an higher mult. In general using a low power value will make the bands move more freely as well as making them closer to each others.

Conclusion

At least the indicator is really nice to the eyes when using high power values, its ability to adapt to the market is a great addition to other more classical bands indicators, i also introduced a volatility estimator based on kama, some might have used the following estimation : kama(abs(price - kama)) which would have created a slower result. A trailing stop might be made from it if i see request about such addition.

If you are curious here are some more images of the indicator performing on different markets. Thanks for reading !

Double KAMA + VWMAThis study combines a fast and slow Kaufman Adaptive Moving Averages (KAMA) with a fast and slow Volume-Weighted Moving Average(VWMA).

The KAMA is definitely one of our favorite moving averages because it takes into account volatility and filters out false signals during periods of insignificant or horizontal price movement. This results in more patient, less impulsive trading. At its most basic, the KAMA's value remains relatively close in value to the price when volatility is low then lags slightly behind it during highly volatile movements and larger trends.

We've plotted two Kaufman's Adaptive Moving Averages:

-The first KAMA is the slow KAMA, which we use as a trend filter. It is shown on the graph as the thicker solid line that alternates between green and red. When the trend filter KAMA is bullish, the line turns green. It then turns red when bearish. Users can adjust the lengths of the fast and slow EMA for the KAMA's calculation in the input option menu, but it is important to remember that the number of periods should remain high in comparison to the fast KAMA as this allows it to track long-term price movements and trends.

-We then include a fast KAMA which has shorter EMA Lengths to focus in on movements within a smaller timeframe.

NOTE: The fast KAMA is only plotted when the trend filter KAMA is generating bullish signals. It is shown as the alternating pink and teal line above the main green line. When the fast KAMA is increasing, its line and the area between it and the slow KAMA are filled teal. When the fast KAMA is falling, its line and the area between the fast and slow KAMA lines are colored pink. This helps with timing exits.

Lastly, we've included a fast and slow VWMA to time long entries. These are only plotted when the Trend Filter KAMA is bearish. The fast VWMA is the teal solid line under the trend filter KAMA and the slow VWMA is the pink line. Optimal entries will occur when the fast VWMA crosses above the slow VWMA. When the slow VWMA is greater than the fast VWMA, the area between the two lines is filled red, while the same area is filled teal when the fast VWMA is greater than the slow.

I've included entry signals (shown on the screenshot as the lime green background highlights), but this is the basic version of the indicator. If you're interested in taking a look at the full version with alerts and entry + exit signals, feel free to send us a message!

Koby's 3 average MACD indicatorThis MACD is averaging 3 different MACD; KAMA MACD, ZLEMA MACD, and normal MACD.

Can find easier MACD's divergence and convergence than normal MACD.

And more smoothly drawing than ZLEMA MACD (KZ_MACD) which is I've made before.

Koby's ZLEMA MACD and KAMA signalUsing zero lag ema for MACD line, and using KAMA for MACD's signal line.

Test version.

This has MACD and signal cross alert, and 0 line alert.

Moving Average CrossoverIt was planned as an addition to Moving Average Smoothness Benchmark and Profitable Moving Average Crossover , but can be used standalone.

Supports 62 types of well-known moving averages and allows full-featured customization.

Supported types of averages and filters:

AEMA , Adaptive Exponential MA (by Vitali Apirine)

AHMA , Ahrens MA (by Richard D. Ahrens)

ALMA , Arnaud Legoux MA (by Arnaud Legoux and Dimitris Kouzis-Loukas)

ALF , Adaptive Laguerre Filter (by John F. Ehlers)

AMA , Adaptive MA (by Vitali Apirine)

ARSI , Adaptive RSI

BAMA , Bryant Adaptive MA (by Michael R. Bryant)

BF2 , Butterworth Filter with 2 poles

BF3 , Butterworth Filter with 3 poles

DEMA , Double Exponential MA (by Patrick G. Mulloy)

DWMA , Double Weighted (Linear) MA

EDCF , Ehlers Distance Coefficient Filter (by John F. Ehlers)

EDSMA , Ehlers Deviation-Scaled MA (by John F. Ehlers)

EHMA , Exponential Hull MA

EMA , Exponential MA

EVWMA , Elastic Volume Weighted MA (by Christian P. Fries)

FRAMA , Fractal Adaptive MA (by John F. Ehlers)

GF1 , Gaussian Filter with 1 pole

GF2 , Gaussian Filter with 2 poles

GF3 , Gaussian Filter with 3 poles

GF4 , Gaussian Filter with 4 poles

HFSMA , Hampel Filter on Simple Moving Average

HFEMA , Hampel Filter on Exponential Moving Average

HMA , Hull MA (by Alan Hull)

HWMA , Henderson Weighted MA (by Robert Henderson)

IDWMA , Inverse Distance Weighted MA

IIRF , Infinite Impulse Response Filter (by John F. Ehlers)

JAMA , Jurik Adaptive MA (by Mark Jurik)

JMA , Jurik MA (by Mark Jurik, )

KAMA , Kaufman Adaptive MA (by Perry J. Kaufman)

LF , Laguerre Filter (by John F. Ehlers)

LMA , Leo MA (by ProRealCode' user Leo)

LSMA , Least Squares MA (Moving Linear Regression)

MAMA (by John F. Ehlers)

FAMA , Following Adaptive MA (by John F. Ehlers)

MD , McGinley Dynamic (by John R. McGinley)

MHLMA , Middle-High-Low MA (by Vitali Apirine)

MNMA , McNicholl MA (by Dennis McNicholl)

NSMA , Moving Average 3.0 on SMA (by Manfred G. Dürschner)

NEMA , Moving Average 3.0 on EMA (by Manfred G. Dürschner)

NWMA , Moving Average 3.0 on WMA (by Manfred G. Dürschner)

NVWMA , Moving Average 3.0 on VWMA (by Manfred G. Dürschner)

PEMA , Pentuple Exponential MA (by Bruno Pio)

PWMA , Parabolic Weighted MA

QMA , Quick MA (by John McCormick)

QEMA , Quadruple Exponential MA (by Bruno Pio)

REMA , Regularized Exponential MA (by Chris Satchwell)

RMA , Running MA (by J. Welles Wilder)

RMF , Recursive Median Filter (by John F. Ehlers )

RMTA , Recursive Moving Trend Average (by Dennis Meyers)

SHMMA , Sharp Modified MA (by Joe Sharp)

SMA , Simple MA

SSF2 , Super Smoother Filter with 2 poles (by John F. Ehlers)

SSF3 , Super Smoother Filter with 3 poles (by John F. Ehlers)

SWMA , Sine Weighted MA

TEMA , Triple Exponential MA (by Patrick G. Mulloy)

TMA , Triangular MA (generalized by John F. Ehlers)

T3 , (by Tim Tillson)

VIDYA , Variable Index Dynamic Average (by Tushar S. Chande)

VWMA , Volume Weighted MA (by Buff P. Dormeier)

WMA , Weighted (Linear) MA

ZLEMA , Zero Lag Exponential MA (by John F. Ehlers and Ric Way)

Bryant Adaptive Moving Average@ChartArt got my attention to this idea.

This type of moving average was originally developed by Michael R. Bryant (Adaptrade Software newsletter, April 2014). Mr. Bryant suggested a new approach, so called Variable Efficiency Ratio (VER), to obtain adaptive behaviour for the moving average. This approach is based on Perry Kaufman' idea with Efficiency Ratio (ER) which was used by Mr. Kaufman to create KAMA.

As result Mr. Bryant got a moving average with adaptive lookback period. This moving average has 3 parameters:

Initial lookback

Trend Parameter

Maximum lookback

The 2nd parameter, Trend Parameter can take any positive or negative value and determines whether the lookback length will increase or decrease with increasing ER.

Changing Trend Parameter we can obtain KAMA' behaviour

To learn more see www.adaptrade.com