Polynomial Regression Keltner Channel [ChartPrime]Polynomial Regression Keltner Channel

⯁ OVERVIEW

The Polynomial Regression Keltner Channel [ ChartPrime ] indicator is an advanced technical analysis tool that combines polynomial regression with dynamic Keltner Channels. This indicator provides traders with a sophisticated method for trend analysis, volatility assessment, and identifying potential overbought and oversold conditions.

◆ KEY FEATURES

Polynomial Regression: Uses polynomial regression for trend analysis and channel basis calculation.

Dynamic Keltner Channels: Implements Keltner Channels with adaptive volatility-based bands.

Overbought/Oversold Detection: Provides visual cues for potential overbought and oversold market conditions.

Trend Identification: Offers clear trend direction signals and change indicators.

Multiple Band Levels: Displays four levels of upper and lower bands for detailed market structure analysis.

Customizable Visualization: Allows toggling of additional indicator lines and signals for enhanced chart analysis.

◆ FUNCTIONALITY DETAILS

⬥ Polynomial Regression Calculation:

Implements a custom polynomial regression function for trend analysis.

Serves as the basis for the Keltner Channel, providing a smoothed centerline.

//@function Calculates polynomial regression

//@param src (series float) Source price series

//@param length (int) Lookback period

//@returns (float) Polynomial regression value for the current bar

polynomial_regression(src, length) =>

sumX = 0.0

sumY = 0.0

sumXY = 0.0

sumX2 = 0.0

sumX3 = 0.0

sumX4 = 0.0

sumX2Y = 0.0

n = float(length)

for i = 0 to n - 1

x = float(i)

y = src

sumX += x

sumY += y

sumXY += x * y

sumX2 += x * x

sumX3 += x * x * x

sumX4 += x * x * x * x

sumX2Y += x * x * y

slope = (n * sumXY - sumX * sumY) / (n * sumX2 - sumX * sumX)

intercept = (sumY - slope * sumX) / n

n - 1 * slope + intercept

⬥ Dynamic Keltner Channel Bands:

Calculates ATR-based volatility for dynamic band width adjustment.

Uses a base multiplier and adaptive volatility factor for flexible band calculation.

Generates four levels of upper and lower bands for detailed market structure analysis.

atr = ta.atr(length)

atr_sma = ta.sma(atr, 10)

// Calculate Keltner Channel Bands

dynamicMultiplier = (1 + (atr / atr_sma)) * baseATRMultiplier

volatility_basis = (1 + (atr / atr_sma)) * dynamicMultiplier * atr

⬥ Overbought/Oversold Indicator line and Trend Line:

Calculates an OB/OS value based on the price position relative to the innermost bands.

Provides visual representation through color gradients and optional signal markers.

Determines trend direction based on the polynomial regression line movement.

Generates signals for trend changes, overbought/oversold conditions, and band crossovers.

◆ USAGE

Trend Analysis: Use the color and direction of the basis line to identify overall trend direction.

Volatility Assessment: The width and expansion/contraction of the bands indicate market volatility.

Support/Resistance Levels: Multiple band levels can serve as potential support and resistance areas.

Overbought/Oversold Trading: Utilize OB/OS signals for potential reversal or pullback trades.

Breakout Detection: Monitor price crossovers of the outermost bands for potential breakout trades.

⯁ USER INPUTS

Length: Sets the lookback period for calculations (default: 100).

Source: Defines the price data used for calculations (default: HLC3).

Base ATR Multiplier: Adjusts the base width of the Keltner Channels (default: 0.1).

Indicator Lines: Toggle to show additional indicator lines and signals (default: false).

⯁ TECHNICAL NOTES

Implements a custom polynomial regression function for efficient trend calculation.

Uses dynamic ATR-based volatility adjustment for adaptive channel width.

Employs color gradients and opacity levels for intuitive visual representation of market conditions.

Utilizes Pine Script's plotchar function for efficient rendering of signals and heatmaps.

The Polynomial Regression Keltner Channel indicator offers traders a sophisticated tool for trend analysis, volatility assessment, and trade signal generation. By combining polynomial regression with dynamic Keltner Channels, it provides a comprehensive view of market structure and potential trading opportunities. The indicator's adaptability to different market conditions and its customizable nature make it suitable for various trading styles and timeframes.

Bands

Linear Regression ChannelLinear Regression Channel with Logarithmic Scale Option

This advanced Linear Regression Channel indicator offers traders a powerful tool for technical analysis, with unique features that set it apart from standard implementations.

Key Features:

Logarithmic Scale Option: One of the most distinctive aspects of this indicator is the ability to switch between classic and logarithmic scales. This feature is particularly valuable for long-term analysis, as it ensures that equal percentage changes are represented equally, regardless of the price level.

Flexible Start Date: Unlike many indicators that rely on a fixed number of periods, this tool allows users to set a specific start date and time. This feature provides precise control over the regression analysis timeframe, enhancing its adaptability to various trading strategies.

Customizable Channel Settings: Users can adjust the upper and lower deviation multipliers, allowing for fine-tuning of the channel width to suit different market conditions and trading styles.

Trend Strength Indicator: An optional feature that displays the strength of the trend based on the Pearson correlation coefficient, offering additional insight into the reliability of the current trend.

Comprehensive Visual Customization: The indicator offers extensive color and style options for the regression line, upper and lower channel lines, and fill areas, allowing traders to create a visually appealing and easy-to-read chart setup.

Extended Line Options: Users can choose to extend the regression lines to the left, right, or both, facilitating projection and analysis of future price movements.

Multiple Alert Conditions: The indicator includes four alert conditions for crossing the upper deviation, lower deviation, and the main regression line in both directions, enhancing its utility for active traders.

Why Choose This Indicator:

The combination of logarithmic scale option and flexible start date setting makes this Linear Regression Channel uniquely suited for both short-term and long-term analysis. The logarithmic scale is particularly beneficial for analyzing assets with significant price changes over time, as it normalizes percentage moves across different price levels. This feature, coupled with the ability to set a precise start date, allows traders to perform more accurate and relevant regression analyses, especially when studying specific market cycles or events.

Moreover, the trend strength indicator and customizable visual elements provide traders with a comprehensive tool that not only identifies potential support and resistance levels but also offers insight into the reliability and strength of the current trend.

In summary, this Linear Regression Channel indicator combines flexibility, precision, and insightful analytics, making it an invaluable tool for traders seeking to enhance their technical analysis capabilities on TradingView.

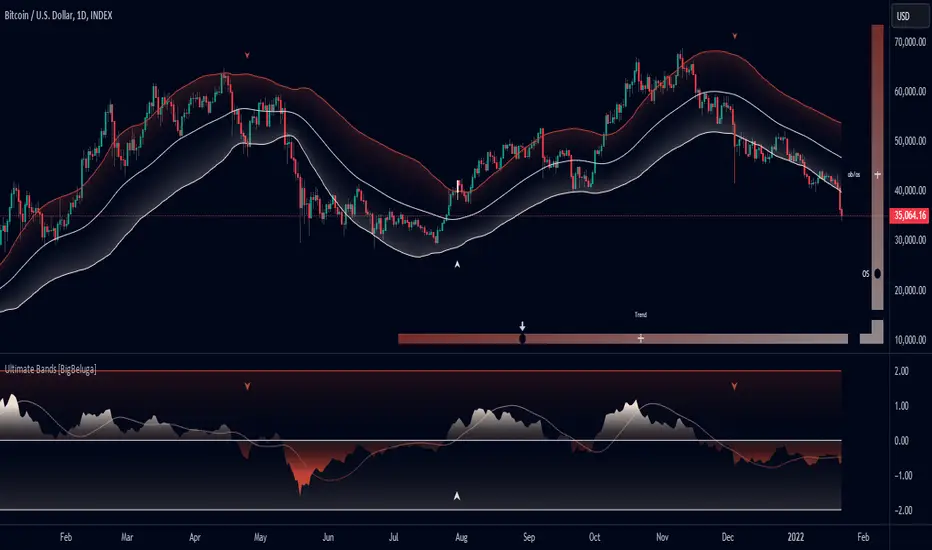

Ultimate Bands [BigBeluga]Ultimate Bands

The Ultimate Bands indicator is an advanced technical analysis tool that combines elements of volatility bands, oscillators, and trend analysis. It provides traders with a comprehensive view of market conditions, including trend direction, momentum, and potential reversal points.

