RSI + MA StrategyHello, everyone!

We have just released an innovative strategy for TradingView. It allows you to facilitate the trading process when you have to use both indicators.

This strategy is:

User-friendly

Configurable

Equipped with the combination of Relative Strength Index (RSI) and Moving Average (MA) indicators

Designed with all required functions to manage positions

Features

The RSI+MA strategy can:

Identify entry points for Long and Short positions.

Depict RSI and MA values concerning each other.

Reduce visual congestion and import usability thanks to using a combo of 2 indicators.

Allow using pivot trading. The RSI+MA strategy will enter a Long position according to the Short position conditions. And vice versa.

Note! If you want to open a Long position, the RSI line should cross MA from top to bottom. If you want to open a Short position, RSI has to cross MA from bottom to top.

Parameters

We have equipped our strategy with more than 14 additional parameters. So, you can configure the EA according to your needs!

Inputs :

Use Reverse Trade — allows swapping Long and Short positions opening conditions.

Resolution — allows you to view an indicator with data on a higher or lower timeframe on the current chart.

RSI Length

RSI Source: Open, High, Low, Close, HL2, HLC3, OHLC4

Show MA — allows you to enable or disable MA displaying.

MA Length

MA Offset

Style:

RSI — RSI indicator line color and style settings.

MA — MA indicator line color and style configuration.

Upper Band — allows customizing line style, color, and RSI upper bound value.

Lower Band — allows you to customize line style, color, and RSI lower bound value.

Background — background color setting within the RSI upper and lower borders.

Precision — number of decimals for RSI values.

Note! Try RSI+MA on your demo account first before going live.

Oscillatori

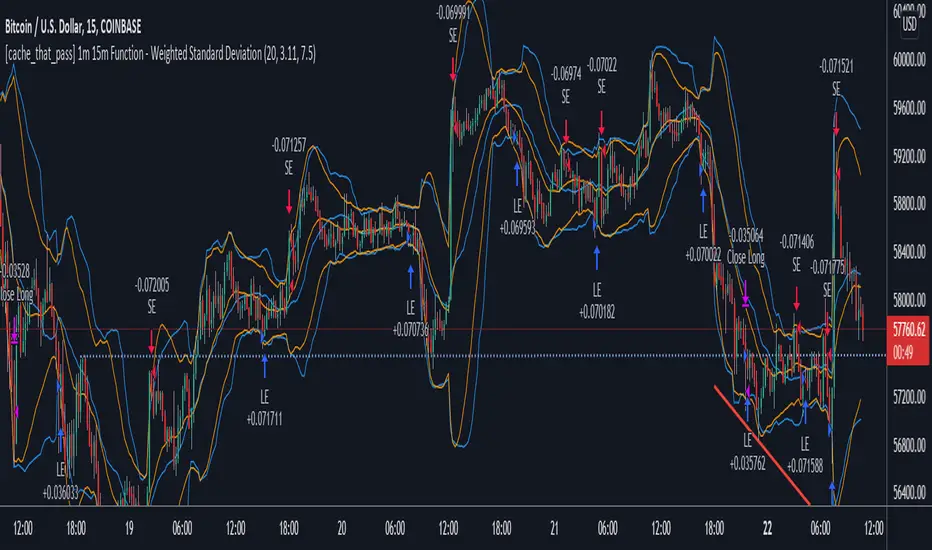

[cache_that_pass] 1m 15m Function - Weighted Standard DeviationTradingview Community,

As I progress through my journey, I have come to the realization that it is time to give back. This script isn't a life changer, but it has the building blocks for a motivated individual to optimize the parameters and have a production script ready to go.

Credit for the indicator is due to @rumpypumpydumpy

I adapted this indicator to a strategy for crypto markets. 15 minute time frame has worked best for me.

It is a standard deviation script that has 3 important user configured parameters. These 3 things are what the end user should tweak for optimum returns. They are....

1) Lookback Length - I have had luck with it set to 20, but any value from 1-1000 it will accept.

