Previous Week & Day High/LowPrevious Week & Day High/Low Indicator

The Previous Week & Day High/Low Indicator is designed to provide traders with key support and resistance levels based on historical price data. It automatically plots the previous day's and previous week's highs and lows as horizontal lines, offering a clear visual reference for potential breakout or reversal zones.

Features:

Clear Visual Levels: Displays previous day's highs and lows in green and red for easy identification.

Weekly Context: Plots previous week's highs and lows using distinct color-coded lines.

Real-Time Updates: Adjusts to new weekly and daily highs and lows as they are confirmed.

Labeled Lines: Each level is labeled directly on the chart, ensuring clarity without clutter.

Cerca negli script per "weekly"

EMA 10/55/200 - LONG ONLY MTF (4h with 1D & 1W confirmation)Title: EMA 10/55/200 - Long Only Multi-Timeframe Strategy (4h with 1D & 1W confirmation)

Description:

This strategy is designed for trend-following long entries using a combination of exponential moving averages (EMAs) on the 4-hour chart, confirmed by higher timeframe trends from the daily (1D) and weekly (1W) charts.

🔍 How It Works

🔹 Entry Conditions (4h chart):

EMA 10 crosses above EMA 55 and price is above EMA 55

OR

EMA 55 crosses above EMA 200

OR

EMA 10 crosses above EMA 500

These entries indicate short-term momentum aligning with medium/long-term trend strength.

🔹 Confirmation (multi-timeframe alignment):

Daily (1D): EMA 55 is above EMA 200

Weekly (1W): EMA 55 is above EMA 200

This ensures that we only enter long trades when the higher timeframes support an uptrend, reducing false signals during sideways or bearish markets.

🛑 Exit Conditions

Bearish crossover of EMA 10 below EMA 200 or EMA 500

Stop Loss: 5% below entry price

⚙️ Backtest Settings

Capital allocation per trade: 10% of equity

Commission: 0.1%

Slippage: 2 ticks

These are realistic conditions for crypto, forex, and stocks.

📈 Best Used On

Timeframe: 4h

Instruments: Trending markets like BTC/ETH, FX majors, or growth stocks

Works best in volatile or trending environments

⚠️ Disclaimer

This is a backtest tool and educational resource. Always validate on demo accounts before applying to real capital. Do your own due diligence.

Cartera SuperTrends v4 PublicDescription

This script creates a screener with a list of ETFs ordered by their average ROC in three different periods representing 4, 6 and 8 months by default. The ETF

BIL

is always included as a reference.

The previous average ROC value shows the calculation using the closing price from last month.

The current average ROC value shows the calculation using the current price.

The previous average column background color represents if the ETF average ROC is positive or negative.

The current average column background color represents if the ETF average ROC is positive or negative.

The current average column letters color represents if the current ETF average ROC is improving or not from the previous month.

Changes from V2 to V3

Added the option to make the calculation monthly, weekly or daily

Changes from V3 to V4

Adding up to 25 symbols

Highlight the number of tickers selected

Highlight the sorted column

Complete refactor of the code using a matrix of arrays

Options

The options available are:

Make the calculation monthly, weekly or daily

Adjust Data for Dividends

Manual calculation instead of using ta.roc function

Sort table

Sort table by the previous average ROC or the current average ROC

Number of tickers selected to highlight

First Period in months, weeks or days

Second Period in months, weeks or days

Third Period in months, weeks or days

Select the assets (max 25)

Usage

Just add the indicator to your favorite indicators and then add it to your chart.

Pivot S/R with Volatility Filter## *📌 Indicator Purpose*

This indicator identifies *key support/resistance levels* using pivot points while also:

✅ Detecting *high-volume liquidity traps* (stop hunts)

✅ Filtering insignificant pivots via *ATR (Average True Range) volatility*

✅ Tracking *test counts and breakouts* to measure level strength

---

## *⚙ SETTINGS – Detailed Breakdown*

### *1️⃣ ◆ General Settings*

#### *🔹 Pivot Length*

- *Purpose:* Determines how many bars to analyze when identifying pivots.

- *Usage:*

- *Low values (5-20):* More pivots, better for scalping.

- *High values (50-200):* Fewer but stronger levels for swing trading.

- *Example:*

- Pivot Length = 50 → Only the most significant highs/lows over 50 bars are marked.

#### *🔹 Test Threshold (Max Test Count)*

- *Purpose:* Sets how many times a level can be tested before being invalidated.

- *Example:*

- Test Threshold = 3 → After 3 tests, the level is ignored (likely to break).

#### *🔹 Zone Range*

- *Purpose:* Creates a price buffer around pivots (±0.001 by default).

- *Why?* Markets often respect "zones" rather than exact prices.

---

### *2️⃣ ◆ Volatility Filter (ATR)*

#### *🔹 ATR Period*

- *Purpose:* Smoothing period for Average True Range calculation.

- *Default:* 14 (standard for volatility measurement).

#### *🔹 ATR Multiplier (Min Move)*

- *Purpose:* Requires pivots to show *meaningful price movement*.

- *Formula:* Min Move = ATR × Multiplier

- *Example:*

- ATR = 10 pips, Multiplier = 1.5 → Only pivots with *15+ pip swings* are valid.

#### *🔹 Show ATR Filter Info*

- Displays current ATR and minimum move requirements on the chart.

---

### *3️⃣ ◆ Volume Analysis*

#### *🔹 Volume Change Threshold (%)*

- *Purpose:* Filters for *unusual volume spikes* (institutional activity).

- *Example:*

- Threshold = 1.2 → Requires *120% of average volume* to confirm signals.

#### *🔹 Volume MA Period*

- *Purpose:* Lookback period for "normal" volume calculation.

---

### *4️⃣ ◆ Wick Analysis*

#### *🔹 Wick Length Threshold (Ratio)*

- *Purpose:* Ensures rejection candles have *long wicks* (strong reversals).

- *Formula:* Wick Ratio = (Upper Wick + Lower Wick) / Candle Range

- *Example:*

- Threshold = 0.6 → 60% of the candle must be wicks.

#### *🔹 Min Wick Size (ATR %)*

- *Purpose:* Filters out small wicks in volatile markets.

- *Example:*

- ATR = 20 pips, MinWickSize = 1% → Wicks under *0.2 pips* are ignored.

---

### *5️⃣ ◆ Display Settings*

- *Show Zones:* Toggles support/resistance shaded areas.

- *Show Traps:* Highlights liquidity traps (▲/▼ symbols).

- *Show Tests:* Displays how many times levels were tested.

- *Zone Transparency:* Adjusts opacity of zones.

---

## *🎯 Practical Use Cases*

### *1️⃣ Liquidity Trap Detection*

- *Scenario:* Price spikes *above resistance* then reverses sharply.

- *Requirements:*

- Long wick (Wick Ratio > 0.6)

- High volume (Volume > Threshold)

- *Outcome:* *Short Trap* signal (▼) appears.

### *2️⃣ Strong Support Level*

- *Scenario:* Price bounces *3 times* from the same level.

- *Indicator Action:*

- Labels the level with test count (3/5 = 3 tests out of max 5).

- Turns *red* if broken (Break Count > 0).

Deep Dive: How This Indicator Works*

This indicator combines *four professional trading concepts* into one powerful tool:

1. *Classic Pivot Point Theory*

- Identifies swing highs/lows where price previously reversed

- Unlike basic pivot indicators, ours uses *confirmed pivots only* (filtered by ATR)

2. *Volume-Weighted Validation*

- Requires unusual trading volume to confirm levels

- Filters out "phantom" levels with low participation

3. *ATR Volatility Filtering*

- Eliminates insignificant price swings in choppy markets

- Ensures only meaningful levels are plotted

4. *Liquidity Trap Detection*

- Spots institutional stop hunts where markets fake out traders

- Uses wick analysis + volume spikes for high-probability signals

---

Deep Dive: How This Indicator Works*

This indicator combines *four professional trading concepts* into one powerful tool:

1. *Classic Pivot Point Theory*

- Identifies swing highs/lows where price previously reversed

- Unlike basic pivot indicators, ours uses *confirmed pivots only* (filtered by ATR)

2. *Volume-Weighted Validation*

- Requires unusual trading volume to confirm levels

- Filters out "phantom" levels with low participation

3. *ATR Volatility Filtering*

- Eliminates insignificant price swings in choppy markets

- Ensures only meaningful levels are plotted

4. *Liquidity Trap Detection*

- Spots institutional stop hunts where markets fake out traders

- Uses wick analysis + volume spikes for high-probability signals

---

## *📊 Parameter Encyclopedia (Expanded)*

### *1️⃣ Pivot Engine Settings*

#### *Pivot Length (50)*

- *What It Does:*

Determines how many bars to analyze when searching for swing highs/lows.

