Liquidity Zones [ActiveQuants]The Liquidity Zones indicator detects price areas where high trading volume coincides with below-average volatility , critical zones where large players often accumulate or distribute positions. Ideal for spotting potential reversal points and strategic liquidity pools.

Core Detection Formula

Liquidity Zone = (Volume > SMA(Volume, Length) × Multiplier) AND (Short-Term Volatility < 0.5 × Average Volatility)

Volume Surge Detection

Compares current volume to its SMA (user-defined length).

Multiplies threshold with " Volume Threshold Multiplier " parameter.

Volatility Contraction Filter

Calculates 5-bar volatility (standard deviation of closes).

Compares to average volatility over " Price Std. Dev. Length " period.

Requires short-term volatility < 50% of average.

█ KEY FEATURES

Merging Consecutive Zones

If the " Merge Consecutive Zones " option is enabled, the indicator will:

Calculate the number of consecutive bars that meet the liquidity zone criteria.

Sum the volume of these consecutive bars.

Display only the most recent label for the merged zone (previous labels in the sequence are removed).

Displays volume in either

Raw units (" Units ").

Dollar-equivalent (" Currency Value ") using closing price.

Alerts

An alert condition is built into the script. Traders can selectively enable alerts via TradingView’s alert system. Whenever a liquidity zone is detected, an alert is triggered with the message: " High-volume and low-volatility zone detected! ".

█ USER INPUTS

- Liquidity Zones Color

Sets the background color for liquidity zones.

Default: Orange (with 70 transparency).

- Volume SMA Length

Determines the number of bars over which the volume simple moving average is calculated.

Default: 20 bars.

- Volume Threshold Multiplier

Multiplies the volume SMA to establish a threshold. A bar’s volume must exceed this product to be considered high volume.

Default: 2.0.

- Price Std. Dev. Length

The period used to calculate the standard deviation of the closing prices. This is the basis for measuring average volatility.

Default: 14 bars.

- Zone Volume

A toggle to display a label with the volume value on liquidity zones.

Allows you to choose how the volume is displayed: Units (shows raw volume) or Currency Value (multiplies volume by the current closing price).

Allows you to choose the font size of the volume label.

- Merge Consecutive Zones

When enabled, volumes from consecutive liquidity zones are summed into a single total, and only the most recent label is displayed (previous labels in the sequence are removed).

Default: Enabled.

- Show Last

Specifies the number of bars back that the indicator will evaluate and plot liquidity zones.

Default: 500 bars.

- Timeframe

Analysis period.

Default: Chart.

█ CONCLUSION

The Liquidity Zones indicator is a powerful tool for traders seeking to identify key areas on the chart where liquidity is concentrated, characterized by high volume and low volatility . With customizable settings for volume analysis and volatility measurement , this indicator can be integrated into a wide range of trading strategies. It not only highlights these zones visually but also provides volume data labels and alerts for timely decision-making.

█ IMPORTANT NOTES

⚠ Volume and Volatility Settings: Adjust the Volume SMA Length , Volume Threshold Multiplier , and Price Std. Dev. Length to suit the typical trading volume and volatility of the asset you are analyzing.

⚠ Confirmed Bars Only: Signals are generated only on confirmed bars. This minimizes false signals due to intra-bar noise and also prevents indicator repainting .

⚠ Risk Management: Liquidity zones may signal areas of potential accumulation or distribution, but they should be used in conjunction with other technical analysis tools (e.g., support/resistance levels, trendlines, or momentum indicators). Trading involves risk, and it is recommended to combine this indicator with proper risk management techniques.

█ RISK DISCLAIMER

Trading involves substantial risk of loss. Liquidity zones indicate potential interest areas but don't guarantee price reactions. Always confirm with additional analysis and proper risk management. Past performance is not indicative of future results.

📈 Happy trading! 🚀

Cerca negli script per "trendline"

Market Structure MTF Trend [Pt]█ Author's Notes

There are numerous market structure indicators in the TradingView library, each offering a unique approach to identifying price action shifts. Market Structure MTF Trend was created with simplicity and flexibility in mind—providing a highly customizable multi-timeframe setup, visually clear trendlines, and straightforward labeling. This combination helps both new and experienced traders easily spot and interpret market structure changes.

█ Overview

Market Structure MTF Trend is a powerful yet user-friendly indicator designed to identify and visualize key turning points in price action. It focuses on two core concepts:

Change of Character (CHoCH): A momentary shift in the market’s behavior, signaling that the current price movement may be losing momentum and could soon reverse.

Break of Structure (BoS): A more definitive event confirming a new price pattern, where the market establishes a fresh trend direction by surpassing previous swing highs or lows.

By combining these signals across up to four different timeframes, even traders unfamiliar with market structure can quickly learn to spot and validate potential trend reversals or continuations.

█ Key Features

Multi-Timeframe Analysis: Monitors CHoCH and BoS events simultaneously on multiple intervals (e.g., 15m, 30m, 60m, 240m), providing a clear, layered understanding of market dynamics.

Straightforward Visual Cues: Labels are placed directly on the chart at swing highs and lows, while colored bars at the bottom give an instant snapshot of whether each timeframe is bullish or bearish.

Configurable Timeframes & Pivot Strength: Easily set up the desired intervals and adjust pivot strength to tune how sensitive the indicator is to minor price fluctuations.

Color-Coded Signals: Different colors help you distinguish between potential early reversals (CHoCH) and confirmed shifts (BoS), ensuring each signal’s importance is immediately clear.

█ Usage & Benefits

Learn Market Structure Basics: For those new to swing highs/lows, CHoCH, and BoS, the script’s on-chart labels and dynamic bar coloring provide a practical, visual way to grasp these concepts.

Spot Reversals Early: CHoCH alerts you to possible shifts in momentum, allowing you to anticipate trend changes before they fully develop.

Confirm Trend Breaks: BoS events confirm that the market has established a new directional bias, reinforcing higher‐probability entry or exit points.

Reduce Noise & Stay Focused: The multi-timeframe setup ensures you won’t overlook larger trends or get lost in smaller fluctuations.

Streamline Decision-Making: Color-coded bars let you gauge overall market sentiment at a glance—ideal for quickly validating trades without juggling multiple charts.

Market Structure MTF Trend is perfect for traders who want to learn or refine their understanding of price action. By integrating multiple timeframes into a single, cohesive interface, this tool highlights both subtle shifts and confirmed breaks in market structure, empowering you to trade with greater insight and confidence.

Sweep Engulf 2 Candle🔍 Overview:

This script identifies Bullish Engulfing and Bearish Engulfing candlestick patterns on the chart. These formations are widely used in technical analysis to spot potential reversals in price action. The indicator helps traders quickly identify these patterns by marking them directly on the chart with small arrows.

📌 Features:

✅ Bullish Engulfing & Bearish Engulfing Detection

✅ Customizable Display Options (Enable/Disable Bullish or Bearish signals)

✅ Real-Time Alerts (Receive notifications when a pattern is formed)

✅ Optimized Marker Size (Smaller icons for better chart visibility)

📊 How It Works:

1. Bullish Engulfing Condition:

The second candle's low is lower than the first candle's low.

The second candle's close is higher than the first candle's open (if the first candle is bearish) OR higher than the first candle's close (if the first candle is bullish).

2. Bearish Engulfing Condition:

The second candle's high is higher than the first candle's high.

The second candle's close is lower than the first candle's close (if the first candle is bearish) OR lower than the first candle's open (if the first candle is bullish).

⚙️ How to Use:

Add the script to your TradingView chart.

Adjust settings to enable/disable Bullish or Bearish Engulfing patterns.

Enable alerts to receive real-time notifications when a pattern is detected.

Use this indicator to support your technical analysis and trade decisions.

📌 Notes:

This indicator is best used in combination with other technical analysis tools like support & resistance levels, trendlines, or volume analysis.

It works on all timeframes and asset

Demand, Supply and Channel by BULL┃NET

The B | N DESC (Demand, Supply, and Channel by BULL / NET)

Indicator helps traders identify demand and supply lines. Breakouts are detected, and potential targets are calculated. Additionally, channels are automatically detected.