2) stopPer - Stop Loss percentage of each trade

3) takePer - Take Profit percentage of each trade

2 and 3 above are where you will see significant changes in returns by altering them and trying different percentages. An experienced pinescript programmer can take this and build on it even more. If you do, I ask that you please share the script with the community in an open-source fashion.

It also already accounts for the commission percentage of 0.075% that Binance.US uses for people who pay fees with BNB.

How it works...

It calculates a weighted standard deviation of the price for the lookback period set (so 20 candles is default). It recalculates each time a new candle is printed. It trades when price lows crossunder the bottom of that deviation channel, and sells when price highs crossover the top of that deviation channel. It works best in mid to long term sideways channels / Wyckoff accumulation periods.

RSI StrategySimple way how to use RSI and MA indicators for trading.

What we use:

• RSI

• SMA calculated by RSI (title: SMA_RSI)

• Delta of RSI and SMA_RSI (title: delta)

• SMA calculated by delta of RSI and SMA & RSI (title: SMA_RSI2)

Logic:

Upon the fact that we use the difference between two indicators that have similar values ( RSI and SMA_RSI), we get number around zero. Next, result is smoothed by calculated the SMA . This is the blue/purple line that appears on the chart - SMA_RSI2.

The trade open when SMA_RSI2 cross over the threshold. The trade close when SMA_RSI2 cross under the threshold below.

Also, the usual EMA 200 is used as a filter, which you can switch on or switch off.

No-lose trading targets (Based on EoRfA) By Mustafa ÖZVERI simulated the NLTTa_EoRfA indicator with the Bitcoin-USD

For details about the indicator, visit my profile on tradingview

For Simulation, with default settings, we order

When on Long setup and price on green area

- open a long position that closes on red area

When on Short setup and price on red area

- open a short position that closes on green area

And we got

- about 15% profit

But only this value can not guarantee good results for trading. BE CAREFUL

Smoothed Waddah ATR~~~All Credit to LAZY BEAR for posting the original Script which is an old MT4 indicator.~~~~

No this system does not repaint... if it does let me know. Either the code is wrong or you are using a repainting chart such as renko candles.

*PURPOSE*

This Is an "Enhanced or Smoothed" version of the script that captures the heiken-ashi closing price as its main calculation variable. While using normal bar or line charts. Enhancements integrate trade filters to reduce false signals.

*WHAT TYPE OF TRADING STRATEGY IS THIS?*

This is a Long Only, Trend Trading System. Is intended to be applied to Charts/Timeframes that produce sustainable trends for which ever asset you are trading.

*NOTE OF ADVICE REGARDING SETTINGS*

Settings can be tweaked but I have found that best results come with the given settings. If a chart is too choppy to trade this indicator successfully, it is advised not to change the settings but either find a different timeframe or different asset to apply this strategy to.

TLDR

Indicator measures the change of the MacD (difference between MAC D of given EMA's) and compares it to the difference between the Upper and Lower Bollinger bands. Green bar over trigger line= entry. Red bar over trigger line = close.

*SETTINGS AND INPUTS*

-MacD of HeikenAshi chart (will always be of the Heikenashi chart even when applied to different chart type)

sensitivity = input(150, title='Sensitivity') =range should be (125-175)multiplier so that MacD can be compared to BB

fastLength = input(20, title='MacD FastEMA Length')

slowLength = input(40, title='MacD SlowEMA Length')

-Bollinger Band of currently used price chart type

channelLength = input(20, title='BB Channel Length')

mult = input(1.5, title='BB Stdev Multiplier')

-14 Period RSI Trade Filter (set to 0 to Disable)

RSI14filter = input(40, title='RSI Value trade filter') =only gives entry when RSI is higher than given value

*ABSTRACT & CONCEPT*

TLDR - Indicator measures the change of the MacD (difference between MAC D of given EMA's) and compares it to the difference between the Upper and Lower Bollinger bands. Green bar over trigger line= entry. Red bar over trigger line = close.

Indicator plots -

Bars are the change in the MAC D and the indicator line is the difference in the BB.

When Bars are higher than the indicator line then it is considered a trend "Explosion"

Green Bars are Trend Explosion to the upside, Red Bars are Trend explosion to the downside.

GENERAL DETAIL-

the core calculation is measuring the change in MacD of current candle compared to the MacD of two previous candles.

This value is multiplied by the sensitivy so it can be compared to the change in Bollinger Band Width.

if the MACD change is positive then you get a green/lime bar for that value. If the MacDchange is negative you get a red/orange bar for that value.

and are determined by whether the actual change is increasing in that direction or decreasing. (bars getting taller or bars getting shorter)

Entry signal for long is A positive change in MACD difference (Green bar) that is greater than the change of the bollinger band (orange signal line) AND if the RSI value is above your filter.

Close signal or Trend Stop Warning Signal is given when a Negative MacD Difference (red bar) is greater than the change of the bollinger band (orange Line)

*CONSIDERATIONS AND THOUGHTS*

I have over 150 iterations of this indicator and this is the most consistent and best version of settings and filters I was able to generate. I built this indicator specifically for 3 charts. SPY monthly, QQQ monthly, BTC 3 Day. However this indicator works well on any long term bullish chart. (tech stocks are great) .

Trend trading systems are intended to be homerun hitting, plunge protecting indicators that allow for long legs and expanding volatility. This indicator does this as the trigger line is Dynamic with the expansion and contraction of the bollinger band.

I do not take every signal specifically not the close signals. Instead they more like warnings in ultra bullish environments.

If i had to pair this indicator with any other filter than the RSI, it would be a long term moving average i.e. the 50 week or equivalent for your chart. signals above rising moving averages means that you are trading with an upward trending market.

Hope this helps. Happy trades.

-SnarkyPuppy

Simple EMA20 Strategy + StochasticThis is a Trend Following Strategy.

The intent of this strategy is to catchthe price as it trends higher than the 20-period EMA and sell immediately after the price closes below it.

I have implemented calculations from Stochastic to make sure the price is coming from an oversold area.

There is also a check to see if the 20-period EMA is trending higher than before.

Supertrend + RSI Strategy [Alose]This strategy combines the best of both indicators (Supertrend & RSI).

As we know, Supertrend is excellent at finding changes in the market trend and thus finding the best entries, however in my opinion it has a great weakness and it is that it does not know how to find the best exit point.

For this reason I decided to combine it with the RSI that we know usually knows the highest and lowest rebound points of the price, thus managing to find the best exit point for the strategy.

The best thing about combining these 2 indicators is that our trades will obtain better profits in less time.

LONG ENTRY

When SuperTrend changes its direction and it is less than 0.

LONG EXIT

There are two ways to close the trade:

When RSI is overbought, you can choose the "Overbought Level " inside the strategy settings (Default: 72).

When SuperTrend changes its direction and it is grater than 0.

SHORT ENTRY (You can enable short entries in strategy settings)

When SuperTrend changes its direction and it is grater than 0.

LONG EXIT

There are two ways to close the trade:

When RSI is oversold, you can choose the "Oversold Level " inside the strategy settings (Default: 28).

When SuperTrend changes its direction and it is less than 0.

grid strategy longDesign ideas for the first edition:

Only go long, not short, choose a time period when the general trend is up. The default grid size is 1x ATR, the next one, two, and three grids will take orders, and the fifth grid will stop loss. When the empty position reaches the upper grid, the grid as a whole rises.

Chinese Introduction:

只做多、不做空,选择大趋势向上的时间段。网格大小默认为1倍ATR,往下1、2、3个网格吃单,第5个网格止损。空仓时到达往上一个网格则网格整体抬升。

Sideways Strategy DMI + Bollinger Bands (by Coinrule)Markets don’t always trade in a clear direction. At a closer look, most of the time, they move sideways. Relying on trend-following strategies all the time can thus lead to repeated false signals in such conditions.

However, before you can safely trade sideways, you have to identify the most suitable market conditions.

The main features of such strategies are:

Short-term trades, with quick entries and quick exits

Slightly contrarian and mean-reversionary

Require some indicator that tells you it’s a sideways market

This Sideways DMI + Bollinger Bands strategy incorporates such features to bring you a profitable alternative when the regular trend-following systems stop working.

ENTRY

1. The trading system requires confirmation for a sideways market from the Directional Movement Index (DMI) before you can start opening any trades. For this purpose, the strategy uses the absolute difference between positive and negative DMI, which must be lower than 20.

2. To pick the right moment to buy, the strategy looks at the Bollinger Bands (BB). It enters the trade when the price crosses over the lower BB.

EXIT

The strategy then exits when the move has been exhausted. Generally, in sideways markets, the price should revert lower. The position is closed when the price crosses back down below the upper BB.

The best time frame for this strategy based on our backtest is the 1-hr. Shorter timeframes can also work well on certain coins that are more volatile and trade sideways more often. However, as expected, these exhibit larger volatility in their returns. In general, this approach suits medium timeframes. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

You can execute this strategy on your favourite exchange at coinrule.com.

RSI multitimeframe SMA crossoverStrategy based on the multi timeframe equally weighted RSI moving averages turned into single average and then cross of the 2 combined outputs, seems to be promising, default settings work good on 5m chart(better entry) but very filtered trade amount. If you want to use it on different timeframes be my guest and mess with adjustments, pretty much every aspect of strategy is adjustable, idea is same. If somebody liked the idea and able to improve it - share with me :)

John F. Ehlers Center Of Gravity Balanced by [DM]Greetings to all colleagues.

I share this indicator turned into a strategy, (this is one of my first strategies so some inputs are missing and others are somewhat archaic)

this cog is formed by three signals which can be reduced by dividing by phi

Available settings:

Length setting for signal

Trigger parameter setting for strategy

stoploss settings

trailing stop settings

tp settings

I hope it fuels your curiosity

The Center of Gravity (COG) indicator is a technical indicator developed by John Ehlers in 2002, used to identify potential turning points in the price as early as possible. In fact, the creator John Ehlers claims zero lag to the price, and the smoothing effect of the indicator helps to spot turning points clearly and without distractions.

DI Crossing Daily Straregy HulkTradingSimple strategy based on crossing DI+ and DI- and Average True Range.

Long entry when DI+ crossover DI-

Short entry when DI+ crossunder DI-

Stop Loss and Take Profits based on Average True Range.

Default values are 1*ATR(14) for stop loss and 2*ATR(14) for Take Profit.

Risk reward 1 to 2 ratio.

Recommended default values, but you can change it if you want.

Recommended timeframe - 1D.

Script was tested on BTCUSDT pair and have a 2.4 profit factor.

TradingGroundhog - Strategy & Fractal V1#-- Public Strategy - No Repaint - Fractals -- Short term

Here I come with another script, more simple than Wavetrend V1. You will love it.

#-- Synopsis --

Another simple idea, on a small time frame (15 min) we buy when the opening price goes below a Bottom fractals and sell when it goes over a Top fractals, but as this script do not use Wavetrends. You should stop by your self to use the script during long lasting downtrends.

I developed the strategy using BTC /EUR 3 MIN BINANCE but it can be applied to many other cryptos, I don't know for forex or others. You can use it for short term (to a month of uptrend) and automated trading.

#-- Graph reading --

And now, how to read it ?

Fractals:

Yellow Flags occur when the opening price goes below a Bottom fractal , it means Buy.

White Flags appear when the opening price goes over a Top fractal , it means Sell.

