[blackcat] L1 Whale Jumping out of the OceanLevel: 1

Background

One of the biggest differences between cryptocurrency and traditional financial markets is that cryptocurrency is based on blockchain technology. Individual investors can discover the direction of the flow of large funds through on-chain transfers. These large funds are often referred to as Whale. Whale can have a significant impact on the price movements of cryptocurrencies, especially Bitcoin . Therefore, how to monitor Whale trends is of great significance both in terms of fundamentals and technical aspects.

We often see whales suddenly jump out of the ocean and then set off huge waves. What we need to do is to surf the wave according to the trend after the whale jumps out of the sea. This is really an exciting sport!

Function

By modeling the behavior of Whale and individuals (Surfers), L1 Whale Jumping out of the Ocean can not only simply describe the behavior trends of Whale and individuals, but also describe the shape of waves generated by the whale jump. Individual traders need to follow the wave trend to take profit.

NOTE: white line and yellow candles represent whale appears but it CANNOT indicate the direction as PUMP or DUMP. This indicator is one of the whale series. It is featured by vividness. A technical indicator is drawn as ocean (momentum in blue and aqua), whale (whale PUMP/DUMP in white,yellow, red, fuchsia and green), huge wave (mid-term trend or swing trend in aqua and blue).However, it does not accurately generate buying and selling points.

Key Signal

var01 --> huge wave caused by whale jump. it is used to confirm whale jump and describe the trend of wave for surfers.

var02 --> whale move signal

var12 --> whale move signal

var28 --> high confidence level of huge whale move

dynabot --> deep ocean (dynamic bottom)

Pros and Cons

Pros:

1. Detect Whale pump and dump and the strength of huge wave.

2. Vividly compare the market movement to a huge wave caused by a whale jumping out of the sea.

3. When it resonante with buy or sell signal from other independent indicators, it has higher confidence level.

Cons:

1. No exact long and short entries.

2. It is sensitive and may have noise inside and generate fake entry signal.

Remarks

Please do not think that this is just a technical indicator, this is a documentary about whales.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

Cerca negli script per "wave"

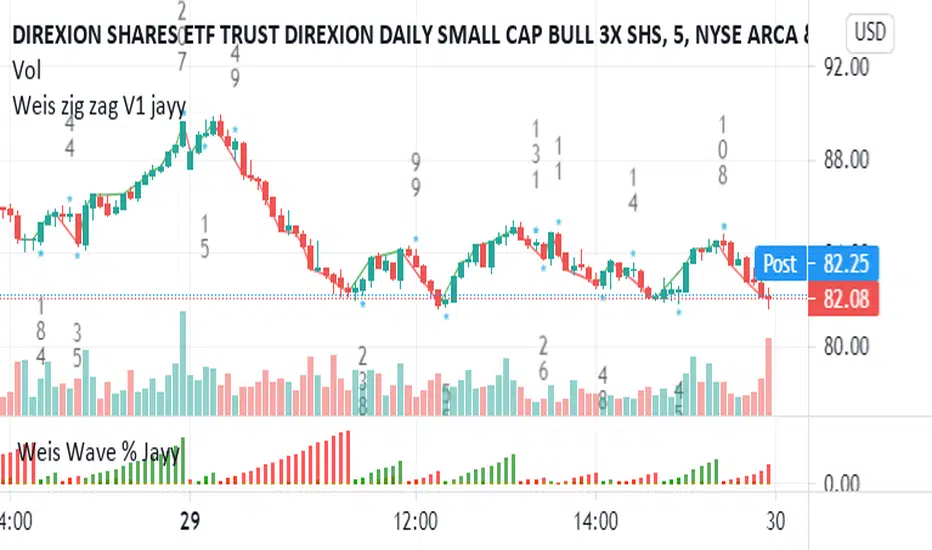

Weis pip zigzag jayyWhat you see here is the Weis pip zigzag wave plotted directly on the price chart. This script is the companion to the Weis pip wave ( ) which is plotted in the lower panel of the displayed chart and can be used as an alternate way of plotting the same results. The Weis pip zigzag wave shows how far in terms of price a Weis wave has traveled through the duration of a Weis wave. The Weis pip zigzag wave is used in combination with the Weis cumulative volume wave. The two waves must be set to the same "wave size".

To use this script you must set the wave size. Using the traditional Weis method simply enter the desired wave size in the box "Select Weis Wave Size" In this example, it is set to 5. Each wave for each security and each timeframe requires its own wave size. Although not the traditional method a more automatic way to set wave size would be to use ATR. This is not the true Weis method but it does give you similar waves and, importantly, without the hassle described above. Once the Weis wave size is set then the pip wave will be shown.

I have put a pip zigzag of a 5 point Weis wave on the bar chart - that is a different script. I have added it to allow your eye to see what a Weis wave looks like. You will notice that the wave is not in straight lines connecting wave tops to bottoms this is a function of the limitations of Pinescript version 1. This script would need to be in version 4 to allow straight lines. There are too many calculations within this script to allow conversion to Pinescript version 4 or even Version 3. I am in the process of rewriting this script to reduce the number of calculations and streamline the algorithm.

The numbers plotted on the chart are calculated to be relative numbers. The script is limited to showing only three numbers vertically. Only the highest three values of a number are shown. For example, if the highest recent pip value is 12,345 only the first 3 numerals would be displayed ie 123. But suppose there is a recent value of 691. It would not be helpful to display 691 if the other wave size is shown as 123. To give the appropriate relative value the script will show a value of 7 instead of 691. This informs you of the relative magnitude of the values. This is done automatically within the script. There is likely no need to manually override the automatically calculated value. I will create a video that demonstrates the manual override method.

What is a Weis wave? David Weis has been recognized as a Wyckoff method analyst he has written two books one of which, Trades About to Happen, describes the evolution of the now popular Weis wave. The method employed by Weis is to identify waves of price action and to compare the strength of the waves on characteristics of wave strength. Chief among the characteristics of strength is the cumulative volume of the wave. There are other markers that Weis uses as well for example how the actual price difference between the start of the Weis wave from start to finish. Weis also uses time, particularly when using a Renko chart. Weis specifically uses candle or bar closes to define all wave action ie a line chart.

David Weis did a futures io video which is a popular source of information about his method.

This is the identical script with the identical settings but without the offending links. If you want to see the pip Weis method in practice then search Weis pip wave. If you want to see Weis chart in pdf then message me and I will give a link or the Weis pdf. Why would you want to see the Weis chart for May 27, 2020? Merely to confirm the veracity of my algorithm. You could compare my Weis chart here () from the same period to the David Weis chart from May 27. Both waves are for the ES!1 4 hour chart and both for a wave size of 5.

qEMA 3 LineMy scenario consists of 3 ema lines which are ema 34, ema89, ema 144.

3 ema lines are important in elliott waves:

- A complete elliott wave of 144 waves

- An eliott wave has 89 waves

- In wave with wave, in wave 89 again wave 34 waves

I used to find the waves in elliott, know where the cycle elliott will end up (when the price hit ema144)

DeepClean Linear indicator 1. Indicator Name

DeepClean Linear indicator

2. One-Line Introduction

A trend-recognition indicator that overlays a “transparent wave” on price, removing noise and revealing directional bias and trend intensity in a highly intuitive visual form.

3. Overall Summary

The DeepClean Linear indicator calculates trend direction using changes in linear regression slope and determines trend strength by comparing how consistently the regression line moves over a defined lookback window.

Rather than merely identifying trend direction, the indicator applies a triple-layer noise-filtering process (EMA → SMA → RMA) to produce a clean, wave-shaped data line that filters out unnecessary market noise.

This transparent wave sits directly on top of price, allowing traders to visually compare price movement and trend strength at the same time.

A stronger trend results in a taller, thicker wave, while weakening momentum causes the wave to thin, making it easier to spot trend continuation, exhaustion, or upcoming reversal.

Color automatically shifts based on trend:

Bright cyan/teal during bullish conditions

Reddish tones during bearish conditions

Transparency dynamically adjusts depending on strength

The indicator excels at identifying the true underlying trend by ignoring minor fluctuations and is well suited for scalping, swing trading, and position trading.

It also significantly reduces false signals in ranging markets, making it ideal for trend-following strategies.

4. Advantages

① Ultra-Clean Noise-Reduced Wave

Utilizes a 3-stage smoothing filter (EMA → SMA → RMA) to produce a much cleaner wave than standard moving averages, highlighting only core trend movement.

② Trend Direction & Strength at a Glance

Based on comparative linear regression behavior, the indicator quantifies both direction and strength, making convergence/divergence highly visible.

③ Intuitive Price Overlay Visualization

The semi-transparent wave sits directly on price action, allowing traders to instantly see divergence from price, trend weakening, or early turning points.

④ Dynamic Transparency Coloring

Strong trends appear bold and intense, while weaker trends fade visually—making signal interpretation effortless.

⑤ Excellent Range Filtering

During low-direction phases (state = 0), the wave turns neutral, preventing forced or premature entries.

⑥ Multi-Timeframe Compatibility

The wave remains stable from 1-minute to weekly charts, making it suitable for trend analysis, execution, and risk control across all timeframes.

📌 Core Concept Overview

The indicator evaluates the relative comparison of linear regression values over the last n periods.

A positive trend value indicates bullish bias

A negative trend value indicates bearish bias

Intensity represents strength and controls wave height

waveTop / waveBot define the visual wave area relative to price

State Values

1 = Bullish Trend

-1 = Bearish Trend

0 = Neutral / Weak Direction

⚙️ Settings Overview

Option Description

Trend Lookback (n) Comparison window for regression slope. Higher = bigger trend focus.

Range Tolerance (%) Strength threshold to classify bullish/bearish movement. Higher = more conservative.

Source Price source for regression calculations.

Linear Reg Length Length of the linear regression.

Noise Filter Strength (smoothK) Controls the smoothing intensity. Higher = smoother wave.

Wave Amplitude (amp) Adjusts the height/thickness of the wave.

Bull/Bear Color Colors for bullish/bearish waves.

Base Transparency Base opacity level; modified dynamically by trend strength.

📈 Bullish Timing Recognition Examples

Wave begins turning brighter teal and more opaque, indicating strengthening upward pressure.

waveTop expands above price, signaling early trend expansion.

State flips to 1, often marking a trend restart or early reversal phase.

A steadily rising wave height suggests sustained bullish momentum.

📉 Bearish Timing Recognition Examples

Wave shifts into red tones, showing bearish dominance.

waveBot expands below price, indicating rising downside volatility.

State stays at -1 while intensity increases, signaling entry into strong downtrend conditions.

A shift from weak → strong bearish intensity can provide short-entry timing cues.

🧪 Recommended Usage

Use as a core component in trend-following systems

Adjust position size based on wave thickness (trend strength)

Combine with RSI/MACD to reduce false signals during overbought/oversold zones

Sudden wave expansion during volatility increases helps detect trend acceleration

In sideways markets, frequent state = 0 readings help avoid low-probability trades

🔒 Important Notes

As a trend-based indicator, it may misread choppy/ranging markets

Because of smoothing, signals may appear slightly delayed

Extreme news volatility can temporarily distort trend clarity

Hellenic EMA Matrix - PremiumHellenic EMA Matrix - Alpha Omega Premium

Complete User Guide

Table of Contents

Introduction

Indicator Philosophy

Mathematical Constants

EMA Types

Settings

Trading Signals

Visualization

Usage Strategies

FAQ

Introduction

Hellenic EMA Matrix is a premium indicator based on mathematical constants of nature: Phi (Phi - Golden Ratio), Pi (Pi), e (Euler's number). The indicator uses these universal constants to create dynamic EMAs that adapt to the natural rhythms of the market.

Key Features:

6 EMA types based on mathematical constants

Premium visualization with Neon Glow and Gradient Clouds

Automatic Fast/Mid/Slow EMA sorting

STRONG signals for powerful trends

Pulsing Ribbon Bar for instant trend assessment

Works on all timeframes (M1 - MN)

Indicator Philosophy

Why Mathematical Constants?

Traditional EMAs use arbitrary periods (9, 21, 50, 200). Hellenic Matrix goes further, using universal mathematical constants found in nature:

Phi (1.618) - Golden Ratio: galaxy spirals, seashells, human body proportions

Pi (3.14159) - Pi: circles, waves, cycles

e (2.71828) - Natural logarithm base: exponential growth, radioactive decay

Markets are also a natural system composed of millions of participants. Using mathematical constants allows tuning into the natural rhythms of market cycles.

Mathematical Constants

Phi (Phi) - Golden Ratio

Phi = 1.618033988749895

Properties:

Phi² = Phi + 1 = 2.618

Phi³ = 4.236

Phi⁴ = 6.854

Application: Ideal for trending movements and Fibonacci corrections

Pi (Pi) - Pi Number

Pi = 3.141592653589793

Properties:

2Pi = 6.283 (full circle)

3Pi = 9.425

4Pi = 12.566

Application: Excellent for cyclical markets and wave structures

e (Euler) - Euler's Number

e = 2.718281828459045

Properties:

e² = 7.389

e³ = 20.085

e⁴ = 54.598

Application: Suitable for exponential movements and volatile markets

EMA Types

1. Phi (Phi) - Golden Ratio EMA

Description: EMA based on the golden ratio

Period Formula:

Period = Phi^n × Base Multiplier

Parameters:

Phi Power Level (1-8): Power of Phi

Phi¹ = 1.618 → ~16 period (with Base=10)

Phi² = 2.618 → ~26 period

Phi³ = 4.236 → ~42 period (recommended)

Phi⁴ = 6.854 → ~69 period

Recommendations:

Phi² or Phi³ for day trading

Phi⁴ or Phi⁵ for swing trading

Works excellently as Fast EMA

2. Pi (Pi) - Circular EMA

Description: EMA based on Pi for cyclical movements

Period Formula:

Period = Pi × Multiple × Base Multiplier

Parameters:

Pi Multiple (1-10): Pi multiplier

1Pi = 3.14 → ~31 period (with Base=10)

2Pi = 6.28 → ~63 period (recommended)

3Pi = 9.42 → ~94 period

Recommendations:

2Pi ideal as Mid or Slow EMA

Excellently identifies cycles and waves

Use on volatile markets (crypto, forex)

3. e (Euler) - Natural EMA

Description: EMA based on natural logarithm

Period Formula:

Period = e^n × Base Multiplier

Parameters:

e Power Level (1-6): Power of e

e¹ = 2.718 → ~27 period (with Base=10)

e² = 7.389 → ~74 period (recommended)

e³ = 20.085 → ~201 period

Recommendations:

e² works excellently as Slow EMA

Ideal for stocks and indices

Filters noise well on lower timeframes

4. Delta (Delta) - Adaptive EMA

Description: Adaptive EMA that changes period based on volatility

Period Formula:

Period = Base Period × (1 + (Volatility - 1) × Factor)

Parameters:

Delta Base Period (5-200): Base period (default 20)

Delta Volatility Sensitivity (0.5-5.0): Volatility sensitivity (default 2.0)

How it works:

During low volatility → period decreases → EMA reacts faster

During high volatility → period increases → EMA smooths noise

Recommendations:

Works excellently on news and sharp movements

Use as Fast EMA for quick adaptation

Sensitivity 2.0-3.0 for crypto, 1.0-2.0 for stocks

5. Sigma (Sigma) - Composite EMA

Description: Composite EMA combining multiple active EMAs

Composition Methods:

Weighted Average (default):

Sigma = (Phi + Pi + e + Delta) / 4

Simple average of all active EMAs

Geometric Mean:

Sigma = fourth_root(Phi × Pi × e × Delta)

Geometric mean (more conservative)

Harmonic Mean:

Sigma = 4 / (1/Phi + 1/Pi + 1/e + 1/Delta)

Harmonic mean (more weight to smaller values)

Recommendations:

Enable for additional confirmation

Use as Mid EMA

Weighted Average - most universal method

6. Lambda (Lambda) - Wave EMA

Description: Wave EMA with sinusoidal period modulation

Period Formula:

Period = Base Period × (1 + Amplitude × sin(2Pi × bar / Frequency))

Parameters:

Lambda Base Period (10-200): Base period

Lambda Wave Amplitude (0.1-2.0): Wave amplitude

Lambda Wave Frequency (10-200): Wave frequency in bars

How it works:

Period pulsates sinusoidally

Creates wave effect following market cycles

Recommendations:

Experimental EMA for advanced users

Works well on cyclical markets

Frequency = 50 for day trading, 100+ for swing

Settings

Matrix Core Settings

Base Multiplier (1-100)

Multiplies all EMA periods

Base = 1: Very fast EMAs (Phi³ = 4, 2Pi = 6, e² = 7)

Base = 10: Standard (Phi³ = 42, 2Pi = 63, e² = 74)

Base = 20: Slow EMAs (Phi³ = 85, 2Pi = 126, e² = 148)

Recommendations by timeframe:

M1-M5: Base = 5-10

M15-H1: Base = 10-15 (recommended)

H4-D1: Base = 15-25

W1-MN: Base = 25-50

Matrix Source

Data source selection for EMA calculation:

close - closing price (standard)

open - opening price

high - high

low - low

hl2 - (high + low) / 2

hlc3 - (high + low + close) / 3

ohlc4 - (open + high + low + close) / 4

When to change:

hlc3 or ohlc4 for smoother signals

high for aggressive longs

low for aggressive shorts

Manual EMA Selection

Critically important setting! Determines which EMAs are used for signal generation.

