Monthly beta (5Y monthly) with multi-timeframe supportThe PROPER way to calculate beta for a stock using monthly price returns . None of this nonsense using daily returns and sliding windows as done by other scripts...

Works on any timeframe.

This script has been checked against 100s of stocks on Yahoo finance and Zacks research data and matches 100% (some rounding error as this script is kept updated live on unconfirmed monthly bars).

You can check for yourself:

Zacks fundamentals - beta

The script calculates beta using the Variance-Covariance Method as described on Investopedia

How to calculate Beta

Volatilità storica

Percentage Range Consolidation HistogramThe Percentage Range Consolidation histogram is a measure of volatility, ranking current price range compared to past ranges.

🟩 USAGE

Here there are 2 heavy contractions of price shown on chart that lead to a big rally. Shows a possible way to approach trading this. Take into account that this is for illustration purposes only and these entry methods have not been tested for long term profitability.

Same price behaviour.

🟩 CALCULATION

The script will use 3 different ranges all configurable by the user to check for low volatility on different zone lengths . On default zone 1 will be 10 period, 2 will be 30 period and 3 is 50 periods long.

It will then measure the percentage these ranges have from top (highest close) to bottom (lowest close) and plot those numbers as 3 gray histograms.

For each of these histograms separately it will use 'percentage zone PNR Length setting' as a lookback to rank current zone percentage compared to past results.

How it will do that is using the 'percentage zone PNR % setting' it will draw a line using ta.percentile_nearest_rank() formula. At default this is 20% meaning that only 20% of lookback values where below this level.

When the histogram is below this white line (small range compared to past ranges) it will color the histogram. Yellow for zone 1, orange for zone 2 and blue for zone 3.

There is also a 'Percentage zone % filter' which you can use as a maximum % current zone for it to be considered a small range. On default this is set to 15%. You can turn this off by selecting 'median' as 'Consolidation filters' instead of 'all' . Or only use this by selecting 'percentage'

🟩 BAR COLORING

Now that you understand how to find small ranges (contractions of price) with the indicator there is a bar coloring option in the indicator.

You can select how many of the 3 zones have to be ranging for it to color the bar. On default this is set to 3 so the script will only color when price is in a very small range. As illustrated by the above charts these can lead to the beginnings of big trends.

Intraday Volatility BarsThis script produce a volatility histrogram by bar with the current volatility overlayed.

The histogram shows cumulative average volatility over n days.

And the dots are todays cumulative volatility.

In other words, it calculates the True Range of each bar and adds it to todays value.

This script is build for intraday timeframes between one and 1440 minutes only.

I use this to show me when volatility is above/below/equal to the average volatility.

When the dots are above the histogram then it is a more volatile day, and vice versa.

Recognizing a more volatile day as early as possible can be an advantage for daytrader.

Days that start with higher volatility seems to continue to increase relative to the past few days. Or when midday volatility rises it seems to continue as well.

Happy Trading!

Volatility Price RangeThe Volatility Price Range is an overlay which estimates a price range for the next seven days and next day, based on historical volatility (already available in TradingView). The upper and lower bands are calculated as follows:

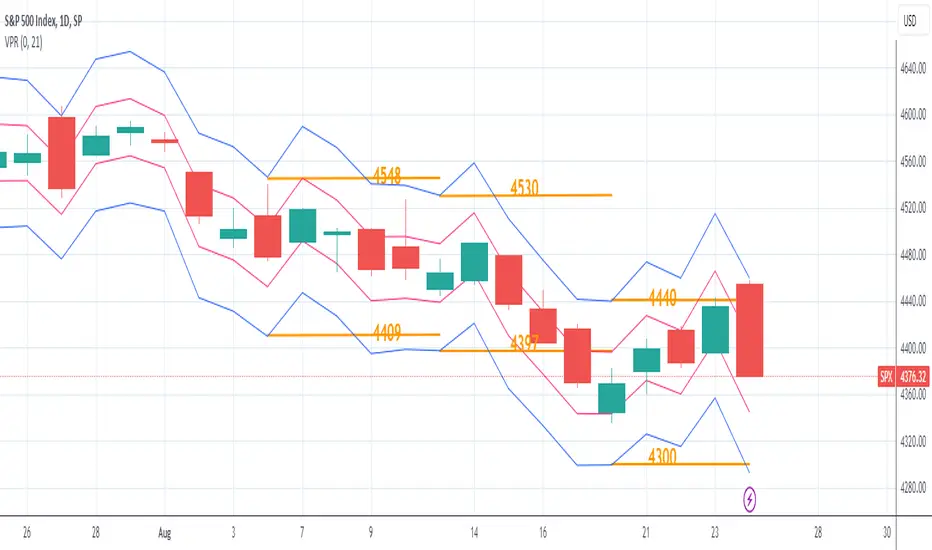

The Volatility for one week is calculated using the formula: WV = HV * √t where:

WV: one-week volatility

HV: annual volatility

√: square root

t: the time factor expressed in years

From this formula we can deduce the weekly volatility WV = HV * √(1 / 52) = HV / 7.2 where 52: weeks in a year.

The daily volatility DV = HV * √(1 / 365) = HV / 19.1 where 365: days in a year.

To calculate the lower and upper value of the bands, the weekly/daily volatility value obtained will be subtracted/added from/to the current price.

REVE Cohorts - Range Extension Volume Expansion CohortsREVE Cohorts stands for Range Extensions Volume Expansions Cohorts.

Volume is divided in four cohorts, these are depicted in the middle band with colors and histogram spikes.

0-80 percent i.e. low volumes; these get a green color and a narrow histogram bar

80-120 percent, normal volumes, these get a blue color and a narrow histogram bar

120-200 percent, high volume, these get an orange color and a wide histogram bar

200 and more percent is extreme volume, maroon color and wide bar.

All histogram bars have the same length. They point to the exact candle where the volume occurs.

Range is divided in two cohorts, these are depicted as candles above and below the middle band.

0-120 percent: small and normal range, depicted as single size, square candles

120 percent and more, wide range depicted as double size, rectangular candles.

The range candles are placed and colored according to the Advanced Price Algorithm (published script). If the trend is up, the candles are in the uptrend area, which is above the volume band, , downtrend candles below in the downtrend area. Dark blue candles depict a price movement which confirms the uptrend, these are of course in the uptrend area. In this area are also light red candles with a blue border, these depict a faltering price movement countering the uptrend. In the downtrend area, which is below the volume band, are red candles which depict a price movement confirming the downtrend and light blue candles with a red border depicting price movement countering the downtrend. A trend in the Advanced Price Algorithm is in equal to the direction of a simple moving average with the same lookback. The indicator has the same lagging.as this SMA.

Signals are placed in the vacated spaces, e.g. during an uptrend the downtrend area is vacated.

There are six signals, which arise as follows:

1 Two blue triangles up on top of each other: high or extreme volume in combination with wide range confirming uptrend. This indicates strong and effective up pressure in uptrend

2 Two pink tringles down on top of each other: high or extreme volume in combination with wide range down confirming downtrend. This indicates strong and effective down pressure in downtrend

3 Blue square above pink down triangle down: extreme volume in combination with wide range countering uptrend. This indicates a change of heart, down trend is imminent, e.g. during a reversal pattern. Down Pressure in uptrend

4 Pink square below blue triangle up: extreme volume in combination with wide range countering downtrend. This indicates a change of heart, reversal to uptrend is imminent. Up Pressure in downtrend

5 single blue square: a. extreme volume in combination with small range confirming uptrend, b. extreme volume in combination with small range countering downtrend, c. high volume in combination with wide range countering uptrend. This indicates halting upward price movement, occurs often at tops or during distribution periods. Unresolved pressure in uptrend

6 Single pink square: a extreme volume in combination with small range confirming downtrend, b extreme volume in combination with small range countering uptrend, c high volume in combination with wide range countering downtrend. This indicated halting downward price movement. Occurs often at bottoms or during accumulation periods. Unresolved pressure in downtrend.

The signals 5 and 6 are introduced to prevent flipping of signals into their opposite when the lookback is changed. Now signals may only change from unresolved in directional or vice versa. Signals 3 and 4 were introduced to make sure that all occurrences of extreme volume will result in a signal. Occurrences of wide volume only partly lead to a signal.

Use of REVE Cohorts.

This is the indicator for volume-range analyses that I always wanted to have. Now that I managed to create it, I put it in all my charts, it is often the first part I look at, In my momentum investment system I use it primarily in the layout for following open positions. It helps me a lot to decide whether to close or hold a position. The advantage over my previous attempts to create a REVE indicator (published scripts), is that this version is concise because it reports and classifies all possible volumes and ranges, you see periods of drying out of volume, sequences of falter candles, occurrences of high morning volume, warning and confirming signals.. The assessment by script whether some volume should be considered low, normal, high or extreme gives an edge over using the standard volume bars.

Settings of REVE Cohorts

The default setting for lookback is ‘script sets lookback’ I put this in my indicators because I want them harmonized, the script sets lookback according to timeframe. The tooltip informs which lookback will be set at which timeframe, you can enable a feedback label to show the current lookback. If you switch ‘script sets lookback’ off, you can set your own preferred user lookback. The script self-adapts its settings in such a way that it will show up from the very first bar of historical chart data, it adds volume starting at the fourth bar.

You can switch off volume cohorts, only range candles will show while the middle band disappears. Signals will remain if volume is present in the data. Some Instruments have no volume data, e.g. SPX-S&P 500 Index,, then only range candles will be shown.

Colors can be adapted in the inputs. Because the script calculates matching colors with more transparency it is advised to use 100 percent opacity in these settings.

Take care, Eykpunter

VIX Monitor [Zero54]NSE:BANKNIFTY1!

This is a simple but invaluable tool for both day traders and positional traders. VIX is about market expectations of volatility

The VIX is a very good and sound measure of risk in the markets. It gives these stock traders who are in intraday trading and short term traders an idea of whether the volatility is going up or going down in the market. They can calibrate their strategy accordingly. When the volatility is likely to shoot up sharply, the intraday traders run the risk of stop losses getting triggered quickly. Hence they can either reduce their leverage or they can widen their stop losses accordingly.

Also if you notice VIX is a very good and reliable gauge of index movement. If you plot the VIX and the Nifty movement you will see a clear negative correlation in the charts itself. Markets typically tend to peak out when the VIX is bottoming out and the markets tend to bottom out when the VIX is peaking out. This is a useful input for index trades.

You can use this simple indicator to monitor VIX real time. You can use it for short time frame intraday and also multi-hour, multi-day charts. You can also plot a moving average to gauge the VIX trend.

Also is the ability to monitor, Nifty and BankNifty the same way you are able to monitor the VIX (as explained above). The overall market moves in correlation with these main Indexes. So if you are trading a specific counter, you can also keep an eye on the index to get an idea where the counter may be going next.

The source code is open, please feel to modify or re-use as you feel it’s necessary. Any changes, improvements, bugs, please let me know.

Please like/boost this indicator and also add your comments, if you find it useful.

Daily Factor Indicator [CC]The Daily Factor Indicator was created by Andrea Unger (Stocks and Commodities Jun 2023 pgs 26-31), and this is a new volatility indicator that compares the body, which is the absolute difference between the previous open and previous close, and the range which is the difference between the previous high and previous low. The indicator is calculated by dividing the body and range to determine the volatility for the previous bar. This indicator will range between 0 and 1. Values closer to 1 mean very high volatility, and values closer to 0 mean very low volatility. I have introduced a simple moving average strategy to decide buy or sell signals and colors. Darker colors mean the indicator is above the threshold level, and lighter colors mean the indicator is below the threshold level. Colors are shades of green when the price is above the moving average and shades of red when the price is below the moving average. Feel free to try out your own threshold level and general buy and sell signals.

Let me know if there are any other indicators you would like me to publish!

L&S Volatility IndexOverview

L&S Volatility Index is a tool designed to helps traders identify overpriced or underpriced moments in the market and adjust their trading strategies accordingly.

Calculations

This tool calculates how far the price is from the 21-period simple moving average as a ratio of the average historical volatility calculated over the last 21 candles.

How It Works

A L&S Volatility Index with a value greater than 30% may indicate that the asset is overpriced or underpriced relative to its average price.

How To Use

If the L&S Volatility Index > 30, the asset is overpriced or underpriced. This means that there is a good probability of initiating a mean reversion.

If the L&S Volatility Index < 30, the asset is in a fair price region. This means that it is acceptable to buy or sell in that price region.

Where To Use

Mean Reversion Strategy

Breakout Strategy

What Makes it Original

There is already an indicator that use a normalized calculation and a different approach to calculate historical volatility, whereas this script calculation is non-normalized and historical volatility is calculated using Don Fishback's formula. All calculations are used as originally described.

Credits

The L&S Volatility Index indicator was originally written by L&S Educação Financeira.

Historical Volatility calculation is based on the book "Odds: The Key to 90% Winners" written by Don Fishback.

Intraday Mean Reversion Money Performance indicatorThe diagram shows Money Performance when buying stocks for 10 000 at every buy signal from the Intraday Mean Reversion indicator.

The indicator is best used in combination with Intraday Mean Reversion Main Indicator

The rules for trading are: Buy on Open price if the Intraday Mean Reversion Main indicator gives a buy signal. Sell on the daily close price.

According to my knowledge it is not possible to create a PineScript strategy based on these rules, because the indicator is used on Day to Day graph. Therefore this indicator can be used to analyze Money performance of this strategy.

The lines show the performance of the Intraday Mean Reversion Strategy, based on the different levels in the strategy (from 0.5 Standard deviation to 1.1 standard deviation)

Using this indicator it is possible to find stocks that often reverse towards mean after open.

Use this strategy on stocks with high positive performance. Do not use on stocks with negative performance.

Intraday Mean Reversion MainThe Intraday Mean Reversion Indicator works well on certain stocks. It should be used for day trading stocks but need to be applied on the Day to Day timeframe.

The logic behind the indicator is that stocks that opens substantially lower than yesterdays close, very often bounces back during the day and closes higher than the open price, thus the name Intraday Mean reversal. The stock so to speak, reverses to the mean.

The indicator has 7 levels to choose from:

0.5 * standard deviation

0.6 * standard deviation

0.7 * standard deviation

0.8 * standard deviation

0.9 * standard deviation

1.0 * standard deviation

1.1 * standard deviation

The script can easily be modified to test other levels as well, but according to my experience these levels work the best.

The info box shows the performance of one of these levels, chosen by the user.

Every Yellow bar in the graph shows a buy signal. That is: The stocks open is substantially lower (0.5 - 1.1 standard deviations) than yesterdays close. This means we have a buy signal.

The Multiplier shows which multiplier is chosen, the sum shows the profit following the strategy if ONE stock is bought on every buy signal. The Ratio shows the ratio between winning and losing trades if we followed the strategy historically.

We want to find stocks that have a high ratio and a positive sum. That is More Ups than downs. A ratio over 0.5 is good, but of course we want a margin of safety so, 0.75 is a better choice but harder to find.

If we find a stock that meets our criteria then the strategy will be to buy as early as possible on the open, and sell as close as possible on the close!

Volatility patterns / Flowly Indicators- Overview

Volatility patterns detect various forms of indecisive price action, on a larger scale as a compressed range and on a smaller scale as indecision candles. Indecisive and volatility suppressing price action can be thought of as a spring being pressed down. The more suppression, the more tension is built and eventually released as a spike or series of spikes in volatility. Each volatility pattern is assigned an influence period, during which average and peak relative volatility is recorded and stored to volatility metrics.

- Patterns

The following scenarios are qualified as indecision candles: inside candles, indecision engulfing candles and volatility shifts.

By default, each indecision candle is considered a valid pattern only when another indecision candle has taken place within 3 periods, e.g. prior inside candle + indecision engulfing candle = valid volatility pattern. This measurement is taken to filter noise by looking for multiple hints of pending volatility, rather than just one. Level of tolerated noise can be changed via input menu by using sensitivity setting, by default set to 2.

Sensitivity at 1: Any single indecision candle is considered a valid pattern

Sensitivity at 2: 2 indecision candles within 3 bars is considered a valid pattern

Sensitivity at 3: 2 indecision candles within 2 bars (consecutive) is considered a valid pattern

The following scenarios are qualified as range patterns: series of lower highs/higher lows and series of low volatility pivots.

A pivot is defined by highest/lowest point in price, by default within 2 periods back and 2 periods forward. When 4 pivots with qualities mentioned above are found, a box indicating compressed range will appear. Both required pivots and pivot definition can be adjusted via input menu.

- Influence time and metrics

By default, influence time for each volatility pattern is set to 6 candles, a period for which spike(s) in volatility is expected. For each influence period, average relative volatility (volatility relative to volatility SMA 20) and peak relative volatility is recorded and stored to volatility metrics. All metrics used in calculations are visible in "Data Window "tab. Average and peak volatility during influence period will vary depending on chart, timeframe and chosen settings. Tweaking the settings might result in an improvement and is worth experimenting with.

- Visuals

By default, indecision candles are visualized as yellow lines and range patterns as orange boxes. Influence time periods are respectively visualized as colored candle borders, applied as long as influence time period is active. All colors are fully customizable via input menu.

- Practical guide

Volatility patterns depict moments of equal strength from both bulls and bears. While this equilibrium is in place, price is stagnant and compresses until either side initiates volatility, releasing the built up tension. On top of hedging and playing the volatility using volatility based instruments, some other methods can be applied to take advantage of the somewhat tricky areas of indecision.

Example #1: Trading volatility

Volatility is not a bad thing from a trading perspective, but can actually be fertile ground for executing trade setups. Trading volatility influence periods from higher timeframes on lower timeframes gives greater resolution to work with and opportunities to take advantage of the wild swings created.

Example #2: Finding bias for patterns

Points of confluence where it anyway makes sense to favor one side over the other can be used for establishing bias for indecisive price action as well. At face value, it makes sense to expect bearish reactions at range highs and bullish reactions at range low, for which volatility patterns can provide a catalyst.

Example #3: Betting on initiation direction

Betting on direction of the first volatile move can easily go against you, but if risk/reward is able to compensate for the poor win rate, it's a valid idea to consider and explore.

Historical VolatilityThis script calculates the historical volatility of a given market using the standard deviation of its returns over a specified lookback period.

The indicator also includes a volatility Simple Moving Average (SMA), a VIX SMA, and the VIX index as reference market.

The script uses the inputs from the user to adjust the calculation, such as lookback period, volatility SMA period, and reference market.

The Historical Volatility indicator can be a useful tool for traders and investors who want to measure the degree of variation of a market's price over time, which can help them to better understand market trends and potential risks. This script is licensed under the Mozilla Public License 2.0, which means that it can be used, modified, and distributed under the terms of this license.

Fixed Volatility OscillatorA fixed volatility plotter set to a 0-100 range - Plots the current volatility % using the formula to calculate volatility and stdev (standard deviation) based on the candle lookback.

The indicator is Fixed, which means that regardless of the chart, the volatility will be plotted on a percentage of 0% - 100% with a 101% threshold set to indicate a volatility reset. While the volume of volatility will change depending on the chart, the volatility will ALWAYS stay within this range.

if a plot exceeds 100% it should be marked as volatility reset - not an expansion

and should also be noted that the volatility spikes are also very inconsistent in volume and vary greatly.

The candle lookbacks on standard are organized be from 10 candles to 100 candles. I found the best results using the 50 candles lookback, and therefore have set it as the default value. These different values can be used to pull the information from the # of candles on the selected option - and therefore the volatility will be calculated from the number of candles selected.

// note for other people versed in pinescript

While this indicator may be useful in trading or strategies, it is more meant to incorporated into other scripts or used as a basis that can be further expanded on. The visuals are not built at all - for that purpose.

This script has not been listed as a library for the fact that it can be used as an actual indicator within a strategy - hope you enjoy.

Nonfarm [TjnTjn]This indicator will draw a line on your chart to show the Nonfarm announcement date and a line showing the Nonfarm announcement time for that day.

Because normally the Nonfarm announcement date is not simply the first Friday of the month. Because there are days Nonfarm days can be 8 or 9 or 10.

By checking the entire history of nonfarm announcements, I found some more rules such as if the first Friday of the month hits a holiday, the nonfarm day will be the friday of the following week. The previous months are 28, 29, or 30 days and if the first Friday of this month is on the 3, 2 or 1, the nonfarm day will be the friday of the following week.

Since this type of indicator is not available on the Tradingview library, I have put it up for everyone's convenience to backtest the price movement on nonfarm days to better support trading or simply to avoid trading at time of announed nonfarm.

Historical Volatility Scale [ChartPrime]This indicator outputs a visual scale representing the level of volatility in the market relative to the timeframe selected on the users chart. The method of volatility used is "historical volatility" which is calculated by taking the standard deviation of a series of "x" length which contains the current closing price divided by the previous closing price for all nodes. The output of the volatility is standardized by also running an additional percentrank calculation over the raw volatility values to allow the volatility scale to oscillate properly between its minimum of 0 and maximum of 100.

📗 SETTINGS

Length: The length determines how many bars/nodes should be considered when calculating the standard deviation. In simple terms, the higher the length, the less sensitive and less reactive the scale will be to current price action, and larger moves would be required to trigger the scale.

🧰 UTILITY

The arrow or "The Pin" will move upwards towards the "fire" emoji when the volatility is higher than the majority of values for the amount of bars back that you set the "length" setting to. Vise Versa for when the pin is lowering towards the "snooze" emoji, the volatility is less than the majority of nodes/values for the past "length" amount of values.

When the volatility is low, a trader could consider utilizing more leading indicators to make their trading decisions as opposed to lagging indicator such as trend indicators. When the volatility is low, the price action is consolidation which would be bad for a trend following strategy. Vise Versa for trend strategies, having a higher volatility may be better for such strategies.

Its important to remember that this indicator itself is a lagging indicator, in that it relies on historical data to showcase the current state of the markets volatility. This means that although the recommendation in the previous paragraph may make logical sense, it is not a guarantee that if the volatility is showcasing a trending market, that your trend strategies will necessarily be profitable.

Inter-Exchanges Crypto Price Spread Clouds (Tartigradia)Display variations in min-max and median values of high, low and close across exchanges. It's a kind of realized volatility indicator, as the idea is that in times of high volatility (high emotions, fear, uncertainty), it's more likely that market inefficiencies will appear for the same asset between different market makers, ie, the price can temporarily differ a lot. This indicator will catch these instants of high differences between exchanges, even if they lasted only an instant (because we use high and low values).

Compared with my other "Inter-Exchanges Crypto Price Spread Deviation" indicator, this one overlays directly on the chart, and offers a different take based on the same premisses. Instead of summarizing volatility via standard deviation, here we display clouds of the range of values that were observed.

A big advantage of this approach is that it can also be used to determine safe stop loss levels, especially the values of percentile rank (i.e., what are the high values that were observed in at least 50% of exchanges?).

Indeed, all price levels are displayed in the indicator's status bar:

green for high values,

red for low values,

aqua for median,

purple for average,

The first two values are max and min values of high across exchanges (in green).

The next two values are max and min of low across exchanges (in red).

The next two values are median (aqua) and average (purple).

The last two values are percentile rank values for high (green) and low (red) respectively.

Another advantage is that the high (green) vs low (red) clouds can be seen as representing the buying or selling pressure respectively across exchanges, and this may in itself provide a signal to know whether one side is winning.

Link to my other complementary indicator:

Compared to other inter-exchanges spread indicators, this one offers two major features:

The symbol automatically adapts to the symbol currently selected in user's chart. Hence, switching between tickers does not require the user to modify any option, everything is dynamically updated behind the scenes.

It's easy to add more exchanges (requires some code editing because PineScript v5 does not allow dynamical request.security() calls).

Limitations/things to know:

History is limited to what the ticker itself display. Ie, even if the exchanges specified in this indicator have more data than the ticker currently displayed in the user's chart, the indicator will show only a timeperiod as long as the chart.

The indicator can manage multiple exchanges of different historical length (ie, some exchanges having more data going way earlier in the past than others), in which case they will simply be ignored from calculations when far back in the past. Hence, you should be aware that the further you go in the past, the less exchanges will have such data, and hence the less accurate the measures will be (because the deviation will be calculated from less sources than more recent bars). This is thanks to how the array.* math functions behave in case of na values, they simply skip them from calculations, contrary to math.* functions.

Volatility Gap TrackerThe Volatility Gap Tracker ( *VGT ) indicator calculates the historical volatility of an asset using the standard deviation of the natural logarithm of the closing price relative to the previous period's closing price. *VGT visualizes the HV with gap lines to highlight when the current HV has increased or decreased significantly compared to the previous period, and adds labels to show the HV value for each of those bars.

Low HV calculated by *VGT can potentially signify a potential move up or down in the price of an asset. When HV is low, it indicates that the price of the asset has been relatively stable or range-bound over the specified period of time. This can sometimes be a precursor to a significant move in either direction, as the price may be building up energy to break out of its range.

*VGT can be used for any market that TradingView supports, including stocks, forex, and cryptocurrencies. It is especially useful for traders who want to identify periods of high volatility or sudden changes in volatility , which can indicate potential trading opportunities or risks. However, it's important to note that HV is a historical measure and may not always accurately predict future volatility .

The indicator can be used under various market conditions, but is especially useful during periods of high volatility , such as market crashes or major news events. It can also be useful for traders who want to monitor the volatility of specific stocks or assets over a longer period of time.

*VGT is provided for informational purposes only and is not a guarantee of future performance or accuracy. Traders should use multiple indicators and analysis methods to make informed trading decisions. Trading involves risks and traders should always conduct their own research and analysis before making any investment decisions.

Implied and Historical Volatility v4There is a famous option strategy📊 played on volatility📈. Where people go short on volatility, generally, this strategy is used before any significant event or earnings release. The basic phenomenon is that the Implied Volatility shoots up before the event and drops after the event, while the volatility of the security does not increase in most of the scenarios. 💹

I have tried to create an Indicator using which you

can analyse the historical change in Implied Volatility Vs Historic Volatility.

To get a basic idea of how the security moved during different events.

Notes:

a) Implied Volatility is calculated using the bisection method and Black 76 model option pricing model.

b) For the risk-free rate I have fetched the price of the “10-Year Indian Government Bond” price and calculated its yield to be used as our Risk-Free rate.

BTC Performance Table / BTC Seasonality Visualization

This script visualizes Bitcoins "seasonality", in form of a colored table (based on the idea from "BigBangTheory")

The history table shows you which months do statistically perform better/worse in comparison to other months.

How to use this script:

Choose ticker "BLX" ("BraveNewCoin Liquid Index for Bitcoin").

Set the charts time frame to weekly or daily. Tables position on the screen and its colors are configurable.

Table explanation:

Cells show whether a gain or a loss occured from month to month, since BTC came out in 2010.

The price difference, between monthly open and monthly close, determines the cell color (negative -> red, positive -> green).

The year column shows total gain (green) or loss (red) for that particular year.

Each value is presented as a rounded percentage number.

How this script works:

The script calculates the price difference between each monthly and yearly open and close, storing those numbers inside arrays.

Then it populates the table, by using those numbers and doing the cell coloring (there will be a yellow cell, in case no change should occur).

German Short-Description

Prozentuale Übersicht in Tabellenform, der monatlichen, sowie jährlichen, Performance des Bitcoin (basierend auf der Idee von "BigBangTheory").

Hierdurch wird die "Saisonalität" des Bitcoin sichtbar. D.h. welche Monate des Jahres, im Vergleich zu anderen Monaten, statistisch gesehen öfter positiv/negativ schließen.

Zwecks vollständiger Darstellung muss der Ticker "BLX" ("BraveNewCoin Liquid Index for Bitcoin") im weekly oder daily time frame aktiv sein.

Cryptos Pump Hunter[liwei666]🔥 Cryptos Pump Hunter captured high volatility symbols in real-time, Up to 40 symbols can be monitored at same time.

Help you find the most profitable symbol with excellent visualization.

🔥 Indicator Design logic

🎯 The core pump/dump logic is quite simple

1. calc past bars highest and lowest High price, get movement by this formula

" movement = (highest - lowest) / lowest * 100 "

2. order by 'movement' value descending, you will get a volatility List

3. use Table tool display List, The higher the 'movement', the higher the ranking.

🔥 Settings

🎯 2 input properties impact on the results, 2 input impact on display effects, others look picture below.

pump_bars_cnt : lookback bar to calc pump/dump

resolution for pump : 1min to 1D

show_top1 : when ranking list top1 change, will draw a label

show pump : when symbol over threhold, draw a pump lable

🔥 How TO USE

🎯 only trade high volatility symbols

1. focus on top1 symbol on Table panel at top-right postion, trading symbols at label in chart.

2. Short when 'postion' ~ 0, Long when 'postion' ~ 1 on Table Cell

🎯 Monitor the symbols you like

1. 100+ symbols added in script, cancel remarks in code line if symbol is your want

2. add 1 line code if symbol not exist. if you want monitor 'ETHUSDTPERP ', then add

" ETHUSDTPERP = create_symbol_obj('BINANCE:ETHUSDTPERP'), array.unshift(symbol_a, ETHUSDTPERP ) "

🎯 Alert will be add soon, any questions or suggestion please comment below, I would appreciate it greatly.

Hope this indicator will be useful for you :)

enjoy! 🚀🚀🚀

Average True Range PercentWhen writing the Quickfingers Luc base scanner (Marvin) script, I wanted a measure of volatility that would be comparable between charts. The traditional Average True Range (ATR) indicator calculates a discrete number providing the average true range of that chart for a specified number of periods. The ATR is not comparable across different price charts.

Average True Range Percent (ATRP) measures the true range for the period, converts it to a percentage using the average of the period's range ((high + low) / 2) and then smooths the percentage. The ATRP provides a measure of volatility that is comparable between charts showing their relative volatility.

Enjoy.

OHLC ToolOHLC Tool allows you to display Current or Historical OHLC Values as horizontal lines that extend to the right on your chart.

Features

Variable Lookback to display a specific historical bar's values. Default = 1 (Previous Candle)

Customizable Timeframe to view HTF Candle values.

Custom Line Colors, Styles, and Thicknesses.

Price Scale Value Display Capability.

For displaying the line values and labels on the price scale you will need to enable:

"Indicator and financials name labels"

and

"Indicator and financials value labels"

These options are found in the Price Scale Menu under Labels. Price Scale Menu > Labels

When you do this you will notice your other indicator values will also be on the price scale,

if you wish to disable these, go to the indicator settings under the "Style" Tab, Uncheck the "Labels on price scale" box.

Indicator Settings > Style > "Labels on price scale"

Enjoy!

Volatility Compression Ratio by M-CarloHello traders. I created this simple indicator to use as a FILTER.

He does not provide any operational signals but tells us if we are in a period of volatility compression or expansion and it can work on all market.

This filter works great for all strategies that work on breakouts

The concept is this: I will enter at breakout of a price level that I consider important, only if there is a volatility compression and not in the case of expansion of volatility.

Technically the calculation is very simple:

Step 1: I calculate the ATR at "x" periods, I set 7 by default because I get better results but you can change it as you like using the "atr length" field. You can also choose whether to calculate the ATR via RMA, SMA or EMA.

Step 2: I Calculate a simple average of the previous ATR over a longer period, longer period than set with the "length multiplier" parameter, which multiplies the "atr length" value by "x" times. Here I set the default 3 but you can change it as you like.

Step 3: I divide the ATR value calculated in step1 by its long-term average calculated in step2, obtaining a value that will oscillate above and below the value of 1

So:

if the indicator is above the value of 1 it means that volatility is expanding

If the indicator is below the value of 1 it means that we are in a period of volatility compression (and as we know volatility explodes sooner or later)

If you have any questions write to me and I hope this filter helps you! Have good Trading!