#-- Parameters --

*** Parameters have been intensively optimized using 10 cryptocurrency markets in order to have potent efficiency for each of them. I would recommend to only change the Can Be touch parameter. For the others, I don't recommend any modifications. The idea behind the script is to be able to switch between markets without having to optimize parameters, less work, easy to target active crypto and therefor limit the risks. ***

Can be touch :

'Filter fractals' : Activate or Disable the filtering fractal operation. If Enable, buy during less risky periods. (Activate is often better)

Can be touch but not necessary :

'VolumeMA' : The Volume corrector used by the fractals

'Extreme window' : The number of price individuals to look for if we want to remove extreme fractals.

Not to touch :

'Long Sop Loss (%)' : The minimal difference of price between a Fractal bottom and the opening price to buy.

#-- Time frame --

Should be used with the following time frames depending on the necessity:

1 MIN

3 MIN (Preferred with the parameters set)

5 MIN

#-- Last words --

The script can be set up to send Tradingview signals to 3comma just by adding comment = " " in strategy.close_all() and strategy.entry().

Good trades !

Disclaimer (As it should always be one to any script)

***

This script is intended for and only to be used for personal purposes only. No such information provided by it constitutes advice or a recommendation for any investment or trading strategy for any specific person. There is no guarantee presented or implied as to the accuracy of specific forecasts, projections, or predictive statements offered by the script. Users of the script agree that its original developer does not take responsibility for any of your investment decisions. Please seek professional advice before trading.

***

# Here are the results from the 20rst of September 2021 with 100% of equity on the BTC /EUR 3 Min and with a capital of 10 000 EUR. So almost, one month.

# As I saw, it goes from +30% to more than +160% (the great SHIB) depending on the selected crypto. It may be negative if you spot a downtrend.

Volume Difference Delta Cycle OscillatorVolume Difference Delta Cycle Oscillator indicator:

Using the power of my Volume Difference Indicator and standard deviations based on Bollinger Bands and more, we present this wonderful indicator with the following features:

Price Action Histogram: This is the bread and butter of this graph, if the PAH is above 0, this is considered a BULL cycle, and if below 0, this is considered a BEAR cycle. The histogram will move up and down based on the Histagram settings you set in the properties field. Be careful, we advise using default settings.

Custom Overbought & Oversold Lines:mean

These lines can be used to identify when to buy and sell the security, and help you make sense of the action of the histogram. Change the color, size, and linewidth!

These lines are what are used to perform the trades with the strategy as well, so if you change them, they will make an impact on the strategy itself.

EzSpot Background:

Do you want to turn your brain off and just trade when you you're inside an Overbought or Oversold line? Awesome! Turn on EzSpot backgrounds, and when it's green, go long, when it's red go short! Simple as that!

How it works:

By taking the Delta of the Volume Difference Indicator we're able to find the rate of change of the amount of change of volume, allowing us to see changes in volume before price changes. To add onto these, we supercharge it by taking the output of this line as the input source of bollinger bands which we use to output the %B of the Delta of the Volume Difference Indicator.

Separately, we calculate the %B of the current close to use later.

The final step is taking the second %B (which is an indication of where price lies on the curve of historical price data), and from it subtract the first %B, which allows us to visualize the standard deviation of the closing price, minus the standard deviation of Delta of the Volume Difference , which in essence allows us to see when volume changes but price does not and vice versa.

This final output is then plotted along with an over bought and over sold line, which we use to perform our trades on.

Simplified: This indicator shows the cycles of price action - volume based on the rate of the rate of volume changes based on price and the closing price.

Super Simple: Notice when volume increases but price hasn't, and vice versa with this indicator.

RSI StrategyThis RSI strategy is different than most in that it doesn't pick a buy signal based on the RSI rising above a specific number (usually 30). Instead, it creates a 14 day exponential moving average of the Relative Strength Index and uses the following two conditions together to trigger a buy:

Entry conditions:

Condition1: Rising of the RSI's moving average for (user defined) candles in a row

Condition 2: The RSI is < 70

The reasoning behind condition 1 is that we are trying to buy into a rising trend, the moving average helps to confirm the trend, whereas the RSI rising above a specific number (usually 30) gives us no real indication that the asset will increase and produces less wins overall. The reasoning behind condition 2 is to avoid buying at the top of a climb.

Exit conditions:

Condition 1: The RSI moving average is falling

Condition 2: Close < Trailing stop activation Level

Condition 3: We have at least (user defined) % profit

The reasoning behind sell condition 1 is a falling RSI moving average (down trend starting). The close has to be under the trailing stop activation level, if we've triggered the trailing stop, we want the trailing stop to do it's job and not exit the trade until the trailing stop takes us out. The reasoning behind condition 3 is to not exit without at least some profit (user defined).

Supertrend + Stoch StrategyA strategy using ema , supertrend and stochastic .

Long entry conditions:

1. EMA 25 > EMA 50 and EMA 100 > EMA 100.

2. Supertrend indicator is green.

3. Stochastic k line cross over d line.

Long stop: the lowest price of the last k

Supertrend + Stoch Strategy Multi-pair Signal AlarmBITSTAMP:BTCUSD

An entry alarm on Supertrend Stoch Strategy . It can monitor 10 trading pairs in one alarm.

Use this script on any trading pair and deploy the alarm. The alert comment shows the pair name, direction, entry point, sl/tp, and percentage of your position you should cost.

I currently use it as a signal for my grid trading.

Rising ADX strategyI have always been a huge fan of ADX. Its good for finding out good trending moves.

But it has been said that only ADX after 20 or 25 is good for trending market, but few trend gets completed at that level.

So I have come up with a logic to find out the rising ADX. This could be used to determine the trending moves from the start.

Buy signal:

When close is greater than moving average 1 and 2. This moving average can be SMA, EMA, WMA or HMA.

When ADX is greater than the threshold range. I have taken 10 as my minimum range.

Of course important of all ADX should be rising which implies trend is about to start.

Buy exit:

When close is less than moving average 1 and 2. This moving average can be SMA, EMA, WMA or HMA.

When ADX is lesser than the threshold range. I have taken 10 as my minimum range.

ADX falling which implies trend is about to end.

Sell signal:

I don't repeat the above logic again.

Everything similar to buy signal except above moving average. For selling it should be below moving average.

Strategy can be tested for long and short sides.

Note: No Repainting as the logic is very simple.

Using this script we can identify the best timeframe the script trend yields profit.

Test and provide your comments.

Cumulative RSI StrategyI suppose nothing drives a point home like a 10+ year backtest! A couple of weeks ago I published a custom indicator called the Cumulative RSI. This indicator was straight out of chapter 9 of "Short Term Trading Strategies That Work." Today I am publishing a basic sample strategy in that uses the Cumulative RSI as its only entry and exit signals on a Nasdaq 100 leveraged index ETF (TQQQ). In this example, the indicator is being used as a longer term strategy with just 10% leverage over the account equity and a $25k start balance.

If I had it 10 years ago I would probably be retired! I'm sharing because I've found that it can provide an edge when determining exit/take profit points for trades. Many traders wait for a price reversal / trailing-stop to exit a trade when it starts losing. I've found that, using tools like the Cumulative RSI, you can achieve better exit points over the long term. Disclaimer: Even though this example significantly beats buy and hold, I wouldn't advise using it as a stand-alone strategy without significant additions/modifications to strategy and risk management functions.

RSI Overbought Oversold Divergence Strategy w/ Buy/Sell SignalsThis indicator is a copy of my RSI Overbought/Oversold Divergence Indicator with-Alerts

Only difference is that the alerts are disabled, instead it uses tradingviews strategy tester signals

If you want alerts just use the other indicator

Williams Fractals StrategyThis indicator made with using Williams Fractals, 20 50 100 Moving Averages and Relative Strength Index. You can easily find entry points by using Long (L), Short (S) signals.

Note : Settings are optimized for BTC:USDT Perpetual 15min TF. For use different pairs or TFs you may need to change settings.

inside bar strategy Wıth SL-TP Based on strat bars to enter trades, you can use it with very low stop loss level and try all coins in daily frequency