⚠️ Disclaimer – Please Read Before Using ⚠️

Concepts

Trend, demand, and supply lines are fundamental concepts in trading to identify a trend and detect a potential trend change. However, there’s a significant issue: if you show a chart to 10 traders and ask them to draw trend, demand, and supply lines, you’ll likely get 10 different results. This is where B | N DESC comes into play. The indicator defines demand and supply lines objectively using pivot points of different levels.

A pivot point is a high or low on the chart surrounded by bars that form lower highs or higher lows. The number of bars to the left and right defines the pivot length or level. Supply lines connect pivot highs top-down, and demand lines connect pivot lows bottom-up. Unlike traditional trendlines, which are drawn from left to right and require three anchor points, supply and demand lines are drawn from right to left.

Features

Supply Line Options

These settings control how supply lines and channels are calculated and drawn on the chart. You can display up to three supply lines.

- 1st, 2nd, and 3rd Supply Line : By default, two supply lines are active. Each line can be enabled or disabled individually.

- Channel: Determines whether channels are displayed.

- Confirm : If enabled, the channel will not be shown until confirmed by the price.

- Fill : When enabled, the channel will be filled with the chosen color once confirmed by the price.

- Level : You can define pivot points for any level between 1 and 100. Default values are 3, 5, and 15.

- Color, Style, Width: These settings customize the appearance of the supply lines.

Demand Line Options

Similar to the supply lines, these settings control how demand lines and channels are calculated and displayed on the chart. You can display up to three demand lines.

- 1st, 2nd, and 3rd Demand Line : By default, two demand lines are active.

- Channel and Confirm : Functions similarly to supply lines.

- Level: Levels between 1 and 100 are available, with default values of 3, 5, and 15.

- Color, Style, Width : These settings allow you to adjust the appearance of the demand lines.

Level Label Options

When a new demand or supply line is drawn, a small label appears at the x2 coordinate of the line. The label shows the height of the extreme point and the direction (up or down) along with the line type (D = Demand, S = Supply) and the selected pivot level.

Breakout Label Options

- Show in Timeframe : Breakout and target labels are shown by default in timeframes above 30 minutes. In shorter timeframes, pivot points can change rapidly, causing the labels to cover the bars.

- Breakout : The breakout label contains the breakout price, direction, pivot level, and breakout attempts.

- Target : A label that displays the target price, which is linked to the breakout point on the supply or demand line.

Additional Options

- Burned Line : Supply and demand lines remain active until new pivot points create a new line of the same level. After the 4th breakout, the line is marked as “burned” and will no longer be monitored for further breakouts.

- Spread : This feature allows you to account for your broker’s spread in the target calculation to avoid discrepancies.

-------------------------------------

Disclaimer BullNet: [ /i] The information provided in this document is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Any use of the content is at your own risk. No liability is assumed for any losses or damages resulting from reliance on this information. Trading financial instruments involves significant risks, including the potential loss of all invested capital. There is no guarantee of profits or specific outcomes. Please conduct your own research and consult a professional financial advisor if needed.

Disclaimer TradingView: According to the www.tradingview.com

Copyright: 2025-BULLNET - All rights reserved.

Roadmap:

Version 1.0 03.03.2025

Trend Vanguard StrategyHow to Use:

Trend Vanguard Strategy is a multi-feature Pine Script strategy designed to identify market pivots, draw dynamic support/resistance, and generate trade signals via ZigZag breakouts. Here’s how it works and how to use it:

ZigZag Detection & Pivot Points

The script locates significant swing highs and lows using configurable Depth, Deviation, and Backstep values.

It then connects these pivots with lines (ZigZag) to highlight directional changes and prints labels (“Buy,” “Sell,” etc.) at key turning points.

Support & Resistance Trendlines

Pivot highs and lows are used to draw dashed S/R lines in real-time.

When price crosses these lines, the script triggers a breakout signal (long or short).

EMA Overlays

Up to four EMAs (with customizable lengths and colors) can be overlaid on the chart for added trend confirmation.

Enable/disable each EMA independently via the settings.

Repaint Option

Turning on “Smooth Indicator Lines” (repaint) uses future data to refine past pivots.

This can make historical signals look cleaner but does not reflect true historical conditions.

Turning it off ensures signals remain fixed once they appear.

Strategy Entries & Exits

On each new ZigZag “Buy” or “Sell” signal, the script closes any open position and flips to the opposite side (if desired).

Works with the built-in TradingView Strategy engine for backtesting.

Additional Inputs (Placeholders)

Volume Filter and RSI Filter settings exist but are not fully implemented in the current code. Future versions may incorporate these filters more directly.

How to Use

Add to Chart: Click “Indicators” → “Invite-Only Scripts” (or “My Scripts”) and select “Trend Vanguard Strategy.”

Configure Settings:

Adjust ZigZag Depth, Deviation, and Backstep to fine-tune pivot sensitivity.

Enable or disable each EMA to see how it aligns with market trends.

Toggle “Smooth Indicator Lines” on or off depending on whether you want repainting.

Backtest and Forward Test:

Use TradingView’s “Strategy Tester” tab to review hypothetical performance.

Remember that repainting can alter past signals if enabled.

Monitor Live:

Watch for breakout triangles or ZigZag labels to identify potential reversal or breakout trades in real time.

Disclaimer: This script is purely educational and not financial advice. Always combine it with sound risk management and thorough analysis. Enjoy exploring the script, and feel free to experiment with the different settings to match your trading style!

MA Cross Multi Alert KrafturMA Cross Multi Alert Kraftur

Description

The "MA Cross Multi Alert Kraftur" indicator is a versatile tool designed to help traders identify potential buy and sell opportunities based on the crossings of multiple moving averages (MAs). Unlike traditional MA crossover indicators that focus on a single pair of averages, this script offers three distinct crossover levels (e.g., 21/50, 50/90, 50/200) for greater flexibility and precision. It overlays signals directly on the price chart and delivers real-time alerts when crossings occur, making it an excellent choice for traders seeking to pinpoint entry and exit points across various market conditions.

Key Features

Multi-Level Crossovers: Tracks crossings between configurable moving averages (e.g., 21 crossing 50, 50 crossing 90, 50 crossing 200) to detect varying trend strengths and reversals.

Visual Signals: Buy signals are displayed as upward triangles below the bars, and sell signals as downward triangles above the bars, each color-coded for quick recognition.

Real-Time Alerts: Triggers alerts once per bar when a crossover occurs, with a filter to avoid repetitive notifications during minor fluctuations.

Customizable: Adjustable MA lengths, timeframe, and signal colors allow tailoring to individual trading preferences and strategies.

Recommended Usage

This indicator shines as a scanning tool for identifying trade setups across multiple assets. Apply it to your watchlist of stocks, forex pairs, or cryptocurrencies, and set up alerts to catch crossover signals in real time. It performs exceptionally well in trending or consolidating markets and can be paired with additional tools (e.g., trendlines, RSI, or volume analysis) to validate signals and boost reliability. Ideal for multi-timeframe traders or those managing diverse portfolios.

How to Use

Add the indicator to your chart.

Adjust the MA lengths (e.g., 21, 50, 90, 200), timeframe, and signal colors to align with your trading approach.

Configure alerts for the indicator and apply them to your asset watchlist.

Watch for buy (upward triangles) and sell (downward triangles) signals on the chart, or rely on alert notifications for timely updates.

Perfect for day traders, swing traders, or anyone aiming to streamline signal detection and automate their workflow!

Three Bar Reversal Pattern [ActiveQuants]This indicator identifies bullish and bearish three-bar reversal patterns , offering traders a visual tool to spot potential trend reversals. By analyzing consecutive candlesticks, volume trends, and candlestick morphology, it highlights signals while filtering out false patterns. Ideal for traders using price action strategies, it simplifies pattern recognition and enhances decision-making with customizable parameters.

█ KEY FEATURES

Pattern Detection Logic :

Bullish Reversals : Detects two consecutive bearish candles followed by a bullish candle that closes above the open of the first bearish candle .

Bearish Reversals : Identifies two consecutive bullish candles followed by a bearish candle that closes below the open of the first bullish candle .

Volume Confirmation :

Filters signals using a Volume SMA (user-defined length) to ensure reversals occur with above-average volume, adding validity to the pattern.

Candlestick Filtering :

Shooting Star Filter : Discards bullish patterns if the third candle is a Shooting Star (body confined to the lower portion of the candle’s range, adjustable via Shooting Star Body Limit ).

Hammer Filter : Discards bearish patterns if the third candle is a Hammer (body confined to the upper portion of the candle’s range, adjustable via Hammer Body Limit ).

Customizable Display :

Toggle visibility of bullish/bearish patterns and customize their colors.

Adjust the Show Last parameter to limit plotted labels to recent bars.

Alerts Integration :

Separate Bullish/Bearish Alerts : Generate independent alerts for bullish and bearish patterns. Traders can selectively enable one or both alerts via TradingView’s alert system.

Real-time notifications ensure you never miss a potential reversal signal.

█ CONCLUSION

The Three Bar Reversal Pattern Indicator streamlines the identification of reversal setups by combining candlestick patterns, volume analysis, and customizable filters. Its focus on price action dynamics makes it invaluable for traders seeking to capitalize on trend exhaustion or market sentiment shifts.

█ IMPORTANT NOTES

⚠ Use with Confluence : Reversal signals should be validated with additional tools like support/resistance levels, trendlines, or momentum oscillators.

⚠ Adapt Parameters : Adjust Volume SMA Length , Show Last , and body limits ( Shooting Star Body Limit and Hammer Body Limit ) to suit your timeframe and asset volatility.

█ RISK DISCLAIMER

Trading involves significant risk, and you may lose capital. Past performance is not indicative of future results. This tool provides informational signals only and does not constitute financial advice. Use it at your own risk and consult a qualified financial professional before making trading decisions.

Incorporate this indicator into your strategy to refine reversal entries, manage risk, and align with market momentum.

📈 Happy trading! 🚀

Trading Sessions Highs/Lows | InvrsROBINHOODTrading Sessions Highs/Lows | InvrsROBINHOOD

🚀 A powerful indicator for tracking key trading sessions and the highs and lows of each session!

📌 Description

The Trading Sessions Highs/Lows indicator visually marks the most critical trading sessions—Asia, London, and New York—using small colored dots at the bottom of the candle. It also tracks and plots the highs and lows of each session, along with the Daily Open and Weekly Open levels.

This tool is designed to help traders identify session-based liquidity zones, price reactions, and potential trade setups with minimal chart clutter.

Key Features:

✅ Session markers (Asia, London, NY AM, NY Lunch, NY PM) plotted as small dots

✅ Plots session highs and lows for market structure insights

✅ Daily Open line for intraday reference

✅ Weekly Open line for higher timeframe bias

✅ Alerts for session high/low breaks to capture momentum shifts

✅ User-defined UTC offset for global traders

✅ Customizable session colors for personal preference

📖 How to Use the Indicator

1️⃣ Understanding the Sessions

Asia Session (Yellow Dot) → Marks liquidity buildup & pre-London moves

London Session (Blue Dot) → Strong volatility, breakout opportunities

New York AM Session (Green Dot) → Major trends & institutional participation

New York Lunch (Red Dot) → Low volume, ranging market

New York PM Session (Dark Green Dot) → End-of-day movements & reversals

2️⃣ Session Highs & Lows for Market Structure

Session Highs can act as resistance or breakout points.

Session Lows can act as support or stop-hunt zones.

Break of a session high/low with volume may indicate continuation or reversal.

3️⃣ Using the Daily & Weekly Open

The Daily Open (Black Line) helps gauge the intraday trend.

Above Daily Open → Bearish Bias

Below Daily Open → Bullish Bias

The Weekly Open (Red Line) sets the higher timeframe directional bias.

4️⃣ Alerts for Breakouts

The indicator will trigger alerts when price breaks session highs or lows.

Useful for setting stop-losses, breakout trades, and risk management.

💡 Why This Indicator is Important for Beginners

1️⃣ Avoids Overtrading:

Many beginners trade in low-volume periods (NY Lunch, Asia session) and get stuck in choppy price action.

This indicator highlights when volatility is high so traders focus on better opportunities.

2️⃣ Session-Based Liquidity Traps:

Market makers often run stops at session highs/lows before reversing.

Watching session breaks prevents traders from falling into liquidity grabs.

3️⃣ Reduces Emotional Trading:

If price is above the Daily Open, a beginner shouldn’t look for shorts.

If price is below a key session low, it may signal a fake breakout.

4️⃣ Aligns with Institutional Trading:

Smart money traders use session highs/lows to set stop hunts & reversals.

Beginners can use this indicator to spot these zones before entering trades.

🛡️ How to Mitigate Risk with This Indicator

✅ Wait for Confirmations – Don’t trade blindly at session highs/lows. Look for wicks, rejections, or break/retests.

✅ Use Stop-Loss Above/Below Session Levels – If you’re going long, set SL below a session low. If short, set SL above a session high.

✅ Watch Volume & News Events – Breakouts without strong volume or news may be fake moves.

✅ Combine with Other Strategies – Use price action, trendlines, or EMAs with this indicator for higher probability trades.

✅ Use the Weekly Open for Trend Bias – If price stays below the Weekly Open, avoid bullish setups unless key support holds.

🎯 Who is This Indicator For?

📌 Beginners who need clear session-based trading levels.

📌 Day traders & scalpers looking to refine their intraday setups.

📌 Smart money traders using liquidity concepts.

📌 Swing traders tracking higher timeframe momentum shifts.

🚀 Final Thoughts

This indicator is an essential tool for traders who want to understand market structure, liquidity, and volatility cycles. Whether you’re trading forex, stocks, or crypto, it helps you stay on the right side of the market and avoid unnecessary risks.

🔹 Set it up, customize your colors, define your UTC offset, and start trading smarter today! 🏆📈

Trending Market Toolkit [LuxAlgo]The Trending Market Toolkit focuses exclusively on trending market structures and high-confluence, high-risk-to-reward entry models. It is designed to complement discretionary trading by offering different entry strategies based on market structure.

🔶 USAGE

In the chart above we can see how the tool detects several reversals, draws the broken trendlines, the reversal areas from which the tool starts looking for a trigger, and when it finally happens, a potential trade with risk and reward areas and the risk/reward ratio.

🔹 Detection Mode

Traders can choose between three different modes: trend only, reversal only, or both.

If both are active, reversals have priority over trends, so the tool will not detect a trend if a reversal is active.

In the chart above we can see all three modes.

🔹 Detection on Higher Timeframes

Traders can choose to identify structures on the chart timeframe or on a higher timeframe.

In the chart above, we have the SP500 futures on the 5m timeframe with different settings: chart timeframe, 30m, and 1H.

🔹 Risk And Targets

Depending on whether the high-risk/reward parameter is enabled, traders can choose between three different targets and two different stops.

The chart above shows how different choices affect the risk/reward ratio for the same potential trade on the Gold Futures 2m chart.

🔶 SETTINGS

Show: Traders can choose between Trends, Reversals or Both.

🔹 Structures

Swing Length: Number of candles to confirm a swing high or swing low. A higher number detects larger swings.

Custom Timeframe: Traders can make use of the current chart timeframe, or choose a custom timeframe.

Reversal Area Threshold: A higher number increases the reversal area.

🔹 Trades

Trade Trigger Length: Number of candles to confirm an internal high or internal low. A lower number detects smaller swings. It must be the same size or smaller than the swing length.

Target: Traders can choose between the default target (0) or two extended targets (0.27 or 0.618).

Risk to Reward Threshold: Set the minimum risk-to-reward ratio to detect trades. Use the 0 value to detect all trades.

High Risk to Reward: Enable/Disable the high risk to reward mode.

Volume Delta with Custom Colors and Min Delta Input### Indicator Description: **Volume Delta with Custom Colors and Min Delta Input**

---

Volume Delta with Custom Colors and Min Delta Input is a powerful and flexible indicator for analyzing volume delta (the difference between buying and selling volume) on TradingView charts. This indicator visualizes volume delta with customizable colors and allows filtering based on a minimum delta value. It is an ideal tool for traders who want to gain deeper insights into market activity and identify significant volume changes.

---

### Key Features:

Volume Delta Visualization:

- The indicator displays volume delta as candlesticks, where:

- Green candles indicate positive delta (buying volume dominance).

- Red candles indicate negative delta (selling volume dominance).

Customizable Colors:

- Users can choose their preferred colors for positive and negative delta to tailor the indicator to their preferences.

Minimum Delta Volume Filter:

- Added functionality to set a minimum delta volume threshold. This helps ignore insignificant volume changes and focus on important movements.

Flexible Timeframe Selection:

- The indicator supports analyzing volume delta on a different timeframe than the current chart. For example, you can analyze hourly volume delta on a daily chart.

Adaptive Settings:

- Users can configure the moving average (SMA) period and standard deviation multiplier to calculate the delta threshold.

---

### How to Use the Indicator:

Add the Indicator to Your Chart:

- Search for the indicator in the TradingView library and add it to your chart.

Configure the Settings:

- Positive Delta Bar Color: Choose the color for bars with positive delta.

- Negative Delta Bar Color: Choose the color for bars with negative delta.

- Minimum Delta Volume: Set the minimum delta volume value to be displayed.

- Use Custom Timeframe: Enable if you want to analyze volume on a different timeframe.

- Timeframe: Specify the desired timeframe for volume analysis (e.g., "1H" for hourly).

- SMA Period: Set the moving average period for delta calculation.

- Delta Multiplier: Adjust the standard deviation multiplier to fine-tune the delta threshold.

Analyze the Chart:

- Green candles indicate buying volume dominance, while red candles indicate selling volume dominance.

- Use the minimum delta volume filter to focus on significant movements.

---

### Benefits of the Indicator:

Flexibility: Customizable colors, timeframe selection, and filtering make the indicator versatile for various trading strategies.

Clarity: Volume delta visualization as candlesticks allows for quick assessment of market activity.

Noise Reduction: The minimum delta volume filter helps ignore insignificant changes and focus on important movements.

---

### Example Use Cases:

For Scalping: Use a minute timeframe and set a minimum delta volume filter to identify short-term volume anomalies.

For Long-Term Trading: Analyze volume delta on daily or weekly timeframes to identify key support and resistance levels.

---

### Recommendations:

Use the indicator in combination with other technical analysis tools (e.g., support/resistance levels or trendlines) to improve signal accuracy.

Experiment with the settings to adapt the indicator to your trading strategies.

---

Volume Delta with Custom Colors and Min Delta Input is an essential tool for traders who want to gain a deeper understanding of market dynamics and make more informed trading decisions. Try it out today and see its effectiveness for yourself!

Zerg range filter credit to Kivanc turkish pinecoder for base indicator i reworked with chatgpt and some common sense

this indicator similar to the ADX but i think its better visually to keep you out of market conditions that are unfavorable.

i made original indicator to work in a 0-100 enviroment (before it was a zero middle line oscillator) and added background coloring that has a lower and higher threshold setting. i also added a smoothing moving average. this will trigger threshold levels (not the core oscillator)

above higher level would indicate trending market conditions and its purple. these are the areas where you might want to buy low period moving average bounces like 10 or 21 ema

lower band will paint indicator background blue and its cold, meaning range bound trade ideas are likely play out better. selling resistance and buying horizontal supports for example.

you are encourage to play with lookback period and change thresholds until you find something that works for your trading.

on the picture above it illustrates how i intended its usage.

it also shows divergences which was not intended but also a function.

you can also observe as the oscillator likes to coil up into a tight range (horizontal or a wedge formation) and when these break their trendlines explosive moves are incoming usually.

if you have a trading system and can generate a lot of signals but want to filter out some loser trades this could be the indicator you were looking for.

i hope this will be inline with community guidelines. my other publishing got removed unfortunately

Jay Stock Vs S&P Sector Performance

This indicator facilitates stock comparison with an S&P sector while also identifying sector trends and potential trend beginnings, continuations, and conclusions by integrating moving averages with trend lines.

Its unique trend curves also assist in pinpointing key support and resistance levels for the sector. The sector grouping and market cap are calculated within the indicator using a curated list of stocks.

Multi-timeframe plots provide valuable insights by displaying short-term and long-term trends on the same chart, making it suitable for both intraday and swing trading analysis.

Multiple sector charts and trends can be visualized at the same time by adding multiple instances of same indicator to compare different sectors for portfolio rebalancing between sectors.

Another distinctive and essential feature is performance lines, which allow for visualizing S&P sector performance relative to the SPX market and stock performance relative to the S&P sector. Using the performance lines, one can identify top-performing sectors and then pinpoint the best stocks within those sectors.

How to read multi-timeframe charts?

The first timeframe, such as daily, is represented by a red EMA8 line (labeled DE) and a corresponding thin trend line (labeled DT). The second timeframe, such as weekly, uses a green EMA8 line (labeled WE) and a medium trend line (labeled WT). The third timeframe, such as monthly, is depicted with a blue EMA8 line (labeled ME) and a thick trend line (labeled MT).

As the timeframe increases, the true range increases and hence trend curve thickness increases.

How do EMA and Trend Line Work Together?

In the Electronic Tech sector daily chart screenshot below, trend initiation is highlighted with a green circle, trend continuation is marked by arrow, and trend completion is indicated with a red circle. A total of two trends are identified on the chart.

When the EMA crosses above the corresponding trend line, it signals the start of a trend, while a cross below the trend line marks its end. The period between the trend start and end represents trend continuation.

How do Trend Lines Serve as Support or Resistance?

In the Electronics Sector daily chart screenshot below, the monthly green trend line serves as support when the price declines toward it, while the red trend line acts as resistance when the price rises from below.

Green circles on the chart highlight instances where the monthly trend provided support, while red circles indicate points where the weekly trend acted as resistance.

How Multi-Timeframe Trends Assist in Stock Analysis?

In the Transportation sector daily chart screenshot below, the monthly trend is rising, and the weekly trend is also moving upward, indicating a favorable outlook for both long-term (monthly) and medium-term (weekly) trends. While, the daily chart suggests a up trend starting.

How to use performance lines to pick outperforming sectors and stocks?

In the screenshot below, the sector candles and trendlines have been disabled in the settings for better clarity, while the performance lines remain enabled. The chart displays META's performance lines, comparing its performance against the Technology Services sector.

The upward movement of the red lines indicates that META is performing well relative to its sector, while the rising blue lines suggest that the sector itself is gaining strength. This trend signals a potential improvement in both the sector’s overall performance and META’s standing within it.

Inputs and customization:

The combination of ema and trend plots will be plotted for 4 different time frames all at once. The first three timeframes(60, 240, D, W, M, etc) can be chosen in the settings while the fourth one is for current chart timeframe.

One can manually select the sector for comparison in the settings or choose to have it automatically selected for most of S&P 500 stocks. At what price to plot the sector chart can be set in the settings.

The sector candles, trend lines, performance lines and labels, can all be shown or hidden by adjusting settings.

How is Trend Line and EMA calculated?

The Trend line is calculated using an arithmetic equation based on the last 8 data points, which are themselves a combination of weighted moving averages of varying lengths. A 14-period true range of the price is calculated and plotted as a buffer zone around the trend lines.

Trend curves appear green when the price is above the trend line and red when it is below. Trend lines are labeled using the timeframe followed by 'T' (e.g., DT, WT, MT).

The EMA represents the weighted moving average of the most recent eight candles and is labeled with the timeframe followed by 'E' (e.g., DE, WE, ME).

How is sector data(representational) Calculated ?

The representational sector data (market cap) is calculated by summing each stock's price, weighted by its market cap percentage within the selected group, and then scaling the result to display at the desired price point on the chart.

The sector plot data shown here is the representation(not actual) of total market value of a few chosen stocks (list shown on chart) in the S&P 500. Large-cap stocks are excluded from the calculation to mitigate bias. Therefore, the displayed chart offers an approximate representation of the sector movement.

How is performance Calculated ?

The stock vs. sector performance, shown in red, is calculated as the stock's market cap movement divided by the sector's market cap movement. If the stock is doing much better than the rest of its sector group, this line will go up. Similarly, sector Vs SPX performance, shown in blue, is calculated as sector movement divide by SPX movement. When a sector outperforms the broader(SPX) market, the blue line trends upward.

Pro Tip: For optimal visibility, apply this indicator to a separate pane below the stock chart.

Caution: This indicator is intended solely for educational and analytical purposes, assisting traders in studying stock movements relative to their sector group. Stocks selected for sector market cap calculations are curated and hence these plots should only be taken for comparison study purposes. Exercise caution when using it for investment decisions.

Gufran - Volume DivergenceThis indicator detects bullish and bearish divergences by analyzing price action, volume trends, and RSI (Relative Strength Index) for added confirmation. It highlights key market reversals or trend continuations by identifying when price movement diverges from volume dynamics, providing traders with actionable insights for entry and exit points.

Key Features:

Divergence Detection:

Bullish Divergence: Price makes a lower low, but volume shows higher lows, signaling potential upward reversals.

Bearish Divergence: Price makes a higher high, but volume shows lower highs, signaling potential downward reversals.

RSI Confirmation:

Bullish Signals: Confirmed when RSI is in the oversold zone.

Bearish Signals: Confirmed when RSI is in the overbought zone (optional relaxation of RSI conditions available).

Normalized Volume Analysis:

Volume is scaled to the price range, ensuring clear and meaningful visualization alongside price action.

Customizable Parameters:

Lookback Period: Define how far back the script looks to identify divergences.

Volume Significance: Adjust the threshold for significant volume movements.

RSI Levels: Fine-tune overbought and oversold thresholds for optimal signal accuracy.

Gap Control: Avoid clutter by setting a minimum number of candles between successive divergence signals.

Clear Visual Representation:

Bullish Divergence: Marked with green labels and connecting lines.

Bearish Divergence: Marked with red labels and connecting lines.

Dotted lines show normalized volume divergence, while solid lines indicate price divergence.

Ideal For:

Traders who rely on volume dynamics to validate price movements.

Those looking for an added layer of confidence using RSI to filter false signals.

Swing and intraday traders aiming to identify market reversal zones or continuation patterns.

Customization Options:

Lookback Period: Adjustable range for detecting highs and lows.

Volume Threshold: Define the multiplier for significant volume changes.

RSI Settings: Tailor overbought/oversold levels to suit your trading style.

Relax RSI Condition: Toggle stricter or more flexible conditions for bearish divergences.

How to Use:

Add the indicator to your chart and configure the parameters to fit the asset and timeframe you are trading.

Look for:

Green “Bullish Div” labels near price lows for potential buying opportunities.

Red “Bearish Div” labels near price highs for potential selling opportunities.

Use this indicator in combination with other tools like support/resistance levels, trendlines, or moving averages for a comprehensive trading strategy.

Disclaimer:

This indicator is a tool for educational purposes and should not be used as a standalone trading signal. Always conduct proper risk management and consider additional technical/fundamental analysis before making trading decisions.

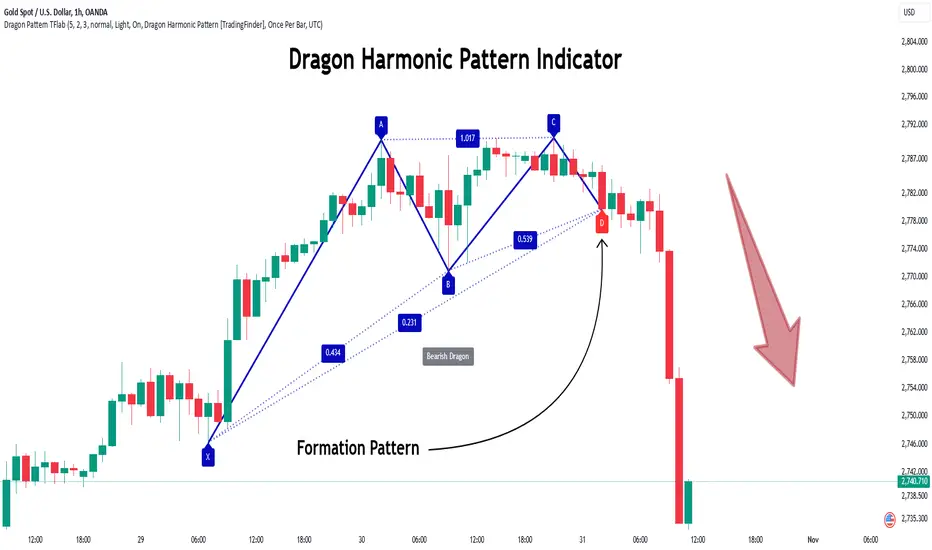

Dragon Harmonic Pattern [TradingFinder] Dragon Detector🔵 Introduction

The Dragon Harmonic Pattern is one of the technical analysis tools that assists traders in identifying Potential Reversal Zones (PRZ). Resembling an "M" or "W" shape, this pattern is recognized in financial markets as a method for predicting bullish and bearish trends. By leveraging precise Fibonacci ratios and measuring price movements, traders can use this pattern to forecast market trends with high accuracy.

The Dragon Harmonic Pattern is built on the XABCD structure, where each point plays a significant role in shaping and forecasting price movements. Point X marks the beginning of the trend, representing the initial price movement. Point A indicates the first retracement, usually falling within the 0.380 to 0.620 range of the XA wave.

Next, point B signals the second retracement, which lies within 0.200 to 0.400 of the AB wave. Point C, acting as the hump of the pattern, is generally located within 0.800 to 1.100 of the XA wave. Finally, point D represents the endpoint of the pattern and the Potential Reversal Zone (PRZ), where the primary price reversal occurs.

In bullish scenarios, the Dragon Pattern indicates a reversal from a downtrend to an uptrend, where prices move upward from point D. Conversely, in bearish scenarios, prices decline after reaching point D. Accurate identification of this pattern through Fibonacci ratio analysis and PRZ examination can significantly increase the success rate of trades, enabling traders to adjust their strategies based on key market levels such as 0.618 or 1.100.

Due to its high accuracy in identifying Potential Reversal Zones (PRZ) and its alignment with Fibonacci ratios, the Dragon Harmonic Pattern is considered one of the most popular tools in technical analysis. Traders can use this pattern to pinpoint entry and exit points with greater confidence while minimizing trading risks.

Bullish :

Bearish :

🔵 How to Use

The Dragon Harmonic Pattern indicator helps traders identify bullish and bearish patterns in the market, allowing them to capitalize on available trading opportunities. By analyzing Fibonacci ratios and the XABCD structure, the indicator highlights Potential Reversal Zones (PRZ).

🟣 Bullish Dragon Pattern

In the Bullish Dragon Pattern, the price transitions from a downtrend to an uptrend after reaching point D. At this stage, points X, A, B, C, and D must be carefully identified.

Fibonacci ratios for these points are as follows: Point A should fall within 0.380 to 0.620 of the XA wave, point B within 0.200 to 0.400 of the AB wave, and point C within 0.800 to 1.100 of the XA wave.

When the price reaches point D, traders should look for bullish signals such as reversal candlesticks or increased trading volume to enter a buy position. The take-profit level can be set near the previous price high or based on the 1.272 Fibonacci ratio of the XA wave, while the stop-loss should be placed slightly below point D.

🟣 Bearish Dragon Pattern

In the Bearish Dragon Pattern, the price shifts from an uptrend to a downtrend after reaching point D. In this pattern, points X, A, B, C, and D must also be identified. Fibonacci ratios for these points are as follows: Point A should fall within 0.380 to 0.620 of the XA wave, point B within 0.200 to 0.400 of the AB wave, and point C within 0.800 to 1.100 of the XA wave.

Upon reaching point D, bearish signals such as reversal candlesticks or decreasing trading volume indicate the opportunity to enter a sell position. The take-profit level can be set near the previous price low or based on the 1.272 Fibonacci ratio of the XA wave, while the stop-loss should be placed slightly above point D.