Use Manual Fast/Slow/Mid Selection

Enabled (default): You select EMAs manually

Disabled: Automatic selection by periods

Fast EMA

Fast EMA - reacts first to price changes

Recommendations:

Phi Golden (recommended) - universal choice

Delta Adaptive - for volatile markets

Must be fastest (smallest period)

Slow EMA

Slow EMA - determines main trend

Recommendations:

Pi Circular (recommended) - excellent trend filter

e Natural - for smoother trend

Must be slowest (largest period)

Mid EMA

Mid EMA - additional signal filter

Recommendations:

e Natural (recommended) - excellent middle level

Pi Circular - alternative

None - for more frequent signals (only 2 EMAs)

IMPORTANT: The indicator automatically sorts selected EMAs by their actual periods:

Fast = EMA with smallest period

Mid = EMA with middle period

Slow = EMA with largest period

Therefore, you can select any combination - the indicator will arrange them correctly!

Premium Visualization

Neon Glow

Enable Neon Glow for EMAs - adds glowing effect around EMA lines

Glow Strength:

Light - subtle glow

Medium (recommended) - optimal balance

Strong - bright glow (may be too bright)

Effect: 2 glow layers around each EMA for 3D effect

Gradient Clouds

Enable Gradient Clouds - fills space between EMAs with gradient

Parameters:

Cloud Transparency (85-98): Cloud transparency

95-97 (recommended)

Higher = more transparent

Dynamic Cloud Intensity - automatically changes transparency based on EMA distance

Cloud Colors:

Phi-Pi Cloud:

Blue - when Pi above Phi (bullish)

Gold - when Phi above Pi (bearish)

Pi-e Cloud:

Green - when e above Pi (bullish)

Blue - when Pi above e (bearish)

2 layers for volumetric effect

Pulsing Ribbon Bar

Enable Pulsing Indicator Bar - pulsing strip at bottom/top of chart

Parameters:

Ribbon Position: Top / Bottom (recommended)

Pulse Speed: Slow / Medium (recommended) / Fast

Symbols and colors:

Green filled square - STRONG BULLISH

Pink filled square - STRONG BEARISH

Blue hollow square - Bullish (regular)

Red hollow square - Bearish (regular)

Purple rectangle - Neutral

Effect: Pulsation with sinusoid for living market feel

Signal Bar Highlights

Enable Signal Bar Highlights - highlights bars with signals

Parameters:

Highlight Transparency (88-96): Highlight transparency

Highlight Style:

Light Fill (recommended) - bar background fill

Thin Line - bar outline only

Highlights:

Golden Cross - green

Death Cross - pink

STRONG BUY - green

STRONG SELL - pink

Show Greek Labels

Shows Greek alphabet letters on last bar:

Phi - Phi EMA (gold)

Pi - Pi EMA (blue)

e - Euler EMA (green)

Delta - Delta EMA (purple)

Sigma - Sigma EMA (pink)

When to use: For education or presentations

Show Old Background

Old background style (not recommended):

Green background - STRONG BULLISH

Pink background - STRONG BEARISH

Blue background - Bullish

Red background - Bearish

Not recommended - use new Gradient Clouds and Pulsing Bar

Info Table

Show Info Table - table with indicator information

Parameters:

Position: Top Left / Top Right (recommended) / Bottom Left / Bottom Right

Size: Tiny / Small (recommended) / Normal / Large

Table contents:

EMA list - periods and current values of all active EMAs

Effects - active visual effects

TREND - current trend state:

STRONG UP - strong bullish

STRONG DOWN - strong bearish

Bullish - regular bullish

Bearish - regular bearish

Neutral - neutral

Momentum % - percentage deviation of price from Fast EMA

Setup - current Fast/Slow/Mid configuration

Trading Signals

Show Golden/Death Cross

Golden Cross - Fast EMA crosses Slow EMA from below (bullish signal) Death Cross - Fast EMA crosses Slow EMA from above (bearish signal)

Symbols:

Yellow dot "GC" below - Golden Cross

Dark red dot "DC" above - Death Cross

Show STRONG Signals

STRONG BUY and STRONG SELL - the most powerful indicator signals

Conditions for STRONG BULLISH:

EMA Alignment: Fast > Mid > Slow (all EMAs aligned)

Trend: Fast > Slow (clear uptrend)

Distance: EMAs separated by minimum 0.15%

Price Position: Price above Fast EMA

Fast Slope: Fast EMA rising

Slow Slope: Slow EMA rising

Mid Trending: Mid EMA also rising (if enabled)

Conditions for STRONG BEARISH:

Same but in reverse

Visual display:

Green label "STRONG BUY" below bar

Pink label "STRONG SELL" above bar

Difference from Golden/Death Cross:

Golden/Death Cross = crossing moment (1 bar)

STRONG signal = sustained trend (lasts several bars)

IMPORTANT: After fixes, STRONG signals now:

Work on all timeframes (M1 to MN)

Don't break on small retracements

Work with any Fast/Mid/Slow combination

Automatically adapt thanks to EMA sorting

Show Stop Loss/Take Profit

Automatic SL/TP level calculation on STRONG signal

Parameters:

Stop Loss (ATR) (0.5-5.0): ATR multiplier for stop loss

1.5 (recommended) - standard

1.0 - tight stop

2.0-3.0 - wide stop

Take Profit R:R (1.0-5.0): Risk/reward ratio

2.0 (recommended) - standard (risk 1.5 ATR, profit 3.0 ATR)

1.5 - conservative

3.0-5.0 - aggressive

Formulas:

LONG:

Stop Loss = Entry - (ATR × Stop Loss ATR)

Take Profit = Entry + (ATR × Stop Loss ATR × Take Profit R:R)

SHORT:

Stop Loss = Entry + (ATR × Stop Loss ATR)

Take Profit = Entry - (ATR × Stop Loss ATR × Take Profit R:R)

Visualization:

Red X - Stop Loss

Green X - Take Profit

Levels remain active while STRONG signal persists

Trading Signals

Signal Types

1. Golden Cross

Description: Fast EMA crosses Slow EMA from below

Signal: Beginning of bullish trend

How to trade:

ENTRY: On bar close with Golden Cross

STOP: Below local low or below Slow EMA

TARGET: Next resistance level or 2:1 R:R

Strengths:

Simple and clear

Works well on trending markets

Clear entry point

Weaknesses:

Lags (signal after movement starts)

Many false signals in ranging markets

May be late on fast moves

Optimal timeframes: H1, H4, D1

2. Death Cross

Description: Fast EMA crosses Slow EMA from above

Signal: Beginning of bearish trend

How to trade:

ENTRY: On bar close with Death Cross

STOP: Above local high or above Slow EMA

TARGET: Next support level or 2:1 R:R

Application: Mirror of Golden Cross

3. STRONG BUY

Description: All EMAs aligned + trend + all EMAs rising

Signal: Powerful bullish trend

How to trade:

ENTRY: On bar close with STRONG BUY or on pullback to Fast EMA

STOP: Below Fast EMA or automatic SL (if enabled)

TARGET: Automatic TP (if enabled) or by levels

TRAILING: Follow Fast EMA

Entry strategies:

Aggressive: Enter immediately on signal

Conservative: Wait for pullback to Fast EMA, then enter on bounce

Pyramiding: Add positions on pullbacks to Mid EMA

Position management:

Hold while STRONG signal active

Exit on STRONG SELL or Death Cross appearance

Move stop behind Fast EMA

Strengths:

Most reliable indicator signal

Doesn't break on pullbacks

Catches large moves

Works on all timeframes

Weaknesses:

Appears less frequently than other signals

Requires confirmation (multiple conditions)

Optimal timeframes: All (M5 - D1)

4. STRONG SELL

Description: All EMAs aligned down + downtrend + all EMAs falling

Signal: Powerful bearish trend

How to trade: Mirror of STRONG BUY

Visual Signals

Pulsing Ribbon Bar

Quick market assessment at a glance:

Symbol Color State

Filled square Green STRONG BULLISH

Filled square Pink STRONG BEARISH

Hollow square Blue Bullish

Hollow square Red Bearish

Rectangle Purple Neutral

Pulsation: Sinusoidal, creates living effect

Signal Bar Highlights

Bars with signals are highlighted:

Green highlight: STRONG BUY or Golden Cross

Pink highlight: STRONG SELL or Death Cross

Gradient Clouds

Colored space between EMAs shows trend strength:

Wide clouds - strong trend

Narrow clouds - weak trend or consolidation

Color change - trend change

Info Table

Quick reference in corner:

TREND: Current state (STRONG UP, Bullish, Neutral, Bearish, STRONG DOWN)

Momentum %: Movement strength

Effects: Active visual effects

Setup: Fast/Slow/Mid configuration

Usage Strategies

Strategy 1: "Golden Trailing"

Idea: Follow STRONG signals using Fast EMA as trailing stop

Settings:

Fast: Phi Golden (Phi³)

Mid: Pi Circular (2Pi)

Slow: e Natural (e²)

Base Multiplier: 10

Timeframe: H1, H4

Entry rules:

Wait for STRONG BUY

Enter on bar close or on pullback to Fast EMA

Stop below Fast EMA

Management:

Hold position while STRONG signal active

Move stop behind Fast EMA daily

Exit on STRONG SELL or Death Cross

Take Profit:

Partially close at +2R

Trail remainder until exit signal

For whom: Swing traders, trend followers

Pros:

Catches large moves

Simple rules

Emotionally comfortable

Cons:

Requires patience

Possible extended drawdowns on pullbacks

Strategy 2: "Scalping Bounces"

Idea: Scalp bounces from Fast EMA during STRONG trend

Settings:

Fast: Delta Adaptive (Base 15, Sensitivity 2.0)

Mid: Phi Golden (Phi²)

Slow: Pi Circular (2Pi)

Base Multiplier: 5

Timeframe: M5, M15

Entry rules:

STRONG signal must be active

Wait for price pullback to Fast EMA

Enter on bounce (candle closes above/below Fast EMA)

Stop behind local extreme (15-20 pips)

Take Profit:

+1.5R or to Mid EMA

Or to next level

For whom: Active day traders

Pros:

Many signals

Clear entry point

Quick profits

Cons:

Requires constant monitoring

Not all bounces work

Requires discipline for frequent trading

Strategy 3: "Triple Filter"

Idea: Enter only when all 3 EMAs and price perfectly aligned

Settings:

Fast: Phi Golden (Phi³)

Mid: e Natural (e²)

Slow: Pi Circular (3Pi)

Base Multiplier: 15

Timeframe: H4, D1

Entry rules (LONG):

STRONG BUY active

Price above all three EMAs

Fast > Mid > Slow (all aligned)

All EMAs rising (slope up)

Gradient Clouds wide and bright

Entry:

On bar close meeting all conditions

Or on next pullback to Fast EMA

Stop:

Below Mid EMA or -1.5 ATR

Take Profit:

First target: +3R

Second target: next major level

Trailing: Mid EMA

For whom: Conservative swing traders, investors

Pros:

Very reliable signals

Minimum false entries

Large profit potential

Cons:

Rare signals (2-5 per month)

Requires patience

Strategy 4: "Adaptive Scalper"

Idea: Use only Delta Adaptive EMA for quick volatility reaction

Settings:

Fast: Delta Adaptive (Base 10, Sensitivity 3.0)

Mid: None

Slow: Delta Adaptive (Base 30, Sensitivity 2.0)

Base Multiplier: 3

Timeframe: M1, M5

Feature: Two different Delta EMAs with different settings

Entry rules:

Golden Cross between two Delta EMAs

Both Delta EMAs must be rising/falling

Enter on next bar

Stop:

10-15 pips or below Slow Delta EMA

Take Profit:

+1R to +2R

Or Death Cross

For whom: Scalpers on cryptocurrencies and forex

Pros:

Instant volatility adaptation

Many signals on volatile markets

Quick results

Cons:

Much noise on calm markets

Requires fast execution

High commissions may eat profits

Strategy 5: "Cyclical Trader"

Idea: Use Pi and Lambda for trading cyclical markets

Settings:

Fast: Pi Circular (1Pi)

Mid: Lambda Wave (Base 30, Amplitude 0.5, Frequency 50)

Slow: Pi Circular (3Pi)

Base Multiplier: 10

Timeframe: H1, H4

Entry rules:

STRONG signal active

Lambda Wave EMA synchronized with trend

Enter on bounce from Lambda Wave

For whom: Traders of cyclical assets (some altcoins, commodities)

Pros:

Catches cyclical movements

Lambda Wave provides additional entry points

Cons:

More complex to configure

Not for all markets

Lambda Wave may give false signals

Strategy 6: "Multi-Timeframe Confirmation"

Idea: Use multiple timeframes for confirmation

Scheme:

Higher TF (D1): Determine trend direction (STRONG signal)

Middle TF (H4): Wait for STRONG signal in same direction

Lower TF (M15): Look for entry point (Golden Cross or bounce from Fast EMA)

Settings for all TFs:

Fast: Phi Golden (Phi³)

Mid: e Natural (e²)

Slow: Pi Circular (2Pi)

Base Multiplier: 10

Rules:

All 3 TFs must show one trend

Entry on lower TF

Stop by lower TF

Target by higher TF

For whom: Serious traders and investors

Pros:

Maximum reliability

Large profit targets

Minimum false signals

Cons:

Rare setups

Requires analysis of multiple charts

Experience needed

Practical Tips

DOs

Use STRONG signals as primary - they're most reliable

Let signals develop - don't exit on first pullback

Use trailing stop - follow Fast EMA

Combine with levels - S/R, Fibonacci, volumes

Test on demo before real

Adjust Base Multiplier for your timeframe

Enable visual effects - they help see the picture

Use Info Table - quick situation assessment

Watch Pulsing Bar - instant state indicator

Trust auto-sorting of Fast/Mid/Slow

DON'Ts

Don't trade against STRONG signal - trend is your friend

Don't ignore Mid EMA - it adds reliability

Don't use too small Base Multiplier on higher TFs

Don't enter on Golden Cross in range - check for trend

Don't change settings during open position

Don't forget risk management - 1-2% per trade

Don't trade all signals in row - choose best ones

Don't use indicator in isolation - combine with Price Action

Don't set too tight stops - let trade breathe

Don't over-optimize - simplicity = reliability

Optimal Settings by Asset

US Stocks (SPY, AAPL, TSLA)

Recommendation:

Fast: Phi Golden (Phi³)

Mid: e Natural (e²)

Slow: Pi Circular (2Pi)

Base: 10-15

Timeframe: H4, D1

Features:

Use on daily for swing

STRONG signals very reliable

Works well on trending stocks

Forex (EUR/USD, GBP/USD)

Recommendation:

Fast: Delta Adaptive (Base 15, Sens 2.0)

Mid: Phi Golden (Phi²)

Slow: Pi Circular (2Pi)

Base: 8-12

Timeframe: M15, H1, H4

Features:

Delta Adaptive works excellently on news

Many signals on M15-H1

Consider spreads

Cryptocurrencies (BTC, ETH, altcoins)

Recommendation:

Fast: Delta Adaptive (Base 10, Sens 3.0)

Mid: Pi Circular (2Pi)

Slow: e Natural (e²)

Base: 5-10

Timeframe: M5, M15, H1

Features:

High volatility - adaptation needed

STRONG signals can last days

Be careful with scalping on M1-M5

Commodities (Gold, Oil)

Recommendation:

Fast: Pi Circular (1Pi)

Mid: Phi Golden (Phi³)

Slow: Pi Circular (3Pi)

Base: 12-18

Timeframe: H4, D1

Features:

Pi works excellently on cyclical commodities

Gold responds especially well to Phi

Oil volatile - use wide stops

Indices (S&P500, Nasdaq, DAX)

Recommendation:

Fast: Phi Golden (Phi³)

Mid: e Natural (e²)

Slow: Pi Circular (2Pi)

Base: 15-20

Timeframe: H4, D1, W1

Features:

Very trending instruments

STRONG signals last weeks

Good for position trading

Alerts

The indicator supports 6 alert types:

1. Golden Cross

Message: "Hellenic Matrix: GOLDEN CROSS - Fast EMA crossed above Slow EMA - Bullish trend starting!"

When: Fast EMA crosses Slow EMA from below

2. Death Cross

Message: "Hellenic Matrix: DEATH CROSS - Fast EMA crossed below Slow EMA - Bearish trend starting!"

When: Fast EMA crosses Slow EMA from above

3. STRONG BULLISH

Message: "Hellenic Matrix: STRONG BULLISH SIGNAL - All EMAs aligned for powerful uptrend!"

When: All conditions for STRONG BUY met (first bar)

4. STRONG BEARISH

Message: "Hellenic Matrix: STRONG BEARISH SIGNAL - All EMAs aligned for powerful downtrend!"

When: All conditions for STRONG SELL met (first bar)

5. Bullish Ribbon

Message: "Hellenic Matrix: BULLISH RIBBON - EMAs aligned for uptrend"

When: EMAs aligned bullish + price above Fast EMA (less strict condition)

6. Bearish Ribbon

Message: "Hellenic Matrix: BEARISH RIBBON - EMAs aligned for downtrend"

When: EMAs aligned bearish + price below Fast EMA (less strict condition)

How to Set Up Alerts:

Open indicator on chart

Click on three dots next to indicator name

Select "Create Alert"

In "Condition" field select needed alert:

Golden Cross

Death Cross

STRONG BULLISH

STRONG BEARISH

Bullish Ribbon

Bearish Ribbon

Configure notification method:

Pop-up in browser

Email

SMS (in Premium accounts)

Push notifications in mobile app

Webhook (for automation)

Select frequency:

Once Per Bar Close (recommended) - once on bar close

Once Per Bar - during bar formation

Only Once - only first time

Click "Create"

Tip: Create separate alerts for different timeframes and instruments

FAQ

1. Why don't STRONG signals appear?

Possible reasons:

Incorrect Fast/Mid/Slow order

Solution: Indicator automatically sorts EMAs by periods, but ensure selected EMAs have different periods

Base Multiplier too large

Solution: Reduce Base to 5-10 on lower timeframes

Market in range

Solution: STRONG signals appear only in trends - this is normal

Too strict EMA settings

Solution: Try classic combination: Phi³ / Pi×2 / e² with Base=10

Mid EMA too close to Fast or Slow

Solution: Select Mid EMA with period between Fast and Slow

2. How often should STRONG signals appear?

Normal frequency:

M1-M5: 5-15 signals per day (very active markets)

M15-H1: 2-8 signals per day

H4: 3-10 signals per week

D1: 2-5 signals per month

W1: 2-6 signals per year

If too many signals - market very volatile or Base too small

If too few signals - market in range or Base too large

4. What are the best settings for beginners?

Universal "out of the box" settings:

Matrix Core:

Base Multiplier: 10

Source: close

Phi Golden: Enabled, Power = 3

Pi Circular: Enabled, Multiple = 2

e Natural: Enabled, Power = 2

Delta Adaptive: Enabled, Base = 20, Sensitivity = 2.0

Manual Selection:

Fast: Phi Golden

Mid: e Natural

Slow: Pi Circular

Visualization:

Gradient Clouds: ON

Neon Glow: ON (Medium)

Pulsing Bar: ON (Medium)

Signal Highlights: ON (Light Fill)

Table: ON (Top Right, Small)

Signals:

Golden/Death Cross: ON

STRONG Signals: ON

Stop Loss: OFF (while learning)

Timeframe for learning: H1 or H4

5. Can I use only one EMA?

No, minimum 2 EMAs (Fast and Slow) for signal generation.

Mid EMA is optional:

With Mid EMA = more reliable but rarer signals

Without Mid EMA = more signals but less strict filtering

Recommendation: Start with 3 EMAs (Fast/Mid/Slow), then experiment

6. Does the indicator work on cryptocurrencies?

Yes, works excellently! Especially good on:

Bitcoin (BTC)

Ethereum (ETH)

Major altcoins (SOL, BNB, XRP)

Recommended settings for crypto:

Fast: Delta Adaptive (Base 10-15, Sensitivity 2.5-3.0)

Mid: Pi Circular (2Pi)

Slow: e Natural (e²)

Base: 5-10

Timeframe: M15, H1, H4

Crypto market features:

High volatility → use Delta Adaptive

24/7 trading → set alerts

Sharp movements → wide stops

7. Can I trade only with this indicator?

Technically yes, but NOT recommended.

Best approach - combine with:

Price Action - support/resistance levels, candle patterns

Volume - movement strength confirmation

Fibonacci - retracement and extension levels

RSI/MACD - divergences and overbought/oversold

Fundamental analysis - news, company reports

Hellenic Matrix:

Excellently determines trend and its strength

Provides clear entry/exit points

Doesn't consider fundamentals

Doesn't see major levels

8. Why do Gradient Clouds change color?

Color depends on EMA order:

Phi-Pi Cloud:

Blue - Pi EMA above Phi EMA (bullish alignment)

Gold - Phi EMA above Pi EMA (bearish alignment)

Pi-e Cloud:

Green - e EMA above Pi EMA (bullish alignment)

Blue - Pi EMA above e EMA (bearish alignment)

Color change = EMA order change = possible trend change

9. What is Momentum % in the table?

Momentum % = percentage deviation of price from Fast EMA

Formula:

Momentum = ((Close - Fast EMA) / Fast EMA) × 100

Interpretation:

+0.5% to +2% - normal bullish momentum

+2% to +5% - strong bullish momentum

+5% and above - overheating (correction possible)

-0.5% to -2% - normal bearish momentum

-2% to -5% - strong bearish momentum

-5% and below - oversold (bounce possible)

Usage:

Monitor momentum during STRONG signals

Large momentum = don't enter (wait for pullback)

Small momentum = good entry point

10. How to configure for scalping?

Settings for scalping (M1-M5):

Base Multiplier: 3-5

Source: close or hlc3 (smoother)

Fast: Delta Adaptive (Base 8-12, Sensitivity 3.0)

Mid: None (for more signals)

Slow: Phi Golden (Phi²) or Pi Circular (1Pi)

Visualization:

- Gradient Clouds: ON (helps see strength)

- Neon Glow: OFF (doesn't clutter chart)

- Pulsing Bar: ON (quick assessment)

- Signal Highlights: ON

Signals:

- Golden/Death Cross: ON

- STRONG Signals: ON

- Stop Loss: ON (1.0-1.5 ATR, R:R 1.5-2.0)

Scalping rules:

Trade only STRONG signals

Enter on bounce from Fast EMA

Tight stops (10-20 pips)

Quick take profit (+1R to +2R)

Don't hold through news

11. How to configure for long-term investing?

Settings for investing (D1-W1):

Base Multiplier: 20-30

Source: close

Fast: Phi Golden (Phi³ or Phi⁴)

Mid: e Natural (e²)

Slow: Pi Circular (3Pi or 4Pi)

Visualization:

- Gradient Clouds: ON

- Neon Glow: ON (Medium)

- Everything else - to taste

Signals:

- Golden/Death Cross: ON

- STRONG Signals: ON

- Stop Loss: OFF (use percentage stop)

Investing rules:

Enter only on STRONG signals

Hold while STRONG active (weeks/months)

Stop below Slow EMA or -10%

Take profit: by company targets or +50-100%

Ignore short-term pullbacks

12. What if indicator slows down chart?

Indicator is optimized, but if it slows:

Disable unnecessary visual effects:

Neon Glow: OFF (saves 8 plots)

Gradient Clouds: ON but low quality

Lambda Wave EMA: OFF (if not using)

Reduce number of active EMAs:

Sigma Composite: OFF

Lambda Wave: OFF

Leave only Phi, Pi, e, Delta

Simplify settings:

Pulsing Bar: OFF

Greek Labels: OFF

Info Table: smaller size

13. Can I use on different timeframes simultaneously?

Yes! Multi-timeframe analysis is very powerful:

Classic scheme:

Higher TF (D1, W1) - determine global trend

Wait for STRONG signal

This is our trading direction

Middle TF (H4, H1) - look for confirmation

STRONG signal in same direction

Precise entry zone

Lower TF (M15, M5) - entry point

Golden Cross or bounce from Fast EMA

Precise stop loss

Example:

W1: STRONG BUY active (global uptrend)

H4: STRONG BUY appeared (confirmation)

M15: Wait for Golden Cross or bounce from Fast EMA → ENTRY

Advantages:

Maximum reliability

Clear timeframe hierarchy

Large targets

14. How does indicator work on news?

Delta Adaptive EMA adapts excellently to news:

Before news:

Low volatility → Delta EMA becomes fast → pulls to price

During news:

Sharp volatility spike → Delta EMA slows → filters noise

After news:

Volatility normalizes → Delta EMA returns to normal

Recommendations:

Don't trade at news release moment (spreads widen)

Wait for STRONG signal after news (2-5 bars)

Use Delta Adaptive as Fast EMA for quick reaction

Widen stops by 50-100% during important news

Advanced Techniques

Technique 1: "Divergences with EMA"

Idea: Look for discrepancies between price and Fast EMA

Bullish divergence:

Price makes lower low

Fast EMA makes higher low

= Possible reversal up

Bearish divergence:

Price makes higher high

Fast EMA makes lower high

= Possible reversal down

How to trade:

Find divergence

Wait for STRONG signal in divergence direction

Enter on confirmation

Technique 2: "EMA Tunnel"

Idea: Use space between Fast and Slow EMA as "tunnel"

Rules:

Wide tunnel - strong trend, hold position

Narrow tunnel - weak trend or consolidation, caution

Tunnel narrowing - trend weakening, prepare to exit

Tunnel widening - trend strengthening, can add

Visually: Gradient Clouds show this automatically!

Trading:

Enter on STRONG signal (tunnel starts widening)

Hold while tunnel wide

Exit when tunnel starts narrowing

Technique 3: "Wave Analysis with Lambda"

Idea: Lambda Wave EMA creates sinusoid matching market cycles

Setup:

Lambda Base Period: 30

Lambda Wave Amplitude: 0.5

Lambda Wave Frequency: 50 (adjusted to asset cycle)

How to find correct Frequency:

Look at historical cycles (distance between local highs)

Average distance = your Frequency

Example: if highs every 40-60 bars, set Frequency = 50

Trading:

Enter when Lambda Wave at bottom of sinusoid (growth potential)

Exit when Lambda Wave at top (fall potential)

Combine with STRONG signals

Technique 4: "Cluster Analysis"

Idea: When all EMAs gather in narrow cluster = powerful breakout soon

Cluster signs:

All EMAs (Phi, Pi, e, Delta) within 0.5-1% of each other

Gradient Clouds almost invisible

Price jumping around all EMAs

Trading:

Identify cluster (all EMAs close)

Determine breakout direction (where more volume, higher TFs direction)

Wait for breakout and STRONG signal

Enter on confirmation

Target = cluster size × 3-5

This is very powerful technique for big moves!

Technique 5: "Sigma as Dynamic Level"

Idea: Sigma Composite EMA = average of all EMAs = magnetic level

Usage:

Enable Sigma Composite (Weighted Average)

Sigma works as dynamic support/resistance

Price often returns to Sigma before trend continuation

Trading:

In trend: Enter on bounces from Sigma

In range: Fade moves from Sigma (trade return to Sigma)

On breakout: Sigma becomes support/resistance

Risk Management

Basic Rules

1. Position Size

Conservative: 1% of capital per trade

Moderate: 2% of capital per trade (recommended)

Aggressive: 3-5% (only for experienced)

Calculation formula:

Lot Size = (Capital × Risk%) / (Stop in pips × Pip value)

2. Risk/Reward Ratio

Minimum: 1:1.5

Standard: 1:2 (recommended)

Optimal: 1:3

Aggressive: 1:5+

3. Maximum Drawdown

Daily: -3% to -5%

Weekly: -7% to -10%

Monthly: -15% to -20%

Upon reaching limit → STOP trading until end of period

Position Management Strategies

1. Fixed Stop

Method:

Stop below/above Fast EMA or local extreme

DON'T move stop against position

Can move to breakeven

For whom: Beginners, conservative traders

2. Trailing by Fast EMA

Method:

Each day (or bar) move stop to Fast EMA level

Position closes when price breaks Fast EMA

Advantages:

Stay in trend as long as possible

Automatically exit on reversal

For whom: Trend followers, swing traders

3. Partial Exit

Method:

50% of position close at +2R

50% hold with trailing by Mid EMA or Slow EMA

Advantages:

Lock profit

Leave position for big move

Psychologically comfortable

For whom: Universal method (recommended)

4. Pyramiding

Method:

First entry on STRONG signal (50% of planned position)

Add 25% on pullback to Fast EMA

Add another 25% on pullback to Mid EMA

Overall stop below Slow EMA

Advantages:

Average entry price

Reduce risk

Increase profit in strong trends

Caution:

Works only in trends

In range leads to losses

For whom: Experienced traders

Trading Psychology

Correct Mindset

1. Indicator is a tool, not holy grail

Indicator shows probability, not guarantee

There will be losing trades - this is normal

Important is series statistics, not one trade

2. Trust the system

If STRONG signal appeared - enter

Don't search for "perfect" moment

Follow trading plan

3. Patience

STRONG signals don't appear every day

Better miss signal than enter against trend

Quality over quantity

4. Discipline

Always set stop loss

Don't move stop against position

Don't increase risk after losses

Beginner Mistakes

1. "I know better than indicator"

Indicator says STRONG BUY, but you think "too high, will wait for pullback"

Result: miss profitable move

Solution: Trust signals or don't use indicator

2. "Will reverse now for sure"

Trading against STRONG trend

Result: stops, stops, stops

Solution: Trend is your friend, trade with trend

3. "Will hold a bit more"

Don't exit when STRONG signal disappears

Greed eats profit

Solution: If signal gone - exit!

4. "I'll recover"

After losses double risk

Result: huge losses

Solution: Fixed % risk ALWAYS

5. "I don't like this signal"

Skip signals because of "feeling"

Result: inconsistency, no statistics

Solution: Trade ALL signals or clearly define filters

Trading Journal

What to Record

For each trade:

1. Entry/exit date and time

2. Instrument and timeframe

3. Signal type

Golden Cross

STRONG BUY

STRONG SELL

Death Cross

4. Indicator settings

Fast/Mid/Slow EMA

Base Multiplier

Other parameters

5. Chart screenshot

Entry moment

Exit moment

6. Trade parameters

Position size

Stop loss

Take Profit

R:R

7. Result

Profit/Loss in $

Profit/Loss in %

Profit/Loss in R

8. Notes

What was right

What was wrong

Emotions during trade

Lessons

Journal Analysis

Analyze weekly:

1. Win Rate

Win Rate = (Profitable trades / All trades) × 100%

Good: 50-60%

Excellent: 60-70%

Exceptional: 70%+

2. Average R

Average R = Sum of all R / Number of trades

Good: +0.5R

Excellent: +1.0R

Exceptional: +1.5R+

3. Profit Factor

Profit Factor = Total profit / Total losses

Good: 1.5+

Excellent: 2.0+

Exceptional: 3.0+

4. Maximum Drawdown

Track consecutive losses

If more than 5 in row - stop, check system

5. Best/Worst Trades

What was common in best trades? (do more)

What was common in worst trades? (avoid)

Pre-Trade Checklist

Technical Analysis

STRONG signal active (BUY or SELL)

All EMAs properly aligned (Fast > Mid > Slow or reverse)

Price on correct side of Fast EMA

Gradient Clouds confirm trend

Pulsing Bar shows STRONG state

Momentum % in normal range (not overheated)

No close strong levels against direction

Higher timeframe doesn't contradict

Risk Management

Position size calculated (1-2% risk)

Stop loss set

Take profit calculated (minimum 1:2)

R:R satisfactory

Daily/weekly risk limit not exceeded

No other open correlated positions

Fundamental Analysis

No important news in coming hours

Market session appropriate (liquidity)

No contradicting fundamentals

Understand why asset is moving

Psychology

Calm and thinking clearly

No emotions from previous trades

Ready to accept loss at stop

Following trading plan

Not revenging market for past losses

If at least one point is NO - think twice before entering!

Learning Roadmap

Week 1: Familiarization

Goals:

Install and configure indicator

Study all EMA types

Understand visualization

Tasks:

Add indicator to chart

Test all Fast/Mid/Slow settings

Play with Base Multiplier on different timeframes

Observe Gradient Clouds and Pulsing Bar

Study Info Table

Result: Comfort with indicator interface

Week 2: Signals

Goals:

Learn to recognize all signal types

Understand difference between Golden Cross and STRONG

Tasks:

Find 10 Golden Cross examples in history

Find 10 STRONG BUY examples in history

Compare their results (which worked better)

Set up alerts

Get 5 real alerts

Result: Understanding signals

Week 3: Demo Trading

Goals:

Start trading signals on demo account

Gather statistics

Tasks:

Open demo account

Trade ONLY STRONG signals

Keep journal (minimum 20 trades)

Don't change indicator settings

Strictly follow stop losses

Result: 20+ documented trades

Week 4: Analysis

Goals:

Analyze demo trading results

Optimize approach

Tasks:

Calculate win rate and average R

Find patterns in profitable trades

Find patterns in losing trades

Adjust approach (not indicator!)

Write trading plan

Result: Trading plan on 1 page

Month 2: Improvement

Goals:

Deepen understanding

Add additional techniques

Tasks:

Study multi-timeframe analysis

Test combinations with Price Action

Try advanced techniques (divergences, tunnels)

Continue demo trading (minimum 50 trades)

Achieve stable profitability on demo

Result: Win rate 55%+ and Profit Factor 1.5+

Month 3: Real Trading

Goals:

Transition to real account

Maintain discipline

Tasks:

Open small real account

Trade minimum lots

Strictly follow trading plan

DON'T increase risk

Focus on process, not profit

Result: Psychological comfort on real

Month 4+: Scaling

Goals:

Increase account

Become consistently profitable

Tasks:

With 60%+ win rate can increase risk to 2%

Upon doubling account can add capital

Continue keeping journal

Periodically review and improve strategy

Share experience with community

Result: Stable profitability month after month

Additional Resources

Recommended Reading

Technical Analysis:

"Technical Analysis of Financial Markets" - John Murphy

"Trading in the Zone" - Mark Douglas (psychology)

"Market Wizards" - Jack Schwager (trader interviews)

EMA and Moving Averages:

"Moving Averages 101" - Steve Burns

Articles on Investopedia about EMA

Risk Management:

"The Mathematics of Money Management" - Ralph Vince

"Trade Your Way to Financial Freedom" - Van K. Tharp

Trading Journals:

Edgewonk (paid, very powerful)

Tradervue (free version + premium)

Excel/Google Sheets (free)

Screeners:

TradingView Stock Screener

Finviz (stocks)

CoinMarketCap (crypto)

Conclusion

Hellenic EMA Matrix is a powerful tool based on universal mathematical constants of nature. The indicator combines:

Mathematical elegance - Phi, Pi, e instead of arbitrary numbers

Premium visualization - Neon Glow, Gradient Clouds, Pulsing Bar

Reliable signals - STRONG BUY/SELL work on all timeframes

Flexibility - 6 EMA types, adaptation to any trading style

Automation - auto-sorting EMAs, SL/TP calculation, alerts

Key Success Principles:

Simplicity - start with basic settings (Phi/Pi/e, Base=10)

Discipline - follow STRONG signals strictly

Patience - wait for quality setups

Risk Management - 1-2% per trade, ALWAYS

Journal - document every trade

Learning - constantly improve skills

Remember:

Indicator shows probability, not guarantee

Important is series statistics, not one trade

Psychology more important than technique

Quality more important than quantity

Process more important than result

Acknowledgments

Thank you for using Hellenic EMA Matrix - Alpha Omega Premium!

The indicator was created with love for mathematics, markets, and beautiful visualization.

Wishing you profitable trading!

Guide Version: 1.0

Date: 2025

Compatibility: Pine Script v6, TradingView

"In the simplicity of mathematical constants lies the complexity of market movements"

SulLaLuna — HTF M2 x Ultimate BB (Fusion) 🌕 **SulLaLuna — HTF M2 x Ultimate BB (Fusion)** 🚀💵

**By SulLaLuna Trading**

(Portions of the Bollinger Band logic adapted with permission/credit from the *Ultimate Buy & Sell Indicator* by its original author — thank you for the brilliance!)

---

🧭 **What This Is**

This is not just another price-following tool.

This is **a macro liquidity detector** — a **Daily Higher Timeframe Hull Moving Average of the Global M2 Money Supply**, smoothed via lower timeframe candles (default 5m, 48 Hull length), overlaid with **Ultimate-style double Bollinger Bands** to reveal *over-extension & mean reversion zones*.

It doesn’t chase candles.

It watches the tides beneath the market — the **money supply currents** that have a **direct correlation** to asset price behavior.

When liquidity expands → risk-on assets tend to rise.

When liquidity contracts → risk-off waves hit.

We ride those waves.

---

🔍 **What It Does**

* **Tracks Global M2** across major economies, FX-adjusted, and scales it to your chart’s price.

* **HTF Hull MA** (Daily, smoothed via 5m base) → gives you the macro liquidity trend.

* **Ultimate BB logic** applied to the HTF M2 Hull → inner/outer bands for volatility envelopes.

* **Pivot Labels** → ideal entry/exit zones on macro turns.

* **Over-Extension Alerts** → when HTF M2 Hull pushes outside the outer bands.

* **Re-Entry Alerts** → mean reversion triggers when liquidity moves back inside the range.

* **Background Paint** from chart TF M2 slope → for confluence on your entry timeframe.

---

📜 **Suggested How-To**

1. **Choose your execution chart** — e.g., 1–15m for scalps, 1H–4H for swings.

2. **Use the background paint** as your *local tide check* (chart TF M2 slope).

3. **Trade in the direction of the HTF M2 Hull** — green line = liquidity rising, red line = liquidity falling.

4. **Watch pivot labels** — these are potential “macro inflection” points.

5. **Confluence stack** — pair with ZLSMA, WaveTrend divergences, VWAP volume, or your favorite price-action setups.

6. **Size down** when HTF M2 Hull is flat/gray (chop zone).

7. **Scale in/out** on over-extension + re-entry alerts for higher probability swings.

---

⚠️ **Important Note**

This indicator **does not predict price** — it tracks macro liquidity flows that *influence* price.

Think of it as your market’s **tide chart**: when the water’s coming in, you can swim out; when it’s going out, you’d better be ready for the undertow.

---

📢 **Alerts Available**

* HTF Pivot HIGH / LOW

* Over-Extension (HTF Hull outside outer BB)

* Re-Entry (return from overbought/oversold)

---

🤝 **Join the SulLaLuna Tribe**

If this indicator helps you capture better entries, follow & share so more traders can learn to trade *math, not emotion*.

We rise together — **and we’ll meet you on the Moon** 🌕🚀💵.

Green*DiamondGreen*Diamond (GD1)

Unleash Dynamic Trading Signals with Volatility and Momentum

Overview

GreenDiamond is a versatile overlay indicator designed for traders seeking actionable buy and sell signals across various markets and timeframes. Combining Volatility Bands (VB) bands, Consolidation Detection, MACD, RSI, and a unique Ribbon Wave, it highlights high-probability setups while filtering out noise. With customizable signals like Green-Yellow Buy, Pullback Sell, and Inverse Pullback Buy, plus vibrant candle and volume visuals, GreenDiamond adapts to your trading style—whether you’re scalping, day trading, or swing trading.

Key Features

Volatility Bands (VB): Plots dynamic upper and lower bands to identify breakouts or reversals, with toggleable buy/sell signals outside consolidation zones.

Consolidation Detection: Marks low-range periods to avoid choppy markets, ensuring signals fire during trending conditions.

MACD Signals: Offers flexible buy/sell conditions (e.g., cross above signal, above zero, histogram up) with RSI divergence integration for precision.

RSI Filter: Enhances signals with customizable levels (midline, oversold/overbought) and bullish divergence detection.

Ribbon Wave: Visualizes trend strength using three EMAs, colored by MACD and RSI for intuitive momentum cues.

Custom Signals: Includes Green-Yellow Buy, Pullback Sell, and Inverse Pullback Buy, with limits on consecutive signals to prevent overtrading.

Candle & Volume Styling: Blends MACD/RSI colors on candles and scales volume bars to highlight momentum spikes.

Alerts: Set up alerts for VB signals, MACD crosses, Green*Diamond signals, and custom conditions to stay on top of opportunities.

How It Works

Green*Diamond integrates multiple indicators to generate signals:

Volatility Bands: Calculates bands using a pivot SMA and standard deviation. Buy signals trigger on crossovers above the lower band, sell signals on crossunders below the upper band (if enabled).

Consolidation Filter: Suppresses signals when candle ranges are below a threshold, keeping you out of flat markets.

MACD & RSI: Combines MACD conditions (e.g., cross above signal) with RSI filters (e.g., above midline) and optional volume spikes for robust signals.

Custom Logic: Green-Yellow Buy uses MACD bullishness, Pullback Sell targets retracements, and Inverse Pullback Buy catches reversals after downmoves—all filtered to avoid consolidation.

Visuals: Ribbon Wave shows trend direction, candles blend momentum colors, and volume bars scale dynamically to confirm signals.

Settings

Volatility Bands Settings:

VB Lookback Period (20): Adjust to 10–15 for faster markets (e.g., 1-minute scalping) or 25–30 for daily charts.

Upper/Lower Band Multiplier (1.0): Increase to 1.5–2.0 for wider bands in volatile stocks like AEHL; decrease to 0.5 for calmer markets.

Show Volatility Bands: Toggle off to reduce chart clutter.

Use VB Signals: Enable for breakout-focused trades; disable to focus on Green*Diamond signals.

Consolidation Settings:

Consolidation Lookback (14): Set to 5–10 for small caps (e.g., AEHL) to catch quick consolidations; 20 for higher timeframes.

Range Threshold (0.5): Lower to 0.3 for stricter filtering in choppy markets; raise to 0.7 for looser signals.

MACD Settings:

Fast/Slow Length (12/26): Shorten to 8/21 for scalping; extend to 15/34 for swing trading.

Signal Smoothing (9): Reduce to 5 for faster signals; increase to 12 for smoother trends.

Buy/Sell Signal Options: Choose “Cross Above Signal” for classic MACD; “Histogram Up” for momentum plays.

Use RSI Div + MACD Cross: Enable for high-probability reversal signals.

RSI Settings:

RSI Period (14): Drop to 10 for 1-minute charts; raise to 20 for daily.

Filter Level (50): Set to 55 for stricter buys; 45 for sells.

Overbought/Oversold (70/30): Tighten to 65/35 for small caps; widen to 75/25 for indices.

RSI Buy/Sell Options: Select “Bullish Divergence” for reversals; “Cross Above Oversold” for momentum.

Color Settings:

Adjust bullish/bearish colors for visibility (e.g., brighter green/red for dark themes).

Border Thickness (1): Increase to 2–3 for clearer candle outlines.

Volume Settings:

Volume Average Length (20): Shorten to 10 for scalping; extend to 30 for swing trades.

Volume Multiplier (2.0): Raise to 3.0 for AEHL’s volume surges; lower to 1.5 for steady stocks.

Bar Height (10%): Increase to 15% for prominent bars; decrease to 5% to reduce clutter.

Ribbon Settings:

EMA Periods (10/20/30): Tighten to 5/10/15 for scalping; widen to 20/40/60 for trends.

Color by MACD/RSI: Disable for simpler visuals; enable for dynamic momentum cues.

Gradient Fill: Toggle on for trend clarity; off for minimalism.

Custom Signals:

Enable Green-Yellow Buy: Use for momentum confirmation; limit to 1–2 signals to avoid spam.

Pullback/Inverse Pullback % (50): Set to 30–40% for small caps; 60–70% for indices.

Max Buy Signals (1): Increase to 2–3 for active markets; keep at 1 for discipline.

Tips and Tricks

Scalping Small Caps (e.g., AEHL):

Use 1-minute charts with VB Lookback = 10, Consolidation Lookback = 5, and Volume Multiplier = 3.0 to catch $0.10–$0.20 moves.

Enable Green-Yellow Buy and Inverse Pullback Buy for quick entries; disable VB Signals to focus on Green*Diamond logic.

Pair with SMC+ green boxes (if you use them) for reversal confirmation.

Day Trading:

Try 5-minute charts with MACD Fast/Slow = 8/21 and RSI Period = 10.

Enable RSI Divergence + MACD Cross for high-probability setups; set Max Buy Signals = 2.

Watch for volume bars turning yellow to confirm entries.

Swing Trading:

Use daily charts with VB Lookback = 30, Ribbon EMAs = 20/40/60.

Enable Pullback Sell (60%) to exit after rallies; disable RSI Color for cleaner candles.

Check Ribbon Wave gradient for trend strength—bright green signals strong bulls.

Avoiding Noise:

Increase Consolidation Threshold to 0.7 on volatile days to skip false breakouts.

Disable Ribbon Wave or Volume Bars if the chart feels crowded.

Limit Max Buy Signals to 1 for disciplined trading.

Alert Setup:

In TradingView’s Alerts panel, select:

“GD Buy Signal” for standard entries.

“RSI Div + MACD Cross Buy” for reversals.

“VB Buy Signal” for breakout plays.

Set to “Once Per Bar Close” for confirmed signals; “Once Per Bar” for scalping.

Backtesting:

Replay on small caps ( Float < 5M, Price $0.50–$5) to test signals.

Focus on “GD Buy Signal” with yellow volume bars and green Ribbon Wave.

Avoid signals during gray consolidation squares unless paired with RSI Divergence.

Usage Notes

Markets: Works on stocks, forex, crypto, and indices. Best for volatile assets (e.g., small-cap stocks, BTCUSD).

Timeframes: Scalping (1–5 minutes), day trading (15–60 minutes), or swing trading (daily). Adjust settings per timeframe.

Risk Management: Combine with stop-losses (e.g., 1% risk, $0.05 below AEHL entry) and take-profits (3–5%).

Customization: Tweak inputs to match your strategy—experiment in replay to find your sweet spot.

Disclaimer

Green*Diamond is a technical tool to assist with trade identification, not a guarantee of profits. Trading involves risks, and past performance doesn’t predict future results. Always conduct your own analysis, manage risk, and test settings before live trading.

Feedback

Love Green*Diamond? Found a killer setup?

Long Term Profitable Swing | AbbasA Story of a Profitable Swing Trading Strategy

Imagine you're sailing across the ocean, looking for the perfect wave to ride. Swing trading is quite similar—you're navigating the stock market, searching for the ideal moments to enter and exit trades. This strategy, created by Abbas, helps you find those waves and ride them effectively to profitable outcomes.

🌊 Finding the Perfect Wave (Entry)

Our journey begins with two simple signs that tell us a great trading opportunity is forming:

- Moving Averages: We use two lines that follow price trends—the faster one (EMA 16) reacts quickly to recent price moves, and the slower one (EMA 30) gives us a longer-term perspective. When the faster line crosses above the slower line, it's like a clear signal saying, "Hey! The wave is rising, and prices might move higher!"

- RSI Momentum: Next, we check a tool called the RSI, which measures momentum (how strongly prices are moving). If the RSI number is above 50, it means there's enough strength behind this rising wave to carry us forward.

When both signals appear together, that's our green light. It's time to jump on our surfboard and start riding this promising wave.

⚓ Safely Riding the Wave (Risk Management)

While we're riding this wave, we want to ensure we're safe from sudden surprises. To do this, we use something called the Average True Range (ATR), which measures how volatile (or bumpy) the price movements are:

- Stop-Loss: To avoid falling too hard, we set a safety line (stop-loss) 8 times the ATR below our entry price. This helps ensure we exit if the wave suddenly turns against us, protecting us from heavy losses.

- Take Profit: We also set a goal to exit the trade at 11 times the ATR above our entry. This way, we capture significant profits when the wave reaches a nice high point.

🌟 Multiple Rides, Bigger Adventures

This strategy allows us to take multiple positions simultaneously—like riding several waves at once, up to 5. Each trade we make uses only 10% of our trading capital, keeping risks manageable and giving us multiple opportunities to win big.

🗺️ Easy to Follow Settings

Here are the basic settings we use:

- Fast EMA**: 16

- Slow EMA**: 30

- RSI Length**: 9

- RSI Threshold**: 50

- ATR Length**: 21

- ATR Stop-Loss Multiplier**: 8

- ATR Take-Profit Multiplier**: 11

These settings are flexible—you can adjust them to better suit different markets or your personal trading style.

🎉 Riding the Waves of Success

This simple yet powerful swing trading approach helps you confidently enter trades, clearly know when to exit, and effectively manage your risk. It’s a reliable way to ride market waves, capture profits, and minimize losses.

Happy trading, and may you find many profitable waves to ride! 🌊✨

Please test, and take into account that it depends on taking multiple longs within the swing, and you only get to invest 25/30% of your equity.

Multi-Timeframe Recursive Zigzag [Trendoscope®]🎲 Welcome to the Advanced World of Zigzag Analysis

Embark on a journey through the most comprehensive and feature-rich Zigzag implementation you’ll ever encounter. Our Multi-Timeframe Recursive Zigzag Indicator is not just another tool; it's a groundbreaking advancement in technical analysis.

🎯 Key Features

Multi Time-Frame Support - One of the rare open-source Zigzag indicators with robust multi-timeframe capabilities, this feature sets our tool apart, enabling a broader and more dynamic market analysis.

Innovative Recursive Zigzag Algorithm - At its core is our unique Recursive Zigzag Algorithm, a pioneering development that powers multiple Zigzag levels, offering an intricate view of market movements. This proprietary algorithm is the backbone of our advanced pattern recognition indicators.

Sub-Waves and Micro-Waves Analysis - Dive deeper into market trends with our Sub-Waves and Micro-Waves feature. Sub-Waves reveal the interconnectedness of various Zigzag levels, while Micro-Waves offer insight into the fundamental waves at the base level.

Enhanced Indicator Tracking - Integrate and track your custom indicators or oscillators with the zigzag, capturing their values at each Zigzag level, complete with retracement ratios. This offers a comprehensive view of market dynamics.

Curved Zigzag Visualization - Experience a new way of visualizing market movements with our Curved Zigzag Display, employing Pine Script’s polyline feature for a more intuitive and visually appealing representation.

Built-in Customizable Alerts - Stay ahead with built-in alerts that can be customized via user input settings.

🎯 Practical Applications

Our Zigzag Indicator is designed with an understanding of its inherent nature - the last unconfirmed pivot that consistently repaints. This characteristic, while by design, directs its usage more towards pattern recognition rather than direct identification of market tops and bottoms. Here's how you can leverage the Zigzag Indicator:

Harmonic Patterns - Ideal for those familiar with harmonic patterns, this tool simplifies the manual spotting of complex XABCD, ABC, and ABCD patterns on charts.

Chart Patterns - Effortlessly identify patterns like Double/Triple Taps, Head and Shoulders, Inverse Head and Shoulders, and Cup and Handle patterns with enhanced clarity. Navigate through challenging patterns such as Triangles, Wedges, Flags, and Price Channels, where the Zigzag Indicator adds a layer of precision to your breakout strategy.

Elliott Wave Components - The indicator's detailed pivot highlighting aids in identifying key Elliott Wave components, enhancing your wave analysis and decision-making process.

🎲 Deep Dive into Indicator Features

Join us as we explore the intricate features of our indicator in more detail.

🎯 Multi-Timeframe Capability

Our indicator comes equipped with an input option for selecting the desired resolution. This unique feature allows users to view higher timeframe Zigzag patterns directly on their lower timeframe charts.

🎯 Recursive Multi Level Zigzag

Our advanced recursive approach creates multi-level Zigzags from lower-level data. For instance, the level 0 Zigzag forms the base, calculated from specified length and depth parameters, while level 1 Zigzag is derived using level 0 as its foundation, and so forth.

The indicator not only displays multiple Zigzag levels but also offers settings to emphasize specific levels for more detailed analysis.

🎯 Sub-Components and Micro-Components of Zigzag Wave

Sub-components within a Zigzag wave consist of the previous level's Zigzag pivots. Meanwhile, the micro-components are composed of the base level (Level 0) Zigzag pivots encapsulated within the wave.

🎯 Curved Zigzag

Experience a new perspective with our curved Zigzag display. This innovative feature utilizes the polyline curved option to automatically generate sinusoidal waves based on multiple points.

🎯 Indicator Tracking

Default indicators such as RSI, MFI, and OBV are included, alongside the ability to track one external indicator at each Zigzag pivot.

🎯 Customizable Alerts

Our indicator employs the `alert()` function for alert creation. While this means the absence of a customization text box in the alert settings, we've included a custom text area for users to create their own alert templates.

Template placeholders include:

{alertType} - type of alert. Either Confirmed Pivot Update or Last Pivot Update. Depends on the alert type selected in the inputs.

When Last Pivot Update type is selected, the alerts are triggered whenever there is a new Zigzag Pivot. This may also be a repaint of last unconfirmed pivot.

When Confirmed Pivot Update type is selected, the alerts are triggered only when a pivot becomes a confirmed pivot.

{level} - Zigzag level on which the alert is triggered.

{pivot} - Details of the last pivot or confirmed pivot including price, ratio, indicator values and ratios, subcomponent and micro-component pivots.

🎲 User Settings Overview

🎯 Zigzag and Generic Settings

This involves some generic zigzag calculation settings such as length, depth, and timeframe. And few display options such as theme, Highlight Level and Curved Zigzag. By default, zigzag calculation is done based on the latest real time bar. An option is provided to disable this and use only confirmed bars for the calculation.

Indicator Settings

Allows users to track one or more oscillators or volume indicators. Option to add any indicator via external input is provided.

🎯 Alert Settings