Mythical EMAs + Dynamic VWAP BandThis indicator titled "Mythical EMAs + Dynamic VWAP Band." It overlays several volatility-adjusted Exponential Moving Averages (EMAs) on the chart, along with a Volume Weighted Average Price (VWAP) line and a dynamic band around it.

Additionally, it uses background coloring (clouds) to visualize bullish or bearish trends, with intensity modulated by the price's position relative to the VWAP.

The EMAs are themed with mythical names (e.g., Hermes for the 9-period EMA), but this is just stylistic flavoring and doesn't affect functionality.

I'll break it down section by section, explaining what each part does, how it works, and its purpose in the context of technical analysis. This indicator is designed for traders to identify trends, momentum, and price fairness relative to volume-weighted averages, with volatility adjustments to make the EMAs more responsive in volatile markets.

### 1. **Volatility Calculation (ATR)**

```pine

atrLength = 14

volatility = ta.atr(atrLength)

```

- **What it does**: Calculates the Average True Range (ATR) over 14 periods (a common default). ATR measures market volatility by averaging the true range (the greatest of: high-low, |high-previous close|, |low-previous close|).

- **Purpose**: This volatility value is used later to dynamically adjust the EMAs, making them more sensitive in high-volatility conditions (e.g., during market swings) and smoother in low-volatility periods. It helps the indicator adapt to changing market environments rather than using static EMAs.

### 2. **Custom Mythical EMA Function**

```pine

mythical_ema(src, length, base_alpha, vol_factor) =>

alpha = (2 / (length + 1)) * base_alpha * (1 + vol_factor * (volatility / src))

ema = 0.0

ema := na(ema ) ? src : alpha * src + (1 - alpha) * ema

ema

```

- **What it does**: Defines a custom function to compute a modified EMA.

- It starts with the standard EMA smoothing factor formula: `2 / (length + 1)`.

- Multiplies it by a `base_alpha` (a user-defined multiplier to tweak responsiveness).

- Adjusts further for volatility: Adds a term `(1 + vol_factor * (volatility / src))`, where `vol_factor` scales the impact, and `volatility / src` normalizes ATR relative to the source price (making it scale-invariant).

- The EMA is then calculated recursively: If the previous EMA is NA (e.g., at the start), it uses the current source value; otherwise, it weights the current source by `alpha` and the prior EMA by `(1 - alpha)`.

- **Purpose**: This creates "adaptive" EMAs that react faster in volatile markets (higher alpha when volatility is high relative to price) without overreacting in calm periods. It's an enhancement over standard EMAs, which use fixed alphas and can lag in choppy conditions. The mythical theme is just naming—functionally, it's a volatility-weighted EMA.

### 3. **Calculating the EMAs**

```pine

ema9 = mythical_ema(close, 9, 1.2, 0.5) // Hermes - quick & nimble

ema20 = mythical_ema(close, 20, 1.0, 0.3) // Apollo - short-term foresight

ema50 = mythical_ema(close, 50, 0.9, 0.2) // Athena - wise strategist

ema100 = mythical_ema(close, 100, 0.8, 0.1) // Zeus - powerful oversight

ema200 = mythical_ema(close, 200, 0.7, 0.05) // Kronos - long-term patience

```

- **What it does**: Applies the custom EMA function to the close price with varying lengths (9, 20, 50, 100, 200 periods), base alphas (decreasing from 1.2 to 0.7 for longer periods to make shorter ones more responsive), and volatility factors (decreasing from 0.5 to 0.05 to reduce volatility influence on longer-term EMAs).

- **Purpose**: These form a multi-timeframe EMA ribbon:

- Shorter EMAs (e.g., 9 and 20) capture short-term momentum.

- Longer ones (e.g., 200) show long-term trends.

- Crossovers (e.g., short EMA crossing above long EMA) can signal buy/sell opportunities. The volatility adjustment makes them "mythical" by adding dynamism, potentially improving signal quality in real markets.

### 4. **VWAP Calculation**

```pine

vwap_val = ta.vwap(close) // VWAP based on close price

```

- **What it does**: Computes the Volume Weighted Average Price (VWAP) using the built-in `ta.vwap` function, anchored to the close price. VWAP is the average price weighted by volume over the session (resets daily by default in Pine Script).

- **Purpose**: VWAP acts as a benchmark for "fair value." Prices above VWAP suggest bullishness (buyers in control), below indicate bearishness (sellers dominant). It's commonly used by institutional traders to assess entry/exit points.

### 5. **Plotting EMAs and VWAP**

```pine

plot(ema9, color=color.fuchsia, title='EMA 9 (Hermes)')

plot(ema20, color=color.red, title='EMA 20 (Apollo)')

plot(ema50, color=color.orange, title='EMA 50 (Athena)')

plot(ema100, color=color.aqua, title='EMA 100 (Zeus)')

plot(ema200, color=color.blue, title='EMA 200 (Kronos)')

plot(vwap_val, color=color.yellow, linewidth=2, title='VWAP')

```

- **What it does**: Overlays the EMAs and VWAP on the chart with distinct colors and titles for easy identification in TradingView's legend.

- **Purpose**: Visualizes the EMA ribbon and VWAP line. Traders can watch for EMA alignments (e.g., all sloping up for uptrend) or price interactions with VWAP.

### 6. **Dynamic VWAP Band**

```pine

band_pct = 0.005

vwap_upper = vwap_val * (1 + band_pct)

vwap_lower = vwap_val * (1 - band_pct)

p1 = plot(vwap_upper, color=color.new(color.yellow, 0), title="VWAP Upper Band")

p2 = plot(vwap_lower, color=color.new(color.yellow, 0), title="VWAP Lower Band")

fill_color = close >= vwap_val ? color.new(color.green, 80) : color.new(color.red, 80)

fill(p1, p2, color=fill_color, title="Dynamic VWAP Band")

```

- **What it does**: Creates a band ±0.5% around the VWAP.

- Plots the upper/lower bands with full transparency (color opacity 0, so lines are invisible).

- Fills the area between them dynamically: Semi-transparent green (opacity 80) if close ≥ VWAP (bullish bias), red if below (bearish bias).

- **Purpose**: Highlights deviations from VWAP visually. The color change provides an at-a-glance sentiment indicator—green for "above fair value" (potential strength), red for "below" (potential weakness). The narrow band (0.5%) focuses on short-term fairness, and the fill makes it easier to spot than just the line.

### 7. **Trend Clouds with VWAP Interaction**

```pine

bullish = ema9 > ema20 and ema20 > ema50

bearish = ema9 < ema20 and ema20 < ema50

bullish_above_vwap = bullish and close > vwap_val

bullish_below_vwap = bullish and close <= vwap_val

bearish_below_vwap = bearish and close < vwap_val

bearish_above_vwap = bearish and close >= vwap_val

bgcolor(bullish_above_vwap ? color.new(color.green, 50) : na, title="Bullish Above VWAP")

bgcolor(bullish_below_vwap ? color.new(color.green, 80) : na, title="Bullish Below VWAP")

bgcolor(bearish_below_vwap ? color.new(color.red, 50) : na, title="Bearish Below VWAP")

bgcolor(bearish_above_vwap ? color.new(color.red, 80) : na, title="Bearish Above VWAP")

```

- **What it does**: Defines trend conditions based on EMA alignments:

- Bullish: Shorter EMAs stacked above longer ones (9 > 20 > 50, indicating upward momentum).

- Bearish: The opposite (downward momentum).

- Sub-conditions combine with VWAP: E.g., bullish_above_vwap is true only if bullish and price > VWAP.

- Applies background colors (bgcolor) to the entire chart pane:

- Strong bullish (above VWAP): Green with opacity 50 (less transparent, more intense).

- Weak bullish (below VWAP): Green with opacity 80 (more transparent, less intense).

- Strong bearish (below VWAP): Red with opacity 50.

- Weak bearish (above VWAP): Red with opacity 80.

- If no condition matches, no color (na).

- **Purpose**: Creates "clouds" for trend visualization, enhanced by VWAP context. This helps traders confirm trends—e.g., a strong bullish cloud (darker green) suggests a high-conviction uptrend when price is above VWAP. The varying opacity differentiates signal strength: Darker for aligned conditions (trend + VWAP agreement), lighter for misaligned (potential weakening or reversal).

### Overall Indicator Usage and Limitations

- **How to use it**: Add this to a TradingView chart (e.g., stocks, crypto, forex). Look for EMA crossovers, price bouncing off EMAs/VWAP, or cloud color changes as signals. Bullish clouds with price above VWAP might signal buys; bearish below for sells.

- **Strengths**: Combines momentum (EMAs), volume (VWAP), and volatility adaptation for a multi-layered view. Dynamic colors make it intuitive.

- **Limitations**:

- EMAs lag in ranging markets; volatility adjustment helps but doesn't eliminate whipsaws.

- VWAP resets daily (standard behavior), so it's best for intraday/session trading.

- No alerts or inputs for customization (e.g., changeable lengths)—it's hardcoded.

- Performance depends on the asset/timeframe; backtest before using.

- **License**: Mozilla Public License 2.0, so it's open-source and modifiable.

Prezzo medio ponderato con i volumi (VWAP)

VWAP Entry Assistant (v1.0)Description:

Anchored VWAP with a lightweight assistant for VWAP reversion trades.

It shows the distance to VWAP, an estimated hit probability for the current bar, the expected number of bars to reach VWAP, and a recommended entry price.

If the chance of touching VWAP is low, the script suggests an adjusted limit using a fraction of ATR.

The VWAP line is white by default, and a compact summary table appears at the bottom-left.

Educational tool. Not financial advice. Not affiliated with TradingView or any exchange. Always backtest before use.

xVWAP (Multi-Source VWAP)This indicator lets you plot a true cross-symbol VWAP — volume-weighted average price taken from any symbol or from your current chart. It’s ideal for futures, micros/minis, indices, and correlated assets (e.g., MGC ↔ GC1!, MNQ ↔ NQ1!, ES ↔ SPX).

You can choose the source symbol, anchor period, and display up to three standard-deviation bands around VWAP.

In the chart, since I trade Micros, I used MGC1! (colored), then overlay it with the VWAP from GC1! (Grey).

ORBs, EMAs, AVWAPThis Pine Script (version 6) is a multi-session trading indicator that combines Opening Range Breakouts (ORBs), Exponential Moving Averages (EMAs), and an Anchored VWAP (AVWAP) system — all in one overlay script for TradingView.

Here’s a clear breakdown of its structure and functionality:

🕒 1. Session Logic and ORB Calculation

Purpose: Identify and plot the high and low of the first 30 minutes (default) for the Tokyo, London, and New York trading sessions.

Session Anchors (NY time):

Tokyo → 20:00

London → 03:00

New York → 09:30

(All configurable in inputs.)

ORB Duration: Default is 30 minutes (orbDurationMin), also user-configurable.

Resets:

London and NY ORBs reset at the start of each new New York trading day (17:00 NY time).

Tokyo ORB resets independently using a stored timestamp.

Process:

For each session:

While the time is within the ORB window, the script captures the session’s high and low.

Once the window closes, those levels remain plotted until reset.

Plot Colors:

Tokyo → Yellow (#fecc02)

London → Gray (#8c9a9c)

New York → Magenta (#ff00c8)

These form visible horizontal lines marking the prior session ranges — useful for breakout or retest trading setups.

📈 2. EMA System

Purpose: Provide trend and dynamic support/resistance guidance.

It calculates and plots four EMAs:

EMA Period Color Purpose

EMA 9 Short-term Green Fast signal

EMA 20 Short-term Red Confirms direction

EMA 113 Medium Aqua Trend filter

EMA 200 Long-term Orange Macro trend baseline

Each EMA is plotted directly on the price chart for visual confluence with ORB and VWAP levels.

⚖️ 3. Anchored VWAP (AVWAP)

Purpose: Display a volume-weighted average price anchored to specific timeframes or events, optionally with dynamic deviation or percentage bands.

Features:

Anchor Options:

Time-based: Session, Week, Month, Quarter, Year, Decade, Century

Event-based: Earnings, Dividends, Splits

VWAP resets when the chosen anchor condition is met (e.g., new month, new earnings event, etc.).

Bands:

Up to three levels of symmetric upper/lower bands.

Choose between Standard Deviation or Percentage-based widths.

Display Toggles:

Each band’s visibility is optional.

VWAP can be hidden on 1D+ timeframes (hideonDWM option).

Color Scheme:

VWAP: Fuchsia (magenta-pink) line

Bands: Green / Olive / Teal with light-filled zones

⚙️ 4. Technical Highlights

Uses ta.vwap() with built-in band calculations.

Handles instruments with or without volume (errors if missing volume).

Uses time-zone aware timestamps (timestamp(NY_TZ, …)).

Uses timeframe.change() to detect new anchors for the VWAP.

Employs persistent variables (var) to maintain session state across bars.

💡 In Practice

This indicator is designed for multi-session intraday traders who:

Trade Tokyo, London, or NY open breakouts or retests.

Use EMA stacking and crossovers for trend confirmation.

Use Anchored VWAP as a fair-value or mean-reversion reference.

Need clear visual structure across different market sessions.

It provides strong session separation, trend context, and volume-weighted price reference — making it ideal for discretionary or semi-systematic trading strategies focused on liquidity zones and session momentum.

VWAP + Multi-Condition RSI Signals + FibonacciPlatform / System

Platform: TradingView

Language: Pine Script® v6

Purpose: This script is an overlay indicator for technical analysis on charts. It combines multiple tools: VWAP, RSI signals, and Fibonacci levels.

1️⃣ VWAP (Volume Weighted Average Price)

What it does:

Plots the VWAP line on the chart, which is a weighted average price based on volume.

Can be anchored to different periods: Session, Week, Month, Quarter, Year, Decade, Century, or corporate events like Earnings, Dividends, Splits.

Optionally plots bands above and below VWAP based on standard deviation or a percentage.

Supports up to 3 bands with customizable multipliers.

Will not display if the timeframe is daily or higher and the hideonDWM option is enabled.

Visual on chart: A main VWAP line with optional shaded bands.

2️⃣ RSI (Relative Strength Index) Signals

What it does:

Calculates RSI with a configurable period.

Identifies overbought and oversold zones using user-defined levels.

Generates buy/sell signals based on:

RSI crossing above oversold → Buy

RSI crossing below overbought → Sell

Detects strong signals using divergences:

Bullish divergence: Price makes lower low, RSI makes higher low → Strong Buy

Bearish divergence: Price makes higher high, RSI makes lower high → Strong Sell

Optional momentum signals when RSI crosses 50 after recent overbought/oversold conditions.

Visual on chart:

Triangles for buy/sell

Different color triangles/circles for strong and momentum signals

Background shading in RSI overbought/oversold zones

Alerts: The script can trigger alerts when any of these signals occur.

3️⃣ Fibonacci Levels

What it does:

Calculates Fibonacci retracement and extension levels based on the highest high and lowest low over a configurable lookback period.

Plots standard Fibonacci levels: 0.146, 0.236, 0.382, 0.5, 0.618, 0.786, 1.0

Plots extension levels: 1.272, 1.618, 2.0, 2.618

Helps identify potential support/resistance zones.

Visual on chart: Horizontal lines at each Fibonacci level, shaded with different transparencies.

Summary

This script is essentially a multi-tool trading indicator that combines:

VWAP with dynamic bands for trend analysis and price positioning

RSI signals with divergences for entry/exit points

Fibonacci retracement and extension levels for support/resistance

It is interactive and visual, providing both chart overlays and alert functionality for active trading strategies.

This code is provided for training and educational purposes only. It is not financial advice and should not be used for live trading without proper testing and professional guidance.

Anchored VWAP Polyline [CHE] Anchored VWAP Polyline — Anchored VWAP drawn as a polyline from a user-defined bar count with last-bar updates and optional labels

Summary

This indicator renders an anchored Volume-Weighted Average Price as a continuous polyline starting from a user-selected anchor point a specified number of bars back. It accumulates price multiplied by volume only from the anchor forward and resets cleanly when the anchor moves. Drawing is object-based (polyline and labels) and updated on the most recent bar only, which reduces flicker and avoids excessive redraws. Optional labels mark the anchor and, conditionally, a delta label when the current close is below the historical close at the anchor offset.

Motivation: Why this design?

Anchored VWAP is often used to track fair value after a specific event such as a swing, breakout, or session start. Traditional plot-based lines can repaint during live updates or incur overhead when frequently redrawn. This implementation focuses on explicit state management, last-bar rendering, and object recycling so the line stays stable while remaining responsive when the anchor changes. The design emphasizes deterministic updates and simple session gating from the anchor.

What’s different vs. standard approaches?

Baseline: Classic VWAP lines plotted from session open or full history.

Architecture differences:

Anchor defined by a fixed bar offset rather than session or day boundaries.

Object-centric drawing via `polyline` with an array of `chart.point` objects.

Last-bar update pattern with deletion and replacement of the polyline to apply all points cleanly.

Conditional labels: an anchor marker and an optional delta label only when the current close is below the historical close at the offset.

Practical effect: You get a visually continuous anchored VWAP that resets when the anchor shifts and remains clean on chart refreshes. The labels act as lightweight diagnostics without clutter.

How it works (technical)

The anchor index is computed as the latest bar index minus the user-defined bar count.

A session flag turns true from the anchor forward; prior bars are excluded.

Two persistent accumulators track the running sum of price multiplied by volume and the running sum of volume; they reset when the session flag turns from false to true.

The anchored VWAP is the running sum divided by the running volume whenever both are valid and the volume is not zero.

Points are appended to an array only when the anchored VWAP is valid. On the most recent bar, any existing polyline is deleted and replaced with a new one built from the point array.

Labels are refreshed on the most recent bar:

A yellow warning label appears when there are not enough bars to compute the reference values.

The anchor label marks the anchor bar.

The delta label appears only when the current close is below the close at the anchor offset; otherwise it is suppressed.

No higher-timeframe requests are used; repaint is limited to normal live-bar behavior.

Parameter Guide

Bars back — Sets the anchor offset in bars; default two hundred thirty-three; minimum one. Larger values extend the anchored period and increase stability but respond more slowly to regime changes.

Labels — Toggles all labels; default enabled. Disable to keep the chart clean when using multiple instances.

Reading & Interpretation

The polyline represents the anchored VWAP from the chosen anchor to the current bar. Price above the line suggests strength relative to the anchored baseline; price below suggests weakness.

The anchor label shows where the accumulation starts.

The delta label appears only when today’s close is below the historical close at the offset; it provides a quick context for negative drift relative to that reference.

A yellow message at the current bar indicates the chart does not have enough history to compute the reference comparison yet.

Practical Workflows & Combinations

Trend following: Anchor after a breakout bar or a swing confirmation. Use the anchored VWAP as dynamic support or resistance; look for clean retests and holds for continuation.

Mean reversion: Anchor at a local extreme and watch for approaches back toward the line; require structure confirmation to avoid early entries.

Session or event studies: Re-set the anchor around earnings, macro releases, or session opens by adjusting the bar offset.

Combinations: Pair with structure tools such as swing highs and lows, or with volatility measures to filter chop. The labels can be disabled when combining multiple instances to maintain chart clarity.

Behavior, Constraints & Performance

Repaint and confirmation: The line is updated on the most recent bar only; historical values do not rely on future bars. Normal live-bar movement applies until the bar closes.

No higher timeframe: There is no `security` call; repaint paths related to higher-timeframe lookahead do not apply here.

Resources: Uses one polyline object that is rebuilt on the most recent bar, plus two labels when conditions are met. `max_bars_back` is two thousand. Arrays store points from the anchor forward; extremely long anchors or very long charts increase memory usage.

Known limits: With very thin volume, the VWAP can be unavailable for some bars. Very large anchors reduce responsiveness. Labels use ATR for vertical placement; extreme gaps can place them close to extremes.

Sensible Defaults & Quick Tuning

Starting point: Bars back two hundred thirty-three with Labels enabled works well on many assets and timeframes.

Too noisy around the line: Increase Bars back to extend the accumulation window.

Too sluggish after regime changes: Decrease Bars back to focus on a shorter anchored period.

Chart clutter with multiple instances: Disable Labels while keeping the polyline visible.

What this indicator is—and isn’t

This is a visualization of an anchored VWAP with optional diagnostics. It is not a full trading system and does not include entries, exits, or position management. Use it alongside clear market structure, risk controls, and a plan for trade management. It does not predict future prices.

Inputs with defaults

Bars back: two hundred thirty-three bars, minimum one.

Labels: enabled or disabled toggle, default enabled.

Pine version: v6

Overlay: true

Primary outputs: one polyline, optional labels (anchor, conditional delta, and a warning when insufficient bars).

Metrics and functions: volume, ATR for label offset, object drawing via polyline and chart points, last-bar update pattern.

Special techniques: session gating from the anchor, persistent state, object recycling, explicit guards against unavailable values and zero volume.

Compatibility and assets: Designed for standard candlestick or bar charts across liquid assets and common timeframes.

Diagnostics: Yellow warning label when history is insufficient.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

VWAP HMA Trend Execution SystemVWAP Trend Execution System

🧭 Purpose

Most traders don’t fail from bad charts — they fail from bad timing.

Jumping in too early, bailing too soon, or freezing when the real move begins.

The VWAP Trend Execution System cuts through that chaos.

It visually syncs Trend, VWAP, and Confidence — giving you instant clarity to trade with calm precision.

⚙️ The Three Core Gauges:

1. 📈 Trend Green for up, Red for down (Trend: Confirms direction)

2. 💰 VWAP Price vs. Volume Weighted Average Price. Institutional Fair Value. (Bull or Bear)

3. 🎯 Confidence Agreement between trend & VWAP. Dont fight the trend.

Bonus Feature: Confidence Turns 🟢 Confident when aligned, 🟡 Cautious when mixed.

Bonus 2: This version has the cross / confirmed direction arrow in the table.

Together, these create a clean, visual readout of the market’s health.

🧩 How to Use

Watch the Color Flow:

🟢 Green Cloud → Buyers in control.

🔴 Red Cloud → Sellers in control.

Check VWAP (Orange Line):

Price above VWAP → bullish strength.

Price below VWAP → bearish control.

Hovering at VWAP → indecision. Wait.

---

Act With Discipline:

Trade only when all gauges agree.

Add size only in Confident conditions.

Trim or tighten stops when it shifts to Cautious.

⚡ Quick Reference:

🟢 Green cloud + above VWAP + Confident | Uptrend continuation | Favor long bias

🔴 Red cloud + below VWAP + Confident | Downtrend continuation | Favor short bias

Mixed colors or Cautious: Wait or scale back

Cloud flips color: Possible shift. Reassess bias next bar

🧠 Best Practices

Works best on liquid symbols (SPY, QQQ, BTC, GOLD).

Ideal timeframes: 5m to 1h.

Use at bar close for confirmation, but enjoy live responsiveness for awareness.

Combine with your existing risk management — VTES is a timing enhancer, not a signal generator.

Designed for clarity on both light and dark themes (optimized for dark).

💡 Mindset

This isn’t a prediction tool — it’s a discipline tool. Wait for agreement.

Execute when the picture is clear. Protect capital when it’s not.

🧘 Clarity over clutter. Timing over guessing.

⚖️ Disclaimer: Educational and informational use only. Not financial advice. Always use independent judgment and position sizing.

VWAP HMA Trends

It visually syncs Trend, VWAP, and Confidence — giving you instant clarity to trade with calm precision.

⚙️ The Three Core Gauges:

1. 📈 Trend Green for up, Red for down (Trend: Confirms direction)

2. 💰 VWAP Price vs. Volume Weighted Average Price. Institutional Fair Value. (Bull or Bear)

3. 🎯 Confidence Agreement between trend & VWAP. Dont fight the trend.

Bonus Feature: Confidence Turns 🟢 Confident when aligned, 🟡 Cautious when mixed.

Together, these create a clean, visual readout of the market’s health.

🧩 How to Use

Watch the Color Flow:

🟢 Green Cloud → Buyers in control.

🔴 Red Cloud → Sellers in control.

Check VWAP (Orange Line):

Price above VWAP → bullish strength.

Price below VWAP → bearish control.

Hovering at VWAP → indecision. Wait.

---

Act With Discipline:

Trade only when all gauges agree.

Add size only in Confident conditions.

Trim or tighten stops when it shifts to Cautious.

⚡ Quick Reference:

🟢 Green cloud + above VWAP + Confident | Uptrend continuation | Favor long bias

🔴 Red cloud + below VWAP + Confident | Downtrend continuation | Favor short bias

Mixed colors or Cautious: Wait or scale back

Cloud flips color: Possible shift. Reassess bias next bar

⚖️ Disclaimer: Educational and informational use only. Not financial advice. Always use independent judgment and position sizing.

Volume x Close in CroresThis indicator provides a clear visualization of the monetary volume activity for each candle by calculating the product of trading volume and closing price and converting it into crores for easier readability.

Volume Weighted Average Price Band Extension## Volume Weighted Average Price Band Extension (VWAPb)

**Volume Weighted Average Price Band Extension** is an enhanced VWAP indicator that extends the traditional three-band system to include up to **five configurable standard deviation bands**, making it particularly well-suited for analyzing volatile market conditions where price action frequently extends beyond conventional boundaries.

### Key Features

**Extended Band System**

Unlike standard VWAP indicators that typically offer three bands, this indicator provides five independently configurable bands with customizable multipliers (default: 0.5x, 1.0x, 1.5x, 2.0x, and 3.0x). Each band can be toggled on or off, allowing traders to adapt the display to current market volatility and their specific trading strategy.

**Dual Calculation Modes**

The indicator offers flexibility in how bands are calculated:

- **Standard Deviation Mode**: Traditional statistical approach measuring price dispersion from the VWAP

- **Percentage Mode**: Distance calculated as a percentage of VWAP (1 multiplier = 1%), useful for comparing relative moves across different price levels

**Flexible Anchor Periods**

Calculate VWAP from multiple timeframes and events:

- Time-based: Session, Week, Month, Quarter, Year, Decade, Century

- Event-based: Earnings reports, Dividend announcements, Stock splits

- Customizable source (default: hlc3)

**Visual Clarity**

Color-coded bands with semi-transparent fills between upper and lower boundaries help identify key support and resistance zones at a glance. The indicator automatically hides on daily and higher timeframes when enabled, keeping charts clean.

### Ideal For

- **Volatile Markets**: The extended band system captures extreme price movements that often exceed traditional 2-3 standard deviation bounds

- **Scalping & Day Trading**: Multiple bands provide granular entry and exit zones for short-term trades

- **Mean Reversion Strategies**: Identify overextended price action relative to volume-weighted fair value

- **Institutional Order Flow Analysis**: VWAP remains a key benchmark for institutional execution

### How It Works

The Volume Weighted Average Price represents the average price weighted by volume throughout the selected anchor period. The surrounding bands act as dynamic support and resistance levels, with each successive band representing areas of increasing deviation from the volume-weighted mean. In volatile conditions, price may regularly test the outer bands (2.0x, 3.0x), which would be invisible on standard three-band implementations.

**Trading Applications:**

- Price near outer bands (±2.0x, ±3.0x) may signal exhaustion and potential reversal opportunities

- Price oscillating between inner bands (±0.5x, ±1.0x) indicates consolidation

- VWAP itself acts as a dynamic pivot point—bullish above, bearish below

### Settings Overview

- **VWAP Settings**: Anchor period selection, source input, offset capability, option to hide on D/W/M timeframes

- **Bands Settings**: Toggle each of the five bands independently, adjust multipliers, choose between Standard Deviation or Percentage calculation mode

---

**Note**: This indicator requires volume data to function properly. A runtime error will display if volume data is unavailable for the selected symbol.

**Disclaimer**: This indicator is designed for technical analysis and should be used in conjunction with other forms of analysis and proper risk management. Past performance and indicator signals do not guarantee future results.

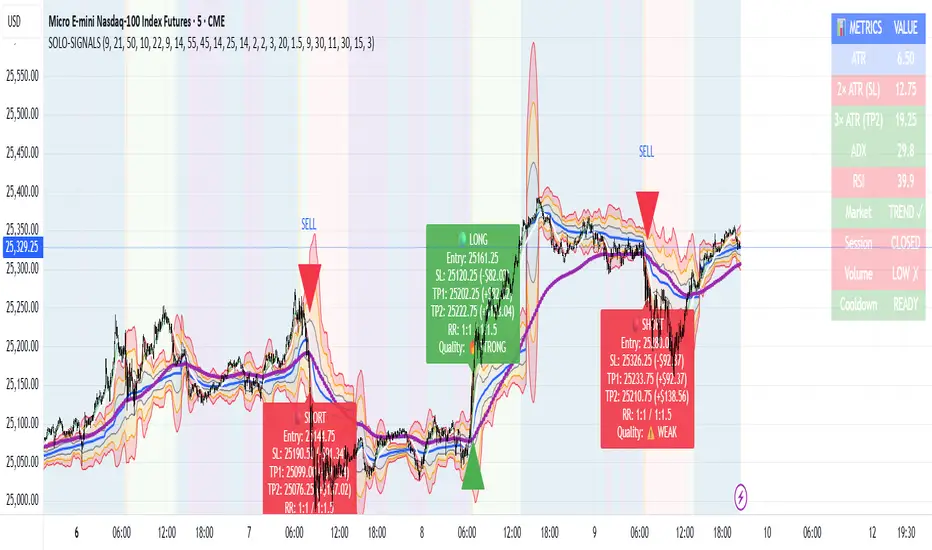

MNQ TopStep 50K | Ultra Quality v3.0MNQ TopStep 50K | Ultra Quality v3.0 - Publish Summary📊 OverviewA professional-grade trading indicator designed specifically for MNQ futures traders using TopStep funded accounts. Combines 7 technical confirmations with 5 advanced safety filters to deliver high-quality trade signals while managing drawdown risk.🎯 Key FeaturesCore Signal System

7-Point Confirmation: VWAP, EMA crossovers, 15-min HTF trend, MACD, RSI, ADX, and Volume

Signal Grading: Each signal is rated A+ through D based on 7 quality factors

Quality Threshold: Adjustable minimum grade requirement (A+, A, B, C, D)

Advanced Safety Filters (Customizable)

Mean Reversion Filter - Prevents chasing extended moves beyond VWAP bands

ATR Spike Filter - Avoids trading during extreme volatility events

EMA Spacing Filter - Ensures proper trend separation (optional)

Momentum Filter - Requires consecutive directional bars (optional)

Multi-Timeframe Confirmation - Aligns with 15-min trend (optional)

TopStep Risk Management

Real-time drawdown tracking

Position sizing calculator based on remaining cushion

Daily loss limit monitoring

Consecutive loss protection

Max trades per day limiter

Visual Components

VWAP with 1σ, 2σ, 3σ bands

EMA 9/21 with cloud fill

15-min EMA 50 for HTF trend

Comprehensive metrics dashboard

Risk management panel

Filter status panel

Detailed trade labels with entry, stops, and targets

⚙️ Default Settings (Balanced for Regular Signals)Technical Indicators

Fast EMA: 9 | Slow EMA: 21 | HTF EMA: 50 (15-min)

MACD: 10/22/9

RSI: 14 period | Thresholds: 52 (buy) / 48 (sell)

ADX: 14 period | Minimum: 20

ATR: 14 period | Stop: 2x | TP1: 2x | TP2: 3x

Volume: 1.2x average required

Session Settings

Default: 9:30 AM - 11:30 AM ET (adjustable)

Avoids first 15 minutes after market open

Customizable trading hours

Safety Filters (Default Configuration)

✅ Mean Reversion: Enabled (2.5σ max from VWAP)

✅ ATR Spike: Enabled (2.0x threshold)

❌ EMA Spacing: Disabled (can enable for quality)

❌ Momentum: Disabled (can enable for quality)

❌ MTF Confirmation: Disabled (can enable for quality)

Risk Controls

Minimum Signal Quality: C (adjustable to A+ for fewer/better signals)

Min Bars Between Signals: 10

Max Trades Per Day: 5

Stop After Consecutive Losses: 2

📈 Expected PerformanceWith Default Settings:

Signals per week: 10-15 trades

Estimated win rate: 55-60%

Risk-Reward: 1:2 (TP1) and 1:3 (TP2)

With Aggressive Settings (Min Quality = D, All Filters Off):

Signals per week: 20-25 trades

Estimated win rate: 50-55%

With Conservative Settings (Min Quality = A, All Filters On):

Signals per week: 3-5 trades

Estimated win rate: 65-70%

🚀 How to UseBasic Setup:

Add indicator to MNQ 5-minute chart

Adjust TopStep account settings in inputs

Set your risk per trade percentage (default: 0.5%)

Configure trading session hours

Set minimum signal quality (Start with C for balanced results)

Signal Interpretation:

Green Triangle (BUY): Long signal - all confirmations aligned

Red Triangle (SELL): Short signal - all confirmations aligned

Label Details: Shows entry, stop loss, take profit levels, position size, and signal grade

Signal Grade: A+ = Elite (6-7 points) | A = Strong (5) | B = Good (4) | C = Fair (3)

Dashboard Monitoring:

Top Right: Technical metrics and market conditions

Top Left: Filter status (which filters are passing/blocking)

Bottom Right: TopStep risk metrics and position sizing

⚡ Customization TipsFor More Signals:

Lower "Minimum Signal Quality" to D

Decrease ADX threshold to 18-20

Lower RSI thresholds to 50/50

Reduce Volume multiplier to 1.1x

Disable additional filters

For Higher Quality (Fewer Signals):

Raise "Minimum Signal Quality" to A or A+

Increase ADX threshold to 25-30

Enable all 5 advanced filters

Tighten VWAP distance to 2.0σ

Increase momentum requirement to 3-4 bars

For TopStep Compliance:

Adjust "Max Total Drawdown" and "Daily Loss Limit" to match your account

Update "Already Used Drawdown" daily

Monitor the Risk Panel for cushion remaining

Use recommended contract sizing

🛡️ Risk DisclaimerIMPORTANT: This indicator is for educational and informational purposes only.

Past performance does not guarantee future results

All trading involves substantial risk of loss

Use proper risk management and position sizing

Test thoroughly in paper trading before live use

The indicator does not guarantee profitable trades

Adjust settings based on your risk tolerance and trading style

Always comply with your broker's and TopStep's rules

MNQ Morning Indicator | Clean SignalsMNQ Morning Trading Indicator Summary

What It Does

This is a TradingView indicator designed for day trading MNQ (Micro Nasdaq-100 futures) during morning sessions. It generates BUY and SELL signals only when multiple technical conditions align, helping traders identify high-probability trade setups.

Core Strategy

BUY Signal Requirements (All must be true):

✅ Price above VWAP (volume-weighted average price)

✅ Fast EMA (9) above Slow EMA (21) - uptrend confirmation

✅ Price above 15-minute 50 EMA - higher timeframe confirmation

✅ MACD histogram positive - momentum confirmation

✅ RSI above 55 - strength confirmation

✅ ADX above 25 - trending market (not choppy)

✅ Volume 1.5x above average - strong participation

SELL Signal (opposite conditions)

Key Features

🎯 Risk Management

Stop Loss: 2× ATR (Average True Range)

Take Profit 1: 2× ATR (1:2 risk-reward)

Take Profit 2: 3× ATR (1:3 risk-reward)

Dollar values: Calculates P&L based on MNQ's $2/point value

⏰ Session Filter

Default: 9:30 AM - 11:30 AM ET (customizable)

Safety feature: Avoids first 15 minutes (high volatility period)

Won't generate signals outside trading hours

🛡️ Signal Quality

Rates each signal: 🔥 STRONG, ⚡ MEDIUM, or ⚠️ WEAK

Requires minimum 15 bars between signals (prevents overtrading)

📊 Visual Dashboard

Shows real-time metrics:

ATR values

ADX (trend strength)

RSI (momentum)

Market condition (TREND/CHOP)

Session status

Volume status

Signal cooldown timer

Visual Elements

📈 VWAP with standard deviation bands (1σ, 2σ, 3σ)

📉 Multiple EMAs with trend-based coloring

🟢/🔴 Buy/Sell arrows on chart

📋 Detailed trade labels showing entry, SL, TPs, and risk-reward ratios

🎨 Background highlighting for market conditions

Safety Features

Cooldown period between signals

Session restrictions (no trading outside set hours)

First 15-minute avoidance (post-open volatility)

Multi-confirmation requirement (all 7 conditions must align)

Trend filter (ADX minimum to avoid choppy markets)

Best For

Day traders focused on morning sessions

MNQ futures traders

Traders who prefer systematic, rule-based entries

Those wanting pre-calculated risk management levels

Customization

All parameters are adjustable:

EMA periods

MACD settings

RSI thresholds

ADX minimum

ATR multipliers

Session times

Visual preferences

This indicator is designed to be conservative — it waits for strong confirmation before signaling, which means fewer but potentially higher-quality trades.

cd_VWAP_mtg_CxCd_VWAP_mtg_Cx

Overview

The most important condition for being successful and profitable in the market is to consistently follow the same rules without compromise, while the price constantly moves in countless different ways.

Regardless of the concept or trading school, those who have rules win.

In this indicator, we will define and use three main sections to set and apply our rules.

The indicator uses the VWAP (Volume Weighted Average Price) — price weighted by volume.

Two VWAPs can be displayed either by manually entering date and time, or by selecting from the menu.

From the menu, you can select the following reference levels:

• HTF Open: Opening candle of the higher timeframe

• ATH / ATL: All-Time High / All-Time Low candles

• PMH / PML, PWH / PWL, PDH / PDL, PH4H / PH4L: Previous Month, Week, Day, or H4 Highs/Lows

• MH / ML, WH / WL, DH / DL, H4H / H4L: Current Month, Week, Day, or H4 Highs/Lows

Additionally, it includes:

• Mitigation / Order Block zones (local buyer-seller balance) across two timeframes.

• Buy/Sell Side Liquidity levels (BSL / SSL) from the aligned higher timeframe (target levels).

________________________________________

Components and Usage

1 – VWAP

Calculated using the classical method:

• High + Volume for the upper value

• Close + Volume for the middle value

• Low + Volume for the lower value

The VWAP is displayed as a colored band, where the coloring represents the bias.

Let’s call this band FVB (Fair Value Band) for ease of explanation.

The FVB represents the final line of defense, the buyer/seller boundary, and in technical terms, it can be viewed as premium/discount zones or support/resistance levels.

Within this critical area, the strong side continues its move, while the weaker side is forced to retreat.

But does the side that breaks beyond the band always keep going?

We all know that’s not always the case — in different pairs and timeframes, price often violates both the upper and lower edges multiple times.

To achieve more consistent analysis, we’ll define a new set of rules.

________________________________________

2 – Mitigation / Order Blocks

In trading literature, there are dozens of different definitions and uses of mitigation or order blocks.

Here, we will interpret the candlesticks to create our own definition, and we’ll use the zones defined by candles that fit this pattern.

For simplicity, let’s abbreviate mitigation as “mtg.”

For a candle to be selected as an mtg, it must clearly show strength from one side (buyers or sellers) — which can also be observed visually on the chart.

________________________________________

Bullish mtg criteria:

1. The first candle must be bullish (close > open) → buyers are strong.

2. The next candle makes a new high (buyers push higher) but fails to close above and pulls back to close inside the previous range → sellers react.

It also must not break the previous low → buyers defend.

3. In the following candle(s), as long as the first candle’s low is protected and the second candle’s high is broken, it indicates buyer strength → a bullish mtg is confirmed.

When price returns to this zone later (gets mitigated), the expectation is that the zone holds and price pushes upward again.

If the low is violated, the mtg becomes invalid.

In technical terms:

If the previous candle’s high is broken but no close occurs above it, the expectation is a reversal move that will retest its low.

Question:

What if the low is protected and in the next candle(s) a new high forms?

Answer: → Bullish mtg.

Bearish mtg (opposite)

3 – Buy/Sell Side Liquidity Levels

With the help of the aligned higher timeframe (swing points), we will define our market structure framework and set our liquidity targets accordingly.

Let’s put the pieces together.

If we continue explaining from a trade-focused perspective, our first priority should be our bias — our projection or expectation of the market’s potential movement.

We will determine this bias using the FVB.

Since we know the band often gets violated on both sides, we want the price action to convince us of its strength.

To do that, we’ll use the first candle that closes beyond the band.

The distance from that candle’s high to low will be our threshold range

Bullish level = high + (candle length × coefficient)

Bearish level = low - (candle length × coefficient)

When the price closes beyond this threshold, it demonstrates strength, and our bias will now align in that direction.

How long will this bias remain valid?

→ Until a closing candle appears on the opposite side of the band.

If a close occurs on the opposite side, then a new bias will only be confirmed once the new threshold level is broken.

During the period in between, we have no bias.

Let’s continue on the chart:

Now that our bias has been established, where and how do we look for trade opportunities?

There are two possible entry approaches:

• Aggressive entry: Enter immediately with the breakout.

• Conservative entry: Wait for a pullback and enter once a suitable structure forms.

(The choice depends on the user’s preference.)

At this stage, the user can apply their own entry model. Let’s give an example:

Let’s assume we’re looking for setups using HTF sweep + LTF CISD confirmation.

Once our bias turns bearish, we look for an HTF sweep forming on or near an FVB or mtg block, and then confirm the entry with a CISD signal.

In summary:

• FVB defines the bias, the entry zone, and the target zone.

• Mtg blocks represent entry zones.

• BSL / SSL levels suggest target zones.

Overlapping FVB and mtg blocks are expected to be more effective.

The indicator also provides an option for a second FVB.

A band attached to a lower timeframe can be used as confirmation.

• Main band: Bias + FVB

• Extra band: Entry trigger confirmed by a close beyond it.

Mtg blocks can provide trade entry opportunities, especially when the price is moving strongly in one direction (flow).

Consecutive or complementary mtg blocks indicate that the price is decisive in one direction, while sometimes also showing areas where we should wait before entering.

Mtg blocks that contain an FVG (Fair Value Gap) within their body are expected to be more effective.

Settings:

The default values are set to 1-3-5m, optimized for scalping trades.

VWAP settings:

Main VWAP (FVB):

• Can be set by selecting a start time, manually entering date and time, or choosing a predefined level.

Extra VWAP (FVB):

• Set from the menu. If not needed, select “none.”

• Visibility, color, and fill settings for VWAP are located here.

• Threshold levels visibility and color options are also in this section.

• The multiplier is used for calculating the threshold level.

Important:

• If the Extra VWAP is selected but not displayed, you need to increase the chart timeframe.

o Example: If the chart is on 3m and you select WH from the extra options, it will not display correctly.

• Upper limits for VWAP:

o 1m and 3m charts: daily High/Low

o 5m chart: weekly High/Low

________________________________________

Mtg Settings:

• Visibility and color settings for blocks are configured here.

• To display on a second timeframe, the box must be checked and the timeframe specified.

• Optional display modes: “only active blocks,” “only last violated mtg,” or “all.”

• For confirmation and removal criteria, choosing high/low or close determines the source used for mtg block formation and deletion conditions.

BSL/SSL Settings:

• Visibility, color, font size, and line style can be configured in this section.

When “Auto” is selected, the aligned timeframe is determined automatically by the indicator, while in manual mode, the user defines the timeframe.

Final Words:

Simply opening trades every time the price touches the VWAP or mtg blocks will not make you a profitable trader. Searching for setups with similar structures while maintaining proper risk management will yield better results in the long run.

I would be happy to hear your feedback and suggestions.

Happy trading!

Auto AVWAP (Anchored-VWAP) with Breakout Screener_v2Updated indicator for AWAP breakout. The indicator identified the candle that breaks out of AVWAP

VWAP 10:00–15:00 (MSK, daily reset)Calculates the volume-weighted average price (VWAP) from 10:00 to 15:00 MSK.

The data is used to determine the funding rate of MOEX perpetual futures by comparing the average price of the perpetual contract with the official Central Bank exchange rate on the following day.

Rolling Midpoint of Price & VWAP with ATR BandsThe Rolling Midpoint of Price & VWAP with ATR Bands indicator is a dual-equilibrium concept that fuses price-range structure and traded-volume flow into one continuously updating hybrid model. Traditional VWAPs reset each session and reflect where trading occurred by volume, while midpoints used here reveal where price has structurally balanced between extremes. This script merges both ideas into a cohesive, dynamic system. The Rolling Price Midpoint (50 % of range) represents the structural fair-value line, calculated as the average of the highest high and lowest low over a selected window. The Rolling VWAP (Volume-Weighted Window) tracks the flow-based fair-value line by weighting each bar’s typical price by its volume. Together, these components form the Hybrid Equilibrium — the adaptive center of gravity that shifts as price and volume evolve. Surrounding this equilibrium, ATR Bands at ± 2.226 ATR and ± 5.382 ATR define volatility envelopes that expand and contract with market energy. The result is a living cloud that breathes with the market: compressing during phases of balance and widening during impulsive movements, offering traders a clear visual framework for understanding equilibrium, volatility, and directional bias in real time.

➖

⚙️ Auto-Preset System

The Auto-Preset System intelligently adjusts lookback windows for both the Price Midpoint and VWAP calculations according to the active chart timeframe.

This ensures that the indicator automatically adapts to any trading style — from scalping on 1-minute charts to swing trading on daily or weekly charts — without manual tuning.

🔹 How It Works

When Auto-Preset mode is enabled, the script dynamically selects the most effective lookback lengths for each timeframe.

These presets are optimized to balance responsiveness and stability, maintaining consistent real-world coverage (e.g., the same approximate duration of price data) across all intervals.

📊 Preset Mapping Table

| Chart Timeframe | Price Midpoint Lookback | VWAP Lookback |

|:----------------:|:-----------------------:|:--------------:|

| 1–3m | 13 bars | 21 bars

| 5–10m | 21 bars | 34 bars

| 15–30m | 34 bars | 55 bars

| 1–2 hr | 55 bars | 89 bars

| 4 hr-1D | 89 bars | 144 bars

| 1W | 144 bars | 233 bars

| 1M | 233 bars | 377 bars

⚡ Notes & Customization

- Manual Override: Turn off Auto-Preset Mode to specify your own custom lookback lengths.

- Consistency Across Scales: These adaptive values keep the indicator visually coherent when switching between timeframes — avoiding distortions that can occur with static lengths.

- Practical Benefit: Traders can maintain a single chart layout that self-tunes seamlessly, removing the need to manually recalibrate settings when shifting from short-term to long-term analysis.

In short, the Auto-Preset System is designed to make this hybrid equilibrium tool timeframe-aware — automatically scaling its logic so that the cloud behaves consistently, regardless of chart resolution.

➖

🌐 Hybrid Equilibrium Envelope

The core hybrid midpoint acts as the mean of structural (price) and volumetric (VWAP) balance.

ATR-based bands project natural expansion zones:

🔸+2.226 / –2.226 ATR → inner equilibrium (controlled trend)

*🔸+5.382 / –5.382 ATR → outer volatility extension (over-stretch / reversion zones)

Color-coded fills show regime strength:

* 🟧 Upper Outer (+5.382) – strong bullish expansion

* 🟩 Upper Inner (+2.226) – trending equilibrium

* 🔴 Lower Inner (–2.226) – mild bearish control

* 🟣 Lower Outer (–5.382) – volatility exhaustion

➖

🧭 Higher-Timeframe Framework

Two macro anchors — Price length of 144 and VWAP length of 233 — outline higher-timeframe bias zones. These help confirm when local momentum aligns with (or fades against) long-term structure.

Labels on the right show active lookback values for quick readout:

`$(13) V(21)` → current rolling pair

`$144 / V233` → macro anchors

➖

🧩 Chart Examples

**AMD 15m (Equilibrium Expansion)**

Price steadily rides above the hybrid midpoint as teal and orange (bullish) ATR zones widen, confirming a phase of controlled bullish volatility and healthy trend expansion.

BTCUSD 1m (Volatility Compression)

Bitcoin coils tightly inside the teal-to-maroon equilibrium bands before breaking out.

The hybrid midpoint flattens and ATR envelopes contract, signaling a state of balance before volatility expansion.

ETHUSD 15m (Transition from Compression → Impulse)

Ethereum transitions from purple-zone compression into a clear upper-band expansion.

The hybrid midpoint breaks above the macro VWAP 233, confirming the shift from equilibrium to directional momentum.

SOFI 1m (Micro Bias Reversal)

SOFI’s intraday structure flips as price reclaims the hybrid midpoint.

The macro VWAP 233 flattens, signaling a transition from oversold lower bands back toward equilibrium and early trend recovery.

➖

🎯 How to Use

1. Bias Detection – Price > Hybrid Midpoint → bullish; < → bearish.

2. Volatility Gauge – Watch band spacing for compression / expansion cycles.

3. Confluence Checks – Align Hybrid Midpoint with HTF 233 VWAP for strong continuation signals.

4. Mean Reversion Zones – Outer bands highlight areas where probability of snap-back increases.

➖

🔧 Inputs & Customization

Auto Presets toggle

🔸Manual Lookback Overrides** for fine-tuning

🔸Plot Window Length** (show recent vs full history)

🔸ATR Sensitivity & Fill Opacity** controls

🔸Label Padding / Font Size** for cleaner overlay visuals

➖

🧮 Formula Highlights

➖Rolling Midpoint = (highest(high,N) + lowest(low,N)) / 2

➖Rolling VWAP = Σ(Typical Price×Vol) / Σ(Vol)

➖Hybrid = (PriceMid + VWAP) / 2

➖Upper₂ = Hybrid + ATR×2.226

➖Lower₂ = Hybrid − ATR×2.226

➖Upper₅ = Hybrid + ATR×5.382

➖Lower₅ = Hybrid − ATR×5.382

➖

🎯 Ideal For

➡️ Traders who want adaptive fair-value zones that evolve with both price and volume.

➡️ Analysts who shift between scalping, swing, and position timeframes, and need a tool that self-adjusts.

➡️ Those who rely on visual structure clarity to confirm setups across changing volatility conditions.

➡️ Anyone seeking a hybrid model that unites structural range logic (midpoint) and flow-based balance (VWAP).

➖

🏁 Final Word

This script is more than a visual overlay — it’s a complete trend and structure framework built to adapt with market rhythm. It helps traders visualize equilibrium, momentum, and volatility as one cohesive system. Whether you’re seeking clean trend alignment, dynamic support/resistance, or early warning signs of reversals, this indicator is tuned to help you react with confidence — not hindsight.

➖

Remember — no single indicator should ever stand alone. For best results, pair it with price action context, higher-timeframe structure, and complementary tools such as moving averages or trendlines. Use it to confirm setups, not define them in isolation.

💡 Turn logic into clarity, structure into trades, and uncertainty into confidence.

Rolling VWAP by VibieRolling VWAP

🧠 Concept

Rolling VWAP is a continuously updating VWAP that doesn’t reset at fixed anchors like daily or weekly VWAP.

Instead, it applies VWAP calculation to a moving window of recent bars, making it more adaptive and responsive to current market conditions.

⸻

⚙️ How It Works

1. VWAP Formula

• VWAP = Σ(price × volume) ÷ Σ(volume) over a rolling lookback period.

2. Rolling Window

• The indicator calculates VWAP only for the last N bars (e.g., 50).

• As each new bar appears, the oldest drops out, creating a continuously updated VWAP line.

3. Real-Time Adjustment

• Rolling VWAP constantly shifts with new data, tracking short-term fair value as market conditions evolve.

⸻

🧭 How to Use

• Intraday trading → use short rolling windows (20–50 bars) for scalping and mean reversion setups.

• Swing trading → use longer windows (e.g., 10 days) to track medium-term fair value.

• Rolling VWAP acts as dynamic support/resistance and can serve as a trend filter.

⸻

🌟 Why It’s Original and Useful

• Reacts faster to volume changes than anchored VWAP.

• Continuously represents short-term fair price without session resets.

• Excellent for adaptive strategies in volatile markets.

• Particularly valuable for active day traders.

Aggregated VWAP by VibieAggregated VWAP (Professional Layout)

🧠 Concept

VWAP (Volume Weighted Average Price) is a widely used institutional benchmark for fair price.

This indicator enhances standard VWAP by aggregating multiple exchanges, adding standard deviation bands, and offering two visualization modes (bands or lines), providing a professional-grade VWAP analysis tool.

⸻

⚙️ How It Works

1. VWAP Calculation

• VWAP = Σ(price × volume) ÷ Σ(volume), using hlc3 as price reference.

• The indicator supports multiple anchor periods: Daily, Weekly, Monthly, Quarterly, and Yearly.

2. Exchange Aggregation

• VWAP values are aggregated from Binance, Bybit, and Coinbase to compute a market-wide VWAP.

• This prevents bias from a single exchange.

3. Standard Deviation Bands

• Plots ±1σ, ±2σ, ±3σ, ±4σ bands around VWAP.

• These show statistical extremes relative to fair value and act as dynamic overbought/oversold zones.

4. Display Modes

• Bands Mode → continuous VWAP and deviation bands.

• Lines Mode → plots VWAP and deviation levels as fixed horizontal lines for each completed period (e.g., pWeek VAL, dMonth VWAP).

⸻

🧭 How to Use

• VWAP levels act as dynamic support/resistance.

• Deviation bands highlight statistically stretched price areas.

• Previous period VWAP levels (e.g., pWeek, pMonth) often act as institutional reference points.

• Ideal for both swing and intraday trading strategies.

⸻

🌟 Why It’s Original and Useful

• Uses aggregated data for more reliable VWAP calculations.

• Integrates standard deviations, period anchoring, and labeling into one tool.

• Professional layout mirrors institutional analysis techniques.

• Extremely versatile for trend following, mean reversion, and breakout systems.

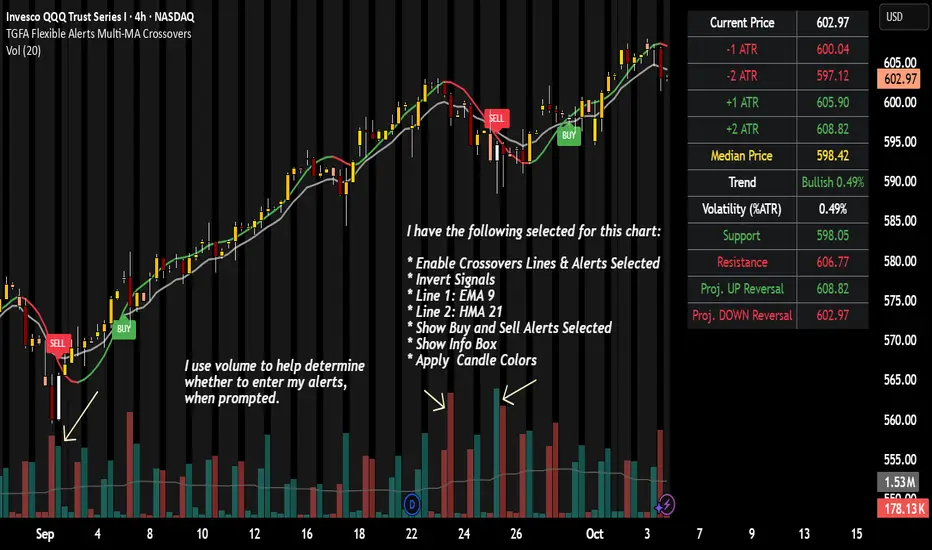

TGFA Flexible Alerts Multi-MA CrossoversTGFA Flexible Alerts, Multi-MA Crossovers

Description

Flexible MA crossovers with BUY/SELL alerts, customizable candle colors, and an info box for ATR/volatility insights. Supports EMA/SMA/HMA/VWAP on any chart.

Overview

TGFA Flexible Alerts is a versatile Pine Script indicator for traders seeking customizable moving average (MA) crossovers, visual signals, and quick-reference metrics. It overlays crossover lines (e.g., fast EMA over slow SMA), generates BUY/SELL labels and alerts, colors candles based on themes, and includes an optional info box with ATR bands, support/resistance, and trend projections. Built for any symbol and timeframe (optimized for 1H intraday), it auto-detects Heikin Ashi charts and handles mixed MA types like responsive HMA with lagging EMAs. All logic uses built-in TA functions for reliability—no repainting on confirmed bars.

Key Features

MA Crossover Engine: Configurable lines (EMA, SMA, HMA, VWAP) with dynamic colors (HMA tints green/red based on slope). Enable/disable via inputs.

Invert Signals Toggle: Flips BUY/SELL logic for mixed MA setups (e.g., HMA as fast line over EMA).

Reasoning: Traditional crossovers assume a fast line (low lag) crossing above a slow line (high lag) for buys. HMA's hull design makes it ultra-responsive, so it may "lead" too aggressively—causing premature signals. Inverting aligns it with user intuition (e.g., HMA dipping below then recovering signals strength), reducing false positives in trending markets. Test on your pairs!

Visual Alerts: BUY/SELL labels at crossover price (with optional price display and offset adjustment).

Single MA Overlays: Independent plots for EMA/SMA/HMA/VWAP (length 0 to hide).

Info Box: Real-time table with current price, ±1/2 ATR bands, median price (over lookback), trend (SMA50 slope), volatility % (ATR normalized), support/resistance (recent highs/lows), and reversal projections (tied to SMA50 pivot for up/down bias).

Candle Coloring: 20+ themes (dark/light canvases) for bull/bear/reversal/low-volume bars—e.g., Emerald Blaze greens uptrends, dims on low vol. Toggle off for no changes.

Chart Source Flexibility: Auto-switches to Heikin Ashi if detected; manual override for Regular/HA.

Alerts fire on crossovers/crossunders (custom messages with ticker/interval). Open-source for forking.

How to Use

Add to Chart: Search in TradingView's public library, apply to any symbol (e.g., stocks, forex). Best on 1H for intraday, but works on daily/weekly too.

Setup Crossovers: Choose Line 1/2 types/lengths (e.g., HMA 9 over SMA 20). Enable "Invert Signals" if using HMA—prevents lag mismatches in volatile assets.

Alerts & Labels: Toggle labels for visuals; set TradingView alerts on "Buy"/"Sell" conditions. Use offset for crowded charts.

Info Box Insights: Enable for quick scans—e.g., enter long near support if trend is bullish and price > median. Adjust ATR length (default 14) for sensitivity.

Candle Themes: Pick a scheme (e.g., Neon Pulse for dark mode); it overrides bar colors without altering data.

Customization Tip: For HMA-heavy setups, invert + short lengths (5-9) catch turns early; pair with volume filter in alerts.

Limitations & Disclaimers - Designed for overlay on price charts; may overlap in tight ranges—adjust transparency via styles.

HMA can repaint intra-bar; signals confirm on close. Not back tested for all assets—validate with strategy tester.

Info box projections use SMA(50) as a trend pivot (same for up/down as reference); customize via code for advanced calcs. Candle colors are cosmetic only.

This is an analysis tool, not advice. Trading involves risk; combine with fundamentals/news. Past performance isn't indicative of future results. No liability for losses.

I'm still a newbie, so feedback encouraged!

Thank you!!

ThisGirl

Anchored VWAP + Prev Session Levels by Avenoircustom vwap for weekly, monthly, quarterly and yearly vawp.

also highlighting previous vwaps.

VWAP Daily/Weekly/Monthly - Automatic AnchoredExplanation:

This script plots Volume-Weighted Average Price (VWAP) lines that are automatically anchored to the beginning of key timeframes — daily, weekly, and monthly. VWAP is a widely used trading indicator that shows the average price of an asset weighted by trading volume, making it useful for identifying fair value and institutional trading levels.

The “automatic anchored” feature means that you don’t have to manually select starting points. Instead, the script automatically resets the VWAP at the start of each day, week, or month, depending on the chosen setting. This ensures the VWAP always reflects the true average price for that period, providing traders with a consistent reference for support, resistance, and trend direction across multiple timeframes.

Notice:

On the chart, you may notice visible “jumps” in the VWAP lines. These are intentional. Each jump marks the reset point at the start of a new day, week, or month, depending on the selected setting. This design keeps the VWAP history from the previous period intact, allowing you to clearly see how price interacted with VWAP in past sessions.

By keeping these historical resets, you can easily compare short-term (daily) VWAP behavior against longer-term levels like weekly and monthly VWAP. This provides valuable context, helping you spot when price respects or diverges from fair value across different timeframes.

In short:

Daily VWAP resets at the start of each trading day.

Weekly VWAP resets at the beginning of each trading week.

Monthly VWAP resets at the start of each month.

This makes it easy to analyze how price interacts with VWAP levels across different time horizons without manual adjustments.

Swing High Low by MIRRORPIPThis strategy finds swing high and lows and marks them as SH and SL respectively.

if the pattern tries to form higher high it will trigger a buy signal

if the pattern tries to form lower low, it will trigger a short signal

This setup is very popular among price action lovers

BAB VWAP V2 Daily, Weekly & Monthly (Optimized)Overview

BAB VWAP V2 displays 3 automatically anchored VWAPs (Daily, Weekly, Monthly) plus 2 customizable intraday VWAPs (anchored at user-defined HH:MM). Optional ±σ bands (volume-weighted) for D/W/M. Includes dynamic labels and an optional summary table.

Main Features

Daily/Weekly/Monthly VWAPs with automatic reset per period.

2 Intraday anchored VWAPs (default 09:00 & 15:30, configurable).

Volume-weighted standard deviation bands (σ) for D/W/M with optional fill.

Alerts on VWAP D/W/M crossovers.

Labels dynamically updated (no stacking) + optional table (2×4) with key values.

Parameters

Display: toggle D/W/M VWAPs, labels, table.

Colors & Style: line colors, thickness, style.

Bands (σ): enable per period, set multiplier, toggle fill.

Intraday (Anchored): enable VWAP 1 & 2, choose hour/minute, set colors & thickness.

How to Use

Add the indicator to a clean chart.

Enable desired VWAPs (D/W/M and/or intraday).

Optionally enable σ bands to contextualize price deviation from VWAP.

Configure intraday VWAP anchors to match your market session (e.g., RTH, EU open, etc.).

Alerts

Price crossing over/under Daily, Weekly, Monthly VWAPs.

Configure alerts from the Alerts panel.

Best Practices

Publish chart screenshots without other indicators for clarity.

Adjust intraday anchor times according to your instrument’s trading session (pre-/post-market handling may vary).

Limitations

Intraday VWAPs are calculated in 1-minute resolution via request.security to remain consistent across all timeframes.

Intraday σ bands are not included by default (can be added in a later version).

Changelog

V2: Performance refactor, non-mutable labels, fixed fill() usage, added 2 intraday VWAPs with time selectors, stabilized table.

V1: Basic D/W/M VWAPs + alerts.

Disclaimer

This script is for educational and informational purposes only. It does not constitute financial advice. You are solely responsible for your trading decisions.

Credits & License

© BAB Trading. Pine Script® — TradingView.

Open-source under the Mozilla Public License (MPL 2.0) by default (or specify your own license in the script header if different).