By combining the Dragon Harmonic Pattern indicator with precise Fibonacci ratio analysis, traders can identify key opportunities while minimizing risks and improving their decision-making in both bullish and bearish market conditions.

🔵 Setting

🟣 Logical Setting

ZigZag Pivot Period : You can adjust the period so that the harmonic patterns are adjusted according to the pivot period you want. This factor is the most important parameter in pattern recognition.

Show Valid Forma t: If this parameter is on "On" mode, only patterns will be displayed that they have exact format and no noise can be seen in them. If "Off" is, the patterns displayed that maybe are noisy and do not exactly correspond to the original pattern.

Show Formation Last Pivot Confirm : if Turned on, you can see this ability of patterns when their last pivot is formed. If this feature is off, it will see the patterns as soon as they are formed. The advantage of this option being clear is less formation of fielded patterns, and it is accompanied by the latest pattern seeing and a sharp reduction in reward to risk.

Period of Formation Last Pivot : Using this parameter you can determine that the last pivot is based on Pivot period.

🟣 Genaral Setting

Show : Enter "On" to display the template and "Off" to not display the template.

Color : Enter the desired color to draw the pattern in this parameter.

LineWidth : You can enter the number 1 or numbers higher than one to adjust the thickness of the drawing lines. This number must be an integer and increases with increasing thickness.

LabelSize : You can adjust the size of the labels by using the "size.auto", "size.tiny", "size.smal", "size.normal", "size.large" or "size.huge" entries.

🟣 Alert Setting

Alert : On / Off

Message Frequency : This string parameter defines the announcement frequency. Choices include: "All" (activates the alert every time the function is called), "Once Per Bar" (activates the alert only on the first call within the bar), and "Once Per Bar Close" (the alert is activated only by a call at the last script execution of the real-time bar upon closing). The default setting is "Once per Bar".

Show Alert Time by Time Zone : The date, hour, and minute you receive in alert messages can be based on any time zone you choose. For example, if you want New York time, you should enter "UTC-4". This input is set to the time zone "UTC" by default.

🔵 Conclusion

The Dragon Harmonic Pattern is an advanced and practical technical analysis tool that aids traders in accurately predicting bullish and bearish trends by identifying Potential Reversal Zones (PRZ) and utilizing Fibonacci ratios. Built on the XABCD structure, this pattern stands out for its flexibility and precision in identifying price movements, making it a valuable resource among technical analysts. One of its key advantages is its compatibility with other technical tools such as trendlines, support and resistance levels, and Fibonacci retracements.

By using the Dragon Harmonic Pattern indicator, traders can accurately determine entry and exit points for their trades. The indicator analyzes key Fibonacci ratios—0.380 to 0.620, 0.200 to 0.400, and 0.800 to 1.100—to identify critical levels such as price highs and lows, offering precise trading strategies. In bullish scenarios, traders can profit from rising prices, while in bearish scenarios, they can capitalize on price declines.

In conclusion, the Dragon Harmonic Pattern is a highly reliable tool for identifying trading opportunities with exceptional accuracy. However, for optimal results, it is recommended to combine this pattern with other analytical tools and thoroughly assess market conditions. By utilizing this indicator, traders can reduce their trading risks while achieving higher profitability and confidence in their trading strategies.

Quartile For Loop [SeerQuant]Quartile For Loop (QFL)

- The Quartile For Loop (QFL) is an advanced trend-following and scoring oscillator designed to detect momentum shifts and trend transitions using a quartile-based analysis. By leveraging quartile calculations and iterative scoring logic, QFL delivers dynamic trend signals which can be tailored to suit various market conditions.

--------------------------------------------------------------------------------------------------

⚙️ How It Works

1️⃣ Quartile-Based Calculation

The indicator calculates the weighted average of the first quartile (Q1), median (Q2), and third quartile (Q3) over a customizable length, providing a robust adaptive trend value.

2️⃣ For Loop Scoring System

A unique for-loop structure iteratively scores each quartile value against historical data, delivering actionable trend signals. Users can toggle between price-based and quartile-based scoring methods for flexibility.

3️⃣ Threshold Logic

Bullish (Uptrend): Score exceeds the positive threshold.

Bearish (Downtrend): Score falls below the negative threshold.

Neutral: Score remains between thresholds.

4️⃣ Visual Trend Enhancements

Optional candle coloring and a color-coded SMA provide clear visual cues for identifying trend direction. The adaptive quartile is dynamically updated to reflect changing market conditions.

--------------------------------------------------------------------------------------------------

✨ Customizable Settings

Indicator Inputs

Quartile Length: Define the calculation length for quartile analysis.

Calculation Source: Choose the data source for quartile calculations (e.g., close price).

Alternate Signal: Toggle between price-based and quartile-based scoring.

Loop Settings

Start/End Points: Set the range for the for-loop scoring system.

Thresholds: Customize uptrend and downtrend thresholds.

Style Settings

Candle Coloring: Enable optional trend-based candle coloring.

Color Schemes: Select from five unique palettes for trend visualization.

--------------------------------------------------------------------------------------------------

🚀 Features and Benefits

Quartile-Driven Analysis: Harnesses the statistical power of quartiles for adaptive trend evaluation.

Dynamic Scoring: Iterative scoring logic adjusts to market fluctuations.

Clear Visual Representation: Color-coded histograms, candles, and trendlines enhance readability.

Fully Customizable: Flexible inputs allow adaptation to diverse trading styles and strategies.

--------------------------------------------------------------------------------------------------

📜 Disclaimer

This indicator is for educational purposes only and does not constitute financial advice. Market analysis is inherently speculative and subject to risk. Users should consult a licensed financial advisor before making trading decisions. Use at your own discretion.

--------------------------------------------------------------------------------------------------

Volatility Footprint CandlesVolatility Footprint is an innovative volume profile indicator that dynamically adapts to real-time market conditions, providing traders with a powerful tool to visualize and interpret market structure, order flow, and potential areas of support and resistance.

At its core, Volatility Footprint combines the concepts of market profile, volume analysis, and volatility measurement to create a unique and adaptive charting experience. The indicator intelligently adjusts its display based on the current market volatility, ensuring that traders always have a clear and readable chart, regardless of the instrument or timeframe they are analyzing.

The footprint chart is composed of a series of color-coded boxes, each representing a specific price level. The color of the box indicates whether there is a net buying or selling pressure at that level, while the opacity reflects the relative strength of the volume. This intuitive visualization allows traders to quickly identify areas of high and low volume, as well as potential imbalances in order flow.

In addition to the individual box volumes, Volatility Footprint also calculates and displays the cumulative volume delta. This running total of buy and sell volumes across all price levels provides valuable insight into the overall market sentiment and potential trends.

One of the key features of Volatility Footprint is its ability to identify and highlight the Point of Control (POC). The POC represents the price level with the highest volume concentration and serves as a key reference point for potential support or resistance. By drawing attention to this crucial level, the indicator helps traders make more informed decisions about potential entry and exit points.

Volatility Footprint is designed to be highly customizable, allowing traders to tailor the appearance of the footprint chart to their specific preferences. Users can easily modify the colors, opacity, and size of the boxes, labels, and POC marker to enhance readability and clarity.

The indicator's versatility makes it suitable for a wide range of trading styles and strategies. Whether you are a scalper looking for short-term opportunities or a swing trader aiming to identify potential trend reversals, Volatility Footprint can provide valuable insights into market dynamics.

By combining Volatility Footprint with other forms of analysis, such as price action, key levels, and technical indicators, traders can gain a more comprehensive understanding of market behavior and make better-informed trading decisions.

Volatility Footprint's adaptive approach to volume profile analysis sets it apart from traditional fixed-resolution volume profile indicators. By dynamically adjusting to the unique characteristics of each instrument and timeframe, the indicator ensures that traders always have a clear and meaningful representation of market structure and order flow.

Volatility Footprint is a powerful tool that traders can incorporate into their market analysis and decision-making process. By providing a dynamic, visual representation of volume and order flow at different price levels, this indicator offers valuable insights into market structure, sentiment, and potential areas of support and resistance. Let's explore how traders might effectively utilize Volatility Footprint in their trading approach.

1. Identifying Key Levels:

One of the primary uses of Volatility Footprint is to identify key price levels where significant trading activity has occurred. The color-coded boxes allow traders to quickly spot areas of high volume concentration, which may indicate potential support or resistance zones. For example, if a trader notices a cluster of boxes with high opacity at a specific price level, they may interpret this as a strong support or resistance area, depending on the prevailing market context. By paying attention to these key levels, traders can make more informed decisions about potential entry and exit points, as well as placement of stop-loss orders and profit targets.

2. Assessing Market Sentiment:

The cumulative volume delta feature of Volatility Footprint provides traders with a valuable gauge of overall market sentiment. By analyzing the running total of buy and sell volumes across all price levels, traders can gain insight into the dominant market forces at play. If the cumulative delta is significantly positive, it may suggest a bullish sentiment, as buying pressure has been consistently outpacing selling pressure. Conversely, a negative cumulative delta may indicate a bearish sentiment. Traders can use this information to confirm or question their bias and adjust their trading plan accordingly.

3. Confirming Breakouts and Trend Reversals:

Volatility Footprint can be particularly useful in confirming the strength and validity of breakouts and potential trend reversals. When a price level is breached, traders can refer to the footprint chart to assess the volume and order flow characteristics around that level. If the breakout is accompanied by a surge in volume and a clear imbalance between buying and selling pressure, it may suggest a strong and sustainable move. On the other hand, if the volume is relatively low or evenly distributed, the breakout may be less reliable. By using Volatility Footprint to confirm breakouts, traders can make more informed decisions about whether to enter or exit a trade, or to adjust their position size.

4. Detecting Imbalances and Potential Reversals:

Imbalances between buying and selling pressure at specific price levels can often precede significant market moves or reversals. Volatility Footprint makes it easy for traders to spot these imbalances visually. For instance, if a trader observes a price level with a significantly larger number of sell boxes compared to buy boxes, it may indicate a potential exhaustion point for a bullish trend, and a reversal might be imminent. Traders can use this information in conjunction with other technical analysis tools, such as trendlines, moving averages, or momentum oscillators, to identify high-probability trading opportunities.

5. Adapting to Market Conditions:

One of the key strengths of Volatility Footprint is its ability to dynamically adapt to the unique volatility characteristics of different instruments and timeframes. This adaptability ensures that the indicator remains relevant and informative across a wide range of market conditions. Traders can use Volatility Footprint to gauge the relative volatility and volume of a particular instrument or timeframe, and adjust their trading approach accordingly. For example, in a highly volatile market, traders may opt for wider stop-loss levels and smaller position sizes to account for the increased risk.

Incorporating Volatility Footprint into a trading strategy requires a combination of technical analysis, market understanding, and risk management. Traders should use this indicator as part of a comprehensive approach, combining it with other forms of analysis, such as price action, key levels, and technical indicators. By doing so, traders can gain a more complete picture of market dynamics and make better-informed trading decisions.

It's important to note that while Volatility Footprint provides valuable insights, it should not be relied upon as a standalone trading signal. Traders should always consider the broader market context, their risk tolerance, and their overall trading plan when making decisions based on the information provided by this indicator.

In conclusion, Volatility Footprint offers traders a dynamic and visually intuitive way to analyze market structure, volume, and order flow. By identifying key levels, assessing market sentiment, confirming breakouts, detecting imbalances, and adapting to market conditions, traders can leverage this powerful tool to make more informed and confident trading decisions. As with any technical analysis tool, Volatility Footprint should be used in conjunction with sound risk management principles and a well-defined trading strategy to maximize its effectiveness.

Flow-Weighted Volume Oscillator (FWVO)Volume Dynamics Oscillator (VDO)

Description

The Volume Dynamics Oscillator (VDO) is a powerful and innovative tool designed to analyze volume trends and provide traders with actionable insights into market dynamics. This indicator goes beyond simple volume analysis by incorporating a smoothed oscillator that visualizes the flow and momentum of trading activity, giving traders a clearer understanding of volume behavior over time.

What It Does

The VDO calculates the flow of volume by scaling raw volume data relative to its highest and lowest values over a user-defined period. This scaled volume is then smoothed using an exponential moving average (EMA) to eliminate noise and highlight significant trends. The oscillator dynamically shifts above or below a zero line, providing clear visual cues for bullish or bearish volume pressure.

Key features include:

Smoothed Oscillator: Displays the direction and momentum of volume using gradient colors.

Threshold Markers: Highlights overbought or oversold zones based on upper and lower bounds of the oscillator.

Visual Fill Zones: Uses color-filled areas to emphasize positive and negative volume flow, making it easy to interpret market sentiment.

How It Works

The calculation consists of several steps:

Smoothing with EMA: An EMA of the scaled volume is applied to reduce noise and enhance trends. A separate EMA period can be adjusted by the user (Volume EMA Period).

Dynamic Thresholds: The script determines upper and lower bounds around the smoothed oscillator, derived from its recent highest and lowest values. These thresholds indicate critical zones of volume momentum.

How to Use It

Bullish Signals: When the oscillator is above zero and green, it suggests strong buying pressure. A crossover from negative to positive can signal the start of an uptrend.

Bearish Signals: When the oscillator is below zero and blue, it indicates selling pressure. A crossover from positive to negative signals potential bearish momentum.

Overbought/Oversold Zones: Use the upper and lower threshold levels as indicators of extreme volume momentum. These can act as early warnings for trend reversals.

Traders can adjust the following inputs to customize the indicator:

High/Low Period: Defines the period for volume scaling.

Volume EMA Period: Adjusts the smoothing factor for the oscillator.

Smooth Factor: Controls the responsiveness of the smoothed oscillator.

Originality and Usefulness

The VDO stands out by combining dynamic volume scaling, EMA smoothing, and gradient-based visualization into a single, cohesive tool. Unlike traditional volume indicators, which often display raw or cumulative data, the VDO emphasizes relative volume strength and flow, making it particularly useful for spotting reversals, confirming trends, and identifying breakout opportunities.

The integration of color-coded fills and thresholds enhances usability, allowing traders to quickly interpret market conditions without requiring deep technical expertise.

Chart Recommendations

To maximize the effectiveness of the VDO, use it on a clean chart without additional indicators. The gradient coloring and filled zones make it self-explanatory, but traders can overlay basic trendlines or support/resistance levels for additional context.

For advanced users, the VDO can be paired with price action strategies, candlestick patterns, or other trend-following indicators to improve accuracy and timing.

Dynamic S/R Levels: Edge FinderOverview

The Dynamic S/R Levels: Edge Finder indicator is designed to identify dynamic support and resistance levels based on historical price action. It uses a combination of price extremes (highs and lows) over user-defined lookback periods, weighted moving averages (WMAs), and touch-count analysis to provide actionable insights into key market levels.

This tool is ideal for traders who want to:

Identify dynamic support and resistance zones.

Understand the strength of these levels based on price touches.

Make informed decisions using clear, adaptive levels.

How It Works

Dynamic Levels Calculation:

The indicator calculates dynamic support levels using the lowest lows and dynamic resistance levels using the highest highs over user-defined lookback periods (e.g., 20, 40, 60 bars, etc.).

These levels are updated dynamically as new price data becomes available.

Touch Count Analysis:

The indicator counts how many times the price has touched or come close to each support/resistance level within the lookback period.

Levels with more touches are considered stronger and are highlighted accordingly.

Weighted Moving Averages (WMAs):

The indicator uses 50-period and 100-period WMAs to identify the closest support/resistance levels to the current trend.

Levels near these WMAs are given additional weight, as they are more likely to act as significant barriers.

Level Merging:

If two support or resistance levels are too close to each other (based on the minimum distance percentage), the weaker level (with fewer touches) is removed to avoid clutter.

Visualization:

Support levels are displayed as dashed red lines, and resistance levels are displayed as dashed blue lines.

Each level is labeled with its corresponding touch count, allowing traders to quickly assess its strength.

How to Interpret the Indicator

Strong Support/Resistance Levels:

Levels with higher touch counts (e.g., 5, 10, or more) are considered stronger and are more likely to hold in the future.

