Liquidity Levels (Smart Swing Lows)Liquidity Levels — Smart Swing Low Detection

Efficient Liquidity Sweep Visualization for Smart Money Traders

This script automatically identifies and plots liquidity-rich swing lows based on pivot logic, filters them to remove redundant levels, and overlays daily highs/lows for added context — giving Smart Money Concept (SMC) traders a clean, actionable map of liquidity.

It’s designed to be minimal yet powerful: perfect for spotting potential liquidity grabs, mitigation zones, and sweep targets with zero chart clutter.

🔍 What This Script Does:

Detects Smart Swing Lows

Uses fixed pivot detection (left = 3, right = customizable) to identify structurally significant swing lows.

Filters out swing lows that are too close together using a percentage-based spacing threshold to reduce noise.

Mitigation Cleanup Logic

Tracks whether recent price action breaches past swing lows.

If breached, the swing level is automatically removed, keeping only relevant, unmitigated liquidity levels on your chart.

Plots Daily Highs and Lows

Each new trading day, horizontal rays mark the prior day’s high and low — useful for identifying resting liquidity and possible sweep zones.

Labeling and Style Customization

Optional labels for swing lows.

Full control over label size, color, and visibility to match any chart aesthetic.

Timeframe Filtering

Runs exclusively on 5m, 10m, and 15m charts to ensure optimal reliability and signal clarity.

⚙️ Customization Features:

Pivot sensitivity (Right side control)

Minimum distance between swing lows (in %)

Label visibility, size, and color

Line width and colors for both swing levels and daily highs/lows

Mitigation cleanup lookback length

💡 How to Use:

Add the script to a qualifying intraday chart (5–15m).

Use the swing low levels to monitor liquidity-rich zones.

Combine with your personal strategy to identify liquidity grabs, potential reversal zones, or entry points following a sweep.

Let the built-in cleanup logic remove any already-mitigated levels so you can focus on active targets.

🚀 What Makes It Unique:

This isn’t just another pivot plotter — it’s a smart, self-cleaning SMC tool designed for modern liquidity-based trading strategies.

A must-have for traders using concepts like liquidity grabs, mitigation blocks, or sweep-to-reverse trade models.

🔗 Best used in combination with:

✅ First FVG — Opening Range Fair Value Gap Detector: Pinpoint the day’s first imbalance zone for intraday setups.

✅ ICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels: Confluence-based entries powered by liquidity logic, order blocks, and premium/discount zones.

Used together, these scripts form a complete Smart Money toolkit — helping you build high-probability setups with confidence, clarity, and clean charts.

Cerca negli script per "smart"

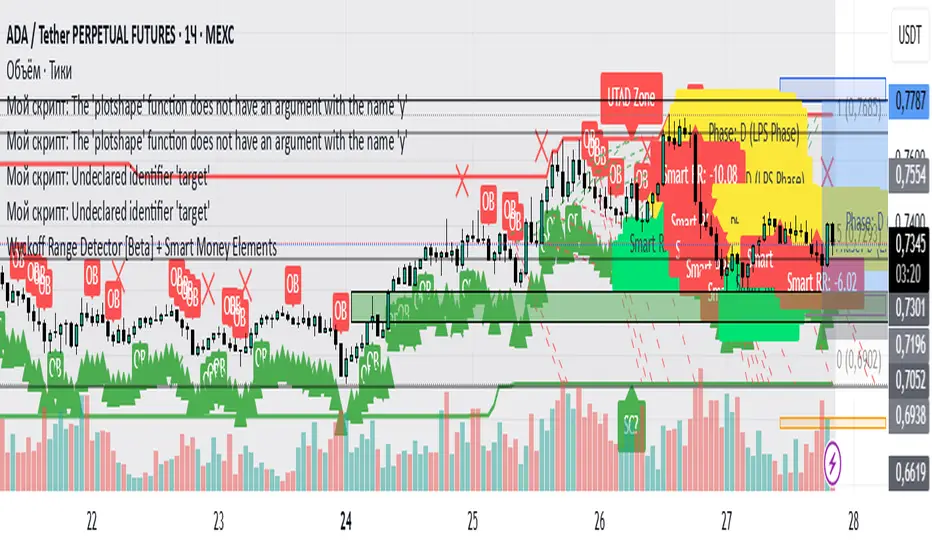

Wyckoff Range Detector [Beta] + Smart Money ElementsThis indicator detects the key phases of the Wyckoff market structure and integrates smart money elements, such as Order Blocks (OB), Fair Value Gaps (FVG), and Breaker Blocks. It also helps identify potential reversal zones (LPS, UTAD, Spring), breakout opportunities, and provides automatic Risk-Reward (R:R) calculations.

Key Features:

Wyckoff Phases Detection:

Automatically detects key phases of Wyckoff's market structure:

B (Range) – The initial range of accumulation.

C (Spring Phase) – Accumulation phase with a potential breakout.

C (UTAD Phase) – Upthrust After Distribution, indicating a potential reversal.

D (LPS Phase) – Last Point of Support, signaling accumulation before a breakout.

E (Breakout) – Phase marking breakout from range.

Re-Accumulation – Possible continuation in the range after a breakout.

Re-Distribution – Possible breakdown of a distribution phase.

Smart Money Elements:

Order Blocks (OB): Identifies Bullish and Bearish OBs to anticipate market entries.

Fair Value Gap (FVG): Highlights imbalance areas where price is likely to return.

Breaker Blocks: Marks areas where the price has previously broken a structure, indicating strong supply/demand zones.

Automatic Risk-Reward Calculation:

Smart RR: Automatically calculates Risk-Reward (R:R) ratios from LPS phases and Order Blocks. It draws lines to indicate target and stop levels with green for the target and red for the stop.

Visual representation of the entry signal with target and stop levels displayed.

Alerts:

Set alerts for phase changes, breakout, re-accumulation, or re-distribution to stay updated on the market’s movements.

Visual Tools:

Labels are used to indicate key zones such as AR, SC, LPS, and Spring Zones.

Draw boxes for the Spring and LPS phases to highlight areas where price action is likely to reverse.

Lines to represent potential breakouts, with customizable risk-reward indicators.

How to Use:

Apply the Indicator on any chart.

Identify Wyckoff phases to understand market trends.

Monitor Smart Money Elements (OB, FVG, Breaker) for entry and exit points.

Use automatic Risk-Reward levels for managing trades.

Set alerts for various Wyckoff phases and smart money signals to stay updated.

RSI+ Crypto Smart Strategy by Ignotus ### **RSI+ Crypto Smart Strategy by Ignotus**

**Description:**

The **RSI+ Crypto Smart Strategy by Ignotus** is an advanced and visually enhanced version of the classic **Relative Strength Index (RSI)**, developed by the **Crypto Smart** community. This indicator is designed to provide traders with a clear and actionable view of market momentum, overbought/oversold conditions, and potential reversal points. With its sleek design, customizable settings, and intuitive visual signals, this tool is perfect for traders who want to align their strategies with the principles of the **Crypto Smart** methodology.

Whether you're a beginner or an experienced trader, this indicator simplifies technical analysis while offering powerful insights into market behavior. It combines traditional RSI calculations with advanced visual enhancements and natural language interpretations, making it easier than ever to interpret market conditions at a glance.

---

### **Key Features:**

1. **Enhanced RSI Visualization:**

- The RSI line dynamically changes color based on its position relative to the 50-level midpoint:

- **Green** for bullish momentum (RSI > 50).

- **Red** for bearish momentum (RSI < 50).

- Overbought (default: 70) and oversold (default: 30) levels are clearly marked with customizable colors and shaded clouds for better visibility.

2. **Customizable Settings:**

- Adjust the RSI period, overbought/oversold thresholds, and background transparency to match your trading style.

- Fine-tune pivot lookback ranges and other parameters to adapt the indicator to different timeframes and assets.

3. **Interactive Information Table:**

- A compact, easy-to-read table provides real-time data on the current RSI value, its direction (▲, ▼, →), and a natural language interpretation of market conditions.

- Choose from three text sizes (small, medium, large) to optimize readability.

4. **Natural Language Interpretations:**

- The indicator includes a detailed explanation of the RSI's current state in plain English:

- Momentum trends (bullish, bearish, or neutral).

- Overbought/oversold warnings with potential reversal alerts.

- Clear guidance on whether the market is trending or ranging.

5. **Visual Buy/Sell Signals:**

- Triangles (▲ for buy, ▼ for sell) highlight potential entry and exit points based on RSI crossovers and divergence patterns.

- Configurable alerts notify you in real-time when key signals are triggered.

6. **Improved Aesthetics:**

- Clean, modern design with customizable colors for lines, clouds, and backgrounds.

- Dynamic shading and transparency options enhance chart clarity without cluttering the workspace.

---

### **How to Use This Indicator:**

- **Overbought/Oversold Zones:** Use the RSI's overbought (above 70) and oversold (below 30) zones to identify potential reversal points. Look for confirmation from price action or other indicators before entering trades.

- **Momentum Analysis:** Monitor the RSI's position relative to the 50-level midpoint to gauge bullish or bearish momentum.

- **Trend Identification:** Combine the RSI's readings with price trends to confirm the strength and direction of the market.

- **Entry/Exit Signals:** Use the visual signals (triangles) to spot potential entry and exit points. These signals are particularly useful for swing traders and scalpers.

---

### **Why Choose RSI+ Crypto Smart Strategy?**

This indicator is more than just an RSI—it's a complete tool designed to streamline your trading process. By focusing on clarity, customization, and actionable insights, the **RSI+ Crypto Smart Strategy** empowers traders to make informed decisions quickly and confidently. Whether you're trading cryptocurrencies, stocks, or forex, this indicator adapts seamlessly to your needs.

---

### **Developed by Crypto Smart:**

The **RSI+ Crypto Smart Strategy by Ignotus** is part of the **Crypto Smart** ecosystem, a community-driven initiative aimed at providing innovative tools and strategies for traders worldwide. Our mission is to simplify technical analysis while maintaining the depth and precision required for successful trading.

If you find this indicator helpful, please leave a review and share it with fellow traders! Your feedback helps us continue developing cutting-edge tools for the trading community.

---

### **Disclaimer:**

This indicator is a technical analysis tool and should not be considered financial advice. Trading involves risk, and past performance is not indicative of future results. Always conduct your own research and consult with a financial advisor before making trading decisions. Use of this indicator is at your own risk.

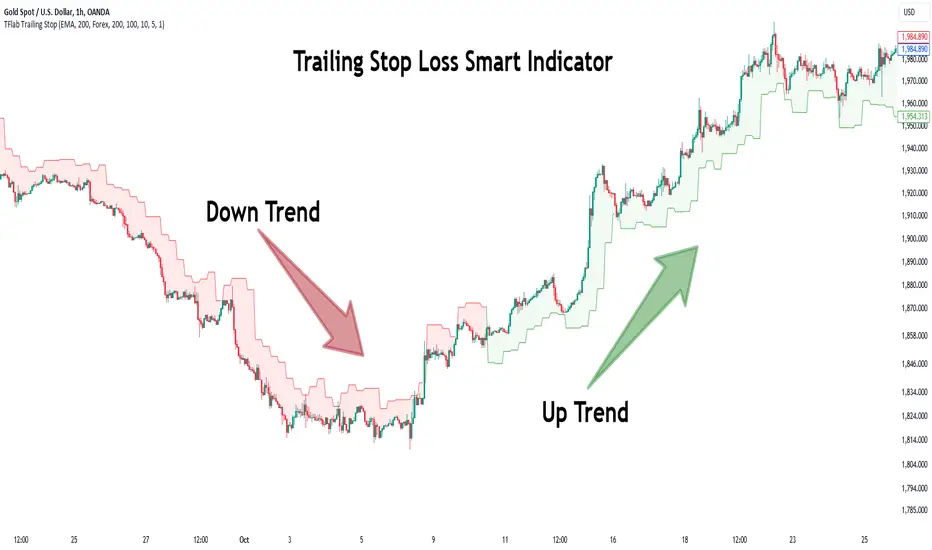

Trailing Stop Loss Smart [TradingFinder] Market Trend + CVD/EMA🔵 Introduction

Trailing Stop Loss (TSL) is one of the most powerful tools available. A Trailing Stop Loss is a modification of a typical stop order that adjusts dynamically based on market price movement. It can be set at a defined percentage or dollar amount away from the security's current market price, making it a flexible tool for locking in profits while minimizing risk. Unlike standard stop-loss orders, a Trailing Stop follows the market in the direction of the trade, protecting gains without requiring constant manual adjustments.

The Trailing Stop Loss Smart (TFlab Trailing Stop) indicator takes this concept even further by incorporating advanced metrics like Cumulative Volume Delta (CVD), volume dynamics, and Average True Range (ATR). This combination not only enhances risk management but also acts as a trend identifier, providing traders with a powerful tool to capitalize on both short-term and long-term price movements.

This indicator also supports various Order Types, allowing for flexible strategies that include a trailing stop/stop-loss combo to maximize winning trades while minimizing losses. The trailing stop limit is particularly useful for traders who want to set their stop at a precise level relative to the current market price, either by a percentage or a dollar amount. The Trailing Stop Loss Smart indicator can help ensure that traders do not exit too early during trends, while the stop-loss feature kicks in during reversals.

The advantages of using a Trailing Stop Loss are its ability to protect profits and reduce the emotional decision-making process in volatile markets. However, like all trading strategies, it has disadvantages, such as the risk of triggering too early during normal market fluctuations. By understanding how the Trailing Stop Loss Smart indicator integrates features like CVD, ATR, and volume analysis, traders can leverage its full potential while navigating these pros and cons.

With its unique ability to track market movements and trends using Cumulative Volume Delta, volume dynamics, and ATR-based trailing stops, this indicator offers a complete solution for traders looking to secure profits while minimizing downside risk. Whether you're employing a simple trailing stop or a trailing stop/stop-loss combo, this tool provides all the flexibility and precision needed to execute winning trades in various markets, including Forex, Crypto, and Stock.

🔵 How to Use

The Trailing Stop Loss Smart indicator integrates multiple advanced components to provide traders with superior risk management and trend identification.

Here’s how each part of the logic works :

🟣 Cumulative Volume Delta (CVD) Logic

The CVD tracks buying and selling pressure by calculating the difference between upward and downward price movements. When there’s more buying pressure, the CVD is positive, indicating a potential bullish trend. Conversely, more selling pressure results in a negative CVD, pointing to a bearish trend.

CVD Trend Detection : The indicator determines whether the market is in a bullish or bearish phase by comparing the CVD to its moving average. A bullish trend is confirmed when the CVD is above its moving average and the price is closing higher.

A bearish trend occurs when the CVD is below its moving average and the price is closing lower. This trend detection is critical for determining whether the trailing stop should be placed below the price (bullish) or above it (bearish).

🟣 Volume Dynamics

Volume is a key factor in identifying market strength. The Trailing Stop Loss Smart indicator pulls volume data based on the market selected (Forex, Crypto, or Stock) and adjusts the trailing stop based on whether the market is experiencing high volume or low volume.

High Volume : When the current volume exceeds the average volume, the market is in a high-volume state. During these conditions, the trailing stop is placed closer to the price, as high volume often indicates strong trends with less chance of reversals.

Low Volume : In low-volume conditions, the trailing stop gives the market more room to breathe by placing the stop further away from the price. This prevents premature stop-outs in periods of reduced market activity.

🟣 ATR-Based Trailing Stop

The Average True Range (ATR) is used to measure market volatility. The Trailing Stop Loss Smart uses the ATR to dynamically adjust the stop-loss distance.

Bullish Market : When a bullish trend is detected, the trailing stop is placed below the lowest price of the recent bars (determined by the Bar Back parameter), and adjusted by the ATR Multiplier. This allows for tighter protection during strong bullish trends.

Bearish Market : When the market is bearish, the trailing stop is placed above the highest price of recent bars, also adjusted by the ATR Multiplier. This ensures that short positions are safeguarded against sudden reversals.

🟣 Dynamic Stop-Loss Updates

The trailing stop is updated every few bars (according to the Refiner parameter), ensuring it remains relevant to the most recent price action and volume changes. This dynamic feature ensures the stop-loss adapts to both trending and volatile market conditions, without requiring manual intervention.

High Volume with Trends : In periods of high volume and a confirmed trend, the stop-loss is positioned tightly to lock in profits while minimizing the risk of reversal.

Low Volume with Trends : In low-volume conditions, the stop-loss is placed further from the price, allowing the market to move freely without triggering premature exits.

🟣 Visual Representation

The indicator visually represents the trailing stop on the chart, with green lines indicating bullish trends and red lines for bearish trends. This visual aid helps traders quickly assess the state of the market and the position of their trailing stop in real-time.

🔵 Settings

The Trailing Stop Loss Smart indicator offers several customizable settings to suit various trading strategies. Understanding these inputs is key to optimizing the tool for your specific trading style.

🟣 General Settings

Cumulative Mode : This controls how the CVD is calculated.

You can choose between :

EMA : Exponential Moving Average smoothing.

Periodic : Sums the delta over a fixed period.

CVD Period : Defines the look-back period for CVD calculation. A longer period smooths the data, making it less sensitive to short-term fluctuations.

Ultra Data : This Boolean input aggregates volume across multiple exchanges for a more comprehensive view of market activity.

Market Ultra Data : Select between Forex, Crypto, and Stock to ensure the indicator pulls accurate volume data for your market.

🟣 Logical Settings

Moving Average CVD Period : Defines the period for the moving average of the CVD. A longer period smooths the trend, reducing noise.

Moving Average Volume Period : Sets the period for the moving average used to distinguish between high and low volume conditions.

Level Finder Bar Back : Determines how many bars to look back when identifying the highest or lowest price for trailing stop placement.

Levels update per candles : Sets how often (in bars) the trailing stop should be updated to remain in sync with market movements.

ATR On : Toggles the use of ATR to adjust the trailing stop based on volatility.

ATR Multiplie r: Defines how far the stop is placed from the price based on the ATR. A larger multiplier increases the stop distance, reducing the likelihood of getting stopped out during market fluctuations.

ATR Multiplier Adjusts the distance of the trailing stop based on the ATR. A higher multiplier places the stop further from the price, providing more breathing room in volatile markets.

🔵 Conclusion

The Trailing Stop Loss Smart indicator is a comprehensive tool for traders looking to manage risk while identifying market trends. By incorporating Cumulative Volume Delta (CVD) to detect buying and selling pressure, volume dynamics to gauge market activity, and ATR to adjust for volatility, this indicator ensures that stop-loss levels are both adaptive and protective.

Whether you’re trading in Forex, Crypto, or Stock markets, the Trailing Stop Loss Smart allows you to capitalize on trends while dynamically adjusting to changing market conditions. Its ability to distinguish between high-volume and low-volume periods ensures that you’re not stopped out prematurely during periods of consolidation or market hesitation.

By providing real-time visual feedback, dynamic adjustments, and trend identification, this indicator serves as a vital tool for traders aiming to maximize profits while minimizing risk. Its versatility and adaptability make it an essential part of any trader’s toolkit, helping you stay ahead in fast-moving markets while safeguarding your positions.

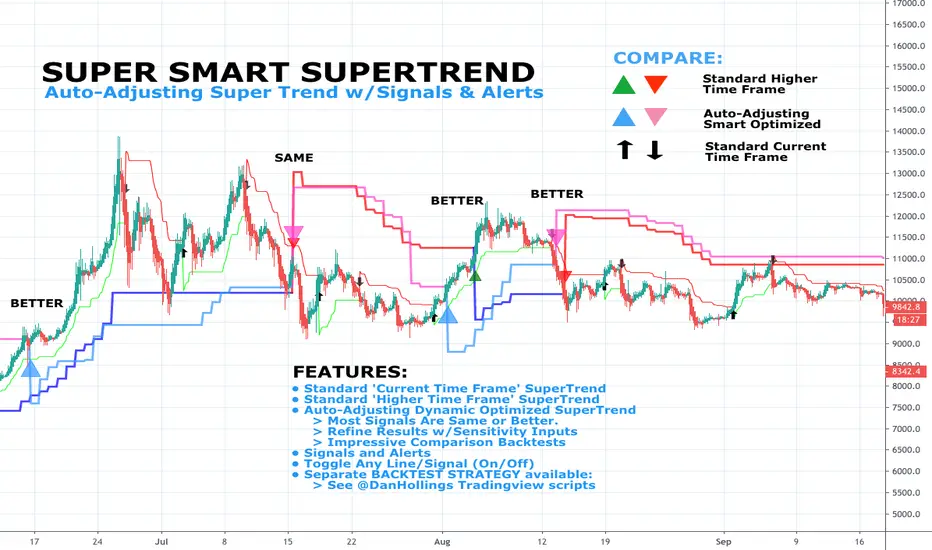

DH: (Study) Super Smart SuperTrend: Self AdjustingSUPER SMART SUPERTREND (Study Version w/Alerts)

Using data from other indicators I came up with a SMART SUPERTREND that auto-adjusts as the market changes - shall we call it "Artificial Intelligence?" Yes, you can fine tune it for specific assets and timeframes, but once the settings are entered, it auto-adjusts as the market and prices evolve.

This is the STUDY version of "Super Smart SuperTrend" with ALERTS. There is also a STRATEGY version which is designed for backtesting various settings.

STRATEGY VERSION FOR BACKTESTING IS HERE

ABOUT THIS INDICATOR

As the name suggests, 'Supertrend' is a trend-following indicator that is notably popular here on Tradingview and elsewhere. It does a remarkably great job of recognizing a trend (in progress) and it will signal you to initiate a position when the trend is clear. Perhaps the greater value of Supertrend is that it helps keep you in your position until that trend is over.

WHAT'S THE BEST ATR PERIOD AND MULTIPLIER?

There are two important data points we must enter for Supertrend to work, namely the 'period (ATR number of candles or days)' and the 'multiplier (value by which ATR is multiplied)' BTW, in case you don't know, ATR signals the degree of price volatility. A common default setting is 10 for the ATR period and 3 for the multiplier.

SORRY, BUT THE MOVIE STARTED HALF HOUR AGO...

Unfortunately Supertrend has a couple of big weaknesses. Generally, it fails in a sideways-moving market and when it does detect a trend, the signal to get in (or out) comes rather late. It's like someone telling you about a great movie they're watching, but by the time you start watching, one-third of the movie is over... bummer, right?

HOW TO IMPROVE SUPERTREND

One solution is to combine Supertrend with other indicators such as MACD, Parabolic SAR, RSI, etc. And another solution is to experiment (backtest) with the Period and Multiplier settings for the asset and timeframe you are considering for trade.

For the STANDARD SETTINGS in this "Super Smart SuperTrend" indicator, I have set 9 for the ATR and 2.2 for the multiplier as default after backtesting on Bitcoin and other crypto (mostly in the 15 minute to 6 HOUR timeframe). Of course you can change this easily to any ATR period and Multiplier you like.

BUT... WHY NOT GET SMART?

I started thinking, it might be best if we let the market determine candle-by-candle what the settings should be. If everyone says that Supertrend works best in conjunction with other indicators, why not do our "conjuncting" programmatically (ie: automatically) sorta like artificial intelligence!

HOW IT WORKS

So here's what I did. Using data from other indicators I came up with a SMART SUPERTREND that auto-adjusts as the market changes. It still has settings so you can fine tune it for specific assets and timeframes, but once the settings are entered, it auto-adjusts as the market and prices evolve.

With "Super Smart SuperTrend" there is no ATR period setting (that is determined programmatically) and now there are TWO multipliers you can experiment with... (a lower one set at 1.7 default and a higher one at 2.5). These multiplier settings create a multiplier range that can be used programmatically to adjust the multiplier as the market and prices evolve.

THE RESULTS

Across all time frames and assets I've tested, I generally get better results. Better entries, better exits and well defined trends. In comparison with a STANDARD Supertrend, it is not radically different, but when it does differ "Super Smart SuperTrend: is almost always better. All this is substantiated by backtesting of course.

SAMPLE BACKTEST RESULTS (BTC/USD)

Using Indicator Defaults

TIMEFRAME STANDARD RESULTS SUPER SMART RESULTS

% Profitable | Profit Factor % Profitable | Profit Factor

DAY 58.33% 9.38 75.00% 10.77

4 HOUR 78.43% 18.22 80.95% 21.78

1 HOUR 74.11% 8.98 70.13% 9.34

15 MIN 58.10% 6.10 71.43% 9.48

Keep in mind that "Profit Factor" is key. It basically tells you what you'd make for every ONE DOLLAR invested by consistently trading with the backtested parameters.

SUPER SMART SUPERTREND FEATURES

• There is a STUDY VERSION w/Alerts

• There is a STRATEGY VERSION for Backtesting

• Standard 'Current Time Frame' SuperTrend Line

• Standard 'Higher Time Frame' SuperTrend Line

• Auto-Adjusting Dynamic Optimized SuperTrend Line

> Most Signals Are Same or Better than Standard

> Refine Results w/Sensitivity Inputs (2 Multipliers)

> Impressive Comparison Backtests

• Both Standard and Smart Signals and Alerts

• Toggle Any Line/Signal (On/Off)

• Toggle Backtest

> Standard vs. "Smart Auto-Adjust"

> Backtest Higher Timeframe Only

WHAT MORE COULD YOU ASK FOR?

So glad you asked. Actually, there is more... Super Smart SuperTrend is incorporated into my premier indicator set called: STONEHENGE PLUS: SUPERTREND TRADING TOOLKIT.

With STONEHENGE, I'm combining this Super Smart SuperTrend with dozens of other indicators plus predictive "Stones." Check out STONEHENGE... you'll be in Trader's Heaven.

That's it. Get "SMART" Today!

STONEHENGE PLUS:

The Complete SuperTrend Trading Toolkit

SUPER SMART SUPERTREND ALSO WORKS WITH:

STONEHENGE BASIC: Double Stone Version (Study w/Alerts):

######

######

PLEASE HIT THE LIKE BUTTON (and follow me... lots of great stuff in the works!)

As always, I appreciate your support. Please share with others.

ENJOY!

Dan Hollings

Master Crypto Grid Trader

Stonehenge Master Mason

Host of the "High Leverage Lounge"

Please Explore My Other Indicators, Scripts, Grids and Educational Ideas.

@DanHollings on Tradingview.

Additional Links Below...

Elev8+ Impulse Levels | Smart Support & ResistanceElev8+ Impulse Levels

Why does price reject specific levels that look "empty" on the chart?

The answer usually lies in the past. These are Institutional Impulses—footprints left behind by massive market moves that algorithms and smart money defend days or even weeks later.

The Elev8+ Impulse Levels indicator is designed to automatically reveal this hidden Market Structure. It scans for the "Perfect Storm" of Volume + Aggression and projects these critical levels forward for you.

🧠 How It Works (The Logic)

This is not a standard Support & Resistance tool. It does not look for swing highs or lows. Instead, it detects Market Intent.

The indicator highlights specific candles where:

Volume Spikes: Buying or Selling pressure exceeds the average by a significant multiplier.

Volatility Expands: The candle body is unusually large relative to recent price action (ATR).

When these two factors combine, it signals that a major player has entered the market. The closing price of this impulse becomes a "Line in the Sand" for future price action.

🎯 How to Trade This Strategy

We built a "Smart Line" feature into this tool that changes the visual style of the level based on price behavior. This helps you trade two distinct setups:

1. The Defense (Bounce)

Visual: 🟢 Solid Lines

The Setup: A Solid Line represents a Fresh Level that has never been touched.

Why it works: Institutions often defend their entry price. When price returns to a fresh Solid Line, look for a rejection or a bounce.

2. The Flip (Break & Retest)

Visual: ◌ Dotted Lines

The Setup: When a candle closes past a level, the indicator automatically dims it to a Dotted Line.

Why it works: This signals a "Breaker Block." If a Support level (Green) is broken, it often flips to become Resistance. Watch for price to come back and "kiss" the Dotted Line from the other side before continuing the trend.

✨ Key Features

Smart Visualization: Lines automatically switch from Solid to Dotted when broken, keeping your chart analysis clean and logical.

Impulse Coloring: The indicator highlights the specific candle that created the level, so you can see the origin of the move.

Fully Customizable: Adjust the sensitivity of the Volume and Size detection to fit any asset class (Crypto, Forex, Futures, or Stocks).

🚀 The Elev8+ Workflow

Elev8+ Impulse Levels gives you the "Map"—it tells you where the market is likely to react.

To know exactly when to enter, we recommend pairing this tool with our premium Elev8+ Reversal Indicator, which specializes in timing the entry signal precisely when price hits these high-value levels.

Build your narrative. See the structure. Elev8 your trading.

Disclaimer: Trading involves high risk. This tool is for educational purposes to assist with technical analysis and does not guarantee future performance.

See Where The Banks Are Hunting: Liquidity X-Ray[@Ash_TheTrader]# 🛑 Stop Being "Liquidity." Start Seeing the Trap.

### Introducing: **Liquidity X-Ray **

How many times have you placed your stop-loss just below a perfect support level, only to watch a single candle wick down, trigger your stop, and immediately reverse toward your original target?

You weren't unlucky. You were targeted.

Welcome to the world of Smart Money Concepts (SMC). In the institutional game, your stop loss isn't protection—it's fuel. The market makers need liquidity to fill huge orders, and they find it clustered at obvious swing highs and lows.

I developed the **Liquidity X-Ray** to stop guessing where these traps are laid. This isn't just another support and resistance tool; it’s a dynamic, living heatmap of market psychology.

---

### 🧠 The Philosophy: The "Time-Decay" Algorithm

Standard indicators draw static lines that clutter your chart. The **Liquidity X-Ray** is different. It understands that *time* is a crucial factor in building liquidity pressure.

I have engineered a unique **Time-Decay Intensity** feature into this script. It visualizes the density of resting orders based on how long a level has remained untouched.

#### The Visual Language:

* **👻 The Ghosts (New Zones):** When a new swing high or low forms, a faint, transparent zone appears. It’s watching.

* **💡 The Neon Traps (Mature Zones):** As time passes and price fails to revisit that level, the zone solidifies. It becomes brighter, more opaque, and intensely neon. **This is your signal.** A bright neon zone means a massive pile of retail stop-losses has accumulated there. The Banks *need* to visit it.

* **💥 The Sweep Explosion:** When price finally pushes into a mature zone, the script detects the "Liquidity Grab." The box flashes bright white, cuts off immediately, and prints a **💥 LIQ GRAB** label on your chart. The trap has been sprung.

---

### ⚙️ Key Features & Cyberpunk Aesthetics

This tool is designed to look incredible on dark charts while providing institutional-grade data.

* **Dynamic Buyside/Sellside Heatmaps:** Clear visual distinction between where shorts are trapped (Neon Red/Pink) and where longs are trapped (Neon Cyan).

* **Smart Memory Management:** The script intelligently manages old zones to ensure your chart *never* lags, regardless of the timeframe.

* **Volume Filtering (Optional):** You can choose to only plot zones formed on high-volume pivot points, ensuring you are only watching significant market structures.

* **Instant Alerts:** Set alerts for the "Sweep Explosion" so you never miss a major reversal setup.

---

### 🎯 How to Trade the X-Ray

**Do NOT trade the breakout of these zones.** These are traps.

1. **Identify the Target:** Look for the oldest, brightest, most solid neon zones on your timeframe (H1 and H4 are powerful).

2. **Wait for the Hunt:** Be patient. Let price aggressively move toward the zone.

3. **The Explosion:** Wait for the candle to wick into the zone and trigger the **💥 LIQ GRAB** visual.

4. **The Reversal Entry:** Once the liquidity is taken, look for lower timeframe confirmation (like a Change of Character or engulfing candle) in the *opposite* direction. You are now trading *with* the smart money recovery, not *against* their stop hunt.

---

### Author's Note

Trading is about information asymmetry. The institutions have seen your stops for decades. It’s time you started seeing where they are hunting.

Trade smart, stay safe.

— **@Ash_TheTrader**

AlgoZ Smart Divergence [Trend Filtered]AlgoZ Smart Divergence is a precision entry tool designed to catch market reversals by analyzing Volume Divergence combined with Multi-Timeframe Trend Filtering. Unlike standard divergence indicators that signal on every minor price fluctuation, this script uses a strict set of filters to only present high-probability trade setups that align with the broader market trend.

This is the Free Edition of the AlgoZ Suite, focused on providing clean, non-repainting Buy and Sell signals based on institutional volume flow.

How It Works The script operates on a 3-step validation process:

Volume Divergence:

It detects anomalies where volume spikes relative to price action (e.g., Price makes a Lower Low, but Volume hits a Higher High).

HTF Trend Painting:

It analyzes a Higher Timeframe (Default: 3 Hours) to determine the macro trend. If the 3H trend is Bullish, the candles turn Green. If Bearish, they turn Red.

Color Match Filtering:

The script includes a smart filter that blocks signals that go against the trend. You will only see BUY signals when the candles are Green (Uptrend) and SELL signals when the candles are Red (Downtrend).

Key Features

Volume Divergence Engine:

Identifies hidden accumulation and distribution zones.

HTF Trend Coloring:

Automatically paints your chart based on Higher Timeframe breakouts (Default: 3-Hour Trend).

Smart Signal Filtering:

Toggles are available to "Only Show Signals Matching Candle Color," ensuring you never trade against the momentum.

EMA Trend Filter:

Includes a built-in 10-period EMA filter to further refine entries.

Volatility Filters:

Optional RSI and ADX filters are included to avoid trading during low-volatility "chop."

How to Use

For Longs (Buys):

Wait for the candles to turn Green (indicating the 3-Hour trend is up) and look for a BUY label. The price must also be above the 10 EMA (if enabled).

For Shorts (Sells):

Wait for the candles to turn Red (indicating the 3-Hour trend is down) and look for a SELL label.

Risk Management:

This script is designed to catch reversals. Always place your Stop Loss below the recent swing low (for buys) or above the swing high (for sells).

Settings

Higher Timeframe:

Default is set to 3 Hours (180 minutes). You can adjust this to 1 Day or 4 Hours depending on your trading style.

EMA Length:

Default is 10.

Color Match Filter:

On by default.

智能趋势-多周期动态信号 Smart Trend Oscillator MTF V1🚀 智能趋势-多周期动态信号 Smart Trend Oscillator MTF V1

—— 让交易像红绿灯一样简单直观 | Making Trading as Simple as Traffic Lights

告别复杂的参数设置,把市场噪音变成明确的信号。 Say goodbye to complex parameters. Turn market noise into clear signals.

🌟 它是做什么的? / What Does It Do?

“智能趋势管家” 就像您的私人交易副驾驶。它内置了一套先进的智能平滑算法,能够自动过滤掉市场中那些骗人的假动作,只把最核心的**“市场真实韵律”通过一条平滑的波浪线展示给您。它不只是一根线,它是一套会思考的系统**。

"Smart Trend Oscillator " is like your personal trading co-pilot. It features a built-in advanced smoothing algorithm that automatically filters out deceptive market "fake-outs," revealing the "true rhythm" of the market through a single, smooth wave. It’s not just a line; it’s a thinking system.

🔥 核心功能 / Core Features

1. 🌊 智能波浪引擎 / Smart Wave Engine

不要被K线的上蹿下跳迷惑。我们的引擎能识别市场内部的真实能量。 Don't be confused by erratic candlesticks. Our engine identifies the true internal energy of the market.

过滤噪音 (Filter Noise):自动忽略短暂的随机波动。

捕捉趋势 (Capture Trends):波浪上升代表买方主导,波浪下降代表卖方主导。

2. 🛡️ 自适应波动通道 / Adaptive Channels

市场有时候像乌龟(波动小),有时候像兔子(波动大)。指标拥有一个“弹性通道”,它会根据市场活跃度自动变宽或变窄,精准判断价格是否“过热”或“超卖”。 The market moves between low and high volatility. The indicator features an "elastic channel" that automatically widens or narrows, accurately judging if the price is "Overheated" or "Oversold."

3. 🌍 全局监控面板 / Global Dashboard

右上角的面板是您的战况指挥室。一眼看懂 6 个不同时间维度的状态。全绿代表多周期共振向上,全红代表多周期共振向下。 The panel in the top-right corner is your Command Center. Understand the status of 6 different time dimensions at a glance. All Green means upward resonance; All Red means downward resonance.

⚙️ 极致的个性化定制 / Ultimate Customization

v16 版本为您提供了前所未有的控制权,让指标完全适应您的交易风格。 Version 16 gives you unprecedented control to tailor the indicator to your trading style.

🕒 1. 时间周期,由你定义 (Customizable Timeframes)

不再局限于系统默认设置。您可以在设置面板中自由输入 6 个您最关心的周期(例如:5分钟、1小时、甚至 3天)。

短线手:设置为 1分/3分/5分/15分...

波段手:设置为 1小时/4小时/日线/周线...

Benefit: You can freely input the 6 timeframes that matter most to you in the settings panel, whether you are a scalper or a swing trader.

🎯 2. 灵敏度调节 (Adjustable Sensitivity)

想要更多交易机会?还是想要更稳健的信号?

高灵敏度:调高 Zone Sensitivity,捕捉每一次微小的回调(适合激进风格)。

低灵敏度:调低数值,过滤掉小波动,只抓大趋势(适合稳健风格)。

Benefit: Dial up the sensitivity to catch every minor pullback (Aggressive), or dial it down to filter noise and catch only big trends (Conservative).

📊 3. 两种平滑模式 (SMA vs. VWMA)

您可以选择通道的计算核心:

Standard (SMA):经典模式,适合大多数市场。

Volume Weighted (VWMA):成交量加权模式。在加密货币或股票市场,它能帮您过滤掉“无量空涨”或“无量空跌”的假信号。

Benefit: Choose Standard (SMA) for general markets, or Volume Weighted (VWMA) to filter out fake moves on low volume (great for Crypto/Stocks).

🚦 信号含义 / Signals Guide

我们把复杂的逻辑浓缩成了最简单的视觉标签: We have condensed complex logic into the simplest visual labels:

🟢 绿色 BUY 标签:市场“便宜”且能量向上。 (Market is "Cheap" & Energy is Up.)

🔴 红色 SELL 标签:市场“过热”且能量向下。 (Market is "Overheated" & Energy is Down.)

🔵 蓝色 HOLD 标签:趋势延续中,建议持仓。 (Trend is continuing, suggest holding position.)

📥 快速上手 / Quick Start

加载指标 (Load):添加到您的图表。

设置周期 (Set Timeframes):在输入选项里填入您习惯查看的 6 个时间周期。

选择模式 (Choose Mode):如果是成交量重要的资产,建议开启 VWMA 模式。

等信号 (Wait):等待带方框的 BUY 或 SELL 标签出现。

把复杂留给算法,把简单留给您。 Leave the complexity to the algorithms, and keep the simplicity for yourself.

FX OSINT - Institutional Midnight Intelligence For ForexFX OSINT — Institutional Midnight Intelligence For Forex

See Your FX Charts Like an Intelligence Briefing, Not a Guess

If you’ve ever stared at EURUSD or GBPJPY and thought:

Where is the real liquidity?

Is this move sponsored by smart money or just noise?

Am I buying into premium or discount?

…then FX OSINT is designed for you.

FX OSINT (Forex Open Source Intelligence) treats the FX market the way an analyst treats an investigation:

Collect open‑source signals from price, time, and volatility.

Map out liquidity, structure, and sessions in a repeatable way.

Present them in a clean, non‑cluttered dashboard so you can read context quickly.

No rainbow spaghetti. No 12 indicators stacked on top of each other. Just structured information, midnight visuals, and a clear read on what the market is doing right now.

Why FX OSINT Exists

Many FX traders run into the same problems:

Overloaded charts – multiple indicators fighting for space, none talking to each other.

Signals with no context – arrows that ignore structure, sessions, and liquidity.

Tools not tuned for FX – generic indicators that don’t care what pair you are on.

FX OSINT brings this together into one FX‑focused framework that:

Understands structure : BOS/CHOCH, swings, and trend across multiple timeframes.

Respects liquidity : sweeps, order blocks, and FVGs with controlled visibility.

Reads volatility & ADR : how far today’s range has developed.

Knows the clock : London, New York, and key killzones.

Scores confluence : a 0–100 engine that summarizes how much is lining up.

FX OSINT is built for traders who want structured, institutional‑style logic with a disciplined, midnight‑themed UI —not flashing buy/sell buttons.

1. Midnight Dashboard — Top‑Right Intelligence Panel

This panel acts as your compact “situation room”:

CONFLUENCE — 0–100 score blending trend alignment, volatility regime, sessions, liquidity events, order blocks, FVGs, and ADR context.

REGIME — Low / Building / Normal / Expansion / Extreme, driven by ATR relationships, so you know if you’re in chop, trend, or expansion.

HTF / MTF / LTF TREND — Higher‑, medium‑, and current‑timeframe bias in one place, so you see if you are trading with or against the larger flow.

ADR USED — How much of today’s typical range has already been consumed in percentage terms.

PIP VALUE — Approximate pip size per pair, including JPY‑style pairs.

Everything is bold, legible, and color‑coded, but the layout stays minimal so you can:

Look once → understand the context.

2. Structure, BOS, CHOCH — Smart‑Money‑Style Skeleton

FX OSINT tracks swing highs and lows, then shows how structure evolves:

Trend logic based on evolving swings, not just a moving average cross.

BOS (Break of Structure) when price expands in the direction of trend.

CHOCH (Change of Character) when behavior flips and the market structure changes.

Labels are selective, not spammy . You don’t get a tag on every minor wiggle—only when structure meaningfully shifts, so it’s easier to answer:

"Are we continuing the current leg, or did something actually change here?"

3. Liquidity Sweeps, Order Blocks & FVGs — The OSINT Layer

FX OSINT treats liquidity as a key information layer:

Liquidity sweeps — Detects when price spikes through recent highs/lows and then snaps back, flagging potential stop runs.

Order blocks — The last opposite candle before a displacement move, drawn as controlled boxes with limited lifespan to avoid clutter.

Fair Value Gaps (FVGs) — Three‑candle imbalances rendered as precise zones with a cap on how many can exist at once.

Under the hood, boxes are managed so your chart does not become a wall of old zones:

// Draw Order Blocks with overlap prevention

if isBullishOB and showOrderBlocks

if array.size(obBoxes) >= maxBoxes

oldBox = array.shift(obBoxes)

box.delete(oldBox)

newBox = box.new(bar_index , low , bar_index + obvLength, high ,

border_color = bullColor, bgcolor = bullColorTransp,

border_width = 2, extend = extend.none)

array.push(obBoxes, newBox)

Box limits keep the number of zones under control.

Borders and transparency are tuned so you still see price clearly.

You end up with a curated liquidity map , rather than a chart buried under every level price has ever touched.

4. Volatility, ADR & Sessions — Time and Range Intelligence

FX OSINT runs a Volatility Regime Analyzer and an ADR engine in the background:

Volatility regime — Five states (Low → Extreme) derived from fast vs. slow ATR.

ADR bands — Daily high/mid/low projected from the current daily open.

ADR used % — How far today’s move has traveled relative to its typical range.

On the time side:

Asia, London, New York sessions are softly highlighted with a single active background to avoid overlapping colors.

Killzones (e.g., London and New York opens) can be emphasized when you want to focus on where significant moves often begin.

Together, this helps you answer:

"What time is it in the trading day?"

"How stretched are we?"

"Is expansion just starting, or are we late to the move?"

5. ICT‑Style Add‑Ons — BOS/CHOCH, Premium/Discount, and Confluence

For modern FX / ICT‑inspired workflows, FX OSINT includes:

BOS / CHOCH labels — Clear structural shifts based on swings.

Premium / Discount zones — 25%, 50%, 75% levels of the daily range, so you know if you are buying discount in an uptrend or selling premium in a downtrend.

Confluence score — A single number summarizing how many conditions line up in the current context.

Instead of replacing your plan, FX OSINT compresses your checklist into the chart:

Structure

Liquidity

Session / Time

Volatility / ADR

Higher‑timeframe alignment

When these agree, the dashboard reflects it. When they don’t, it stays neutral and lets you see the conflict.

How To Use FX OSINT

FX OSINT is not a signal bot. It is an information engine that organizes context so you can apply your own plan.

A typical workflow might look like:

Start on higher timeframes (e.g., H4/D1) to form directional bias from structure, volatility regime, and ADR context.

Move to intraday timeframes (e.g., M15/H1) around your chosen sessions (London and/or New York).

Look for confluence :

HTF / MTF / LTF trends aligned.

Price in discount for longs or premium for shorts.

Recent liquidity sweep into a meaningful OB or FVG.

Confluence score at or above a level you consider significant.

Then refine entries using BOS/CHOCH on lower timeframes according to your own risk and execution rules.

FX OSINT aims to make sure you do not enter a trade without seeing:

Where you are in the day (ADR and sessions).

Where you are in the volatility cycle (regime).

Who currently appears in control (structure and trend).

Which liquidity was just targeted (sweeps and zones).

Design Choices and Scope

FX OSINT was designed around a few clear constraints:

FX‑focused — Logic and filters tuned for FX majors, minors, exotics, and metals. It is intended for FX markets, not for every possible asset class.

Open‑source — The full Pine Script code is available so you can read it, learn from it, and adapt it to your own workflow if needed.

Clear themes — Two main visual styles (e.g., dark institutional “midnight” and a lighter accent variant) with a focus on readability, not visual noise.

Chart‑friendly — Panels use fixed areas, session highlights avoid overlapping, and boxes are capped/pruned so the chart remains usable.

FX OSINT is for only Forex pairs, not anything else!

Hope you enjoyed and remember your Open Source Intelligence Matters 😉!

-officialjackofalltrades

Forex Knack — Premium Smart Money Indicator📈 Forex Knack — Premium Smart Money Indicator

Developed by Vineesh Rohini

Forex Knack is an invite-only, institutional-grade Smart Money Concepts toolkit built for traders who want clarity, precision and high-quality confluence — without leaking the internal logic.

This indicator combines market structure mapping, dynamic trend shifts, valuation zones and multi-layer confirmation into a clean, professional interface suitable for Forex, XAUUSD (Gold), Crypto and major Indices.

★ Core Benefits

- ✅ Cleaner Market Structure: Live BOS / CHoCH mapping for internal + swing structure.

- ✅ Directional Clarity: Proprietary “Shift” model to identify buy/sell phases.

- ✅ Confluence Signals: Combo confirmations when structure + momentum align.

- ✅ Premium / Discount Zones: Automatic institutional zones for better entries.

- ✅ Order Block Visuals: Internal & swing order block identification.

- ✅ Fair Value Gaps (optional): Imbalance highlighting for tactical entries.

- ✅ Momentum Confirmation: Oscillator-based trend confirmation.

- ✅ Strong / Weak Highs & Lows: Quick strength/weakness view for swing decisions.

🚫 What’s NOT included

- No full strategy code or secret formulas are revealed.

- Not a turnkey “auto-trade” bot — it is a professional decision-support tool.

🔒 Invite-only Access

This script is invite-only: the source code is fully protected and hidden.

You may apply for access; approved users can add the indicator to their charts but **will never** see the source code.

📬 How to request access

1. Follow the author profile on TradingView.

2. Send a message with your TradingView username and the note:

“Requesting access to Forex Knack indicator.”

(Access is granted manually after verification.)

⚠ Disclaimer

For educational purposes only. Not financial advice. Use with proper risk management.

© Vineesh Rohini — Forex Knack

SMC Pre-Trade Checklist (Mozzys)Here is a **clean, professional description** you can use when publishing your TradingView script.

It clearly explains what the indicator does and why traders use it—perfect for the public library.

---

# **📌 Script Description (for Publishing)**

**SMC Pre-Trade Checklist (Compact Edition)**

This indicator provides a **smart, compact on-chart checklist** designed for traders who use **Smart Money Concepts (SMC)**.

Instead of guessing or rushing entries, the checklist helps you confirm the essential SMC conditions *before* taking a trade.

The checklist displays as a **small 3-column panel** in the corner of your chart, making it easy to scan without covering price action.

All items are controlled through indicator settings, where you can tick each condition as you validate it in your analysis.

---

## **🔥 What This Tool Helps You Do**

This script helps you stay disciplined by verifying the core components of an SMC setup:

### **1. Higher-Timeframe (HTF) Bias**

* Market direction clarity

* Premium vs. discount zones

* HTF POIs and liquidity targets

### **2. Liquidity Conditions**

* Liquidity sweeps

* Liquidity-based take-profit targets

### **3. Market Structure**

* BOS/CHOCH confirmation

* Displacement

* Clean pullback into POI

### **4. Entry Validation**

* Quality POI

* LTF confirmation

* Logical SL/TP and RR

### **5. Risk Management**

* Correct position sizing

* Avoiding high-impact news

* Spread/volatility conditions

### **6. Trader Discipline**

* Trade matches your model

* No revenge or emotional trading

---

## **🎯 Why Traders Love This**

Most losses come from **breaking rules**, not market randomness.

This checklist forces consistency, clarity, and patience—especially in fast environments like FX, indices, and crypto.

* Prevents emotional entries

* Reduces impulsive trades

* Keeps you aligned with your SMC plan

* Works with any strategy or SMC style

* Clean, minimal, non-intrusive layout

---

## **📌 Features**

* Compact 3-column layout

* Customizable from the indicator settings

* Works on all timeframes and assets

* Zero chart clutter

* Perfect for rule-based traders

---

## **🚀 Who This Indicator Is For**

* SMC traders

* ICT-style traders

* Liquidity-based traders

* Anyone who wants more discipline & consistency

* Backtesters who want structured trade evaluation

--

Bassi MACD Pro + ADX Filter + Smart Histogram TP + RSIA professional-grade MACD indicator that dramatically reduces false signals by combining four powerful filters:

Key Features

Classic MACD (12,26,9) with clean, high-visibility histogram coloring

ADX + DI filter – only takes trades when ADX > user-defined threshold (default 25) ensuring you trade only in strong trending markets

Smart Histogram Take-Profit logic – automatically detects the exact moment bullish/bearish momentum starts to weaken after a strong move and marks a precise TP level (one TP per trade – no repainting, no multiple signals)

Zero-line crossover confirmation + histogram direction filter – eliminates many whipsaw signals common in regular MACD

Separate RSI pane with overbought/oversold levels and visual markers (for additional confluence – does not interfere with main logic)

Visual Signals

Green “MACD BUY” label + lime triangle = confirmed long entry in strong trend

Red “MACD SELL” label + red triangle = confirmed short entry in strong trend

Small lime/red “TP” triangles = Smart Histogram Take-Profit triggered (perfect exit timing based on momentum fade)

Alert Conditions Included

MACD BUY

MACD SELL

TP Long Hit

TP Short Hit

Combined “Any Signal” alert

Why this version outperforms standard MACD

Most MACD crossovers fail in ranging markets. This script solves that by:

Requiring strong trend (ADX filter)

Confirming histogram is actually growing in the new direction

Waiting for the true zero-line cross with momentum

Giving you an intelligent, non-fixed % take-profit based on real histogram exhaustion

Excellent for swing trading, day trading, crypto, forex, and stocks on any timeframe (works especially well on 1H–4H–Daily).

Clean, fast, no repainting, fully alert-ready.

Add to chart → set your alerts → trade only the highest-probability MACD signals.

Sima-Smart Money Concepts + RSI CandlestickThis indicator displays the RSI in a candlestick format and marks its support and resistance levels, as well as oversold and overbought zones based on Smart Money concepts.

In fact, this indicator is a combination of a candlestick-style RSI and a Smart Money indicator.

Sima-Smart Money Concepts + RSI Candlestick [LuxAlgo]This indicator displays the RSI in a candlestick format and marks its support and resistance levels, as well as oversold and overbought zones based on Smart Money concepts.

In fact, this indicator is a combination of a candlestick-style RSI and a Smart Money indicator.

JFX Smart ORBJFX Smart ORB is a complete visual trading framework built around the classic

Opening Range Breakout (ORB) concept, enhanced with:

Fixed position sizing (lots)

Automatic Martingale-style size increase after full SL only

A full, event-based alert system for entries, targets, stops, and break-even exits

All of that, plus a clean dual-language HUD (AR/EN) directly on your chart.

What JFX Smart ORB Does

🔹 Smart Opening Range (ORB)

Automatically defines the opening range via:

Fixed timeframe (e.g., 30 minutes), or

Custom session window (e.g., 09:30–09:45) with configurable time zone (UTC-5, etc.).

Plots ORH / ORL and the midline, and shades the OR building zone for visual clarity.

🔹 Regime Detection (Context)

Background shading tells you where price is trading:

📈 Green: Above ORH (bullish regime)

📉 Red: Below ORL (bearish regime)

🔵 Neutral: Inside the OR range

This gives you an instant read on context before you even think about entries.

🔹 Trade Logic & Multi-Target Management

Automatic entry when:

Price breaks ORH for long trades

Price breaks ORL for short trades

Stop loss on the opposite side of the range.

Targets calculated in R-multiples:

TP1 = 0.5R

TP2 = 1R

TP3 = 2R

Position is split across TP1 / TP2 / TP3 according to user-defined percentages, normalized automatically.

💰 Fixed Size + Martingale After Loss Only

Inputs:

Capital ($) – for display/analysis

Base Position Size (lots) – your standard trade size

Contract per 1.00 lot – to convert price movement to P/L in dollars

If a trade hits a full stop loss before TP1, the indicator:

Doubles the position size for the next trade (Martingale factor).

If the trade hits any profit (TP1, TP2, TP3) or closes at Break-Even, the:

Martingale factor resets back to 1× (base size).

Everything is tracked and shown on the chart: current trade size, P/L per trade, and net P/L.

🧠 Session Protection & Inner-Range Logic

Optional session block:

After a strong winning trade (e.g., TP2 or TP3), you can block any further trades for the rest of the ORB session to avoid overtrading.

Inner-range logic after TP1:

Prevents immediate re-entry in the same direction after a BE exit from TP1.

Waits for price to return into a defined inner range around the OR midline, filtering out random noise.

📊 On-Chart HUD / Stats (AR & EN)

The built-in info panel shows in real time:

Session status:

✅ Trading enabled

🚫 Trading disabled until a new ORB

⏳ Waiting for two bars back inside the range

Current price regime (Above ORH / Below ORL / Inside OR).

Entry price, stop loss, TP1, TP2.

Total trades, losing trades, and win rate.

Counts of TP1 / TP2 / TP3 hits.

Reported capital, current position size (lots).

Current trade P/L and total net P/L in dollars.

🔔 Full Alert System (Ready for Webhooks/Bots)

The indicator generates per-bar event flags that feed into alertcondition() so you can build any alert setup you want (pop-up, email, SMS, webhook, bot, EA, etc.).

Available alerts:

Buy Entry: JFX_ORB_BUY_ENTRY

Sell Entry: JFX_ORB_SELL_ENTRY

Stop Loss Hit: JFX_ORB_SL_HIT

TP1 Hit: JFX_ORB_TP1

TP2 Hit: JFX_ORB_TP2

TP3 Hit: JFX_ORB_TP3

Break-Even Exit: JFX_ORB_BE_EXIT

Simply create alerts in TradingView based on these conditions and messages, or plug them into your automation via webhooks.

Who Is JFX Smart ORB For?

Day traders and scalpers who like structured ORB strategies instead of random entries.

Traders who want clear, rule-based entries, well-defined stops and multi-target exits.

Anyone looking to combine ORB + position management + Martingale logic + Alerts in a single, professional tool.

Disclaimer:

This indicator is a professional analysis and trade-management tool, not a guarantee of profit.

Always test on demo first and adapt the position sizing and Martingale behavior to your own risk management and trading plan.

ICT Fair Value Gap (FVG) Detector │ Auto-Mitigated │ 2025Accurate ICT / Smart Money Concepts Fair Value Gap (FVG) detector

Features:

• Detects both Bullish (-FVG) and Bearish (+FVG) using strict 3-candle rule

• Boxes automatically extend right until price mitigates them

• Boxes auto-delete when price closes inside the gap (true mitigation)

• No repainting – 100% reliable

• Clean, lightweight, and works on all markets & timeframes

• Fully customizable colors and transparency

How to use:

– Bullish FVG (green) = potential support / buy zone in uptrend

– Bearish FVG (red) = potential resistance / sell zone in downtrend

Exactly matches The Inner Circle Trader (ICT) methodology used by thousands of SMC traders in 2024–2025.

Enjoy and trade safe!

Titan EMA Liquidity [Stansbooth]

🔥 Precision EMA + FVG Liquidity Sweep System

Advanced Buy/Sell Signal Engine for High-Probability Trade Entries

Unlock a new level of precision with this all-in-one market structure indicator built for traders who demand accuracy, clarity, and confidence.

This tool combines EMA trend filtration , Fair Value Gap (FVG) detection , and liquidity sweep analysis to deliver powerful buy and sell signals that align with institutional price behavior.

✅ Key Features

Dynamic EMA Trend Filter:

Identifies true trend direction and filters out low-quality trades. Signals only trigger when momentum aligns with higher-timeframe directional bias.

Smart FVG Detection:

Automatically highlights bullish and bearish Fair Value Gaps, helping you spot premium/discount zones where institutional traders seek entries.

Liquidity Sweep Identification:

Detects equal highs/lows, stop hunts, and engineered liquidity grabs—then confirms reversals when price sweeps liquidity and returns inside structure.

High-Accuracy Signal Engine:

Buy/Sell alerts trigger only when three layers agree:

1. EMA trend alignment

2. FVG confirmation

3. Liquidity sweep completion

This results in cleaner signals , fewer false entries, and strong trend continuation setups.

Optimized for All Market Conditions:

Works for scalping, day trading, and swing trading across Forex, Crypto, Indices, and Stocks.

What This Indicator Helps You Achieve

Capture smart-money style entries with reduced drawdown

Enter after liquidity grabs instead of before them

Avoid chop with EMA-filtered market direction

Spot precision premium/discount zones using automatic FVG mapping

Obtain high-confidence Buy/Sell signals based on institutional concept

Why Traders Love It

This system isn’t just another signal generator—it’s a market-structure aware model that reads the chart the same way professional traders do.

Every signal is based on probability stacking , giving you the clarity and confidence to take the best setups while ignoring noise.

ICT Smart Money Trading Suite PRO [SwissAlgo]ICT SMC Trading Suite Pro

Structure Detection. Imbalance Tracking. Trade Planning. Contextual Alerts.

Why This Integrated System Was Built

The ICT/SMC methodology requires tracking multiple analytical components simultaneously - a process prone to manual errors, time inefficiency, and visual clutter . This indicator consolidates these elements into a single, unified system , providing rules-based validation for experienced ICT traders who may struggle with execution speed, consistency, and manual calculations.

-----------------------------------------------------------------

What This Indicator Does

ICT/SMC methodology involves tracking multiple analytical components simultaneously. This indicator consolidates them into a single system.

Common challenges when applying ICT manually:

1️⃣ Structure Identification

Determining which pivots qualify as external (macro) structure versus internal (micro) structure requires consistent rules. Inconsistent structure identification affects the detection of the relevant trading range for entries , Change of Character (ChoCH) , and Break of Structure (BoS) . Accurate structure identification is paramount ; a faulty reading invalidates the entire ICT thesis for the current swing. While no automated system can replace human judgment, the indicator provides you with a rules-based starting point for structural analysis. The key goal is to help you find and map the relevant structural leg to focus on.

2️⃣ Chart Organization

Drawing Fibonacci retracements, Fair Value Gaps, Order Blocks, and other imbalances manually creates visual complexity that can obscure the analysis. The indicator addresses this by striving to show all imbalances in a consistent, unified, and understandable visual way , using color coding and z-order layering to maintain clarity even when multiple components are active.

3️⃣ Imbalance Tracking

ICT methodology requires monitoring a vast array of institutional footprints : Fair Value Gaps (FVG), Order Blocks (OB), Breaker Blocks (BB), Liquidity Pools (LP), Volume Imbalances, Wick Imbalances, and Kill Zone ranges. Tracking all these simultaneously and manually monitoring their mitigation status is highly time-intensive and prone to oversight . The indicator constantly scans and tracks all key imbalance types for you, automatically updating their status and creating a dynamic, real-time visual heatmap of unmitigated institutional inefficiency.

4️⃣ Trade Calculation

Determining structure-based Stop Loss (SL) placement, calculating multiple Take Profit (TP) levels with accurate position-sizing splits, and computing the final blended Risk-to-Reward (R:R) ratio involves multiple time-sensitive, manual calculations per setup . The indicator automates this entire trade calculation process for you, instantly providing the necessary pricing (entry, SL, TP), sizing, and performance projections, and mitigating the risk of execution error .

5️⃣ Condition Monitoring

ICT setups often require specific technical conditions to align: price reaching discount Fibonacci levels (0.618-0.882 for shorts, 0.118-0.382 for longs), EMA crossovers confirming momentum, or structural shifts (ChoCH/BoS). Identifying these moments requires continuous chart observation across multiple assets and timeframes.

This indicator includes an alert system that monitors these technical conditions and sends notifications when they occur (real-time). The alert system is designed to minimize spam. This allows traders to review potential setups on demand rather than through continuous observation - particularly relevant for those monitoring multiple instruments or trading sessions outside their local timezone.

-----------------------------------------------------------------

Intended Use

This indicator is designed for traders who:

♦ Apply ICT/SMC methodology - Familiarity with concepts such as Fair Value Gaps, Order Blocks, Liquidity Pools, market structure, and discount/premium zones is assumed. The indicator does not teach these concepts but provides tools to apply them.

♦ Trade on intraday to swing timeframes - The structure detection and Fibonacci zone mapping work across multiple timeframes. Recommended primary timeframe: 1H (adjustable based on trading approach).

♦ Prefer systematic entry planning - The trade calculation feature computes stop loss, take profit levels, and risk-to-reward ratios based on structure and Fibonacci positioning. Suitable for traders who use defined entry criteria.

♦ Monitor multiple instruments or sessions - The alert functionality notifies when specific technical conditions occur (discount zone entries, EMA crossovers, structure changes), reducing the need for continuous manual monitoring.

♦ Use trade execution platforms - The trade summary table displays pre-formatted values (entry, SL, TP levels with quantity splits) that can be manually input into trading platforms or bot services like 3Commas.

-----------------------------------------------------------------

How To Use

Step 1: Structure Analysis

The indicator automatically detects external and internal market structure using pivot analysis. Structure lines are color-coded: red for bearish structure, green for bullish. External pivots are marked with larger triangles, internal pivots with smaller markers. The pivot length parameters (default: 20/20) can be adjusted in settings to align with your structural analysis approach and the asset you are analyzing.

Step 2: Define Your Trading Zone

Use the "Start Swing" and "End Swing" date inputs to mark the beginning and end of the (external) structural leg you wish to analyze. The indicator calculates Fibonacci retracement levels based on these points and color-codes the zones:

* Green zones: Discount area (0.618-0.882 for bearish / 0.118-0.382 for bullish)

* Yellow zones: Premium area (0.786-1.0 for bearish / 0.0-0.214 for bullish)

* Red zones: Extension area beyond structure (potential fake-out zones)

Step 3: Review Imbalances

The indicator identifies and displays multiple imbalance types:

🔥 Volume imbalances (from displacement candles based on PVSRA methodology)

🔥 Fair Value Gaps (FVG)

🔥 Order Blocks (OB) and Breaker Blocks (BB)

🔥 Liquidity Pools (LP) at equal highs/lows

🔥 Wick imbalances (exceptional wick formations)

🔥 Kill Zone liquidity from specific trading sessions (Asian, London, NY AM)

Volume Imbalances

Fair Value Gaps

Order Blocks

Liquidity Pools

Wick Imbalances

Kill Zone Imbalances

According to ICT methodology, imbalances act as price magnets - areas where price tends to return for mitigation. When multiple imbalances overlap at the same price level, this creates a confluence zone with a higher probability of price reaction .

Imbalances are displayed as gray boxes , creating a visual heatmap of institutional inefficiencies. When imbalances overlap, the zones appear darker due to layering, and labels combine to show confluence (e.g., "FVG + OB" or "Vol + LP").

Heatmap of Imbalances

User can view each type alone, or all together (heatmap)

Each imbalance type is tracked until mitigated by price according to ICT principles and can be toggled on/off independently in settings.

Step 4: Reference Levels & Sessions

The indicator displays additional reference data:

🔥 Daily Pivot Points (PP, R1-R3, S1-S3) calculated from previous day

🔥Average Daily Range (ADR) projected from the current day's extremes

🔥 Daily OHLC levels: Today's Open (DO), Previous Day High (PDH), Previous Day Low (PDL)

🔥Session backgrounds (optional): Color-coded boxes for Asian, London, NY AM, and NY PM sessions

Sessions

While these are not ICT-specific imbalances, they represent widely-watched price levels that often attract institutional activity and can act as additional reference points for support, resistance, and liquidity targeting.

All reference levels can be toggled independently in settings.

Step 5: Momentum Reference

EMA 14 and EMA 21 lines are displayed for momentum analysis. When EMA 14 enters discount zones and crosses EMA 21, a triangle marker appears on the chart. This indicates a potential alignment of structure and momentum conditions.

Step 6: Trade Planning

Input your intended entry price in the "Entry Price" field along with your margin and leverage parameters. The indicator automatically calculates all trade parameters:

* Stop loss level (based on Fibonacci structure - typically at 1.118 extension)

* Three take profit levels (TP1, TP2, TP3) with position quantity splits

* Risk-to-reward ratio (blended across all three targets)

* Projected profit/loss values in both dollars and percentage

All calculated values are displayed both visually on the chart (as horizontal lines with labels) and in a formatted Trade Summary table. The table organizes the information for quick reference: entry details, take profit levels with quantities, stop loss parameters, and performance projections.

This pre-calculated data can be manually copied into trading platforms or bot services (such as 3Commas Smart Trades) without requiring additional calculations.

Step 7: Alert Configuration

Create alerts using TradingView's alert system (select "Any alert() function call"). The indicator sends notifications when:

* Price reaches specific discount Fibonacci levels (0.618, 0.786, 0.882 for shorts / 0.382, 0.214, 0.118 for longs)

* EMA 14/21 crossovers occur within discount zones

* Change of Character (ChoCH) is detected

* Break of Structure (BoS) is detected

Note: Alerts require active TradingView alert functionality. Update alerts when changing your trading zone parameters.

-----------------------------------------------------------------

Key Features

Structure & Zone Analysis

* Automated structure detection with external/internal pivots and zig-zag visualization

* Fibonacci retracement mapping with color-coded discount/premium zones

* Visual zone classification: Green (optimal discount), Yellow (premium), Red (fake-out risk)

ICT Imbalances Heatmap

* Volume imbalances (PVSRA displacement candles)

* Fair Value Gaps (FVG)

* Order Blocks (OB) and Breaker Blocks (BB)

* Liquidity Pools (LP) at equal highs/lows

* Wick imbalances (exceptional wick formations)

* Kill Zone liquidity (Asian, London, NY AM sessions)

* Confluence detection with combined labels and visual layering

Reference Levels

* Daily Pivot Points (PP, R1-R3, S1-S3)

* Average Daily Range (ADR) projections

* Daily OHLC levels (DO, PDH, PDL)

* Session backgrounds for kill zones

Trade Planning Tools

* Automated stop loss calculation based on Fibonacci structure

* Three-tier take profit system with position quantity splits

* Risk-to-reward ratio calculation (blended across all targets)

* P&L projections in dollars and percentages

* Trade Summary table formatted for manual platform entry

Momentum & Signals

* EMA 14/21 overlay for momentum analysis

* Visual crossover markers (triangles) in discount zones

* Change of Character (ChoCH) detection and labels

* Break of Structure (BoS) detection and labels

Chart Enhancements

* Higher timeframe candle overlay (5m to Monthly)

* PVSRA candle coloring (volume-based)

* Symbol legend for quick reference

* Customizable visual elements (toggle all components independently)

Alert System

* Discount zone entry notifications (Fibonacci level monitoring)

* EMA crossover signals within discount zones

* Structure change alerts (ChoCH and BoS)

* Configurable via TradingView alert functionality

Alert Functionality

The indicator includes an alert system that monitors technical conditions continuously.

When configured, alerts notify users when specific events occur:

❗ Discount Zone Monitoring

When EMA 14 crosses into key Fibonacci levels (0.618, 0.786, 0.882 for bearish structure / 0.382, 0.214, 0.118 for bullish structure), an alert is triggered. Example: Trading BTC and ETH simultaneously - instead of monitoring both charts for zone entries, alerts notify when either asset reaches the specified level.

❗ Momentum Alignment

When EMA 14 crosses EMA 21 within discount zones, an alert is sent. Example: Monitoring setups across multiple timeframes (1H, 4H, Daily) - alerts indicate when momentum conditions align on any timeframe being tracked.

❗ Structure Changes

Change of Character (ChoCH) and Break of Structure (BoS) events trigger alerts. Example: Trading during the Asian session while located in a different timezone - alerts notify of structure changes occurring outside active monitoring hours.

Configuration

Alerts are set up through TradingView's native alert system. Select "Any alert() function call" when creating the alert.

⚠️ Note: Alert parameters are captured at creation time, so alerts must be updated when changing trading zone settings (Start/End Swing dates) or any other parameter.

How to Create Alerts

Step 1: Open Alert Creation

Click the "Alert" button (clock icon) in the top toolbar of TradingView, or right-click on the chart and select "Add Alert."

Step 2: Configure Alert Condition

* In the alert dialog, set the Condition dropdown to select this indicator

* Set the alert type to ⚠️ " Any alert() function call "

* This configuration allows the indicator to trigger alerts based on its internal logic

Step 3: Set Alert Timing

* Timeframe: Same as chart

* Expiration: Choose "Open-ended (when triggered)" to keep the alert active until conditions occur

* Message tab: choose a name for the alert

Step 4: Notification Settings

Configure how you want to receive notifications:

* Popup within TradingView

* Email notification

* Mobile app push notification (requires TradingView mobile app)

Step 5: Create

Important Notes:

* Alert parameters are captured at creation time . If you change your trading zone (Start/End Swing dates) or entry price, delete the old alert and create a new one .

* One alert per chart: Create separate alerts for each instrument and timeframe you're monitoring.

* TradingView alert limits apply based on your TradingView subscription tier.

What Triggers Alerts: This indicator sends alerts for four key event types:

1. Discount Zone Entry - EMA 14 crossing key Fibonacci levels

2. Momentum Crossover - EMA 14/21 crossovers within discount zones

3. Change of Character (ChoCH) - Structure reversal detected

4. Break of Structure (BoS) - Trend continuation confirmed

All four conditions are monitored by a single alert configuration .

-----------------------------------------------------------------

Recommended Settings

* Timeframe : 1H works well for most assets

* Theme : Dark mode recommended

* Structural Pivots : Default 20/20 captures reasonable structure; adjust to match your analysis

-----------------------------------------------------------------

Chart Elements Guide

♦ Structure Visualization

Zig-zag lines

Automated structure detection - green lines indicate bullish structure, red lines indicate bearish structure. Thick lines represent external structure , thin faded lines show internal structure .

Triangle markers

Large triangles mark external pivots (swing highs/lows), small triangles mark internal pivots.

Fibonacci Zones

* Green zones: Discount area - potential entry zones (0.618-0.882 for shorts / 0.118-0.382 for longs)

* Yellow zones: Premium area - higher extension zones (0.786-1.0 for shorts / 0.0-0.214 for longs)

* Red zones: Fake-out risk area - price beyond structural extremes (above 1.0 for shorts / below 0.0 for longs)

* White dashed lines: Individual Fibonacci levels (1.0, 0.882, 0.786, 0.618, 0.5, 0.382, 0.214, 0.118, 0.0)

♦ Imbalance Heatmap

Gray boxes with dotted midlines

Unmitigated imbalances create a visual heatmap. Overlapping imbalances appear darker due to layering.

Combined labels

When multiple imbalances overlap, labels show confluence (e.g., "FVG + OB", "Vol + LP + Wick")

Types displayed : Vol (Volume), FVG (Fair Value Gap), OB (Order Block), BB (Breaker Block), LP (Liquidity Pool), Wick, KZ (Kill Zone)

♦ Momentum Indicators

* Red line: EMA 14

* Yellow line: EMA 21

* Small triangles on price: Crossover signals - red triangle (bearish crossover), green triangle (bullish crossover) when occurring within discount zones

♦ Structure Change Markers

* Labels with checkmarks/crosses: ChoCH (Change of Character) and BoS (Break of Structure) events (Green label with ✓: Bullish ChoCH or BoS, Red label with ✗: Bearish ChoCH or BoS)

♦ Trade Planning Lines (when entry price is set)

* Blue horizontal line: Entry price

* Green dashed lines: TP1 and TP2

* Green solid line: TP3 (final target)

* Red horizontal line: Stop Loss level

TP levels and SL are calculated based on the structure range, entry price, and mapped trading zone, and aim to achieve a minimum risk: reward ratio of 1:1.5 (R:R)

♦ Colored background zones:

Green shading between entry and TP3 (profit zone), red shading between entry and SL (loss zone)

♦ Reference Levels

* Orange dotted lines with labels: Daily Pivot Points (PP, R1-R3, S1-S3)

* Purple dotted lines with labels: ADR High and ADR Low projections

* Cyan dotted lines with labels: DO (Daily Open), PDH (Previous Day High), PDL (Previous Day Low)

♦ Session Backgrounds (optional)

* Yellow shaded box: Asian session (19:00-00:00 NY time)

* Blue shaded box: London session (02:00-05:00 NY time)

* Green shaded box: NY AM session (09:30-11:00 NY time)

* Orange shaded box: NY PM session (13:30-16:00 NY time)

♦ Trade Summary Table (top-right corner)

Displays a complete trade plan with sections:

* Sanity Check: Plan validation status

* Setup: Trade type, leverage, entry price, position size

* Take Profit: TP1, TP2, TP3 with prices, percentages, and quantity splits

* Stop Loss: SL price and type

* Performance: Potential profit/loss, ROI, and risk-to-reward ratio

♦ HTF Candle Overlay (optional, displayed to the right of the current price)