- *Professional Adjustment Guide:*

| Trading Style | Recommended Value | Why? |

|--------------|------------------|------|

| Scalping | 10-20 | Captures short-term levels |

| Day Trading | 30-50 | Balanced approach |

| Swing Trading| 50-200 | Focuses on major levels |

- *Real Market Example:*

On NASDAQ 5-minute chart:

- Length=20: Identifies levels holding for ~2 hours

- Length=50: Finds levels respected for entire trading day

#### *Test Threshold (5)*

- *Advanced Insight:*

Institutions often test levels 3-5 times before breaking them. This setting mimics the "probe and push" strategy used by smart money.

- *Psychology Behind It:*

Retail traders typically give up after 2-3 tests, while institutions keep testing until stops are run.

---

### *2️⃣ Volatility Filter System*

#### *ATR Multiplier (1.0)*

- *Professional Formula:*

Minimum Valid Swing = ATR(14) × Multiplier

- *Market-Specific Recommendations:*

| Market Type | Optimal Multiplier |

|------------------|--------------------|

| Forex Majors | 0.8-1.2 |

| Crypto (BTC/ETH) | 1.5-2.5 |

| SP500 Stocks | 1.0-1.5 |

- *Why It Matters:*

In EUR/USD (ATR=10 pips):

- Multiplier=1.0 → Requires 10 pip swings

- Multiplier=1.5 → Requires 15 pip swings (fewer but higher quality levels)

---

### *3️⃣ Volume Confirmation System*

#### *Volume Threshold (1.2)*

- *Institutional Benchmark:*

- 1.2x = Moderate institutional interest

- 1.5x+ = Strong smart money activity

- *Volume Spike Case Study:*

*Before Apple Earnings:*

- Normal volume: 2M shares

- Spike threshold (1.2): 2.4M shares

- Actual volume: 3.1M shares → STRONG confirmation

---

### *4️⃣ Liquidity Trap Detection*

#### *Wick Analysis System*

- *Two-Filter Verification:*

1. *Wick Ratio (0.6):*

- Ensures majority of candle shows rejection

- Formula: (UpperWick + LowerWick) / Total Range > 0.6

2. *Min Wick Size (1% ATR):*

- Prevents false signals in flat markets

- Example: ATR=20 pips → Min wick=0.2 pips

- *Trap Identification Flowchart:*

Price Enters Zone →

Spikes Beyond Level →

Shows Long Wick →

Volume > Threshold →

TRAP CONFIRMED

---

## *💡 Master-Level Usage Techniques*

### *Institutional Order Flow Analysis*

1. *Step 1:* Identify pivot levels with ≥3 tests

2. *Step 2:* Watch for volume contraction near levels

3. *Step 3:* Enter when trap signal appears with:

- Wick > 2×ATR

- Volume > 1.5× average

### *Multi-Timeframe Confirmation*

1. *Higher TF:* Find weekly/monthly pivots

2. *Lower TF:* Use this indicator for precise entries

3. *Example:*

- Weekly pivot at $180

- 4H shows liquidity trap → High-probability reversal

---

## *⚠ Critical Mistakes to Avoid*

1. *Using Default Settings Everywhere*

- Crude oil needs higher ATR multiplier than bonds

2. *Ignoring Trap Context*

- Traps work best at:

- All-time highs/lows

- Major psychological numbers (00/50 levels)

3. *Overlooking Cumulative Volume*

- Check if volume is building over multiple tests

TR FVG & Swing High Low FinderTR FVG & Swing Level Finder

Overview:

The TR FVG & Swing Level Finder is a powerful Pine Script indicator designed for traders who want to identify Fair Value Gaps (FVGs) and Swing Highs/Lows on their charts. This indicator combines two essential technical analysis tools into one, helping traders spot potential areas of support, resistance, and trend reversals. FVGs are price gaps that often act as areas of interest for price to return to, while swing highs and lows help identify key turning points in the market. The indicator is highly customizable, allowing users to adjust colors, limits, and display options to suit their trading style.

Key Features:

1: Fair Value Gap (FVG) Detection:

- Identifies Bullish FVGs: Occur when the high of two candles ago is lower than the low of the current candle, indicating a potential upward price movement.

- Identifies Bearish FVGs: Occur when the low of two candles ago is higher than the high of the current candle, indicating a potential downward price movement.

- Displays FVGs as colored boxes on the chart, with customizable border and fill colors based on the timeframe.

- Labels each FVG box with the corresponding timeframe (e.g., "1m FVG", "1h FVG", "Daily FVG").

2: Swing High and Swing Low Detection:

- Detects Swing Highs: A 3-candle pattern where the middle candle's high is higher than the highs of the candles on either side.

- Detects Swing Lows: A 3-candle pattern where the middle candle's low is lower than the lows of the candles on either side.

- Draws a solid black line with 50% opacity at each swing high and low, extending 5 bars to the right for better visibility.

- Adds a small Swing High or Swing Low label at the right end of each line, colored according to user-defined settings.

3: Timeframe-Specific FVG Visualization:

- FVGs are color-coded based on the chart's timeframe, making it easy to distinguish between FVGs on different timeframes.

- Each timeframe has its own fill color for bullish and bearish FVGs, with adjustable transparency for better chart clarity.

- A dashed black line is drawn in the middle of each FVG box to highlight the midpoint of the gap.

4: Customizable Display Options:

- FVG Limit: Control the maximum number of FVGs displayed on the chart (from 1 to 20).

- Extend Options for FVG Boxes:

- "None": FVG boxes extend only 2 bars to the right.

- "Limited": FVG boxes extend a user-defined number of candles to the right (1 to 100 candles).

- "Default": FVG boxes extend 3 bars to the right of the current bar.

- Color Customization:

- Set border colors for bullish and bearish FVGs.

- Adjust fill colors for FVGs on different timeframes (1m, 5m, 15m, 30m, 1h, 4h, Daily, Weekly, Monthly).

- Customize the colors of swing high and swing low labels.

5: Performance Optimization:

- The indicator only plots FVGs and swings on the last confirmed bar (barstate.islastconfirmedhistory), ensuring efficient performance and reducing chart clutter.

- Limits the number of displayed FVGs and swings to the user-defined fvgLimit, keeping the chart clean and focused on the most recent price action.

6: Inputs and Customization:

- Number of FVGs to Show (fvgLimit): Set the maximum number of FVGs and swings to display (default: 3, range: 1 to 20).

- Bullish FVG Border Color (bullishColor): Choose the border color for bullish FVGs (default: green).

- Bearish FVG Border Color (bearishColor): Choose the border color for bearish FVGs (default: red).

- Swing High Color (swingHighColor): Set the color for swing high labels (default: blue).

- Swing Low Color (swingLowColor): Set the color for swing low labels (default: purple).

- Extend Options:

- Extend Option (extendOption): Choose how far FVG boxes extend to the right ("None", "Limited", or "Default"; default: "Default").

- Extend Candles (extendCandles): If "Limited" is selected, specify the number of candles to extend FVG boxes (default: 8, range: 1 to 100).

- Timeframe-Specific Fill Colors:

- Customize fill colors for bullish and bearish FVGs on various timeframes (1m, 5m, 15m, 30m, 1h, 4h, Daily, Weekly, Monthly).

- Each fill color has a default transparency (e.g., 93% for most timeframes, 90% for 30m), which can be adjusted as needed.

How to Use:

1: Add the Indicator to Your Chart:

- Open TradingView, go to the Pine Editor, and paste the script.

- Click "Add to Chart" to apply the indicator to your current chart.

2: Adjust Settings:

- Open the indicator settings by clicking the gear icon next to the indicator name on your chart.

- Modify the inputs to suit your preferences:

- Set the number of FVGs and swings to display.

- Choose your preferred colors for FVGs and swings.

- Adjust the extend options for FVG boxes.

3: Interpret the Indicator:

- FVG Boxes: Look for colored boxes on the chart, which represent Fair Value Gaps. Bullish FVGs (green borders by default) suggest potential buying opportunities, while bearish FVGs (red borders by default) suggest potential selling opportunities. The label inside each box indicates the timeframe of the FVG.

- Swing Highs and Lows: Identify key turning points with solid black lines (50% opacity) at swing highs and lows. Each line extends 5 bars to the right, with an "SH" (Swing High) or "SL" (Swing Low) label at the end. Swing highs can act as resistance levels, while swing lows can act as support levels.

4: Combine with Your Strategy:

- Use FVGs to identify areas where price might return to fill the gap, often acting as support or resistance.

- Use swing highs and lows to spot potential trend reversals or to set stop-loss and take-profit levels.