Use these levels to plan entries, exits, or stop-loss placements.

Proximity to WMAs:

Levels closest to the 50-period or 100-period WMA are more significant, especially in trending markets.

These levels often act as dynamic barriers where price reactions are more likely.

Breakouts and Rejections:

If the price breaks through a strong resistance level, it may indicate a potential bullish trend.

If the price rejects a strong support level, it may indicate a potential bearish trend.

Always confirm breakouts or rejections with additional analysis (e.g., volume, candlestick patterns).

Level Merging:

Merged levels indicate areas of high confluence, where multiple support/resistance zones overlap.

These areas are particularly important for decision-making, as they represent stronger market reactions.

Key Features

Customizable Lookback Periods: Adjust the lookback periods for each dynamic level to suit your trading style.

Touch Count Labels: Quickly identify the strength of each level based on the number of price touches.

Adaptive Levels: The indicator dynamically updates levels based on recent price action.

Clean Visualization: Levels are automatically merged to avoid clutter and provide a clear view of the market structure.

Usage Tips

Trend Identification: Combine the indicator with trend-following tools (e.g., moving averages, trendlines) to confirm the overall market direction.

Risk Management: Use the identified levels to set stop-loss orders or take-profit targets.

Timeframe Flexibility: The indicator works on all timeframes, but it is particularly effective on higher timeframes (e.g., 1H, 4H, Daily) for more reliable levels.

Example Scenarios

Bounce Trade:

If the price approaches a strong support level (high touch count) and shows signs of rejection (e.g., bullish candlestick patterns), consider a long position with a stop-loss below the support level.

Breakout Trade:

If the price breaks above a strong resistance level with high volume, consider a long position with a target at the next resistance level.

Range-Bound Market:

In a sideways market, use the support and resistance levels to identify range boundaries and trade bounces between them.

Disclaimer

Dynamic S/R Levels: Edge Finder is a technical analysis tool designed to identify dynamic support and resistance levels based on historical price action. It is intended for informational and educational purposes only. This indicator does not provide financial, investment, or trading advice. Users are solely responsible for their trading decisions and should conduct their own research and analysis before making any trades. The developer of this tool is not liable for any financial losses or damages resulting from the use of this indicator. Trading in financial markets involves risk, and you should only trade with capital you can afford to lose.

Rolling Angled Volume Profile [Trendoscope®]🎲 Volume Profile Indicators

🎯Traditional Volume Profile

Volume profile indicators visually represent the distribution of volume across price levels. These indicators typically operate on horizontal price levels, making them effective in identifying supply and demand zones in ranging markets. However, they are less useful in trending markets where price movements follow a slope.

🎯The Need for Angled Volume Profiles

Just as support and resistance levels differ from trendlines, volume profile indicators require an equivalent method to account for volume distribution along a sloped trajectory. This would enable more accurate volume analysis in trending markets.

We identified the need of Angled Volume profile and have already published few indicators that implements the concept.

Angled Volume Profile calculates volume distribution along a slope. Users interact with the indicator by selecting the starting point, after which the volume profile is calculated for the selected trajectory.

Volume Forks is another tool that extends angled volume profile analysis, aligning volume profiles along the trajectory of pitchforks.

🎲 Rolling Volume Profile Indicator

The Rolling Volume Profile offers a new approach to angled volume profile calculations, addressing some limitations of earlier implementations:

🎯 Rolling Calculation

The volume profile is calculated for the last N bars of the instrument

The slope of the profile lines is determined by the closing prices of the starting and ending bars

Profiles are drawn in the direction of price movement between the start and end bars.

🎯 Dynamic Updates

As new bars are added, the calculations are updated, and the profile is redrawn based on the latest data.

This dynamic behavior earns it the name "Rolling Volume Profile."

🎯 Advantages Over Earlier Versions

Unlimited Profile Lines : Unlike previous implementations limited to 500 profile lines, this indicator uses polyline objects, overcoming the restriction.

Live Updates : Previous angled volume profile tools lacked real-time updates when new bars appeared. This limitation is resolved in the Rolling Volume Profile Indicator.

The Rolling Volume Profile provides an efficient and scalable solution for analyzing volume in trending markets.

🎯 Indicator Settings

Simple settings include few customisable options

Enhanced Retail vs Institutional ActivityThis script highlights market activity in real-time, making it easier to infer the type of market participants driving price and volume changes.

Here’s a list of what the script analyzes:

Volume:

Current volume of the candle.

Moving average of volume over a specified number of periods.

Volume spikes: Current volume compared to a threshold multiple of the moving average.

Price Movement:

Percentage change in price between the current and previous candle.

Identifies significant price changes based on a user-defined threshold.

Institutional Activity:

High volume spikes combined with significant price movements.

Retail Activity:

Periods without volume spikes or significant price changes.

VWAP (Volume-Weighted Average Price):

The average traded price over a specified lookback period, weighted by volume, used as a benchmark.

Market Context Visualization:

Background colors to differentiate institutional (red) and retail (green) activity.

Overlays for:

-Volume bars.

-Average volume line.

-VWAP line.

In summary:

Red = Institutional activity: High volume + significant price change.

Green = Retail activity: Low volume or insignificant price change.

---------------------------------------------------------------------------------------------------------------------

Analysis Explanation:

I’m forecasting that Bitcoin will retest its November 12th low (~$85,098.75) around January 20th, 2025, where the horizontal support line intersects with the downtrend line. This conclusion is based on the following:

Trend Analysis:

The chart shows a clear downtrend with price respecting the descending trendline.

The intersection of the horizontal support and the downtrend line on January 20th indicates a confluence point where price action may gravitate.

Volume and Activity Insights:

Using the Retail vs Institutional Activity indicator, the chart highlights periods dominated by institutional (red background) or retail (green background) activity.

Current price action is in a green zone, suggesting predominantly retail participation with lower volume and insignificant price movements.

Retail vs Institutional Dynamics:

Institutional activity (red zones) aligns with significant price movements and volume spikes, often marking key turning points or trends.

The recent green retail-dominated periods suggest a lack of strong momentum, which may lead to continued price decline until institutions re-enter around the confluence area.

Volume Observations:

Volume remains relatively low during the current retail phase, indicating weak buying pressure.

A potential surge in institutional activity (red zones) near the support level could trigger a rebound or breakdown.

I expect Bitcoin’s price to drop further and test the November 12th low near $85,098.75 on January 20th, 2025. This projection is supported by the convergence of the downtrend line and horizontal support, low retail-driven volume, and historical institutional activity patterns observed using the "Retail vs Institutional Activity" indicator.

Candle Spread Oscillator (CS0)The Candle Spread Oscillator (CSO) is a custom technical indicator designed to help traders identify momentum and directional strength in the market by analyzing the relationship between the candle body spread and the total candle range. This oscillator provides traders with a visually intuitive representation of price action dynamics and highlights key transitions between positive and negative momentum.

How It Works:

Body Spread vs. Total Range:

The CSO calculates the body spread (difference between the close and open price) and compares it to the total range (difference between the high and low price) of a candle.

The ratio of the body spread to the total range represents the proportion of price movement driven by directional momentum.

Smoothed Oscillator:

To remove noise and enhance clarity, the ratio is smoothed using a Hull Moving Average (HMA). The smoothing period can be adjusted through the "Smoothing Period" input, enabling traders to tailor the indicator to their preferred timeframes or strategies.

Gradient Visualization:

A gradient coloring is applied to the oscillator, transitioning smoothly between colors (e.g., fuchsia for negative momentum and aqua for positive momentum). This provides traders with a clear, intuitive visual cue of market behavior.

Visual Features:

Oscillator Plot:

The oscillator is displayed as an area-style plot, dynamically colored using a gradient. Positive values are represented in shades of aqua, while negative values are in shades of fuchsia.

Midline (0 Level):

A horizontal midline is plotted at the zero level, serving as a key reference point for identifying transitions between positive and negative momentum.

Background Highlights:

The chart background is subtly colored to match the oscillator's state, enhancing the visual emphasis on current momentum conditions.

Alerts for Key Crossovers:

The CSO comes with built-in alert conditions, making it highly actionable for traders: