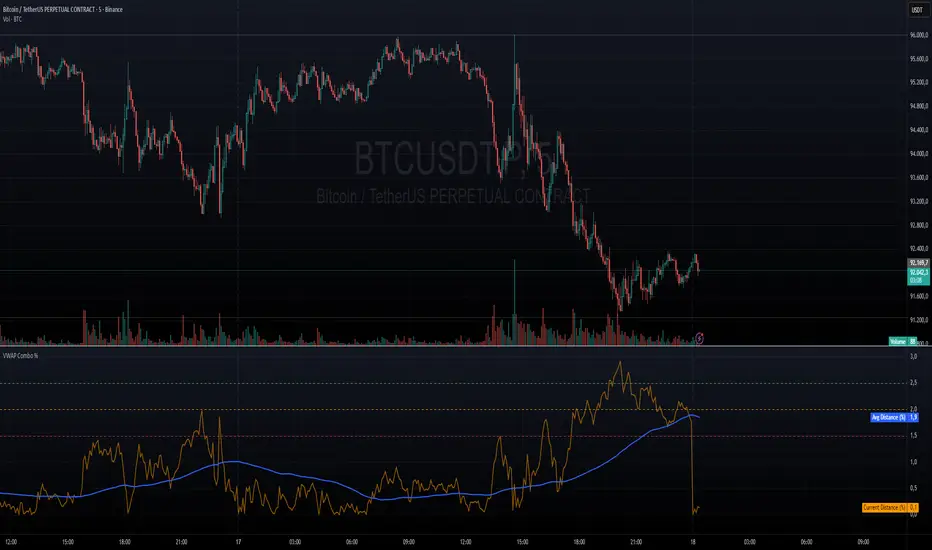

VWAP + VWAP Distance Avg + Alert Lines (%)VWAP Distance & Average Distance Indicator – Detailed Description

The VWAP + VWAP Distance Avg + Alert Lines (%) indicator is designed to measure the distance of the current price from the VWAP (Volume Weighted Average Price), as well as the average distance over a specified period. This tool is particularly useful for traders who use the VWAP as a magnet for price, helping to identify potential trend changes and areas where price may revert toward the VWAP.

Key Features

Current Distance (%)

Calculates the absolute percentage difference between the current price and the VWAP

This line shows how far the price has moved away from the VWAP at any given moment.

Average Distance (%)

Calculates a simple moving average (SMA) of the distance over a specified lookback period.

This provides a reference for typical price deviations from the VWAP, helping traders assess whether the current distance is unusually high or low.

Alert Lines (%)

Allows up to three customizable horizontal alert lines, which can be turned on or off individually.

Each line can be configured with:

Value in percent.

Color.

Line thickness.

These lines serve as visual thresholds, helping traders detect extreme deviations from the VWAP that may precede trend reversals.

Use Case – Detecting Potential Trend Changes

Traders often treat the VWAP as a price magnet, where price tends to revert after significant deviations.

When the current distance exceeds typical average levels or crosses an alert line, it can signal that the price may revert toward the VWAP, potentially indicating a shift in trend or a high-probability mean-reversion scenario.

Disclaimer

This indicator is provided for educational and analytical purposes only. It does not constitute financial advice, and trading decisions are always the sole responsibility of the individual trader. Users should carefully evaluate market conditions and their own risk tolerance before taking any trade.

Better used with VWAP on chart , and be careful around the end of session, for now this works just for session...

still improving on this....

Volume

Delta Manipulation FootprintIntroduction

The Delta Manipulation Footprint indicator highlights significant shifts in volume delta between consecutive candles, helping traders visually identify potential market manipulation or strong buying/selling pressure. By analyzing the difference in buy and sell volume (delta) and its changes over time, this indicator reveals aggressive market behavior often associated with big players.

Key Features

- Calculates the absolute difference of volume delta between candles, maintaining the direction of change.

- Uses a customizable moving average and threshold multiplier to filter meaningful volume shifts.

- Colors candles green when delta difference is notably increasing, and red when decreasing, for clear visual signals.

- Fully overlays the main price chart, painting candles directly for intuitive interpretation.

How to Use

Apply this indicator to your price chart to instantly visualize periods of significant volume delta shifts. Look for green candles signaling rising buying pressure and red candles showing increasing selling pressure. Adjust the moving average length and threshold multiplier inputs to tune sensitivity to your trading style or particular market behavior. Use in conjunction with other price action and volume indicators to confirm signals and improve trade timing.

This tool is ideal for traders aiming to spot footprint-like manipulations in volume delta, aiding in the detection of institutional activity and potential market turning points.

Alpha VWAP Regime🔥 Alpha VWAP Regime — Institutional VWAP Strategy (Closed Source)

Alpha VWAP Regime is a multi-layered VWAP trading system that identifies the active market regime and adapts its signals based on institutional liquidity behavior.

This strategy is closed-source because it uses a proprietary combination of VWAP structures, anchored pivot logic, band deviations, and regime detection filters that are not publicly available.

🧠 How the Strategy Works (Conceptual Explanation)

This strategy does not rely on a single VWAP line.

Instead, it builds a VWAP matrix consisting of:

1) Session VWAP

Defines fair value for the current session.

Used to detect intraday directional bias.

2) Anchored VWAP (AVWAP)

Automatically anchored to swing highs and lows (pivot-based).

Tracks where large players accumulated or distributed positions.

3) VWAP Bands (±1σ and ±2σ)

Used as dynamic volatility envelopes:

±1σ = fair-value zone / no-trade area

±2σ = mean-reversion extremes

4) Market Regime Classification (ADX-based)

The strategy determines which environment the market is in:

Trending Regime: ADX above threshold

Ranging Regime: ADX below threshold

Breakout Regime: Volume-based breakout of AVWAP

Each regime activates a different entry model.

📌 Entry Logic (High-Level Overview)

Trend Mode

Triggered only when ADX confirms a trend.

Entries occur near VWAP or −1σ using price-action confirmation.

Mean Reversion Mode

Activated when the market is ranging.

Entries target the ±2σ deviation bands.

Breakout Mode

Triggered by price crossing AVWAP with above-average volume.

Used to catch institutional continuation moves.

ALL Mode

Combines the three models for a full adaptive system.

📉 Exits & Risk Management

All stops and targets use ATR-based volatility sizing

Trend trades aim for larger targets

Mean-reversion trades aim for smaller snapback moves

Breakouts use wider stops but high R:R

🔍 How to Use the Strategy

Load the script on a clean chart

Choose your preferred regime mode (Trend / MR / Breakout / ALL)

Optionally hide VWAP indicators and display signals only

Use realistic position sizing and commissions

Evaluate performance across multiple assets and timeframes

🔒 Why It Is Closed-Source

The code uses:

A custom anchoring engine

Multi-layered regime filters

Dynamic VWAP matrix

Prop logic for bias scoring

These components were built from scratch and form a unique decision model, so the source is protected.