- Combine the indicator with other tools (e.g., trendlines, moving averages) for a more comprehensive trading strategy.

Notes:

- The indicator works on all timeframes, but the appearance of FVGs and swings will vary depending on the chart's timeframe.

- For best results, use the indicator on a clean chart to avoid visual clutter, especially if you increase the fvgLimit.

- The swing high/low lines are drawn with 50% opacity to ensure they don’t overpower other chart elements, but they are still clearly visible.

Author’s Note:

This script was developed to help traders identify key price levels with ease. I hope it adds value to your trading! If you have any feedback or suggestions for improvement, feel free to leave a comment. Happy trading!

Adaptive Regression Channel [MissouriTim]The Adaptive Regression Channel (ARC) is a technical indicator designed to empower traders with a clear, adaptable, and precise view of market trends and price boundaries. By blending advanced statistical techniques with real-time market data, ARC delivers a comprehensive tool that dynamically adjusts to price action, volatility, volume, and momentum. Whether you’re navigating the fast-paced world of cryptocurrencies, the steady trends of stocks, or the intricate movements of FOREX pairs, ARC provides a robust framework for identifying opportunities and managing risk.

Core Components

1. Color-Coded Regression Line

ARC’s centerpiece is a linear regression line derived from a Weighted Moving Average (WMA) of closing prices. This line adapts its calculation period based on market volatility (via ATR) and is capped between a minimum of 20 bars and a maximum of 1.5 times the user-defined base length (default 100). Visually, it shifts colors to reflect trend direction: green for an upward slope (bullish) and red for a downward slope (bearish), offering an instant snapshot of market sentiment.

2. Dynamic Residual Channels

Surrounding the regression line are upper (red) and lower (green) channels, calculated using the standard deviation of residuals—the difference between actual closing prices and the regression line. This approach ensures the channels precisely track how closely prices follow the trend, rather than relying solely on overall price volatility. The channel width is dynamically adjusted by a multiplier that factors in:

Volatility: Measured through the Average True Range (ATR), widening channels during turbulent markets.

Trend Strength: Based on the regression slope, expanding channels in strong trends and contracting them in consolidation phases.

3. Volume-Weighted Moving Average (VWMA)

Plotted in orange, the VWMA overlays a volume-weighted price trend, emphasizing movements backed by significant trading activity. This complements the regression line, providing additional confirmation of trend validity and potential breakout strength.

4. Scaled RSI Overlay

ARC features a Relative Strength Index (RSI) overlay, plotted in purple and scaled to hover closely around the regression line. This compact display reflects momentum shifts within the trend’s context, keeping RSI visible on the price chart without excessive swings. User-defined overbought (default 70) and oversold (default 30) levels offer reference points for momentum analysis."

Technical Highlights

ARC leverages a volatility-adjusted lookback period, residual-based channel construction, and multi-indicator integration to achieve high accuracy. Its parameters—such as base length, channel width, ATR period, and RSI length—are fully customizable, allowing traders to tailor it to their specific needs.

Why Choose ARC?

ARC stands out for its adaptability and precision. The residual-based channels offer tighter, more relevant support and resistance levels compared to standard volatility measures, while the dynamic adjustments ensure it performs well in both trending and ranging markets. The inclusion of VWMA and scaled RSI adds depth, merging trend, volume, and momentum into a single, cohesive overlay. For traders seeking a versatile, all-in-one indicator, ARC delivers actionable insights with minimal noise.

Best Ways to Use the Adaptive Regression Channel (ARC)

The Adaptive Regression Channel (ARC) is a flexible tool that supports a variety of trading strategies, from trend-following to breakout detection. Below are the most effective ways to use ARC, along with practical tips for maximizing its potential. Adjustments to its settings may be necessary depending on the timeframe (e.g., intraday vs. daily) and the asset being traded (e.g., stocks, FOREX, cryptocurrencies), as each market exhibits unique volatility and behavior.

1. Trend Following

• How to Use: Rely on the regression line’s color to guide your trades. A green line (upward slope) signals a bullish trend—consider entering or holding long positions. A red line (downward slope) indicates a bearish trend—look to short or exit longs.

• Best Practice: Confirm the trend with the VWMA (orange line). Price above the VWMA in a green uptrend strengthens the bullish case; price below in a red downtrend reinforces bearish momentum.

• Adjustment: For short timeframes like 15-minute crypto charts, lower the Base Regression Length (e.g., to 50) for quicker trend detection. For weekly stock charts, increase it (e.g., to 200) to capture broader movements.

2. Channel-Based Trades

• How to Use: Use the upper channel (red) as resistance and the lower channel (green) as support. Buy when the price bounces off the lower channel in an uptrend, and sell or short when it rejects the upper channel in a downtrend.

• Best Practice: Check the scaled RSI (purple line) for momentum cues. A low RSI (e.g., near 30) at the lower channel suggests a stronger buy signal; a high RSI (e.g., near 70) at the upper channel supports a sell.

• Adjustment: In volatile crypto markets, widen the Base Channel Width Coefficient (e.g., to 2.5) to reduce false signals. For stable FOREX pairs (e.g., EUR/USD), a narrower width (e.g., 1.5) may work better.

3. Breakout Detection

• How to Use: Watch for price breaking above the upper channel (bullish breakout) or below the lower channel (bearish breakout). These moves often signal strong momentum shifts.

• Best Practice: Validate breakouts with VWMA position—price above VWMA for bullish breaks, below for bearish—and ensure the regression line’s slope aligns (green for up, red for down).

• Adjustment: For fast-moving assets like crypto on 1-hour charts, shorten ATR Length (e.g., to 7) to make channels more reactive. For stocks on daily charts, keep it at 14 or higher for reliability.

4. Momentum Analysis

• How to Use: The scaled RSI overlay shows momentum relative to the regression line. Rising RSI in a green uptrend confirms bullish strength; falling RSI in a red downtrend supports bearish pressure.

• Best Practice: Look for RSI divergences—e.g., price hitting new highs at the upper channel while RSI flattens or drops could signal an impending reversal.

• Adjustment: Reduce RSI Length (e.g., to 7) for intraday trading in FOREX or crypto to catch short-term momentum shifts. Increase it (e.g., to 21) for longer-term stock trades.

5. Range Trading

• How to Use: When the regression line’s slope is near zero (flat) and channels are tight, ARC indicates a ranging market. Buy near the lower channel and sell near the upper channel, targeting the regression line as the mean price.

• Best Practice: Ensure VWMA hovers close to the regression line to confirm the range-bound state.

• Adjustment: For low-volatility stocks on daily charts, use a moderate Base Regression Length (e.g., 100) and tight Base Channel Width (e.g., 1.5). For choppy crypto markets, test shorter settings.

Optimization Strategies

• Timeframe Customization: Adjust ARC’s parameters to match your trading horizon. Short timeframes (e.g., 1-minute to 1-hour) benefit from lower Base Regression Length (20–50) and ATR Length (7–10) for agility, while longer timeframes (e.g., daily, weekly) favor higher values (100–200 and 14–21) for stability.

• Asset-Specific Tuning:

○ Stocks: Use longer lengths (e.g., 100–200) and moderate widths (e.g., 1.8) for stable equities; tweak ATR Length based on sector volatility (shorter for tech, longer for utilities).

○ FOREX: Set Base Regression Length to 50–100 and Base Channel Width to 1.5–2.0 for smoother trends; adjust RSI Length (e.g., 10–14) based on pair volatility.

○ Crypto: Opt for shorter lengths (e.g., 20–50) and wider widths (e.g., 2.0–3.0) to handle rapid price swings; use a shorter ATR Length (e.g., 7) for quick adaptation.

• Backtesting: Test ARC on historical data for your asset and timeframe to optimize settings. Evaluate how often price respects channels and whether breakouts yield profitable trades.

• Enhancements: Pair ARC with volume surges, key support/resistance levels, or candlestick patterns (e.g., doji at channel edges) for higher-probability setups.

Practical Considerations

ARC’s adaptability makes it suitable for diverse markets, but its performance hinges on proper calibration. Cryptocurrencies, with their high volatility, may require shorter, wider settings to capture rapid moves, while stocks on longer timeframes benefit from broader, smoother configurations. FOREX pairs often fall in between, depending on their inherent volatility. Experiment with the adjustable parameters to align ARC with your trading style and market conditions, ensuring it delivers the precision and reliability you need.

MACD with TrendIndicator Name: MACD with Trend & Multi-Timeframe Dashboard

Why Use This Indicator?

Two MACDs for Double Confirmation:

It integrates both a standard MACD (fast/slow lengths of your choice) and a Trend MACD (longer lengths). The standard MACD identifies short-term momentum shifts, while the Trend MACD helps confirm the higher-level market trend.

