Out of the Noise Intraday Strategy with VWAP [YuL]This is my (naive) implementation of "Beat the Market An Effective Intraday Momentum Strategy for S&P500 ETF (SPY)" paper by Carlo Zarattini, Andrew Aziz, Andrea Barbon, so the credit goes to them.

It is supposed to run on SPY on 30-minute timeframe, there may be issues on other timeframes.

I've used settings that were used by the authors in the original paper to keep it close to the publication, but I understand that they are very aggressive and probably shouldn't be used like that.

Results are good, but not as good as they are stated in the paper (unsurprisingly?): returns are smaller and Sharpe is very low (which is actually weird given the returns and drawdown ratio), there are also margin calls if you enable margin check (and you should).

I have my own ideas of improvements which I will probably implement separately to keep this clean.

Cerca negli script per "momentum"

US30 Stealth StrategyOnly works on US30 (CAPITALCOM) 5 Minute chart

📈 Core Concept:

This is a trend-following strategy that captures strong market continuations by entering on:

The 3rd swing in the current trend,

Confirmed by a volume-verified engulfing candle,

With adaptive SL/TP and position sizing based on risk.

🧠 Entry Logic:

✅ Trend Filter

Uses a 50-period Simple Moving Average (SMA).

Buy only if price is above SMA → Uptrend

Sell only if price is below SMA → Downtrend

✅ Swing Count Logic

For buy: Wait for the 3rd higher low

For sell: Wait for the 3rd lower high

Uses a 5-bar lookback to detect highs/lows

This ensures you’re not buying early — but after trend is confirmed with structure.

✅ Engulfing Candle Confirmation

Bullish engulfing for buys

Bearish engulfing for sells

Candle must engulf previous bar completely (body logic)

✅ Volume Filter

Current candle volume must be greater than the 20-period volume average

Ensures trades only occur with institutional participation

✅ MA Slope Filter

Requires the slope of the 50 SMA over the last 3 candles to exceed 0.1

Avoids chop or flat trends

Adds momentum confirmation to the trade

✅ Session Filter (Time Filter)

Trades only executed between:

2:00 AM to 11:00 PM Oman Time (UTC+4)

Helps avoid overnight chop and illiquidity

📊 Position Sizing & Risk Management

✅ Smart SL (Adaptive Stop Loss)

SL is based on full size of the signal candle (including wick)

But if candle is larger than 25 points, SL is cut to half the size

This prevents oversized risk from long signals during volatile moves.

OBV ATR Strategy (OBV Breakout Channel) bas20230503ผมแก้ไขจาก OBV+SMA อันเดิม ของเดิม ดูที่เส้น SMA สองเส้นตัดกันมั่นห่วยแตกสำหรับที่ผมลองเทรดจริง และหลักการเบรค ได้แรงบันดาลใจ ATR จาก เทพคอย ที่ใช้กับราคา แต่นี้ใช้กับ OBV แทน

และผมใช้เจมินี้ เพื่อแก้ ให้ เป็น strategy เพื่อเช็คย้อนหลังได้ง่ายกว่าเดิม

หลักการง่ายคือถ้ามันขึ้น มันจะขึ้นเรื่อยๆ

เขียน แบบสุภาพ (น่าจะอ่านได้ง่ายกว่าผมเขียน)

สคริปต์นี้ได้รับการพัฒนาต่อยอดจากแนวคิด OBV+SMA Crossover แบบดั้งเดิม ซึ่งจากการทดสอบส่วนตัวพบว่าประสิทธิภาพยังไม่น่าพอใจ กลยุทธ์ใหม่นี้จึงเปลี่ยนมาใช้หลักการ "Breakout" ซึ่งได้รับแรงบันดาลใจมาจากการใช้ ATR สร้างกรอบของราคา แต่เราได้นำมาประยุกต์ใช้กับ On-Balance Volume (OBV) แทน นอกจากนี้ สคริปต์ได้ถูกแปลงเป็น Strategy เต็มรูปแบบ (โดยความช่วยเหลือจาก Gemini AI) เพื่อให้สามารถทดสอบย้อนหลัง (Backtest) และประเมินประสิทธิภาพได้อย่างแม่นยำ

หลักการของกลยุทธ์: กลยุทธ์นี้ทำงานบนแนวคิดโมเมนตัมที่ว่า "เมื่อแนวโน้มได้เกิดขึ้นแล้ว มีโอกาสที่มันจะดำเนินต่อไป" โดยจะมองหาการทะลุของพลังซื้อ-ขาย (OBV) ที่แข็งแกร่งเป็นพิเศษเป็นสัญญาณเข้าเทร

----

สคริปต์นี้เป็นกลยุทธ์ (Strategy) ที่ใช้ On-Balance Volume (OBV) ซึ่งเป็นอินดิเคเตอร์ที่วัดแรงซื้อและแรงขายสะสม แทนที่จะใช้การตัดกันของเส้นค่าเฉลี่ย (SMA Crossover) ที่เป็นแบบพื้นฐาน กลยุทธ์นี้จะมองหาการ "ทะลุ" (Breakout) ของพลัง OBV ออกจากกรอบสูงสุด-ต่ำสุดของตัวเองในรอบที่ผ่านมา

สัญญาณกระทิง (Bull Signal): เกิดขึ้นเมื่อพลังการซื้อ (OBV) แข็งแกร่งจนสามารถทะลุจุดสูงสุดของตัวเองในอดีตได้ บ่งบอกถึงโอกาสที่แนวโน้มจะเปลี่ยนเป็นขาขึ้น

สัญญาณหมี (Bear Signal): เกิดขึ้นเมื่อพลังการขาย (OBV) รุนแรงจนสามารถกดดันให้ OBV ทะลุจุดต่ำสุดของตัวเองในอดีตได้ บ่งบอกถึงโอกาสที่แนวโน้มจะเปลี่ยนเป็นขาลง

ส่วนประกอบบนกราฟ (Indicator Components)

เส้น OBV

เส้นหลัก ที่เปลี่ยนเขียวเป็นแดง เป็นทั้งแนวรับและแนวต้าน และ จุด stop loss

เส้นนี้คือหัวใจของอินดิเคเตอร์ ที่แสดงถึงพลังสะสมของ Volume

เมื่อเส้นเป็นสีเขียว (แนวรับ): จะปรากฏขึ้นเมื่อกลยุทธ์เข้าสู่ "โหมดกระทิง" เส้นนี้คือระดับต่ำสุดของ OBV ในอดีต และทำหน้าที่เป็นแนวรับไดนามิก

เมื่อเส้นกลายเป็นสีแดงสีแดง (แนวต้าน): จะปรากฏขึ้นเมื่อกลยุทธ์เข้าสู่ "โหมดหมี" เส้นนี้คือระดับสูงสุดของ OBV ในอดีต และทำหน้าที่เป็นแนวต้านไดนามิก

สัญลักษณ์สัญญาณ (Signal Markers):

Bull 🔼 (สามเหลี่ยมขึ้นสีเขียว): คือสัญญาณ "เข้าซื้อ" (Long) จะปรากฏขึ้น ณ จุดที่ OBV ทะลุขึ้นไปเหนือกรอบด้านบนเป็นครั้งแรก

Bear 🔽 (สามเหลี่ยมลงสีแดง): คือสัญญาณ "เข้าขาย" (Short) จะปรากฏขึ้น ณ จุดที่ OBV ทะลุลงไปต่ำกว่ากรอบด้านล่างเป็นครั้งแรก

วิธีการใช้งาน (How to Use)

เพิ่มสคริปต์นี้ลงบนกราฟราคาที่คุณสนใจ

ไปที่แท็บ "Strategy Tester" ด้านล่างของ TradingView เพื่อดูผลการทดสอบย้อนหลัง (Backtest) ของกลยุทธ์บนสินทรัพย์และไทม์เฟรมต่างๆ

ใช้สัญลักษณ์ "Bull" และ "Bear" เป็นตัวช่วยในการตัดสินใจเข้าเทรด

ข้อควรจำ: ไม่มีกลยุทธ์ใดที่สมบูรณ์แบบ 100% ควรใช้สคริปต์นี้ร่วมกับการวิเคราะห์ปัจจัยอื่นๆ เช่น โครงสร้างราคา, แนวรับ-แนวต้านของราคา และการบริหารความเสี่ยง (Risk Management) ของตัวคุณเองเสมอ

การตั้งค่า (Inputs)

SMA Length 1 / SMA Length 2: ใช้สำหรับพล็อตเส้นค่าเฉลี่ยของ OBV เพื่อดูเป็นภาพอ้างอิง ไม่มีผลต่อตรรกะการเข้า-ออกของ Strategy อันใหม่ แต่มันเป็นของเก่า ถ้าชอบ ก็ใช้ได้ เมื่อ SMA สองเส้นตัดกัน หรือตัดกับเส้น OBV

High/Low Lookback Length: (ค่าพื้นฐาน30/แก้ตรงนี้ให้เหมาะสมกับ coin หรือหุ้น ตามความผันผวน ) คือระยะเวลาที่ใช้ในการคำนวณกรอบสูงสุด-ต่ำสุดของ OBV

ค่าน้อย: ทำให้กรอบแคบลง สัญญาณจะเกิดไวและบ่อยขึ้น แต่อาจมีสัญญาณหลอก (False Signal) เยอะขึ้น

ค่ามาก: ทำให้กรอบกว้างขึ้น สัญญาณจะเกิดช้าลงและน้อยลง แต่มีแนวโน้มที่จะเป็นสัญญาณที่แข็งแกร่งกว่า

แน่นอนครับ นี่คือคำแปลฉบับภาษาอังกฤษที่สรุปใจความสำคัญ กระชับ และสุภาพ เหมาะสำหรับนำไปใช้ในคำอธิบายสคริปต์ (Description) ของ TradingView ครับ

---Translate to English---

OBV Breakout Channel Strategy

This script is an evolution of a traditional OBV+SMA Crossover concept. Through personal testing, the original crossover method was found to have unsatisfactory performance. This new strategy, therefore, uses a "Breakout" principle. The inspiration comes from using ATR to create price channels, but this concept has been adapted and applied to On-Balance Volume (OBV) instead.

Furthermore, the script has been converted into a full Strategy (with assistance from Gemini AI) to enable precise backtesting and performance evaluation.

The strategy's core principle is momentum-based: "once a trend is established, it is likely to continue." It seeks to enter trades on exceptionally strong breakouts of buying or selling pressure as measured by OBV.

Core Concept

This is a Strategy that uses On-Balance Volume (OBV), an indicator that measures cumulative buying and selling pressure. Instead of relying on a basic Simple Moving Average (SMA) Crossover, this strategy identifies a "Breakout" of the OBV from its own highest-high and lowest-low channel over a recent period.

Bull Signal: Occurs when the buying pressure (OBV) is strong enough to break above its own recent highest high, indicating a potential shift to an upward trend.

Bear Signal: Occurs when the selling pressure (OBV) is intense enough to push the OBV below its own recent lowest low, indicating a potential shift to a downward trend.

On-Screen Components

1. OBV Line

This is the main indicator line, representing the cumulative volume. Its color changes to green when OBV is rising and red when it is falling.

2. Dynamic Support & Resistance Line

This is the thick Green or Red line that appears based on the strategy's current "mode." This line serves as a dynamic support/resistance level and can be used as a reference for stop-loss placement.

Green Line (Support): Appears when the strategy enters "Bull Mode." This line represents the lowest low of the OBV in the recent past and acts as dynamic support.

Red Line (Resistance): Appears when the strategy enters "Bear Mode." This line represents the highest high of the OBV in the recent past and acts as dynamic resistance.

3. Signal Markers

Bull 🔼 (Green Up Triangle): This is the "Long Entry" signal. It appears at the moment the OBV first breaks out above its high-low channel.

Bear 🔽 (Red Down Triangle): This is the "Short Entry" signal. It appears at the moment the OBV first breaks down below its high-low channel.

How to Use

Add this script to the price chart of your choice.

Navigate to the "Strategy Tester" panel at the bottom of TradingView to view the backtesting results for the strategy on different assets and timeframes.

Use the "Bull" and "Bear" signals as aids in your trading decisions.

Disclaimer: No strategy is 100% perfect. This script should always be used in conjunction with other forms of analysis, such as price structure, key price-based support/resistance levels, and your own personal risk management rules.

Inputs

SMA Length 1 / SMA Length 2: These are used to plot moving averages on the OBV for visual reference. They are part of the legacy logic and do not affect the new breakout strategy. However, they are kept for traders who may wish to observe their crossovers for additional confirmation.

High/Low Lookback Length: (Most Important Setting) This determines the period used to calculate the highest-high and lowest-low OBV channel. (Default is 30; adjust this to suit the asset's volatility).

A smaller value: Creates a narrower channel, leading to more frequent and faster signals, but potentially more false signals.

A larger value: Creates a wider channel, leading to fewer and slower signals, which are likely to be more significant.

Long-Leg Doji Breakout StrategyThe Long-Leg Doji Breakout Strategy is a sophisticated technical analysis approach that capitalizes on market psychology and price action patterns.

Core Concept: The strategy identifies Long-Leg Doji candlestick patterns, which represent periods of extreme market indecision where buyers and sellers are in equilibrium. These patterns often precede significant price movements as the market resolves this indecision.

Pattern Recognition: The algorithm uses strict mathematical criteria to identify authentic Long-Leg Doji patterns. It requires the candle body to be extremely small (≤0.1% of the total range) while having long wicks on both sides (at least 2x the body size). An ATR filter ensures the pattern is significant relative to recent volatility.

Trading Logic: Once a Long-Leg Doji is identified, the strategy enters a "waiting mode," monitoring for a breakout above the doji's high (long signal) or below its low (short signal). This confirmation approach reduces false signals by ensuring the market has chosen a direction.

Risk Management: The strategy allocates 10% of equity per trade and uses a simple moving average crossover for exits. Visual indicators help traders understand the pattern identification and trade execution process.

Psychological Foundation: The strategy exploits the natural market cycle where uncertainty (represented by the doji) gives way to conviction (the breakout), creating high-probability trading opportunities.

The strength of this approach lies in its ability to identify moments when market sentiment shifts from confusion to clarity, providing traders with well-defined entry and exit points while maintaining proper risk management protocols.

How It Works

The strategy operates on a simple yet powerful principle: identify periods of market indecision, then trade the subsequent breakout when the market chooses direction.

Step 1: Pattern Detection

The algorithm scans for Long-Leg Doji candles, which have three key characteristics:

Tiny body (open and close prices nearly equal)

Long upper wick (significant rejection of higher prices)

Long lower wick (significant rejection of lower prices)

Step 2: Confirmation Wait

Once a doji is detected, the strategy doesn't immediately trade. Instead, it marks the high and low of that candle and waits for a definitive breakout.

Step 3: Trade Execution

Long Entry: When price closes above the doji's high

Short Entry: When price closes below the doji's low

Step 4: Exit Strategy

Positions are closed when price crosses back through a 20-period moving average, indicating potential trend reversal.

Market Psychology Behind It

A Long-Leg Doji represents a battlefield between bulls and bears that ends in a stalemate. The long wicks show that both sides tried to push price in their favor but failed. This creates a coiled spring effect - when one side finally gains control, the move can be explosive as trapped traders rush to exit and momentum traders jump aboard.

Key Parameters

Doji Body Threshold (0.1%): Ensures the body is truly small relative to the candle's range

Wick Ratio (2.0): Both wicks must be at least twice the body size

ATR Filter: Uses Average True Range to ensure the pattern is significant in current market conditions

Position Size: 10% of equity per trade for balanced risk management

Pros:

High Probability Setups: Doji patterns at key levels often lead to significant moves as they represent genuine shifts in market sentiment.

Clear Rules: Objective criteria for entry and exit eliminate emotional decision-making and provide consistent execution.

Risk Management: Built-in position sizing and exit rules help protect capital during losing trades.

Market Neutral: Works equally well for long and short positions, adapting to market direction rather than fighting it.

Visual Confirmation: The strategy provides clear visual cues, making it easy to understand when patterns are forming and trades are triggered.

Cons:

False Breakouts: In choppy or ranging markets, price may break the doji levels only to quickly reverse, creating whipsaws.

Patience Required: Traders must wait for both pattern formation and breakout confirmation, which can test discipline during active market periods.

Simple Exit Logic: The moving average exit may be too simplistic, potentially cutting profits short during strong trends or holding losers too long during reversals.

Volatility Dependent: The strategy relies on sufficient volatility to create meaningful doji patterns - it may underperform in extremely quiet markets.

Lagging Entries: Waiting for breakout confirmation means missing the very beginning of moves, reducing potential profit margins.

Best Market Conditions

The strategy performs optimally during periods of moderate volatility when markets are making genuine directional decisions rather than just random noise. It works particularly well around key support/resistance levels where the market's indecision is most meaningful.

Optimization Considerations

Consider combining with additional confluence factors like volume analysis, support/resistance levels, or other technical indicators to improve signal quality. The exit strategy could also be enhanced with trailing stops or multiple profit targets to better capture extended moves while protecting gains.

Best for Index option,

Enjoy !!

AutoFib Breakout Strategy for Uptrend AssetsThis trading strategy is designed to help you catch powerful upward moves on assets that are in a long-term uptrend, such as Gold (XAUUSD). It uses a popular technical tool called the Fibonacci Extension, combined with a trend filter and a risk-managed exit system.

✅ When to Use This Strategy

• Works best on higher timeframes: Daily (1D), 3-Day (3D), or Weekly (W).

• Best used on uptrending assets like Gold.

• Designed for swing trading – holding trades from a few days to weeks.

📊 How It Works

1. Find the Trend

We only want to trade in the direction of the trend.

• The strategy uses the 200-period EMA (Exponential Moving Average) to identify if the market is in an uptrend.

• If the price is above the 200 EMA, we consider it an uptrend and allow long trades.

2. Identify Breakout Levels

• The strategy detects recent high and low pivot points to draw Fibonacci extension levels.

• It focuses on the 1.618 Fibonacci level, which is often a target in strong trends.

• When the price breaks above this level in an uptrend, it signals a potential momentum breakout – a good time to buy.

3. Enter a Trade

• The strategy enters a long (buy) position when the price closes above the 1.618 Fibonacci level and the market is in an uptrend (above the 200 EMA).

4. Manage Risk Automatically

• The trade includes a stop-loss set to 1x the ATR (Average True Range) below the entry price – this protects against sudden drops.

• It sets a take-profit at 3x the ATR above the entry – aiming for higher rewards than risks.

⚠️ Important Notes

• 📈 Higher Timeframes Preferred: This strategy works best on Daily (D), 3-Day (3D), and Weekly (W) charts, especially on Gold (XAUUSD).

• 🧪 Not for Deep Backtesting: Due to the nature of how pivot points and Fib levels are calculated, this strategy may not perform well in backtesting simulations (because the historical calculations can shift). It is better used for live analysis and forward testing.

Strategy Builder With IndicatorsThis strategy script is designed for traders who enjoy building systems using multiple indicators.

Please note: This script does not include any built-in indicators. Instead, it works by referencing the plot outputs of the indicators you’ve already added to your chart.

For example, if you add a MACD and an ATR indicator to your chart, you can assign their plot values as inputs in the settings panel of this strategy.

• MACD as a trigger

• ATR as a filter

How Filters Work

Filters check whether certain conditions are met before a trade can be opened. For instance, if you set a filter like ATR > 30, then no trade will be executed unless that condition is true — even if the trigger fires.

All filters are linked, meaning every active filter must be satisfied for a trade to occur.

How Triggers Work

Triggers are what actually fire a trade signal — such as a moving average crossover or RSI breaking above a specific level. Unlike filters, triggers are independent. Only one active trigger needs to be true for the trade to execute.

Thanks to its modular structure, this strategy can be used with any indicator of your choice.

⸻

Risk Management Features

In the settings, you’ll find flexible options for:

• Stop Loss (SL)

• Trailing Stop Loss (TSL)

• Multi Take-Profit (TP)

These features enhance trade safety and let you tailor your risk management.

SL types available:

• Tick-based SL

• Percent-based SL

• ATR-based SL

Once you select your preferred SL type, you can fine-tune its distance using the offset field.

Trailing SL allows your stop to follow price as it moves in your favor — helping to lock in profits.

Multi-TP lets you take profits at two different levels, helping you secure gains while leaving room for extended moves.

Breakeven option is also available to automatically move your SL to entry after reaching a profit threshold.

⸻

How to Build a Solid Strategy

Let’s break down a good setup into three key components:

1. Trend Filter

Avoid trading against the trend — that’s like swimming against the current.

Use a filter like:

• Supertrend

• Momentum indicators

• Candlestick bias, etc.

Example: In this case, I used Supertrend and filtered for trades only if the price is above the uptrend line.

2. Trigger Condition

Once we confirm the trend is on our side, we need a trigger to execute at the right moment. This can be:

• RSI cross

• Candlestick patterns

• Trendline breaks

• Moving average crossovers, etc.

Example: I used RSI crossing above 50 as the entry trigger.

3. Risk Management

Even in the right trend at the right time — anything can happen. That’s why you should always define Stop Loss and Take Profit levels.

⸻

And there you have it! Your strategy is ready to backtest, refine, and deploy with alerts for live trading.

Questions or suggestions? Feel free to reach out

Three Candle Bullish Engulfing StrategyThe Three Candle Bullish Engulfing Strategy is a versatile, multi-mode trading system designed for TradingView, combining classic candlestick patterns with momentum confirmation and dynamic risk management. This script supports both swing trading and intraday approaches, as well as an optional RSI-based breakout mode for additional signal filtering.

Key Features:

Three Candle Pattern Detection:

The strategy identifies potential trend reversal points using a three-candle pattern:

The first candle is a strong bullish (or bearish) move.

The second candle is a doji or small-bodied candle, indicating indecision.

The third candle is a bullish (or bearish) engulfing candle that closes above (or below) the previous high (or low), confirming the reversal.

Flexible Trading Modes:

Swing Long Only: Enter long trades on bullish three-candle setups.

Intraday Long & Short: Trade both long and short based on bullish and bearish three-candle patterns, with automatic session-end exits.

RSI Breakout Mode: Enter long trades when the 1-hour RSI exceeds a user-defined threshold (default 80) and a bullish candle forms, with breakout confirmation and a fixed-percentage stop loss.

Visual Aids:

Plots the RSI breakout trigger price and stop loss on the chart for easy monitoring.

How It Works:

Three Candle Pattern Entries:

Long Entry: Triggered when a bullish candle is followed by a doji, then a bullish engulfing candle closes above the previous high.

Short Entry (Intraday only): Triggered by the inverse pattern—bearish candle, doji, then bearish engulfing candle closing below the previous low.

RSI Breakout Entries:

When the RSI on a higher timeframe (default 1 hour) exceeds the set threshold and a bullish candle forms, the script records a trigger price.

A long trade is entered if the price breaks above this trigger, with a stop loss set a fixed percentage below.

Exits:

Positions are closed if the trailing stop is hit, the session ends (for intraday mode), or the stop loss is triggered in RSI breakout mode.

In RSI breakout mode, positions are also closed if a new breakout trigger forms while in position.

Multi-Indicator Trend-Following Strategy v6Multi-Indicator Trend-Following Strategy v6

This strategy uses a combination of technical indicators to identify potential trend-following trade entries and exits. It is intended for educational and research purposes.

How it works:

Moving Averages (EMA): Entry signals are generated on crossovers between a fast and slow exponential moving average.

RSI Filter: Confirms momentum with a threshold above/below 50 for long/short entries.

Volume Confirmation: Requires volume to exceed a moving average multiplied by a user-defined factor.

ATR-Based Risk Management: Stop loss and take profit levels are calculated using the Average True Range (ATR), allowing for dynamic risk control based on market volatility.

Customizable Inputs:

Fast/Slow MA lengths

RSI length and levels

MACD settings (used in calculation, not directly in signal)

Volume MA and multiplier

ATR period and multipliers for stop loss and take profit

Notes:

This strategy does not guarantee future results.

It is provided for analysis and backtesting only.

Alerts are available for buy/sell conditions.

Feel free to adjust parameters to explore different market conditions and asset classes.

NY Opening Range Breakout - MA StopCore Concept

This strategy trades breakouts from the New York opening range (9:30-9:45 AM NY time) on intraday timeframes, designed for scalping and day trading.

Setup Requirements

Timeframe: Works on any timeframe under 15 minutes (1m, 2m, 3m, 5m, 10m)

Session: New York market hours

Range Period: 9:30-9:45 AM NY time (15-minute opening range)

Entry Rules

Long Entries:

Wait for a candle to close above the opening range high

Enter long on the next candle (before 12:00 PM NY time)

Must be above moving average if using MA-based take profit

Short Entries:

Wait for a candle to close below the opening range low

Enter short on the next candle (before 12:00 PM NY time)

Must be below moving average if using MA-based take profit

Risk Management

Stop Loss:

Long trades: Opening range low

Short trades: Opening range high

Take Profit Options:

Fixed Risk Reward: 1.5x the range size (customizable ratio)

Moving Average: Exit when price crosses back through MA

Both: Whichever comes first

Key Features

Trade Direction Options:

Long Only

Short Only

Both directions

Moving Average Filter:

Prevents entries that would immediately hit stop loss

Uses EMA/SMA/WMA/VWMA with customizable length

Acts as dynamic support/resistance

Time Restrictions:

No entries after 12:00 PM NY time (customizable cutoff)

One trade per direction per day

Daily reset of all variables

Visual Elements

Red/green lines showing opening range

Purple line for moving average

Entry and breakout signals with shapes

Take profit and stop loss levels plotted

Information table with current status

Strategy Logic Flow

Morning: Capture 9:30-9:45 range high/low

Wait: Monitor for breakout (previous candle close outside range)

Filter: Check MA condition if using MA-based exits

Enter: Trade on next candle after breakout

Manage: Exit at fixed TP, MA cross, or stop loss

Reset: Start fresh next trading day

This is a momentum-based breakout strategy that capitalizes on early market volatility while using the opening range as natural support/resistance levels.

magic wand STSM"Magic Wand STSM" Strategy: Trend-Following with Dynamic Risk Management

Overview:

The "Magic Wand STSM" (Supertrend & SMA Momentum) is an automated trading strategy designed to identify and capitalize on sustained trends in the market. It combines a multi-timeframe Supertrend for trend direction and potential reversal signals, along with a 200-period Simple Moving Average (SMA) for overall market bias. A key feature of this strategy is its dynamic position sizing based on a user-defined risk percentage per trade, and a built-in daily and monthly profit/loss tracking system to manage overall exposure and prevent overtrading.

How it Works (Underlying Concepts):

Multi-Timeframe Trend Confirmation (Supertrend):

The strategy uses two Supertrend indicators: one on the current chart timeframe and another on a higher timeframe (e.g., if your chart is 5-minute, the higher timeframe Supertrend might be 15-minute).

Trend Identification: The Supertrend's direction output is crucial. A negative direction indicates a bearish trend (price below Supertrend), while a positive direction indicates a bullish trend (price above Supertrend).

Confirmation: A core principle is that trades are only considered when the Supertrend on both the current and the higher timeframe align in the same direction. This helps to filter out noise and focus on stronger, more confirmed trends. For example, for a long trade, both Supertrends must be indicating a bearish trend (price below Supertrend line, implying an uptrend context where price is expected to stay above/rebound from Supertrend). Similarly, for short trades, both must be indicating a bullish trend (price above Supertrend line, implying a downtrend context where price is expected to stay below/retest Supertrend).

Trend "Readiness": The strategy specifically looks for situations where the Supertrend has been stable for a few bars (checking barssince the last direction change).

Long-Term Market Bias (200 SMA):

A 200-period Simple Moving Average is plotted on the chart.

Filter: For long trades, the price must be above the 200 SMA, confirming an overall bullish bias. For short trades, the price must be below the 200 SMA, confirming an overall bearish bias. This acts as a macro filter, ensuring trades are taken in alignment with the broader market direction.

"Lowest/Highest Value" Pullback Entries:

The strategy employs custom functions (LowestValueAndBar, HighestValueAndBar) to identify specific price action within the recent trend:

For Long Entries: It looks for a "buy ready" condition where the price has found a recent lowest point within a specific number of bars since the Supertrend turned bearish (indicating an uptrend). This suggests a potential pullback or consolidation before continuation. The entry trigger is a close above the open of this identified lowest bar, and also above the current bar's open.

For Short Entries: It looks for a "sell ready" condition where the price has found a recent highest point within a specific number of bars since the Supertrend turned bullish (indicating a downtrend). This suggests a potential rally or consolidation before continuation downwards. The entry trigger is a close below the open of this identified highest bar, and also below the current bar's open.

Candle Confirmation: The strategy also incorporates a check on the candle type at the "lowest/highest value" bar (e.g., closevalue_b < openvalue_b for buy signals, meaning a bearish candle at the low, suggesting a potential reversal before a buy).

Risk Management and Position Sizing:

Dynamic Lot Sizing: The lotsvalue function calculates the appropriate position size based on your Your Equity input, the Risk to Reward ratio, and your risk percentage for your balance % input. This ensures that the capital risked per trade remains consistent as a percentage of your equity, regardless of the instrument's volatility or price. The stop loss distance is directly used in this calculation.

Fixed Risk Reward: All trades are entered with a predefined Risk to Reward ratio (default 2.0). This means for every unit of risk (stop loss distance), the target profit is rr times that distance.

Daily and Monthly Performance Monitoring:

The strategy tracks todaysWins, todaysLosses, and res (daily net result) in real-time.

A "daily profit target" is implemented (day_profit): If the daily net result is very favorable (e.g., res >= 4 with todaysLosses >= 2 or todaysWins + todaysLosses >= 8), the strategy may temporarily halt trading for the remainder of the session to "lock in" profits and prevent overtrading during volatile periods.

A "monthly stop-out" (monthly_trade) is implemented: If the lres (overall net result from all closed trades) falls below a certain threshold (e.g., -12), the strategy will stop trading for a set period (one week in this case) to protect capital during prolonged drawdowns.

Trade Execution:

Entry Triggers: Trades are entered when all buy/sell conditions (Supertrend alignment, SMA filter, "buy/sell situation" candle confirmation, and risk management checks) are met, and there are no open positions.

Stop Loss and Take Profit:

Stop Loss: The stop loss is dynamically placed at the upTrendValue for long trades and downTrendValue for short trades. These values are derived from the Supertrend indicator, which naturally adjusts to market volatility.

Take Profit: The take profit is calculated based on the entry price, the stop loss, and the Risk to Reward ratio (rr).

Position Locks: lock_long and lock_short variables prevent immediate re-entry into the same direction once a trade is initiated, or after a trend reversal based on Supertrend changes.

Visual Elements:

The 200 SMA is plotted in yellow.

Entry, Stop Loss, and Take Profit lines are plotted in white, red, and green respectively when a trade is active, with shaded areas between them to visually represent risk and reward.

Diamond shapes are plotted at the bottom of the chart (green for potential buy signals, red for potential sell signals) to visually indicate when the buy_sit or sell_sit conditions are met, along with other key filters.

A comprehensive trade statistics table is displayed on the chart, showing daily wins/losses, daily profit, total deals, and overall profit/loss.

A background color indicates the active trading session.

Ideal Usage:

This strategy is best applied to instruments with clear trends and sufficient liquidity. Users should carefully adjust the Your Equity, Risk to Reward, and risk percentage inputs to align with their individual risk tolerance and capital. Experimentation with different ATR Length and Factor values for the Supertrend might be beneficial depending on the asset and timeframe.

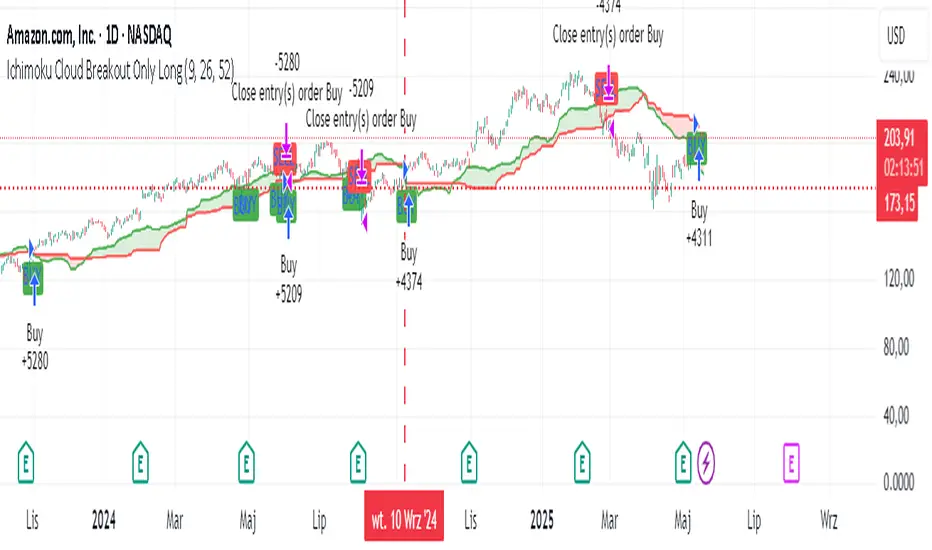

Ichimoku Cloud Breakout Only LongThis is a very simple trading strategy based exclusively on the Ichimoku Cloud. There are no additional indicators or complex rules involved. The key condition is that we only open long positions when the price is clearly above the cloud — indicating a bullish trend.

For optimal results, the recommended timeframes are 1D (daily) or 1W (weekly) charts. These higher timeframes help filter out market noise and provide more reliable trend signals.

We do not short the market under any circumstances. The focus is purely on riding upward momentum when the price breaks out or stays above the cloud.

This strategy works best when applied to growth stocks with strong upward trends and good fundamentals — such as Google (GOOGL), Tesla (TSLA), Apple (AAPL), or NVIDIA (NVDA).

Supertrade's RVI Long-Only Strategy with SL/TP (RR 1:3)This strategy, titled "Supertrade’s RVI Long-Only Strategy with SL/TP (RR 1:3)", is designed to capitalize on potential bullish reversals using the Relative Vigor Index (RVI) as its core signal generator. It is best optimized for trading XAUUSD on the 15-minute timeframe , where it has demonstrated favorable historical performance.

The RVI is calculated using a 10-period standard deviation of the closing price, with smoothing applied through a 14-period exponential moving average. This approach helps to distinguish between uptrend and downtrend volatility, allowing the strategy to identify momentum shifts with precision. A long position is triggered when the RVI crosses above the 20 level, suggesting a potential transition from a weak to a stronger bullish phase.

Risk management is embedded through a user-defined stop-loss (default set at 1% below the entry price) and a fixed reward-to-risk ratio of 1:3. This means that for every 1% of capital risked, the strategy targets a 3% gain, maintaining favorable risk-reward dynamics throughout its execution. Once a position is entered, it will exit automatically at either the stop-loss or take-profit level, depending on which is reached first.

This strategy is meant for educational and research purposes only. While it has performed well historically on specific assets and timeframes, past performance is not indicative of future results . Market conditions can change, and no strategy guarantees success in all environments. Please exercise proper risk management and test thoroughly before applying in live markets.

Hybrid: RSI + Breakout + DashboardHybrid RSI + Breakout Strategy

Adaptive trading system that switches modes based on market regime:

Ranging: Buys when RSI < 30 and sells when RSI > 70.

Trending: Enters momentum breakouts only in the direction of the 200-EMA bias, with ADX confirming trend strength.

Risk Management: Trailing stop locks profits and caps drawdown.

Optimized for BTC, ETH, and SOL on 1 h–1 D charts; back-tested from 2017 onward. Educational use only—run your own tests before deploying live funds.

Timeframe StrategyThis is a multi-timeframe trading strategy inspired by Ross Cameron's style, optimized for scalping and trend-following across various timeframes (1m, 5m, 15m, 1h, and 1D). The strategy integrates a comprehensive set of technical indicators, dynamic risk management, and visual tools.

Core Features

Dynamic Take Profit, Stop Loss & Trailing Stop

> Separate settings per timeframe for:

-TP% (Take Profit)

-SL% (Stop Loss)

-Trailing Stop %

-Cooldown bars

> Configurable via UI inputs.

>Smart Entry Conditions

Bullish entry: EMA9 crossover EMA20 and EMA50 > EMA200

Bearish entry: EMA9 crossunder EMA20 and EMA50 < EMA200

>Additional confirmation filters:

-Volume Filter (enabled/disabled via UI)

-Time Filter (e.g., only between 15:00–20:00 UTC)

-Spike Filter: rejects high-volatility candles

-RSI Filter: above/below 50 for trend confirmation

-ADX Filter (only applied on 1m, e.g., ADX > 15)

-Micro-Volatility Filter: minimum range percentage (1m only)

-Trend Filter (1m only): price must be above/below EMA200

>Trailing Stop Logic

-Configurable for each timeframe.

- Optional via toggle (use_trailing).

>Trade Cooldown Logic

-Prevents consecutive trades within X bars, configurable per timeframe.

>Technical Indicators Used

-EMA 9 / 20 / 50 / 200

-VWAP

-RSI (14)

-ATR (14) for volatility-based spike filtering

-Custom-calculated ADX (14) (manually implemented)

>Visual Elements

🔼/🔽 Entry signals (long/short) plotted on the chart.

📉 Table in bottom-left:

Displays current values of EMA/VWAP/volume/ATR/ADX.

> Optional "Tab info" panel in top-right (toggleable):

-Timeframe & strategy settings

-Live status of filters (volume, time, cooldown, spike, RSI, ADX, range, trend)

-Uses emoji (✅ / ❌) for quick diagnostics.

>User Customization

-Inputs per timeframe for all key parameters.

-Toggle switches for:

-Trailing stop

-Volume filter

-Info table visibility

This strategy is designed for active traders seeking a balance between momentum entry, risk control, and adaptability across timeframes. It's ideal for backtesting quick reversals or breakout setups in fast markets, especially at lower timeframes like 1m or 5m.

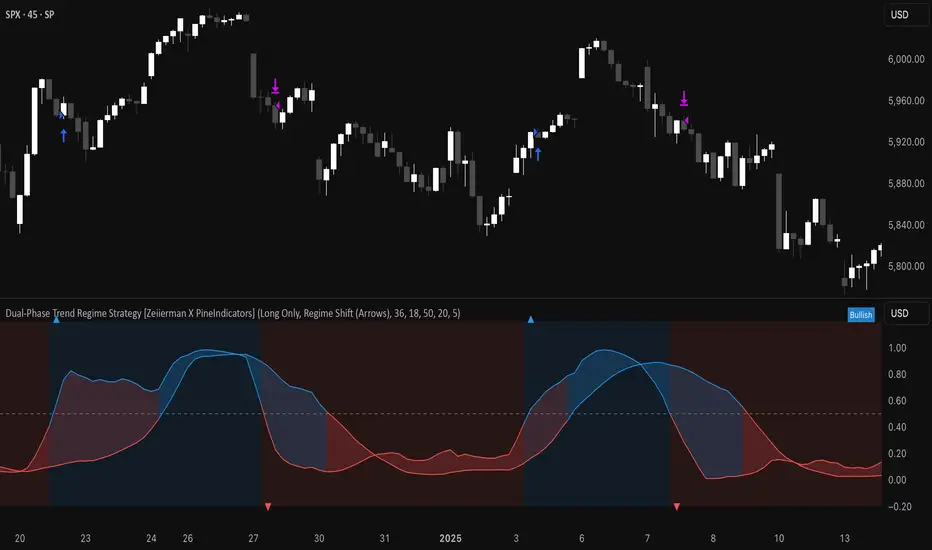

Dual-Phase Trend Regime Strategy [Zeiierman X PineIndicators]This strategy is based on the Dual-Phase Trend Regime Indicator by Zeiierman.

Full credit for the original concept and logic goes to Zeiierman.

This non-repainting strategy dynamically switches between fast and slow oscillators based on market volatility, providing adaptive entries and exits with high clarity and reliability.

Core Concepts

1. Adaptive Dual Oscillator Logic

The system uses two oscillators:

Fast Oscillator: Activated in high-volatility phases for quick reaction.

Slow Oscillator: Used during low-volatility phases to reduce noise.

The system automatically selects the appropriate oscillator depending on the market's volatility regime.

2. Volatility Regime Detection

Volatility is calculated using the standard deviation of returns. A median-split algorithm clusters volatility into:

Low Volatility Cluster

High Volatility Cluster

The current volatility is then compared to these clusters to determine whether the regime is low or high volatility.

3. Trend Regime Identification

Based on the active oscillator:

Bullish Trend: Oscillator > 0.5

Bearish Trend: Oscillator < 0.5

Neutral Trend: Oscillator = 0.5

The strategy reacts to changes in this trend regime.

4. Signal Source Options

You can choose between:

Regime Shift (Arrows): Trade based on oscillator value changes (from bullish to bearish and vice versa).

Oscillator Cross: Trade based on crossovers between the fast and slow oscillators.

Trade Logic

Trade Direction Options

Long Only

Short Only

Long & Short

Entry Conditions

Long Entry: Triggered on bullish regime shift or fast crossing above slow.

Short Entry: Triggered on bearish regime shift or fast crossing below slow.

Exit Conditions

Long Exit: Triggered on bearish shift or fast crossing below slow.

Short Exit: Triggered on bullish shift or fast crossing above slow.

The strategy closes opposing positions before opening new ones.

Visual Features

Oscillator Bands: Plots fast and slow oscillators, colored by trend.

Background Highlight: Indicates current trend regime.

Signal Markers: Triangle shapes show bullish/bearish shifts.

Dashboard Table: Displays live trend status ("Bullish", "Bearish", "Neutral") in the chart’s corner.

Inputs & Customization

Oscillator Periods – Fast and slow lengths.

Refit Interval – How often volatility clusters update.

Volatility Lookback & Smoothing

Color Settings – Choose your own bullish/bearish colors.

Signal Mode – Regime shift or oscillator crossover.

Trade Direction Mode

Use Cases

Swing Trading: Take entries based on adaptive regime shifts.

Trend Following: Follow the active trend using filtered oscillator logic.

Volatility-Responsive Systems: Adjust your trade behavior depending on market volatility.

Clean Exit Management: Automatically closes positions on opposite signal.

Conclusion

The Dual-Phase Trend Regime Strategy is a smart, adaptive, non-repainting system that:

Automatically switches between fast and slow trend logic.

Responds dynamically to changes in volatility.

Provides clean and visual entry/exit signals.

Supports both momentum and reversal trading logic.

This strategy is ideal for traders seeking a volatility-aware, trend-sensitive tool across any market or timeframe.

Full credit to Zeiierman.

ChopFlow ATR Scalp StrategyA lean, high-velocity scalp framework for NQ and other futures that blends trend clarity, volume confirmation, and adaptive exits to give you precise, actionable signals—no cluttered bands or lagging indicators.

⸻

🔍 Overview

This strategy locks onto rapid intraday moves by:

• Filtering for directional momentum with the Choppiness Index (CI)

• Confirming conviction via On-Balance Volume (OBV) against its moving average

• Automatically sizing stops and targets with a multiple of the Average True Range (ATR)

It’s designed for scalp traders who need clean, timely entries without wading through choppy noise.

⸻

⚙️ Key Features & Inputs

1. ATR Length & Multiplier

• Controls exit distances based on current volatility.

2. Choppiness Length & Threshold

• Measures trend strength; only fires when the market isn’t “stuck in the mud.”

3. OBV SMA Length

• Smoothes volume flow to confirm genuine buying or selling pressure.

4. Custom Session Hours

• Avoid overnight gaps or low-liquidity periods.

All inputs are exposed for rapid tuning to your preferred scalp cadence.

🚀 How It Works

1. Long Entry triggers when:

• CI < threshold (strong trend)

• OBV > its SMA (positive volume flow)

• You’re within the defined session

2. Short Entry mirrors the above (CI < threshold, OBV < SMA)

3. Exit uses ATR × multiplier for both stop-loss and take-profit

⸻

🎯 Usage Tips

• Start with defaults (ATR 14, multiplier 1.5; CI 14, threshold 60; OBV SMA 10).

• Monitor signal frequency, then tighten/loosen CI or OBV look-back as needed.

• Pair with a fast MA crossover or price-action trigger if you want even sharper timing.

• Backtest across different sessions (early open vs. power hours) to find your edge.

⸻

⚠️ Disclaimer

This script is provided “as-is” for educational and research purposes. Always paper-trade any new setup extensively before deploying live capital, and adjust risk parameters to your personal tolerance.

⸻

Elevate your scalp game with ChopFlow ATR—where trend, volume, and volatility converge for clear, confident entries. Happy scalping!

Dskyz (DAFE) AI Adaptive Regime - Beginners VersionDskyz (DAFE) AI Adaptive Regime - Pro: Revolutionizing Trading for All

Introduction

In the fast-paced world of financial markets, traders need tools that can keep up with ever-changing conditions while remaining accessible. The Dskyz (DAFE) AI Adaptive Regime - Pro is a groundbreaking TradingView strategy that delivers advanced, AI-driven trading capabilities to everyday traders. Available on TradingView (TradingView Scripts), this Pine Script strategy combines sophisticated market analysis with user-friendly features, making it a standout choice for both novice and experienced traders.

Core Functionality

The strategy is built to adapt to different market regimes—trending, ranging, volatile, or quiet—using a robust set of technical indicators, including:

Moving Averages (MA): Fast and slow EMAs to detect trend direction.

Average True Range (ATR): For dynamic stop-loss and volatility assessment.

Relative Strength Index (RSI) and MACD: Multi-timeframe confirmation of momentum and trend.

Average Directional Index (ADX): To identify trending markets.

Bollinger Bands: For assessing volatility and range conditions.

Candlestick Patterns: Recognizes patterns like bullish engulfing, hammer, and double bottoms, confirmed by volume spikes.

It generates buy and sell signals based on a scoring system that weighs these indicators, ensuring trades align with the current market environment. The strategy also includes dynamic risk management with ATR-based stops and trailing stops, as well as performance tracking to optimize future trades.

What Sets It Apart

The Dskyz (DAFE) AI Adaptive Regime - Pro distinguishes itself from other TradingView strategies through several unique features, which we compare to common alternatives below:

| Feature | Dskyz (DAFE) | Typical TradingView Strategies|

|---------|-------------|------------------------------------------------------------|

| Regime Detection | Automatically identifies and adapts to **four** market regimes | Often static or limited to trend/range detection |

| Multi‑Timeframe Analysis | Uses higher‑timeframe RSI/MACD for confirmation | Rarely incorporates multi‑timeframe data |

| Pattern Recognition | Detects candlestick patterns **with volume confirmation** | Limited or no pattern recognition |

| Dynamic Risk Management | ATR‑based stops and trailing stops | Often uses fixed stops or basic risk rules |

| Performance Tracking | Adjusts thresholds based on past performance | Typically static parameters |

| Beginner‑Friendly Presets | Aggressive, Conservative, Optimized profiles | Requires manual parameter tuning |

| Visual Cues | Color‑coded backgrounds for regimes | Basic or no visual aids |

The Dskyz strategy’s ability to integrate regime detection, multi-timeframe analysis, and user-friendly presets makes it uniquely versatile and accessible, addressing the needs of everyday traders who want professional-grade tools without the complexity.

-Key Features and Benefits

[Why It’s Ideal for Everyday Traders

⚡The Dskyz (DAFE) AI Adaptive Regime - Pro democratizes advanced trading by offering professional-grade tools in an accessible package. Unlike many TradingView strategies that require deep technical knowledge or fail in changing market conditions, this strategy simplifies complex analysis while maintaining robustness. Its presets and visual aids make it easy for beginners to start, while its adaptive features and performance tracking appeal to advanced traders seeking an edge.

🔄Limitations and Considerations

Market Dependency: Performance varies by market and timeframe. Backtesting is essential to ensure compatibility with your trading style.

Learning Curve: While presets simplify use, understanding regimes and indicators enhances effectiveness.

No Guaranteed Profits: Like all strategies, success depends on market conditions and proper execution. The Reddit discussion highlights skepticism about TradingView strategies’ universal success (Reddit Discussion).

Instrument Specificity: Optimized for futures (e.g., ES, NQ) due to fixed tick values. Test on other instruments like stocks or forex to verify compatibility.

📌Conclusion

The Dskyz (DAFE) AI Adaptive Regime - Pro is a revolutionary TradingView strategy that empowers everyday traders with advanced, AI-driven tools. Its ability to adapt to market regimes, confirm signals across timeframes, and manage risk dynamically. sets it apart from typical strategies. By offering beginner-friendly presets and visual cues, it makes sophisticated trading accessible without sacrificing power. Whether you’re a novice looking to trade smarter or a pro seeking a competitive edge, this strategy is your ticket to mastering the markets. Add it to your chart, backtest it, and join the elite traders leveraging AI to dominate. Trade like a boss today! 🚀

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

-Dskyz

TrendTwisterV1.5 (Forex Ready + Indicators)A Precision Trend-Following TradingView Strategy for Forex**

HullShiftFX is a Pine Script strategy for TradingView that combines the power of the **Hull Moving Average (HMA)** and a **shifted Exponential Moving Average (EMA)** with multi-layered momentum filters including **RSI** and **dual Stochastic Oscillators**.

It’s designed for traders looking to catch high-probability breakouts with tight risk management and visual clarity.

Chart settings:

1. Select "Auto - Fits data to screen"

2. Please Select "Scale Price Chart Only" (To make the chart not squished)

### ✅ Entry Conditions

**Long Position:**

- Price closes above the 12-period Hull Moving Average.

- Price closes above the 5-period EMA shifted forward by 2 bars.

- RSI is above 50.

- Stochastic Oscillator (12,3,3) %K is above 50.

- Stochastic Oscillator (5,3,3) %K is above 50.

- Hull MA crosses above the shifted EMA.

**Short Position:**

- Price closes below the 12-period Hull Moving Average.

- Price closes below the 5-period EMA shifted forward by 2 bars.

- RSI is below 50.

- Stochastic Oscillator (12,3,3) %K is below 50.

- Stochastic Oscillator (5,3,3) %K is below 50.

- Hull MA crosses below the shifted EMA.

---

## 📉 Risk Management

- **Stop Loss:** Set at the low (for long) or high (for short) of the previous 2 candles.

- **Take Profit:** Calculated at a risk/reward ratio of **1.65x** the stop loss distance.

---

## 📊 Indicators Used

- **Hull Moving Average (12)**

- **Exponential Moving Average (5) **

- **Relative Strength Index (14)**

- **Stochastic Oscillators:**

- %K (12,3,3)

- %K (5,3,3)

Donchian Breakout Strategy📈 Donchian Breakout Strategy (Inspired by Way of the Turtle)

This strategy is a modern adaptation of the legendary Turtle Trading system as taught in Way of the Turtle by Curtis Faith — re-engineered for the crypto market’s volatility, 24/7 nature, and frequent fakeouts.

⸻

🐢 Original Inspiration

The original Turtle system, created by Richard Dennis and William Eckhardt, used:

• Breakouts of Donchian Channels (20-day for entry, 10-day for exit)

• Volatility-based position sizing using ATR (N)

• Simple rules, big trend exposure, and pyramiding to grow winners

It was built for futures and commodities, trading daily bars, assuming stable trading hours and regulated markets.

⸻

🚀 What’s Different in This Strategy?

✅ Optimized for Crypto

• Adapts to constant volatility and price manipulation common in crypto

• Adds commission modeling for realistic results (0.045% default)

✅ Improved Entry Filtering

• Uses EMA filter to align with trend direction

• Adds RSI momentum check to avoid early or weak breakouts

• Optional volatility and volume filters to reduce false signals

✅ Smarter Exits

• ATR-based volatility stop loss, not just Donchian reversal

• Avoids pyramiding to reduce risk from sudden reversals

✅ Backtest-Friendly

• Default backtest window starts from 2025-01-01

• Fully configurable: long/short toggle, filter control, stop loss multiplier

⸻

🧪 Use Case

• Best on trending coins with strong directional moves

• Avoids chop via filters, preserving capital

• Can be tuned for aggressive or conservative setups with just a few tweaks

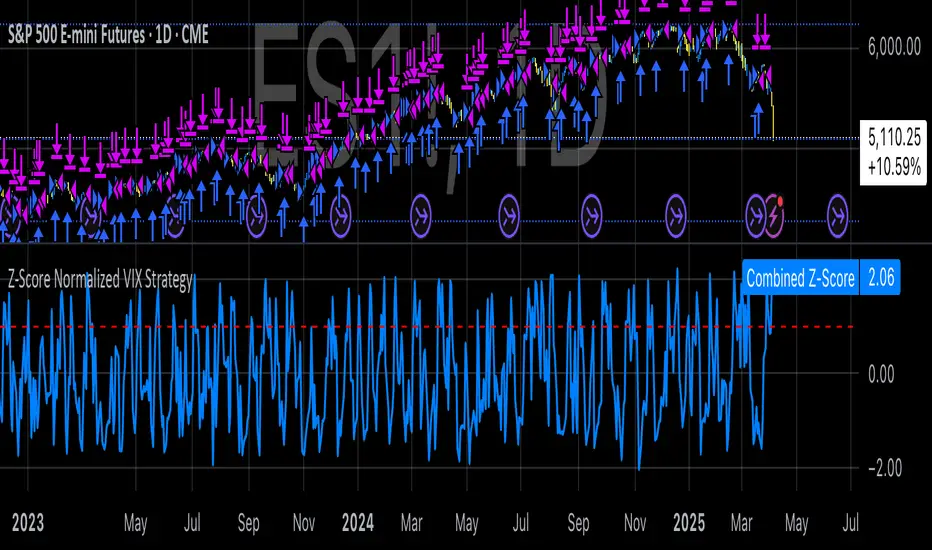

Z-Score Normalized VIX StrategyThis strategy leverages the concept of the Z-score applied to multiple VIX-based volatility indices, specifically designed to capture market reversals based on the normalization of volatility. The strategy takes advantage of VIX-related indicators to measure extreme levels of market fear or greed and adjusts its position accordingly.

1. Overview of the Z-Score Methodology

The Z-score is a statistical measure that describes the position of a value relative to the mean of a distribution in terms of standard deviations. In this strategy, the Z-score is calculated for various volatility indices to assess how far their values are from their historical averages, thus normalizing volatility levels. The Z-score is calculated as follows:

Z = \frac{X - \mu}{\sigma}

Where:

• X is the current value of the volatility index.

• \mu is the mean of the index over a specified period.

• \sigma is the standard deviation of the index over the same period.

This measure tells us how many standard deviations the current value of the index is away from its average, indicating whether the market is experiencing unusually high or low volatility (fear or calm).

2. VIX Indices Used in the Strategy

The strategy utilizes four commonly referenced volatility indices:

• VIX (CBOE Volatility Index): Measures the market’s expectations of 30-day volatility based on S&P 500 options.

• VIX3M (3-Month VIX): Reflects expectations of volatility over the next three months.

• VIX9D (9-Day VIX): Reflects shorter-term volatility expectations.

• VVIX (VIX of VIX): Measures the volatility of the VIX itself, indicating the level of uncertainty in the volatility index.

These indices provide a comprehensive view of the current volatility landscape across different time horizons.

3. Strategy Logic

The strategy follows a long entry condition and an exit condition based on the combined Z-score of the selected volatility indices:

• Long Entry Condition: The strategy enters a long position when the combined Z-score of the selected VIX indices falls below a user-defined threshold, indicating an abnormally low level of volatility (suggesting a potential market bottom and a bullish reversal). The threshold is set as a negative value (e.g., -1), where a more negative Z-score implies greater deviation below the mean.

• Exit Condition: The strategy exits the long position when the combined Z-score exceeds the threshold (i.e., when the market volatility increases above the threshold, indicating a shift in market sentiment and reduced likelihood of continued upward momentum).

4. User Inputs

• Z-Score Lookback Period: The user can adjust the lookback period for calculating the Z-score (e.g., 6 periods).

• Z-Score Threshold: A customizable threshold value to define when the market has reached an extreme volatility level, triggering entries and exits.

The strategy also allows users to select which VIX indices to use, with checkboxes to enable or disable each index in the calculation of the combined Z-score.

5. Trade Execution Parameters

• Initial Capital: The strategy assumes an initial capital of $20,000.

• Pyramiding: The strategy does not allow pyramiding (multiple positions in the same direction).

• Commission and Slippage: The commission is set at $0.05 per contract, and slippage is set at 1 tick.

6. Statistical Basis of the Z-Score Approach

The Z-score methodology is a standard technique in statistics and finance, commonly used in risk management and for identifying outliers or unusual events. According to Dumas, Fleming, and Whaley (1998), volatility indices like the VIX serve as a useful proxy for market sentiment, particularly during periods of high uncertainty. By calculating the Z-score, we normalize volatility and quantify the degree to which the current volatility deviates from historical norms, allowing for systematic entry and exit based on these deviations.

7. Implications of the Strategy

This strategy aims to exploit market conditions where volatility has deviated significantly from its historical mean. When the Z-score falls below the threshold, it suggests that the market has become excessively calm, potentially indicating an overreaction to past market events. Entering long positions under such conditions could capture market reversals as fear subsides and volatility normalizes. Conversely, when the Z-score rises above the threshold, it signals increased volatility, which could be indicative of a bearish shift in the market, prompting an exit from the position.

By applying this Z-score normalized approach, the strategy seeks to achieve more consistent entry and exit points by reducing reliance on subjective interpretation of market conditions.

8. Scientific Sources

• Dumas, B., Fleming, J., & Whaley, R. (1998). “Implied Volatility Functions: Empirical Tests”. The Journal of Finance, 53(6), 2059-2106. This paper discusses the use of volatility indices and their empirical behavior, providing context for volatility-based strategies.

• Black, F., & Scholes, M. (1973). “The Pricing of Options and Corporate Liabilities”. Journal of Political Economy, 81(3), 637-654. The original Black-Scholes model, which forms the basis for many volatility-related strategies.

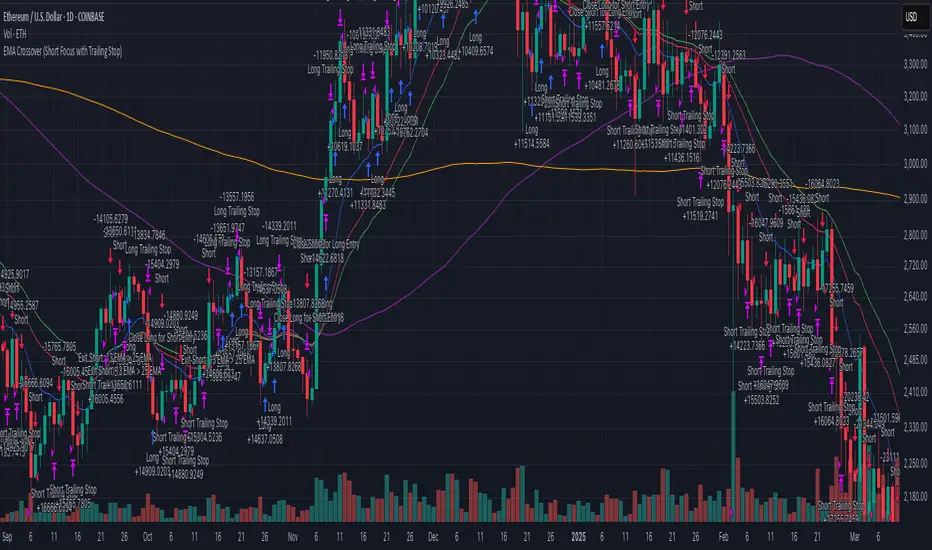

EMA Crossover (Short Focus with Trailing Stop)This strategy utilizes a combination of Exponential Moving Averages (EMA) and Simple Moving Averages (SMA) to generate entry and exit signals for both long and short positions. The core of the strategy is based on the 13-period EMA (short EMA) crossing the 33-period EMA (long EMA) for entering long trades, while a 13-period EMA crossing the 25-period EMA (mid EMA) generates short trade signals. The 100-period SMA and 200-period SMA serve as additional trend indicators to provide context for the market conditions. The strategy aims to capitalize on trend reversals and momentum shifts in the market.

The strategy is designed to execute trades swiftly with an emphasis on entering positions when conditions align in real time. For long entries, the strategy initiates a buy when the 13 EMA is greater than the 33 EMA, indicating a bullish trend. For short entries, the 13 EMA crossing below the 33 EMA signals a bearish trend, prompting a short position. Importantly, the code includes built-in exit conditions for both long and short positions. Long positions are exited when the 13 EMA falls below the 33 EMA, while short positions are closed when the 13 EMA crosses above the 25 EMA.

A key feature of the strategy is the use of trailing stops for both long and short positions. This dynamic exit method adjusts the stop level as the market moves in favor of the trade, locking in profits while reducing the risk of losses. The trailing stop for long positions is based on the high price of the current bar, while the trailing stop for short positions is set using the low price, providing more flexibility in managing risk. This trailing stop mechanism helps to capture profits from favorable market moves while ensuring that positions are exited if the market moves against them.

This strategy works best on the daily timeframe and is optimized for major cryptocurrency pairs. The daily chart allows for the EMAs to provide more reliable signals, as the strategy is designed to capture broader trends rather than short-term market fluctuations. Using it on major crypto pairs increases its effectiveness as these assets tend to have strong and sustained trends, providing better opportunities for the strategy to perform well.

Adaptive Fibonacci Pullback System -FibonacciFluxAdaptive Fibonacci Pullback System (AFPS) - FibonacciFlux

This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0). Original concepts by FibonacciFlux.

Abstract

The Adaptive Fibonacci Pullback System (AFPS) presents a sophisticated, institutional-grade algorithmic strategy engineered for high-probability trend pullback entries. Developed by FibonacciFlux, AFPS uniquely integrates a proprietary Multi-Fibonacci Supertrend engine (0.618, 1.618, 2.618 ratios) for harmonic volatility assessment, an Adaptive Moving Average (AMA) Channel providing dynamic market context, and a synergistic Multi-Timeframe (MTF) filter suite (RSI, MACD, Volume). This strategy transcends simple indicator combinations through its strict, multi-stage confluence validation logic. Historical simulations suggest that specific MTF filter configurations can yield exceptional performance metrics, potentially achieving Profit Factors exceeding 2.6 , indicative of institutional-level potential, while maintaining controlled risk under realistic trading parameters (managed equity risk, commission, slippage).

4 hourly MTF filtering

1. Introduction: Elevating Pullback Trading with Adaptive Confluence

Traditional pullback strategies often struggle with noise, false signals, and adapting to changing market dynamics. AFPS addresses these challenges by introducing a novel framework grounded in Fibonacci principles and adaptive logic. Instead of relying on static levels or single confirmations, AFPS seeks high-probability pullback entries within established trends by validating signals through a rigorous confluence of:

Harmonic Volatility Context: Understanding the trend's stability and potential turning points using the unique Multi-Fibonacci Supertrend.

Adaptive Market Structure: Assessing the prevailing trend regime via the AMA Channel.

Multi-Dimensional Confirmation: Filtering signals with lower-timeframe Momentum (RSI), Trend Alignment (MACD), and Market Conviction (Volume) using the MTF suite.

The objective is to achieve superior signal quality and adaptability, moving beyond conventional pullback methodologies.

2. Core Methodology: Synergistic Integration

AFPS's effectiveness stems from the engineered synergy between its core components:

2.1. Multi-Fibonacci Supertrend Engine: Utilizes specific Fibonacci ratios (0.618, 1.618, 2.618) applied to ATR, creating a multi-layered volatility envelope potentially resonant with market harmonics. The averaged and EMA-smoothed result (`smoothed_supertrend`) provides a robust, dynamic trend baseline and context filter.

// Key Components: Multi-Fibonacci Supertrend & Smoothing

average_supertrend = (supertrend1 + supertrend2 + supertrend3) / 3

smoothed_supertrend = ta.ema(average_supertrend, st_smooth_length)

2.2. Adaptive Moving Average (AMA) Channel: Provides dynamic market context. The `ama_midline` serves as a key filter in the entry logic, confirming the broader trend bias relative to adaptive price action. Extended Fibonacci levels derived from the channel width offer potential dynamic S/R zones.

// Key Component: AMA Midline

ama_midline = (ama_high_band + ama_low_band) / 2

2.3. Multi-Timeframe (MTF) Filter Suite: An optional but powerful validation layer (RSI, MACD, Volume) assessed on a lower timeframe. Acts as a **validation cascade** – signals must pass all enabled filters simultaneously.

2.4. High-Confluence Entry Logic: The core innovation. A pullback entry requires a specific sequence and validation:

Price interaction with `average_supertrend` and recovery above/below `smoothed_supertrend`.

Price confirmation relative to the `ama_midline`.

Simultaneous validation by all enabled MTF filters.

// Simplified Long Entry Logic Example (incorporates key elements)

long_entry_condition = enable_long_positions and

(low < average_supertrend and close > smoothed_supertrend) and // Pullback & Recovery

(close > ama_midline and close > ama_midline) and // AMA Confirmation

(rsi_filter_long_ok and macd_filter_long_ok and volume_filter_ok) // MTF Validation

This strict, multi-stage confluence significantly elevates signal quality compared to simpler pullback approaches.

1hourly filtering

3. Realistic Implementation and Performance Potential

AFPS is designed for practical application, incorporating realistic defaults and highlighting performance potential with crucial context:

3.1. Realistic Default Strategy Settings:

The script includes responsible default parameters:

strategy('Adaptive Fibonacci Pullback System - FibonacciFlux', shorttitle = "AFPS", ...,

initial_capital = 10000, // Accessible capital

default_qty_type = strategy.percent_of_equity, // Equity-based risk

default_qty_value = 4, // Default 4% equity risk per initial trade

commission_type = strategy.commission.percent,

commission_value = 0.03, // Realistic commission

slippage = 2, // Realistic slippage

pyramiding = 2 // Limited pyramiding allowed

)

Note: The default 4% risk (`default_qty_value = 4`) requires careful user assessment and adjustment based on individual risk tolerance.

3.2. Historical Performance Insights & Institutional Potential:

Backtesting provides insights into historical behavior under specific conditions (always specify Asset/Timeframe/Dates when sharing results):

Default Performance Example: With defaults, historical tests might show characteristics like Overall PF ~1.38, Max DD ~1.16%, with potential Long/Short performance variance (e.g., Long PF 1.6+, Short PF < 1).

Optimized MTF Filter Performance: Crucially, historical simulations demonstrate that meticulous configuration of the MTF filters (particularly RSI and potentially others depending on market) can significantly enhance performance. Under specific, optimized MTF filter settings combined with appropriate risk management (e.g., 7.5% risk), historical tests have indicated the potential to achieve **Profit Factors exceeding 2.6**, alongside controlled drawdowns (e.g., ~1.32%). This level of performance, if consistently achievable (which requires ongoing adaptation), aligns with metrics often sought in institutional trading environments.

Disclaimer Reminder: These results are strictly historical simulations. Past performance does not guarantee future results. Achieving high performance requires careful parameter tuning, adaptation to changing markets, and robust risk management.

3.3. Emphasizing Risk Management:

Effective use of AFPS mandates active risk management. Utilize the built-in Stop Loss, Take Profit, and Trailing Stop features. The `pyramiding = 2` setting requires particularly diligent oversight. Do not rely solely on default settings.

4. Conclusion: Advancing Trend Pullback Strategies

The Adaptive Fibonacci Pullback System (AFPS) offers a sophisticated, theoretically grounded, and highly adaptable framework for identifying and executing high-probability trend pullback trades. Its unique blend of Fibonacci resonance, adaptive context, and multi-dimensional MTF filtering represents a significant advancement over conventional methods. While requiring thoughtful implementation and risk management, AFPS provides discerning traders with a powerful tool potentially capable of achieving institutional-level performance characteristics under optimized conditions.

Acknowledgments

Developed by FibonacciFlux. Inspired by principles of Fibonacci analysis, adaptive averaging, and multi-timeframe confirmation techniques explored within the trading community.

Disclaimer

Trading involves substantial risk. AFPS is an analytical tool, not a guarantee of profit. Past performance is not indicative of future results. Market conditions change. Users are solely responsible for their decisions and risk management. Thorough testing is essential. Deploy at your own considered risk.

LUX CLARA - EMA + VWAP (No ATR Filter) - v6EMA STRAT SHOUT OUTOUTLIERSSSSS

Overview:

an intraday strategy built around two core principles:

Trend Confirmation using the 50 EMA (Exponential Moving Average) in relation to the VWAP (Volume-Weighted Average Price).

Entry Signals triggered by the 8 EMA crossing the 50 EMA in the direction of that confirmed trend.

Key Logic:

Bullish Trend if the 50 EMA is above VWAP. Only long entries are allowed when the 8 EMA crosses above the 50 EMA during that bullish phase.

Bearish Trend if the 50 EMA is below VWAP. Only short entries are allowed when the 8 EMA crosses below the 50 EMA during that bearish phase.

Intraday Focus: Trades are restricted to a user-defined session window (default 7:30 AM–11:30 AM), aligning entries/exits with peak intraday liquidity.

Exit Rule: Positions close automatically when the 8 EMA crosses back in the opposite direction of the entry.

Why It Works:

EMA + VWAP helps detect both immediate momentum (EMAs) and overall institutional bias (VWAP).

By confining trades to a set intraday window, the strategy aims to capture morning volatility while avoiding choppy afternoon or overnight sessions.

Customization:

Users can adjust EMA lengths, session times, or incorporate stops/targets for additional risk management.

It can be tested on various symbols and intraday timeframes to gauge performance and robustness.