🇸🇦 الشرح العربي لاستراتيجية Alpha VWAP Regime

Alpha VWAP Regime هي استراتيجية تداول مؤسسية متقدمة تعتمد على تحليل السيولة، وتحديد حالة السوق (Market Regime)، ودمج عدة طبقات من VWAP داخل نموذج واحد متكيف.

الهدف من الاستراتيجية هو التداول في المناطق التي يتواجد فيها المال الذكي، وتجنب التداول في المناطق العشوائية أو منخفضة الجودة.

________________________________________

🧠 كيف تعمل الاستراتيجية؟

الاستراتيجية لا تعتمد على VWAP واحد، بل تستخدم “مصفوفة VWAP” كاملة تتكوّن من:

1) VWAP اليومي (Session VWAP)

يُستخدم لتحديد القيمة العادلة خلال الجلسة، وتحديد الاتجاه اللحظي (Intraday Bias).

________________________________________

2) VWAP المثبّت (Anchored VWAP)

يتم تثبيته تلقائيًا على:

• القمم المهمة (Swing Highs)

• القيعان المهمة (Swing Lows)

ويساعد في تحديد مناطق تمركز المؤسسات، ومناطق الانعكاس أو الاختراقات الحقيقية.

________________________________________

3) نطاقات VWAP (±1σ و ±2σ)

تُستخدم كأغلفة ديناميكية للسيولة والتقلب:

• ±1σ = منطقة القيمة العادلة (Fair-Value Zone)

→ غالبًا منطقة غير مناسبة للتداول (No-Trade Zone)

• ±2σ = مناطق التشبّع الحركي (Extremes)

→ مناسبة لاستراتيجيات الانعكاس (Mean Reversion)

________________________________________

4) تصنيف حالة السوق Market Regimes

الاستراتيجية تستخدم مؤشر ADX لتحديد حالة السوق الحالية:

حالة السوق الوصف

Trending اتجاه واضح وقوي

Ranging تذبذب بدون اتجاه

Breakout اختراق مدعوم بحجم تداول

كل Regime يفعّل نموذج دخول مختلف داخل الاستراتيجية.

________________________________________

🎯 نماذج الدخول داخل الاستراتيجية

1) نموذج الاتجاه (Trend Mode)

يعمل فقط عندما يكون السوق في اتجاه حقيقي.

يعتمد على دخول Pullbacks قرب VWAP أو نطاق −1σ مع تأكيد شموعي.

________________________________________

2) نموذج الانعكاس (Mean Reversion Mode)

يعمل فقط عندما يكون السوق متذبذبًا (Range).

الدخول عند لمس ±2σ بهدف العودة نحو VWAP.

________________________________________

3) نموذج الاختراق (Breakout Mode)

يستخدم اختراقات Anchored VWAP

ولكن بشرط وجود حجم تداول أعلى من المتوسط (Volume Confirmation).

________________________________________

4) وضع الدمج (ALL Mode)

يجمع بين النماذج الثلاثة ويجعل الاستراتيجية متكيفة تلقائيًا مع كل حالات السوق.

________________________________________

📉 الخروج وإدارة المخاطر

تستخدم الاستراتيجية نظامًا ديناميكيًا لإدارة المخاطر:

• وقف الخسارة مبني على ATR

• الأهداف مبنية على طبيعة النموذج

• الصفقات الاتجاهية تستهدف R:R أعلى

• صفقات MR أقصر وأسرع

• صفقات Breakout أوسع ولكن مدعومة بزخم قوي

________________________________________

🧩 كيفية استخدام الاستراتيجية

1. ضع الاستراتيجية على رسم بياني نظيف بدون مؤشرات إضافية

2. اختر نموذج الدخول المناسب من الإعدادات

3. فعّل أو أخفِ خطوط VWAP حسب الحاجة

4. استخدم إعدادات مخاطرة واقعية

5. اختبر الاستراتيجية على عدة أسواق وفريمات

________________________________________

🔒 سبب إغلاق الكود

تم إغلاق الكود لأنها تعتمد على:

• محرك تثبيت AVWAP خاص

• نظام Regime Detection متقدم

• مصفوفة VWAP متعددة الطبقات

• منطق دخول/خروج خاص تم تطويره بالكامل

كل ذلك يتطلب حماية الملكية الفكرية، لذا تم نشرها Closed-Source.

BS by bigmmBS by bigmm is a powerful tool designed to track and display cumulative trading volumes for bullish (green) and bearish (red) bars over a user-defined period. This indicator provides valuable insights into market sentiment by quantifying buying and selling pressure through volume analysis.

Adjustable lookback period from 20 to 10,000 bars

Default setting of 500 bars for balanced analysis

Real-time calculation updates on each new bar

BUY Volume: Total volume of green bars (close > open)

SELL Volume: Total volume of red bars (close < open)

Interpretation:

Higher BUY Volume: Indicates stronger buying pressure

Higher SELL Volume: Suggests stronger selling pressure

Balanced Volumes: Shows equilibrium between buyers and sellers

Ideal For:

Swing traders analyzing medium-term trends

Position traders evaluating long-term market sentiment

Volume-based trading strategies

Market structure analysis

3 Band Volume matched Candles3 Band Volume matched Candles– is a clean, high-signal volume-based candle colouring system designed to highlight the extremes of market participation. Instead of using complex multi-band gradients, this simplified version focuses on what truly matters to scalpers and intraday traders:

🔵 Very Weak Volume (Exhaustion)

Shows when the market is running out of participation. These candles often appear near tops, stalled moves, fake breakouts, and areas where liquidity is drying up. Perfect for spotting potential reversals or rug-pull conditions.

⚪ Normal Volume (Baseline Flow)

Represents regular market activity. These neutral candles keep the chart clean and make the extremes stand out instantly.

🟥 Neon Hot-Red (High-Impact Volume)

Highlights moments of significant volume — intervention, aggression, absorption, stop hunts, or strong rejection wicks. These candles are critical for identifying real moves vs. fake ones, spotting wickbacks, and confirming momentum shifts.

Why This Tool Works

By focusing only on the very low and very high ends of market volume, the indicator cuts through noise and exposes the true behaviour behind each candle. Traders can instantly see:

When a move is losing strength

When a trend is topping or stalling

When big volume enters the market

When a wickback is driven by strong rejection

Whether a breakout is real or weak

When reversals are highly probable

This makes it ideal for scalpers, and anyone who trades fast-moving instruments

Customisation

Fully customisable weak/normal and normal/strong thresholds

User-defined colours for each band

Brightness control

Borders-only mode

Adjustable fill opacity

Optional corner legend for clarity

Effort HeatmapThe Effort Heatmap visualizes where meaningful, same-direction volume occurred inside an imbalance during strong directional movement.

Instead of analyzing total bar volume or traditional volume-at-price distributions, this tool reconstructs a simplified internal volume profile using lower-timeframe data.

When a Fair Value Gap forms during a high-volume displacement, the script highlights the portions of the imbalance candle where directional effort was concentrated and projects those regions forward as a heatmap.

The purpose of this indicator is not to predict price or represent institutional activity, but to offer a visual way to study how the market delivered volume inside a move that created an imbalance.

How It Works

1. Lower-Timeframe Volume Extraction

The indicator retrieves open, close, and volume data from a selected lower timeframe.

Only sub-candles that move in the same direction as the previous bar are considered, ensuring the heatmap reflects directional effort—not mixed volume.

2. Candle Body Binning

The FVG candle is divided into multiple horizontal bins.

Each lower-timeframe sub-candle contributes volume proportionally to the bins it overlaps, creating a vertical volume distribution for that bar.

3. Imbalance (FVG) Detection

A simple 3-bar displacement logic detects bullish or bearish imbalances.

An optional Z-Score filter ensures the heatmap only forms when volume is relatively elevated compared to recent history.

4. Heatmap Projection

When a qualifying imbalance occurs:

• The FVG bar’s volume distribution is normalized

• Only areas with relatively elevated volume are displayed

• Colored heatmap boxes are created and extend forward

• These boxes remain until price trades into or through them

This allows traders to observe how price interacts with past zones of concentrated directional effort.

What Makes It Different

Most volume tools focus on fixed session profiles, market-wide volume-at-price calculations, or bar-level volume totals.

The Effort Heatmap instead reconstructs a per-bar vertical volume distribution using lower-timeframe price action and displays it only when displacement occurs.

Rather than treating the candle as a single block of volume, the indicator highlights where inside the candle body volume was delivered while moving in the displacement direction.

This creates a unique visualization of directional effort that conventional profiles, OB/FVG indicators, and classic oscillators do not show.

How to Use It

1. Apply to any timeframe: The indicator works on all chart timeframes, but gains more detail when higher timeframes are used in combination with lower-timeframe volume data.

2. Identify displacement moments: When a bullish or bearish FVG forms with a high volume Z-Score, the heatmap will appear.

3. Observe the heatmap structure:

Each horizontal band represents the relative concentration of same-direction volume inside the previous candle.

4. Watch how price interacts with these zones:

Heatmap areas extend until price touches or trades through them, at which point they stop extending and are finalized.

5. Combine with your own analysis:

These areas can be used to study...

...how past directional volume clusters influence current movement

...structural reactions to zones of prior effort

...which parts of a displacement candle were most active

The indicator is a visual study tool, not a signal generator.

Settings

• Volume Source Timeframe

Chooses the lower timeframe used to reconstruct internal volume. Smaller timeframes give more detail; larger timeframes give smoother profiles.

• Z-Score Lookback

Controls how many bars are used to measure relative volume. Larger values make the volume filter stricter.

• Z-Score Threshold

Minimum relative-volume strength required to draw a heatmap. Higher values show only high-effort moves.

• Volume Filter (%)

Removes weaker bins based on how much volume they contain compared to the strongest one. Higher percentages = fewer but more meaningful zones.

• Bullish / Bearish Colors

Sets the base color for heatmap boxes depending on direction.

Advanced Intraday Darvas BoxThis indicator applies a modern Darvas Box strategy for intraday traders, using non-repainting pivot detection combined with strong filters to reduce chart noise:

Confirmed swing highs and lows: Boxes only form when genuine swing pivots appear, ensuring fully non-repainting signals.

Minimum box height: Small, "noise" boxes are filtered out using ATR multiples for meaningful zones.

Trend filter: Choose EMA, SMA, or VWAP to lock boxes and breakouts to market direction.

Volume confirmation: Boxes are only confirmed when volume is above a user-defined threshold, highlighting high-participation moves.

Breakout filter: Signals trigger only if the breakout candle closes substantially beyond the box, reducing false breakouts.

Limited box display: Recent boxes only, keeping your chart clean and readable.

Features & Inputs

Pivot sensitivity: Set the number of bars for swing calculation.

Box filtering: Specify the minimum ATR multiple for box size.

Trend selection: EMA, SMA, VWAP, or None.

Volume filter & threshold: Activate for greater breakout confidence.

Breakout/Breakdown strength: Set how far price must close beyond the box to signal power.

Maximum boxes: Control the number of active boxes to keep the chart clear.

How to Add and Use

Add to Chart:

Click the “Add to Favorite Scripts” star to mark this indicator.

Open your desired intraday chart (1m–30m works best).

Click “Indicators,” search for “Advanced Intraday Darvas Box,” and add to your chart.

Customize Inputs:

Use the settings gear ⚙️ to adjust pivot sensitivity, trend logic, box filtering, and volume confirmation.

Lower minimum box height or pivot length for more frequent signals. Raise them for sparser, higher conviction setups.

Reading Darvas Boxes:

Box Edges: Horizontal lines mark resistance (top) and support (bottom) of detected zones.

Shaded regions: Highlight the most relevant trading zones and where price could coil before breakout.

Breakout labels (↑/↓): These appear only when price makes a powerful, confirmed move beyond the box edge—aligned with trend.

Alerts: Turn on chart alerts using the “Strong Bullish Breakout” or “Strong Bearish Breakdown” alert conditions for automated signal monitoring.

Best Practices:

Use Darvas boxes to complement price action analysis. Combine with candlestick patterns, volume spikes, and other price structure.

Only trade strong breakout signals confirmed by volume and market direction.

Avoid excessive boxes—adjust "Max Boxes" and filters for your instrument and timeframe.

Important

This indicator is non-repainting and built for display clarity and clean signals.

No brokerage automation, no external linking, and pure price/volume logic—fully compliant with TradingView House Rules.

Always test settings and confirmations before using for live decision-making.

Dashti XAU Liquidity Map ELITE"No Sweep = No Trade

No BOS = No Trade

No Killzone = No Trade

No Volume = No Trade"

14:30 New York OpenRed dotted line at NY open. Shows new traders where NY opens. Helpful for backtesting and when trading that session where it starts very quickly

Custom MTF VWAP 4x with IBI put this indicator together to have my main VWAP levels displayed on the chart easily with shaded areas when price is over extended. The IB I added to have the option to change futures based on an initial balance strategy combined with the daily and NY VWAP.

Volume Peak Box📄 English Description

Overview

The Volume Peak Box indicator highlights periods of unusually high volume by identifying volume spikes using Bollinger Bands on volume and drawing a price-range box around each spike window. This provides traders with a clear visual representation of supply/demand imbalances, absorption zones, and breakout/false-break areas.

All calculations come from one unified concept: detecting statistically significant volume peaks on a locked timeframe and mapping them onto the chart.

Concept & Logic

1. Locked Timeframe Volume Analysis

Instead of using the current chart timeframe, this script allows users to lock volume analysis to any timeframe (e.g., 60m, 4H, 1D).

The script retrieves from the chosen timeframe:

Volume

High price

Low price

This allows volume structure from higher timeframes to be used while trading lower timeframes.

2. Bollinger Bands on Volume

Volume volatility is analyzed using a standard Bollinger Band model:

Basis = SMA(volume, BB length)

Upper Band = Basis + (mult × standard deviation)

When:

Volume > Upper Band

→ This bar is classified as a Volume Peak.

This approach makes the peak detection statistically meaningful, instead of simply comparing raw volume to previous bars.

3. Peak Session Detection (Continuous Peaks Form One Box)

The script tracks continuous volume peaks:

When a peak starts → begin a session

While peaks continue → extend the session

When peaks end → session closes and a box is created

For each peak session, the script records:

Start bar index

End bar index

Highest high within the session

Lowest low within the session

These values determine the box boundaries.

This allows the indicator to group related peaks into a single price zone, instead of drawing a box for every bar.

4. Drawing the Volume Peak Box

When a session ends, the script draws:

A filled box covering the full price range

From startBar → endBar

Using user-defined:

Box fill color

Border color

Each box visually marks a region where strong participation entered the market, often signaling:

Breakout validation

Absorption zones

Supply/demand imbalance

High-activity trading decisions

How to Use

Use the boxes to identify high-volume reaction zones.

When price revisits a box:

Expect strong reactions (bounce, rejection, or absorption).

When price breaks out from a box:

Can signal continuation with momentum.

Lower-timeframe entry signals become more reliable when aligned with high-timeframe volume boxes.

Recommended to lock the TF to:

60m for intraday

4H or 1D for swing trading

Why This Script Is Original

It uses Bollinger Bands on volume, not price — a less common volatility-based method for detecting volume anomalies.

It groups continuous peaks into unified zones instead of treating each spike separately.

The ability to lock the volume analysis to a higher timeframe allows multi-timeframe volume interpretation without cluttering the chart.

Boxes give traders a clean and intuitive view of volume-based “decision zones”.

🇹🇭 Thai Description — คำอธิบายภาษาไทย

ภาพรวม

อินดิเคเตอร์ Volume Peak Box ใช้การตรวจจับ “Volume Peak” โดยใช้ Bollinger Band บน Volume แล้วสร้าง “กล่องช่วงราคา” ครอบช่วงที่มี Volume สูงผิดปกติ ทำให้เห็นบริเวณที่มีแรงซื้อขายเข้ามาอย่างชัดเจน เช่น จุด Breakout, จุด Absorption, หรือเขต Supply/Demand

แนวคิดและหลักการทำงาน

1. วิเคราะห์ Volume จาก Timeframe ที่ล็อกไว้

คุณสามารถเลือก TF ที่ต้องการให้ Volume ถูกนำมาคำนวณ เช่น 60 นาที, 4 ชั่วโมง, 1 วัน

แม้คุณจะเปิดกราฟ TF เล็ก เช่น 5m แต่กล่องยังอิง volume จาก TF ที่เลือกไว้ ทำให้ได้ “โซน Volume ใหญ่” ที่แม่นยำขึ้น

2. Bollinger Band บน Volume

ใช้ SMA + ส่วนเบี่ยงเบนมาตรฐานของ Volume เพื่อหา “จุดที่ Volume สูงกว่าปกติอย่างมีนัยสำคัญ”

เงื่อนไข Peak:

Volume > Upper Bollinger Band

นี่เป็นวิธีที่ดีกว่า “เทียบกับแท่งก่อนหน้า” เพราะคิดจากสถิติของทั้งช่วง

3. รวม Peak ต่อเนื่องเป็นกล่องเดียว

ถ้า Volume Peak เกิดต่อเนื่องหลายแท่ง:

จะถูกจับรวมเป็น Peak session เดียว

ใช้ High สูงสุด และ Low ต่ำสุดของทั้ง session

เมื่อ Peak จบ → วาดกล่องช่วงราคา

เหมาะกับการหาจุดที่ตลาดมีแรงเข้าซื้อ/ขายหนักในช่วงเวลาเดียวกัน

4. วาดกล่อง Volume Peak

กล่องจะครอบ:

ช่วงแท่งเริ่มต้น → แท่งสุดท้ายของ Peak

ความสูงของกล่อง = ช่วงราคาที่มี Volume สูงผิดปกติ

กล่องสามารถใช้เป็น:

โซน Breakout/Breakdown

โซน Supply/Demand

เขตที่ราคามักมี reaction

วิธีใช้งาน

ใช้กล่องเป็น “เขตการตัดสินใจ” (Decision Zone)

ราคาแตะซ้ำมักเกิดการกลับตัวหรือความผันผวนสูง

การทะลุกล่องบ่อยครั้งนำไปสู่ขาเทรนด์ใหญ่

เหมาะกับการใช้ร่วมกับ Price Action และโครงสร้างราคา

จุดเด่น / ความเป็น Original

ใช้ Bollinger Band บน Volume (น้อยอินดี้ทำ)

รวม Peak ต่อเนื่องเป็น session เดียว

วิเคราะห์ Volume ข้าม TF ได้ โดยไม่ต้องเปลี่ยน TF บนกราฟ

ได้ “โซน Volume สำคัญ” แบบชัดเจน อ่านง่าย ไม่รกจอ

20 Day Range High/Low (Turtle Soup)This indicator identifies the Highest High and Lowest Low of the last 20 periods (customizable) and projects horizontal support/resistance lines to the right.

Unlike standard Donchian Channels or other High/Low indicators that clutter the chart with historical "steps" or extend lines infinitely to the left, this script focuses on chart cleanliness.

Key Features:

Pivot-Point Start: The lines do not span the whole chart. They start exactly at the candle where the High or Low occurred.

Right Extension: Lines extend only to the future, providing a clear visual for potential breakouts or support levels.

No Historical Clutter: It does not draw the past movement of the High/Low, keeping your chart clean for price action analysis.

Dynamic: As new Highs or Lows are made, the lines instantly update to the new positions.

How to Use:

Trend Identification: Use the High line as a resistance/breakout level (similar to Turtle Trading strategies).

Stop Loss Placement: The Low line of the last 20 days often acts as a trailing stop location for long-term trends.

Timeframes: While designed for the classic "20-Day" lookback on the Daily chart, this script works on any timeframe (e.g., finding the 20-hour range on a 1H chart).

Settings:

Length: Default is 20 bars. You can change this in the settings to any lookback period you prefer (e.g., 50, 100).

Smoothed VWAP Bands + EMAsSmoothed VWAP bands

With my script, you take the raw standard deviation and apply an EMA (exponential moving

Advantages:

1. Less noise:

* The bands don’t jump around with every tiny price spike.

* Makes it easier to judge real price extremes.

2. Better zone visualization:

* Inner and outer bands are smoother and more visually “stable.”

* Easier to see meaningful trends, support/resistance, and breakout zones.

3. Fewer fakeouts:

* Traders can filter out small false signals because smoothed bands only move when volatility actually changes.

4. Dynamic to volatility:

* EMA smoothing keeps the bands adaptive:

* In quiet periods, bands tighten.

* In volatile periods, bands expand.

* But it avoids extreme jitter caused by every micro-move.

Safe Zone Rules

1. Long entries (green zone):

* Price above VWAP (trend bullish).

* Price inside inner band ±1σ (not touching outer extremes).

* Optional: candle close confirmation (price fully above inner band).

2. Short entries (red zone):

* Price below VWAP (trend bearish).

* Price inside inner band ±1σ.

* Optional: candle close confirmation.

3. Outer bands (±2σ):

* Considered overextended zones → avoid entries to reduce fakeouts.

4. Visual cues:

* Safe zones shaded lightly green/red inside inner band.

* Outer bands remain unshaded (for context).

Here’s a cheat sheet for trading the Smoothed VWAP Bands + EMAs that shows safe entry zones and trend alignment clearly.

Smoothed VWAP Bands + EMAs Cheat Sheet

Price Action Relative to Bands & EMAs

+2σ (Outer Upper Band)

----------------

Extreme volatility zone

Avoid entries here

+1σ (Inner Upper Band)

----------------

Safe zone limit for longs

Consider profit taking here

VWAP Line (Green = Bullish, Red = Bearish)

==================

Core trend indicator

Only trade in VWAP trend direction

-1σ (Inner Lower Band)

----------------

Safe zone limit for shorts

Good for entries in trend direction

-2σ (Outer Lower Band)

----------------

Extreme volatility zone

Avoid entries here

1️⃣ Trend Direction with VWAP & EMAs

* VWAP → shows the overall session trend.

* Price above VWAP → bullish

* Price below VWAP → bearish

* EMA 5 (blue) → short-term momentum

* EMA 20 (orange) → medium-term trend

Rule: Only take trades in the direction of the trend:

* Long trades → price > VWAP and EMA 5 > EMA 20

* Short trades → price < VWAP and EMA 5 < EMA 20

This prevents chasing trades against the trend and reduces fakeouts.

2️⃣ Entry Zones Using Smoothed VWAP Bands

* Inner band (±1σ) → “safe entry zone”

* Outer band (±2σ) → volatility extremes → avoid entries here

Rule: Enter longs inside the inner band above VWAP and shorts inside the inner band below VWAP.

Best used on intraday timeframes.

15, 5, 2, 1 min charts.

Normalised Volume Oscillator [BackQuant]Normalised Volume Oscillator

A refined evolution of the Klinger Volume Oscillator, rebuilt for clarity, precision, and adaptability. This tool normalizes volume-driven momentum into a bounded scale so you can easily identify shifts in accumulation and distribution across any asset or timeframe, while keeping readings comparable between markets.

What this indicator does

The Normalised Volume Oscillator quantifies the balance between buying and selling pressure using the Klinger Volume Oscillator (KVO) as its base, then rescales it dynamically into a normalized range between -0.5 and +0.5. This normalization allows traders to interpret relative strength and exhaustion in volume flow, rather than dealing with raw unbounded values that differ across symbols.

It is a momentum-volume hybrid that reveals the strength of trend participation: when buyers dominate, normalized readings rise toward +0.5; when sellers dominate, they fall toward -0.5. The midline (0) acts as an equilibrium between accumulation and distribution.

Core components

Klinger Volume Oscillator: The foundation of this indicator, combining volume with price trend direction to measure long-term money flow relative to short-term movement.

Normalization process: The raw KVO is scaled over a user-defined Normalisation Period , computing `(KVO - lowest) / (highest - lowest) - 0.5`. This centers all readings around zero, allowing overbought/oversold detection independent of asset volatility or volume magnitude.

Signal moving average: The normalized KVO is smoothed with a user-selectable moving average type—SMA, EMA, DEMA, TEMA, HMA, ALMA, and others. This becomes the signal line for confirmation of trend direction or mean-reversion setups.

How it works conceptually

1. The KVO detects when volume supports price movement (bullish) or diverges from it (bearish).

2. The script normalizes the raw KVO so that relative magnitude is consistent—what is “strong buying pressure” looks the same on BTCUSD as it does on AAPL.

3. Overbought and oversold regions are derived statistically, rather than from arbitrary values, based on percentile zones around ±0.4 and ±0.5.

4. The oscillator is optionally combined with a moving average to help identify crossovers, momentum shifts, and divergence confirmation.

How to interpret it

Above 0: Indicates dominant buying pressure and likely continuation of upward momentum.

Below 0: Suggests dominant selling pressure and potential continuation of downward movement.

Crosses of 0: Often mark transitions between accumulation and distribution phases.

+0.4 to +0.5 zone: Overbought region where buying intensity is stretched; watch for deceleration or divergence.

[-0.4 to -0.5 zone: Oversold region indicating panic or exhaustion in selling.

Signal-line crossover: A traditional momentum confirmation method; when the normalized KVO crosses above its moving average, buyers regain control, and vice versa.

Why normalization matters

Typical volume oscillators are asset-specific—what is considered “high” volume for one symbol is not the same for another. By dynamically normalizing KVO values within a rolling lookback, this version transforms raw amplitude into a standardized scale. This means you can:

Compare multiple assets objectively.

Set consistent alert thresholds for overbought/oversold regions.

Avoid misleading interpretations from absolute oscillator values.

Customization and UI

Moving Average Type & Period: Select your preferred smoothing method (SMA, EMA, TEMA, etc.) and adjust its period to tune sensitivity.

Normalisation Period: Defines how many bars the KVO range is measured over; shorter periods adapt faster, longer ones smooth more.

Visual Toggles:

* Show Oscillator : enables or hides the core histogram.

* Show Moving Average : adds a smoothed overlay for signal confirmation.

* Paint Candles : optional color overlay for chart candles based on oscillator direction.

* Show Static Levels : displays ±0.4 and ±0.5 zones for overbought/oversold boundaries.

How to use it

Trend confirmation: Use midline (0) crossovers as confirmation of emerging trend shifts—cross above 0 suggests a new bullish phase, cross below 0 a bearish one.

Reversal spotting: Look for normalized readings reaching ±0.5 and flattening, or diverging against price extremes.

Divergence analysis: When price makes a new high but the normalized oscillator fails to, it signals waning buying conviction (and vice versa for lows).

Multi-timeframe integration: Works best alongside higher timeframe trend filters or moving averages; normalization makes this consistent.

Alerts

Prebuilt alert conditions allow quick automation:

Midline crossovers (0): transition between accumulation and distribution.

Overbought (+0.4) and Oversold (-0.4) triggers for potential exhaustion.

Signal moving-average crosses for confirmation entries.

Tips for use

Combine with price structure—don’t fade every overbought/oversold reading; confirm with break of structure or candle patterns.

Use longer normalization periods for position trading, shorter for intraday analysis.

In choppy markets, treat 0-line oscillations as noise filters, not trade triggers.

Summary

The Normalised Volume Oscillator modernizes the classic Klinger Volume Oscillator by normalizing its readings into a standardized range. This makes it more adaptive across assets and timeframes, improves interpretability, and provides intuitive, data-driven overbought/oversold levels. Whether used standalone or as a confirmation layer, it offers a clearer view of volume dynamics—revealing when markets are truly being accumulated, distributed, or stretched beyond their sustainable extremes.

My script//@version=5

indicator("200-Day Volume MACD Oscillator", overlay=false)

length = 200

vol_avg = ta.sma(volume, length)

oscillator = volume - vol_avg

plot(oscillator, style=plot.style_histogram, color=oscillator >= 0 ? color.green : color.red, title="Volume MACD Oscillator")

Smart RSI Money Flow - Core Bands V1.01SMART RSI – Money Flow Bands (Technical Overview)

1. Background: RSI and Its Behavior on Lower Timeframes

The Relative Strength Index (RSI) originally is a momentum oscillator calculated from average gains and losses over a selected period. In its standard form, RSI is derived solely from price changes; it does not incorporate volume data or order-flow information in its formula.

Because RSI is price-based, its interpretation depends strongly on the timeframe:

• On higher timeframes, each bar aggregates more trading activity, and RSI tends to behave more smoothly.

• On lower timeframes (1-hour down to intraday scalping intervals), price fluctuations are quicker, and RSI becomes more sensitive to short-term noise.

This does not imply that RSI becomes invalid, but that its signals on fast charts can be more reactive and may benefit from additional context such as volume behavior or structural information.

2. Purpose of This Indicator

This indicator extends the classical RSI by adding information that RSI does not include:

• Mapping RSI values into price-based bands instead of the 0–100 oscillator space.

• Retrieving lower timeframe volume data and separating it into buy and sell components.

• Comparing the slope (angle) of price movement with the slope of buy and sell volume.

The goal is to provide a structural interpretation of where price sits relative to RSI conditions and how volume is behaving on a lower timeframe.

3. Technical Differences Compared to Classical RSI

A) Classical RSI

• Input: price only (usually close).

• Output: normalized oscillator between 0 and 100.

• Does not incorporate intra-bar volume distribution.

• Does not separate buy/sell volume.

B) SMART RSI – Money Flow Bands

1) RSI-to-Price Mapping

Converts RSI values into upper/lower price bands using recent price extremes.

2) Lower Timeframe Volume Decomposition

Retrieves LTF data and splits each bar’s volume into buy (close>open) and sell (close

Smoothed VWAP Bands🎯 Best Smoothing Setting for Scalping (What You Should Use)

Style σ Smoothing Result

Fast scalping (1min) EMA 14 Very responsive, still filters noise

Balanced intraday (1–5min) EMA 20 Best overall reliability

Slow confirmation (5–15min) EMA 30 Eliminates nearly all fakeouts

✅ What We Are Actually Smoothing

You are NOT smoothing VWAP itself.

You are smoothing the standard deviation (σ) that creates the VWAP bands:

✔ What this does:

* Computes the raw standard deviation (σ) of price relative to VWAP

* Smooths that σ using EMA smoothing

* Builds ±1 and ±2 bands using the smoothed σ

* You get clean, stable bands that filter fakeouts

✔ Result:

* Bands do NOT twitch in chop

* Fakeouts are filtered

* Real breakouts show obvious expansion

RED-E Market Structure (Pro V2)RED-E Market Structure - Comprehensive Technical Analysis System

⚠️ EDUCATIONAL TOOL - NO GUARANTEES

This indicator is designed for educational purposes to help traders learn technical analysis concepts. It does not predict future price movements or guarantee profitable trades. Trading involves substantial risk of loss.

═══════════════════════════════════════════════════════════════

📊 WHAT THIS INDICATOR DOES

This indicator combines multiple standard technical analysis methods into a unified system for analyzing market structure, momentum, volume dynamics, and key price levels. Rather than adding 10 separate indicators to your chart, this consolidates related information into one cohesive interface where each component informs the others.

═══════════════════════════════════════════════════════════════

🔧 TECHNICAL METHODOLOGY - HOW IT WORKS

1️⃣ MOMENTUM CANDLE COLORING (6 Levels)

Calculation Method:

- Compares close vs EMA(9) and EMA(21)

- Applies RSI(14) thresholds for strength

- Color codes: Royal Blue (strongest bull) → Cyan → Green → Yellow → Orange → Red (strongest bear) → White (neutral)

Formula Logic:

IF close > EMA(9) AND close > EMA(21) AND close > open:

RSI > 70 = Level 3 Bull (Royal Blue)

RSI 60-70 = Level 2 Bull (Cyan)

RSI < 60 = Level 1 Bull (Green)

Purpose: Visualizes momentum strength by combining trend (EMAs), candle direction, and overbought/oversold conditions (RSI).

2️⃣ ENTRY SIGNAL LABELS

Calculation Method:

- Uses EMA alignment: EMA(9) > EMA(21) > EMA(50) for bullish

- Filters RSI to avoid extremes

- Requires confirming candle

BUY Signal Logic:

IF close > EMA(9) AND RSI between 40-70 AND EMA(9) > EMA(21) > EMA(50) AND close > open

THEN: Display "BUY" label

Purpose: Identifies potential entries when multiple trend and momentum conditions align. This is standard multi-confirmation technical analysis.

3️⃣ VOLUME DELTA PERCENTAGE

Calculation Method:

FOR each bar in lookback period (default 20):

IF close > open: add volume to bullish_volume

IF close < open: add volume to bearish_volume

bullish_percent = (bullish_volume / total_volume) × 100

Purpose: Quantifies buying vs selling pressure as percentages. Shows if volume supports the current trend.

Display: "🟢65.3% | 🔴34.7%" in dashboard

4️⃣ PRE-MARKET HIGH/LOW TRACKING

Calculation Method:

1. Detect pre-market session (4:00-9:30 AM ET)

2. Track highest high during pre-market

3. Track lowest low during pre-market

4. Draw horizontal lines when market opens

Purpose: Pre-market levels often act as support/resistance during regular hours. This automates their tracking and visualization.

5️⃣ OPENING RANGE BREAKOUT (ORB)

Calculation Method:

1. User sets start time (default 9:30 AM) and duration (default 15 min)

2. Track highest high and lowest low during this period

3. Draw box and extend lines

Purpose: The opening range breakout is a well-documented day trading strategy. First X minutes establish a range, and breakouts often signal directional moves.

6️⃣ SUPPORT/RESISTANCE TRENDLINES

Calculation Method:

1. Identify pivot highs: ta.pivothigh(high, 5, 5)

2. Identify pivot lows: ta.pivotlow(low, 5, 5)

3. Connect last two pivot highs = Resistance (red)

4. Connect last two pivot lows = Support (blue)

Purpose: Automatically connects significant pivot points. Based on standard pivot analysis where price respects these levels.

7️⃣ GAMMA ZONE DETECTION

Calculation Method:

1. Calculate 30-min range: (high - low)

2. Calculate 10-period SMA of range

3. Calculate ratio: current_range / average_range

IF ratio < (1.0 / sensitivity): HIGH GAMMA = Low volatility

IF ratio > (1.0 × sensitivity): LOW GAMMA = High volatility

Purpose: Approximates options gamma effects. High gamma = dealers hedge more = suppressed volatility. Low gamma = less hedging = potential explosive moves.

8️⃣ TAKE PROFIT LEVELS (5 Levels + ATR Stop Loss)

Calculation Method:

LONG: TP = entry_price × (1 + percentage/100)

SHORT: TP = entry_price × (1 - percentage/100)

Stop Loss (ATR): entry ± (ATR(14) × multiplier)

Purpose: Automatically calculates percentage-based targets and volatility-adjusted stops. ATR adapts stop to current market conditions.

9️⃣ THE STRAT PATTERN RECOGNITION

Calculation Method:

Compare current bar to previous:

- Strat 3 (outside bar): high > high AND low < low

- Strat 1 (inside bar): high ≤ high AND low ≥ low

- Strat 2 (directional): All others

Purpose: The Strat is a price action system categorizing bars by relationship to previous bars. This automates classification.

🔟 FIBONACCI RETRACEMENTS

Calculation Method:

1. Find highest high in lookback (default 30 bars)

2. Find lowest low in lookback

3. Calculate: 0.0, 0.382, 0.5, 0.618, 1.0 levels

Purpose: Standard Fibonacci tool. These ratios are commonly used support/resistance in technical analysis.

1️⃣1️⃣ MULTI-TIMEFRAME ANALYSIS

Calculation Method:

FOR each timeframe (default 15m, 1H, 4H):

Check if close > EMA(9) on that timeframe

IF true: "BULLISH", else: "BEARISH"

Purpose: Shows trend alignment across timeframes using Pine's request.security(). Common confirmation technique.

═══════════════════════════════════════════════════════════════

💡 WHY THESE COMPONENTS WORK TOGETHER

This indicator's originality lies in its unified system approach:

1. TREND IDENTIFICATION (EMAs, MTF) - Shows direction

2. MOMENTUM MEASUREMENT (RSI, candles) - Shows strength

3. VOLUME CONFIRMATION (Volume Delta) - Shows conviction

4. KEY LEVELS (PM, ORB, Fib, S/R) - Shows decision points

5. RISK MANAGEMENT (TP levels, ATR stops) - Shows exits

VALUE OF INTEGRATION:

Rather than 10 separate indicators creating chart clutter, this consolidates related concepts where each component provides different information that, when viewed together, gives a more complete market picture.

Example Integration:

- Entry signal appears (EMA + RSI aligned)

- Volume Delta confirms (more buying than selling)

- MTF shows higher timeframes agree

- TP levels auto-calculate with good risk:reward

- Support trendline nearby provides stop reference

═══════════════════════════════════════════════════════════════

⚙️ CUSTOMIZATION OPTIONS

All features independently toggleable:

- EMAs: Adjust lengths (9, 21, 50, 200), colors, widths

- RSI: Change overbought/oversold levels (70/30)

- Volume Delta: Adjust lookback period (20)

- ORB: Set custom start time, duration, timezone

- Gamma: Adjust sensitivity (1-10)

- TP Levels: Customize all 5 percentages

- Dashboard: Reposition, resize, recolor

═══════════════════════════════════════════════════════════════

📖 HOW TO USE

Step 1 - Assess Context:

- Check MTF Dashboard for alignment

- Check EMA indicator for trend

- Check Gamma Zone for volatility expectation

Step 2 - Identify Setups:

- Wait for BUY/SELL signal

- Check Volume Delta matches direction

- Verify RSI not extreme (30-70)

- Look for support/resistance confluence

Step 3 - Evaluate Risk:Reward:

- Review TP3 R:R ratio (target 2:1+)

- Check stop loss placement

- Ensure risk acceptable

Step 4 - Monitor:

- Track P&L % in real-time

- Use TP levels as potential exits

- Adjust stops based on S/R

═══════════════════════════════════════════════════════════════

⚠️ LIMITATIONS & REALISTIC EXPECTATIONS

This indicator does NOT:

- Predict future price movements

- Guarantee profitable trades

- Work in all market conditions

- Replace proper education and practice

This indicator CAN:

- Display standard technical indicators in organized way

- Automate common calculations

- Visualize multiple analysis methods simultaneously

- Help learn how different indicators relate

Key Understanding:

All technical indicators use historical data. They help identify patterns and conditions but cannot predict the future. Successful trading requires risk management, psychology, and experience—not just indicators.

═══════════════════════════════════════════════════════════════

📚 EDUCATIONAL CONCEPTS TAUGHT

- How EMAs show trend direction and alignment

- How RSI identifies momentum extremes

- How volume confirms or diverges from price

- How support/resistance levels form

- How multiple timeframes provide context

- How ATR adapts stops to volatility

- How risk:reward ratios work

═══════════════════════════════════════════════════════════════

📊 BEST SUITED FOR

- Scalping: 1m-5m charts with quick entries/exits

- Day Trading: 15m-1H focusing on ORB and PM levels

- Swing Trading: 4H-D following major trends

═══════════════════════════════════════════════════════════════

⚠️ RISK DISCLAIMER

Trading involves substantial risk of loss. This educational tool:

- Does NOT guarantee profits

- Cannot predict future performance

- Requires proper risk management

- Should be practiced on demo accounts first

Always use stop losses, risk only 1-2% per trade, and consult licensed financial professionals before trading with real capital.

═══════════════════════════════════════════════════════════════

Educational tool for learning technical analysis. Not financial advice. Past results do not indicate future performance.

NEW PRICE ACTION ALGO (v2)Updated price action indicator for day trading QQQ,SPY & IWM on the 5-6min chart

One Minute AI scalper keep extended trading hours on# One Minute AI Scalper - Trading Indicator

## Overview

The One Minute AI Scalper is a precision-engineered trading indicator designed specifically for short-term scalping strategies on 1-minute timeframes. This indicator combines multiple technical analysis methods to identify high-probability entry points for both long and short positions, making it ideal for active traders seeking quick, momentum-based opportunities.

## Key Features

### Visual Signals

- **Long Entry Arrows**: Clear green triangle markers appear below price bars when bullish conditions align

- **Short Entry Arrows**: Clear red triangle markers appear above price bars when bearish conditions align

- Clean, uncluttered chart interface focusing on actionable signals

### Advanced Signal Generation

The indicator utilizes a sophisticated multi-factor approach to generate trading signals:

1. **Trend Analysis**: Employs moving average crossover methodology to identify the prevailing market direction

2. **Momentum Confirmation**: Analyzes candlestick patterns and price behavior to confirm momentum strength

3. **Volume Validation**: Incorporates volume analysis to distinguish between high-conviction and standard signals

4. **Reversal Detection**: Identifies potential trend reversals by examining recent price action patterns

5. **Precision Entry Filtering**: Uses specific candlestick characteristics to minimize false signals

### Alert System

Comprehensive alert functionality for all signal types:

- Long Entry alerts

- Short Entry alerts

## How It Works

### Long Position Signals

The indicator generates long entry signals when multiple bullish conditions simultaneously align, including:

- Confirmation of upward momentum through price action

- Specific candlestick structure indicating strong buying pressure

- Price position relative to key moving averages

- Recent price behavior suggesting reversal potential

- Volume characteristics supporting the move

### Short Position Signals

Short entry signals are generated when multiple bearish conditions converge, including:

- Confirmation of downward momentum through price action

- Specific candlestick structure indicating strong selling pressure

- Price position relative to key moving averages

- Recent price behavior suggesting reversal potential

- Volume characteristics supporting the move

### Position Management

The indicator includes intelligent position state tracking to:

- Prevent duplicate signals while in an active position

- Generate exit signals based on opposing price action

- Maintain clear status of whether you're in a long or short position

## Best Practices

### Recommended Usage

- **Timeframe**: Optimized for 1-minute charts

- **Extended Hours**: Keep extended trading hours enabled for full market coverage

- **Markets**: Works on stocks, forex, crypto, and futures

- **Strategy**: Best suited for scalping and day trading strategies

### Risk Management

- Always use proper stop-loss orders

- Consider position sizing based on account risk tolerance

- Pay attention to volume-indicated signals for higher conviction trades

- Avoid trading during low-liquidity periods

- Combine with your own risk management rules

### Trading Tips

- Higher volume signals generally indicate stronger conviction

- Wait for clear arrow signals rather than trying to anticipate them

- Monitor overall market conditions and major support/resistance levels

- Be aware of news events that may cause unusual volatility

- Practice in a paper trading account before using real capital

## Important Notes

### What This Indicator Does

✅ Provides clear visual entry signals for long and short positions

✅ Incorporates multiple technical factors for signal generation

✅ Includes volume analysis for conviction assessment

✅ Offers comprehensive alert options for all signal types

✅ Maintains position state awareness

### What This Indicator Doesn't Do

❌ Does not guarantee profitable trades

❌ Does not provide specific price targets or stop-loss levels

❌ Does not replace the need for proper risk management

❌ Does not account for fundamental analysis or news events

❌ Does not adapt settings automatically to market conditions

## Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice, and past performance does not guarantee future results. Trading involves substantial risk of loss, and you should only trade with capital you can afford to lose. Always conduct your own research and consider consulting with a qualified financial advisor before making trading decisions.

## Configuration

This indicator uses fixed, optimized parameters that have been carefully calibrated for 1-minute scalping. No user configuration is required - simply add it to your chart and monitor for signals.

## Support

For questions, suggestions, or feedback about this indicator, please use the comments section or contact the author directly through TradingView.

---

**Version**: 6.0

**Category**: Momentum/Scalping

**Overlay**: Yes

**Timeframe**: 1 minute (optimized)

Fair Value Gaps - Cucaracha📘 Fair Value Gaps (FVG) – Clean, Automatic Detection & Real-Time Tracking

The Fair Value Gaps (FVG) indicator automatically detects and visualizes Bullish and Bearish Fair Value Gaps directly on your chart. Built with precision, it highlights imbalance zones, continuously extends them in real time, and removes them the moment they’re mitigated — giving you a clean and accurate market structure view.

✅ Key Features

Automatic FVG Detection

Identifies bullish and bearish FVGs using a strict 3-candle imbalance model.

Dynamic Boxes

Each detected FVG is drawn as a shaded box and extends forward until price fills or mitigates the zone.

Auto-Cleanup (Mitigation Logic)

When price returns to the gap and fills it, the zone is instantly removed, keeping your chart clean and focused.

Custom Colors

Choose your own colors for bullish and bearish FVG boxes.

🎯 Why Traders Use This

Fair Value Gaps are widely used in:

Smart Money Concepts (SMC)

ICT-style trading

Market imbalance analysis

They highlight areas where price moved aggressively and may later return to rebalance.

This indicator helps you:

Spot institutional imbalances instantly

Track unmitigated FVGs without manually drawing boxes

Stay focused on key reaction zones

Improve entries based on premium/discount and liquidity concepts

🧠 How It Works

Bullish FVG:

Occurs when price leaves a gap where low > high , creating an upward imbalance zone.

Bearish FVG:

Occurs when high < low , indicating a downward imbalance zone.

Detected gaps are plotted as forward-extending boxes until price mitigates them.

Once mitigated (price fills the gap), the zone is automatically removed.

🟦🟥 Visuals

Blue (or your chosen color): Bullish FVG

Red (or your chosen color): Bearish FVG

150% Volume Surge1M charts show 150% volume surge to confirm scalping oppos in the direction of the general trend.