🔵 KEY FEATURES

● Ultimate Bands

Consists of an upper band, lower band, and a smooth middle line

Based on John Ehler's SuperSmoother algorithm for reduced lag

Bands are calculated using Root Mean Square Deviation (RMSD) for adaptive volatility measurement

Helps identify potential support and resistance levels

● Ultimate Oscillator

Derived from the price position relative to the Ultimate Bands

Oscillates between overbought and oversold levels

Provides insights into potential reversals and trend strength

● Trend Signal Line

Based on a Hull Moving Average (HMA) of the Ultimate Oscillator

Helps identify the overall trend direction

Color-coded for easy trend interpretation

● Heatmap Visualization

Displays the current state of the oscillator and trend signal

Provides an intuitive visual representation of market conditions

Shows overbought/oversold status and trend direction at a glance

● Breakout Signals

Optional feature to detect and display breakouts beyond the Ultimate Bands

Helps identify potential trend reversals or continuations

Visualized with arrows on the chart and color-coded candles

🔵 HOW TO USE

● Trend Identification

Use the color and position of the Trend Signal Line to determine the overall market trend

Refer to the heatmap for a quick visual confirmation of trend direction

● Entry Signals

Look for price touches or breaks of the Ultimate Bands for potential entry points

Use oscillator extremes in conjunction with band touches for stronger signals

Consider breakout signals (if enabled) for trend-following entries

● Exit Signals

Use opposite band touches or breakouts as potential exit points

Monitor the oscillator for divergences or extreme readings as exit signals

● Overbought/Oversold Analysis

Use the Ultimate Oscillator and heatmap to identify overbought/oversold conditions

Look for potential reversals when the oscillator reaches extreme levels

● Confirmation

Combine Ultimate Bands, Oscillator, and Trend Signal for stronger trade confirmation

Use the heatmap for quick visual confirmation of market conditions

🔵 CUSTOMIZATION

The Ultimate Bands indicator offers several customization options:

Adjust the main calculation length for bands and oscillator

Modify the number of standard deviations for band calculation

Change the signal line length for trend analysis

Toggle the display of breakout signals and candle coloring

By fine-tuning these settings, traders can adapt the Ultimate Bands indicator to various market conditions and personal trading strategies.

The Ultimate Bands indicator provides a multi-faceted approach to market analysis, combining volatility-based bands, oscillator analysis, and trend identification in one comprehensive tool. Its adaptive nature and visual cues make it suitable for both novice and experienced traders across various timeframes and markets. The integration of multiple analytical elements offers traders a rich set of data points to inform their trading decisions.

TP RSITP RSI - Integrated Trend, Momentum, and Volatility Analyzer

The TP RSI indicator is an innovative 3-in-1 technical analysis tool that combines RSI, Bollinger Bands, and an EMA ribbon to provide traders with a comprehensive view of trend, momentum, and volatility in a single, easy-to-interpret visual display.

Why This Combination? This mashup addresses three critical aspects of market analysis simultaneously:

Trend identification and strength (EMA ribbon)

Momentum measurement (RSI)

Volatility assessment (Bollinger Bands)

By integrating these components, traders can make more informed decisions based on multiple factors without switching between different indicators.

How Components Work Together:

1. EMA Ribbon (Trend):

10 EMAs form 5 color-coded bands

Blue: Uptrend, Red: Downtrend

Provides a nuanced view of trend strength and potential reversals

2. RSI (Momentum):

Color-coded for quick interpretation

Blue: Upward momentum, Red: Downward momentum, White: Neutral

Position relative to the ribbon offers additional insight

3. Bollinger Bands (Volatility):

Applied to RSI for dynamic overbought/oversold levels

Narrow bands indicate low volatility, suggesting potential breakouts

Unique Aspects and Originality:

Synergistic visual cues: Color coordination between ribbon and RSI

Multi-factor confirmation: Requires alignment of trend, momentum, and volatility for strong signals

Volatility-adjusted momentum: RSI interpreted within the context of Bollinger Bands

How these components work together:

Buy Signal: Blue ribbon with blue RSI outside the ribbon.

Sell Signal: Red ribbon with red RSI outside the ribbon.

Neutral: White RSI or RSI inside the ribbon (not recommended for trading)

Increasing Momentum: RSI crossing above upper Bollinger Band (upward) or below lower Band (downward).

Trend Strength: RSI rejection by the ribbon, while all bands are colored along with the trend direction, identifies a strong trend.

Adaptive RSI BandsThe RSI Band Optimizer is an innovative technical analysis tool designed to identify and display the most effective Relative Strength Index (RSI) band values for any given trading instrument. This powerful indicator dynamically calculates optimal overbought and oversold levels, moving beyond the traditional static 70/30 or 80/20 bands.

Core Functionality:

Dynamic RSI Band Calculation:

The indicator analyzes historical price data to determine the most effective RSI levels for identifying overbought and oversold conditions specific to the current trading instrument and timeframe.

Adaptive Optimization:

Rather than relying on external factors, the tool uses a proprietary algorithm that focuses solely on the relationship between historical RSI values and subsequent price movements. This pure RSI-based approach ensures that the bands are optimized for the indicator's own dynamics.

Continuous Recalibration:

The optimal RSI bands are continuously recalculated as new price data becomes available, ensuring that the indicator adapts to changing market conditions and remains relevant over time.

Key Inputs:

RSI Length:

Allows users to set the period for the RSI calculation. While the default is typically 14, users can adjust this to suit their trading style and the characteristics of the instrument they're trading.

Optimization Lookback:

Defines the historical period the indicator uses to calculate optimal bands. This balance between recent market behavior and longer-term patterns.

Band Sensitivity:

Enables fine-tuning of how aggressively the indicator adjusts the RSI bands. Higher sensitivity results in more frequent band adjustments, while lower sensitivity provides more stable levels.

What Makes It Unique:

Self-Contained Optimization:

Unlike indicators that rely on external data sources or comparisons, this tool focuses purely on optimizing RSI bands based on the indicator's own historical performance.

Instrument-Specific Bands:

By calculating optimal bands for each specific instrument, the indicator acknowledges that different assets may have different typical RSI ranges and behaviors.

Timeframe Adaptability:

The optimization process adapts to the selected timeframe, recognizing that optimal RSI bands may differ between short-term and long-term charts.

Dynamic Band Adjustment:

The continuous recalibration of bands allows the indicator to adapt to changing market volatility and trends, providing more relevant signals over time.

Enhanced RSI Interpretation:

By providing optimized, asset-specific overbought and oversold levels, the indicator offers a more nuanced and potentially more accurate interpretation of RSI values.

The RSI Band Optimizer represents a significant advancement in the application of the Relative Strength Index. By dynamically calculating optimal band values, it addresses one of the main criticisms of traditional RSI usage – the reliance on static, one-size-fits-all overbought and oversold levels. This tool empowers traders to make more informed decisions based on RSI readings that are truly tailored to the specific characteristics of the asset they're trading.

Signals & Overlays [UAlgo]The Signals & Overlays indicator is a comprehensive trading tool designed to provide traders with a holistic view of market conditions. It combines multiple analysis techniques to offer insights into trend direction, potential reversal points, and optimal entry and exit levels. This versatile indicator is suitable for various trading styles and timeframes, also has Beginner-Friendly presets to enable multiple features at once within one-click.

🔶 Key Features:

🔹 Contrarian Signals:

This feature identifies potential trend reversals and market turning points. These contrarian signals are displayed as arrow markers on the chart, alerting traders to possible opportunities that go against the prevailing trend. The signals are based on a combination of price action, momentum, and volatility factors, providing a multi-faceted approach to market analysis.

Customizable Settings :

Signal Sensitivity: Adjustable from 0.1 to 10.0. This controls how sensitive the indicator is to potential reversal signals.

🔹 Reversal Zones:

This feature utilizes statistical methods that compute a smoothed average and associated bands around a data series using Gaussian weights. The Gaussian distribution helps to assign more weight to data points near the center of the window, and the bands represent the average plus/minus a scaled measure of deviation.

This technique is often used in financial analysis to detect trends and measure volatility to identify key areas where price reversals are more likely to occur. These zones providing a dynamic representation of potential support and resistance areas. Traders can use these zones to anticipate potential price reactions and plan their entries and exits accordingly.

Users can also customize the responsiveness of the Reversal Zones through the "Zone Speed" setting. This allows for fine-tuning the model's sensitivity to price changes:

Swift Mode: Quickly adapts to recent price movements, ideal for short-term trading.

Standard Mode: Balances recent and historical data for a medium-term perspective.

Slow Mode: Emphasizes longer-term trends, suitable for position trading.

Customizable Settings :

Zone Data Source: Users can select which price data (open, high, low, close, etc.) to use for zone calculations.

Zone Speed: Choosable between "Swift", "Standard", and "Slow", affecting how quickly the zones adapt to price changes.

🔹 Smart Trail:

The Smart Trail feature provides an adaptive trend-following mechanism. It plots a dynamic line that adjusts based on price action and volatility, helping traders stay in trending moves while providing a trailing stop-loss reference. This feature is particularly useful for managing open positions and optimizing exit points.

🔹 Trend Cloud:

Generates a specialized trend indicator using double-smoothed EMAs applied to closing prices and the high-low price range. It visualizes market trends and volatility by shading the area between different indicator values over time. The color of the shading changes to reflect whether the current trend is strengthening or weakening.

The Trend Cloud feature provides a visually intuitive representation of the overall market trend. It generates a dynamic colored cloud on the chart that helps traders quickly assess the current market direction and strength. Bullish trends represented by blue clouds and bearish trends by red clouds.

🔹 Trend Analyzer:

The Trend Analyzer component provides an in-depth analysis of the current market trend. It uses a customizable moving average system to determine the trend direction and strength. The analyzer can be configured to focus on short-term, medium-term, or long-term trends, allowing traders to align their strategy with their preferred trading timeframe.

Customizable Settings :

Analyzer Calculation Period: Adjustable period for trend analysis calculations.

Analyzer Mode: Selectable between "Short-Term", "Medium-Term", and "Long-Term".

Analyzer Calculation Source: Customizable price data source for trend analysis.

Use Heikin Ashi: Option to use Heikin Ashi candles instead of regular candles for calculations.

🔹 TP/Exit/Entry Levels:

The indicator calculates and displays potential take profit (TP), exit, and entry levels based on market structure and volatility. These levels are marked on the chart, offering traders guidance on optimal points for trade management. This feature can be particularly helpful for setting profit targets and managing risk.

🔹 Dashboard:

The customizable dashboard provides a quick overview of key market metrics. It displays information such as trend strength, volume analysis, market volatility, the current state of the Trend Catcher and the market is "Bearish" or "Bullish". This at-a-glance summary helps traders make informed decisions without the need to switch between multiple indicators.

Customizable Settings :

Toggle: Option to display or hide the dashboard.

Dashboard Position and Size: Selectable between "Top Right", "Bottom Right", and "Bottom Left". Adjustable size to "Tiny", "Small" or "Normal".

🔶 Disclaimer:

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Absolute Move BandsOverview:

The Absolute Move Bands indicator calculates the absolute value of the expected return, also known as "momentum" by some traders, and then displays it with standard deviation bands. The indicator also shows a moving average and a Kalman filter of the absolute move. If you take the expected return, you get what many traders commonly call "momentum." Now, if you turn the negative values into positive values by getting the magnitude of the expected return, it shows the "strength or intensity of the expected return." A low value of the absolute value of the expected return shows that the expected return is close to 0, which means that there is no significant trending behavior. The higher the value, the higher the deviation is from the mean, indicating stronger trend moves in the expected return itself. This indicator then gets the standard score of the absolute value of the expected return and then gets the moving average and Kalman Filter.

This indicator is not a directional indicator, but it can help you time moves and determine the "strength" of the expected returns (also known as momentum).

Interpreting the Magnitude:

Low Values: A low absolute value of the expected return indicates that the expected return is close to 0, suggesting no significant trending behavior in the market.

High Values: A high absolute value indicates a strong deviation from the mean, reflecting stronger trend moves in the expected return itself.

Standard Score Calculation:

This indicator computes the standard score (z-score) of the absolute value of the expected return. The value shows how many standard deviations the absolute return is from the mean. This helps in identifying periods of extreme magnitude.

Moving Average and Kalman Filter:

Moving Average: The indicator calculates the moving average of the standard score to smooth out the short-term fluctuations and show the longer-term trends in the absolute returns.

Kalman Filter: Applied to further reduce noise and provide a clearer signal, it enhances the indicator's effectiveness in determining the strength of the expected returns.

Standard Deviation Bands

Purpose: The standard deviation bands help determine if the standard score is at an extreme low or high.

High Standard Score (+2 Standard Deviation Band): Indicates that the absolute value of the expected return is at a high level, suggesting a strong trend. This could mean that the trend is at its peak and might be nearing completion.

Low Standard Score (-2 Standard Deviation Band): Indicates that the absolute value of the expected return is at a low level, suggesting minimal or no trending behavior. This could imply that the expected return is around 0, and a new trend (in any direction) may start soon.

How to interpret and use this indicator

Two ways will be discussed on how you can use this indicator. First of all lets go back over the interpretation of the standard score and bands.

High Standard Score: Indicates that the absolute value is significantly higher than usual, which suggest a strong trend which may be nearing its peak. Some traders who entered a trade at a low standard score value might want to consider taking profits or preparing for a potential reversal.

Low Standard Score: Indicates that the absolute value is significantly low, close to 0, which suggest minimal trending behavior and a new trend or move may soon start.

This indicator shouldn't be used alone; you may need an indicator that shows you the trend with an expected return indicator or a "momentum" indicator, because all this shows you is the strength of the trend or "momentum." So let's say that if you see that the standard score is low and the Kalman filter is increasing, then this shows that a trend may start soon, so you can use the "momentum" indicator and enter with whatever the trend is on.

Another way to use the indicator is to trade extreme occurrences. If on an indicator that shows the expected returns, or "momentum," and its at an extreme standard deviation occurrence level like -2 standard deviation from the mean, and the standard score is at 2 standard deviation (the top band), and the Kalman filter starts decreasing, then the downtrend may be over and you could place a long.

Anchored Monte Carlo Shuffled Projection [LuxAlgo]The Anchored Monte Carlo Shuffled Projection tool randomly simulates future price points based on historical bar movements made before a user-anchored point in time.

By anchoring our data and projections to a single point in time, users can better understand and reflect on how the price played out while taking into consideration our random simulations.

🔶 USAGE

After selecting the indicator to apply to the chart, you will be prompted to "Set the Anchor Point". Do so by clicking on the desired location on your chart, only time is used as the anchor point.

Note: To select a new anchor point when applied to the chart, click on the 'More' dropdown next to the indicator status bar (○○○), then select "Reset points...".

Alternate Method: You are also able to click and drag the vertical line that displays on the anchor point bar when the indicator is highlighted.

By randomly simulating bar movements, a range is developed of potential price action which could be utilized to locate future price development as well as potential support/resistance levels.

Performing numerous simulations and taking the average at each step will converge toward the result highlighted by the "Average Line", and can point out where the price might develop, assuming the trend and amount of volatility persist.

Current closing price + Sum of changes in the calculation window

This constraint will cause the simulations always to display an endpoint consistent with the current lookback's slope.

While this may be helpful to some traders, this indicator includes an option to produce a less biased range, as seen below:

🔶 DETAILS

The Anchored Monte Carlo Shuffled Projection tool creates simulations based on prices within a user-set lookback window originating at the specified anchor point. Simulations are done as follows:

Collect each bar's price changes in the user-set window.

Randomize the order of each change in the window.

Project the cumulative sum of the shuffled changes from the current closing price.

Collect data on each point along the way.

This is the process for the Default calculation; for the 'Randomize Direction' calculation, when added onto the front for every other change, the value is inverted, creating the randomized endpoints for each simulation.

The script contains each simulation's data for that bar, with a maximum of 1000 simulations.

To get a glimpse behind the scenes, each simulation (up to 99) can be viewed using the 'Visualize Simulations' Options, as seen below.

Because the script holds the full simulation data, the script can also calculate this data, such as standard deviations.

In this script the Standard deviation lines are the average of all standard deviations across the vertical data groups, this provides a singular value that can be displayed a distance away from the simulation center line.

🔶 SETTINGS

Lookback: Sets the number of Bars to include in calculations.

Simulation Count: Sets the number of randomized simulations to calculate. (Max 1000)

Randomize Direction: See Details Above. Creates a more 'Normalized' Distribution

Visualize Simulations: See Details Above. Turns on Visualizations, and colors are randomly generated. Visualized max does not cap the calculated max. If 1000 simulations are used, the data will be from 1000 simulations, however, only the last 99 simulations will be visualized.

🔹 Standard Deviations

Standard Deviation Multiplier: Sets the multiplier to use for the Standard Deviation distance away from the center line.

🔹 Style

Extend Lines: Extends the Simulated Value Lines into the future for further reference and analysis.

MTF Bollinger BandWidth [CryptoSea]The MTF Bollinger BandWidth Indicator is an advanced analytical tool crafted for traders who need to gauge market volatility and trend strength across multiple timeframes. This powerful indicator leverages the Bollinger BandWidth concept to provide a comprehensive view of price movements and volatility changes, making it ideal for those looking to enhance their trading strategies with multi-timeframe analysis.

Key Features

Multi-Timeframe Analysis: Allows users to monitor Bollinger BandWidth across various timeframes, providing a macro and micro perspective on market volatility.

Pivot Point Detection: Identifies crucial high and low pivot points, offering insights into potential support and resistance levels. Pivot points are dynamic and adjust based on the timeframe viewed, reflecting short-term fluctuations or longer-term trends.

Customizable Parameters: Includes options to adjust the length of the moving average, the standard deviation multiplier, and more, enabling traders to tailor the tool to their specific needs.

Dynamic Color Coding: Utilizes color changes to indicate different market conditions, aiding in quick visual assessments.

In the example below, notice how changes in BBW across different timeframes provide early signals for potential volatility increases or decreases.

How it Works

Calculation of BandWidth: Measures the percentage difference between the upper and lower Bollinger Bands, which expands or contracts based on market volatility.

High and Low Pivot Tracking: Automatically calculates and tracks the pivots in BBW values, which are critical for identifying turning points in market behavior. High and low levels will change depending on the timeframe, capturing distinct market behaviors from granular movements to broad trends.

Visual Alerts and Table Display: Highlights significant changes in BBW with visual alerts and provides a detailed table view for comparison across timeframes.

In the example below, BBW identifies a significant contraction followed by an expansion, suggesting a potential breakout.

Application

Strategic Market Entry and Exit: Assists traders in making well-informed decisions about when to enter and exit trades based on volatility cues.

Trend Strength Assessment: Helps in determining the strength of the prevailing market trend through detailed analysis of expansion and contraction periods.

Adaptable to Various Trading Styles: Suitable for day traders, swing traders, and long-term investors due to its customization capabilities and effectiveness across different timeframes.

The MTF Bollinger BandWidth Indicator is a must-have in the arsenal of traders who demand depth, accuracy, and responsiveness in their market analysis tools. Enhance your trading decisions by integrating this sophisticated indicator into your strategy to navigate the complexities of various market conditions effectively.

Volatility ATR Support and Resistance Bands [Quantigenics]Volatility ATR Support and Resistance Bands

The “Volatility ATR Support and Resistance Bands” is a trend visualization tool that uses Average True Range (ATR) to create a dynamic channel around price action, adapting to changes in volatility and offering clear trend indicators. The band direction can indicate trend and the lines can indicate support and resistance levels.

The script works by calculating a series of moving averages from the highest and lowest prices, then applies an ATR-based multiplier to generate a set of bands. These bands expand and contract with the market’s volatility, providing a visual guide to the strength and potential direction of price movements.

How to Trade with Volatility ATR Band:

Identify Trend Direction: When the bands slope upwards, the market is trending upwards, which may be a good opportunity to consider a long position. When the bands slope downward, the market is trending downwards, which could be a sign to sell or short.

Volatility Awareness: The wider the bands, the higher the market volatility. Narrow bands suggest a quieter market, which might indicate consolidation or a potential breakout/breakdown.

Confirm Entries and Exits: Use the bands as dynamic support and resistance; entering trades as the price bounces off the bands and considering exits as it reaches the opposite side or breaches the bands.

Hope you enjoy this script!

Happy trading!

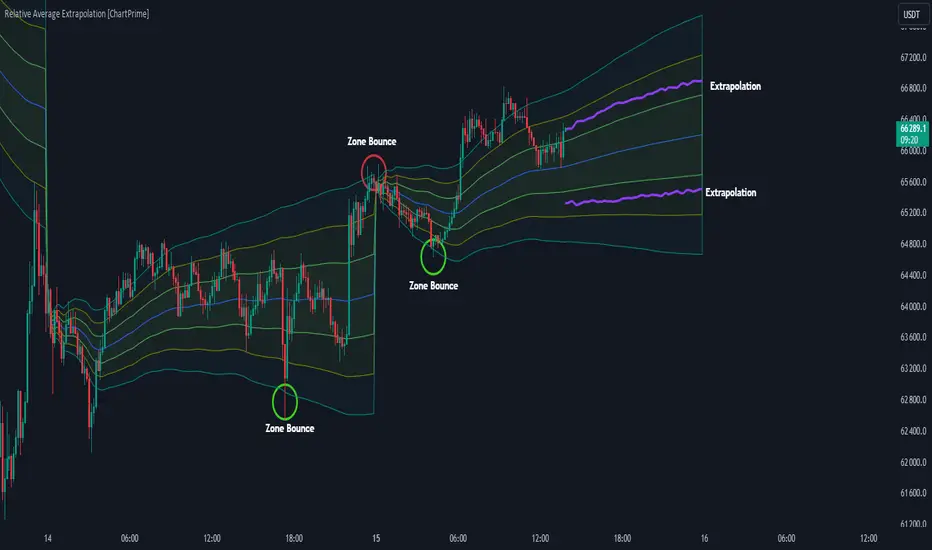

Relative Average Extrapolation [ChartPrime]Relative Average Extrapolation (ChartPrime) is a new take on session averages, like the famous vwap . This indicator leverages patterns in the market by leveraging average-at-time to get a footprint of the average market conditions for the current time. This allows for a great estimate of market conditions throughout the day allowing for predictive forecasting. If we know what the market conditions are at a given time of day we can use this information to make assumptions about future market conditions. This is what allows us to estimate an entire session with fair accuracy. This indicator works on any intra-day time frame and will not work on time frames less than a minute, or time frames that are a day or greater in length. A unique aspect of this indicator is that it allows for analysis of pre and post market sessions independently from regular hours. This results in a cleaner and more usable vwap for each individual session. One drawback of this is that the indicator utilizes an average for the length of a session. Because of this, some after hour sessions will only have a partial estimation. The average and deviation bands will work past the point where it has been extrapolated to in this instance however. On low time frames due to the limited number of data points, the indicator can appear noisy.

Generally crypto doesn't have a consistent footprint making this indicator less suitable in crypto markets. Because of this we have implemented other weighting schemes to allow for more flexibility in the number of use cases for this indicator. Besides volume weighting we have also included time, volatility, and linear (none) weighting. Using any one of these weighting schemes will transform the vwap into a wma, volatility adjusted ma, or a simple moving average. All of the style are still session period and will become longer as the session progresses.

Relative Average Extrapolation (ChartPrime) works by storing data for each time step throughout the day by utilizing a custom indexing system. It takes the a key , ie hour/minute, and transforms it into an array index to stor the current data point in its unique array. From there we can take the current time of day and advance it by one step to retrieve the data point for the next bar index. This allows us to utilize the footprint the extrapolate into the future. We use the relative rate of change for the average, the relative deviation, and relative price position to extrapolate from the current point to the end of the session. This process is fast and effective and possibly easier to use than the built in map feature.

If you have used vwap before you should be familiar with the general settings for this indicator. We have made a point to make it as intuitive for anyone who is already used to using the standard vwap. You can pick the source for the average and adjust/enable the deviation bands multipliers in the settings group. The average period is what determines the number of days to use for the average-at-time. When it is set to 0 it will use all available data. Under "Extrapolation" you will find the settings for the estimation. "Direction Sensitivity" adjusts how sensitive the indicator is to the direction of the vwap. A higher number will allow it to change directions faster, where a lower number will make it more stable throughout the session. Under the "Style" section you will find all of the color and style adjustments to customize the appearance of this indicator.

Relative Average Extrapolation (ChartPrime) is an advanced and customizable session average indicator with the ability to estimate the direction and volatility of intra-day sessions. We hope you will find this script fascinating and useful in your trading and decision making. With its unique take on session weighting and forecasting, we believe it will be a secret weapon for traders for years to come.

Enjoy

Quadratic Weighted Bands"Quadratic Weighted Bands" (QWB) is designed to identify and visualize market trends and volatility using quadratic weighted filtering techniques. It works by applying quadratic weighting to a selected data source over a specified length, enhancing the sensitivity and responsiveness of the indicator to recent market movements. A major advantage of this indicator is the ability to have a longer lookback period without having too much lag. This results in a smoother output that is still very responsive. Its about twice as fast as a normal average so adjust accordingly.

The indicator is customizable, allowing users to select between the normal Quadratic Weighting (QWF) and Volume Quadratic Weighting (VQWF), choose their data source, adjust the lookback period, and modify the deviation multiplier to fit their analysis needs. Additionally, users can customize the colors of the bands and center line.

The color of the central line changes based on the direction of the trend, as well as having a neutral (ranging) color. This visual aspect makes it easier for traders to quickly see the strength and direction of the market.

Style Select: Choose between "Normal Quadratic Weighting" or "Volume Quadratic Weighting" to adapt the indicator based on volume data or standard price data.

Source: This allows for the selection of the input source for the indicator, such as HL2, ensuring the analysis is aligned with specific trading preferences.

Length: Define the lookback period for the average, with the system automatically utilizing the maximum available length if the specified range exceeds available data, ensuring it always works.

Deviation Length: Optionally adjust the lookback period for calculating deviation, enhancing the indicator's sensitivity and accuracy in identifying market volatility.

Multiplier: Fine tune the deviation multiplier to control the width of the bands, allowing traders to adjust for market volatility and personal risk tolerance.

Top Color: Customize the color of the top band, which also affects the center line's appearance. Adjusting the brightness provides visual clarity and personalization.

Bottom Color: Similarly, select the color for the bottom band, which also influences the center line. The option to adjust brightness ensures the indicator's readability and aesthetic preference.

Neutral Color: Designate a color for indicating a ranging market.

Enjoy

RWEDT Weighted Moving Average Overview:

The RWEDT MA, which is short for rolling, weighted, exponential, double exponential, and triple exponential, is a group of moving averages that were subjected to a log transformation to deal with the skewness of price, and the weight of each of these moving averages was also used for calculating the standard deviations from the mean.

Clearing a misunderstanding on Standard Deviation Bands and Moving Averages

Bands, such as standard deviation bands, are frequently misinterpreted as indicators of support and resistance levels or as "mean-reverting" indicators." However, this is not their intended purpose. Bands are statistical tools that provide ranges within which price (in this case) movements are expected to occur based on historical data. Deviations beyond these bands suggest a decrease in confidence in the model rather than a reversal back to a moving average or a "support/resistance level."

Example : Assuming you correctly applied a log transformation to your standard deviation bands to remove the right skew, and assuming your data closely resembles a normal distribution or some other type of symmetrical distribution, then the probability of a value being in the 2 standard deviation range is around 95%. This does not mean it will reject or go up, or mean revert. The price won't bounce from -2 STDEV 95% of the time; that is incorrect. It just tells you that around 95% of the values will be within the 2 SD range.

Moving averages, including the ones in this indicator, are often misinterpreted as signals of trend reversals or levels of "bouncing." What moving averages actually tell you is what the expected value is. It does not show where you expect the price to be in the future; it tells you that based on the lookback, the expected value is in the center, and the confidence you have in the estimate is the confidence interval or the standard deviation range.

Example: Let's say you enter a trade with a positive expected value (expecting the price to drift up), and we have the limits set at 95%. What it tells you is that as long as the price stays within the limits, you can be 95% certain the model isn't completely random. As the price moves further away from the average, or expected value, it tells you that the model is less likely to be correct.

RWEDT MA

This indicator comes with 5 moving averages, each log transformed to reduce the skewness and asymmetry of price as much as possible

Rolling

Weighted

Exponential

Double Exponential

Triple Exponential

The band standard deviation can be adjusted, and the standard deviations have the weight of all of the moving averages that are present in the indicator. The weight is not customizable.

Why this indicator is useful:

This indicator can tell you what the expected value is. Above the moving average signifies a positive expected value, and below the moving average signifies a negative expected value. As previously stated above, the price moving further from the expected value lets you know that you should have less confidence that the model is "correct," and you could see this as taking profits as the price deviates further from the expected value.

The importance of log-transforming prices for standard deviations and moving averages.

Symmetry: Logarithmic transformations can help achieve symmetry in the distribution of price data. Stock prices, for example, exhibit some type of right-skewed distribution, where large positive price movements are more common than large negative movements. Price also can't go below 0 but can go towards positive infinity, so having a right-skew makes sense; all the outliers will be towards infinity, while all the average occurrences are "near" 0.

Stabilizing Variance: Price data typically exhibit heteroscedasticity, meaning that the variance of price movements changes over time. Log transformations can stabilize the variance and make it more consistent across different price levels. This is important for ensuring that the variability in price moves is not disproportionately influenced by extreme values.

Statistical Assumptions: Many retail indicators like Bollinger Bands use the standard deviation and moving average models of a normal distribution to attempt to model price, whose distribution more closely resembles some type of right-skew distribution. Even with the log-transformation, it still won't always resemble a perfect symmetrical distribution, and you still should not use it for mean reversion. You can still use it to understand the expected value and whether or not you should have confidence in your model.

ATR Bands with Optional Risk/Reward Colors█ OVERVIEW

This indicator projects ATR bands and, optionally, colors them based on a risk/reward advantage for those who trade breakouts/breakdowns using moving averages as partial or full exit points.

█ DEFINITIONS

► True Range

The True Range is a measure of the volatility of a financial asset and is defined as the maximum difference among one of the following values:

- The high of the current period minus the low of the current period.

- The absolute value of the high of the current period minus the closing price of the previous period.

- The absolute value of the low of the current period minus the closing price of the previous period.

► Average True Range

The Average True Range was developed by J. Welles Wilder Jr. and was introduced in his 1978 book titled "New Concepts in Technical Trading Systems". It is calculated as an average of the true range values over a certain number of periods (usually 14) and is commonly used to measure volatility and set stop-loss and profit targets (1).

For example, if you are looking at a daily chart and you want to calculate the 14-day ATR, you would take the True Range of the previous 14 days, calculate their average, and this would be the ATR for that day. The process is then repeated every day to obtain a series of ATR values over time.

The ATR can be smoothed using different methods, such as the Simple Moving Average (SMA), the Exponential Moving Average (EMA), or others, depending on the user's preferences or analysis needs.

► ATR Bands

The ATR bands are created by adding or subtracting the ATR from a reference point (usually the closing price). This process generates bands around the central point that expand and contract based on market volatility, allowing traders to assess dynamic support and resistance levels and to adapt their trading strategies to current market conditions.

█ INDICATOR

► ATR Bands

The indicator provides all the essential parameters for calculating the ATR: period length, time frame, smoothing method, and multiplier.

It is then possible to choose the reference point from which to create the bands. The most commonly used reference points are Open, High, Low, and Close, but you can also choose the commonly used candle averages: HL2, HLC3, HLCC4, OHLC4. Among these, there is also a less common "OC2", which represents the average of the candle body. Additionally, two parameters have been specifically created for this indicator: Open/Close and High/Low.

With the "Open/Close" parameter, the upper band is calculated from the higher value between Open and Close, while the lower one is calculated from the lower value between Open and Close. In the case of bullish candles, therefore, the Close value is taken as the starting point for the upper band and the Open value for the lower one; conversely, in bearish candles, the Open value is used for the upper band and the Close value for the lower band. This setting can be useful for precautionally generating broader bands when trading with candlesticks like hammers or inverted hammers.

The "High/Low" parameter calculates the upper band starting from the High and the lower band starting from the Low. Among all the available options, this one allows drawing the widest bands.

Other possible options to improve the drawing of ATR bands, aligning them with the price action, are:

• Doji Smoothing: When the current candle is a doji (having the same Open and Close price), the bands assume the values they had on the previous candle. This can be useful to avoid steep fluctuations of the bands themselves.

• Extend to High/Low: Extends the bands to the High or Low values when they exceed the value of the band.

• Round Last Cent: Expands the upper band by one cent if the price ends with x.x9, and the lower band if the price ends with x.x1. This function only works when the asset's tick is 0.01.

► Risk/Reward Advantage

The indicator optionally colors the ATR bands after setting a breakpoint, one or two risk/reward ratios, and a series of moving averages. This function allows you to know in advance whether entering a trade can provide an advantage over the risk. The band is colored when the ratio between the distance from the break point to the band and the distance from the break point to the first available moving average reaches at least the set ratio value. It is possible to set two colorings, one for a minimum risk/reward ratio and one for an optimal risk/reward ratio.

The break point can be chosen between High/Low (High in case of breakout, Low in case of breakdown) or Open/Close (on breakouts, Close with bullish candles or Open with bearish candles; on breakdowns, Close with bearish candles or Open with bullish candles).

It is possible to choose up to 10 moving averages of various types, including the VWAP with the Anchor Period (2).

Depending on the "Price to MA" setting, the bands can be individually or simultaneously colored.

By selecting "Single Direction," the risk/reward calculation is performed only when all moving averages are above or below the break point, resulting in only one band being colored at a time. For this reason, when the break point is in between the moving averages, the calculation is not executed. This setting can be useful for strategies involving price movement from a level towards a series of specific moving averages (for example, in reversals starting from a certain level towards the VWAP with possible partial take profits on some previous moving averages, or simply in trend following towards one or more moving averages).

Choosing "Both Directions" the risk/reward ratio is calculated based on the first available moving averages both above and below the price. This setting is useful for those who operate in range bound markets or simply take advantage of movements between moving averages.

█ NOTE

This script may not be suitable for scalping strategies that require immediate entries due to the inability to know the ATR of a candle in advance until its closure. Once the candle is closed, you should have time to place a stop or stop-limit order, so your strategy should not anticipate an immediate start with the next candle. Even more conveniently, if your strategy involves an entry on a pullback, you can place a limit order at the breakout level.

(1) www.tradingview.com

(2) For convenience, the code for the Anchor Period has been entirely copied from the VWAP code provided by TradingView.

Machine Learning Breakouts (from Pivots)I developed the 'Machine Learning Breakouts (from Pivots)' indicator to revolutionize the way we detect breakout opportunities and follow trend, harnessing the power of pivot points and machine learning. This tool integrates the k-Nearest Neighbors (k-NN) method with the Euclidean distance algorithm, meticulously analyzing pivot points to accurately forecast multiple breakout paths/zones. "ML Pivots Breakouts" is designed to identify and visually alert traders on bullish breakouts above high lines and bearish breakouts below low lines, offering essential insights for breakout and trend follower traders.

For traders, the instruction is clear: a bullish breakout signal is given when the price crosses above the forecasted high line, indicating potential entry points for long positions. Conversely, a bearish breakout signal is provided when the price breaks below the forecasted low line, suggesting opportunities to enter short positions. This makes the indicator a vital asset for navigating through market volatilities and capitalizing on emerging trends, designed for both long and short strategies and adeptly adapting to market shifts.

In this indicator I operate in a two-dimensional space defined by price and time. The choice of Euclidean distance as the preferred method for this analysis hinges on its simplicity and effectiveness in measuring and predicting straight-line distances between points in this space.

The Machine Learning Breakouts (from Pivots) Indicator calculations have been transitioned to the MLPivotsBreakouts library, simplifying the process of integration. Users can now seamlessly incorporate the "breakouts" function into their scripts to conduct detailed momentum analysis with ease.

ASFX A2 VWAP [LuxAlgo]The ASFX A2 VWAP is a toolkit based on A2 signals and daily anchored VWAP bands, a methodology proposed by trader & educator Austin Silver (ASFX).

Pre-built alerts are also included.

🔶 USAGE

The A2 strategy involves identifying potential trades using specific signals and confirmation from the 21 EMA (Exponential Moving Average). Below we can see a bullish A2 signal triggering as price is closing below the 21 EMA with less than half of the candles closing price.

Within the settings, we have enabled the stop loss setting to assist us with trade setups generated from A2 signals.

Users can enable multiple layers of StDev multipliers on the AAVWAP to find areas of support & resistance alongside the A2 signals & other features included.

🔶 DETAILS

If 'Filter Based On VWAP' is enabled, bullish signals will only be displayed if located above the anchored VWAP, while bearish signals will only be displayed when located under the VWAP. The image above illustrates this, with transparent signals showing the ones that are supposed to be filtered.

The Stop Loss is based on the most recent A2 signal, and is constructed from the 1.618 Fibonacci retracement using the following points depending on the A2 signal:

Bullish: From candle low to the current daily maximum.

Bearish: From candle high to current daily minimum.

🔶 SETTINGS

🔹 A2

Validation EMA Period : Period of the EMA used to validate triggered A2 signals.

Trigger EMA Period : Period of the EMA used to trigger A2 signals.

Filter Based On VWAP : Filter A2 signals based on their location relative to the VWAP output.

🔹 VWAP

source : Input data for the anchored VWAP calculation

Show Central AVWAP : Display central VWAP on the chart

StDev Multiplier 1 : Display first VWAP bands, using a StDev multiplier of 1 by default.

StDev Multiplier 2 : Display second VWAP bands, using a StDev multiplier of 2 by default.

StDev Multiplier 3 : Display third VWAP bands, using a StDev multiplier of 3 by default.

🔹 Stop Loss

Stop Loss : Display stop loss based on the most recent A2 signal

Kernel Regression RibbonKernel Regression Ribbon is a flexible, visually pleasing trend identification tool. Plotting 8 different kernel regressions of different types and parameters allows the user to see where levels of support and resistance are being tested, retested and broken.

What’s Kernel Regression?

A statistical method for estimating the best fitting curve for a dataset, in this case, a time/price chart.

How’s Kernel Regression different from a Moving Average?

A Moving Average is basically a simple form of Kernel Regression, in that it uses a fixed (Retangular) Kernel function. In an MA, all data points are weighted equally over its length. However, a Kernel function reacts more to data points that are closer to the current point. This means it will adapt more quickly to changes in data than an MA. Due to this adaptability, Kernel functions often form part of Machine Learning.

Using this indicator:

Explore the default Regular mode first to get a feel for the inputs, which are more numerous than for MAs. Try out different settings, filters and intervals to get the best out of each kernel. Not all parameters are available for each KR. There are info tips to explain this in the menu, but I’ve also included handy, optional labels on the chart for each KR as a more accessible guide.

Once you know your way round the Regular mode, check out the Presets and start changing the parameters of each kernel to your liking in the “User KR1, KR2, … “ mode. Each kernel type has its strong and weak points. Blending different kernels is where this indicator comes into its own. Give your charts a funky shine!

This indicator does NOT repaint.

This script acknowledges, and hopefully showcases, the great work of @veryfid Kernel Regression Toolkit.

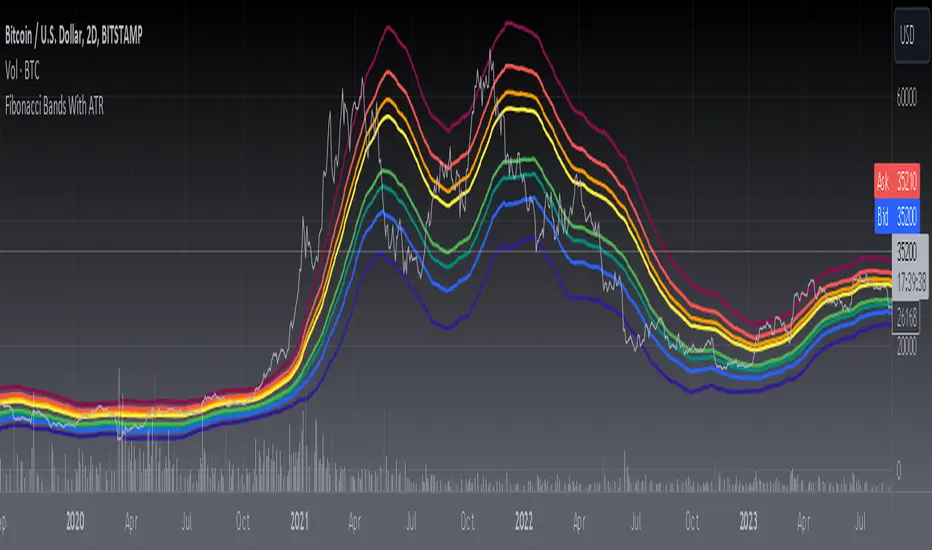

[blackcat] L3 Fibonacci Bands With ATRToday, what I'm going to introduce is a technical indicator that I think is quite in line with the indicator displayed by Tang - Fibonacci Bands with ATR. This indicator combines Bollinger Bands and Average True Range (ATR) to provide insights into market volatility and potential price reversals. Sounds complicated, right? Don't worry, I will explain it to you in the simplest way.

First, let's take a look at how Fibonacci Bands are constructed. They are similar to Bollinger Bands and consist of three lines: upper band, middle band (usually a 20-period simple moving average), and lower band. The difference is that Fibonacci Bands use ATR to calculate the distance between the upper and lower bands and the middle band.

Next is a key factor - ATR multiplier. We need to smooth the ATR using Welles Wilder's method. Then, by multiplying the ATR by a Fibonacci multiplier (e.g., 1.618), we get the upper band, called the upper Fibonacci channel. Similarly, multiplying the ATR by another Fibonacci multiplier (e.g., 0.618 or 1.0) gives us the lower band, called the lower Fibonacci channel.

Now, let's see how Fibonacci Bands can help us assess market volatility. When the channel widens, it means that market volatility is high, while a narrow channel indicates low market volatility. This way, we can determine the market's activity level based on the width of the channel.

In addition, when the price touches or crosses the Fibonacci channel, it may indicate a potential price reversal, similar to Bollinger Bands. Therefore, using Fibonacci Bands in trading can help us capture potential buy or sell signals.

In summary, Fibonacci Bands with ATR is an interesting and practical technical indicator that provides information about market volatility and potential price reversals by combining Bollinger Bands and ATR. Remember, make good use of these indicators and apply them flexibly in trading!

This code is a TradingView indicator script used to plot L3 Fibonacci Bands With ATR.

First, the indicator function is used to define the title and short title of the indicator, and whether it should be overlaid on the main chart.

Then, the input function is used to define three input parameters: MA type (maType), MA length (maLength), and data source (src). There are four options for MA type: SMA, EMA, WMA, and HMA. The default values are SMA, 55, and hl2 respectively.

Next, the moving average line is calculated based on the user's selected MA type. If maType is 'SMA', the ta.sma function is called to calculate the simple moving average; if maType is 'EMA', the ta.ema function is called to calculate the exponential moving average; if maType is 'WMA', the ta.wma function is called to calculate the weighted moving average; if maType is 'HMA', the ta.hma function is called to calculate the Hull moving average. The result is then assigned to the variable ma.

Then, the _atr variable is used to calculate the ATR (Average True Range) value using ta.atr, and multiplied by different coefficients to obtain four Fibonacci bias values: fibo_bias4, fibo_bias3, fibo_bias2, and fibo_bias1.

Finally, the prices of the upper and lower four Fibonacci bands are calculated by adding or subtracting the corresponding Fibonacci bias values from the current price, and plotted on the chart using the plot function.

RSI Bands + Levels (Miu)This indicator was designed to plot lines from prices of overbought (OB) and oversold (OS) RSI levels in chart. It will also create a visible band between these levels.

It's main utility is to show in chart current and past prices for OB/OS RSI levels. Traditionally the RSI is considered overbought when above 70 and oversold when below 30 but you can customize these values in settings. The RSI oscillates between zero and 100.

Users can easily identify overbought and oversold prices using this indicator and then it is expected to help users to make better strategic decisions with their trades.

There are some extra options available in settings:

- Customizable RSI levels

- Customizable RSI length

- RSI Levels: if activated, it will draw lines above OB line and below OS line according to the multiplier, so it will plot sequential lines that goes in different RSI levels (e.g: RSI 72, 74, 76, 78 and 80).

- Backgroud only: it will remove these lines and keep only a backgroung color instead

- RSI 50: it will draw a line as RSI 50

- Customizable multiplier

Enjoy!

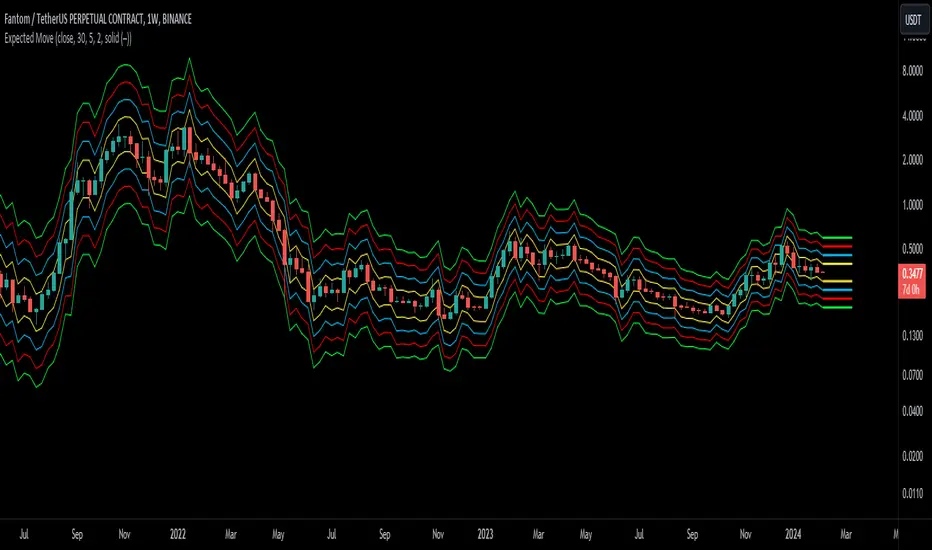

Expected Move BandsExpected Moves

The Expected Move of a security shows the amount that a stock is expected to rise or fall from its current market price based on its level of volatility or implied volatility. The expected move of a stock is usually measured with standard deviations.

An Expected Move Range of 1 SD shows that price will be near the 1 SD range 68% of the time given enough samples.

Expected Move Bands

This indicator gets the Expected Move for 1-4 Standard Deviation Ranges using Historical Volatility. Then it displays it on price as bands.

The Expected Move indicator also allows you to see MTF Expected Moves if you want to.

This indicator calculates the expected price movements by analyzing the historical volatility of an asset. Volatility is the measure of fluctuation.

This script uses log returns for the historical volatility calculation which can be modelled as a normal distribution most of the time meaning it is symmetrical and stationary unlike other scripts that use bands to find "reversals". They are fundamentally incorrect.

What these ranges tell you is basically the odds of the price movement being between these levels.

If you take enough samples, 95.5% of the them will be near the 2nd Standard Deviation. And so on. (The 3rd Standard deviation is 99.7%)

For higher timeframes you might need a smaller sample size.

Features

MTF Option

Parameter customization

Intraday Volatility Bands [Honestcowboy]The Intraday Volatility Bands aims to provide a better alternative to ATR in the calculation of targets or reversal points.

How are they different from ATR based bands?

While ATR and other measures of volatility base their calculations on the previous bars on the chart (for example bars 1954 to 1968). The volatility used in these bands measure expected volatility during that time of the day.

Why would you take this approach?

Markets behave different during certain times of the day, also called sessions.

Here are a couple examples.

Asian Session (generally low volatility)

London Session (bigger volatility starts)

New York Session (overlap of New York with London creates huge volatility)

Generally when using bands or channel type indicators intraday they do not account for the upcoming sessions. On London open price will quickly spike through a bollinger band and it will take some time for the bands to adjust to new volatility.

This script will show expected volatility targets at the start of each new bar and will not adjust during the bar. It already knows what price is expected to do at this time of day.

Script also plots arrows when price breaches either the top or bottom of the bands. You can also set alerts for when this occurs. These are non repainting as the script knows the level at start of the bar and does not change.

🔷 CALCULATION

Think of this script like an ATR but instead it uses past days data instead of previous bars data. Charts below should visualise this more clearly:

The scripts measure of volatility is based on a simple high-low.

The script also counts the number of bars that exist in a day on your current timeframe chart. After knowing that number it creates the matrix used in it's calculations and data storage.

See how it works perfectly on a lower timeframe chart below:

Getting this right was the hardest part, check the coding if you are interested in this type of stuff. I commented every step in the coding process.

🔷 SETTINGS

Every setting of the script has a tooltip but I provided a breakdown here:

Some more examples of different charts:

Donchian MA Bands [LuxAlgo]The Donchian MA Bands script is a complete trend indicator derived from the popular Donchian channel indicator as well as various customizable moving averages to estimate trend direction and build support/resistance levels & zones.

🔶 USAGE

The indicator outputs various elements, the main ones being a lower dynamic zone (blue by default), an upper dynamic zone (in orange by default), and one support and resistance level/zones (red/green by default).

A prominent lower zone is indicative of an uptrend, while a prominent upper zone is indicative of a downtrend. These zones can be used as support/resistance as well.

Support/resistance zones and levels can be used using a breakout methodology or to determine price bounced if a level was tested multiple times.

The indicator contains various modes affecting the output of the indicator, described below.

🔹 Clouds

Clouds return one upper/lower dynamic zone and look/act similarly to a trailing stop. Price over the lower zone is indicative of an uptrend, and price under the upper zone is indicative of a downtrend.

🔹 Upper Band

The upper band mode returns a dynamic zone closer to prices during an uptrend, and farther away during a downtrend.

This band can act as a support during uptrends.

🔹 Lower Band

The lower band mode returns a dynamic zone closer to prices during an uptrend, and farther away during a downtrend.

This band can act as a resistance during downtrends.

🔹 Bands

Bands return both upper and lower zones, the zones are more apparent depending on the price trend direction, with uptrends being indicated by a more visible lower zone, and downtrends being indicated by a more visible upper zone.

Breakout dots are highlighted when price breakout the indicator displayed extremities, and can be indicative of a confirmed trend reversal.

These breakouts can be more effective for trend following during trending markets. Ranging markets might return breakouts highlighting the top/bottom.

🔶 DETAILS

The core of this script is the highest / lowest mean average (MA) value for a given number of bars back ( Donchian lines).

This is repeated a few times with the obtained values.

When Bands are chosen ( Style ) this will be repeated 1 more time.

The type of mean average can be customized ( Type MA ), as well as the number of bars back ( Length ).

Depending on the choice of bands ( Style ) the script will focus on certain area's of interest.

When the option Clouds , Upper band or Lower band is chosen, an extra feature, support/resistance (S/R), will be shown.

These color-filled areas are visible when there is a difference between the 2nd and 3rd highest/lowest values.

The lines/areas can be used for stop loss, entry, exit,...

You can set the type of MA and Length separately ( Settings -> S/R ).

If you don't need this feature, simply set Type ( Settings -> S/R ) -> NONE

The shape sometimes resembles triangles, indicating a potential direction

Default the average of the highest and lowest values is plotted (Style -> Mid Donchian)

This can act as potential support/resistance or visualization of the trend, the mean average is not plotted but can be (Style -> MA)

🔹 Note

When the option Bands is chosen, an indication is plotted when the closing price breaks above the highest band or breaks below the lower band. This isn't necessarily a buy/sell signal, it is merely a signal that these lines are broken.

Users should decide on their own how they use the bands/lines/areas as entry, exit, trailing stop, stop loss, profit taking,...

🔶 SETTINGS

🔹 Bands

Style: Clouds (default), Upper band, Lower band, Bands

Type MA: choose between SMA, EMA, RMA, HullMA, WMA, VWMA (default), DEMA, TEMA, NONE (off)

Length: Length of moving average and Donchian calculations (default 20)

Colour Bands

🔹 S/R (Support/Resistance, visible with Clouds, Upper band or Lower band)

Type MA: choose between SMA, EMA, RMA, HullMA, WMA, VWMA (default), DEMA, TEMA, NONE (off)

Length: Length of moving average and Donchian calculations (default 20)

Colour S/R

Bitcoin wave modelBitcoin wave model is based on the logarithmic regression model and the sinusoidal waves, induced by the halving events.

This chart presents the outcome of an in-depth analysis of the complete set of Bitcoin price data available from October 2009 to August 2023.

The central concept is that the logarithm of the Bitcoin price closely adheres to the logarithmic regression model. If we plot the logarithm of the price against the logarithm of time, it forms a nearly straight line.

The parameters of this model are provided in the script as follows: log (BTCUSD) = 1.48 + 5.44log(h).

The secondary concept involves employing the inherent time unit of Bitcoin instead of days:

'h' denotes a slightly adjusted time measurement intrinsic to the Bitcoin blockchain. It can be approximated as (days since the genesis block) * 0.0007. Precisely, 'h' is defined as follows: h = 0 at the genesis block, h = 1 at the first halving block, and so forth. In general, h = block height / 210,000.

Adjustments are made to account for variations in block creation time.

The third concept revolves around investigating halving waves triggered by supply shock events resulting from the halvings. These halvings occur at regular intervals in Bitcoin's native time 'h'. All halvings transpire when 'h' is an integer. These events induce waves with intervals denoted as h = 1.

Consequently, we can model these waves using a sin(2pih - a) function. The parameter determining the time shift is assessed as 'a = 0.4', aligning with earlier expectations for halving events and their subsequent outcomes.

The fourth concept introduces the notion that the waves gradually diminish in amplitude over the progression of "time h," diminishing at a rate of 0.7^h.

Lastly, we can create bands around the modeled sinusoidal waves. The upper band is derived by multiplying the sine wave by a factor of 3.1*(1-0.16)^h, while the lower band is obtained by dividing the sine wave by the same factor, 3.1*(1-0.16)^h.

The current bandwidth is 2.5x. That means that the upper band is 2.5 times the lower band. These bands are forming an exceptionally narrow predictive channel for Bitcoin. Consequently, a highly accurate estimation of the peak of the next cycle can be derived.

The prediction indicates that the zenith past the fourth halving, expected around the summer of 2025, could result in prices ranging between 200,000 and 240,000 USD.

Enjoy the mathematical insights!