BT Delta AbsorptionBT Absorption detects aggressive counterflow volume—moments where one side

of the market (buyers or sellers) attacks aggressively, yet price fails to move

proportionally.

This is the classic definition of absorption:

"Large market orders are being absorbed by strong passive limit orders."

Absorption is one of the most reliable early signals for:

Reversals

Trap conditions

Failed breakouts

Liquidity grabs

Fake displacement moves

---

■ What BT Absorption Measures

1. Delta Imbalance

Identifies when buying or selling pressure becomes unusually one-sided.

2. Volatility Mismatch

Shows when large delta does NOT translate into meaningful price movement.

3. Absorption Strength Score

A normalized reading (often 0–100) showing the intensity of counterflow activity.

4. Wick & Structure Absorption

Wick-driven absorption helps identify:

Failed sweeps

Stop hunts

Rejection zones

Trapped traders

---

■ Why Absorption Matters

Absorption almost always precedes:

Reversals

Failed breakout moves

SMC/ICT-style displacement

Order block formation

Trend continuation after a trap

When aggressive traders cannot move price toward their desired direction,

the move typically reverses quickly—and with force.

---

■ Visual Elements

• Bull Absorption Marker

Often appears near lows—signals seller aggression failing to push price down.

• Bear Absorption Marker

Often appears near highs—signals buyer aggression failing to break higher.

• Absorption Score Heatmap (optional)

Shows intensity of absorption per candle.

• Threshold Levels

Identify when absorption becomes statistically significant.

---

■ How to Use BT Absorption in Trading

1. Reversal Detection

Look for absorption after:

Equal highs/lows

Sweeps

Stop runs

Breakout failures

This is often the earliest possible signal that a reversal is coming.

2. Filter Breakouts

A breakout without absorption is usually weak.

A breakout with absorption against it is likely a fakeout.

3. Confirm SMC/ICT Concepts

The indicator pairs perfectly with:

Fair Value Gaps

Order Blocks

Liquidity sweeps

Displacement legs

If your setup triggers and absorption confirms → high confidence.

4. Identify Trap Conditions

Absorption often marks:

Trapped breakout chasers

Trapped trend shorts

Imbalanced orderflow

These create ideal high-R trades.

5. Alert-Driven Market Monitoring

Use alerts for:

Bull Absorption

Bear Absorption

High-strength absorption

Absorption clusters

This allows traders to step away from charts while still catching

high-probability reversals.

---

■ High-Probability Absorption Setups

A) Sweep + Absorption

Swept level → absorption → enter opposite direction.

B) Failed Breakout Absorption

Breaks structure → delta fails → absorption prints → strong reversal.

C) Trend Continuation Absorption

Absorption against the correction often precedes continuation.

D) Absorption Clusters

Multiple absorption signals indicate a structural market shift.

---

■ Final Summary

BT Absorption provides:

Early reversal signals

Counterflow pressure detection

Confirmation for existing setups

Identification of liquidity traps

Alert-based monitoring across multiple markets

BT Absorption is the perfect complement to BT Spike:

• BT Spike = detects volatility ignition

• BT Absorption = detects failed aggression + reversals

Combined, they form a complete liquidity and orderflow toolkit.

Volatilità

ATR + BJ Signal(GOLD)This script visualizes a price-based counting pattern that highlights potential market exhaustion and reversal areas.

When a series of candles continues in one direction, the indicator measures price momentum loss and marks possible turning points.

Features

Counts consecutive upward or downward price movement

Highlights possible exhaustion or reversal areas

Optional alerts, take-profit and stop-loss visual levels

Fully customizable colors and display settings

Useful as a confirmation tool with trend or volume indicators

This indicator is designed to assist decision-making, not to generate mechanical buy/sell signals.

Best used together with other trend or volatility tools.

📎 Short Description (for compact field)

Counts consecutive price movement to highlight potential market exhaustion and reversal zones.

Helps identify when strong trends may be weakening.

Liquidation HeatmapSDSH Liquidation Heatmap: Stochastic Microstructure Modeling

Technical Summary

This indicator implements an advanced algorithmic approach for the detection of liquidity and liquidation zones using the State-Dependent Spread Hawkes (SDSH) model. Unlike conventional heatmaps that aggregate raw Ask/Bid and Open Interest (OI) data from external data providers, this script generates a synthetic liquidity topology based purely on the physics of price movement and market microstructure.

Scientific Foundation: The SDSH Model

The core of the indicator relies on two integrated mathematical components that allow for the inference of latent order locations without reading the Limit Order Book (LOB):

State-Dependent Spread Estimation: It uses variations of range-based volatility estimators (based on Corwin-Schultz principles) to calculate the "effective spread" of the market in real-time. This allows determining the actual price friction and, consequently, where leveraged positions are statistically likely to accumulate.

Self-Exciting Hawkes Processes: A stochastic point process model (Hawkes Process) is applied to measure the "intensity" of liquidity events. The algorithm assumes that order arrivals and volatility cluster in time; the model quantifies this market "memory" to project the future intensity of liquidations.

High-Fidelity Replication without Level 2 Data

The critical value of this indicator lies in its ability to replicate with spatial exactitude the zones that a Liquidation Heatmap based on Tick-level or real market depth data would signal, but operating in a "black box" environment regarding provider data.

By triangulating volatility, temporal intensity decay (Hawkes Decay), and standard leverage projections (100x, 50x, 25x), the algorithm reconstructs the liquidation map. Mathematically, real liquidation zones are a function of participant entry and subsequent volatility; by modeling these variables accurately, the visual result converges with the actual location of stop-losses and mass liquidation points.

Utility for Quantitative Modeling (Quants)

This tool is designed for research and quantitative trading environments that require:

Data Independence: Elimination of the need for expensive subscriptions to Open Interest or Depth of Market (DOM) data.

Noise Filtering: As a mathematical model, it filters out "spoofing" (fake orders in the book) that often clutters traditional heatmaps, showing only zones where market structure mathematically forces the existence of liquidity.

Structural Backtesting: It allows for the validation of mean reversion and liquidity breakout strategies on historical data where market depth information is often unavailable or unreliable.

Visual Parameters

The indicator renders "stress boxes" with opacity gradients based on the probability of price collision.

Colors: Map the density of estimated synthetic contracts.

Persistence: Zones remain active until the price interacts with them (absorption) or the model determines that liquidity has dissipated (Hawkes decay).

Scary Flush Indicator R0Work in progress.

Calculates the gradient based on candle lows (previous low to current low). Works on all time frames.

Looks for a selling gradient of >0.75pts per minute then highlights. Anything less than this indicates a lazy grind down and indicates a potential invalidation for the FBD.

RV − IV Spread Alert (SPY vs VIX)Realized vs Implied Volatility Spread (RV − IV) for the S&P 500 / SPY.

Plots the daily difference between 30-day realized volatility (SPY) and implied volatility (VIX) in basis points.

Key insight from the research: when the spread turns and stays above ≈ +50 bps, forward returns historically degrade and volatility of returns rises sharply — a useful early-warning regime flag.

Features:

- Clean daily plot of RV − IV in bps

- Horizontal lines at 0, −50 bps and +50 bps

- Red background when spread > +50 bps

- Built-in alert condition that fires once per bar close when spread closes above +50 bps

- Optional “all-clear” alert when it drops back below

Use on SPY or ES1! daily chart. Perfect for anyone wanting a simple notification when the market enters the “risk-on” volatility regime highlighted by Machina Quanta and the original Bali & Hovakimian (2007) paper.

Triple ATR Adaptive MAs + VWAP Option + Clouds + Candle Trend V2Another one of my experiences ... combining things...

📘 Indicator Description – Triple ATR Adaptive Moving Averages with VWAP Influence

This indicator plots three adaptive moving averages whose behavior changes dynamically based on market volatility (ATR) and optionally VWAP deviation.

Because they adapt in real time to both volatility and VWAP pressure, their movement, slope, and reaction speed differ significantly from traditional moving averages.

🔶 1. ATR-Adaptive Moving Averages

Each of the three MAs uses a custom adaptive formula:

ATR (Average True Range) is measured over a chosen period.

Higher ATR → more volatility → the MA becomes more reactive and moves closer to price.

Lower ATR → stable market → the MA becomes smoother and slower.

This creates a volatility-aware smoothing factor, making the MA expand, contract, and respond to market conditions in ways a classic SMA, EMA, or HMA cannot.

🔷 2. Optional VWAP Influence

Each MA has an independent toggle allowing it to be influenced by VWAP.

When enabled:

The MA is gently “pulled” toward VWAP.

The strength of this attraction is determined by the VWAP Influence parameter (0–1).

This causes the moving averages to behave differently from normal MAs:

In trending markets, the ATR and price push the MA away from VWAP.

In mean-reverting or balanced conditions, VWAP pulls the MA back toward fair value.

The result is an MA that reflects both trend pressure and fair-value pressure.

🔶 3. Visual Behavior: Non-Traditional Movement

Because each MA is simultaneously influenced by volatility, trend magnitude, and VWAP deviation, their shape is often very distinct from normal moving averages.

They may:

Respond faster during high volatility

Flatten out earlier during consolidation

Curve toward VWAP when price becomes extended

Separate or compress depending on ATR strength

This is intentional and essential, since the goal is to show:

✔ Volatility expansion

✔ Trend exhaustion

✔ Overextended price relative to VWAP

✔ Dynamic trend confirmation

Rather than simply smoothing past price.

🔷 4. Three Independent Adaptive Lines

Each of the three moving averages has:

Its own ATR length

Its own sensitivity multiplier

Its own optional VWAP influence

Its own color and trail

This allows the user to combine:

a fast volatility-adaptive trend line

a mid-range adaptive baseline

a slow adaptive long-trend MA

All adapting independently to volatility and VWAP conditions.

🔶 5. Optional Candle Coloring

The indicator can color candles according to trend strength derived from the fast/slow MAs.

Stronger trends produce more vivid colors. Neutral or conflicting trends produce softer colors.

This adds a visual layer to identify:

Trend direction

Trend strength

Volatility state

Market compression

at a glance.

📌 Summary

This indicator does not behave like standard SMAs or EMAs because each line dynamically adapts to:

🔸 ATR (volatility)

🔸 VWAP (fair value)

This makes the indicator extremely responsive to market conditions while still reducing noise during stable phases.

It provides a more realistic, context-aware, and intelligent representation of price behavior compared to traditional moving averages.

TradePulse ProTradepulse is a proprietary trading tool that combines a directional signal engine, a trend-adaptive trailing stop system, and a momentum confirmation oscillator into a unified decision framework. Instead of simply stacking separate indicators on a chart, TradePulse integrates these components into a single rules-based system designed to help traders act with structure rather than emotion by identifying conditions where trend and momentum are aligning.

How It Works:

Directional Signals - TradePulse uses a custom price-average model with ATR-based volatility thresholds to detect transitions between bullish and bearish environments. Buy and Sell markers appear only when price strength and volatility conditions confirm a shift. Reducing noise and late entries.

Trend-Adaptive Trailing Stop - A dynamic trailing system combines smoothed moving averages with ATR expansion logic. As price develops, the trailing level adjusts automatically and target projections update based on symmetry extensions. Helping guide structured exits and trade management.

Momentum Confirmation - A proprietary oscillator blends stochastic positioning with center-of-gravity transformation and dual smoothing. It highlights whether momentum aligns with the directional shift, helping traders avoid weaker setups and focus on higher-quality conditions.

Key Features:

- Clear Buy/Sell transitions based on multi-factor confluence

- Adaptive trailing stop + projected targets for structured management

- Momentum filtering to support higher-quality opportunities

- Sensitivity adjustments to suit different markets & styles

TradePulse is original work protected under invite-only access. It is provided for educational and informational purposes only. Trading involves risk, and signals should always be validated with your own analysis and risk management.

CK Auto Adaptive StoplossThis tool automatically finds the best stop-loss for every trade by analyzing candle structure, ATR volatility, volume spikes, and market momentum. It tightens or widens the stop dynamically and shows you exactly how many contracts you can use based on your risk per trade.

It also plots bold stop-loss lines on your chart and includes a live position-sizing table so you always stay consistent.

Volatility-Dynamic Risk Manager MNQ [HERMAN]Title: Volatility-Dynamic Risk Manager MNQ

Description:

The Volatility-Dynamic Risk Manager is a dedicated risk management utility designed specifically for traders of Micro Nasdaq 100 Futures (MNQ).

Many traders struggle with position sizing because they use a fixed Stop Loss size regardless of market conditions. A 10-point stop might be safe in a slow market but easily stopped out in a high-volatility environment. This indicator solves that problem by monitoring real-time volatility (using ATR) and automatically suggesting the appropriate Stop Loss size and Position Size (Contracts) to keep your dollar risk constant.

Note: This tool is hardcoded for MNQ (Micro Nasdaq) with a tick value calculation of $2 per point.

📈 How It Works

-This script operates on a logical flow that adapts to market behavior:

-Volatility Measurement: It calculates the Average True Range (ATR) over a user-defined length (Default: 14) to gauge the current "speed" of the market.

-State Detection: Based on the current ATR, the script classifies the market into one of three states:

Low Volatility: The market is chopping or moving slowly.

Normal Volatility: Standard trading conditions.

High Volatility: The market is moving aggressively.

Dynamic Stop Loss Selection: Depending on the detected state, the script selects a pre-defined Stop Loss (in points) that you have configured for that specific environment.

Position Sizing Calculation: Finally, it calculates how many MNQ contracts you can trade so that if your Stop Loss is hit, you do not lose more than your defined "Max Risk per Trade."

🧮 Methodology & Calculations

Since this script handles risk management, transparency in calculation is vital.

Here is the exact math used:

ATR Calculation: Contracts = Max Risk / Risk Per Contract

⚙️ Settings

You can fully customize the behavior of the risk manager via the settings panel:

Risk Management

-Max Risk per Trade ($): The maximum amount of USD you are willing to lose on a single trade.

Volatility Thresholds (ATR)

-ATR Length: The lookback period for volatility calculation.

-Upper Limit for LOW Volatility: If ATR is below this number, the market is "Low Volatility."

-Lower Limit for HIGH Volatility: If ATR is above this number, the market is "High Volatility." (Anything between Low and High is considered "Normal").

Stop Loss Settings (Points)

-SL for Low/Normal/High: Define how wide your stop loss should be in points for each of the three market states.

Visual Settings

-Color Theme: Switch between Light and Dark modes.

-Panel Position: Move the dashboard to any corner or center of your chart.

-Panel Size: Adjust the scale (Tiny to Large) to fit your screen resolution.

📊 Dashboard Overview

-The on-screen panel provides a quick-glance summary for live execution:

-Market State: Color-coded status (Green = Low Vol, Orange = Normal, Red = High Vol).

-Current ATR: The live volatility reading.

-Suggested SL: The Stop Loss size you should enter in your execution platform.

-CONTRACTS: The calculated position size.

-Est. Loss: The actual dollar amount you will lose if the stop is hit (usually slightly less than your Max Risk due to rounding down).

Who is this for?

-Discretionary and systematic futures traders on MNQ (/MNQ or MES also works with small adjustments)

-Anyone who wants perfect risk consistency regardless of whether the market is asleep or exploding

-Traders who hate manual position-size calculations on every trade

No repainting

Works on any timeframe

Real-time updates on every bar

Overlay indicator (no signals, pure risk-management tool)

⚠️ Disclaimer

This tool is for informational and educational purposes only. It calculates mathematical position sizes based on user inputs. It does not execute trades, nor does it guarantee profits. Past performance (volatility) is not indicative of future results. Always manually verify your order size before executing trades on your broker platform.

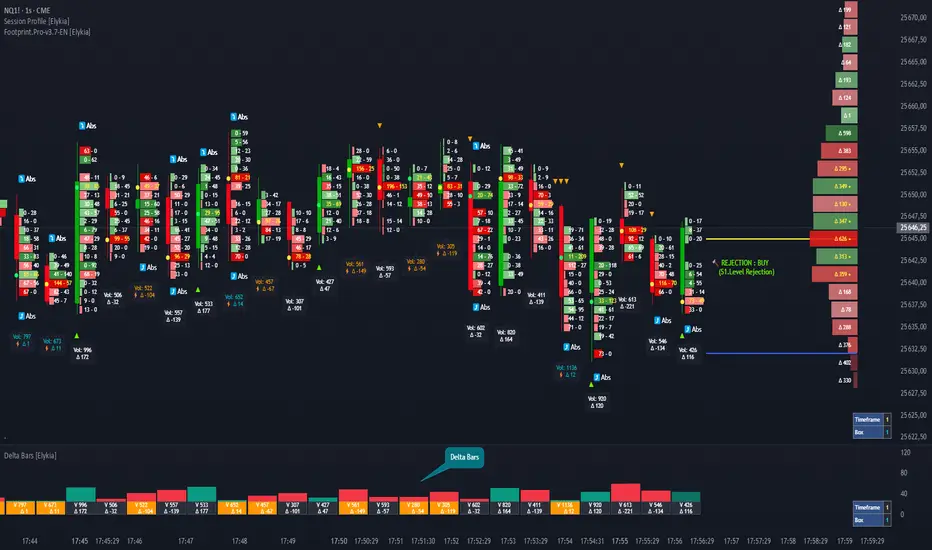

Delta Bars [Elykia]Delta Bars — Order Flow & Momentum Analysis

Description:

Delta Bars is an "Order Flow Oscillator" designed to instantly visualize buyer and seller aggression within every price move.

Unlike standard volume, it breaks down what is happening "under the hood" (Delta) and offers a clear reading of market reversals thanks to intelligent divergence detection.

🔥 Key Features:

1. Dual Calculation Mode:

Timeframe Mode: Displays classic Delta based on time (e.g., 1min, 5min).

Range Bars Mode: (Exclusive) Builds Delta bars based on price movement (volatility) rather than time. This filters out noise during consolidation periods and reveals true strength during impulses.

2. 🧠 Smart Auto-Detection (Plug & Play):

No need to manually calculate "Box" or "Tick" sizes for each asset. The indicator automatically recognizes the asset you are trading and applies the optimal institutional calibration:

US Indices (NQ, ES, YM...)

Forex (EURUSD, JPY...)

Crypto (BTC, ETH)

Commodities (Gold, Oil)

Note: You can still switch to manual mode if needed.

3. "Flip" Detection (Divergences) ⚡:

The indicator automatically identifies anomalies between price and Delta:

If the candle closes Green but Delta is Negative (Absorption/Failed Selling Effort).

If the candle closes Red but Delta is Positive.

These situations are marked with a ⚡ symbol and a specific highlight color (Orange by default), often signaling an imminent reversal.

4. Technical Dashboard:

A discreet panel displays the current mode and "Box" size (in ticks/points) in real-time, ensuring you always know how the data is being filtered.

How to read the signals?

1. Green/Red Bars: They indicate Net Delta (the difference between buying and selling volume). A tall bar implies strong conviction.

2. The ⚡ Symbol (The Flip): This is the most critical signal. It appears when Delta contradicts the candle direction (e.g., Positive Delta on a Bearish candle). This indicates Absorption (passive orders blocking the move) and often precedes a reversal.

3. Range Bars Mode: Use this mode to "smooth out" the market. If the market is choppy, Range Bars will filter the noise and only draw a new bar if the price actually moves.

⚠️ Important: Replay Mode

Since this indicator performs heavy calculations (simulated tick-by-tick), it includes a safety feature for Replay Mode.

To use Replay: Go to settings and set the "Force Replay Date" to a date close to your starting point. This ensures maximum fluidity and avoids TradingView limit errors.

Configuration:

Works on all timeframes but excels on seconds charts (1s, 5s) or fast minute charts (1m) for scalping.

KIMATIX VWAP/EMA System (by ASCE)**KIMATIX VWAP/EMA System (by ASCE)**

A precision-built intraday framework for momentum, structure, and liquidity timing.

**Why this indicator exists**

Most traders see movement, but not context. They enter too late, chase momentum, or fade reversals without understanding where institutional players react.

This tool solves that problem by combining two of the most powerful structural concepts in intraday price discovery:

Trend alignment through EMAs

Liquidity reaction zones through VWAPs

Together, they provide directional clarity, timing, and trade location.

**Core Components**

**Three Trend EMAs**

• **EMA 7** – Microtrend and momentum speed

• **EMA 23** – Intraday trend leadership

• **EMA 50** – Higher-timeframe structure anchor

This trio shows how price accelerates, slows, flips bias, or compresses.

**Three Volume-Weighted Average Prices**

• **Daily VWAP** – Primary scalper reference point

• **Weekly VWAP** – Bias filter and intermediate balance zone

• **Monthly VWAP** – High-impact “magnet” where major reactions occur

VWAP represents the fair value where volume is distributed.

When price taps, rejects, or reclaims these levels, liquidity flow shifts — ideal for scalp-to-swing entries.

**What it helps you see**

• When price is aligned with or diverging from trend

• Where momentum will expand or fail

• Which levels larger participants defend

• Where the highest-probability reaction zones form

This is not a signal tool — it is a structure and decision-making framework used by professional intraday traders.

**How to use it**

1. **Trade with VWAP alignment** – expect reactions at daily/weekly/monthly VWAPs

2. **Follow EMA flow** – when EMAs compress or flip, momentum changes

3. **Look for price interaction** – rejection, reclaim, or breakthrough of a VWAP often leads to fast moves

Ideal for scalping, day-trading, futures, FX, indices, crypto, and metals.

**Customization**

Colors for each EMA and each VWAP can be personalized, allowing alignment with your charting workflow.

**Final Notes**

This system gives you the *context* most traders miss — where trend meets liquidity.

Use it as a roadmap to understand where price *should* react and when momentum is likely to shift.

UDL Matrix: MTF Divergence System [WangBlack]【使用說明 / How to Use】

多頭訊號 (Long Signal):出現綠色「多」標籤。

條件:UDL 進入超賣區 + K線出現反轉型態 + 趨勢過濾通過。

空頭訊號 (Short Signal):出現紅色「空」標籤。

條件:UDL 進入超買區 + K線出現反轉型態 + 趨勢過濾通過。

背離線 (Divergence Lines):

綠色實線:底背離(看漲)。

紅色實線:頂背離(看跌)。

背景色 (Background):

綠色背景:HTF(大級別)處於低位,適合做多。

紅色背景:HTF(大級別)處於高位,適合做空。

【適用市場】 加密貨幣、外匯(黃金 XAUUSD)、指數期貨。適合 1分/5分/15分/1小時 級別操作。

Here is the English translation for the "How to Use" section, optimized for TradingView descriptions:

【How to Use】

Long Signal:

Indicator: A Green label with the text "多" (Long) appears.

Conditions: UDL enters the Oversold zone + Candlestick Reversal Pattern detected + Trend Filter validation passed.

Short Signal:

Indicator: A Red label with the text "空" (Short) appears.

Conditions: UDL enters the Overbought zone + Candlestick Reversal Pattern detected + Trend Filter validation passed.

Divergence Lines:

Green Solid Line: Regular Bullish Divergence (Signal to Buy).

Red Solid Line: Regular Bearish Divergence (Signal to Sell).

Background Color (HTF Context):

Green Background: HTF (Higher Timeframe) is in a low zone; favorable for Long positions.

Red Background: HTF (Higher Timeframe) is in a high zone; favorable for Short positions.

【Applicable Markets】 Cryptocurrencies, Forex (specifically Gold/XAUUSD), and Index Futures. Recommended Timeframes: 1-minute, 5-minute, 15-minute, and 1-hour charts.

Volume profilerMulti-Range Volume Analysis & Absorption Detection

This tool visualises market activity through multi-range volume profiling and absorption signal detection. It helps you quickly identify where volume expands, compresses, or diverges from expected behaviour.

What it does

Volume Profiler plots four volume EMAs (short / mid / long / longer) so you can gauge how current volume compares to different market regimes.

It also highlights structural volume extremes:

• Low-volume bars (liquidity withdrawal)

These are potential signs of exhaustion, pauses, or low liquidity environments.

• High-volume + Low-range absorption

A classic footprint-style signal where aggressive volume fails to move price.

Often seen during:

absorption of one side of the book

liquidity collection

failed breakouts

institutional accumulation/distribution

You can choose:

which EMA defines “high volume”

how to measure candle range (High-Low, True Range, or Body)

how to define baseline volatility (ATR or average range)

Alerts are included so you can monitor absorption automatically.

Features

Multi-range volume EMAs (10 / 50 / 100 / 300 by default)

Low-volume bar flags

Absorption detection based on custom thresholds

Customisable volatility baseline

Optional bar colouring

Labels displayed directly in the volume pane

Alert conditions for absorption events

How to use

This indicator is valuable for:

confirming trend strength or weakness

detecting absorption before reversal or breakout continuation

finding low-liquidity pauses

identifying volume expansion across different time horizons

footprint-style behavioural confirmation without needing order-flow data

Works across all markets and timeframes.

Notes

This script is intended for educational and analytical use.

It does not repaint.

Market Session Clock# Market Session Clock - Real-Time Global Trading Hours

A professional, real-time dashboard that displays the current time and trading status across major global financial markets. Perfect for forex, futures, and stock traders who need to track multiple market sessions simultaneously.

## Key Features

**Live Market Status Tracking**

- Visual color-coded indicators show which markets are currently open (green) or closed (red)

- Automatic weekend detection - all markets show as closed on Saturdays and Sundays

- Real-time clock updates with optional seconds display

**Major Global Markets Covered**

- Tokyo (Asian Session)

- Hong Kong (Asian Session)

- Frankfurt (European Session)

- London (European Session)

- New York (American Session)

- Your Local Time (optional)

**Highly Customizable**

*Display Options:*

- Choose dashboard position (Top Left/Right, Bottom Left/Right)

- Toggle seconds display on/off

- Show/hide your local time

- Three size options: Compact, Normal, Large

*Timezone Settings:*

- Select your local timezone from 40+ global options

- Customize market opening and closing hours for each session

*Professional Styling:*

- Fully customizable color scheme

- Adjustable background, text, header, border colors

- Custom colors for open and closed sessions

- Clean, modern interface that won't clutter your charts

## How It Works

The indicator uses TradingView's `timenow` function to display live, continuously updating times for each market. Session status automatically updates based on the current hour in each timezone, factoring in weekends when markets are closed.

## Use Cases

- **Multi-Market Trading**: Track overlapping sessions for increased volatility opportunities

- **Forex Trading**: Know exactly when major currency pairs are most active

- **Global Portfolio Management**: Monitor when different exchanges are open

- **Session-Based Strategies**: Time your entries and exits around specific market opens/closes

## Default Session Hours

- Tokyo: 9:00 - 18:00 JST

- Hong Kong: 9:00 - 17:00 HKT

- Frankfurt: 8:00 - 17:00 CET

- London: 8:00 - 17:00 GMT

- New York: 8:00 - 17:00 EST

All session times can be adjusted to match your preferred trading hours or specific market schedules.

---

*Note: This indicator is for informational purposes only. Market hours may vary due to holidays and special trading days. Always verify with official exchange schedules.*

ASFX - Automatic VWAPs & Key LevelsAutomate your AVWAPs and key levels for day trading! NY Market open VWAP, Previous day NY VWAP, and more are included. Inital Balance and Opening Range are also automated.

Value Charts by Mark Helweg1. Introduction

This script is a simplified implementation of the Value Charts concept introduced by Mark Helweg and David Stendahl in their work on “Dynamic Trading Indicators”. It converts raw price into value units by normalizing distance from a dynamic fair‑value line, making it easier to see when price is relatively overvalued or undervalued across different markets and timeframes. The code focuses on plotting Value Chart candlesticks and clean visual bands, keeping the logic close to the original idea while remaining lightweight for intraday and swing trading.

2. Key Features

- Dynamic fair‑value axis

Uses a moving average of the chosen price source as the fair‑value line and a volatility‑based deviation (smoothed True Range) to scale all price moves into comparable value units.

- Normalized Value Chart candlesticks

OHLC prices are transformed into value units and displayed as a dedicated candlestick panel, visually similar to standard candles but detached from raw price, highlighting relative extremes instead of absolute levels.

- Custom upper and lower visual limits

User‑defined upper and lower bands frame the majority of action and emphasize extreme value zones, helping the trader spot potential exhaustion or mean‑reversion conditions at a glance.

- Clean, publishing‑friendly layout

Only the normalized candles and three simple reference lines (top, bottom, zero) are plotted, keeping the chart uncluttered and compliant with presentation standards for published scripts.

3. How to Use

1. Attach the indicator to a separate pane (overlay = false) on any market and timeframe you trade.

2. Set the “Period (Value Chart)” to control how fast the fair‑value line adapts: shorter values react more quickly, longer values smooth more.

3. Adjust the “Volatility Factor” so that most candles stay between the upper and lower limits, with only true extremes touching or exceeding them.

4. Use the Value Chart candlesticks as a relative overbought/oversold tool:

- Candles pressing into the Top band suggest overvalued conditions and potential for pullbacks or reversions.

- Candles pressing into the Bottom band suggest undervalued conditions and potential for bounces.

5. Combine the signals with your existing price‑action, volume, or trend‑filter rules on the main chart; the Value Chart panel is designed as a context and timing tool, not a standalone trading system.

Combined: Net Volume, RSI & ATR# Combined: Net Volume, RSI & ATR Indicator

## Overview

This custom TradingView indicator overlays **Net Volume** and **RSI (Relative Strength Index)** on the same chart panel, with RSI scaled to match the visual range of volume spikes. It also displays **ATR (Average True Range)** values in a table.

## Key Features

### Net Volume

- Calculates buying vs selling pressure by analyzing lower timeframe data

- Displays as a **yellow line** centered around zero

- Automatically selects optimal timeframe or allows manual override

- Shows net buying pressure (positive values) and selling pressure (negative values)

### RSI (Relative Strength Index)

- Traditional 14-period RSI displayed as a **blue line**

- **Overlays directly on the volume chart** - scaled to match volume spike heights

- Includes **70/30 overbought/oversold levels** (shown as dotted red/green lines)

- Adjustable scale factor to fine-tune visual sizing relative to volume

- Optional **smoothing** with multiple moving average types (SMA, EMA, RMA, WMA, VWMA)

- Optional **Bollinger Bands** around RSI smoothing line

- **Divergence detection** - identifies regular bullish/bearish divergences with labels

### ATR (Average True Range)

- Displays current ATR value in a **table at top-right corner**

- Configurable period length (default: 50)

- Multiple smoothing methods: RMA, SMA, EMA, or WMA

- Helps assess current market volatility

## Use Cases

- **Momentum & Volume Confirmation**: See if RSI trends align with net volume flows

- **Divergence Trading**: Automatically spots when price makes new highs/lows but RSI doesn't

- **Volatility Assessment**: Monitor ATR for position sizing and stop-loss placement

- **Overbought/Oversold + Volume**: Identify exhaustion when RSI hits extremes with volume spikes

## Customization

All components can be toggled on/off independently. RSI scale factor allows you to adjust how prominent the RSI line appears relative to volume bars.

VIX Termstructure Indicator (Overlay)This indicator visualizes the VIX futures term structure directly on your chart background and highlights three key volatility regimes using color coding. It helps identify when the volatility curve is in normal contango, inverted (backwardation), or undergoing a curve flip between the front-month VIX futures.

What the indicator does

The script pulls and compares:

VIX spot index: VIX

Front-month VIX futures: VX1!

Second-month VIX futures: VX2!

All data is requested on the daily timeframe and used to classify the current volatility environment. The indicator then colors the background of your chart according to the detected VIX term structure:

Green background – Contango:

VIX spot is below the front-month futures (VIX < VX1!).

This is typically associated with more “normal” market conditions and lower perceived short-term stress.

Red background – Inverted curve (Backwardation):

VIX spot is above the front-month futures (VIX > VX1!).

This often signals elevated fear, stress, or risk-off conditions in the market.

Yellow background – Curve flip between VX1! and VX2!:

The front-month futures are trading above the second-month futures (VX1! > VX2!).

This can indicate a transition phase in the volatility term structure and may precede or accompany shifts in market sentiment.

How it works

The script fetches the daily close values of VIX, VX1!, and VX2!. It checks whether the front-month futures are above the second-month futures to detect a curve flip. It compares VIX with VX1! to determine if the curve is contango or inverted. Based on these conditions, the chart background is colored with a semi-transparent overlay:

Red has priority when VIX is above VX1! (inverted curve).

If not inverted, yellow is shown when a curve flip VX1! > VX2! is detected.

Otherwise, the background is green (normal contango).

Use cases

This overlay is designed as a context tool for indices, ETFs, Options, or individual stocks that are sensitive to volatility and risk sentiment. Typical applications include:

Identifying periods of heightened risk (red / inverted curve) to adjust position sizing or risk exposure.

Confirming risk-on environments (green / contango) where volatility is more contained.

Monitoring yellow curve-flip phases as potential early warnings of changing volatility regimes.

The indicator does not generate buy/sell signals on its own, but it can be a valuable regime filter or confirmation layer alongside other technical tools.

Notes

This is an overlay indicator: it colors the background of your active chart.

All VIX-related data is evaluated on the daily timeframe, regardless of the chart timeframe.

Make sure that the symbols VIX, VX1!, and VX2! are available on your broker/data feed in TradingView.

