MA Bands with Dynamic ColorsThe chart displays the 50-day, 100-day, and 200-day moving averages (MAs).

When the 50-day MA is above both the 100-day and 200-day MAs, the chart turns green, indicating a bullish trend with increasing positive momentum.

Conversely, when the 50-day MA is below the 100-day and 200-day MAs, the chart turns red, signaling a bearish trend with negative momentum.

This color-coded system, with green and red clouds, helps traders identify the trend direction and gauge positive or negative momentum for potential trading opportunities.

Trendindicator

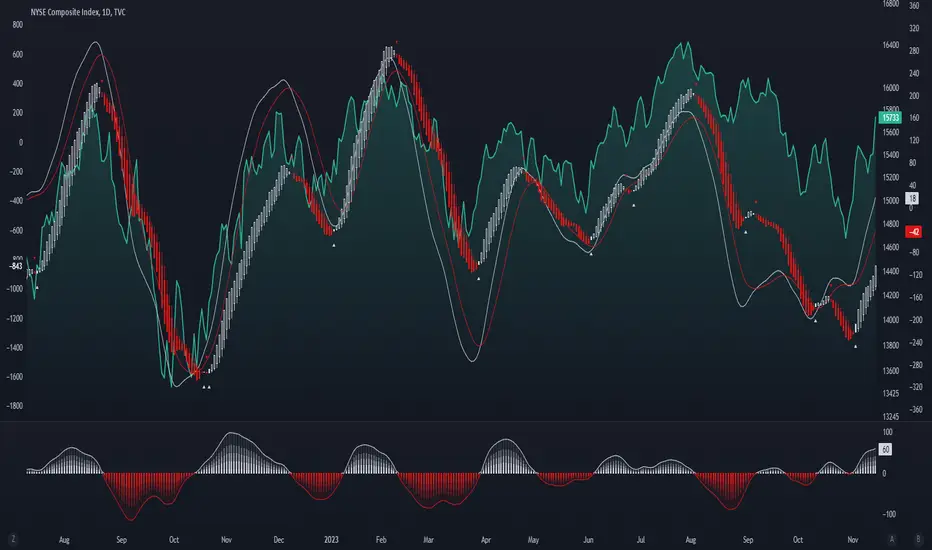

Trend Strength Oscillator📌 What Is the Trend Strength Oscillator?

The Trend Strength Oscillator is a visual tool that helps traders understand the overall direction and strength of the market trend. Instead of using multiple indicators separately, this tool combines three trusted methods into one clear, color-coded bar chart. The bars change based on whether the market is strongly trending up, down, or just moving sideways.

Imagine it as a traffic light for trading:

• Green means it’s safe to consider buying (strong uptrend).

• Red means consider selling or avoiding longs (strong downtrend).

• Gray means wait, the market isn’t clearly trending.

🧠 How It Works — The 3 Main Components

1. EMA Slope

The EMA (Exponential Moving Average) tracks the average price but reacts more quickly to changes. If the EMA is rising, it means the market is likely moving upward. If it’s falling, the trend is likely downward.

2. RSI Direction

RSI (Relative Strength Index) measures momentum. This tool compares the RSI to its smoothed average. If the RSI is above its average, momentum is up. If it’s below, momentum is down.

3. ADX Strength

ADX (Average Directional Index) measures how strong a trend is, not the direction. So even if EMA and RSI agree on a trend, the ADX must confirm it’s strong enough to be worth trading.

Only when all three indicators agree do we consider it a strong trend.

🧮 What the Oscillator Shows

The result of combining those components is a number that becomes a colored bar:

• +2 means all three signals are bullish → green bar.

• -2 means all three signals are bearish → red bar.

• Anything else (e.g., mixed signals or weak ADX) → gray bar.

This makes the chart super easy to read at a glance, even for beginners.

📈 How to Use It in Trading

You can use the Trend Strength Oscillator in a few simple ways:

• Entering Trades:

Look for a green bar when you want to buy or go long. Look for a red bar when you want to sell or go short. These bars mean all systems are “go” in the same direction.

• Avoiding Mistakes:

If the bar is gray, it’s a warning that the market is undecided or weak. It’s often better to wait for a clearer signal rather than force a trade.

• Managing Existing Trades:

If you’re in a trade and the bar color shifts back to gray, that can be a clue that the trend is losing strength. You might tighten your stop-loss or take some profit.

🧭 Final Thoughts

This indicator doesn’t give you a trade entry every few minutes. Instead, it helps you stay on the right side of strong moves and avoid choppy or sideways markets. It’s especially helpful for:

• Trend-following traders

• People who want clean, simple visuals

• Beginners who get overwhelmed with too many indicators

Let me know if you'd like to see this paired with another tool like volume or MACD, or if you’d like a chart screenshot to visualize how this looks live.

Regime Filter IndicatorRegime Filter – Crypto Market Trend Indicator

📊 Overview

The Regime Filter is a powerful market analysis indicator designed specifically for crypto trading. It helps traders identify whether the market is in a bullish or bearish phase by analyzing key assets in the cryptocurrency market, including Bitcoin (BTC), Bitcoin Dominance (BTC.D), and the Altcoin Market (TOTAL3). The indicator compares these assets against their respective Simple Moving Averages (SMA) to determine the overall market regime, allowing traders to make more informed decisions.

🔍 How It Works

The Regime Filter evaluates three main components to determine the market's sentiment:

1. BTC Dominance (BTC.D) vs. 40 SMA (Medium Timeframe)

The Bitcoin Dominance (BTC.D) is compared to its 40-period SMA on a mid-timeframe (e.g.,

1-hour). If BTC.D is below the 40 SMA, it indicates that altcoins are performing well relative

to Bitcoin, suggesting a bullish altcoin market. If BTC.D is above the 40 SMA, Bitcoin is

gaining dominance, indicating a potential bearish phase for altcoins.

2. TOTAL3 Market Cap vs. 100 SMA (Medium Timeframe)

The TOTAL3 index, which tracks the total market capitalization of all cryptocurrencies except

Bitcoin and Ethereum, is compared to its 100-period SMA. A bullish signal occurs when TOTAL3

is above the 100 SMA, indicating strength in altcoins, while a bearish signal occurs when

TOTAL3 is below the 100 SMA, signaling a potential weakness in the altcoin market.

3. BTC Price vs. 200 SMA (Higher Timeframe)

The current Bitcoin price is compared to its 200-period Simple Moving Average (SMA) on a

higher timeframe (e.g., 4-hour). A bullish signal is given when the BTC price is above the 200

SMA, and a bearish signal when it's below.

🟢 Bullish Market Conditions

The market is considered bullish when:

- BTC Dominance (BTC.D) is below the 40 SMA, suggesting altcoins are gaining momentum.

- TOTAL3 Market Cap is above the 100 SMA, signaling strength in the altcoin market.

- BTC price is above the 200 SMA, indicating an uptrend in Bitcoin.

In these conditions, the background turns green 🟢, and a "Bullish" label is displayed on the chart.

🔴 Bearish Market Conditions

The market is considered bearish when:

- BTC Dominance (BTC.D) is above the 40 SMA, indicating Bitcoin is outperforming altcoins.

- TOTAL3 Market Cap is below the 100 SMA, signaling weakness in altcoins.

- BTC price is below the 200 SMA, indicating a downtrend in Bitcoin.

In these conditions, the background turns red 🔴, and a "Bearish" label appears on the chart.

⚙ Customization Options

- The Regime Filter offers flexibility for traders:

- Enable or Disable Specific SMAs: Customize the indicator by enabling or disabling the 200 SMA for Bitcoin, the 40 SMA for BTC Dominance, and the 100 SMA for TOTAL3.

- Adjust Timeframes: Choose the timeframes for each of the moving averages to suit your preferred trading strategy.

- Real-Time Data Adjustments: The indicator updates in real-time to reflect current market conditions, ensuring timely analysis.

📈 Best Use Cases

- Trend Confirmation: The Regime Filter is ideal for confirming the market's overall trend,

helping traders to align their positions with the dominant market sentiment.

- Trade Entry/Exit Signals: Use the indicator to identify favorable entry or exit points based on

whether the market is in a bullish or bearish phase.

- Market Overview: Gain a quick understanding of the broader crypto market, with a focus on

Bitcoin and altcoins, to make more strategic decisions.

⚠️ Important Notes

Trend-Following Indicator: The Regime Filter is a trend-following tool, meaning it works best in strong trending markets. It may not perform well in choppy, sideways markets.

Risk Management: This indicator is designed to assist in identifying market trends, but it does not guarantee profits. Always apply sound risk management strategies and use additional indicators when making trading decisions.

Not a Profit Guarantee: While this indicator can help identify potential market trends, no trading tool or strategy guarantees profits. Please trade responsibly and ensure that your decisions are based on comprehensive analysis and risk tolerance.

SuperTrend MTF Pro [Cometreon]The SuperTrend MTF Pro takes the classic SuperTrend to a whole new level of customization and accuracy. Unlike the standard version, this indicator allows you to select different moving averages, apply it to various chart types, and fine-tune every key parameter.

If you're looking for an advanced, non-repainting, and highly configurable SuperTrend, this is the right choice for you.

🔷 New Features and Improvements

🟩 Multi-MA SuperTrend

Now you can customize the SuperTrend calculation by choosing from 15 different moving averages:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

🟩 Multiple Chart Types

You're no longer limited to candlestick charts! Now you can use SuperTrend with different chart formats, including:

Heikin Ashi

Renko

Kagi

Line Break

Point & Figure

🟩 Customizable Timeframe

Now you can adjust the SuperTrend timeframe without repainting issues, avoiding signal distortions.

🔷 Technical Details and Customizable Inputs

SuperTrend offers multiple customization options to fit any trading strategy:

1️⃣ ATR Period – Defines the ATR length, affecting the indicator’s sensitivity.

2️⃣ Source – Selects the price value used for calculations (Close, HL2, Open, etc.).

3️⃣ ATR Mult – Multiplies the ATR to determine band distance. Higher values reduce false signals, lower values make it more reactive.

4️⃣ Change ATR Calculation Method – When enabled, uses the default ATR method; when disabled, allows selecting another Moving Average with "Use Different Type".

5️⃣ Source Break – Defines the price source for trend changes (Close for more stability, High/Low for more reactivity).

6️⃣ Use Different Type – Allows selecting an alternative Moving Average for ATR calculation if "Change ATR Calculation Method" is disabled.

7️⃣ SuperTrend Type – Advanced options for specific MAs (JMA, ALMA, FRAMA, VIDYA), with dedicated parameters like Phase, Sigma, and Offset for optimized responsiveness.

8️⃣ Ticker Settings – Customize parameters for special chart types such as Renko, Heikin Ashi, Kagi, Line Break, and Point & Figure, adjusting reversal, number of lines, and ATR length.

9️⃣ Timeframe – Enables using SuperTrend on a higher timeframe.

🔟 Wait for Timeframe Closes -

✅ Enabled – Prevents multiple signals, useful for precise alerts.

❌ Disabled – Displays SuperTrend smoothly without interruptions.

🔷 How to Use SuperTrend MTF Pro

🔍 Identifying Trends

SuperTrend follows the ongoing trend and provides clear visual signals:

When the price is above the line, the trend is bullish.

When the price is below the line, the trend is bearish.

📈 Interpreting Signals

Line color and position change → Possible trend reversal

Bounce off the line → Potential trend continuation

Strong breakout of the line → Possible reversal

🛠 Integration with Other Tools

RSI or MACD to filter false signals

Moving Averages to confirm trend direction

Support and Resistance to improve entry points

☄️ If you find this indicator useful, leave a Boost to support its development!

Every feedback helps to continuously improve the tool, offering an even more effective trading experience. Share your thoughts in the comments! 🚀🔥

Trend Speed Analyzer (Zeiierman)█ Overview

The Trend Speed Analyzer by Zeiierman is designed to measure the strength and speed of market trends, providing traders with actionable insights into momentum dynamics. By combining a dynamic moving average with wave and speed analysis, it visually highlights shifts in trend direction, market strength, and potential reversals. This tool is ideal for identifying breakout opportunities, gauging trend consistency, and understanding the dominance of bullish or bearish forces over various timeframes.

█ How It Works

The indicator employs a Dynamic Moving Average (DMA) enhanced with an Accelerator Factor, allowing it to adapt dynamically to market conditions. The DMA is responsive to price changes, making it suitable for both long-term trends and short-term momentum analysis.

Key components include:

Trend Speed Analysis: Measures the speed of market movements, highlighting momentum shifts with visual cues.

Wave Analysis: Tracks bullish and bearish wave sizes to determine market strength and bias.

Normalized Speed Values: Ensures consistency across different market conditions by adjusting for volatility.

⚪ Average Wave and Max Wave

These metrics analyze the size of bullish and bearish waves over a specified Lookback Period:

Average Wave: This represents the mean size of bullish and bearish movements, helping traders gauge overall market strength.

Max Wave: Highlights the largest movements within the period, identifying peak momentum during trend surges.

⚪ Current Wave Ratio

This feature compares the current wave's size against historical data:

Average Wave Ratio: Indicates if the current momentum exceeds historical averages. A value above 1 suggests the trend is gaining strength.

Max Wave Ratio: Shows whether the current wave surpasses previous peak movements, signaling potential breakouts or trend accelerations.

⚪ Dominance

Dominance metrics reveal whether bulls or bears have controlled the market during the Lookback Period:

Average Dominance: Compares the net difference between average bullish and bearish wave sizes.

Max Dominance: Highlights which side had the stronger individual waves, indicating key power shifts in market dynamics.

Positive values suggest bullish dominance, while negative values point to bearish control. This helps traders confirm trend direction or anticipate reversals.

█ How to Use

Identify Trends: Leverage the color-coded candlesticks and dynamic trend line to assess the overall market direction with clarity.

Monitor Momentum: Use the Trend Speed histogram to track changes in momentum, identifying periods of acceleration or deceleration.

Analyze Waves: Compare the sizes of bullish and bearish waves to identify the prevailing market bias and detect potential shifts in sentiment. Additionally, fluctuations in Current Wave ratio values should be monitored as early indicators of possible trend reversals.

Evaluate Dominance: Utilize dominance metrics to confirm the strength and direction of the current trend.

█ Settings

Maximum Length: Sets the smoothing of the trend line.

Accelerator Multiplier: Adjusts sensitivity to price changes.

Lookback Period: Defines the range for wave calculations.

Enable Table: Displays statistical metrics for in-depth analysis.

Enable Candles: Activates color-coded candlesticks.

Collection Period: Normalizes trend speed values for better accuracy.

Start Date: Limits calculations to a specific timeframe.

Timer Option: Choose between using all available data or starting from a custom date.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Weighted CG Oscillator with ATRATR-Weighted CG Oscillator

The ATR-Weighted CG Oscillator is an enhanced version of the Center of Gravity (CG) Oscillator, originally developed by John Ehlers . By adding the Average True Range (ATR) to dynamically adjust the oscillator’s values based on market volatility, this indicator aims to make trend signals more responsive to price changes, offering an adaptive tool for trend analysis.

Functionality Overview :

The CG Oscillator, a classic trend-following indicator, has been modified here to incorporate the ATR for improved context and adaptability in different market conditions. The indicator calculates the CG Oscillator and scales it by dividing the ATR by the closing price to normalize for volatility. This creates a “weighted” CG Oscillator that generates more contextually relevant signals. A colored line shows green for long signals (above the long threshold), red for short signals (below the short threshold), and gray for neutral conditions.

Input Parameters :

CGO Length : Sets the period of the CG Oscillator calculation.

ATR Length : Determines the period of the ATR calculation. Longer periods smooth out the volatility impact.

Long Threshold : The threshold that triggers a long signal; a long (green) signal occurs when the weighted CG Oscillator crosses above this level.

Short Threshold : The threshold that triggers a short signal; a short (red) signal occurs when the weighted CG Oscillator crosses below this level.

Source : Specifies the data source for CG Oscillator calculations, with the default set to the closing price.

Recommended Use :

This indicator is designed to be an adaptive tool, not your sole resource. To ensure its effectiveness, it’s essential to backtest the indicator on your chosen asset over your preferred timeframe. Market dynamics vary, so testing the indicator’s parameters—especially the thresholds—will allow you to find the settings that best suit your strategy. While the default values work well for some scenarios, customizing the settings will help align the indicator with your unique trading style and the asset’s characteristics.

Depth Trend Indicator - RSIDepth Trend Indicator - RSI

This indicator is designed to identify trends and gauge pullback strength by combining the power of RSI and moving averages with a depth-weighted calculation. The script was created by me, Nathan Farmer and is based on a multi-step process to determine trend strength and direction, adjusted by a "depth" factor for more accurate signal analysis.

How It Works

Trend Definition Using RSI: The RSI Moving Average ( rsiMa ) is calculated to assess the current trend, using customizable parameters for the RSI Period and MA Period .

Trends are defined as follows:

Uptrend : RSI MA > Critical RSI Value

Downtrend : RSI MA < Critical RSI Value

Pullback Depth Calculation: To measure pullback strength relative to the current trend, the indicator calculates a Depth Percentage . This is defined as the portion of the gap between the moving average and the price covered by a pullback.

Depth-Weighted RSI Calculation: The Depth Percentage is then applied as a weighting factor on the RSI Moving Average , giving us a Weighted RSI line that adjusts to the depth of pullbacks. This line is rather noisy, and as such we take a moving average to smooth out some of the noise.

Key Parameters

RSI Period : The period for RSI calculation.

MA Period : The moving average period applied to RSI.

Price MA Period : Determines the SMA period for price, used to calculate pullback depth.

Smoothing Length : Length of smoothing applied to the weighted RSI, creating a more stable signal.

RSI Critical Value : The critical value (level) used in determining whether we're in an uptrend or a downtrend.

Depth Critical Value : The critical value (level) used in determining whether or not the depth weighted value confirms the state of a trend.

Notes:

As always, backtest this indicator and modify the parameters as needed for your specific asset, over your specific timeframe. I chose these defaults as they worked well on the assets I look at, but it is likely you tend to look at a different group of assets over a different timeframe than what I do.

Large pullbacks can create large downward spikes in the weighted line. This isn't graphically pleasing, but I have tested it with various methods of normalization and smoothing and found the simple smoothing used in the indicator to be best despite this.

Custom Supertrend Multi-Timeframe Indicator [Pineify]Supertrend Multi-Timeframe Indicator

Introduction

The Supertrend Multi-Timeframe Indicator is an advanced trading tool designed to help traders identify trend directions and potential buy/sell signals by combining Supertrend indicators from multiple timeframes. This script is original in its approach to integrating Supertrend calculations across different timeframes, providing a more comprehensive view of market trends.

Concepts and Calculations

The indicator utilizes the Supertrend algorithm, which is based on the Average True Range (ATR). The Supertrend is a popular tool for trend-following strategies, and this script enhances its capabilities by incorporating data from a larger timeframe.

Supertrend Factor: Determines the sensitivity of the Supertrend line.

ATR Length: Defines the period for calculating the Average True Range.

Larger Supertrend Factor and ATR Length: Applied to the larger timeframe for a broader trend perspective.

Larger Timeframe: The higher timeframe from which the secondary Supertrend data is sourced.

How It Works

The script calculates the Supertrend for the current timeframe using the specified factor and ATR length.

Simultaneously, it requests Supertrend data from a larger timeframe.

Buy and sell signals are generated based on crossovers and crossunders of the Supertrend lines from both timeframes.

Visual cues (up and down arrows) are plotted on the chart to indicate buy and sell signals.

Background colors change to reflect the trend direction: green for an uptrend and red for a downtrend.

Usage

Add the indicator to your TradingView chart.

Customize the Supertrend factors, ATR lengths, and larger timeframe according to your trading strategy.

Enable or disable buy and sell alerts as needed.

Monitor the chart for visual signals and background color changes to make informed trading decisions.

Note: The indicator is best used in conjunction with other technical analysis tools and should not be relied upon as the sole basis for trading decisions.

Conclusion

The Supertrend Multi-Timeframe Indicator offers a unique and powerful way to analyze market trends by leveraging the strengths of the Supertrend algorithm across multiple timeframes. Its customizable settings and clear visual signals make it a valuable addition to any trader's toolkit.

Dynamic Momentum GaugeOverview

The Dynamic Momentum Gauge is an indicator designed to provide information and insights into the trend and momentum of a financial asset. While this indicator is not directional , it helps you know when there will be a trend, big move, or when momentum will have a run, and when you should take profits.

How It Works

This indicator calculates momentum and then removes the negative values to focus instead on when the big trend could likely happen and when it could end, or when you should enter a trade based on momentum or exit. Traders can basically use this indicator to time their market entries or exits, and align their strategies with momentum dynamics.

How To Use

As previously mentioned, this is not a directional indicator but more like a timing indicator. This indicator helps you find when the trend moves, and big moves in the markets will occur and its possibly best to exit the trades. For example, if you decide to enter a long trade if the Dynamic Momentum Gauge value is at an extreme low and another momentum indicator that you use has conditions that you would consider to long with, then this indicator is basically telling you that there isn't more space for the momentum to squeeze any longer, can only really expand from that point or stay where it currently is, but this is also a mean reverting process so it does tend to go back up from the low point.

Settings:

Length: This is the length of the momentum, by default its at 100.

Normalization Length: Length of the Normalization which ensures the the values fall within a consistent range.

Highest-Lowest Trend𝙃𝙄𝙂𝙃𝙀𝙎𝙏-𝙇𝙊𝙒𝙀𝙎𝙏 𝙏𝙍𝙀𝙉𝘿 𝙄𝙉𝘿𝙄𝘾𝘼𝙏𝙊𝙍

Overview:

The "Highest-Lowest Trend" indicator helps traders identify trends based on the highest and lowest values within a specified period. It provides visual cues to understand potential trend changes, making it a valuable tool for technical analysis.

Settings:

Length and Offset: Adjust the length and offset parameters to customize the sensitivity of the indicator.

Source: Determines whether to use the high and low prices or the closing price and others for calculations.

Visual Settings:

Bar Color: Enables or disables the coloring of bars based on the trend direction.

Up Color: Specifies the color for upward trends.

Down Color: Specifies the color for downward trends.

Indicator Calculation:

The indicator calculates the highest and lowest values within the defined length and offset.

The current trend is determined based on whether the closing price is above or below these values.

When the source crossed above highest indicator changes trend to upside and start to use lowest value and vice versa.

/// 𝙄𝙉𝘿𝙄𝘾𝘼𝙏𝙊𝙍 𝘾𝘼𝙇𝘾𝙐𝙇𝘼𝙏𝙄𝙊𝙉 ///

var series float hlt = 0.0

series float upper = ta.highest(Use_High_and_Low ? high : src, length)

series float lower = ta.lowest( Use_High_and_Low ? high : src, length)

hlt := src > upper ?

lower : src < lower ?

upper : nz(hlt)

Usage:

Trend Identification: Watch for price to be above Trend Indicator crosses for up trend and below for down trend.

Length and Offset: Adjust the length and offset parameters to customize the sensitivity of the indicator.

Color, color bars: Change color of trends and bars for your taste

Note:

Trading involves inherent risks, and it is essential to exercise caution and employ multiple tools and indicators for comprehensive analysis. While the "Highest-Lowest Trend" indicator provides valuable insights into potential trend changes, relying solely on one tool for trading decisions is not recommended. Market conditions can be dynamic, and using a combination of indicators can enhance your overall analysis, providing a more robust foundation for decision-making. Always consider the broader market context, risk management strategies, and other relevant factors before executing trades.

SuperTrend ToolkitThe SuperTrend Toolkit (Super Kit) introduces a versatile approach to trend analysis by extending the application of the SuperTrend indicator to a wide array of @TradingView's built-in or Community Scripts . This tool facilitates the integration of the SuperTrend algorithm with various indicators, including oscillators, moving averages, overlays, and channels.

Methodology:

The SuperTrend, at its core, calculates a trend-following indicator based on the Average-True-Range (ATR) and price action. It creates dynamic support and resistance levels, adjusting to changing market conditions, and aiding in trend identification.

pine_st(simple float factor = 3., simple int length = 10) =>

float atr = ta.atr(length)

float up = hl2 + factor * atr

up := up < nz(up ) or close > nz(up ) ? up : nz(up )

float lo = hl2 - factor * atr

lo := lo > nz(lo ) or close < nz(lo ) ? lo : nz(lo )

int dir = na

float st = na

if na(atr )

dir := 1

else if st == nz(up )

dir := close > up ? -1 : 1

else

dir := close < lo ? 1 : -1

st := dir == -1 ? lo : up

@TradingView's native SuperTrend lacks the flexibility to incorporate different price sources into its calculation.

Community scripts, addressed the limitation by implementing the option to input different price sources, for example, one of the most popular publications, @KivancOzbilgic's SuperTrend script.

In May 2023, @TradingView introduced an update allowing the passing of another indicator's plot as a source value via the input.source() function. However, the built-in ta.atr function still relied on the chart's price data, limiting the formerly mentioned scripts to the chart's price data alone.

Unique Approach -

This script addresses the aforementioned limitations by processing the data differently.

Firstly we create a User-Defined-Type (UDT) replicating a bar's open, high, low, close (OHLC) values.

type bar

float o = open

float h = high

float l = low

float c = close

We then use this type to store the external input data.

src = input.source(close, "External Source")

bar b = bar.new(

nz(src ) , open 𝘷𝘢𝘭𝘶𝘦

math.max(nz(src ), src), high 𝘷𝘢𝘭𝘶𝘦

math.min(nz(src ), src), low 𝘷𝘢𝘭𝘶𝘦

src ) close 𝘷𝘢𝘭𝘶𝘦

Finally, we pass the data into our custom built SuperTrend with ATR functions to derive the external source's version of the SuperTrend indicator.

supertrend st = b.st(mlt, len)

- Setup Guide -

Utility and Use Cases:

Universal Compatibility - Apply SuperTrend to any built-in indicator or script, expanding its use beyond traditional price data.

- A simple example on one of my own public scripts -

Trend Analysis - Gain additional trend insights into otherwise mainly mean reverting or volume indicators.

- Alerts Setup Guide -

The Super Kit empowers traders and analysts with a tool that adapts the robust SuperTrend algorithm to a myriad of indicators, allowing comprehensive trend analysis and strategy development.

Enhanced McClellan Summation Index

The Enhanced McClellan Summation Index (MSI) is a comprehensive tool that transforms the MSI indicator with Heikin-Ashi visualization, offering improved trend analysis and momentum insights. This indicator includes MACD and it's histogram calculations to refine trend signals, minimize false positives and offer additional momentum analysis.

Methodology:

McClellan Summation Index (MSI) -

The MSI begins by calculating the ratio between advancing and declining issues in the specified index.

float decl = 𝘐𝘯𝘥𝘪𝘤𝘦 𝘥𝘦𝘤𝘭𝘪𝘯𝘪𝘯𝘨 𝘪𝘴𝘴𝘶𝘦𝘴

float adv = 𝘐𝘯𝘥𝘪𝘤𝘦 𝘢𝘥𝘷𝘢𝘯𝘤𝘪𝘯𝘨 𝘪𝘴𝘴𝘶𝘦𝘴

float ratio = (adv - decl) / (adv + decl)

It then computes a cumulative sum of the MACD (the difference between a 19-period EMA and a 39-period EMA) of this ratio. The result is a smoothed indicator reflecting market breadth and momentum.

macd(float r) =>

ta.ema(r, 19) - ta.ema(r, 39)

float msi = ta.cum(macd(ratio))

Heikin-Ashi Transformation -

Heikin-Ashi is a technique that uses a modified candlestick formula to create a smoother representation of price action. It averages the open, close, high, and low prices of the current and previous periods. This transformation reduces noise and provides a clearer view of trends.

type bar

float o = open

float h = high

float l = low

float c = close

bar b = bar.new()

float ha_close = math.avg(b.o, b.h, b.l, b.c)

MACD and Histogram -

The Enhanced MSI incorporates MACD and histogram calculations to provide additional momentum analysis and refine trend signals. The MACD represents the difference between the 12-period EMA and the 26-period EMA of the MSI. The histogram is the visual representation of the difference between the MACD and its signal line.

Options:

Index Selection - Choose from TVC:NYA , NASDAQ:NDX , or TVC:XAX to tailor the MSI-HA to the desired market index.

MACD Settings - Adjust the parameters for the MACD calculation to fine-tune the indicator's responsiveness.

Ratio Multiplier - Apply scaling to the MSI to suit different market conditions and indices.

Benefits of Heikin-Ashi -

Smoothed Trends - Heikin-Ashi reduces market noise, providing a more apparent and smoothed representation of trends.

Clearer Patterns - Candlestick patterns are more distinct, aiding in the identification of trend reversals and continuations.

Utility and Use Cases:

Trend & Momentum Analysis - Utilize the tool's Heikin-Ashi visualization for clearer trend identification in confluence with it's MACD and histogram to gain additional insights into the strength and direction of trends, while filtering out potential false positives.

Breadth Analysis - Explore market breadth through the MSI's cumulative breadth indicator, gauging the overall health and strength of the underlying market.

- Alerts Setup Guide -

The Enhanced MSI is a robust indicator that combines the breadth analysis of the McClellan Summation Index with the clarity of Heikin-Ashi visualization and additional momentum insights from MACD and histogram calculations. Its customization options make it adaptable to various indices and market conditions, offering traders a comprehensive tool for trend and momentum analysis.

Standardized SuperTrend Oscillator

The Standardized SuperTrend Oscillator (SSO) is a versatile tool that transforms the SuperTrend indicator into an oscillator, offering both trend-following and mean reversion capabilities. It provides deeper insights into trends by standardizing the SuperTrend with respect to its upper and lower bounds, allowing traders to identify potential reversals and contrarian signals.

Methodology:

Lets begin with describing the SuperTrend indicator, which is the fundamental tool this script is based on.

SuperTrend:

The SuperTrend is calculated based on the average true range (ATR) and multiplier. It identifies the trend direction by placing a line above or below the price. In an uptrend, the line is below the price; in a downtrend, it's above the price.

pine_st(float src = hl2, float factor = 3., simple int len = 10) =>

float atr = ta.atr(len)

float up = src + factor * atr

up := up < nz(up ) or close > nz(up ) ? up : nz(up )

float lo = src - factor * atr

lo := lo > nz(lo ) or close < nz(lo ) ? lo : nz(lo )

int dir = na

float st = na

if na(atr )

dir := 1

else if st == nz(up )

dir := close > up ? -1 : 1

else

dir := close < lo ? 1 : -1

st := dir == -1 ? lo : up

SSO Oscillator:

The SSO is derived from the SuperTrend and the source price. It calculates the standardized difference between the SuperTrend and the source price. The standardization is achieved by dividing this difference by the distance between the upper and lower bounds of the SuperTrend.

float sso = (src - st) / (up - lo)

Components and Features:

SuperTrend of Oscillator - An additional SuperTrend based on the direction and volatility of the oscillator, behaving as the SuperTrend OF the SuperTrend. This provides further trend analysis of the underlying broad trend regime.

Reversion Tracer - The RSI of the direction of the original SuperTrend, providing a dynamic threshold for premium and discount price areas.

float rvt = ta.rsi(dir, len)

Heikin Ashi Transform - An option to apply the Heikin Ashi transform to the source price of the oscillator, providing a smoother visual representation of trends.

Display Modes - Choose between Line mode for a standard oscillator view or Candle mode, displaying the oscillator as Heikin Ashi candles for more in-depth trend analysis.

Contrarian and Reversion Signals:

Contrarian Signals - Based on the SuperTrend of the oscillator, these signals can act as potential buy or sell indications, highlighting potential trend exhaustion or premature reversals.

Reversion Signals - Generated when the oscillator crosses above or below the Reversion Tracer, signaling potential mean reversion opportunities or trend breakouts.

Utility and Use Cases:

Trend Analysis - Utilize the SSO as a trend-following tool with the added benefits of the oscillator's SuperTrend and Heikin Ashi transform.

Valuation Analysis - Leverage the oscillator's reversion signals for identifying potential mean reversion opportunities in the market.

The Standardized SuperTrend Oscillator enhances the capabilities of the SuperTrend indicator, offering a balanced approach to both trend-following and mean reversion strategies. Its customizable options and contrarian signals make it a valuable instrument for traders seeking comprehensive trend analysis and potential reversal signals.

AI Moving Average (Expo)█ Overview

The AI Moving Average indicator is a trading tool that uses an AI-based K-nearest neighbors (KNN) algorithm to analyze and interpret patterns in price data. It combines the logic of a traditional moving average with artificial intelligence, creating an adaptive and robust indicator that can identify strong trends and key market levels.

█ How It Works

The algorithm collects data points and applies a KNN-weighted approach to classify price movement as either bullish or bearish. For each data point, the algorithm checks if the price is above or below the calculated moving average. If the price is above the moving average, it's labeled as bullish (1), and if it's below, it's labeled as bearish (0). The K-Nearest Neighbors (KNN) is an instance-based learning algorithm used in classification and regression tasks. It works on a principle of voting, where a new data point is classified based on the majority label of its 'k' nearest neighbors.

The algorithm's use of a KNN-weighted approach adds a layer of intelligence to the traditional moving average analysis. By considering not just the price relative to a moving average but also taking into account the relationships and similarities between different data points, it offers a nuanced and robust classification of price movements.

This combination of data collection, labeling, and KNN-weighted classification turns the AI Moving Average (Expo) Indicator into a dynamic tool that can adapt to changing market conditions, making it suitable for various trading strategies and market environments.

█ How to Use

Dynamic Trend Recognition

The color-coded moving average line helps traders quickly identify market trends. Green represents bullish, red for bearish, and blue for neutrality.

Trend Strength

By adjusting certain settings within the AI Moving Average (Expo) Indicator, such as using a higher 'k' value and increasing the number of data points, traders can gain real-time insights into strong trends. A higher 'k' value makes the prediction model more resilient to noise, emphasizing pronounced trends, while more data points provide a comprehensive view of the market direction. Together, these adjustments enable the indicator to display only robust trends on the chart, allowing traders to focus exclusively on significant market movements and strong trends.

Key SR Levels

Traders can utilize the indicator to identify key support and resistance levels that are derived from the prevailing trend movement. The derived support and resistance levels are not just based on historical data but are dynamically adjusted with the current trend, making them highly responsive to market changes.

█ Settings

k (Neighbors): Number of neighbors in the KNN algorithm. Increasing 'k' makes predictions more resilient to noise but may decrease sensitivity to local variations.

n (DataPoints): Number of data points considered in AI analysis. This affects how the AI interprets patterns in the price data.

maType (Select MA): Type of moving average applied. Options allow for different smoothing techniques to emphasize or dampen aspects of price movement.

length: Length of the moving average. A greater length creates a smoother curve but might lag recent price changes.

dataToClassify: Source data for classifying price as bullish or bearish. It can be adjusted to consider different aspects of price information

dataForMovingAverage: Source data for calculating the moving average. Different selections may emphasize different aspects of price movement.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Standardized MACD Heikin-Ashi TransformedThe Standardized MACD Heikin-Ashi Transformed (St. MACD) is an advanced indicator designed to overcome the limitations of the traditional MACD. It offers a more robust and standardized measure of momentum, making it comparable across different timeframes and securities. By incorporating the Heikin-Ashi transformation, the St. MACD provides a smoother visualization of trends and potential reversals, enhancing its utility for traders seeking a clearer view of the underlying market direction.

Methodology:

The calculation of St. MACD begins with the traditional MACD, which computes the difference between two exponential moving averages (EMAs) of the price. To address the issue of non-comparability across assets, the St. MACD normalizes its values using the exponential average of the price's height. This normalization process ensures that the indicator's readings are not influenced by the absolute price levels, allowing for objective and quantitatively defined comparisons of momentum strength.

Furthermore, St. MACD utilizes the Heikin-Ashi transformation, which involves deriving candles from the price data. These Heikin-Ashi candles provide a smoother representation of trends and help filter out noise in the market. A predictive curve of Heikin-Ashi candles within the St. MACD turns blue or red, indicating the prevailing trend direction. This feature enables traders to easily identify trend shifts and make better informed trading decisions.

Advantages:

St. MACD offers several key advantages over the traditional MACD-

Standardization: By normalizing the indicator's values, St. MACD becomes comparable across different assets and timeframes. This makes it a valuable tool for traders analyzing various markets and seeking consistent momentum measurements.

Heikin-Ashi Transformation: The integration of the Heikin-Ashi transformation smoothes out the indicator's fluctuations and enhances trend visibility. Traders can more easily identify trends and potential reversal points, improving their market analysis.

Quantifiable Momentum: St. MACD's key levels represent the strength of momentum, providing traders with a quantifiable framework to gauge the intensity of market movements. This feature helps identify periods of increased or decreased momentum.

Utility:

The St. MACD indicator offers versatile utility for traders-

Trend Identification: Traders can use the color-coded predictive curve of Heikin-Ashi candles to swiftly determine the prevailing trend direction. This aids in identifying potential entry and exit points in the market.

Reversal Signals: Colored extremes within the St. MACD signal potential price reversals, alerting traders to potential turning points in the market. This assists in making timely decisions during market inflection points.

Overbought/Oversold Conditions: The histogram version of St. MACD can be used in conjunction with the bands to detect short-term overbought or oversold market conditions, allowing traders to adjust their strategies accordingly.

In conclusion, this tool addresses the limitations of the traditional MACD by providing a standardized and comparable momentum indicator. Its incorporation of the Heikin-Ashi transformation enhances trend visibility and assists traders in making more informed decisions. With its quantifiable momentum measurements and various utility features, the St. MACD is a valuable tool for traders seeking a clearer and more objective view of market trends and reversals.

Key Features:

Display Modes: MACD, Histogram or Hybrid

Reversion Triangles by adjustable thresholds

Bar Coloring Methods: MidLine, Candles, Signal Cross, Extremities, Reversions

Example Charts:

-Traditional limitations-

-Comparisons across time and securities-

-Showcase-

See Also:

-Other Heikin-Ashi Transforms-

Days Higher Than Current PriceThe "Days Higher Than Current Price" indicator is a color-coded tool that provides insights into the historical price performance of an underlying asset. By analyzing the number of bars prior to the selected day that had higher closing prices, this indicator visually represents the comparative strength or weakness of the current price level.

The "Days Higher" indicator utilizes a color-coded scheme to indicate the number of days in the asset's price history where the closing prices were higher than the current day's price. The color spectrum ranges from red to blue, representing varying levels of historical price strength.

Color Coding:

The color coding scheme of the indicator offers a quick and intuitive understanding of the price performance:

Red: Represents a higher number of days in the asset's price history where the closing prices were higher than the current day's price. This suggests a weaker price trend or a potential reversal and indicates relative price weakness.

Blue: Represents a lower number of days in the asset's price history where the closing prices were higher than the current day's price. This indicates a strong trend of higher prices and suggests relative price strength.

Orange & Green: Correspond to different numbers of days where the closing prices were higher than the current day's price. The specific color gradations between red and blue reflect increasing or decreasing historical price strength.

Methodology:

The "Days Higher" indicator examines each bar in the asset's price history leading up to the selected day. It counts the number of bars where the closing prices were higher than the current day's price.

The indicator then assigns a specific color to the price chart based on the count of such days, providing a visual representation of historical price strength relative to the current price level.

Utility:

The "Days Higher" indicator offers traders and investors a unique perspective on the historical price performance of an asset. By assessing the color-coded chart, market participants can quickly gauge the presence of strong or weak historical price trends.

This information can be used to identify potential support or resistance levels, assess the overall strength of a trend, or evaluate the likelihood of a price reversal. Traders may incorporate this indicator into their analysis to make more informed trading decisions based on the historical price strength indicated by the color-coded chart.

It is important to note that this tool should be used in conjunction with other technical analysis tools and indicators to validate signals and make well-rounded trading decisions.

Example Charts:

-Indices-

-Stocks-

-Cryptos-

-Multi-Timeframe-

On Balance Volume Heikin-Ashi Transformed

The OBV Heikin Ashi indicator is a modified version of the On-Balance Volume indicator that incorporates the Heikin Ashi transformation. This technical tool aims to provide traders with a smoother representation of volume dynamics and price trends.

The OBV Heikin Ashi indicator combines the principles of OBV and Heikin Ashi to offer insights into the volume and price behavior of an asset. Understanding OBV and Heikin Ashi individually will provide a foundation for comprehending the uniqueness and utility of this indicator.

On-Balance Volume:

OBV is a volume-based indicator that measures the cumulative buying and selling pressure in the market. It considers the relationship between volume and price movements to determine the overall strength and direction of a trend. Rising OBV values suggest bullish buying pressure, while falling values indicate bearish selling pressure.

Heikin Ashi:

Heikin Ashi is a Japanese candlestick charting technique that aims to filter out noise and provide a smoother representation of price trends. It calculates each candlestick based on the average of the previous candle's open, close, high, and low prices. Heikin Ashi candles can reveal the underlying trend more clearly by reducing market noise.

Methodology:

The 𝘖𝘉𝘝 𝘏-𝘈 indicator applies the Heikin Ashi transformation to the OBV values. Each OBV value is replaced with a Heikin Ashi equivalent, which is calculated based on the average of the previous Heikin Ashi candle's open and close prices. This transformation smooths out the OBV values and helps identify the overall trend with reduced noise. Additionaly, 2 optional EMAs are included for convergence-divergence analysis.

By applying the Heikin Ashi transformation to OBV, the indicator aims to enhance the readability of volume and trend information, providing traders with a clearer understanding of market dynamics.

Utility:

The 𝘖𝘉𝘝 𝘏-𝘈 indicator can be a valuable tool for traders and investors in analyzing volume and price trends. It offers a smoother representation of OBV values, allowing for easier identification of trend reversals, bullish or bearish market conditions, and potential trading opportunities. Traders can utilize the indicator to confirm price trends, validate support and resistance levels, and enhance their overall trading strategies.

It is worth noting that the effectiveness of the indicator may vary depending on the specific market and trading strategy. It is recommended to combine its analysis with other technical indicators and perform thorough backtesting before making trading decisions.

Key Features:

2 Adjustable EMAs

Normalized Oscillator Mode

Example Charts:

See Also:

Z-Score Heikin-Ashi Transformed

Z-Score Heikin-Ashi TransformedThe Z-Score Heikin-Ashi Transformed (𝘡 𝘏-𝘈) indicator is a powerful technical tool that combines the principles of Z-Score and Heikin Ashi to provide traders with a smoothed representation of price movements and a standardized measure of market volatility.

The 𝘡 𝘏-𝘈 indicator applies the Z-Score calculation to price data and then transforms the resulting Z-Scores using the Heikin Ashi technique. Understanding the individual components of Z-Score and Heikin Ashi will provide a foundation for comprehending the methodology and unique features of this indicator.

Z-Score:

Z-Score is a statistical measure that quantifies the distance between a data point and the mean, relative to the standard deviation. It provides a standardized value that allows traders to compare different data points on a common scale. In the context of the 𝘡 𝘏-𝘈 indicator, Z-Score is calculated based on price data, enabling the identification of extreme price movements and the assessment of their significance.

Heikin Ashi:

Heikin Ashi is a popular charting technique that aims to filter out market noise and provide a smoother representation of price trends. It involves calculating each candlestick based on the average of the previous candle's open, close, high, and low prices. This approach results in a chart that reduces the impact of short-term price fluctuations and reveals the underlying trend more clearly.

Methodology:

The 𝘡 𝘏-𝘈 indicator starts by calculating the Z-Score of the price data, which provides a standardized measure of how far each price point deviates from the mean. Next, the resulting Z-Scores are transformed using the Heikin Ashi technique. Each Z-Score value is modified according to the Heikin Ashi formula, which incorporates the average of the previous Heikin Ashi candle's open and close prices. This transformation smooths out the Z-Score values and reduces the impact of short-term price fluctuations, providing a clearer view of market trends.

This tool enables traders to identify significant price movements and assess their relative strength compared to historical data. Positive transformed Z-Scores indicate that prices are above the average, suggesting potential overbought conditions, while negative transformed Z-Scores indicate prices below the average, suggesting potential oversold conditions. Traders can utilize this information to identify potential reversals, confirm trend strength, and generate trading signals.

Utility:

The indicator offers valuable insights into price volatility and trend analysis. By combining the standardized measure of Z-Score with the smoothing effect of Heikin Ashi, traders can make more informed trading decisions and improve their understanding of market dynamics. 𝘡 𝘏-𝘈 can be used in various trading strategies, including identifying overbought or oversold conditions, confirming trend reversals, and establishing entry and exit points.

Note that the 𝘡 𝘏-𝘈 should be used in conjunction with other technical indicators and analysis tools to validate signals and avoid false positives. Additionally, traders are encouraged to conduct thorough backtesting and experimentation with different parameter settings to optimize the effectiveness of the indicator for their specific trading approach.

Key Features:

Optional Reversion Doritos

Adjustable Reversion Threshold

2 Adjustable EMAs

Example Charts:

See Also:

On Balance Volume Heikin-Ashi Transformed

Rough AverageThe Rough Average indicator is a unique technical tool that calculates a modified average to provide insights into market conditions. It incorporates a combination of mathematical operations and existing indicators to offer traders a different perspective on price movements.

The Rough Average indicator aims to capture market dynamics through a specific calculation method. It utilizes two main components: a check for the approximate scale of the price and a profile calculation based on the Relative Strength Index (RSI) of the closing price.

Methodology:

Approximate Scale: The indicator determines the approximate scale of the price by analyzing the magnitude of the closing price. This step involves a mathematical process that identifies the power of 10 that best represents the scale. This function reduces overall lag and gives a better smoothing to the output of the calculation

Profile Calculation: The indicator calculates a profile value by summing the absolute values of the RSI of the closing price over a specified period. The RSI provides insights into the strength or weakness of price movements. The profile calculation considers a range of prices based on the determined scale.

Indicator Calculation:

The Rough Average is derived by applying the Exponential Moving Average (EMA) to the calculated profile. The EMA is a smoothing technique that emphasizes recent price data. The resulting value represents the modified average of the indicator.

Utility:

The Rough Average indicator offers traders an alternative perspective on market conditions. By utilizing a modified average calculation, it can reveal potential trends, reversals, or periods of market strength or weakness. Traders can use the Rough Average to complement their analysis and identify possible trading opportunities.

It is important to note that the effectiveness of the Rough Average indicator may vary depending on the specific market and trading strategy. It is recommended to combine its analysis with other technical indicators and conduct thorough testing before making trading decisions.

Key Features:

Customizable OB\OS Levels

Bar coloring methods: Trend, Reversions, Extremities

Example Charts:

Major and Minor Trend Indicator by Nikhil34aScript Description:

This script is designed to provide a visual indication of the major and minor trends of an asset, along with potential buy and sell signals. It calculates two Simple Moving Averages (SMA): a longer-term 200-period SMA (Major SMA) and a shorter-term 20-period SMA (Minor SMA). The script determines whether the asset's closing price is above or below these moving averages to identify the major and minor trends. It also detects potential buying and selling opportunities based on the intersection of the asset's price with the SMA lines.

Usefulness:

This script can be useful for traders and investors who follow trend-based strategies and want to monitor the major and minor trends of an asset. By visually displaying the trends and potential buy and sell signals, it helps traders make informed decisions about entering or exiting positions.

Simple Explanation on BTC Chart:

In the context of a BTC chart, let's consider the following scenario:

BTC is currently trading above the 200-period SMA (Simple Moving Average), which is located at 29,059.

BTC is trading below the 20-period SMA, positioned at 30,178.

The current price of BTC is 29,916.

Based on this information, we can conclude that:

The major trend is bullish since BTC is trading above the 200-period SMA.

The minor trend is bearish as BTC is trading below the 20-period SMA.

The intersection of the price with the moving averages indicates a potential selling opportunity.

Traders using this script would observe that BTC is in a bullish major trend, a bearish minor trend, and there is a possibility of a sell signal. They may consider these factors when making trading decisions, such as adjusting their positions or taking profits.

Remember to conduct your own analysis and consider additional factors before making any trading decisions.

Regularized-Moving-Average Oscillator SuiteThe Regularized-MA Oscillator Suite is a versatile indicator that transforms any moving average into an oscillator. It comprises up to 13 different moving average types, including KAMA, T3, and ALMA. This indicator serves as a valuable tool for both trend following and mean reversion strategies, providing traders and investors with enhanced insights into market dynamics.

Methodology:

The Regularized MA Oscillator Suite calculates the moving average (MA) based on user-defined parameters such as length, moving average type, and custom smoothing factors. It then derives the mean and standard deviation of the MA using a normalized period. Finally, it computes the Z-Score by subtracting the mean from the MA and dividing it by the standard deviation.

KAMA (Kaufman's Adaptive Moving Average):

KAMA is a unique moving average type that dynamically adjusts its smoothing period based on market volatility. It adapts to changing market conditions, providing a smoother response during periods of low volatility and a quicker response during periods of high volatility. This allows traders to capture trends effectively while reducing noise.

T3 (Tillson's Exponential Moving Average):

T3 is an exponential moving average that incorporates additional smoothing techniques to reduce lag and provide a more responsive indicator. It aims to maintain a balance between responsiveness and smoothness, allowing traders to identify trend reversals with greater accuracy.

ALMA (Arnaud Legoux Moving Average):

ALMA is a moving average type that utilizes a combination of linear regression and exponential moving average techniques. It offers a unique way of calculating the moving average by providing a smoother and more accurate representation of price trends. ALMA reduces lag and noise, enabling traders to identify trend changes and potential entry or exit points more effectively.

Z-Score:

The Z-Score calculation in the Regularized-MA Oscillator Suite standardizes the values of the moving average. It measures the deviation of each data point from the mean in terms of standard deviations. By normalizing the moving average through the Z-Score, the indicator enables traders to assess the relative position of price in relation to its mean and volatility. This information can be valuable for identifying overbought and oversold conditions, as well as potential trend reversals.

Utility:

The Regularized-MA Oscillator Suite with its unique moving average types and Z-Score calculation offers traders and investors powerful analytical tools. It can be used for trend following strategies by analyzing the oscillator's position relative to the midline. Traders can also employ it as a mean reversion tool by identifying peak values above user-defined deviations. These features assist in identifying potential entry and exit points, enhancing trading decisions and market analysis.

Key Features:

Variety of 13 MA types.

Potential reversal point bubbles.

Bar coloring methods - Trend (Midline cross), Extremities, Reversions, Slope

Example Charts:

David Varadi Intermediate OscillatorThe David Varadi Intermediate Oscillator (DVI) is a composite momentum oscillator designed to generate trading signals based on two key factors: the magnitude of returns over different time windows and the stretch, which measures the relative number of up versus down days. By combining these factors, the DVI aims to provide a reliable and objective assessment of market trends and momentum.

Methodology:

To calculate the DVI, a specific formula is applied. The magnitude component involves averaging smoothed returns over various lengths, weighted according to user-defined parameters. This calculation helps determine the magnitude of price changes. The stretch component follows a similar process, averaging smoothed returns over different lengths to gauge market momentum. Users have the flexibility to adjust the weights and lengths to suit their trading preferences and styles.

Utility:

The DVI offers versatility in its applications. It can be used for both momentum trading and trend analysis due to its smooth and consistent signals. Unlike some other oscillators, the DVI provides longer and uncorrelated signals, allowing traders to effectively combine trend-following and mean-reversion strategies. For example, the DVI is adept at identifying overbought levels above the 200-day moving average, serving as a useful tool for determining exit points during price strength and even potential shorting opportunities. Traders can develop simple trading systems based on the DVI, buying above the 200-day moving average and selling when the DVI exceeds a specified threshold. Conversely, they can consider short positions below the 200-day moving average and cover when the DVI falls below a specific threshold. The DVI's objective approach to analyzing market momentum makes it a valuable resource for traders seeking to identify trading opportunities.

Key Features:

Bar coloring: based on Trend, Extremeties or Reversions

Reversions: Potential reversal points marked with triangles above\below oscillator

Extremity Hues: Highlighting oxcillator reaching traditional OB\OS levels

Example Charts:

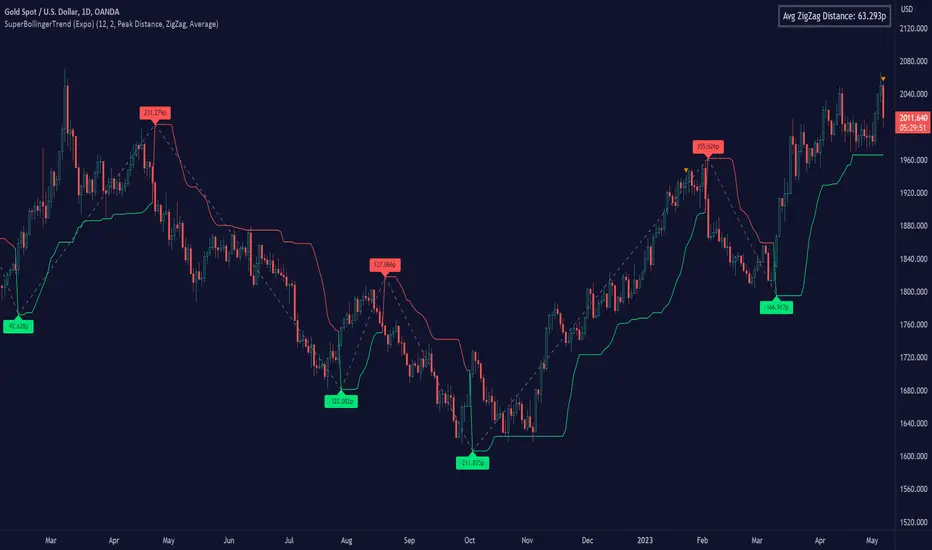

SuperBollingerTrend (Expo)█ Overview

The SuperBollingerTrend indicator is a combination of two popular technical analysis tools, Bollinger Bands, and SuperTrend. By fusing these two indicators, SuperBollingerTrend aims to provide traders with a more comprehensive view of the market, accounting for both volatility and trend direction. By combining trend identification with volatility analysis, the SuperBollingerTrend indicator provides traders with valuable insights into potential trend changes. It recognizes that high volatility levels often accompany stronger price momentum, which can result in the formation of new trends or the continuation of existing ones.

█ How Volatility Impacts Trends

Volatility can impact trends by expanding or contracting them, triggering trend reversals, leading to breakouts, and influencing risk management decisions. Traders need to analyze and monitor volatility levels in conjunction with trend analysis to gain a comprehensive understanding of market dynamics.

█ How to use

Trend Reversals: High volatility can result in more dramatic price fluctuations, which may lead to sharp trend reversals. For example, a sudden increase in volatility can cause a bullish trend to transition into a bearish one, or vice versa, as traders react to significant price swings.

Volatility Breakouts: Volatility can trigger breakouts in trends. Breakouts occur when the price breaks through a significant support or resistance level, indicating a potential shift in the trend. Higher volatility levels can increase the likelihood of breakouts, as they indicate stronger market momentum and increased buying or selling pressure. This indicator triggers when the volatility increases, and if the price is near a key level when the indicator alerts, it might trigger a great trend.

█ Features

Peak Signal Move

The indicator calculates the peak price move for each ZigZag and displays it under each signal. This highlights how much the market moved between the signals.

Average ZigZag Move

All price moves between two signals are stored, and the average or the median is calculated and displayed in a table. This gives traders a great idea of how much the market moves on average between two signals.

Take Profit

The Take Profit line is placed at the average or the median price move and gives traders a great idea of what they can expect in average profit from the latest signals.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!