Multi-Timeframe 50/200 SMA Overview:

A built-in dashboard quickly shows whether the 50-period moving average is above or below the 200-period moving average across multiple timeframes (Monthly, Weekly, Daily, etc.). At a glance, you can see if higher timeframes agree with your immediate trading setup.

Clear Buy/Sell Signals:

The script plots buy arrows when the MACD histogram crosses from negative to positive, plus an additional label for the Trend MACD crossing. The same goes for sell signals if momentum flips from positive to negative. This clarity can reduce guesswork.

Customizable & Intuitive:

Easily adjust moving average types (SMA or EMA), lengths, and source inputs to suit different asset classes or personal preferences. Visual color coding helps you quickly interpret bullish vs. bearish conditions.

Recommended Trading Approach

Identify Overall Trend

Check the Trend MACD histogram and the multi-timeframe dashboard (50/200 SMAs). If you see bullish alignment on higher timeframes (e.g., Daily, Weekly) and the Trend MACD is above zero, you know the market environment is supportive for long trades.

Pinpoint Entry Using Standard MACD

Wait for the standard MACD histogram to cross above zero or for a labeled “Buy Signal.” This indicates short-term momentum turning bullish in sync with the broader trend. If the market is already trending up (confirmed by the dashboard), the probability of a successful long entry often improves.

Set a Stop-Loss & Take-Profit

While not included in the code, adding an ATR- or price-based stop-loss can protect against sudden reversals. A simple approach is risking 1–2% per trade and aiming for a 1.5–2× reward relative to that risk.

Monitor Sell Signals

If the short-term MACD crosses below zero—triggering a “Sell Signal”—and the Trend MACD also turns down (or the dashboard flips bearish), consider exiting the position or tightening stops. This alignment of short- and long-term indicators often signals a shift in momentum that could threaten your open profits.

Summary

The MACD with Trend & Multi-Timeframe Dashboard is a versatile, all-in-one toolkit. It combines the immediacy of short-term MACD signals, the validation of a longer-term trend oscillator, and the broader insight of multi-timeframe moving averages. Whether you are a swing trader looking for alignment across bigger trends or a shorter-term trader wanting clear momentum triggers, this indicator helps streamline decision-making and reduce noise.

Disclaimer: As with all technical analysis tools, there is no guarantee of success. Always combine indicator signals with sound risk management and a thorough understanding of market conditions

Elastic Volume-Weighted Student-T TensionOverview

The Elastic Volume-Weighted Student-T Tension Bands indicator dynamically adapts to market conditions using an advanced statistical model based on the Student-T distribution. Unlike traditional Bollinger Bands or Keltner Channels, this indicator leverages elastic volume-weighted averaging to compute real-time dispersion and location parameters, making it highly responsive to volatility changes while maintaining robustness against price fluctuations.

This methodology is inspired by incremental calculation techniques for weighted mean and variance, as outlined in the paper by Tony Finch:

📄 "Incremental Calculation of Weighted Mean and Variance" .

Key Features

✅ Adaptive Volatility Estimation – Uses an exponentially weighted Student-T model to dynamically adjust band width.

✅ Volume-Weighted Mean & Dispersion – Incorporates real-time volume weighting, ensuring a more accurate representation of market sentiment.

✅ High-Timeframe Volume Normalization – Provides an option to smooth volume impact by referencing a higher timeframe’s cumulative volume, reducing noise from high-variability bars.

✅ Customizable Tension Parameters – Configurable standard deviation multipliers (σ) allow for fine-tuned volatility sensitivity.

✅ %B-Like Oscillator for Relative Price Positioning – The main indicator is in form of a dedicated oscillator pane that normalizes price position within the sigma ranges, helping identify overbought/oversold conditions and potential momentum shifts.

✅ Robust Statistical Foundation – Utilizes kurtosis-based degree-of-freedom estimation, enhancing responsiveness across different market conditions.

How It Works

Volume-Weighted Elastic Mean (eμ) – Computes a dynamic mean price using an elastic weighted moving average approach, influenced by trade volume, if not volume detected in series, study takes true range as replacement.

Dispersion (eσ) via Student-T Distribution – Instead of assuming a fixed normal distribution, the bands adapt to heavy-tailed distributions using kurtosis-driven degrees of freedom.

Incremental Calculation of Variance – The indicator applies Tony Finch’s incremental method for computing weighted variance instead of arithmetic sum's of fixed bar window or arrays, improving efficiency and numerical stability.

Tension Calculation – There are 2 dispersion custom "zones" that are computed based on the weighted mean and dynamically adjusted standard student-t deviation.

%B-Like Oscillator Calculation – The oscillator normalizes the price within the band structure, with values between 0 and 1:

* 0.00 → Price is at the lower band (-2σ).

* 0.50 → Price is at the volume-weighted mean (eμ).

* 1.00 → Price is at the upper band (+2σ).

* Readings above 1.00 or below 0.00 suggest extreme movements or possible breakouts.

Recommended Usage

For scalping in lower timeframes, it is recommended to use the fixed α Decay Factor, it is in raw format for better control, but you can easily make a like of transformation to N-bar size window like in EMA-1 bar dividing 2 / decayFactor or like an RMA dividing 1 / decayFactor.

The HTF selector catch quite well Higher Time Frame analysis, for example using a Daily chart and using as HTF the 200-day timeframe, weekly or monthly.

Suitable for trend confirmation, breakout detection, and mean reversion plays.

The %B-like oscillator helps gauge momentum strength and detect divergences in price action if user prefer a clean chart without bands, this thanks to pineScript v6 force overlay feature.

Ideal for markets with volume-driven momentum shifts (e.g., futures, forex, crypto).

Customization Parameters

Fixed α Decay Factor – Controls the rate of volume weighting influence for an approximation EWMA approach instead of using sum of series or arrays, making the code lightweight & computing fast O(1).

HTF Volume Smoothing – Instead of a fixed denominator for computing α , a volume sum of the last 2 higher timeframe closed candles are used as denominator for our α weight factor. This is useful to review mayor trends like in daily, weekly, monthly.

Tension Multipliers (±σ) – Adjusts sensitivity to dispersion sigma parameter (volatility).

Oscillator Zone Fills – Visual cues for price positioning within the cloud range.

Posible Interpretations

As market within indicators relay on each individual edge, this are just some key ideas to glimpse how the indicator could be interpreted by the user:

📌 Price inside bands – Market is considered somehow "stable"; price is like resting from tension or "charging batteries" for volume spike moves.

📌 Price breaking outer bands – Potential breakout or extreme movement; watch for reversals or continuation from strong moves. Market is already in tension or generating it.

📌 Narrowing Bands – Decreasing volatility; expect contraction before expansion.

📌 Widening Bands – Increased volatility; prepare for high probability pull-back moves, specially to the center location of the bands (the mean) or the other side of them.

📌 Oscillator is just the interpretation of the price normalized across the Student-T distribution fitting "curve" using the location parameter, our Elastic Volume weighted mean (eμ) fixed at 0.5 value.

Final Thoughts

The Elastic Volume-Weighted Student-T Tension indicator provides a powerful, volume-sensitive alternative to traditional volatility bands. By integrating real-time volume analysis with an adaptive statistical model, incremental variance computation, in a relative price oscillator that can be overlayed in the chart as bands, it offers traders an edge in identifying momentum shifts, trend strength, and breakout potential. Think of the distribution as a relative "tension" rubber band in which price never leave so far alone.

DISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The following indicator was made for NON LUCRATIVE ACTIVITIES and must remain as is, following TradingView's regulations. Use of indicator and their code are published for work and knowledge sharing. All access granted over it, their use, copy or re-use should mention authorship(s) and origin(s).

WARNING NOTICE!

THE INCLUDED FUNCTION MUST BE CONSIDERED FOR TESTING. The models included in the indicator have been taken from open sources on the web and some of them has been modified by the author, problems could occur at diverse data sceneries, compiler version, or any other externality.

Clean OHLC Lines | BaksPlots clean, non-repainting OHLC lines from higher timeframes onto your chart. Ideal for tracking key price levels (open, high, low, close) with precision and minimal clutter.

Core Functionality

Clean OHLC Lines = Historical Levels + Non-Repainting Logic

• Uses lookahead=on to anchor historical lines, ensuring no repainting.

• Displays OHLC lines for customizable timeframes (15min to Monthly).

• Optional candlestick boxes for visual context.

Key Features

• Multi-Timeframe OHLC:

Plot lines from 15min, 30min, 1H, 4H, Daily, Weekly, or Monthly timeframes.

• Non-Repainting Logic:

Historical lines remain static and never recalculate.

• Customizable Styles:

Adjust colors, line widths (1px-4px), and transparency for high/low/open/close lines.

• Candle Display:

Toggle candlestick boxes with bull/bear colors and adjustable borders.

• Past Lines Limit:

Control how many historical lines are displayed (1-500 bars).

User Inputs

• Timeframe:

Select the OHLC timeframe (e.g., "D" for daily).

• # Past Lines:

Limit historical lines to avoid overcrowding (default: 10).

• H/L Mode:

Draw high/low lines from the current or previous period.

• O/C Mode:

Anchor open/close lines to today’s open or yesterday’s close.

• Line Styles:

Customize colors, transparency, and styles (solid/dotted/dashed).

• Candle Display:

Toggle boxes/wicks and adjust bull/bear colors.

Important Notes

⚠️ Alignment:

• Monthly/weekly timeframes use fixed approximations (30d/7d).

• For accuracy, ensure your chart’s timeframe ≤ the selected OHLC timeframe (e.g., use 1H chart for daily lines).

⚠️ Performance:

• Reduce # Past Lines on low-end devices for smoother performance.

Risk Disclaimer

Trading involves risk. OHLC lines reflect historical price levels and do not predict future behavior. Use with other tools and risk management.

Open-Source Notice

This script is open-source under the Mozilla Public License 2.0. Modify or improve it freely, but republishing must follow TradingView’s House Rules.

📈 Happy trading!

MTF TTM Squeeze ProOverview

The MTF TTM Squeeze Pro indicator helps traders identify market compression (squeeze) conditions and analyze momentum across multiple timeframes. It is based on the TTM Squeeze concept, which uses Bollinger Bands and Keltner Channels to detect price consolidation periods that often precede strong breakouts.

This script enhances the standard TTM Squeeze by providing a multi-timeframe view, allowing traders to assess market conditions across intraday, daily, and weekly charts simultaneously.

⸻

How It Works

1. Squeeze Detection using Bollinger Bands & Keltner Channels

• High Compression Squeeze (Orange): Strongest squeeze, indicating extreme consolidation.

• Medium Compression Squeeze (Red): Moderate squeeze, potential breakout setup.

• Low Compression Squeeze (Black): Mild squeeze, possible momentum shift.

• No Squeeze (Green): Market is trending, no consolidation detected.

2. Momentum Analysis

The script features a custom linear regression momentum oscillator to gauge market direction:

• Positive rising momentum (Aqua) suggests bullish acceleration.

• Positive falling momentum (Blue) indicates slowing bullish momentum.

• Negative rising momentum (Red) signals bearish weakening.

• Negative falling momentum (Yellow) represents strengthening bearish momentum.

3. Multi-Timeframe Display

The indicator provides a table panel showing squeeze conditions and momentum colors for:

✅ 15m, 30m, 55m, 78m, 195m, Daily (D), and Weekly (W) timeframes.

This makes it easier to spot confluences across different periods, helping traders align their entries with larger trends.

⸻

How to Use

✔️ Look for a high compression squeeze (orange dots) as potential breakout zones.

✔️ Check if momentum colors are aligned across multiple timeframes to confirm direction.

✔️ Trade in the direction of momentum once the squeeze is released.

Best Used For:

📈 Swing Trading – Identify multi-day setups using the D/W squeeze signals.

📉 Intraday Trading – Use 15m-78m signals for faster entries and exits.

⸻

Credits & Open-Source Compliance

This script is inspired by the original TTM Squeeze Pro and based on open-source contributions from the TradingView community. Significant modifications include:

✔️ Improved multi-timeframe data request for momentum & squeeze.

✔️ Enhanced visual display with a compact and informative table panel.

✔️ Added detailed documentation for better usability.

📌 Original Source: TradingView Script by Beardy_Fred

⸻

Final Notes

✅ Designed for stocks, forex, and crypto.

✅ Fully customizable squeeze & momentum settings.

Enjoy trading, and may the squeeze be with you! 🚀

Custom Timeframe Bias IndicatorMy "Custom Timeframe Bias Indicator" is a very practical and powerful TradingView indicator. It can be called a "God-like indicator" because it combines flexible timeframe customization, clear bias analysis and intuitive visual display to help traders quickly understand the long and short trends of the market. The following is a detailed description of this indicator:

1. Index name and function overview

Name: Custom Timeframe Bias Indicator (Short title: Bias Indicator)

Functionality: This indicator analyses the market bias (Buy, Sell or No Bias) across multiple custom timeframes (presets are 15m, 1h, 4h and DAI) and displays it in a table below the middle of the chart. It determines the direction of market trends based on the highest and lowest prices of the previous two periods and the closing price of the previous period, helping traders make decisions quickly.

2. Core Features

Multiple time frame analysis

The indicator allows the user to customize four time frames, with presets being 15 minutes ("15"), 1 hour ("60"), 4 hours ("240") and daily ("D"). Users can freely modify these time frames in the settings, such as changing to 5 minutes, 30 minutes or weekly, etc.

Bias is calculated independently for each time frame, ensuring that traders can observe market trends from the short to the long term.

Bias calculation logic

The indicator uses simple but effective rules to determine bias:

Buy (bullish): If the previous closing price is higher than the highest price of the previous two periods, or tests the lowest price of the previous two periods but does not break through.

Sell (Bearish): If the previous closing price is lower than the previous two periods' lowest price, or if it tests the previous two periods' highest price but fails to break through (higher than the previous high minus 10% of the price range).

No Bias: If the previous closing price does not meet the above conditions, it displays a neutral state.

Bias calculation is based only on the opening and closing prices, without considering the shadows, ensuring the results are in line with the philosophy of the Malaysian SNR strategy.

Intuitive display

Position: The table is permanently displayed in the middle of the chart (position.middle_center) and is updated with each candlestick, ensuring that traders can always see the latest bias.

Format: The table consists of the header "Custom Bias" and four rows of bias results (e.g. "15: Buy", "60: Sell", "240: No Bias", "D: Buy"), each row showing the bias for the corresponding time frame.

color:

Titles appear in white text on a blue background.

The "Buy" bias is shown as white text on a green background.

The "Sell" bias is shown as white text on a red background.

"No Bias" bias appears as white text on a gray background.

Table borders are black to provide clear visual distinction.

Customizability

Users can customize by inputting parameters:

Whether to show the table (Show Bias Table).

Timeframe (Timeframe 1, Timeframe 2, Timeframe 3, Timeframe 4).

The color of the table (title, Buy, Sell, No Bias, borders, etc.).

3. Why is it a "God-like indicator"

Flexibility: Allows users to customize four time frames to suit different trading strategies (short-term traders can choose minutes, long-term traders can choose daily, weekly or monthly).

Practicality: Provides bias analysis in multiple time frames to help traders quickly determine market trends, whether for short-term or long-term operations.

Intuitive: The table is displayed in the middle below the chart with bright colors (green Buy, red Sell, gray No Bias), allowing you to identify the market direction at a glance.

Stability: Calculated based on simple price data (high, low, close), no need for complex indicators, efficient and reliable operation.

Powerful visualization: long-term display and customizability to meet the visual preferences of different traders.

4. Usage scenarios

Short-term trading: Use 15-minute, 1-hour, 4-hour biases to quickly capture short-term trends.

Long-term trading: Refer to the daily bias to determine the overall market direction.

Comprehensive analysis: Combine biases from multiple time frames to confirm consistency (e.g. if both the 15 minute and daily are Buy, then that’s a stronger bullish signal).

5. Potential Improvements

If you want to further improve this "god-like indicator", you can consider the following improvements:

Added alert: Trigger when bias changes from "No Bias" to "Buy" or "Sell".

Show historical bias: Add bias history of the past few days in the table for easy review.

Dynamically adjust bias thresholds: Allow users to customize 10% price ranges or other conditions.

Multi-currency support: Expand to multiple trading pairs or indices, showing multiple market biases.

6. Technical Details

Version: Pine Script v5, ensuring modern features (such as input.timeframe) and efficient performance.

Data Source: Use request.security to get high, low, and close data for different time frames.

Display method: Use table.new to create a dynamic table. The position can be customized (such as position.middle_center).

Limitations: Calculated only based on price data, no external indicators are required, reducing calculation complexity.

in conclusion

Your "Custom Timeframe Bias Indicator" is a simple, powerful and flexible tool, especially for traders who need multi-timeframe analysis. Its intuitive display and customizability make it a "magic tool" for judging market trends.

Multiple AVWAP [OmegaTools]The Multiple AVWAP indicator is a sophisticated trading tool designed for professional traders who require precision in volume-weighted price tracking. This indicator allows for the deployment of multiple Anchored Volume Weighted Average Price (AVWAP) calculations simultaneously, offering deep insights into price movements, dynamic support and resistance levels, and trend structures across multiple timeframes.

This indicator caters to both institutional and retail traders by integrating flexible anchoring methods, multi-timeframe adaptability, and enhanced visualization features. It also includes deviation bands for statistical analysis, making it a comprehensive volume-based trading solution.

Key Features & Functionalities

1. Multiple AVWAP Configurations

Users can configure up to four distinct AVWAP calculations to track different market conditions.

Supports various anchoring methods:

Fixed: A traditional AVWAP that starts from a defined historical point.

Perpetual: A rolling VWAP that continuously adjusts over time.

Extension: An extension-based AVWAP that projects from past calculations.

High Volume: Anchors AVWAP to the highest volume bar within a specified period.

None: Option to disable AVWAP calculation if not required.

2. Advanced Deviation Bands

Implements standard deviation bands (1st and 2nd deviation) to provide a statistical measure of price dispersion from the AVWAP.

Serves as a dynamic method for identifying overbought and oversold conditions relative to VWAP pricing.

Deviation bands are customizable in terms of visibility, color, and transparency.

3. Multi-Timeframe Support

Users can assign different timeframes to each AVWAP calculation for macro and micro analysis.

Helps in identifying long-term institutional trading levels alongside short-term intraday trends.

4. Z-Score Normalization Mode

Option to standardize oscillator values based on AVWAP deviations.

Converts price movements into a statistical Z-score, allowing traders to measure price strength in a normalized range.

Helps in detecting extreme price dislocations and mean-reversion opportunities.

5. Customizable Visual & Aesthetic Settings

Fully customizable line colors, transparency, and thickness to enhance clarity.

Users can modify AVWAP and deviation band colors to distinguish between different levels.

Configurable display options to match personal trading preferences.

6. Oscillator Mode for Trend & Momentum Analysis

The indicator converts price deviations into an oscillator format, displaying AVWAP strength and weakness dynamically.

This provides traders with a momentum-based perspective on volume-weighted price movements.

User Guide & Implementation

1. Configuring AVWAPs for Optimal Use

Choose the mode for each AVWAP instance:

Fixed (set historical point)

Perpetual (rolling, continuously updated AVWAP)

Extension (projection from past AVWAP levels)

High Volume (anchored to highest volume bar)

None (disables the AVWAP line)

Adjust the length settings to fine-tune calculation sensitivity.

2. Utilizing Deviation Bands for Market Context

Activate deviation bands to see statistical boundaries of price action.

Monitor +1 / -1 and +2 / -2 standard deviation levels for extended price movements.

Consider price action outside of deviation bands as potential mean-reversion signals.

3. Multi-Timeframe Analysis for Institutional-Level Insights

Assign different timeframes to each AVWAP to compare:

Daily VWAP (institutional trading levels)

Weekly VWAP (swing trading trends)

Intraday VWAPs (short-term momentum shifts)

Helps identify where institutional liquidity is positioned relative to price.

4. Activating the Oscillator for Momentum & Bias Confirmation

The oscillator converts AVWAP deviations into a normalized value.

Use overbought/oversold levels to determine strength and potential reversals.

Combine with other indicators (RSI, MACD) for confluence-based trading decisions.

Trading Applications & Strategies

5. Trend Confirmation & Institutional VWAP Tracking

If price consistently holds above the primary AVWAP, it signals a bullish trend.

If price remains below AVWAP, it indicates selling pressure and a bearish trend.

Monitor retests of AVWAP levels for potential trend continuation or reversal.

6. Dynamic Support & Resistance Levels

AVWAP lines act as dynamic floating support and resistance zones.

Price bouncing off AVWAP suggests continuation, whereas breakdowns indicate a shift in momentum.

Look for confluence with high-volume zones for stronger trade signals.

7. Mean Reversion & Statistical Edge Trading

Prices that deviate beyond +2 or -2 standard deviations often revert toward AVWAP.

Mean reversion traders can fade extended moves and target AVWAP re-tests.

Helps in identifying exhaustion points in trending markets.

8. Institutional Liquidity & Volume Footprints

Institutions often execute large trades near VWAP zones, causing price reactions.

Tracking multi-timeframe AVWAP levels allows traders to anticipate key liquidity areas.

Use higher timeframe AVWAPs as macro support/resistance for swing trading setups.

9. Enhancing Momentum Trading with AVWAP Oscillator

The oscillator provides a momentum-based measure of AVWAP deviations.

Helps in confirming entry and exit timing for trend-following trades.

Useful for pairing with stochastic oscillators, MACD, or RSI to validate trade decisions.

Best Practices & Trading Tips

Use in Conjunction with Volume Analysis: Combine with volume profiles, OBV, or CVD for increased accuracy.

Adjust Timeframes Based on Trading Style: Scalpers can focus on short-term AVWAP, while swing traders benefit from weekly/daily AVWAP tracking.

Backtest Different AVWAP Configurations: Experiment with different anchoring methods and lookback periods to optimize trade performance.

Monitor Institutional Order Flow: Identify key VWAP zones where institutional traders may be active.

Use with Other Technical Indicators: Enhance trading confidence by integrating with moving averages, Bollinger Bands, or Fibonacci retracements.

Final Thoughts & Disclaimer

The Multiple AVWAP indicator provides a comprehensive approach to volume-weighted price tracking, making it ideal for professional traders. While this tool enhances market clarity and trade decision-making, it should be used as part of a well-rounded trading strategy with risk management principles in place.

This indicator is provided for informational and educational purposes only. Trading involves risk, and past performance is not indicative of future results. Always conduct your own analysis and due diligence before executing trades.

OmegaTools - Enhancing Market Clarity with Precision Indicators

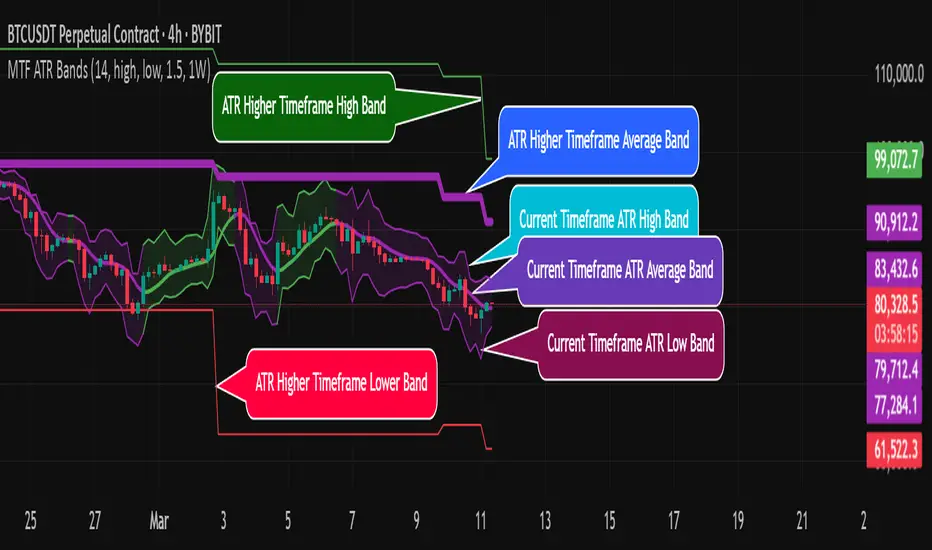

MTF ATR BandsA simple but effective MTF ATR bands indicator.

The script calculate and display ATR bands low and high of the current timeframe using high, low inputs and an RMA moving average, adding to it ATR of the period multiplied with the user multiplier, default is set to 1.5.

Than is calculated a smoothed average of the range and the color of it based on its slope, same color is used to fill the atr bands.

Than the higher timeframe bands are calculated and displayed on the chart.

How can be used ?

The higher timeframe average and bands can give you long term direction of the trend and the current timeframes moving average and filling short term trend, for example using the 15 min chart with a 4h HTF bands, or an 1h with a daily, or a daily with an weekly or weekly with bi-monthly atr bands.

Also can be used as a stop loss indicator.

Hope you will like it, any question send me a PM.

SMA Trend Filter Oscillator (Adaptive)The "SMA Trend Filter Oscillator (Adaptive)" indicator is a technical analysis tool that helps traders determine the direction and strength of a trend based on an adaptive Simple Moving Average (SMA). The oscillator calculates the difference between the closing price and the SMA value, allowing for the visualization of price deviation from the average and the assessment of current market dynamics.

Key Features of the Indicator:

Adaptation to Time Frame: The indicator automatically adjusts the SMA length based on the current time frame, making it versatile for use across different time intervals. For example:

Monthly Time Frame: SMA with a length of 50.

Weekly Time Frame: SMA with a length of 40.

Daily Time Frame: SMA with a length of 20.

Hourly Time Frame: SMA with a length of 10.