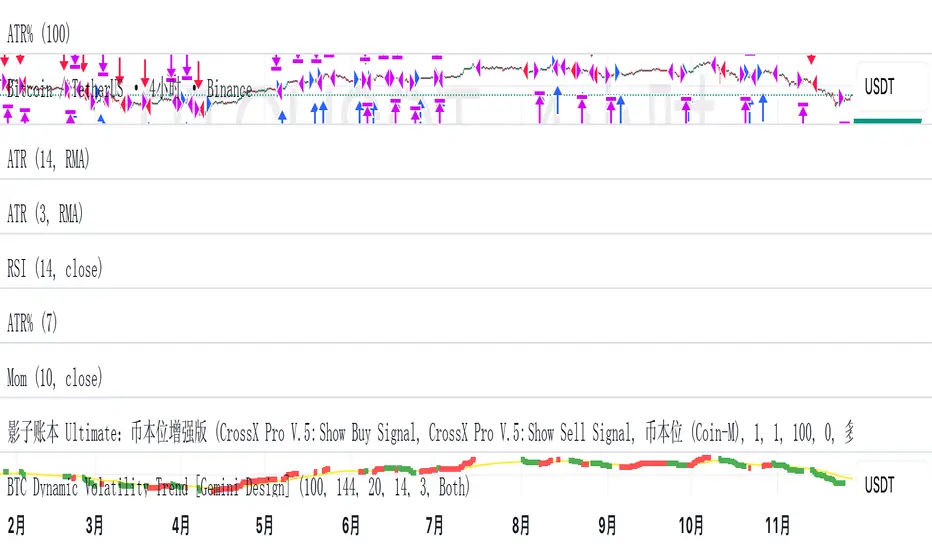

BTC Dynamic Volatility Trend Backtested from 2017 to present, this strategy has delivered a staggering 7100%+ cumulative return. It doesn't just track the market; it dominates it. By capturing major trends and strictly limiting drawdowns, it has significantly outperformed the standard 'Buy & Hold' BTC strategy, proving its ability to generate massive alpha across multiple bull and bear cycles.

自 2017 年至今,本策略实现了惊人的 7100%+ 累计收益率。它不仅仅是跟随市场,更是超越了市场。通过精准捕捉主升浪并严格控制回撤,该策略在穿越多轮牛熊周期后,大幅度跑赢了比特币‘买入持有’(Buy & Hold)的基准收益,展现了极致的阿尔法(Alpha)捕捉能力。"

Introduction :Simplicity is the ultimate sophistication. This strategy is designed specifically for Bitcoin (BTC), capturing its unique characteristics: high volatility, frequent fakeouts, and massive trend persistence. It abandons complex indicators in favor of a robust logic: "Follow the Trend, Filter the Noise, Let Profits Run."

Core Logic

Trend Filter (Fibonacci EMA 144): We use the 144-period Exponential Moving Average as the baseline. Longs are only taken above this line, and shorts only below. This keeps you on the right side of the major trend.

Volatility Breakout (Donchian Channel 20): Entries are triggered only when price breaks the 20-day high (for longs) or low (for shorts). This confirms momentum and avoids trading in chop.

Dynamic Risk Management (ATR Chandelier Exit):

Instead of fixed % stops, we use Average True Range (ATR) to calculate stop losses.

The Ratchet Mechanism: The stop loss moves up with the price but never moves down (for longs). This locks in profits automatically as the trend develops and exits immediately when volatility turns against you.

Why Use This Strategy?

Zero Repainting: All signals are confirmed.

No Curve Fitting: Uses classic parameters (144, 20) that have worked for decades.

Mental Peace: The strategy handles the exit. You don't need to guess where to sell. It holds through minor corrections and exits only when the trend truly reverses.

Settings

Leverage %: Adjust your position size based on equity (default 100% = 1x).

Timeframe: Recommended for 4H charts.

中文版 (Chinese Version)

简介 :大道至简。本策略专为 比特币 (BTC) 设计,针对其高波动、假突破多但趋势爆发力强的特点,摒弃了复杂的过度拟合指标,回归交易本质:“顺大势,滤噪音,截断亏损,让利润奔跑”。

核心逻辑

趋势过滤器 (斐波那契 EMA 144): 使用 144 周期指数移动平均线作为多空分水岭。价格在均线之上只做多,之下只做空。这能有效过滤掉大部分震荡市的噪音。

波动率突破 (唐奇安通道 20): 只有当价格突破过去 20 根 K 线的最高价(做多)或最低价(做空)时才进场。这确保了我们只在趋势确立的瞬间入场。

动态风控 (ATR 吊灯止损):

拒绝固定点数止损,使用 ATR(平均真实波幅)根据市场热度动态计算安全距离。

棘轮机制: 止损线会跟随价格上涨而上移,但绝不会下移(做多时)。这实现了自动化的“利润锁定”,既能扛住正常的波动回调,又能在大势反转时果断离场。

策略优势

绝不重绘: 所有信号均为收盘确认或实时触价。

拒绝拟合: 使用经过数十年市场验证的经典参数组合。

心态管理: 策略全自动管理出场。你不需要纠结何时止盈,它会帮你吃到完整的鱼身,直到趋势结束。

使用建议

资金管理: 可通过参数调整仓位占比(默认 100% = 1倍杠杆)。

推荐周期: 建议在4小时 图表上运行效果最佳。

LiquidTradeRoom Auto Zones1. Finds Swing Highs and Swing Lows

It looks for pivot highs and lows using a user-chosen length.

Swing highs = possible supply

Swing lows = possible demand

These swings help the indicator understand the market structure.

2. Automatically Creates Supply & Demand Zones

When a new swing high or low is found:

🔴 Supply zone (after a swing high)

Draws a box above price

Slight buffer added using ATR

Extends the box forward to the right

🔵 Demand zone (after a swing low)

Draws a box below price

ATR buffer

Extends the box to the right

The boxes act as “areas price may react from.”

3. Stops Overlapping Zones

Before creating a new zone, the script checks:

If the new zone is too close to an existing one → it does not draw it.

This avoids clutter & duplicate zones.

4. Draws POI Labels

Within each supply/demand box it draws a small “POI” label showing the midpoint.

This marks the "most important part" of the zone.

5. Marks BOS (Break of Structure) Automatically

If price breaks above a supply zone top or below a demand zone bottom, the indicator:

Converts that zone into a BOS marker

Draws a line showing where structure was broken

Removes the old supply/demand box

This helps identify trend changes.

6. Extends Active Zones

Existing zones are constantly pushed further right so they stay visible on the chart.

7. Optional Zig-Zag

The script can draw a zig-zag line to help visualize:

Higher highs

Higher lows

Lower highs

Lower lows

But you can turn it on or off.

8. Optional Swing Labels

If enabled, it prints:

HH (Higher High)

HL (Higher Low)

LH (Lower High)

LL (Lower Low)

This visually shows market structure.

✨ In summary

This script automatically builds a full “Smart Money Concepts” structure map including:

✔ Swing points

✔ Supply & demand zones

✔ POIs

✔ Break of structure (BOS)

✔ Zig-zag structure

✔ Market structure labels (HH, HL, LH, LL)

Options Fusion Core - Lite v6Options Fusion Core – Lite v6

A dual-engine oscillator designed to provide clear, confidence-driven market reads. OFC – Lite v6 combines two high-signal components into a single 0–100 panel to help traders interpret momentum strength and liquidity flow at a glance.

Core Components

Momentum Engine (Solid Line)

Above 50: Bullish bias (green shades)

Below 50: Bearish bias (red shades)

Near 20 or 80: Potential exhaustion zones where trends may pause or reverse

Liquidity Gauge (Dotted Line)

Above 55: Strong buying pressure

Below 45: Selling pressure

Around 50: Neutral flow

How to Use (Educational Purpose Only)

Alignment Signals: Watch for Momentum Engine and Liquidity Gauge moving in the same direction.

Example: Momentum >50 and Liquidity >55 → constructive environment

Example: Momentum <50 and Liquidity <45 → weakening conditions

Extremes: Momentum near 20 or 80 indicates potential trend exhaustion. Paired with strong Liquidity changes, these zones may highlight possible reversals or pauses.

Neutral Line (50): Many false moves occur around 50. Wait for a clear break above or below before interpreting as a signal.

Use in Context: Combine with price action, volume, or other indicators for confirmation.

User Inputs

Fast Momentum Length — controls how quickly Momentum reacts

VFI Length — smooths the Liquidity Gauge

VFI Cutoff — adjusts sensitivity to flow spikes

Lite Version:

Oscillator panel only

No automated signals or multi-ticker table

Educational and visualization purposes only

Important Notice

This script is educational and informational only. Not trading, financial, or investment advice.

Calculations are proprietary and protected to safeguard intellectual property.

No repainting; all results reflect real-time calculation.

Gamma Conviction Oscillator LiteGamma Conviction Oscillator Lite

A volume-weighted momentum oscillator designed to help traders visualize conviction in gamma-heavy instruments (SPY, TSLA, NVDA, MSTR, COIN, HOOD, etc.). This LITE edition is fully functional and educational, focusing on reading market momentum without offering trading signals.

Core Features (LITE Version):

Dynamic oscillator panel with volatility-adjusted overbought/oversold levels

Long-term trend filter: 200-period moving average selectable as SMA, EMA, or HMA

Conviction-based coloring system:

Bright Lime → high-conviction oversold (price above long-term MA)

Bright Red → high-conviction overbought (price below long-term MA)

Teal / Maroon → low-conviction extremes (counter-trend)

User Inputs:

Base Oscillator Length, Volatility Smoothing Length, and Sensitivity Factor are adjustable in Settings → Inputs

Long-Term Trend Length and MA Type are selectable for trend confirmation

How to Read Signals (Educational Use Only):

Oscillator Level: Observe the main VWPS line relative to overbought/oversold levels:

Above the red overbought line → price may be stretched

Below the green oversold line → price may be compressed

Trend Context: Compare the oscillator reading to the long-term MA:

Oscillator above oversold + price above MA → potential bullish conviction

Oscillator below overbought + price below MA → potential bearish conviction

Color Coding: The line color communicates conviction strength and trend alignment:

Bright Lime / Bright Red indicate strong alignment with trend extremes

Teal / Maroon indicate weaker, counter-trend extremes

Use the oscillator in conjunction with your own analysis; consider confirming with price action, volume, or other indicators.

LITE Version:

Oscillator panel only

No divergence detection

No multi-ticker gamma table

Important Notice:

This script is educational and informational only. Not trading, financial, or investment advice.

All calculations are proprietary and protected to preserve intellectual property.

No repainting: results reflect real-time calculations.

Source Code:

This script is published as protected/closed-source to safeguard GammaBulldog intellectual property.

Setup Keltner Banda 3 e 5 - MMS

⚙️ How It Works:

• Calculates a 20-period Simple Moving Average (SMA) as the central line.

• Uses the ATR (Average True Range) to build two volatility bands:

o 3x ATR Band (more sensitive)

o 5x ATR Band (more extreme)

• Detects potential reversals when the price closes outside a band and then re-enters it.

🔍 Signals Generated:

• 🔻 Bearish Reversal: Price re-enters from above the upper band.

• 🔺 Bullish Reversal: Price re-enters from below the lower band.

• Signals are displayed with colored arrows on the chart for easy visual recognition.

🔔 Alerts:

The script also triggers automatic alerts for each type of reversal, so you can be notified in real time.

🧱 Ideal For:

• Traders using Renko, Range, or traditional candlestick charts

• Scalping or swing trading strategies

• Anyone looking for visual confirmation of price exhaustion and potential reversals