Order Flow Delta Trackerorderflow manager where you

Delta bars: Show net buying/selling per candle.

Cumulative Delta: Helps identify hidden buying/selling pressure.

If price rises but cumulative delta falls → possible hidden selling (divergence).

If price falls but cumulative delta rises → hidden buying.

M-oscillator

SynchroTrend Oscillator (STO) [PhenLabs]📊 SynchroTrend Oscillator

Version: PineScript™ v5

📌 Description

The SynchroTrend Oscillator (STO) is a multi-timeframe synchronization tool that combines trend information from three distinct timeframes into a single, easy-to-interpret oscillator ranging from -100 to +100.

This indicator solves the common problem of having to analyze multiple timeframe charts separately by consolidating trend direction and strength across different time horizons. The STO helps traders identify when markets are truly synchronized across timeframes, potentially indicating stronger trend conditions and higher probability trading opportunities.

Using either Moving Average crossovers or RSI analysis as the trend definition metric, the STO provides a comprehensive view of market structure that adapts to various trading strategies and market conditions.

🚀 Points of Innovation

Triple-timeframe synchronization in a single view eliminates chart switching

Dual trend detection methods (MA vs Price or RSI) for flexibility across different markets

Dynamic color intensity that automatically increases with signal strength

Scaled oscillator format (-100 to +100) for intuitive trend strength interpretation

Customizable signal thresholds to match your risk tolerance and trading style

Visual alerts when markets reach full synchronization states

🔧 Core Components

Trend Scoring System: Calculates a binary score (+1, -1, or 0) for each timeframe based on selected metrics, providing clear trend direction

Multi-Timeframe Synchronization: Combines and scales trend scores from all three timeframes into a single oscillator

Dynamic Visualization: Adjusts color transparency based on signal strength, creating an intuitive visual guide

Threshold System: Provides customizable levels for identifying potentially significant trading opportunities

🔥 Key Features

Triple Timeframe Analysis: Synchronizes three user-defined timeframes (default: 60min, 15min, 5min) into one view

Dual Trend Detection Methods: Choose between Moving Average vs Price or RSI-based trend determination

Adjustable Signal Smoothing: Apply EMA, SMA, or no smoothing to the oscillator output for your preferred signal responsiveness

Dynamic Color Intensity: Colors become more vibrant as signal strength increases, helping identify strongest setups

Customizable Thresholds: Set your own buy/sell threshold levels to match your trading strategy

Comprehensive Alerts: Six different alert conditions for crossing thresholds, zero line, and full synchronization states

🎨 Visualization

Oscillator Line: The main line showing the synchronized trend value from -100 to +100

Dynamic Fill: Area between oscillator and zero line changes transparency based on signal strength

Threshold Lines: Optional dotted lines indicating buy/sell thresholds for visual reference

Color Coding: Green for bullish synchronization, red for bearish synchronization

📖 Usage Guidelines

Timeframe Settings

Timeframe 1: Default: 60 (1 hour) - Primary higher timeframe for trend definition

Timeframe 2: Default: 15 (15 minutes) - Intermediate timeframe for trend definition

Timeframe 3: Default: 5 (5 minutes) - Lower timeframe for trend definition

Trend Calculation Settings

Trend Definition Metric: Default: “MA vs Price” - Method used to determine trend on each timeframe

MA Type: Default: EMA - Moving Average type when using MA vs Price method

MA Length: Default: 21 - Moving Average period when using MA vs Price method

RSI Length: Default: 14 - RSI period when using RSI method

RSI Source: Default: close - Price data source for RSI calculation

Oscillator Settings

Smoothing Type: Default: SMA - Applies smoothing to the final oscillator

Smoothing Length: Default: 5 - Period for the smoothing function

Visual & Threshold Settings

Up/Down Colors: Customize colors for bullish and bearish signals

Transparency Range: Control how transparency changes with signal strength

Line Width: Adjust oscillator line thickness

Buy/Sell Thresholds: Set levels for potential entry/exit signals

✅ Best Use Cases

Trend confirmation across multiple timeframes

Finding high-probability entry points when all timeframes align

Early detection of potential trend reversals

Filtering trade signals from other indicators

Market structure analysis

Identifying potential divergences between timeframes

⚠️ Limitations

Like all indicators, can produce false signals during choppy or ranging markets

Works best in trending market conditions

Should not be used in isolation for trading decisions

Past performance is not indicative of future results

May require different settings for different markets or instruments

💡 What Makes This Unique

Combines three timeframes in a single visualization without requiring multiple chart windows

Dynamic transparency feature that automatically emphasizes stronger signals

Flexible trend definition methods suitable for different market conditions

Visual system that makes multi-timeframe analysis intuitive and accessible

🔬 How It Works

1. Trend Evaluation:

For each timeframe, the indicator calculates a trend score (+1, -1, or 0) using either:

MA vs Price: Comparing close price to a moving average

RSI: Determining if RSI is above or below 50

2. Score Aggregation:

The three trend scores are combined and then scaled to a range of -100 to +100

A value of +100 indicates all timeframes show bullish conditions

A value of -100 indicates all timeframes show bearish conditions

Values in between indicate varying degrees of alignment

3. Signal Processing:

The raw oscillator value can be smoothed using EMA, SMA, or left unsmoothed

The final value determines line color, fill color, and transparency settings

Threshold levels are applied to identify potential trading opportunities

💡 Note:

The SynchroTrend Oscillator is most effective when used as part of a comprehensive trading strategy that includes proper risk management techniques. For best results, consider using the oscillator in conjunction with support/resistance levels, price action analysis, and other complementary indicators that align with your trading style.

Jinsu RSI 14### 🔍 **Jinsu RSI 14 – EMA 9 & WMA 45**

**Description:**

This custom indicator combines the classic RSI (Relative Strength Index) with two moving averages — EMA (Exponential Moving Average) and WMA (Weighted Moving Average) — applied directly to the RSI value to provide more nuanced momentum signals.

### 📊 **How It Works**

- **RSI 14** measures market momentum and identifies overbought (above 70) or oversold (below 30) conditions.

- **EMA 9 on RSI** responds quickly to short-term changes, signaling momentum shifts.

- **WMA 45 on RSI** captures long-term sentiment, while placing more emphasis on recent data.

### 🧠 **Signal Interpretation**

- **RSI crosses above EMA 9** → Possible bullish momentum shift.

- **RSI falls below EMA 9** → Possible bearish momentum shift.

- **EMA 9 crosses above WMA 45** → Strong bullish momentum.

- **EMA 9 falls below WMA 45** → Strong bearish momentum.

- **RSI is between EMA 9 & WMA 45** → Market may be consolidating or oscillating.

### 🎨 **Visual Enhancement**

- The neutral zone (RSI between 30–70) is lightly shaded purple to reduce visual noise.

- When **RSI > 70**, a green color appears and intensifies with higher RSI values, highlighting strong buying pressure.

- All values are displayed with two decimal precision for clarity.

This tool is ideal for trend-following traders and momentum-based strategies, helping you recognize early shifts in market sentiment with visual cues and cross confirmations.

Mongoose Capital: FlowWave + Conviction Strip🟩 Indicator Name

Mongoose Capital: FlowWave + Conviction Strip

📜 Short Description

Smoothed Money Flow Oscillator with conviction scoring columns to assess flow strength.

🧠 Description (Long Form)

The Mongoose Capital: FlowWave + Conviction Strip is a refined visualization of money flow dynamics designed to identify shifts in volume pressure and trend strength.

This dual-panel indicator includes:

• FlowWave Line — A smoothed momentum curve built from normalized money flow data, filtered through dual EMAs. Green (positive) and purple (negative) segments help traders quickly assess bias shifts.

• Conviction Score Columns — A histogram below the zero line shows strength of flow deltas (momentum of volume pressure). Green/red bars appear when strength exceeds a critical threshold, while gray bars indicate low conviction.

• Background Zone Coloring — Optional dark red/green gradient to enhance visibility of positive/negative phases.

✅ Designed for traders who value clarity and minimal noise

✅ Pairs well with macro trend filters or breakout strategies

✅ Built and published by Mongoose Capital

🔧 Default Settings

Money Flow Length: 14

Signal Cooldown: 5 bars

Source: HLC3

EMA Wave Filter: 3

Strength Threshold: 20

🧪 Suggested Use

Confirm entries/exits in trend continuation setups

Identify divergences between price and money flow

Filter low-conviction trades using the histogram's gray zone

Spot early accumulation or distribution through wave crossovers

📢 Author

Published by: TheRealMongoose

Powered by: Mongoose Capital

Feel free to tag us in your setups.

MTF Stoch RSI Confluence + Combined AlertMTF STOCH RSI CONFLUENCE INDICATOR 1m/5m/15m ( Scalping Indicator added on SRSI 1H)

IF all three Stoch are overbought(above 80) the indicator creates a red vertical line. If all Stoch are oversold(below 20) the indicator creates a green vertical line.

RULES!!!!

NEVER TRADE AGAINST THE TREND!!! This is super important!!!!

If 1H SRSI is above 80 with MTF overbouht and ZC is red (Downtrend) then we open a MR Short- (Prefered at PA Spikes) The same for opposites MR Longs.

If 1H SRSI is above 80 with the MTF oversold and ZC green then we can open a Long position. Prefered Momo Long. The same applies for opposite, hence momo short.

Exponential Regression Log ResidualThis custom indicator measures the logarithmic residual between the current price and an exponential regression line, offering insights into relative overbought and oversold conditions on a logarithmic scale. It can be especially useful when analyzing assets that move exponentially over time, such as growth stocks or cryptocurrencies.

EMA Oscillating Trend📈 EMA Oscillating Trend by AI-123

The EMA Oscillating Trend indicator is a dynamic trend visualizer that enhances traditional EMA behavior by offsetting the line based on trend direction, providing a more intuitive and visually distinct representation of market momentum.

🔍 Key Features:

🔵 Bullish Color Customization – Define your preferred color for bullish trends

🔴 Bearish Color Customization – Set a different tone for bearish phases

🪄 Adjustable Line Thickness – Tailor the EMA's appearance to your chart style

📐 Offset Multiplier Input – Automatically pushes the EMA above price in a downtrend and below price in an uptrend for enhanced clarity

⚙️ User-Friendly Inputs – No coding knowledge required; full customization in the settings panel

🧠 How It Works:

Calculates a primary EMA line (OV) and a sub-component to compare against (OV2)

Determines the trend based on whether OV is above or below OV2

Shifts the EMA line above price during bearish trends and below price during bullish trends

The offset is percentage-based and scales dynamically with the price for optimal readability

✅ Ideal For:

Trend-followers seeking visual clarity

Discretionary traders who want less clutter and more signal

Anyone who likes their EMAs with a little more flair and insight

🛠️ Author: @alphainvestor123

This tool was crafted with simplicity and clarity in mind. If you enjoy the indicator, consider dropping feedback or sharing your use case!

MG Universal model🚀 Summary🚀

The MG univerasal model is a composite of various items such as RSI, price Z-Score, Sharpe Ratio, Sortino Ratio, Omega Ratio, etc

Each component is normalized and then equally wheighted out to perform a global metric.

At the end, an Exponential Moving Average is added on the global metric.

You can easily find a description of each component on the internet, for the Crosby Ratio, it's a metric that comes from bitcoinmagazinepro.com.

✨ Key Features ✨

🗡 Smoothed Global Metric

Using a Moving average to smooth out the whole aggregated metric.

🗡 Bands Zone at extreme levels

Automatically displaying bands at top and bottom levels of the oscillator.

🗡 Normalizing components

Each component is normalized.

🗡 DataTable

Optional DataTable is available to check the score for each components and their related Z-Score.

📊 How I use it 📊

When catching up with 0 line (midline), crossing it :

if it goes above 0.2:

get out when it crosses 0.2 again

else:

get out when it crosses 0 again

That's the way I use it, may be there is a better way, FAFO :)

❓ Seeing a bug or an issue ❓

Feel free to DM me if you see a component that seems badly calculated.

I will be happy to fix it.

❗❗ Disclaimer ❗❗

This is a single indicator, even though it's aggregating many, do not use it as a standalone.

Past performance is not indicative of future results.

Always backtest, check, and align parameters before live trading.

Renko Compression Index (RCI)Renko Compression Index

The Renko Compression Index (RCI) is a unique market structure indicator designed to detect price compression zones on Renko-based charts. It measures the frequency of directional changes in Renko bricks over a specific period, identifying moments of trend indecision or consolidation that may precede major breakouts.

Oath KeeperOath Keeper - Advanced Money Flow & Market Dynamics Indicator

A sophisticated indicator that analyzes market dynamics through money flow patterns, volume analysis, and liquidation detection to identify high-probability trading opportunities.

Core Features:

• Smart Money Flow Analysis: Proprietary calculation of institutional money movement

• Volume-Enhanced Signals: Multi-timeframe volume confirmation

• Liquidation Detection: Identifies potential forced liquidation events

• Advanced Signal Classification: Regular, Super, and Fakeout signals

Signal Types:

1. Regular Signals (Green/Purple Circles)

• Volume-confirmed momentum shifts

• Money flow threshold breaches

• Institutional participation confirmation

2. Super Signals (Green/Purple Squares)

• Deep oversold/overbought reversals

• High-volume rejection patterns

• Liquidation event confirmation

3. Fakeout Signals (Red X)

• Rapid sentiment shifts

• Trap detection

• False breakout warnings

Visual Components:

• Dynamic Money Flow Line (White/Purple)

• Order Flow Clouds (Green/Red with high transparency)

• Reference Levels (20, 50, 80)

• Multi-type Signal Markers

• Color-coded momentum visualization

Interpretation Guide:

• Green Cloud: Bullish money flow dominance

• Red Cloud: Bearish money flow dominance

• Circle Markers: Standard reversals

• Square Markers: High-conviction moves

• X Markers: Potential trap zones

Best Practices:

• Most effective on 1H+ timeframes

• Use with major trading pairs

• Wait for candle close confirmation

• Combine with support/resistance levels

• Monitor volume confirmation

• Use multiple timeframe analysis

This indicator helps traders identify institutional money flow, potential liquidation events, and market reversals by analyzing volume patterns and money flow dynamics, providing multiple confirmation layers for trade decisions.

Note: Performance varies with market conditions and timeframes. Always employ proper risk management.

CVD (Cumulative Volume Delta)

Cumulative Volume Delta

Use a moving average with three different

I thought about determining the volatility and direction of the price of the stock price and finding a place to break through.

I made some Mistake coz I'm new corder

I'm reposting this simple script due to house rule violation. (Whatever can haha) 😁

I'm erasing all the comments in my native language that I had in my script... I thought it would make the User uncomfortable, so I locked the code, and I thought maybe that's the problem

Anyway, I'm sorry 😅

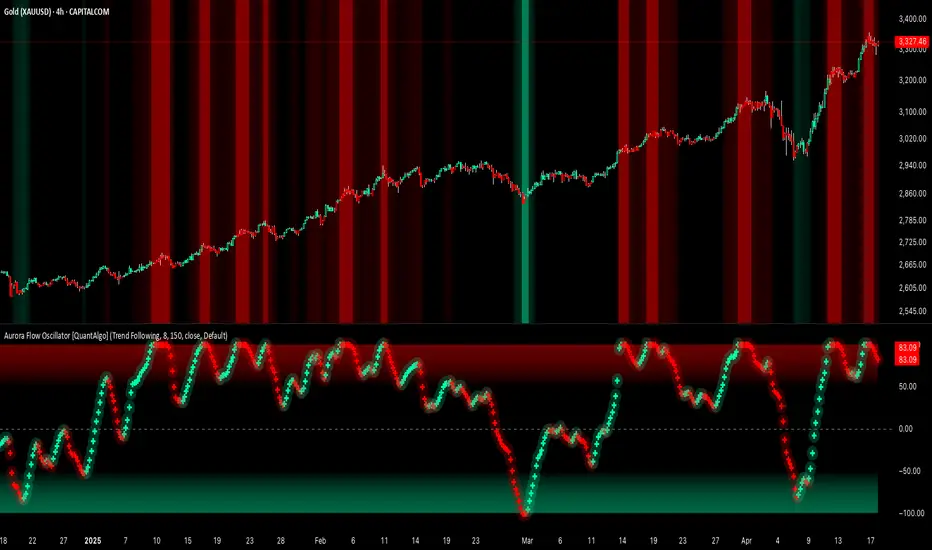

Aurora Flow Oscillator [QuantAlgo]The Aurora Flow Oscillator is an advanced momentum-based technical indicator designed to identify market direction, momentum shifts, and potential reversal zones using adaptive filtering techniques. It visualizes price momentum through a dynamic oscillator that quantifies trend strength and direction, helping traders and investors recognize momentum shifts and trading opportunities across various timeframes and asset class.

🟢 Technical Foundation

The Aurora Flow Oscillator employs a sophisticated mathematical approach with adaptive momentum filtering to analyze market conditions, including:

Price-Based Momentum Calculation: Calculates logarithmic price changes to measure the rate and magnitude of market movement

Adaptive Momentum Filtering: Applies an advanced filtering algorithm to smooth momentum calculations while preserving important signals

Acceleration Analysis: Incorporates momentum acceleration to identify shifts in market direction before they become obvious

Signal Normalization: Automatically scales the oscillator output to a range between -100 and 100 for consistent interpretation across different market conditions

The indicator processes price data through multiple filtering stages, applying mathematical principles including exponential smoothing with adaptive coefficients. This creates an oscillator that dynamically adjusts to market volatility while maintaining responsiveness to genuine trend changes.

🟢 Key Features & Signals

1. Momentum Flow and Extreme Zone Identification

The oscillator presents market momentum through an intuitive visual display that clearly indicates both direction and strength:

Above Zero: Indicates positive momentum and potential bullish conditions

Below Zero: Indicates negative momentum and potential bearish conditions

Slope Direction: The angle and direction of the oscillator provide immediate insight into momentum strength

Zero Line Crossings: Signal potential trend changes and new directional momentum

The indicator also identifies potential overbought and oversold market conditions through extreme zone markings:

Upper Zone (>50): Indicates strong bullish momentum that may be approaching exhaustion

Lower Zone (<-50): Indicates strong bearish momentum that may be approaching exhaustion

Extreme Boundaries (±95): Mark potentially unsustainable momentum levels where reversals become increasingly likely

These zones are displayed with gradient intensity that increases as the oscillator moves toward extremes, helping traders and investors:

→ Identify potential reversal zones

→ Determine appropriate entry and exit points

→ Gauge overall market sentiment strength

2. Customizable Trading Style Presets

The Aurora Flow Oscillator offers pre-configured settings for different trading approaches:

Default (80,150): Balanced configuration suitable for most trading and investing situations.

Scalping (5,80): Highly responsive settings for ultra-short-term trades. Generates frequent signals and catches quick price movements. Best for 1-15min charts when making many trades per day.

Day Trading (8,120): Optimized for intraday movements with faster response than default settings while maintaining reasonable signal quality. Ideal for 5-60min or 4h-12h timeframes.

Swing Trading (10,200): Designed for multi-day positions with stronger noise filtering. Focuses on capturing larger price swings while avoiding minor fluctuations. Works best on 1-4h and daily charts.

Position Trading (14,250): For longer-term position traders/investors seeking significant market trends. Reduces false signals by heavily filtering market noise. Ideal for daily or even weekly charts.

Trend Following (16,300): Maximum smoothing that prioritizes established directional movements over short-term fluctuations. Best used on daily and weekly charts, but can also be used for lower timeframe trading.

Countertrend (7,100): Tuned to detect potential reversals and exhaustion points in trends. More sensitive to momentum shifts than other presets. Effective on 15min-4h charts, as well as daily and weekly charts.

Each preset automatically adjusts internal parameters for optimal performance in the selected trading context, providing flexibility across different market approaches without requiring complex manual configuration.

🟢 Practical Usage Tips

1/ Trend Analysis and Interpretation

→ Direction Assessment: Evaluate the oscillator's position relative to zero to determine underlying momentum bias

→ Momentum Strength: Measure the oscillator's distance from zero within the -100 to +100 range to quantify momentum magnitude

→ Trend Consistency: Monitor the oscillator's path for sustained directional movement without frequent zero-line crossings

→ Reversal Detection: Watch for oscillator divergence from price and deceleration of movement when approaching extreme zones

2/ Signal Generation Strategies

Depending on your trading approach, multiple signal strategies can be employed:

Trend Following Signals:

Enter long positions when the oscillator crosses above zero

Enter short positions when the oscillator crosses below zero

Add to positions on pullbacks while maintaining the overall trend direction

Countertrend Signals:

Look for potential reversals when the oscillator reaches extreme zones (±95)

Enter contrary positions when momentum shows signs of exhaustion

Use oscillator divergence with price as additional confirmation

Momentum Shift Signals:

Enter positions when oscillator changes direction after establishing a trend

Exit positions when oscillator direction reverses against your position

Scale position size based on oscillator strength percentage

3/ Timeframe Optimization

The indicator can be effectively applied across different timeframes with these considerations:

Lower Timeframes (1-15min):

Use Scalping or Day Trading presets

Focus on quick momentum shifts and zero-line crossings

Be cautious of noise in extreme market conditions

Medium Timeframes (30min-4h):

Use Default or Swing Trading presets

Look for established trends and potential reversal zones

Combine with support/resistance analysis for entry/exit precision

Higher Timeframes (Daily+):

Use Position Trading or Trend Following presets

Focus on major trend identification and long-term positioning

Use extreme zones for position management rather than immediate reversals

🟢 Pro Tips

Price Momentum Period:

→ Lower values (5-7) increase sensitivity to minor price fluctuations but capture more market noise

→ Higher values (10-16) emphasize sustained momentum shifts at the cost of delayed response

→ Adjust based on your timeframe (lower for shorter timeframes, higher for longer timeframes)

Oscillator Filter Period:

→ Lower values (80-120) produce more frequent directional changes and earlier response to momentum shifts

→ Higher values (200-300) filter out shorter-term fluctuations to highlight dominant market cycles

→ Match to your typical holding period (shorter holding time = lower filter values)

Multi-Timeframe Analysis:

→ Compare oscillator readings across different timeframes for confluence

→ Look for alignment between higher and lower timeframe signals

→ Use higher timeframe for trend direction, lower for earlier entries

Volatility-Adaptive Trading:

→ Use oscillator strength to adjust position sizing (stronger = larger)

→ Consider reducing exposure when oscillator reaches extreme zones

→ Implement tighter stops during periods of oscillator acceleration

Combination Strategies:

→ Pair with volume indicators for confirmation of momentum shifts

→ Use with support/resistance levels for strategic entry and exit points

→ Combine with volatility indicators for comprehensive market context

Multi-Factor Reversal AnalyzerMulti-Factor Reversal Analyzer – Quantitative Reversal Signal System

OVERVIEW

Multi-Factor Reversal Analyzer is a comprehensive technical analysis toolkit designed to detect market tops and bottoms with high precision. It combines trend momentum analysis, price action behavior, wave oscillation structure, and volatility breakout potential into one unified indicator.

This indicator is not a random mix of tools — each module is carefully selected for a specific purpose. When combined, they form a multi-dimensional view of the market, merging trend analysis, momentum divergence, and volatility compression to produce high-confidence signals.

Why Combine These Modules?

Module Combination Ideas & How to Use Them

Factor A: Trend Detector + Gold Zone

Concept:

• The Trend Detector (light yellow histogram) evaluates market strength:

• Histogram trending downward or staying below 50 → bearish conditions;

• Trending upward or staying above 50 → bullish conditions.

• The Gold Zone identifies areas of volatility compression — typically a prelude to explosive market moves.

Practical Application:

• When the Gold Zone appears and the Trend Detector is bearish → likely downside move;

• When the Gold Zone appears and the Trend Detector is bullish → likely upside breakout.

• Note: The Gold Zone does not mean the bottom is in. It is not a buy signal on its own — always combine it with other modules for directional bias.

Factor B: PAI + Wave Trend

Concept:

• PAI (Price Action Index) is a custom oscillator that combines price momentum with volatility dispersion, displaying strength zones:

• Green area → bullish dominance;

• Red area → bearish pressure.

• Wave Trend offers smoothed crossover signals via the main and signal lines.

Practical Application:

• When PAI is in the green zone and Wave Trend makes a bullish crossover → potential reversal to the upside;

• When PAI is in the red zone and Wave Trend shows a bearish crossover → potential start of a downtrend.

Factor C: Trend Detector + PAI

Concept:

• Combines directional trend strength with price action strength to confirm setups via confluence.

Practical Application:

• Trend Detector histogram bottoms out + PAI enters the green zone → high chance of upward reversal;

• Histogram tops out + PAI in the red zone → increased likelihood of downside continuation.

Multi-Factor Confluence (Advanced Use)

• When Trend Detector, PAI, and Wave Trend all align in the same direction (bullish or bearish), the directional signal becomes significantly more reliable.

• This setup is especially useful for trend-following or swing trade entries.

KEY FEATURES

1. Multi-Layer Reversal Logic

• Combines trend scoring, oscillator divergence, and volatility squeezes for triangulated reversal detection.

• Helps traders distinguish between trend pullbacks and true reversals.

2. Advanced Divergence Detection

• Detects both regular and hidden divergences using pivot-based confirmation logic.

• Customizable lookback ranges and pivot sensitivity provide flexible tuning for different market styles.

3. Gold Zone Volatility Compression

• Highlights pre-breakout zones using custom oscillation models (RSI, harmonic, Karobein, etc.).

• Improves anticipation of breakout opportunities following low-volatility compressions.

4. Trend Direction Context

• PAI and Trend Score components provide top-down insight into prevailing bias.

• Built-in “Straddle Area” highlights consolidation zones; breakouts from this area often signal new trend phases.

5. Flexible Visualization

• Color-coded trend bars, reversal markers, normalized oscillator plots, and trend strength labels.

• Designed for both visual discretionary traders and data-driven system developers.

USAGE GUIDELINES

1. Applicable Markets

• Suitable for stocks, crypto, futures, and forex

• Supports reversal, mean-reversion, and breakout trading styles

2. Recommended Timeframes

• Short-term traders: 5m / 15m / 1H — use Wave Trend divergence + Gold Zone

• Swing traders: 4H / Daily — rely on Price Action Index and Trend Detector

• Macro trend context: use PAI HTF mode for higher timeframe overlays

3. Reversal Strategy Flow

• Watch for divergence (WT/PAI) + Gold Zone compression

• Confirm with Trend Score weakening or flipping

• Use Straddle Area breakout for final trigger

• Optional: enable bar coloring or labels for visual reinforcement

• The indicator performs optimally when used in conjunction with a harmonic pattern recognition tool

4. Additional Note on the Gold Zone

The “Gold Zone” does not directly indicate a market bottom. Since it is displayed at the bottom of the chart, it may be misunderstood as a bullish signal. In reality, the Gold Zone represents a compression of price momentum and volatility, suggesting that a significant directional move is about to occur. The direction of that move—upward or downward—should be determined by analyzing the histogram:

• If histogram momentum is weakening, the Gold Zone may precede a downward move.

• If histogram momentum is strengthening, it may signal an upcoming rebound or rally.

Treat the Gold Zone as a warning of impending volatility, and always combine it with trend indicators for accurate directional judgment.

RISK DISCLAIMER

• This indicator calculates trend direction based on historical data and cannot guarantee future market performance. When using this indicator for trading, always combine it with other technical analysis tools, fundamental analysis, and personal trading experience for comprehensive decision-making.

• Market conditions are uncertain, and trend signals may result in false positives or lag. Traders should avoid over-reliance on indicator signals and implement stop-loss strategies and risk management techniques to reduce potential losses.

• Leverage trading carries high risks and may result in rapid capital loss. If using this indicator in leveraged markets (such as futures, forex, or cryptocurrency derivatives), exercise caution, manage risks properly, and set reasonable stop-loss/take-profit levels to protect funds.

• All trading decisions are the sole responsibility of the trader. The developer is not liable for any trading losses. This indicator is for technical analysis reference only and does not constitute investment advice.

• Before live trading, it is recommended to use a demo account for testing to fully understand how to use the indicator and apply proper risk management strategies.

CHANGELOG

v1.0: Initial release featuring integrated Price Action Index, Trend Strength Scoring, Wave Trend Oscillator, Gold Zone Compression Detection, and dual-type divergence recognition. Supports higher timeframe (HTF) synchronization, visual signal markers, and diversified parameter configurations.

Money Flow Pulse💸 In markets where volatility is cheap and structure is noisy, what matters most isn’t just the move — it’s the effort behind it. Money Flow Pulse (MFP) offers a compact, color-coded readout of real-time conviction by scoring volume-weighted price action on a five-tier scale. It doesn’t try to predict reversals or validate trends. Instead, it reveals the quality of the move in progress: is it fading , driving , exhausting , or hollow ?

🎨 MFP draws from the traditional Money Flow Index (MFI), a volume-enhanced momentum oscillator, but transforms it into a modular “pressure readout” that fits seamlessly into any structural overlay. Rather than oscillating between extremes with little interpretive guidance, MFP discretizes the flow into clean, color-coded regimes ranging from strong inflow (+2) to strong outflow (–2). The result is a responsive diagnostic layer that complements, rather than competes with, tools like ATR and/or On-Balance Volume.

5️⃣ MFP uses a normalized MFI value smoothed over 13 periods and classified into a 5-tier readout of Volume-Driven Conviction :

🍆 Exhaustion Inflow — usually a top or blowoff; not strength, but overdrive (+2)

🥝 Active Inflow — supportive of trend continuation (+1)

🍋 Neutral — chop, coil, or fakeouts (0)

🍑 Selling Intent — weakening structure, possible fade setups (-1)

🍆 Exhaustion Outflow — often signals forced selling or accumulation traps (-2)

🎭 These tiers are not arbitrary. Each one is tuned to reflect real capital behavior across timeframes. For instance, while +1 may support continuation, +2 often precedes exhaustion — especially on the lower timeframes. Similarly, a –1 reading during a pullback suggests sell-side pressure is building, but a shift to –2 may mean capitulation is already underway. The difference between the two can define whether a move is tradable continuation or strategic exhaustion .

🌊 The MFI ROC (Rate of Change) feature can be toggled to become a volatility-aware pulse monitor beneath the derived MFI tier. Instead of scoring direction or structure, ROC reveals how fast conviction is changing — not just where it’s headed, but how hard it's accelerating or decaying. It measures the raw Δ between the current and previous MFI values, exposing bursts of energy, fading pressure, or transitional churn .

🎢 Visually, ROC appears as a low-opacity area fill, anchored to a shared lemon-yellow zero line. When the green swell rises, buying pressure is accelerating; when the red drops, flow is actively deteriorating. A subtle bump may signal early interest — while a steep wave hints at an emotional overreaction. The ROC value itself provides numeric insight alongside the raw MFI score. A reading of +3.50 implies strong upside momentum in the flow — often supporting trend ignition. A score of –6.00 suggests rapid deceleration or full exhaustion — often preceding reversals or failed breakouts.

・ MFI shows you where the flow is

・ ROC tells you how it’s behaving

😎 This blend reveals not just structure or intent — but also urgency . And in flow-based trading, urgency often precedes outcome.

🧩 Divergence isn’t delay — it’s disagreement . One of the most revealing features of MFP is how it exposes momentum dissonance — situations where price and flow part ways. These divergences often front-run pivots , traps , or velocity stalls . Unlike RSI-style divergence, which whispers of exhaustion, MFI divergence signals a breakdown in conviction. The structure may extend — but the effort isn’t there.

・ Price ▲ MFI ▼ → Effortless Markup : Often signals distribution or a grind into liquidity. Without rising MFI, the rally lacks true flow participation — a warning of fragility.

・ Price ▼ MFI ▲ → Absorption or Early Accumulation : Price breaks down, but money keeps flowing in — a hidden bid. Watch for MFI tier shifts or ROC bursts to confirm a reversal.

🏄♂️ These moments don’t require signal overlays or setup hunting. MFP narrates the imbalance. When price breaks structure but flow does not — or vice versa — you’re not seeing trend, you’re seeing disagreement, and that's where edge begins.

💤 MFP is especially effective on intraday charts where volume dislocations matter most. On the 1H or 15m chart, it helps distinguish between breakouts with conviction versus those lacking flow. On higher timeframes, its resolution softens — it becomes more of a drift indicator than a trigger device. That’s by design: MFP prioritizes pulse, not position. It’s not the fire, it’s the heat.

📎 Use MFP in confluence with structural overlays to validate price behavior. A ribbon expansion with rising MFP is real. A compression breakout without +1 flow is "fishy". Watch how MFP behaves near key zones like anchored VWAP, MAs or accumulation pivots. When MFP rises into a +2 and fails to sustain, the reversal isn’t just technical — it’s flow-based.

🪟 MFP doesn’t speak loudly, but it never whispers without reason. It’s the pulse check before action — the breath of the move before the breakout. While it stays visually minimal on the chart, the true power is in the often overlooked Data Window, where traders can read and interpret the score in real time. Once internalized, these values give structure-aware traders a framework for conviction, continuation, or caution.

🛜 MFP doesn’t chase momentum — it confirms conviction. And in markets defined by noise, that signal isn’t just helpful — it’s foundational.

RSI+Stoch Band Oscillator📈 RSI + Stochastic Band Oscillator

Overview:

The RSI + Stochastic Band Oscillator is a technical indicator that combines the strengths of both the Relative Strength Index (RSI) and the Stochastic Oscillator. Instead of using static thresholds, this indicator dynamically constructs upper and lower bands based on the RSI and Stochastic overbought/oversold zones. It then measures the relative position of the current price within this adaptive range, effectively producing a normalized oscillator.

Key Components:

RSI-Based Dynamic Bands:

Using RSI values and exponential moving averages of price changes, upper and lower dynamic bands are constructed.

These bands adjust based on overbought and oversold levels, offering a more responsive framework than fixed RSI thresholds.

Stochastic-Based Dynamic Bands:

Similarly, Stochastic %K and %D values are used to construct dynamic bands.

These adapt to overbought and oversold levels by recalculating potential high/low values within the lookback window.

Oscillator Calculation:

The oscillator (osc) is computed as the relative position of the current close within the combined upper and lower bands of both RSI and Stochastic.

This value is normalized between 0 and 100, allowing clear identification of extreme conditions.

Visual Features:

The oscillator is plotted as a line between 0 and 100.

Color-filled areas highlight when the oscillator enters extreme zones:

Above 100 with falling momentum: Red zone (potential reversal).

Below 0 with rising momentum: Green zone (potential reversal).

Additional trend conditions (falling/rising RSI, %K, and %D) are used to strengthen reversal signals by confirming momentum shifts.

VolumePrice Intensity AnalyzerVolumePrice Intensity Analyzer

The VolumePrice Intensity Analyzer is a Pine Script v6 indicator designed to measure market activity intensity through the trading value (Price * Volume, scaled to millions). It helps traders identify significant volume-price interactions, track trends, and gauge momentum by combining volume analysis with trend-following tools.

Features:

Volume-Based Analysis: Calculates Price * Volume in millions to highlight market activity levels.

Trend Identification: Plots 20-day and 50-day SMAs of the trading value to smooth fluctuations and reveal sustained trends.

Relative Strength: Displays the ratio of daily Price * Volume to the long-term SMA in a separate pane, helping traders assess activity intensity relative to historical averages.

Real-Time Metrics: A table shows the current Price * Volume and its ratio to the long SMA, updated continuously with bold text formatting (v6 feature).

Alerts: Triggers notifications for high trading values (when Price * Volume exceeds 1.5x the long SMA) and SMA crossovers (short SMA crossing above long SMA).

Visual Cues: Uses dynamic bar colors (teal for bullish, gray for bearish) and background highlights to mark significant market activity.

Customizable Inputs: Adjust SMA periods, scaling factor, and alert threshold via the settings panel, with tooltips for clarity (v6 feature).

Originality:

Unlike basic volume indicators, this tool combines Price * Volume with trend analysis (SMAs), relative strength (ratio plot), and actionable alerts. The real-time table and visual highlights provide a unique, at-a-glance view of market intensity, making it a valuable addition for volume and trend-focused traders.

Calculations:

Trading Value (P*V): (Close * Volume) * Scale Factor (default scale factor of 1e-6 converts to millions).

SMAs: 20-day and 50-day Simple Moving Averages of the trading value to identify short- and long-term trends.

Ratio: Daily Price * Volume divided by the 50-day SMA, plotted in a separate pane to show relative activity strength.

Bar Colors: Teal (RGB: 0, 132, 141) for bullish bars (close > open or close > previous close), gray for bearish or neutral bars.

Background Highlight: Light yellow (hex: #ffcb3b, 81% transparency) when Price * Volume exceeds the long SMA by the alert threshold.

Plotted Elements:

Short SMA P*V (M): Red line, 20-day SMA of Price*Volume in millions.

Long SMA P*V (M): Blue line, 50-day SMA of Price*Volume in millions.

Today P*V (M): Columns, daily Price*Volume in millions (teal/gray based on price action).

Daily V*P/Longer Term Average: Purple line in a separate pane, ratio of daily Price * Volume to the 50-day SMA.

Usage:

Spot High Activity: Look for Price * Volume columns exceeding the SMAs or spikes in the ratio plot to identify significant market moves.

Confirm Trends: Use SMA crossovers (e.g., short SMA crossing above long SMA) as bullish trend signals, or vice versa for bearish trends.

Monitor Intensity: The table provides real-time Price * Volume and ratio values, while background highlights signal high activity periods.

Versatility: Suitable for stocks, forex, crypto, or any market with volume data, across various timeframes.

How to Use:

Add the indicator to your chart.

Adjust inputs (SMA periods, scale factor, alert threshold) via the settings panel to match your trading style.

Watch for alerts, check the table for real-time metrics, and observe the ratio plot for relative strength signals.

Use the background highlights and bar colors to quickly spot significant market activity and price action.

This indicator leverages Pine Script v6 features like lazy evaluation for performance and advanced text formatting for better visuals, making it a powerful tool for traders focusing on volume, trends, and momentum.

RSI Forecast [Titans_Invest]RSI Forecast

Introducing one of the most impressive RSI indicators ever created – arguably the best on TradingView, and potentially the best in the world.

RSI Forecast is a visionary evolution of the classic RSI, merging powerful customization with groundbreaking predictive capabilities. While preserving the core principles of traditional RSI, it takes analysis to the next level by allowing users to anticipate potential future RSI movements.

Real-Time RSI Forecasting:

For the first time ever, an RSI indicator integrates linear regression using the least squares method to accurately forecast the future behavior of the RSI. This innovation empowers traders to stay one step ahead of the market with forward-looking insight.

Highly Customizable:

Easily adapt the indicator to your personal trading style. Fine-tune a variety of parameters to generate signals perfectly aligned with your strategy.

Innovative, Unique, and Powerful:

This is the world’s first RSI Forecast to apply this predictive approach using least squares linear regression. A truly elite-level tool designed for traders who want a real edge in the market.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the RSI, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an RSI time series like this:

Time →

RSI →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted RSI, which can be crossed with the actual RSI to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public RSI with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining RSI with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

RSI Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_______________________________________________________________________

🥇 This is the world’s first RSI indicator with: Linear Regression for Forecasting 🥇_______________________________________________________________________

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE RSI❓

The Relative Strength Index (RSI) is a technical analysis indicator developed by J. Welles Wilder. It measures the magnitude of recent price movements to evaluate overbought or oversold conditions in a market. The RSI is an oscillator that ranges from 0 to 100 and is commonly used to identify potential reversal points, as well as the strength of a trend.

⯁ HOW TO USE THE RSI❓

The RSI is calculated based on average gains and losses over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and includes three main zones:

• Overbought: When the RSI is above 70, indicating that the asset may be overbought.

• Oversold: When the RSI is below 30, indicating that the asset may be oversold.

• Neutral Zone: Between 30 and 70, where there is no clear signal of overbought or oversold conditions.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📈 RSI Conditions:

🔹 RSI > Upper

🔹 RSI < Upper

🔹 RSI > Lower

🔹 RSI < Lower

🔹 RSI > Middle

🔹 RSI < Middle

🔹 RSI > MA

🔹 RSI < MA

📈 MA Conditions:

🔹 MA > Upper

🔹 MA < Upper

🔹 MA > Lower

🔹 MA < Lower

📈 Crossovers:

🔹 RSI (Crossover) Upper

🔹 RSI (Crossunder) Upper

🔹 RSI (Crossover) Lower

🔹 RSI (Crossunder) Lower

🔹 RSI (Crossover) Middle

🔹 RSI (Crossunder) Middle

🔹 RSI (Crossover) MA

🔹 RSI (Crossunder) MA

🔹 MA (Crossover) Upper

🔹 MA (Crossunder) Upper

🔹 MA (Crossover) Lower

🔹 MA (Crossunder) Lower

📈 RSI Divergences:

🔹 RSI Divergence Bull

🔹 RSI Divergence Bear

📈 RSI Forecast:

🔮 RSI (Crossover) MA Forecast

🔮 RSI (Crossunder) MA Forecast

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📉 RSI Conditions:

🔸 RSI > Upper

🔸 RSI < Upper

🔸 RSI > Lower

🔸 RSI < Lower

🔸 RSI > Middle

🔸 RSI < Middle

🔸 RSI > MA

🔸 RSI < MA

📉 MA Conditions:

🔸 MA > Upper

🔸 MA < Upper

🔸 MA > Lower

🔸 MA < Lower

📉 Crossovers:

🔸 RSI (Crossover) Upper

🔸 RSI (Crossunder) Upper

🔸 RSI (Crossover) Lower

🔸 RSI (Crossunder) Lower

🔸 RSI (Crossover) Middle

🔸 RSI (Crossunder) Middle

🔸 RSI (Crossover) MA

🔸 RSI (Crossunder) MA

🔸 MA (Crossover) Upper

🔸 MA (Crossunder) Upper

🔸 MA (Crossover) Lower

🔸 MA (Crossunder) Lower

📉 RSI Divergences:

🔸 RSI Divergence Bull

🔸 RSI Divergence Bear

📉 RSI Forecast:

🔮 RSI (Crossover) MA Forecast

🔮 RSI (Crossunder) MA Forecast

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : RSI Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

Kitty PMO [theUltimator5]Kitty PMO is a momentum analysis tool designed to visually track and interpret the Price Momentum Oscillator (PMO) — with stylistic influence inspired by the charting approach made popular by “theRoaringKitty.” It aims to offer clear, actionable momentum signals directly overlaid on the chart without clutter or ambiguity, making it ideal for traders who prioritize simplicity and signal clarity.

At its core, the indicator calculates the PMO by applying a custom recursive smoothing function to the rate of change (ROC) of price. This smoothed momentum measure is then:

Amplified by a scaling factor (×10),

Further smoothed using user-defined parameters,

Compared against a signal line (EMA of PMO),

And tracked with a secondary moving average (PMO MA) to capture medium-term trend inflections.

While the PMO and its associated signal lines can optionally be plotted, the indicator primarily emphasizes crossovers between the PMO MA and the other two components. When the PMO MA crosses above both the PMO and signal line, a green upward arrow (↑) is plotted below the price. When it crosses below both, a red downward arrow (↓) appears above the price — making it easy to spot potential turning points in momentum.

Additionally, a floating info table can be toggled on to display all current user-defined parameters in a clean, resizable format. This makes the script ideal not just for technical execution but also for real-time strategy tuning and tracking across multiple timeframes.

The script includes optional alerts so you can be notified the moment a key crossover signal is triggered, without needing to keep your eyes glued to the screen.

VWAP Separation Oscillator V5 (No Arrows)Okay, here is a draft description you can adapt for your TradingView publication. It starts from the basics and explains the concepts behind the indicator and how to interpret its visual elements.

VWAP Separation Oscillator

Summary

This indicator provides a normalized view of how far the current price has deviated from its Volume-Weighted Average Price (VWAP), helping traders identify potentially overbought or oversold conditions relative to recent VWAP dynamics. It calculates the price separation from VWAP and expresses it in terms of standard deviations (a Z-score), making it easier to gauge the statistical significance of the deviation.

Core Concepts Explained

What is VWAP?

VWAP stands for Volume-Weighted Average Price. It's a trading benchmark calculated by taking the total dollar value traded for every transaction (price multiplied by volume) and dividing it by the total shares traded for the day (or other chosen period).

Unlike a simple moving average, VWAP gives more weight to price levels where more volume occurred. Many institutional traders use it as a reference point for execution quality.

This indicator allows you to choose the "Anchor Period" (Session, Week, Month, etc.) which determines when the VWAP calculation resets.

What is VWAP Separation?

P

rice doesn't always stay at the VWAP; it naturally fluctuates above and below it.

"VWAP Separation" is simply the difference between the current price (Source) and the calculated VWAP value (Separation = Price - VWAP). A positive separation means the price is above VWAP; negative means below.

How Standard Deviation is Used:

While knowing the separation is useful, its significance can vary wildly between different stocks or market conditions. A $1 separation might be huge for one stock but tiny for another.

Standard Deviation is a statistical measure of how spread out data points are from their average. In this indicator, we calculate the standard deviation of the VWAP Separation over a specified Lookback Length. This tells us how volatile or dispersed the separation has been recently.

The Oscillator Line (Z-Score):

The main purple (or Green/Red) line plotted by this indicator is the Z-score of the VWAP Separation.

Formula conceptually: Oscillator Value = (Current Separation - Average Separation) / Standard Deviation of Separation

Interpretation: It tells you how many standard deviations the current separation is away from the average separation over the lookback period.

A value of +2.0 means the current separation is 2 standard deviations higher (more extended to the upside) than the average separation.

A value of -1.5 means the current separation is 1.5 standard deviations lower (more extended to the downside) than the average separation.

This normalization makes it easier to compare readings across different assets or timeframes and to define consistent thresholds for "extreme" deviations.

Visual Elements Explained

Oscillator Line: The primary line showing the Z-score value (explained above). Can optionally be colored Green/Red based on its slope (rising/falling).

Overbought Line (Solid Red): A user-defined level (default: 2.0). When the oscillator moves above this line, it suggests the price deviation above VWAP is statistically significant compared to recent history.

Oversold Line (Solid Green): A user-defined level (default: -2.0). When the oscillator moves below this line, it suggests the price deviation below VWAP is statistically significant compared to recent history.

Overbought/Oversold Zone Fills (Transparent Red/Green): These shaded areas appear only when the oscillator line enters the respective Overbought or Oversold territory (defined by the OB/OS Lines), visually highlighting these periods.

Zero Line (Dotted Gray): Represents the point where the current VWAP separation is exactly equal to the average VWAP separation over the lookback period. Crossings indicate shifts relative to this mean.

Zero Cross Markers (Orange 'X'): Small 'x' marks plotted directly on the oscillator line whenever it crosses the Zero Line, pinpointing these moments.

Potential Usage / Interpretation

Identifying Extremes: High positive values (above OB Level) or low negative values (below OS Level) can suggest the price move relative to VWAP might be over-extended and potentially due for a pause or pullback. Look for the oscillator turning back from these extremes.

Spotting Divergences: Look for discrepancies between price action and the oscillator.

Bearish Divergence: Price makes a new high, but the oscillator makes a lower high (often in the OB zone). Suggests weakening upside momentum relative to VWAP dynamics.

Bullish Divergence: Price makes a new low, but the oscillator makes a higher low (often in the OS zone). Suggests weakening downside momentum relative to VWAP dynamics.

Context is Key: This oscillator measures deviation from a specific benchmark (VWAP). Its interpretation should always be done within the context of the overall market trend, price structure (support/resistance), volume analysis, and potentially other confirming indicators.

Disclaimer: This indicator is a tool for analysis, not a standalone trading system. It does not provide financial advice. Always use risk management.

Settings Overview

Anchor Period: Determines how often the VWAP calculation resets (Session, Week, Month, etc.).

Source: The price data used for the separation calculation (default: hlc3).

Lookback Length: The number of bars used to calculate the average and standard deviation of the separation, influencing the oscillator's responsiveness.

Overbought/Oversold Levels: User-defined thresholds for identifying extreme Z-score values.

Color Oscillator Line: Option to color the oscillator line based on whether it's rising or falling.

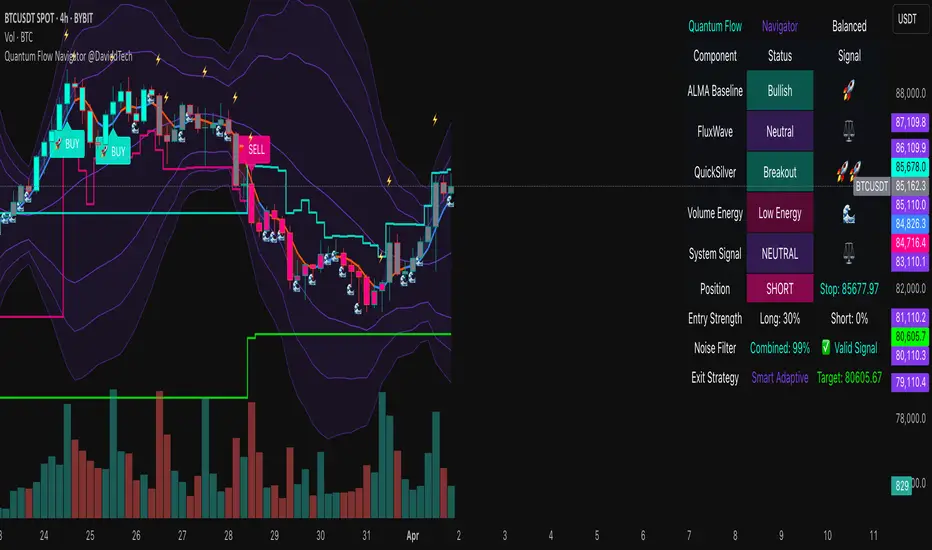

Quantum Flow Navigator @DaviddTechQuantum Flow Navigator – DaviddTech

Precision Strategy Builder Powered by Adaptive Filters, Statistical Noise Reduction & Multi-Modal Confirmation

🚀 Bullish Signal : Enter when ALMA, FluxWave, and QuickSilver all confirm bullish trend, with high volume and valid noise filter state.

🔻 Bearish Signal : Enter short when all components align bearishly and filters validate the signal.

🚪 Exit : Automatically managed by dynamic SL/TP or indicator-based reversal logic.

✅ Overview & DaviddTech Methodology

Quantum Flow Navigator is an advanced, multi-component trading system engineered around the strict modular logic of the DaviddTech methodology .

It integrates every core component required for a fully rule-based and signal-driven strategy—baseline, confirmations, volume filter, exit system, and noise filter.

Designed for traders who demand structure, clarity, and data-backed decision-making on 15M, 1H, and 4H charts.

🔍 Indicator Components

Baseline: Adaptive ALMA Filter

Smooth and responsive dynamic trend detection, with momentum validation and optional filled zones for enhanced visual feedback.

Confirmation #1: FluxWave Oscillator

Developed from an enhanced Trendlio concept by @dudeowns , FluxWave uses ALMA-smoothed rate-of-change logic with configurable signal behavior.

Confirmation #2: QuickSilver Band System

Custom breakout engine that maps volatility envelopes using multi-layered deviation bands for clear confirmation of structure breaks and trend direction.

Volume Filter: Normalized Volume Energy

Innovative volume filter inspired by @ceyhun 's work. Filters trades by classifying energy into High, Normal, or Low based on normalized volume context.

Exit System: Dynamic Momentum Stop Loss

Choose from Smart Adaptive, Trailing, Stepped, Percentage, ATR, or Volatility-adjusted logic. Supports TP via risk/reward, ATR multiples, or percentage targets.

Noise Filtration: Quantum Statistical Noise Reduction

Fuses Kalman smoothing with wavelet decomposition to eliminate non-signal noise and improve trade quality and confidence.

🎨 Visual System & Dashboard

🚀/🔻/🚪 Emoji Labels : Buy, sell, and exit trades clearly marked for instant recognition.

Color-Shifting Bars : Reflect FluxWave’s trend bias in real-time.

ALMA Fill Zone : Visual trend envelope between price and ALMA baseline.

QuickSilver Bands : Volatility envelopes with graduated depth for support/resistance awareness.

SL & TP Visuals : Dynamic stop-loss and take-profit zones plotted directly on chart.

Navigator Panel : In-chart dashboard displays real-time trend status, volume energy, noise filter state, signal strength, and active position tracking.

📈 How to Trade with It

Entry Mode Selection : Choose between Combined, ALMA, FluxWave, QuickSilver, or Custom scoring logic.

Final Signals : Trigger only when confirmations align, volume energy is valid, and noise is low.

Dashboard Summary : Use real-time signal display to validate entry strength.

Timeframes : 15M–1H recommended for swing/intraday setups; 5M–15M for automation.

💡 Advanced Features

Entry Strength Scoring: Composite weight of all active components + filters.

Cooldown System: Limits excessive signals in volatile periods.

Multiple Exit Strategies: SL & TP modes with optional indicator-based exits.

Statistical Filtering: Wavelet + Kalman combination optimizes entry confidence.

Full Alert Suite: Covers entries, exits, filter triggers, volume states, and more.

🧠 Suggested Strategy Usage

Wait for full confirmation from ALMA, FluxWave, and QuickSilver.

Ensure volume energy is High and noise filter confirms trend clarity.

Use adaptive SL/TP or indicator-based exits.

Monitor dashboard for live signal strength ≥ threshold.

Use “Balanced” mode for general use; switch to “Aggressive” for tighter signals.

📝 Credits & Originality

Concept based on DaviddTech’s component-driven methodology .

FluxWave Oscillator built as an evolved version of Trendlio with full signal customization — credit @dudeowns .

Volume Energy Filter adapted from the work of @ceyhun .

Noise filtration and system architecture developed independently using Pine Script v6.

All code and logic is original, non-rehashed, and completely refactored to ensure uniqueness.

Quantum Flow Navigator fuses adaptive baselines, confirmation logic, energy-based filters, and statistical refinement into a precision signal engine—optimized for traders who value structure, clarity, and control.

Triple StochasticTriple Stochastic Elasticity Indicator

This custom indicator leverages the power of multi-timeframe analysis by combining three Stochastic Oscillators across different timeframes to identify potential trade entries based on elasticity and divergence between momentum curves.

📊 How It Works:

The indicator plots Stochastic values from three timeframes (e.g., 5m, 15m, and 1h), allowing you to observe how momentum behaves at different scales.

It highlights moments of elasticity—where the Stochastics stretch apart and then begin to converge—potentially signaling a reversion opportunity or trend continuation.

By identifying these stretches and snapbacks in momentum alignment, you can better time your entries and exits with improved confidence.

🔍 Use Case:

Look for divergence or convergence between the Stochastics.

Ideal for trend-following entries, pullback setups, and momentum reversal spotting.

Works best when combined with price action, S/R zones, or volume confirmation.

🛠 Customization:

Timeframes for each Stochastic are fully customizable.

Options to tweak %K, %D, and smoothing values to fit your strategy.

I recommend to remove the D%

And set the following settings

5 : 3 : 3

14 : 3 : 3

56 : 12 :12

Visual alerts can be added for when certain conditions are met (e.g., all three Stochs cross overbought/oversold levels).

Stochastic with 4 %K LinesQuad Rotation Stochastic Strategy – Indicator Description

The Quad Rotation Strategy is a momentum-based technical analysis tool that overlays four distinct Stochastic %K lines on a single chart. Each line is calculated using a unique set of parameters, allowing traders to visualize and compare momentum signals across varying sensitivities — from fast-reacting setups to slower, trend-confirming ones.

This multi-speed stochastic view is designed to help traders:

Identify rotation points where shorter-term stochastic lines cross faster than longer-term lines, signaling early reversals or trend continuation.

Confirm strength or weakness in price action by observing alignment or divergence among the %K lines.

Fine-tune entries and exits by using fast %K lines for timing and slower ones for confirmation.

🔍 How It Works:

Four separate %K lines are plotted, each with configurable Length and Smoothing.

All lines are calculated using the standard Stochastic formula:

(%K = SMA of (Close - Low) / (High - Low) over period)

No %D lines are included to keep the focus on %K behavior across different speeds.

Standard overbought (80), oversold (20), and midline (50) levels are provided for context.

This indicator is best used in:

Trend continuation setups where faster stochastics pull back to oversold while slower ones remain bullish.

Reversal zones where all four %K lines converge or cross in extreme levels.

Range-bound environments where confluence of extremes offers swing trade opportunities.

Gas/Oil SpreadGas/Oil Spread Analyzer with Static Overbought/Oversold Zones

This indicator measures the spread between the actual price of natural gas and its oil-based equivalent, derived from a defined oil/gas ratio. It helps traders identify potential mispricings and mean-reversion opportunities between the two energy commodities.

Key Features:

- Calculates spread: Gas Price – Oil-Based Equivalent Price

- Supports dynamic or static oil/gas ratio

- Plots a smoothed version of the spread (SMA)

- Displays static overbought and oversold zones to highlight extreme deviations

Use Cases:

- Detect overvalued or undervalued gas relative to oil

- Spot potential reversion setups in intermarket trading

- Evaluate energy market dislocations and hedging opportunities