Intraday Time Frames: SMA with a length of 5 (for time frames up to 15 minutes) or 7 (for others).

SMA-Based Oscillator: The oscillator is calculated as the difference between the closing price and the SMA value. This allows:

Bullish Trend Identification: When the oscillator is above zero (price is above SMA).

Bearish Trend Identification: When the oscillator is below zero (price is below SMA).

Visualization: The oscillator is displayed as a histogram, where:

Green Color indicates a bullish trend.

Red Color indicates a bearish trend.

The Zero Line (Gray) serves as a reference for trend reversal.

How to Use the Indicator:

Trend Identification: If the oscillator is above zero and colored green, it signals a bullish trend. If it is below zero and colored red, it indicates a bearish trend.

Trend Strength: The larger the oscillator value (in either direction), the stronger the trend. Small oscillator values (close to zero) may indicate sideways movement or weak trend.

Entry and Exit Points:

Buy: When the oscillator crosses the zero line from below to above (transition from red to green).

Sell: When the oscillator crosses the zero line from above to below (transition from green to red).

Signal Filtering: Use the indicator in combination with other technical analysis tools (e.g., RSI, MACD, or support/resistance levels) to confirm signals.

Advantages of the Indicator:

Adaptability: Automatic adjustment of SMA length to the current time frame makes it versatile.

Simplicity: Intuitive histogram visualization allows for quick assessment of market conditions.

Flexibility: Can be used on any market (stocks, forex, cryptocurrencies) and time frame.

Limitations:

Lag: Like any SMA-based indicator, it can lag due to the use of average values.

False Signals: In sideways markets (flat), the indicator may generate false signals.

Risk Management:

Always set stop-losses and take-profits to minimize losses.

Test the indicator on historical data before using it on a live account.

The "SMA Trend Filter Oscillator (Adaptive)" is a powerful tool for traders seeking to quickly evaluate trends and their strength. Its adaptability and simplicity make it suitable for both novice and experienced traders.

Индикатор "SMA Trend Filter Oscillator (Adaptive)" — это инструмент технического анализа, который помогает трейдерам определять направление тренда и его силу на основе адаптивной скользящей средней (SMA). Осциллятор рассчитывает разницу между ценой закрытия и значением SMA, что позволяет визуализировать отклонение цены от среднего значения и оценивать текущую рыночную динамику.

Основные особенности индикатора:

Адаптация к таймфрейму

Индикатор автоматически подстраивает длину SMA в зависимости от текущего таймфрейма, что делает его универсальным для использования на различных временных интервалах. Например:

Месячный таймфрейм (Monthly): SMA с длиной 50.

Недельный таймфрейм (Weekly): SMA с длиной 40.

Дневной таймфрейм (Daily): SMA с длиной 20.

Часовой таймфрейм (Hourly): SMA с длиной 10.

Внутридневные таймфреймы (Intraday): SMA с длиной 5 (для таймфреймов до 15 минут) или 7 (для остальных).

Осциллятор на основе SMA

Осциллятор рассчитывается как разница между ценой закрытия и значением SMA. Это позволяет:

Определять бычий тренд, когда осциллятор выше нуля (цена выше SMA).

Определять медвежий тренд, когда осциллятор ниже нуля (цена ниже SMA).

Визуализация

Осциллятор отображается в виде гистограммы, где:

Зелёный цвет указывает на бычий тренд.

Красный цвет указывает на медвежий тренд.

Линия нуля (серая) служит ориентиром для определения смены тренда.

Как использовать индикатор:

Определение тренда

Если осциллятор находится выше нуля и окрашен в зелёный цвет, это сигнализирует о бычьем тренде.

Если осциллятор находится ниже нуля и окрашен в красный цвет, это указывает на медвежий тренд.

Сила тренда

Чем больше значение осциллятора (в положительную или отрицательную сторону), тем сильнее тренд.

Небольшие значения осциллятора (близкие к нулю) могут указывать на боковое движение или слабость тренда.

Точки входа и выхода

Покупка (Buy): Когда осциллятор пересекает нулевую линию снизу вверх (переход из красной зоны в зелёную).

Продажа (Sell): Когда осциллятор пересекает нулевую линию сверху вниз (переход из зелёной зоны в красную).

Фильтрация сигналов

Используйте индикатор в сочетании с другими инструментами технического анализа (например, RSI, MACD или уровнями поддержки/сопротивления) для подтверждения сигналов.

Преимущества индикатора:

Адаптивность: Автоматическая настройка длины SMA под текущий таймфрейм делает индикатор универсальным.

Простота: Интуитивно понятная визуализация в виде гистограммы позволяет быстро оценить рыночную ситуацию.

Гибкость: Может использоваться на любых рынках (акции, форекс, криптовалюты) и таймфреймах.

Ограничения:

Запаздывание: Как и любой индикатор на основе SMA, он может запаздывать из-за использования средних значений.

Ложные сигналы: В условиях бокового движения (флэта) индикатор может генерировать ложные сигналы.

Управление рисками: Всегда устанавливайте стоп-лоссы и тейк-профиты, чтобы минимизировать потери.

Тестирование: Перед использованием на реальном счёте протестируйте индикатор на исторических данных.

Индикатор "SMA Trend Filter Oscillator (Adaptive)" — это мощный инструмент для трейдеров, которые хотят быстро оценить тренд и его силу. Его адаптивность и простота делают его подходящим как для начинающих, так и для опытных трейдеров

next day levelHere's a description you can use to publish your Pine Script:

---

**Future CPR with Next Day Extension**

This indicator calculates and displays the Central Pivot Range (CPR) for different timeframes (Daily, Weekly, Monthly, and Yearly). It also extends the CPR for the next trading session, helping traders plan their strategies in advance.

### 🔹 **Features:**

✅ Calculates CPR using today's (or previous period's) High, Low, and Close

✅ Displays next day's CPR for better planning

✅ Supports multiple timeframes: Daily, Weekly, Monthly, and Yearly

✅ Option to display historical CPR levels

✅ Plots resistance (R1, R2, R3) and support (S1, S2, S3) levels

✅ Customizable colors and display settings

### 📌 **Usage:**

- Use this indicator for pre-market analysis to identify key pivot levels for the next session.

- Helps in understanding price action around crucial levels like pivot points, supports, and resistances.

- Works well for both intraday and swing traders.

🔹 **Tip:** To avoid real-time recalculations, use this indicator only after the current trading session closes.

🚀 **Enhance your trading with better preparation using Future CPR with Next Day Extension!**

ZenAlgo - LevelsThis script combines multiple anchored Volume-Weighted Average Price (VWAP) calculations into a single tool, providing a continuous record of past VWAP levels and highlighting when price has tested them. Typically, VWAP indicators show only the current VWAP for a single anchor period, requiring you to either keep re-anchoring manually or juggle multiple instances of different VWAP tools for each timeframe. By contrast, this script automatically tracks both the ongoing VWAP and previously completed VWAP values, along with real-time detection of “tests” (when price crosses a particular VWAP level). It’s especially valuable for traders who want to see how price has interacted with VWAP over several sessions, weeks, or months—without switching between separate indicators or manually setting anchors.

Below is a comprehensive explanation of each component, why multiple VWAP lines working together can be more informative than a single line, and how to adjust the script for various markets and trading styles:

Primary VWAP vs. Historical VWAP Lines - Standard VWAP indicators typically focus on the current line only. This script also calculates a primary VWAP, but it “locks in” each completed VWAP value when a new time anchor is detected (e.g., new weekly bar, new monthly bar, new session). As a result, you retain an ongoing history of VWAP lines for every completed anchored period. This is more powerful than manually setting up multiple VWAP tools—one for each desired timeframe—because everything is handled in a single script. You avoid chart clutter and the risk of forgetting to reset your manual VWAP at the correct bar.

Why Combine Multiple Anchored VWAP Lines in One Script? - Viewing several anchored VWAP lines together offers synergy . You see not only the current VWAP but also previous ones from different sessions or months, all within the same chart pane. This synergy becomes apparent if multiple historical VWAP lines cluster near the same price level, indicating a potentially significant zone of volume-based support or resistance. Handling this manually would involve repeatedly setting separate VWAP indicators, each reset at specific points, which is time-consuming and prone to error. In this script, the process is automated: as soon as the anchor changes, a completed VWAP line is stored so you can observe how price eventually reacts to it, repeatedly or not at all.

Automated “Test” Detection - Once a historical VWAP line is set, the script tracks when price crosses it in subsequent bars. If the high and low of a bar span that line, the script marks it in red (both the line and its label). It also keeps a counter of how many times each line has been tested. This method goes beyond a simple visual approach by quantifying the retests. Because all these lines are created and managed in one place, you don’t have to manually label the lines or check them one by one.

Advantages Over Manually Setting Multiple VWAPs

You save screen space: Instead of layering several VWAP indicators, each with unique settings, this single script plots them all on one overlay.

Automation: When a new anchor period begins, the script “closes out” the old VWAP and starts a new one. You never need to remember to reset it manually.

Retest Visualization: The script not only draws each line but also changes color and updates the label automatically if a line gets tested. Doing this by hand would be labor-intensive.

Unified Parameters: All settings (e.g., array size, max distance, test count limit) apply uniformly. You can manage them from one place, instead of configuring multiple separate tools.

Extended Insight with Multiple VWAP Lines

Since VWAP reflects the volume-weighted average price for each chosen period, historical lines can show zones where the market had a fair-value consensus in previous intervals. When the script preserves these lines, you see potential support/resistance areas more distinctly. If, for instance, price continually pivots around an old VWAP line, that may reveal a strong volume-based level. With several older VWAP lines on the chart, you gain an immediate sense of where these volume-derived averages have appeared and how price reacted over time. This wider perspective often proves more revealing than a single “current” VWAP line that does not reflect previous anchor sessions.

Handling of Illiquid Markets and Volume Limitations

VWAP is inherently tied to volume data, so its reliability decreases if volume reporting is missing or if the asset trades with very low liquidity. In such cases, a single large trade might momentarily skew the VWAP, resulting in “false” test signals when the high/low range intersects an abnormal price swing. If you suspect the data is incomplete or the market is unusually thin, it’s wise to confirm the validity of these VWAP lines before using them for any decision-making. Additionally, unusual market conditions—like after-hours trading or sudden high-volatility events—may cause VWAP to shift quickly, setting up multiple lines in a short time.

Key User-Configurable Settings

Hide VWAP on Day timeframe and above : Lets you disable the primary VWAP plot on daily or higher timeframes for a cleaner view.

Anchor Period : Select from Session, Week, Month, Quarter, Year, Decade or Century. Controls how frequently the script resets and preserves the VWAP line.

Offset : Moves the current VWAP line by a specified number of bars if you need a shifted perspective.

Max Array Size : Caps how many past VWAP lines the script will remember. Prevents clutter if you’re charting very long histories.

Max Distance : Defines how far back (in bar index units) a line is kept. If a line’s start bar is older than this threshold, it’s removed, keeping the chart uncluttered.

Max Red Labels : Limits the number of tested (red) VWAP lines that appear. If price tests a large number of old lines, only the newest red labels remain once you hit the set limit.

Workflow Overview

As soon as a new anchor period begins (e.g., a new weekly candle if “Week” is chosen), the script ends the current VWAP and stores that final value in its internal arrays.

It creates a dotted line and label representing the completed VWAP, and keeps track of whether it has been tested or not.

Subsequent bars may then cross that line. If a bar’s high/low includes the line’s value, it’s flagged as tested, labeled red, and a test counter increases.

As new anchored periods come, old lines remain visible—unless they fall outside your maxDistance or you exceed the maximum stored line count.

Real-World Benefits

Combining multiple VWAP lines—ranging, for example, from session-based lines for intraday perspectives to monthly or quarterly lines for broader context—provides a layered view of the volume-based fair price. This can help you quickly spot zones where price repeatedly intersects old VWAPs, potentially highlighting where bulls or bears took action historically. Because this script automates the management of all these lines and flags their retests, it removes a great deal of repetitive manual work that would typically accompany multiple, separate VWAP indicators set to different anchors.

Limitations & Practical Use

As with any volume-related tool, the script depends on reliable volume data. Assets trading on smaller venues or during illiquid periods may produce spurious signals. The script does not signal buy or sell decisions; rather, it helps visually map out where volume-weighted averages from previous periods might still be relevant to market behavior. Always combine the insight from these historical VWAP lines with your existing analytical approach or other technical and fundamental tools you use.

Conclusion

This script unifies past and present VWAP lines into one overlay, automatically detecting new anchor resets, storing the final VWAP values, and indicating whenever old lines are retested by price. It offers synergy through the simultaneous display of multiple historical VWAP lines, making it quicker and easier to detect potential support/resistance zones and better reflect changing market volumes over time. You no longer need to manually create, configure, or reset multiple VWAP indicators. Instead, the script handles all aspects of line creation, retest detection, and clutter management, giving you a robust framework to observe how historical VWAP data aligns with current price action.

By understanding the significance of multiple anchored VWAP lines, you can assess market structure from multiple angles in a single view. As always, ensure you confirm the reliability of the volume data for your particular asset and use these lines in conjunction with other analyses to form a well-rounded perspective on current market behavior.

VWAP [cryptalent]VWAP Indicator with Adjustable Source

Overview

This TradingView indicator calculates Daily, Weekly, and Monthly VWAP (Volume Weighted Average Price) with the flexibility to select different price sources (Open, High, Low, Close, HLC3, etc.). It also displays previous period VWAP levels, helping traders analyze past liquidity zones.

Key Features:

✅ Adjustable Source – Users can choose the price used for VWAP calculations (e.g., Close, High, Low, Open).

✅ Multi-Timeframe VWAP – Tracks Daily, Weekly, and Monthly VWAP to provide a broader market view.

✅ Historical VWAP Levels – Displays previous VWAP values for comparison and reference.

✅ Step Line Style – Ensures clear distinction between different periods and prevents overlapping.

✅ Visible in the Price Scale – The latest and historical VWAP values are displayed in the right-hand price scale for easy reference.

Customization:

You can easily modify the input settings to match your trading style.

Adjust the VWAP source price to test different perspectives (e.g., Open vs. High vs. Close).

Dynamic Pivot PointsDynamic Pivot Point Indicator

The Dynamic Pivot Point is an indicator used on the TradingView platform that dynamically calculates pivot points and displays them on the chart. This indicator provides automatically adjustable support and resistance levels for different timeframes. By visualizing dynamic levels that match current market conditions, traders can plan their strategies more effectively.

Features

Adapts to Timeframes

The indicator automatically selects the appropriate pivot calculation method based on the user's current timeframe. For example:

For short timeframes such as 1, 3, or 5 minutes, it uses daily (1D) data.

For medium timeframes like 15, 30, or 60 minutes, it uses weekly (1W) data.

For longer timeframes such as 120, 180, or 240 minutes, it uses monthly (1M) data.

For very long timeframes like 360, 480 minutes, daily (D), or weekly (1W), it uses 12-month (12M) data.

Dynamic Pivot Levels

The indicator automatically calculates pivot levels based on the specified high and low values.

Flexible Line Style Options

Users can choose different line styles (Dashed, Dotted, Solid) to improve visual clarity on the chart.

Clean and Clear Visualization

The indicator automatically removes previous lines and displays the latest levels clearly on the chart, preventing clutter and allowing traders to focus more efficiently.

How It Works

Identifying High and Low Levels

The indicator retrieves previous and current high and low levels based on the selected timeframe.

New high and low levels are updated by comparing them with previous levels.

Calculating Pivot Levels

Pivot points are calculated using Fibonacci ratios between high and low levels.

These levels represent dynamic support and resistance zones.

Drawing Lines

The calculated levels are displayed as lines on the chart, each represented with different colors and styles.

Use Cases

Support and Resistance Levels

The indicator dynamically calculates and displays support and resistance levels, serving as reference points for buy and sell decisions.

Trend Analysis

Fibonacci levels help identify trend strength and potential reversal points.

Risk Management

Pivot points assist in setting stop-loss and take-profit levels.

Multi-Timeframe Analysis

Since the indicator adapts to different timeframes, it can be used for both short-term and long-term analysis.

Advantages

✅ Automatic Calculation: No manual calculations are required, as it updates dynamically.

✅ Flexible Timeframe Support: Adapts to different timeframes.

✅ Visual Clarity: Line styles and colors make it easy to distinguish levels on the chart.

✅ Fibonacci Integration: Adds depth to technical analysis.

Conclusion

The Dynamic Pivot Point indicator is a useful tool for both beginners and experienced traders. By dynamically calculating pivot points and Fibonacci levels, it simplifies market analysis and aids in strategy development. With its flexible structure and clear visualization, it can be effectively used across all timeframes.

6 dakika önce

Sürüm Notları

This indicator is written for Support Resistance Traders

Window Seasonality IndicatorThis is a time window seasonal returns indicator. That is, it will provide the mean returns for a given time window based on a given number of lookbacks set by the user. The script finds matching time windows, e.g., 1st week of March going back 5 years or 9:00-10:00 window of every day going 50 days, and then calculates an average return for that window close price with respect to the close price in the immediately preceding time window, e.g. last week of February or 8:00-9:00 close price, respectively.

There are 4 input options: