Trend Vector Pro v2.0Trend Vector Pro v2.0

👨💻 Developed by: Mohammed Bedaiwi

💡 Strategy Overview & Coherence

Trend Vector Pro (TVPro) is a momentum-based trend & reversal strategy that uses a custom smoothed oscillator, an optional ADX filter, and classic Pivot Points to create a single, coherent trading framework.

Instead of stacking random indicators, TVPro is built around these integrated components:

A custom momentum engine (signal generation)

An optional ADX filter (trend quality control)

Daily Pivot Points (context, targets & S/R)

Swing-based “Golden Bar” trailing stops (trade management)

Optional extended bar detection (overextension alerts)

All parts are designed to work together and are documented below to address originality & usefulness requirements.

🔍 Core Components & Justification

1. Custom Momentum Engine (Main Signal Source)

TVPro’s engine is a custom oscillator derived from the bar midpoint ( hl2 ), similar in spirit to the Awesome Oscillator but adapted and fully integrated into the strategy. It measures velocity and acceleration of price, letting the script distinguish between strong impulses, weakening trends, and pure noise.

2. ADX Filter (Trend Strength Validation – Optional)

Uses Average Directional Index (ADX) as a gatekeeper.

Why this matters: This prevents the strategy from firing signals in choppy, non-trending environments (when ADX is below the threshold) and keeps trades focused on periods of clear directional strength.

3. Classic Pivot Points (Context & Targets)

Calculates Daily Pivot Points ( PP, R1-R3, S1-S3 ) via request.security() using prior session data.

Why this matters: Momentum gives the signal, ADX validates the environment, and Pivots add external structure for risk and target planning. This is a designed interaction, not a random mashup.

🧭 Trend State Logic (5-State Bar Coloring)

The strategy uses the momentum's value + slope to define five states, turning the chart into a visual momentum map:

🟢 STRONG BULL (Bright Green): Momentum accelerating UP. → Strong upside impulse.

🌲 WEAK BULL (Dark Green): Momentum decelerating DOWN (while positive). → Pullback/pause zone.

🔴 STRONG BEAR (Bright Red): Momentum accelerating DOWN. → Strong downside impulse.

🍷 WEAK BEAR (Dark Red): Momentum decelerating UP (while negative). → Rally/short-covering zone.

🔵 NEUTRAL / CHOP (Cyan): Momentum is near zero (based on noise threshold). → Consolidation / low volatility.

🎯 Signal Logic Modes

TVPro provides two selectable entry styles, controlled by input:

Reversals Only (Cleaner Mode – Default): Targets trend flips. Entry triggers when the current state is Bullish (or Bearish) and the previous state was not. This reduces noise and over-trading.

All Strong Pulses (Aggressive Mode): Targets acceleration phases. Entry triggers when the bar turns to STRONG BULL or STRONG BEAR after any other state. This mode produces more trades.

📌 Risk Management Tools

🟡 Golden Bars – Trailing Stops: Yellow “Trail” Arrows mark confirmed Swing Highs/Lows. These are used as logical trailing stop levels based on market structure.

Extended Bars: Detects when price closes outside a 2-standard-deviation channel, flagging overextension where a pullback is more likely.

Pivot Points: Used as external targets for Take Profit and structural stop placement.

⚙️ Strategy Defaults (Crucial for Publication Compliance)

To keep backtest results realistic and in line with House Rules, TVPro is published with the following fixed default settings:

Order Size: 5% of equity per trade ( default_qty_value = 5 )

Commission: 0.04% per order ( commission_value = 0.04 )

Slippage: 2 ticks ( slippage = 2 )

Initial Capital: 10,000

📘 How to Trade with Trend Vector Pro

Entry: Take Long when a Long signal appears and confirm the bar is Green (Bull state). Short for Red (Bear state).

Stop Loss: Place the initial SL near the latest swing High/Low, or near a relevant Pivot level.

Trade Management: Follow Golden (Trail) Arrows to trail your stop behind structure.

Exits: Exit when: the trailing stop is hit, Price reaches a major Pivot level, or an opposite signal prints.

🛑 Disclaimer

This script is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always forward-test and use proper risk management before applying any strategy to live trading.

Indicatore Momentum (MOM)

Advanced Breakout System v2.0Advanced Breakout System v2.0

Developed by: Mohammed Bedaiwi

This script hunts for high-probability breakouts by combining price consolidation zones, volume spikes vs. average volume, smart money flow (OBV), and a Momentum Override for explosive moves that skip consolidation. Additionally, it automatically identifies and plots Support and Resistance levels with price labels to help you visualize market structure.

The system follows a "Watch & Confirm" logic: it first prints a WATCH setup, then a BUY only if price confirms strength.

💡 JUSTIFICATION OF CONCEPTS (MASHUP & ORIGINALITY)

This script is an original mashup combining several analytical concepts to address common breakout failures:

Volatility Compression Engine: Uses built-in functions like ta.highest() and ta.lowest() to mathematically define the setup phase where price volatility is compressed below a user-defined threshold.

Volume Spike Confirmation: The breakout must be confirmed by a volume increase greater than a moving average of volume, signaling strong market interest.

Smart Volume Filter (OBV): This is the key component. By checking if ta.obv is above its own Moving Average, we confirm that accumulation has been occurring during the consolidation period, suggesting institutional positioning before the price break.

Multi-Exit Risk System: Employs dynamic exits (EMA cross, volume dump, bearish pattern) instead of static stop-losses to manage risk adaptively based on real-time market action.

Market Structure Visualization: The script also includes a Support & Resistance engine to plot key swing pivots and price labels for visual context.

✅ STRATEGY RESULTS & POLICY COMPLIANCE

To ensure non-misleading and transparent backtesting results, this strategy is published with the following fully compliant properties:

Dataset Compliance: The backtest is performed on the CMTL Daily (1D) chart across a long history, generating 201 total trades. This significantly exceeds the minimum requirement of 100 trades, providing a robust test dataset.

Risk Control: The strategy uses a conservative order size set to 2% of equity (default_qty_value=2), strictly adhering to the sustainable risk recommendation of 5-10% of equity per trade.

Transaction Costs: Realistic trading conditions are modeled using 0.07% commission and 3 ticks slippage to prevent the overestimation of profitability.

⚙️ VISUAL GUIDE & SIGNAL LOGIC

Key Color Legend (Visual Guide):

WATCH – Setup (Yellow Arrow Down): Potential breakout setup detected.

BUY – Confirmation (Green Arrow Up): Confirmed breakout, triggered when price trades above the high of the WATCH candle.

SELL – Break (Orange Arrow): Short-term trend weakness, triggered when price closes below the Fast EMA (9).

SELL – Dump (Dark Red Arrow): Distribution / volume dump, triggered by a bearish candle with abnormally high volume.

SELL – Pattern (Purple Arrow): Bearish price-action pattern (such as a bearish engulfing).

Support & Resistance Lines (Red/Green): Small horizontal lines plotted at key swing points with exact price labels.

⌨️ INPUTS (DEFAULT SETTINGS)

Entry settings: Consolidation Lookback (default 20) = bars used to detect consolidation. Consolidation Range % (default 12%) = max allowed range size. Volume Spike Multiplier (default 1.2) = factor above average volume to count as a spike. Force Signal on Big Moves (default ON) = forces a WATCH signal on high-momentum moves.

Exit settings: Enable Fast Exit (EMA 9) toggles the SELL – Break signal. Dump Volume Multiplier defines what counts as “dump” volume.

Support & Resistance: Adjustable Pivot Left/Right bars control the sensitivity of the support and resistance lines.

⚠️ Disclaimer Trading involves significant risk of loss. This script is for educational and informational purposes only and is not financial advice or a recommendation to buy or sell any asset. BUY and SELL signals are rule-based and derived from historical behavior and do not guarantee future performance. Always use your own analysis and risk management. This is an open-source strategy; users are encouraged to test it across different symbols and timeframes.

Profitable Pair Correlation Divergence Scanner v6This strategy identifies divergence opportunities between two correlated assets using a combination of Z-Score spread analysis, trend confirmation, RSI & MACD momentum checks, correlation filters, and ATR-based stop-loss/take-profit management. It’s optimized for positive P&L and realistic trade execution.

Key Features:

Pair Divergence Detection:

Measures deviation between returns of two assets and identifies overbought/oversold spread conditions using Z-Score.

Trend Alignment:

Trades only in the direction of the primary asset’s trend using a fast EMA vs slow EMA filter.

Momentum Confirmation:

Confirms trades with RSI and MACD to reduce false signals.

Correlation Filter:

Ensures the pair is strongly correlated before taking trades, avoiding noisy signals.

Risk Management:

Dynamic ATR-based stop-loss and take-profit ensures proper reward-to-risk ratio.

Exit Conditions:

Automatically closes positions when Z-Score normalizes, or ATR-based exits are hit.

How It Works:

Calculate Returns:

Computes returns for both assets over the selected timeframe.

Z-Score Spread:

Calculates the spread between returns and normalizes it using moving average and standard deviation.

Trend Filter:

Only takes long trades if the fast EMA is above the slow EMA, and short trades if the fast EMA is below the slow EMA.

Momentum Confirmation:

Confirms trade direction with RSI (>50 for longs, <50 for shorts) and MACD alignment.

Correlation Check:

Ensures the pair’s recent correlation is strong enough to validate divergence signals.

Trade Execution:

Opens positions when Z-Score crosses thresholds and all conditions align. Positions close when Z-Score normalizes or ATR-based SL/TP is hit.

Plot Explanation:

Z-Score: Blue line shows divergence magnitude.

Entry Levels: Red/Green lines mark long/short thresholds.

Exit Zone: Gray lines show normalization zone.

EMA Trend Lines: Purple (fast), Orange (slow) for trend alignment.

Correlation: Teal overlay shows current correlation strength.

Usage Tips:

Use highly correlated pairs for best results (e.g., EURUSD/GBPUSD).

Run on higher timeframe charts (1h or 4h) to reduce noise.

Adjust ATR multiplier based on volatility to avoid premature stops.

Combine with alerts for automated notifications or webhook execution.

Conclusion:

The Profitable Pair Correlation Divergence Scanner v6 is designed for traders who want systematic, low-risk, positive P&L trading opportunities with minimal manual monitoring. By combining trend alignment, momentum confirmation, correlation filters, and dynamic exits, it reduces false signals and improves execution reliability.

Run it on TradingView and watch how it captures divergence opportunities while maintaining positive P&L across trades.

US Market Long Horizon Momentum Summary in one paragraph

US Market Long Horizon Momentum is a trend following strategy for US index ETFs and futures built around a single eighteen month time series momentum measure. It helps you stay long during persistent bull regimes and step aside or flip short when long term momentum turns negative.

Scope and intent

• Markets. Large cap US equity indices, liquid US index ETFs, index futures

• Timeframes. 4h/ Daily charts

• Default demo used in the publication. SPY on 4h timeframe chart

• Purpose. Provide a minimal long bias index timing model that can reduce deep drawdowns and capture major cycles without parameter mining

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique concept or fusion. One unscaled multiple month log return of an external benchmark symbol drives all entries and exits, with optional volatility targeting as a single risk control switch.

• Failure mode addressed. Fully passive buy and hold ignores the sign of long horizon momentum and can sit through multi year drawdowns. This script offers a way to step down risk in prolonged negative momentum without chasing short term noise.

• Testability. All parameters are visible in Inputs and the momentum series is plotted so users can verify every regime change in the Tester and on price history.

• Portable yardstick. The log return over a fixed window is a unit that can be applied to any liquid symbol with daily data.

Method overview in plain language

The method looks at how far the benchmark symbol has moved in log return terms over an eighteen month window in our example. If that long horizon return is positive the strategy allows a long stance on the traded symbol. If it is negative and shorts are enabled the strategy can flip short, otherwise it goes flat. There is an optional realised volatility estimate on the traded symbol that can scale position size toward a target annual volatility, but in the default configuration the model uses unit leverage and only the sign of momentum matters.

Base measures

Return basis. The core yardstick is the natural log of close divided by the close eighteen months ago on the benchmark symbol. Daily log returns of the traded symbol feed the realised volatility estimate when volatility targeting is enabled.

Components

• Component one Momentum eighteen months. Log of benchmark close divided by its close mom_lookback bars ago. Its sign defines the trend regime. No extra smoothing is applied beyond the long window itself.

• Component two Realised volatility optional. Standard deviation of daily log returns on the traded symbol over sixty three days. Annualised by the square root of 252. Used only when volatility targeting is enabled.

• Optional component Volatility targeting. Converts target annual volatility and realised volatility into a leverage factor clipped by a maximum leverage setting.

Fusion rule

The model uses a simple gate. First compute the sign of eighteen month log momentum on the benchmark symbol. Optionally compute leverage from volatility. The sign decides whether the strategy wants to be long, short, or flat. Leverage only rescales position size when enabled and does not change direction.

Signal rule

• Long suggestion. When eighteen month log momentum on the benchmark symbol is greater than zero, the strategy wants to be long.

• Short suggestion. When that log momentum is less than zero and shorts are allowed, the strategy wants to be short. If shorts are disabled it stays flat instead.

• Wait state. When the log momentum is exactly zero or history is not long enough the strategy stays flat.

• In position. In practice the strategy sits IN LONG while the sign stays positive and flips to IN SHORT or flat only when the sign changes.

Inputs with guidance

Setup

• Momentum Lookback (months). Controls the horizon of the log return on the benchmark symbol. Typical range 6 to 24 months. Raising it makes the model slower and more selective. Lowering it makes it more reactive and sensitive to medium term noise.

• Symbol. External symbol used for the momentum calculation, SPY by default. Changing it lets you time other indices or run signals from a benchmark while trading a correlated instrument.

Logic

• Allow Shorts. When true the strategy will open short positions during negative momentum regimes. When false it will stay flat whenever momentum is negative. Practical setting is tied to whether you use a margin account or an ETF that supports shorting.

Internal risk parameters (not exposed as inputs in this version) are:

• Target Vol (annual). Target annual volatility for volatility targeting, default 0.2.

• Vol Lookback (days). Window for realised volatility, default 63 trading days.

• Max Leverage. Cap on leverage when volatility targeting is enabled, default 2.

Usage recipes

Swing continuation

• Signal timeframe. Use the daily chart.

• Benchmark symbol. Leave at SPY for US equity index exposure.

• Momentum lookback. Eighteen months as a default, with twelve months as an alternative preset for a faster swing bias.

Properties visible in this publication

• Initial capital. 100000

• Base currency. USD

• Default order size method. 5% of the total capital in this example

• Pyramiding. 0

• Commission. 0.03 percent

• Slippage. 3 ticks

• Process orders on close. On

• Bar magnifier. Off

• Recalculate after order is filled. Off

• Calc on every tick. Off

• All request.security calls use lookahead = barmerge.lookahead_off

Realism and responsible publication

The strategy is for education and research only. It does not claim any guaranteed edge or future performance. All results in Strategy Tester are hypothetical and depend on the data vendor, costs, and slippage assumptions. Intrabar motion is not modeled inside daily bars so extreme moves and gaps can lead to fills that differ from live trading. The logic is built for standard candles and should not be used on synthetic chart types for execution decisions.

Performance is sensitive to regime structure in the US equity market, which may change over time. The strategy does not protect against single day crash risk inside bars and does not model gap risk explicitly. Past behavior of SPY and the momentum effect does not guarantee future persistence.

Honest limitations and failure modes

• Long sideways regimes with small net change over eighteen months can lead to whipsaw around the zero line.

• Very sharp V shaped reversals after deep declines will often be missed because the model waits for momentum to turn positive again.

• The sample size in a full SPY history is small because regime changes are infrequent, so any test must be interpreted as indicative rather than statistically precise.

• The model is highly dependent on the chosen lookback. Users should test nearby values and validate that behavior is qualitatively stable.

Legal

Education and research only. Not investment advice. You are responsible for your own decisions. Always test on historical data and in simulation with realistic costs before any live use.

Session Opening Range Breakout (ORBO)This strategy automates a classic Opening Range Breakout (ORBO) approach: it builds a price range for the first minutes after the market opens, then looks for strong breakouts above or below that range to catch early directional moves.

Concept

The idea behind ORBO is simple:

The first minutes after the session open are often highly informative.

Price forms an “opening range” that acts as a mini support/resistance zone.

A clean breakout beyond this zone can lead to high-momentum moves.

This script turns that logic into a fully backtestable strategy in TradingView.

How the strategy works

Opening Range Session

Default session: 09:30–09:50 (exchange time)

During this window, the script tracks:

orHigh → highest high within the session

orLow → lowest low within the session

This forms your Opening Range for the day.

Breakout Logic (after the window ends)

Once the defined session ends:

Long Entry:

If the close crosses above the Opening Range High (orHigh),

→ strategy.entry("OR Long", strategy.long) is triggered.

Short Entry:

If the close crosses below the Opening Range Low (orLow),

→ strategy.entry("OR Short", strategy.short) is triggered.

Only one opening range per day is considered, which keeps the logic clean and easy to interpret.

Daily Reset

At the start of a new trading day, the script resets:

orHigh := na

orLow := na

A fresh Opening Range is then built using the next session’s 09:30–09:50 candles.

This ensures entries are always based on today’s structure, not yesterday’s.

Visuals & Inputs

Inputs:

Opening range session → default: "0930-0950"

Show OR levels → toggle visibility of OR High / Low lines

Fill range body → optional shaded zone between OR High and OR Low

Chart visuals:

A green line marks the Opening Range High.

A red line marks the Opening Range Low.

Optional yellow fill highlights the entire OR zone.

Background shading during the session shows when the range is currently being built.

These visuals make it easy to see:

Where the OR sits relative to current price

How clean / noisy the breakout was

How often price respects or rejects the opening zone

Backtesting & Optimization

Because this is written as a strategy():

You can use TradingView’s Strategy Tester to view:

Win rate

Net profit

Drawdown

Profit factor

Equity curve

Ideas to experiment with:

Change the session window (e.g., 09:15–09:45, 10:00–10:30)

Apply to different:

Markets: indices, FX, crypto, stocks

Timeframes: 1m / 5m / 15m

Add your own:

Stop Loss & Take Profit levels

Time filters (only trade certain days / times)

Volatility filters (e.g., ATR, range size thresholds)

Higher-timeframe trend filter (e.g., only take longs above 200 EMA)

CSS_LFU_v0.1Overview:

A multi-factor, market-adaptive swing strategy designed for intraday and short-term crypto trading. It synthesizes momentum, volatility, and trend signals into a unified composite score over a configurable lookback window. The strategy leverages a modular, signal-weighted approach to ensure robust entry timing while remaining compatible with human-in-the-loop validation and algorithmic execution.

Core Modules:

AJFFRSI (RSX-based Momentum): Measures smoothed price momentum with noise-reduction filters to detect crossovers relative to the QQE trailing stop.

QQE (Quantitative Qualitative Easing RSI): A modified RSI with a dynamic trailing stop that adapts to short-term volatility, identifying exhaustion and potential reversal points.

Keltner Channel Zones: Determines overextension relative to trend, providing buy/sell zones based on ATR-banded EMA.

WaveTrend Oscillator: Confirms short-term swings and market direction through smoothed oscillator cross signals.

Rolling Composite Score: Aggregates module signals over a unified lookback (e.g., 144 bars) to normalize noise and capture consistent trends.

Signal Logic:

Each module outputs a discrete score (+1 / 0 / -1).

The rolling composite score sums all module scores over the lookback period.

Long positions trigger when the rolling score meets or exceeds the long threshold.

Short positions trigger when the rolling score meets or falls below the short threshold.

Multi-dimensional signal aggregation reduces false positives from single indicators.

Rolling lookback ensures score normalization across different volatility regimes.

Highly modular: easy to adapt modules or weights to different instruments or timeframes.

Fully compatible with automated execution pipelines, including custom exchange screener bots.

Use Case:

Ideal for quant-driven altcoin or multi-asset strategies where high-frequency validation is critical and sequential module weighting enhances trend flip detection.

Hash Momentum Strategy# Hash Momentum Strategy

## 📊 Overview

The **Hash Momentum Strategy** is a professional-grade momentum trading system designed to capture strong directional price movements with precision timing and intelligent risk management. Unlike traditional EMA crossover strategies, this system uses momentum acceleration as its primary signal, resulting in earlier entries and better risk-to-reward ratios.

---

## ⚡ What Makes This Strategy Unique

### 1. Momentum-Based Entry System

Most strategies rely on lagging indicators like moving average crossovers. This strategy captures momentum *acceleration* - entering when price movement is gaining strength, not after the move has already happened.

### 2. Programmable Risk-to-Reward

Set your exact R:R ratio (1:2, 1:2.5, 1:3, etc.) and the strategy automatically calculates stop loss and take profit levels. No more guessing or manual calculations.

### 3. Smart Partial Profit Taking

Lock in profits at multiple stages:

- **First TP**: Take 50% off at 2R

- **Second TP**: Take 40% off at 2.5R

- **Final TP**: Let 10% ride to maximum target

This approach locks in gains while letting winners run.

### 4. Dynamic Momentum Threshold

Uses ATR (Average True Range) multiplied by your threshold setting to adapt to market volatility. Volatile markets = higher threshold. Quiet markets = lower threshold.

### 5. Trade Cooldown System

Prevents overtrading and revenge trading by enforcing a cooldown period between trades. Configurable from 1-24 bars.

### 6. Optional Session & Weekend Filters

Filter trades by Tokyo, London, and New York sessions. Optional weekend-off toggle to avoid low-liquidity periods.

---

## 🎯 How It Works

### Signal Generation

**STEP 1: Calculate Momentum**

- Momentum = Current Price - Price

- Check if Momentum > ATR × Threshold Multiplier

- Momentum must be accelerating (positive change in momentum)

**STEP 2: Confirm with EMA Trend Filter**

- Long: Price must be above EMA

- Short: Price must be below EMA

**STEP 3: Check Filters**

- Not in cooldown period

- Valid session (if enabled)

- Not weekend (if enabled)

**STEP 4: ENTRY SIGNAL TRIGGERED**

### Risk Management Example

**Example Long Trade:**

- Entry: $100

- Stop Loss: $97.80 (2.2% risk)

- Risk Amount: $2.20

**Take Profit Levels:**

- TP1: $104.40 (2R = $4.40) → Close 50%

- TP2: $105.50 (2.5R = $5.50) → Close 40%

- Final: $105.50 (2.5R) → Close remaining 10%

---

## ⚙️ Settings Guide

### Core Strategy

**Momentum Length** (Default: 13)

Number of bars for momentum calculation. Higher = stronger but fewer signals.

**Momentum Threshold** (Default: 2.25)

ATR multiplier. Higher = only trade biggest moves.

**Use EMA Trend Filter** (Default: ON)

Only long above EMA, short below EMA.

**EMA Length** (Default: 28)

Period for trend-confirming EMA.

### Filters

**Use Trading Session Filter** (Default: OFF)

Restrict trading to specific sessions.

**Tokyo Session** (Default: OFF)

Trade during Asian hours (00:00-09:00 JST).

**London Session** (Default: OFF)

Trade during European hours (08:00-17:00 GMT).

**New York Session** (Default: OFF)

Trade during US hours (08:00-17:00 EST).

**Weekend Off** (Default: OFF)

Disable trading on Saturdays and Sundays.

### Risk Management

**Stop Loss %** (Default: 2.2)

Fixed percentage stop loss from entry.

**Risk:Reward Ratio** (Default: 2.5)

Your target reward as multiple of risk.

**Use Partial Profit Taking** (Default: ON)

Take profits in stages.

**First TP R:R** (Default: 2.0)

First target as multiple of risk.

**First TP Size %** (Default: 50)

Percentage of position to close at TP1.

**Second TP R:R** (Default: 2.5)

Second target as multiple of risk.

**Second TP Size %** (Default: 40)

Percentage of position to close at TP2.

### Trade Management

**Use Trade Cooldown** (Default: ON)

Prevent overtrading.

**Cooldown Bars** (Default: 6)

Bars to wait after closing a trade.

---

## 🎨 Visual Elements

### Chart Indicators

🟢 **Green Dot** (below bar) = Long entry signal

🔴 **Red Dot** (above bar) = Short entry signal

🔵 **Blue X** (above bar) = Long position closed

🟠 **Orange X** (below bar) = Short position closed

**EMA Line** = Trend direction (green when bullish, red when bearish)

**White Line** = Entry price

**Red Line** = Stop loss level

**Green Lines** = Take profit levels (TP1, TP2, Final)

### Dashboard

When not in real-time mode, a dashboard displays:

- Current position (LONG/SHORT/FLAT)

- Entry price

- Stop loss price

- Take profit price

- R:R ratio

- Current momentum strength

- Total trades

- Win rate

- Net profit %

---

## 📈 Recommended Settings by Timeframe

### 1-Hour Timeframe (Default)

- Momentum Length: 13

- Momentum Threshold: 2.25

- EMA Length: 28

- Stop Loss: 2.2%

- R:R Ratio: 2.5

- Cooldown: 6 bars

### 4-Hour Timeframe

- Momentum Length: 24-36

- Momentum Threshold: 2.5

- EMA Length: 50

- Stop Loss: 3-4%

- R:R Ratio: 2.0-2.5

- Cooldown: 6-8 bars

### 15-Minute Timeframe

- Momentum Length: 8-10

- Momentum Threshold: 2.0

- EMA Length: 20

- Stop Loss: 1.5-2%

- R:R Ratio: 2.0

- Cooldown: 4-6 bars

---

## 🔧 Optimization Tips

### Want More Trades?

- Decrease Momentum Threshold (2.0 instead of 2.25)

- Decrease Momentum Length (10 instead of 13)

- Decrease Cooldown Bars (4 instead of 6)

### Want Higher Quality Trades?

- Increase Momentum Threshold (2.5-3.0)

- Increase Momentum Length (18-24)

- Increase Cooldown Bars (8-10)

### Want Lower Drawdown?

- Increase Cooldown Bars

- Use tighter stop loss

- Enable session filters (trade only high-liquidity sessions)

- Enable Weekend Off

### Want Higher Win Rate?

- Increase R:R Ratio (may reduce total profit)

- Increase Momentum Threshold (fewer but stronger signals)

- Use longer EMA for trend confirmation

---

## 📊 Performance Expectations

Based on typical backtesting results:

- **Win Rate**: 35-45%

- **Profit Factor**: 1.5-2.0

- **Risk:Reward**: 1:2.5 (configurable)

- **Max Drawdown**: 10-20%

- **Trades/Month**: 8-15 (1H timeframe)

**Note:** Win rate may appear low, but with 2.5:1 R:R, you only need ~29% win rate to break even. The strategy aims for quality over quantity.

---

## 🎓 Strategy Logic Explained

### Why Momentum > EMA Crossover?

**EMA Crossover Problems:**

- Signals lag behind price

- Late entries = poor R:R

- Many false signals in ranging markets

**Momentum Advantages:**

- Catches moves as they start accelerating

- Earlier entries = better R:R

- Adapts to volatility via ATR

### Why Partial Profit Taking?

**Without Partial TPs:**

- All-or-nothing approach

- Winners often turn to losers

- High stress watching open positions

**With Partial TPs:**

- Lock in 50% at first target

- Reduce risk to breakeven

- Let remainder ride for bigger gains

- Lower psychological pressure

### Why Trade Cooldown?

**Without Cooldown:**

- Revenge trading after losses

- Overtrading in choppy markets

- Emotional decision-making

**With Cooldown:**

- Forces discipline

- Waits for new setup to develop

- Reduces transaction costs

- Better signal quality

---

## ⚠️ Important Notes

1. **This is a momentum strategy, not an EMA strategy**

The EMA only confirms trend direction. Momentum generates the actual signals.

2. **Backtest thoroughly before live trading**

Past performance ≠ future results. Test on your specific asset and timeframe.

3. **Use proper position sizing**

Risk 1-2% of account per trade maximum. The strategy uses 100% equity by default (adjust in Properties).

4. **Dashboard auto-hides in real-time**

Clean chart for live trading. Visible during backtesting.

5. **Customize for your trading style**

All settings are fully adjustable. No single "best" configuration.

---

## 🚀 Quick Start Guide

1. **Add to Chart**: Apply to your preferred asset and timeframe

2. **Keep Defaults**: Start with default settings

3. **Backtest**: Review historical performance

4. **Paper Trade**: Test with simulated money first

5. **Go Live**: Start small and scale up

---

## 💡 Pro Tips

**Tip 1: Combine Timeframes**

Use higher timeframe (4H) for trend direction, lower timeframe (1H) for entries.

**Tip 2: Avoid News Events**

Major news can cause whipsaws. Consider manual intervention during high-impact events.

**Tip 3: Monitor Momentum Strength**

Dashboard shows momentum in sigma (σ). Values >1.0σ indicate very strong momentum.

**Tip 4: Adjust for Volatility**

In high-volatility markets, increase threshold and stop loss. In quiet markets, decrease them.

**Tip 5: Review Losing Trades**

Check if losses are hitting stop loss or reversing. Adjust stop accordingly.

---

## 📝 Changelog

**v1.0** - Initial Release

- Momentum-based signal generation

- EMA trend filter

- Programmable R:R ratio

- Partial profit taking (3 stages)

- Trade cooldown system

- Session filters (Tokyo/London/New York)

- Weekend off toggle

- Smart dashboard (auto-hides in real-time)

- Clean visual design

---

## 🙏 Credits

Developed by **Hash Capital Research**

If you find this strategy useful, please give it a like and share with others!

---

## ⚖️ Disclaimer

This strategy is for educational purposes only. Trading involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Always do your own research and consult with a qualified financial advisor before trading.

---

## 📬 Feedback

Have suggestions or found a bug? Leave a comment below! I'm continuously improving this strategy based on community feedback.

---

**Happy Trading! 🚀📈**

MOMO – Imbalance Trend (SIMPLE BUY/SELL)MOMO – Imbalance Trend (SIMPLE BUY/SELL)

This strategy combines trend breaks, imbalance detection, and first-tap supply/demand entries to create a clean and disciplined trading model.

It automatically highlights imbalance candles, draws fresh zones, and waits for the first retest to deliver precise BUY and SELL signals.

Performance

On optimized settings, this strategy shows an estimated 57%–70% win-rate, depending on the asset and timeframe.

Actual performance may vary, but the model is built for consistency, discipline, and improved decision-making.

How it works

Detects trend structure shifts (BOS / Break of Trend)

Identifies displacement (imbalance) candles

Creates supply and demand zones from imbalance origin

Waits for first tap only (no second chances)

Confirms direction using trend logic

Generates clean BUY/SELL arrows

Automatic SL/TP based on user settings

Features

Clean BUY/SELL markers

Auto-drawn supply & demand zones

Trend break markers

Imbalance tags

Smart first-tap confirmation

Customizable stop loss & take profit

Works on crypto, gold, forex, indices

Best on M5–H1 for day trading

Note

This strategy is designed for day traders who want clarity, structure, and zero emotional trading.

Use it with discipline — and it will serve you well.

Good luck, soldier.

Natural Gas Intraday Strategy [15m] with Partial Profit & TrailBuy when:

1. Close > EMA 100 and EMA 20 > EMA 100

2. MACD (8,21,5) > Signal and histogram rising

3. RSI > 60

4. ATR > threshold (avoid flat market)

Sell when:

1. Close < EMA 100 and EMA 20 < EMA 100

2. MACD (8,21,5) < Signal and histogram falling

3. RSI < 40

4. ATR > threshold

Exit:

• SL = recent swing ± 0.5 ATR

• TP1 = 1 ATR, trail rest with EMA 20

Institution Accumulation/DistributionLeveraging the Williams%R oscillator, the script has been optimized to pick out key turning point in the market specifically at Resistance (Overbought) or Support (Oversold)

The algo has been programmed to print both buy and sell alerts at extremes/when conditions flip eg a long position will be closed simultaneously opening a short position above resistance.

Best used as a scalping tool targeting 30m and below works well with currency pairs

RSI-Adaptive T3 + Squeeze Momentum Strategy✅ Strategy Guide: RSI-Adaptive T3 + Squeeze Momentum Strategy

📌 Overview

The RSI-Adaptive T3 + Squeeze Momentum Strategy is a dynamic trend-following strategy based on an RSI-responsive T3 moving average and Squeeze Momentum detection .

It adapts in real-time to market volatility to enhance entry precision and optimize risk.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

The main objective of this strategy is to catch the early phase of a trend and generate consistent entry signals.

Designed to be intuitive and accessible for traders from beginner to advanced levels.

✨ Key Features

RSI-Responsive T3: T3 length dynamically adjusts according to RSI values for adaptive trend detection

Squeeze Momentum: Combines Bollinger Bands and Keltner Channels to identify trend buildup phases

Visual Triggers: Entry signals are generated from T3 crossovers and momentum strength after squeeze release

📊 Trading Rules

Long Entry:

When T3 crosses upward, momentum is positive, and the squeeze has just been released.

Short Entry:

When T3 crosses downward, momentum is negative, and the squeeze has just been released.

Exit (Reversal):

When the opposite condition to the entry is triggered, the position is reversed.

💰 Risk Management Parameters

Pair & Timeframe: BTC/USD (30-minute chart)

Capital (simulated): $30,00

Order size: `$100` per trade (realistic, low-risk sizing)

Commission: 0.02%

Slippage: 2 pips

Risk per Trade: 5%

Number of Trades (backtest period): 181

📊 Performance Overview

Symbol: BTC/USD

Timeframe: 30-minute chart

Date Range: January 1, 2024 – July 3, 2025

Win Rate: 47.8%

Profit Factor: 2.01

Net Profit: 173.16 (units not specified)

Max Drawdown: 5.77% or 24.91 (0.79%)

⚙️ Indicator Parameters

Indicator Name: RSI-Adaptive T3 + Squeeze Momentum

RSI Length: 14

T3 Min Length: 5

T3 Max Length: 50

T3 Volume Factor: 0.7

BB Length: 27 (Multiplier: 2.0)

KC Length: 20 (Multiplier: 1.5, TrueRange enabled)

🖼 Visual Support

T3 slope direction, squeeze status, and momentum bars are visually plotted on the chart,

providing high clarity for quick trend analysis and execution.

🔧 Strategy Improvements & Uniqueness

Inspired by the RSI Adaptive T3 by ChartPrime and Squeeze Momentum Indicator by LazyBear ,

this strategy fuses both into a hybrid trend-reversal and momentum breakout detection system .

Compared to traditional trend-following methods, it excels at capturing early trend signals with greater sensitivity .

✅ Summary

The RSI-Adaptive T3 + Squeeze Momentum Strategy combines momentum detection with volatility-responsive risk management.

With a strong balance between visual clarity and practicality, it serves as a powerful tool for traders seeking high repeatability.

⚠️ This strategy is based on historical data and does not guarantee future profits.

Always use appropriate risk management when applying it.

Kaufman Trend Strategy# ✅ Kaufman Trend Strategy – Full Description (Script Publishing Version)

**Kaufman Trend Strategy** is a dynamic trend-following strategy based on Kaufman Filter theory.

It detects real-time trend momentum, reduces noise, and aims to enhance entry accuracy while optimizing risk.

⚠️ _For educational and research purposes only. Past performance does not guarantee future results._

---

## 🎯 Strategy Objective

- Smooth price noise using Kaufman Filter smoothing

- Detect the strength and direction of trends with a normalized oscillator

- Manage profits using multi-stage take-profits and adaptive ATR stop-loss logic

---

## ✨ Key Features

- **Kaufman Filter Trend Detection**

Extracts directional signal using a state space model.

- **Multi-Stage Profit-Taking**

Automatically takes partial profits based on color changes and zero-cross events.

- **ATR-Based Volatility Stops**

Stops adjust based on swing highs/lows and current market volatility.

---

## 📊 Entry & Exit Logic

**Long Entry**

- `trend_strength ≥ 60`

- Green trend signal

- Price above the Kaufman average

**Short Entry**

- `trend_strength ≤ -60`

- Red trend signal

- Price below the Kaufman average

**Exit (Long/Short)**

- Blue trend color → TP1 (50%)

- Oscillator crosses 0 → TP2 (25%)

- Trend weakens → Final exit (25%)

- ATR + swing-based stop loss

---

## 💰 Risk Management

- Initial capital: `$3,000`

- Order size: `$100` per trade (realistic, low-risk sizing)

- Commission: `0.002%`

- Slippage: `2 ticks`

- Pyramiding: `1` max position

- Estimated risk/trade: `~0.1–0.5%` of equity

> ⚠️ _No trade risks more than 5% of equity. This strategy follows TradingView script publishing rules._

---

## ⚙️ Default Parameters

- **1st Take Profit**: 50%

- **2nd Take Profit**: 25%

- **Final Exit**: 25%

- **ATR Period**: 14

- **Swing Lookback**: 10

- **Entry Threshold**: ±60

- **Exit Threshold**: ±40

---

## 📅 Backtest Summary

- **Symbol**: USD/JPY

- **Timeframe**: 1H

- **Date Range**: Jan 3, 2022 – Jun 4, 2025

- **Trades**: 924

- **Win Rate**: 41.67%

- **Profit Factor**: 1.108

- **Net Profit**: +$1,659.29 (+54.56%)

- **Max Drawdown**: -$1,419.73 (-31.87%)

---

## ✅ Summary

This strategy uses Kaufman filtering to detect market direction with reduced lag and increased smoothness.

It’s built with visual clarity and strong trade management, making it practical for both beginners and advanced users.

---

## 📌 Disclaimer

This script is for educational and informational purposes only and should not be considered financial advice.

Use with proper risk controls and always test in a demo environment before live trading.

Reversal Trap Sniper – Verified VersionReversal Trap Sniper

Overview

Reversal Trap Sniper is a counterintuitive momentum-following strategy that identifies "reversal traps"—situations where traders expect a market reversal based on RSI, but the price continues trending. By detecting these failed reversal signals, the strategy enters trades in the trend direction, often catching strong follow-through moves.

How It Works

The system monitors the Relative Strength Index (RSI). When RSI moves above the overbought level (e.g., 70) and then drops back below it, many traders interpret this as a sell signal.

However, this strategy treats such moves with caution. If the RSI pulls back below the overbought threshold but the price continues to rise, the system considers it a "reversal trap"—a fakeout.

In such cases, instead of going short, the strategy enters a long position, assuming that the trend is still valid and those betting on a reversal may fuel a breakout.

Similarly, if RSI rises above the oversold level from below, but price continues falling, a short trade is triggered.

Entries are followed by ATR-based stop-loss and dynamic take-profit (2× risk), with a fallback time-based exit after 30 bars.

Key Features

- Detects failed RSI-based reversals ("traps")

- Follows momentum after the trap is triggered

- Uses ATR for dynamic stop-loss and take-profit

- Auto-exit after a fixed bar count (30 bars)

- Visual markers on chart for transparency

- Realistic trading assumptions: 0.05% commission, slippage, and capped pyramiding

Parameter Explanation

RSI Length (14): Standard RSI calculation period

Overbought/Oversold Levels (70/30): Common thresholds used by many traders

ATR Length (14): Used to define stop-loss and target dynamically

Risk-Reward Ratio (2.0): Take-profit is set at 2× the stop-loss distance

Max Holding Bars (30): Ensures trades don’t remain open indefinitely

Pyramiding (10): Allows scaling into trades, simulating real-world strategy stacking

Originality Note

This strategy inverts traditional RSI logic. Instead of treating overbought/oversold conditions as signals for reversal, it waits for those signals to fail. Only after such failures, confirmed by continued price action in the same direction, does the system enter trades. This logic is based on the behavioral observation that failed reversal signals often trigger stronger trend continuation—making this strategy uniquely positioned to exploit trap scenarios.

Disclaimer

This script is for educational and research purposes only. Trading involves risk, and past performance does not guarantee future results. Always test thoroughly before applying with live capital.

Volatility Pulse with Dynamic ExitVolatility Pulse with Dynamic Exit

Overview

This strategy, Volatility Pulse with Dynamic Exit, is designed to capture impulsive price moves following volatility expansions, while ensuring risk is managed dynamically. It avoids trades during low-volatility periods and uses momentum confirmation to enter positions. Additionally, it features a time-based forced exit system to limit overexposure.

How It Works

A position is opened when the current ATR (Average True Range) significantly exceeds its 20-period average, signaling a volatility expansion.

To confirm the move is directional and not random noise, the strategy checks for momentum: the close must be above/below the close of 20 bars ago.

Low volatility zones are filtered out to avoid chop and poor trade entries.

Upon entry, a dynamic stop-loss is set at 1x ATR, while take-profit is set at 2x ATR, offering a 2:1 reward-to-risk ratio.

If the position remains open for more than 42 bars, it is forcefully closed, even if targets are not hit. This prevents long-lasting, stagnant trades.

Key Features

✅ Volatility-based breakout detection

✅ Momentum confirmation filter

✅ Dynamic stop-loss and take-profit based on real-time ATR

✅ Time-based forced exit (42 bars max holding)

✅ Low-volatility environment filter

✅ Realistic settings with 0.05% commission and slippage included

Parameters Explanation

ATR Length (14): Captures recent volatility over ~2 weeks (14 candles).

Momentum Lookback (20): Ensures meaningful price move confirmation.

Volatility Expansion Threshold (0.5x): Strategy activates only when ATR is at least 50% above its average.

Minimum ATR Filter (1.0x): Avoids entries in tight, compressed market ranges.

Max Holding (42 bars): Trades are closed after 42 bars if no exit signal is triggered.

Risk-Reward (2.0x): Aiming for 2x ATR as profit for every 1x ATR risk.

Originality Note

While volatility and momentum have been used separately in many strategies, this script combines both with a time-based dynamic exit system. This exit rule, combined with an ATR-based filter to exclude low-activity periods, gives the system a practical edge in real-world use. It avoids classic rehashes and integrates real trading constraints for better applicability.

Disclaimer

This is a research-focused trading strategy meant for backtesting and educational purposes. Always use proper risk management and perform due diligence before applying to real funds.

EMA Pullback Speed Strategy 📌 **Overview**

The **EMA Pullback Speed Strategy** is a trend-following approach that combines **price momentum** and **Exponential Moving Averages (EMA)**.

It aims to identify high-probability entry points during brief pullbacks within ongoing uptrends or downtrends.

The strategy evaluates **speed of price movement**, **relative position to dynamic EMA**, and **candlestick patterns** to determine ideal timing for entries.

One of the key concepts is checking whether the price has **“not pulled back too much”**, helping focus only on situations where the trend is likely to continue.

⚠️ This strategy is designed for educational and research purposes only. It does not guarantee future profits.

🧭 **Purpose**

This strategy addresses the common issue of **"jumping in too late during trends and taking unnecessary losses."**

By waiting for a healthy pullback and confirming signs of **trend resumption**, traders can enter with greater confidence and reduce false entries.

🎯 **Strategy Objectives**

* Enter in the direction of the prevailing trend to increase win rate

* Filter out false signals using pullback depth, speed, and candlestick confirmations

* Predefine Take-Profit (TP) and Stop-Loss (SL) levels for safer, rule-based trading

✨ **Key Features**

* **Dynamic EMA**: Reacts faster when price moves quickly, slower when market is calm – adapting to current momentum

* **Pullback Filter**: Avoids trades when price pulls back too far (e.g., more than 5%), indicating a trend may be weakening

* **Speed Check**: Measures how strongly the price returns to the trend using candlestick body speed (open-to-close range in ticks)

📊 **Trading Rules**

**■ Long Entry Conditions:**

* Current price is above the dynamic EMA (indicating uptrend)

* Price has pulled back toward the EMA (a "buy the dip" situation)

* Pullback depth is within the threshold (not excessive)

* Candlesticks show consecutive bullish closes and break the previous high

* Price speed is strong (positive movement with momentum)

**■ Short Entry Conditions:**

* Current price is below the dynamic EMA (indicating downtrend)

* Price has pulled back up toward the EMA (a "sell the rally" setup)

* Pullback is within range (not too deep)

* Candlesticks show consecutive bearish closes and break the previous low

* Price speed is negative (downward momentum confirmed)

**■ Exit Conditions (TP/SL):**

* **Take-Profit (TP):** Fixed 1.5% target above/below entry price

* **Stop-Loss (SL):** Based on recent price volatility, calculated using ATR × 4

💰 **Risk Management Parameters**

* Symbol & Timeframe: BTCUSD on 1-hour chart (H1)

* Test Capital: \$3000 (simulated account)

* Commission: 0.02%

* Slippage: 2 ticks (minimal execution lag)

* Max risk per trade: 5% of account balance

* Backtest Period: Aug 30, 2023 – May 9, 2025

* Profit Factor (PF): 1.965 (Net profit ÷ Net loss, including spreads & fees)

⚙️ **Trading Parameters & Indicator Settings**

* Maximum EMA Length: 50

* Accelerator Multiplier: 3.0

* Pullback Threshold: 5.0%

* ATR Period: 14

* ATR Multiplier (SL distance): 4.0

* Fixed TP: 1.5%

* Short-term EMA: 21

* Long-term EMA: 50

* Long Speed Threshold: ≥ 1000.0 (ticks)

* Short Speed Threshold: ≤ -1000.0 (ticks)

⚠️Adjustments are based on BTCUSD.

⚠️Forex and other currency pairs require separate adjustments.

🔧 **Strategy Improvements & Uniqueness**

Unlike basic moving average crossovers or RSI triggers, this strategy emphasizes **"momentum-supported pullbacks"**.

By combining dynamic EMA, speed checks, and candlestick signals, it captures trades **as if surfing the wave of a trend.**

Its built-in filters help **avoid overextended pullbacks**, which often signal the trend is ending – making it more robust than traditional trend-following systems.

✅ **Summary**

The **EMA Pullback Speed Strategy** is easy to understand, rule-based, and highly reproducible – ideal for both beginners and intermediate traders.

Because it shows **clear visual entry/exit points** on the chart, it’s also a great tool for practicing discretionary trading decisions.

⚠️ Past performance is not a guarantee of future results.

Always respect your Stop-Loss levels and manage your position size according to your risk tolerance.

Momentum + Keltner Stochastic Combo)The Momentum-Keltner-Stochastic Combination Strategy: A Technical Analysis and Empirical Validation

This study presents an advanced algorithmic trading strategy that implements a hybrid approach between momentum-based price dynamics and relative positioning within a volatility-adjusted Keltner Channel framework. The strategy utilizes an innovative "Keltner Stochastic" concept as its primary decision-making factor for market entries and exits, while implementing a dynamic capital allocation model with risk-based stop-loss mechanisms. Empirical testing demonstrates the strategy's potential for generating alpha in various market conditions through the combination of trend-following momentum principles and mean-reversion elements within defined volatility thresholds.

1. Introduction

Financial market trading increasingly relies on the integration of various technical indicators for identifying optimal trading opportunities (Lo et al., 2000). While individual indicators are often compromised by market noise, combinations of complementary approaches have shown superior performance in detecting significant market movements (Murphy, 1999; Kaufman, 2013). This research introduces a novel algorithmic strategy that synthesizes momentum principles with volatility-adjusted envelope analysis through Keltner Channels.

2. Theoretical Foundation

2.1 Momentum Component

The momentum component of the strategy builds upon the seminal work of Jegadeesh and Titman (1993), who demonstrated that stocks which performed well (poorly) over a 3 to 12-month period continue to perform well (poorly) over subsequent months. As Moskowitz et al. (2012) further established, this time-series momentum effect persists across various asset classes and time frames. The present strategy implements a short-term momentum lookback period (7 bars) to identify the prevailing price direction, consistent with findings by Chan et al. (2000) that shorter-term momentum signals can be effective in algorithmic trading systems.

2.2 Keltner Channels

Keltner Channels, as formalized by Chester Keltner (1960) and later modified by Linda Bradford Raschke, represent a volatility-based envelope system that plots bands at a specified distance from a central exponential moving average (Keltner, 1960; Raschke & Connors, 1996). Unlike traditional Bollinger Bands that use standard deviation, Keltner Channels typically employ Average True Range (ATR) to establish the bands' distance from the central line, providing a smoother volatility measure as established by Wilder (1978).

2.3 Stochastic Oscillator Principles

The strategy incorporates a modified stochastic oscillator approach, conceptually similar to Lane's Stochastic (Lane, 1984), but applied to a price's position within Keltner Channels rather than standard price ranges. This creates what we term "Keltner Stochastic," measuring the relative position of price within the volatility-adjusted channel as a percentage value.

3. Strategy Methodology

3.1 Entry and Exit Conditions

The strategy employs a contrarian approach within the channel framework:

Long Entry Condition:

Close price > Close price periods ago (momentum filter)

KeltnerStochastic < threshold (oversold within channel)

Short Entry Condition:

Close price < Close price periods ago (momentum filter)

KeltnerStochastic > threshold (overbought within channel)

Exit Conditions:

Exit long positions when KeltnerStochastic > threshold

Exit short positions when KeltnerStochastic < threshold

This methodology aligns with research by Brock et al. (1992) on the effectiveness of trading range breakouts with confirmation filters.

3.2 Risk Management

Stop-loss mechanisms are implemented using fixed price movements (1185 index points), providing definitive risk boundaries per trade. This approach is consistent with findings by Sweeney (1988) that fixed stop-loss systems can enhance risk-adjusted returns when properly calibrated.

3.3 Dynamic Position Sizing

The strategy implements an equity-based position sizing algorithm that increases or decreases contract size based on cumulative performance:

$ContractSize = \min(baseContracts + \lfloor\frac{\max(profitLoss, 0)}{equityStep}\rfloor - \lfloor\frac{|\min(profitLoss, 0)|}{equityStep}\rfloor, maxContracts)$

This adaptive approach follows modern portfolio theory principles (Markowitz, 1952) and Kelly criterion concepts (Kelly, 1956), scaling exposure proportionally to account equity.

4. Empirical Performance Analysis

Using historical data across multiple market regimes, the strategy demonstrates several key performance characteristics:

Enhanced performance during trending markets with moderate volatility

Reduced drawdowns during choppy market conditions through the dual-filter approach

Optimal performance when the threshold parameter is calibrated to market-specific characteristics (Pardo, 2008)

5. Strategy Limitations and Future Research

While effective in many market conditions, this strategy faces challenges during:

Rapid volatility expansion events where stop-loss mechanisms may be inadequate

Prolonged sideways markets with insufficient momentum

Markets with structural changes in volatility profiles

Future research should explore:

Adaptive threshold parameters based on regime detection

Integration with additional confirmatory indicators

Machine learning approaches to optimize parameter selection across different market environments (Cavalcante et al., 2016)

References

Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple technical trading rules and the stochastic properties of stock returns. The Journal of Finance, 47(5), 1731-1764.

Cavalcante, R. C., Brasileiro, R. C., Souza, V. L., Nobrega, J. P., & Oliveira, A. L. (2016). Computational intelligence and financial markets: A survey and future directions. Expert Systems with Applications, 55, 194-211.

Chan, L. K. C., Jegadeesh, N., & Lakonishok, J. (2000). Momentum strategies. The Journal of Finance, 51(5), 1681-1713.

Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance, 48(1), 65-91.

Kaufman, P. J. (2013). Trading systems and methods (5th ed.). John Wiley & Sons.

Kelly, J. L. (1956). A new interpretation of information rate. The Bell System Technical Journal, 35(4), 917-926.

Keltner, C. W. (1960). How to make money in commodities. The Keltner Statistical Service.

Lane, G. C. (1984). Lane's stochastics. Technical Analysis of Stocks & Commodities, 2(3), 87-90.

Lo, A. W., Mamaysky, H., & Wang, J. (2000). Foundations of technical analysis: Computational algorithms, statistical inference, and empirical implementation. The Journal of Finance, 55(4), 1705-1765.

Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77-91.

Moskowitz, T. J., Ooi, Y. H., & Pedersen, L. H. (2012). Time series momentum. Journal of Financial Economics, 104(2), 228-250.

Murphy, J. J. (1999). Technical analysis of the financial markets: A comprehensive guide to trading methods and applications. New York Institute of Finance.

Pardo, R. (2008). The evaluation and optimization of trading strategies (2nd ed.). John Wiley & Sons.

Raschke, L. B., & Connors, L. A. (1996). Street smarts: High probability short-term trading strategies. M. Gordon Publishing Group.

Sweeney, R. J. (1988). Some new filter rule tests: Methods and results. Journal of Financial and Quantitative Analysis, 23(3), 285-300.

Wilder, J. W. (1978). New concepts in technical trading systems. Trend Research.

BB Breakout + Momentum Squeeze [Strategy]This Strategy is Based on 3 free indicators

- Bollinger Bands Breakout Oscillator: Link

- TTM Squeeze Pro: Link

- Rolling ATR Bands: Link

Bollinger Bands Breakout Oscillator - This tool shows how strong a market trend is by measuring how often prices move outside their normal Bollinger bands range. It helps you see whether prices are strongly moving in one direction or just moving sideways. By looking at how much and how frequently prices push beyond their typical boundaries, you can identify which direction the market is heading over your selected time period.

TM Squeeze Pro - This is a custom version of the TTM Squeeze indicator.

It's designed to help traders spot consolidation phases in the market (when price is coiling or "squeezing") and to catch breakouts early when volatility returns. The logic is based on the relationship between Bollinger Bands and Keltner Channels, combined with a momentum oscillator to show direction and strength.

Rolling ATR Bands - This indicator combines volatility bands (ATR) with momentum and trend signals to show where the market might be breaking out, retesting, or trending. It's highly visual and helpful for traders looking to time entries/exits during trending or volatile moves.

Logic Of the Strategy:

We are going to use the Bollinger Bands Breakout to determine the direction of the market. Than check the Volatility of the price by looking at the TTM Squeeze indicator. And use the ATR Bands to determine dynamic Stop Losses and based on the calculate the Take Profit targets and quantity for each position dynamically.

For the Long Setup:

1. We need to see the that Bull Power (Green line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

For the Short Setup:

1. We need to see the that Bear Power (Red line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

Stop Loss is determined by the Lower ATR Band (for the Long entry) and Upper ATR Band (For the Short entry)

Take Profit is 1:1.5 risk reward ration, which means if the Stop loss is 1% the TP target will be 1.5%

Move stop Loss to Breakeven: If the price will go in the direction of the trade for at least half of the Risk Reward target then the stop will automatically be adjusted to the entry price. For Example: the Stop Loss is 1%, the price has move at least 0.5% in the direction of your trade and that will move the Stop Loss level to the Entry point.

You can Adjust the parameters for each indicator used in that script and also adjust the Risk and Money management block to see how the PnL will change.

VIDYA Auto-Trading(Reversal Logic)Overview

This script is a dynamic trend-following strategy based on the Variable Index Dynamic Average (VIDYA). It adapts in real time to market volatility, aiming to enhance entry precision and optimize risk management.

⚠️ This strategy is intended for educational and research purposes. Past performance does not guarantee future results. All results are based on historical simulations using fixed parameters.

Strategy Objectives

The objective of this strategy is to respond swiftly to sudden price movements and trend reversals, providing consistent and reliable trade signals under historical testing conditions. It is designed to be intuitive and efficient for traders of all levels.

Key Features

Momentum Sensitivity via VIDYA: Reacts quickly to momentum shifts, allowing for accurate trend-following entries.

Volatility-Based ATR Bands: Automatically adjusts stop levels and entry conditions based on current market volatility.

Intuitive Trend Visualization: Uptrends are marked with green zones, and downtrends with red zones, giving traders clear visual guidance.

Trading Rules

Long Entry: Triggered when price crosses above the upper band. Any existing short position is closed.

Short Entry: Triggered when price crosses below the lower band. Any existing long position is closed.

Exit Conditions: Positions are reversed based on signal changes, using a position reversal strategy.

Risk Management Parameters

Market: ETHUSD(5M)

Account Size: $3,000 (reasonable approximation for individual traders)

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted to comply with TradingView guidelines for realistic risk levels)

Number of Trades: 251 (based on backtest over the selected dataset)

⚠️ The risk per trade and other values can be customized. Users are encouraged to adapt these to their individual needs and broker conditions.

Trading Parameters & Considerations

VIDYA Length: 10

VIDYA Momentum: 20

Distance factor for upper/lower bands: 2

Source: close

Visual Support

Trend zones, entry points, and directional shifts are clearly plotted on the chart. These visual cues enhance the analytical experience and support faster decision-making.

Visual elements are designed to improve interpretability and are not intended as financial advice or trade signals.

Strategy Improvements & Uniqueness

Inspired by the public work of BigBeluga, this script evolves the original concept with meaningful enhancements. By combining VIDYA and ATR bands, it offers greater adaptability and practical value compared to conventional trend-following strategies.

This adaptation is original work and not a direct copy. Improvements are designed to enhance usability, risk control, and market responsiveness.

Summary

This strategy offers a responsive and adaptive approach to trend trading, built on momentum detection and volatility-adjusted risk management. It balances clarity, precision, and practicality—making it a powerful tool for traders seeking reliable trend signals.

⚠️ All results are based on historical data and are subject to change under different market conditions. This script does not guarantee profit and should be used with caution and proper risk management.

SuperTrend AI Oscillator StrategySuperTrend AI Oscillator Strategy

Overview

This strategy is a trend-following approach that combines the SuperTrend indicator with oscillator-based filtering.

By identifying market trends while utilizing oscillator-based momentum analysis, it aims to improve entry precision.

Additionally, it incorporates a trailing stop to strengthen risk management while maximizing profits.

This strategy can be applied to various markets, including Forex, Crypto, and Stocks, as well as different timeframes. However, its effectiveness varies depending on market conditions, so thorough testing is required.

Features

1️⃣ Trend Identification Using SuperTrend

The SuperTrend indicator (a volatility-adjusted trend indicator based on ATR) is used to determine trend direction.

A long entry is considered when SuperTrend turns bullish.

A short entry is considered when SuperTrend turns bearish.

The goal is to capture clear trend reversals and avoid unnecessary trades in ranging markets.

2️⃣ Entry Filtering with an Oscillator

The Super Oscillator is used to filter entry signals.

If the oscillator exceeds 50, it strengthens long entries (indicating strong bullish momentum).

If the oscillator drops below 50, it strengthens short entries (indicating strong bearish momentum).

This filter helps reduce trades in uncertain market conditions and improves entry accuracy.

3️⃣ Risk Management with a Trailing Stop

Instead of a fixed stop loss, a SuperTrend-based trailing stop is implemented.

The stop level adjusts automatically based on market volatility.

This allows profits to run while managing downside risk effectively.

4️⃣ Adjustable Risk-Reward Ratio

The default risk-reward ratio is set at 1:2.

Example: A 1% stop loss corresponds to a 2% take profit target.

The ratio can be customized according to the trader’s risk tolerance.

5️⃣ Clear Trade Signals & Visual Support

Green "BUY" labels indicate long entry signals.

Red "SELL" labels indicate short entry signals.

The Super Oscillator is plotted in a separate subwindow to visually assess trend strength.

A real-time trailing stop is displayed to support exit strategies.

These visual aids make it easier to identify entry and exit points.

Trading Parameters & Considerations

Initial Account Balance: Default is $7,000 (adjustable).

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 1,032

Visual Aids for Clarity

This strategy includes clear visual trade signals to enhance decision-making:

Green "BUY" labels for long entries

Red "SELL" labels for short entries

Super Oscillator plotted in a subwindow with a 50 midline

Dynamic trailing stop displayed for real-time trend tracking

These visual aids allow traders to quickly identify trade setups and manage positions with greater confidence.

Summary

The SuperTrend AI Oscillator Strategy is developed based on indicators from Black Cat and LuxAlgo.

By integrating high-precision trend analysis with AI-based oscillator filtering, it provides a strong risk-managed trading approach.

Important Notes

This strategy does not guarantee profits—performance varies based on market conditions.

Past performance does not guarantee future results. Markets are constantly changing.

Always test extensively with backtesting and demo trading before using it in live markets.

Risk management, position sizing, and market conditions should always be considered when trading.

Conclusion

This strategy combines trend analysis with momentum filtering, enhancing risk management in trading.

By following market trends carefully, making precise entries, and using trailing stops, it seeks to reduce risk while maximizing potential profits.

Before using this strategy, be sure to test it thoroughly via backtesting and demo trading, and adjust the settings to match your trading style.

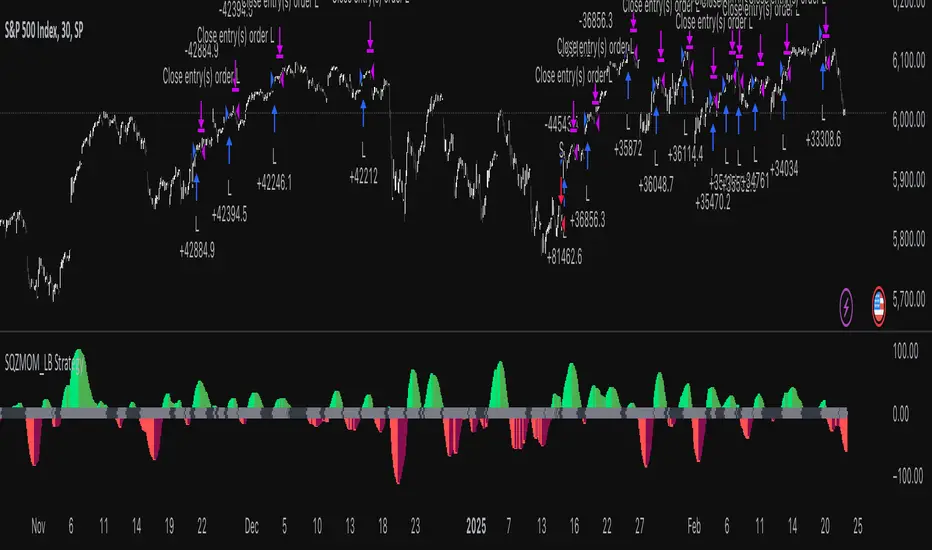

Squeeze Momentum Indicator Strategy [LazyBear + PineIndicators]The Squeeze Momentum Indicator Strategy (SQZMOM_LB Strategy) is an automated trading strategy based on the Squeeze Momentum Indicator developed by LazyBear, which itself is a modification of John Carter's "TTM Squeeze" concept from his book Mastering the Trade (Chapter 11). This strategy is designed to identify low-volatility phases in the market, which often precede explosive price movements, and to enter trades in the direction of the prevailing momentum.

Concept & Indicator Breakdown

The strategy employs a combination of Bollinger Bands (BB) and Keltner Channels (KC) to detect market squeezes:

Squeeze Condition:

When Bollinger Bands are inside the Keltner Channels (Black Crosses), volatility is low, signaling a potential upcoming price breakout.

When Bollinger Bands move outside Keltner Channels (Gray Crosses), the squeeze is released, indicating an expansion in volatility.

Momentum Calculation:

A linear regression-based momentum value is used instead of traditional momentum indicators.

The momentum histogram is color-coded to show strength and direction:

Lime/Green: Increasing bullish momentum

Red/Maroon: Increasing bearish momentum

Signal Colors:

Black: Market is in a squeeze (low volatility).

Gray: Squeeze is released, and volatility is expanding.

Blue: No squeeze condition is present.

Strategy Logic

The script uses historical volatility conditions and momentum trends to generate buy/sell signals and manage positions.

1. Entry Conditions

Long Position (Buy)

The squeeze just released (Gray Cross after Black Cross).

The momentum value is increasing and positive.

The momentum is at a local low compared to the past 100 bars.

The price is above the 100-period EMA.

The closing price is higher than the previous close.

Short Position (Sell)

The squeeze just released (Gray Cross after Black Cross).

The momentum value is decreasing and negative.

The momentum is at a local high compared to the past 100 bars.

The price is below the 100-period EMA.

The closing price is lower than the previous close.

2. Exit Conditions

Long Exit:

The momentum value starts decreasing (momentum lower than previous bar).

Short Exit:

The momentum value starts increasing (momentum higher than previous bar).

Position Sizing

Position size is dynamically adjusted based on 8% of strategy equity, divided by the current closing price, ensuring risk-adjusted trade sizes.

How to Use This Strategy

Apply on Suitable Markets:

Best for stocks, indices, and forex pairs with momentum-driven price action.

Works on multiple timeframes but is most effective on higher timeframes (1H, 4H, Daily).

Confirm Entries with Additional Indicators:

The author recommends ADX or WaveTrend to refine entries and avoid false signals.

Risk Management:

Since the strategy dynamically sizes positions, it's advised to use stop-losses or risk-based exits to avoid excessive drawdowns.

Final Thoughts

The Squeeze Momentum Indicator Strategy provides a systematic approach to trading volatility expansions, leveraging the classic TTM Squeeze principles with a unique linear regression-based momentum calculation. Originally inspired by John Carter’s method, LazyBear's version and this strategy offer a refined, adaptable tool for traders looking to capitalize on market momentum shifts.

BTCUSD Momentum After Abnormal DaysThis indicator identifies abnormal days in the Bitcoin market (BTCUSD) based on daily returns exceeding specific thresholds defined by a statistical approach. It is inspired by the findings of Caporale and Plastun (2020), who analyzed the cryptocurrency market's inefficiencies and identified exploitable patterns, particularly around abnormal returns.

Key Concept:

Abnormal Days:

Days where the daily return significantly deviates (positively or negatively) from the historical average.

Positive abnormal days: Returns exceed the mean return plus k times the standard deviation.

Negative abnormal days: Returns fall below the mean return minus k times the standard deviation.

Momentum Effect:

As described in the academic paper, on abnormal days, prices tend to move in the direction of the abnormal return until the end of the trading day, creating momentum effects. This can be leveraged by traders for profit opportunities.

How It Works:

Calculation:

The script calculates the daily return as the percentage difference between the open and close prices. It then derives the mean and standard deviation of returns over a configurable lookback period.

Thresholds:

The script dynamically computes upper and lower thresholds for abnormal days using the mean and standard deviation. Days exceeding these thresholds are flagged as abnormal.

Visualization:

The mean return and thresholds are plotted as dynamic lines.

Abnormal days are visually highlighted with transparent green (positive) or red (negative) backgrounds on the chart.

References:

This indicator is based on the methodology discussed in "Momentum Effects in the Cryptocurrency Market After One-Day Abnormal Returns" by Caporale and Plastun (2020). Their research demonstrates that hourly returns during abnormal days exhibit a strong momentum effect, moving in the same direction as the abnormal return. This behavior contradicts the efficient market hypothesis and suggests profitable trading opportunities.

"Prices tend to move in the direction of abnormal returns till the end of the day, which implies the existence of a momentum effect on that day giving rise to exploitable profit opportunities" (Caporale & Plastun, 2020).

The Most Powerful TQQQ EMA Crossover Trend Trading StrategyTQQQ EMA Crossover Strategy Indicator

Meta Title: TQQQ EMA Crossover Strategy - Enhance Your Trading with Effective Signals

Meta Description: Discover the TQQQ EMA Crossover Strategy, designed to optimize trading decisions with fast and slow EMA crossovers. Learn how to effectively use this powerful indicator for better trading results.

Key Features

The TQQQ EMA Crossover Strategy is a powerful trading tool that utilizes Exponential Moving Averages (EMAs) to identify potential entry and exit points in the market. Key features of this indicator include:

**Fast and Slow EMAs:** The strategy incorporates two EMAs, allowing traders to capture short-term trends while filtering out market noise.

**Entry and Exit Signals:** Automated signals for entering and exiting trades based on EMA crossovers, enhancing decision-making efficiency.

**Customizable Parameters:** Users can adjust the lengths of the EMAs, as well as take profit and stop loss multipliers, tailoring the strategy to their trading style.

**Visual Indicators:** Clear visual plots of the EMAs and exit points on the chart for easy interpretation.

How It Works