Dskyz (DAFE) Turning Point Indicator - Dskyz (DAFE) Turning Point Indicator — Smart Reversal Signals

Inspired by the intelligent logic of a pervious indicator I saw. This script represents a next-generation reversal detection system—completely re-engineered with cutting-edge filters, adaptive logic, and intelligent dashboards.

The Dskyz (DAFE) Turning Point Indicator

🧠 What Is It?

is designed to identify key market reversal zones with extraordinary accuracy by combining trend direction, volatility confirmation, price action patterns, and smart filtering layers—all visualized in a highly interactive and informative chart overlay.

This isn’t just a signal generator—it’s a decision-making assistant.

⚙️ Inputs & How to Use Them

All input fields are grouped for ease-of-use and explanation:

🔸 Reversal Logic Settings

Source: The price source used for signal generation (default: hlcc4). Can be changed to any standard price formula (open, close, hl2, etc.).

ATR Period: Used for determining volatility and dynamic trailing stop logic.

Supertrend Factor / Period: Calculates directional movement to detect trending vs choppy zones.

Reversal Sensitivity Thresholds: Internal logic filters minor pullbacks from true reversals.

🔸 Filters

Trend Filter: Enables trend-only signals (optional).

Volume Spike Filter: Confirms reversals with significant volume activity.

Volatility Zone Coloring: Visually highlights high-volatility areas to avoid late entries or fakeouts.

Custom High/Low Detection: Smart local top/bottom scanning to reinforce accuracy.

🔸 Visual & Dashboard Options

Signal Labels: Toggle signal labels on the chart.

Color Theme: Choose your visual theme for easier visibility.

Dashboard Toggle: Activate a compact dashboard summarizing strategy health (win rate, drawdown, trend state, volatility).

🧩 Functions Used

ta.supertrend(): Determines trend direction for signal confirmation and filtering.

ta.atr(): Calculates real-time volatility to determine trailing stop exits and visual zones.

ta.rsi() (internally optimized): Helps filter overbought/oversold conditions.

Local High/Low Scanner: Tracks recent pivots using a custom dynamic lookback.

Signal Engine: Consolidates multiple confirmation layers before plotting.

🚀 What Makes It Unique?

Unlike traditional reversal indicators, this one combines:

Multi-factor signal validation: No single indicator makes the call—volume, trend, price action, and volatility all contribute.

Adaptive filtering: The indicator evolves with the market—less noise, smarter signals.

Visual volatility heatmap zones: Avoid entering during uncertainty or manipulation spikes.

Interactive trend dashboard: Immediate insight into the strength and condition of the current market phase.

Highly customizable: Turn features on/off to match your trading style—scalping, swing, or trend-following.

Precision timing: Uses optimized versions of RSI and ATR that adjust automatically with price context.

🧬 Recommended for:

Commodity: Futures, Forex, Crypto

Timeframes: 1m to 1h for active traders. 4h+ for swing trades.

Pair With: Support/resistance zones, Fibonacci levels, and smart money concepts for additional confluence.

🎯 Why It Works

- Traditional reversal signals suffer from lag and noise. This system filters both by:

- Using multi-source confirmation, not just price movement.

-Tracking volatility directly, not assuming static markets.

-Detecting exhaustion, not just divergence.

-Keeping your screen clean, with only the most relevant data shown.

🧾 Credit & Acknowledgement

🧠 Original Concept Inspiration: This project was deeply inspired by the work of Enes_Yetkin_ and their approach to reversal detection. This version expands on the concept with additional technical layers, updated visuals, and real-time adaptability.

📌 Final Thoughts

This is more than a reversal tool. It's a market condition interpreter, entry/exit planner, and risk assistant all in one. Every aspect is engineered to give you an edge—especially when timing means everything.

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

-Dskyz

Average True Range (ATR)

Volume Flow RatioVolume Flow Ratio (VFR) Indicator

Overview

The Volume Flow Ratio (VFR) is a sophisticated volume analysis tool that measures current trading volume relative to the maximum volume of the previous period. Unlike traditional volume indicators that show raw volume or simple moving averages, VFR provides context by comparing current activity to recent maximum activity levels.

Core Features

1. Split Period Analysis

- Multiple Timeframe Options:

- Daily: Compares to previous day's maximum

- Weekly: Week-to-week comparison

- NYSE Weekly: Specialized for stock market trading (Monday-Friday only)

- Monthly: Month-to-month analysis

- Quarterly: Quarter-to-quarter perspective

- Yearly: Year-over-year volume comparison

2. Ratio-Based Measurement

- Displays volume as a ratio (0 to 1+) rather than raw numbers

- 1.0 represents volume equal to previous period's maximum

- Example: If previous max was 50,000 contracts:

- Current volume of 25,000 shows as 0.5

- Current volume of 75,000 shows as 1.5

3. Triple Coloring Modes

- Moving Average Based:

- Compares current ratio to its moving average

- Customizable MA period

- Green: Above MA (higher than average activity)

- Red: Below MA (lower than average activity)

- Previous Candle Comparison:

- Simple increase/decrease from previous bar

- Green: Higher than previous bar

- Red: Lower than previous bar

- Candle Color Based:

- Syncs with price action

- Green: Bullish candles (close > open)

- Red: Bearish candles (close < open)

Primary Use Cases

1. Volume Profile Analysis

- Perfect for traders who need to understand when markets are most active

- Helps identify unusual volume spikes relative to recent history

- Useful for timing entries and exits based on market participation

2. Market Activity Traders

Ideal for traders who:

- Need to identify high-liquidity periods

- Want to avoid low-volume periods

- Look for volume breakouts or divergences

- Trade based on institutional participation levels

3. Mean Reversion Traders

Helps identify:

- Overextended volume conditions (potential reversals)

- Volume exhaustion points

- Return to normal volume levels after spikes

4. Momentum Traders

Useful for:

- Confirming trend strength through volume

- Identifying potential trend exhaustion

- Validating breakouts with volume confirmation

Advantages Over Traditional Volume Indicators

1. Contextual Analysis

- Shows relative strength rather than raw numbers

- Easier to compare across different time periods

- Automatically adjusts to changing market conditions

2. Period-Specific Insights

- Respects natural market cycles (daily, weekly, monthly)

- Special handling for NYSE trading days

- Eliminates weekend noise in stock market analysis

3. Flexible Visualization

- Three distinct coloring methods for different trading styles

- Clear reference line at 1.0 for quick analysis

- Histogram style for easy pattern recognition

Best Practices

For Day Traders

- Use Daily split for intraday volume patterns

- MA coloring mode with shorter periods (5-10)

- Focus on ratios during market hours

For Swing Traders

- Weekly or NYSE Weekly splits

- Longer MA periods (15-20)

- Look for sustained volume patterns

For Position Traders

- Monthly or Quarterly splits

- Candle color mode for trend confirmation

- Focus on major volume shifts

Limitations

- Requires one full period to establish baseline

- May be less effective in extremely low volume conditions

- NYSE Weekly mode specific to stock market hours

This indicator is particularly valuable for traders who understand that volume is a crucial component of price action but need a more sophisticated way to analyze it than simple volume bars. It's especially useful for those who trade based on market participation levels and need to quickly identify whether current volume is significant relative to recent history.

Rogue ORB PRORogue ORB Pro is a precision-engineered Opening Range Breakout (ORB) indicator built for active intraday traders who need real signals, not noise.

This tool identifies high-probability breakout entries from the opening range, enhanced with optional ATR-based stop loss levels, deviation targets, cooldown filters, and a relative volume gate to filter weak setups.

🔍 Key Features:

Opening Range High/Low: Drawn from a user-defined time window and locked for the day

Deviations: Automatically plots target zones above and below the OR range (e.g. 1, 2 deviations)

Pre-Market Levels: Automatically draws pre market high and low lines at the end of pre market session

Buy/Sell Signals: Triggered on breakout of the OR High/Low with configurable breakout logic (touch or close)

ATR Stop Loss Line: Dynamically drawn at a fixed ATR distance from breakout candle, with optional SL label

Cooldown Period: Prevents back-to-back signals by enforcing a user-defined bar delay between entries, can help with overtrading

Volume Filter: Optional relative volume filter that requires breakout candles to exceed a custom volume threshold

VWAP Overlay: Visual VWAP for directional bias and confluence

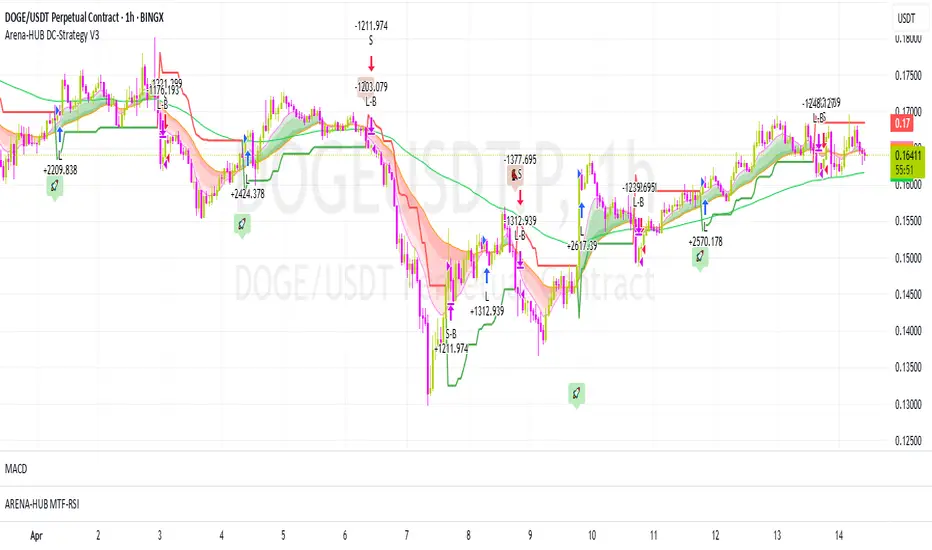

Arena-Hub-DC-Strategy V3.1This script must be individually configured for each cryptocurrency. After monitoring several coins, I’ve realized that each one requires its own unique setup. There's no “one-size-fits-all” — and different timeframes require different configurations as well.

⚠️ Risk management is essential.

If you're not familiar with proper risk management, please do not use this script. Make sure to configure your commission and slippage settings appropriately, as these are critical for realistic backtesting results. The Stop Loss and Take Profit levels are not automated — they must be adjusted by the user.

This script is not a financial advisor. It won't make risk or profit-related decisions for you. It's a tool designed to help identify potential entries, trends, and exit opportunities — but all final decisions must be made by the trader.

The default settings are only examples. You’ll need to customize them for each crypto asset and timeframe to make the strategy truly work for your style and market conditions.

The script evaluates:

The positioning of two RSIs relative to each other

Their alignment with a customizable RSI-EMA

The values of EMAs and the ATR (volatility)

A custom weighting system using ADR and VOLUME, which strongly affects trade signals. The weights can be adjusted in 0.1 increments, and even small changes can have a big impact — so fine-tuning is important!

These indicators were chosen because they complement each other:

RSI and its EMA help identify momentum shifts

ATR gauges volatility to confirm market conditions

ADR and VOLUME help filter weak signals and fine-tune entries and exits

🔍 Important: Only use this script if you understand how RSI, EMA, ATR, ADR, and VOLUME indicators work, and are comfortable making your own trading decisions.

The backtest results are based on historical data — the script cannot see the future, not even guess it. Please use it responsibly.

This script is an advanced trend-following strategy that dynamically combines RSI, SMA, EMA, ATR, ADX, and volume indicators using a unique weighting and filtering mechanism. Instead of simply combining traditional indicators, it applies them in a unique way:

✅ Dual RSI Comparison: The strategy utilizes two RSI indicators, analyzing their relative movement to filter out false signals and provide more precise entry points.

✅ Custom Entry and Exit Rules: EMA crossovers alone do not generate signals; instead, they go through a dynamic RSI filter that takes market volatility into account using ATR and ADX.

✅ Intelligent Trend Identification: Instead of standard moving averages, a uniquely weighted SMA/EMA system is used to assess trend strength and stability.

✅ ATR, ADX & Volume-Based Weighting: The EMA length is dynamically adjusted based on ATR, ADX, and volume, allowing moving averages to react faster in strong trends while smoothing out in choppy markets.

Advanced Dynamic EMA Zone

This is not your typical EMA indicator. It's an enhanced, dynamically adaptive trend zone that:

✅ Applies gradient shading – The zone between EMAs is divided into four layers, highlighting trend strength through smooth color transitions.

✅ Visualizes trend intensity – The strongest trends appear in the darkest shades, while weaker moves fade into lighter tones.

✅ Brings moving averages to life – Instead of static lines, it creates a visually intuitive trend channel.

✅ Differentiates bullish & bearish phases – The cloud fades from dark green to light green during an uptrend and from dark red to light red in a downtrend.

✅ Filters out market noise – Weakening trends appear more transparent, instantly revealing when momentum starts to fade.

✅ Enhances decision-making – Crossovers alone are not trading signals, but the visual representation helps identify market conditions at a glance.

➡️ What makes it unique?

Traditional moving average indicators rely on basic lines, but this is a full-fledged trend visualization system, helping traders filter noise and better understand price momentum.

🔄 Improved Custom EMA Smoothing Control

We’ve enhanced the weighting factor input for better user control! Previously, the EMA smoothing factor (ema1_smooth_factor) had a fixed step size that limited precision. Now, users can fine-tune it in 0.1 increments for greater flexibility.

✅ What’s new?

More precise control over EMA smoothing with adjustable step size (step=0.1).

Better adaptability to different market conditions.

Smoother trend visualization for traders who prefer fine-tuned settings.

This update ensures our custom EMA visualization remains superior to standard indicators. 🎯🔥

ATR Stop-Loss & TargetsATR and Supertrend-based SL/TP & Trailing System

This indicator combines Average True Range (ATR) and Supertrend logic to help traders define precise stop-loss, first target, and trailing stop-loss (TSL) levels.

⚙️ Key Features:

📏 ATR-based Stop-Loss & Target Lines:

Uses ATR (default period: 5) based on the previous day's candle for more stable risk management.

Traders can choose the price source: Close, Open, or enter a manual price.

SL and first target are calculated using multipliers:

Multiplier 1 = Stop Loss

Multiplier 2 = First Target

📉 Supertrend for Trailing Stop:

Built-in Supertrend logic for trailing stop-loss management.

Uses ATR(10) with a multiplier of 2.1, based on HL2.

Supertrend can be toggled ON/OFF from the settings.

ATR % Oscillator - DolphinTradeBot1️⃣ Overview

🔸 This is a simplified version of ATR and TR that shows volatility as percentage changes , making it easier to compare two symbols.

🔸 The indicator compares the volatility of two different assets by calculating the percentage-based price ranges and their moving averages .

📌 This is especially useful for pair traders, as it helps identify which symbol is more volatile, allowing for strategic decisions based on relative movement rather than overall market direction.

2️⃣ How Is It Work?

🔸 For each symbol, it calculates the absolute percentage difference between either:

• Close and Open (net price change), or

• High and Low (daily price range).

🔸 The results are visualized as column bars — the taller the bar, the higher the volatility.

🔸 It also plots a moving average line (SMA) based on the selected range length.

📌 These calculations are independent of the chart you're on — they work purely based on the two selected symbols.

If no symbols are selected, it defaults to using the current chart's symbol.

3️⃣ How to Use It?

With this indicator, you can:

🔸 Compare the volatility between two assets.

🔸 Detect sudden volatility spikes that may signal upcoming momentum.

🔸 Support spread, arbitrage, or correlation-based strategies .

🔸 See which symbol is gaining market attention (a larger difference = more activity).

Example: Compare BTC vs ETH to see which one is dominating in terms of price action or volatility.

4️⃣⚙️ Settings

🔸 Symbol Settings

• Symbol-1 / Symbol-2: Choose the two assets to compare.

• Checkboxes: Enable/disable visibility for each symbol's data.

🔸 Calculation Settings

• Range Average: The number of bars used for the moving average.

• Calculation Source:

- Close-Open: Measures net price movement.

- High-Low: Measures total price range.

VoluTility🌊 VoluTility forecasts trend exhaustion, breakout pressure, and structural inflection by measuring volatility within the effort stream. Built on the concept of ATR applied to volume, it doesn’t read raw volume — it reveals whether that volume is stable, chaotic, or compressing ahead of a move. The goal is to detect structural setups before they resolve. The lower the timeframe, the greater the alpha.

🧠 Core Logic

A zero-centered histogram shows the deviation of smoothed volume from its own volatility baseline. Positive bars indicate expansion; negative bars signal compression. Color reflects rate-of-change in volume volatility. Opacity tracks effort/result strength — showing when moves are real or hollow.

The overlaid ribbon (EMA vs HMA) highlights rhythm shifts. Orange fill signals real expansion; yellow shows decay or absorption. Together, they expose pre-breakout compression and exhaustion tails before price reacts.

🏗️ Structural Read

On the 1H BTC chart shown, price coils into a shallow pullback, compressing within a narrow range marked by shrinking candle bodies and muted wick aggression. A sudden expansion candle breaks the coil cleanly, with no immediate rejection or wick reversion. Price holds above the breakout pivot, establishing a baseline for structural acceptance and shifting bias toward continuation.

🔰 Zone Descriptions

🔴 Volatile blowout

🟠 Clean expansion

🟡 Passive or absorbed effort

🟢 Steady-state rhythm

🔵 Compression coil

🧐 Suggested Use

VoluTility is expressly designed as an overlay for sub-pane indicators, where it acts as a second-order rhythm map — exposing hidden structural pressure within volume or volatility streams. When paired with volume (like ZVOL or OBVX), it highlights when flow is expanding with intent versus fading into noise. When layered over volatility signals (like ATR Turbulence or WIRE), it reveals whether expansion has real effort behind it — or is just structural slack.

It pairs especially well with the Relative Directional Index (RDI), where its histogram and ribbon offer early exhaustion signals before traditional trend or momentum fades appear. On raw momentum tools, it acts as a filter: softening false breaks and confirming pressure-backed continuation.

Run on 15m or lower charts for early entry cues or breakout anticipation. On 1H charts, use it to validate compression resolution or detect fatigue before structure turns. It doesn’t react to price — it forecasts readiness.

FSH ATR MTF MonitorThe FSH ATR MTF Monitor tracks the Average True Range (ATR) and current range across six customizable timeframes, displaying the results in a table. When a timeframe’s range exceeds its ATR, the range value turns yellow, signaling heightened volatility. This multi-timeframe tool helps traders assess market conditions and plan entries or exits.

Key Features:

- Monitors ATR and range for up to six timeframes simultaneously.

- Customizable ATR length and timeframe inputs.

- Highlights ranges exceeding ATR in yellow for quick identification.

- Table display with toggle option for flexibility.

How to Use:

1. Add the indicator to your chart.

2. Adjust the ATR length and timeframes in the inputs as needed.

3. Watch for yellow range values to spot volatility spikes across timeframes.

4. Toggle the table off if not needed.

Ideal for scalpers, swing traders, or anyone analyzing volatility across multiple timeframes.

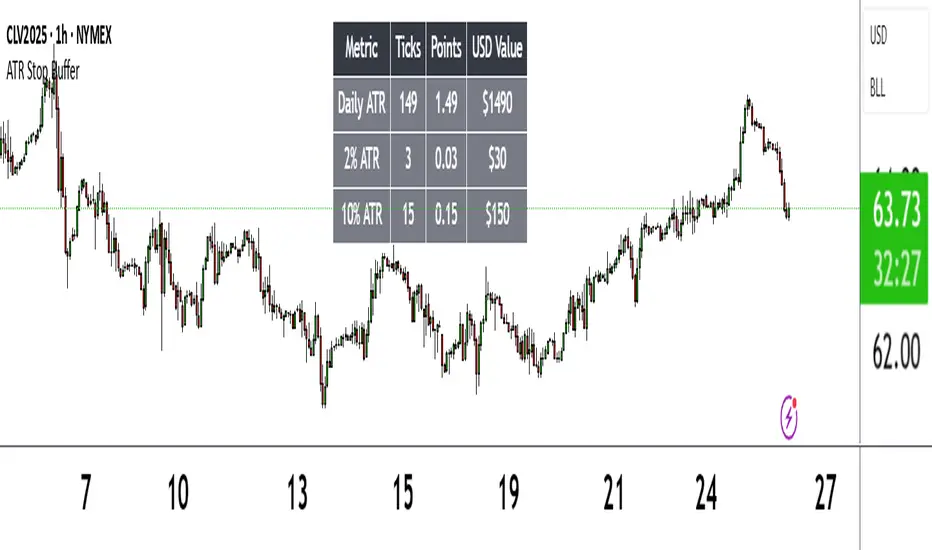

ATR Stop BufferThe ATR Stop Buffer indicator calculates the Daily Average True Range (ATR) and converts it into ticks based on the symbol's minimum price movement. It then displays the full ATR, 2% of ATR, and 10% of ATR in a clean table format, rounded up for simplicity. This tool is ideal for traders who want to set volatility-based stop-loss levels or buffers for their trades.

Key Features:

- Uses a 14-period Daily ATR for robust volatility measurement.

- Converts ATR into ticks for precise application across different instruments.

- Table display with toggle option for flexibility.

- Perfect for risk management and trade planning.

How to Use:

1. Add the indicator to your chart.

2. Use the table values to adjust your stop-loss distances (e.g., 2% ATR for tight stops, 10% ATR for wider buffers).

3. Toggle the table off if you only need the values occasionally.

Note: Works best on instruments with defined tick sizes (e.g., futures, forex, stocks).

Daily Bollinger Band StrategyOverview of the Daily Bollinger Band Strategy

1. Strategy Overview and Features

This strategy is a tool for backtesting a trading method that uses Bollinger Bands. It is *not* a tool for automated trading.

1-1. Main Display Items

The main chart displays the Bollinger Bands and the 200-day moving average.

It also shows the entry and exit points along with the position size (in units of 100 shares).

1-2. Summary of Trading Rules

For long (buy) strategies, the trade enters when the price crosses above the +1σ line of the Bollinger Bands, aiming to ride an upward trend. The position is exited when the price crosses below the middle band.

For short (sell) strategies, the trade enters when the price crosses below the -1σ line of the Bollinger Bands, aiming to ride a downward trend. The position is exited when the price crosses above the middle band.

1-3. Strategic Enhancements

The strategy uses the slope of the 200-day moving average to determine the trend direction and enter trades accordingly. This improves the win rate and payoff ratio.

Additionally, to reduce the probability of ruin, the risk per trade is limited to 1.0% of capital, and position sizing is adjusted using ATR (a volatility indicator).

2. Trading Rules

2-1. Chart Type

Only daily charts are used.

2-2. Indicators Used

(1) Bollinger Bands** (used for entry and exit signals)

- Period: Fixed at 80 days

- Upper and lower bands: Fixed at ±1σ

(2) Moving Average** (used to determine trend direction)

- Period: Fixed at 200 days

- Trend direction is judged based on whether the difference from the previous day is positive (upward) or negative (downward)

2-3. Buy Rules

Setup:

- Price crosses above the +1σ line from below

- Both the middle band and 200-day moving average are upward sloping

Entry:

- Buy at the next day’s market open using a market order

Exit:

- If the price crosses below the middle band, sell at the next day’s open using a market order

2-4. Sell Rules

Setup:

- Price crosses below the -1σ line from above

- Both the middle band and 200-day moving average are downward sloping

Entry:

- Sell at the next day’s market open using a market order

Exit:

- If the price crosses above the middle band, buy back at the next day’s open using a market order

2-5. Risk Management Rules

- Risk per trade: 1.0% of total capital (acceptable loss = capital × 1.0%)

- Position size: Acceptable loss ÷ 2ATR (rounded down to the nearest unit of 100 shares)

2-6. Other Notes

- No brokerage fees

- No pyramiding

- No partial exits

- No reverse positions (no “stop-and-reverse” trades)

3. Strategy Parameters

The following settings can be specified:

3-1. Period Settings

- Start date: Set the start date for the backtest period

- Stop date: Set the end date for the backtest period

3-2. Display of Trend and Signals

- Show trend: When checked, the background color of the bars is light red for an uptrend and light blue for a downtrend

- Show signal: When checked, entry and exit signals are displayed (note: signals are executed at the next day’s open, so there is a one-day lag in the display)

3-3. Capital Management Settings

- Funds: Capital available for trading (in JPY)

- Risk rate: Specify what percentage of the capital to risk per trade

Settings in the “Properties” tab are not used in this strategy.

4. Backtest Results (Example)

Here are the backtest results conducted by the author:

- Target Stocks: All components of the Nikkei 225

- Test Period: January 4, 2000 – December 30, 2024

- Data Points: 12,886

- Win Rate: 33.45%

- Net Profit: ¥82,132,380

- Payoff Ratio: 2.450

- Expected Value: ¥6,373.8

- Risk Rate: 1.0%

- Probability of Ruin: 0.00%

---

デイリー・ボリンジャーバンド・ストラテジーの概要

1. ストラテジーの概要と特徴

このストラテジーは、ボリンジャーバンドを使ったトレード手法のバックテストを行うツールです。自動売買を行うツールではありません。

1-1. 主な表示項目

メインチャートにボリンジャーバンドと 200日移動平均線を表示します。

また、エントリーと手仕舞いのタイミングと数量(100株単位)も表示されます。

1-2. トレードルールの概要

買い戦略の場合、ボリンジャーバンドの +1σ 超えでエントリーして上昇トレンドに乗り、ミドルバンドを割ったら決済します。

売り戦略の場合、ボリンジャーバンドの -1σ 割りでエントリーして下降トレンドに乗り、ミドルバンドを上抜けたら決済します。

1-3. ストラテジーの工夫点

200日移動平均線の傾きを見てトレンド方向にエントリーをしています。こうして勝率とペイオフレシオの成績を向上しています。

また、破産確率を抑えるために、リスク資金比率を 1.0% にして、ATR(ボラティリティ指標) を使って注文数を調整しています。

2. 売買ルール

2-1. 使用するチャート

日足チャートに限定します

2-2. 使用する指標

(1) ボリンジャーバンド(仕掛けと手仕舞いのシグナルに使用)

期間は80日に固定

上下バンドは ±1σ に固定

(2) 移動平均線(トレンドの方向を見るために使用)

期間は200日に固定

移動平均の値の前日との差がプラスのとき上向き、マイナスのとき下向きと判断

2-3. 買いのルール

セットアップ:ボリンジャーバンドの +1σ を価格が下から上に交差 かつ ミドルバンドと 200日移動平均線が上向き

仕掛け:翌日の寄り付きに成行で買う

手仕舞い:ボリンジャーバンドのミドルバンドを価格が上から下に交差したら、翌日の寄り付きに成行で売る

2-4. 売りのルール

セットアップ:ボリンジャーバンドの -1σ を価格が上から下に交差 かつ ミドルバンドと 200日移動平均線が下向き

仕掛け:翌日の寄り付きに成行で売る

手仕舞い:ボリンジャーバンドのミドルバンドを価格が下から上に交差したら、翌日の寄り付きに成行で買い戻す

2-5. 資金管理のルール

リスク資金比率:資産の 1.0%(許容損失 = 資産 × 1.0%)

注文数:許容損失 ÷ 2ATR(単元株数未満は切り捨て)

2-6. その他

仲介手数料:なし

ピラミッディング:なし

分割決済:なし

ドテン:しない

3. ストラテジーのパラメーター

次の項目が指定できます。

3-1. 期間の設定

Staer date : バックテストの検証期間の開始日を指定します

Stop date : バックテストの検証期間の終了日を指定します

3-2. トレンドとシグナルの表示

Show trend : チェックを入れると、バーの背景色が、トレンドが上昇のときは薄い赤で、下落のときは薄い青で表示されます

Show signal : チェックを入れると、エントリーと手仕舞いのシグナルを表示します(シグナルの出た翌日の寄り付きに売買をするので表示に1日のずれがあります)

3-3. 資金管理用の設定

Funds : トレード用の資金(円)

Risk rate : 許容損失を資金の何%にするかで指定します

「プロパティタブ」で設定する値は、このストラテジーでは有効ではありません。

4. バックテストの結果(例)

作者がバックテストを実施した結果をお知らせします。

対象銘柄:日経225構成銘柄すべて

対象期間:2000年1月4日~2024年12月30日

データ件数:12,886

勝率:33.45%

純利益:82,132,380

ペイオフレシオ:2.450

期待値:6,373.8

リスク資金比率:1.0%

破産確率:0.00%

DD ATR ReadingsThe DD ATR Readings indicator displays customizable Average True Range (ATR) multiplier values directly on your chart. Unlike standard ATR indicators that only show a line, this indicator calculates and displays the exact numeric values for three different ATR multipliers, giving you precise volatility measurements for your trading decisions.

It's specifically created for people taking the "Deep Dip Buy" stock trading course, and attempts to provide a ready-to-go solution to allow easy position size calculations as per the course, with the required ATR values visible at a glance.

The default values of 2.0, 1.5 and 0.45 are the same values used by the course instructor in his charting software, but you can change these values to any multiplier you choose.

Any input from students or the instructor is welcome to improve this indicator so it offers more value to those looking to learn how to trade.

Features

Displays three customizable ATR multiplier values (default: 2.0, 1.5, and 0.45 from the course)

Uses either SMA or EMA for ATR calculation (20-period default)

Fully customizable label appearance (position, color, size)

Real-time value updates as you move through the chart

Clean, unobtrusive display that doesn't clutter your chart with additional lines

Customization Options

ATR Length: Number of bars used in the ATR calculation (default: 20)

ATR Multipliers: Three customizable multiplier values

SMA/EMA: Choose your preferred moving average type for ATR calculation

Label Style: Multiple positioning options for the text display

Colors and Size: Fully customizable appearance

BB Breakout + Momentum Squeeze [Strategy]This Strategy is Based on 3 free indicators

- Bollinger Bands Breakout Oscillator: Link

- TTM Squeeze Pro: Link

- Rolling ATR Bands: Link

Bollinger Bands Breakout Oscillator - This tool shows how strong a market trend is by measuring how often prices move outside their normal Bollinger bands range. It helps you see whether prices are strongly moving in one direction or just moving sideways. By looking at how much and how frequently prices push beyond their typical boundaries, you can identify which direction the market is heading over your selected time period.

TM Squeeze Pro - This is a custom version of the TTM Squeeze indicator.

It's designed to help traders spot consolidation phases in the market (when price is coiling or "squeezing") and to catch breakouts early when volatility returns. The logic is based on the relationship between Bollinger Bands and Keltner Channels, combined with a momentum oscillator to show direction and strength.

Rolling ATR Bands - This indicator combines volatility bands (ATR) with momentum and trend signals to show where the market might be breaking out, retesting, or trending. It's highly visual and helpful for traders looking to time entries/exits during trending or volatile moves.

Logic Of the Strategy:

We are going to use the Bollinger Bands Breakout to determine the direction of the market. Than check the Volatility of the price by looking at the TTM Squeeze indicator. And use the ATR Bands to determine dynamic Stop Losses and based on the calculate the Take Profit targets and quantity for each position dynamically.

For the Long Setup:

1. We need to see the that Bull Power (Green line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

For the Short Setup:

1. We need to see the that Bear Power (Red line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

Stop Loss is determined by the Lower ATR Band (for the Long entry) and Upper ATR Band (For the Short entry)

Take Profit is 1:1.5 risk reward ration, which means if the Stop loss is 1% the TP target will be 1.5%

Move stop Loss to Breakeven: If the price will go in the direction of the trade for at least half of the Risk Reward target then the stop will automatically be adjusted to the entry price. For Example: the Stop Loss is 1%, the price has move at least 0.5% in the direction of your trade and that will move the Stop Loss level to the Entry point.

You can Adjust the parameters for each indicator used in that script and also adjust the Risk and Money management block to see how the PnL will change.

Multi-Timeframe ATR MonitorThis indicator displays a table of ATR values across multiple user-defined timeframes (1m, 3m, 5m, 15m, 60m, daily by default) and tracks the session range since 18:00. Customize the timeframes and ATR length via inputs.

RSI + ADX + ATR Combo Indicator: RSI + ADX + ATR Combo Filter

This indicator is a confluence filter tool that combines RSI, ADX, and ATR into a single, easy-to-read chart overlay. It is designed to help traders identify low-volatility, non-trending zones with balanced momentum—ideal for strategies that rely on breakouts or reversals.

🔍 Core Components:

RSI (Relative Strength Index)

Standard RSI with custom upper and lower bounds (default: 60 and 40).

Filters out extreme overbought/oversold regions and focuses on price consolidation zones.

ADX (Average Directional Index)

Measures trend strength.

When ADX is below a custom threshold (default: 20), it indicates a weak or range-bound trend.

ATR (Average True Range)

Represents volatility.

Low ATR values (default threshold: 2.5) are used to filter out high-volatility environments, helping refine entries.

🟣 Signal Logic:

A signal is highlighted with a background color when all three conditions are met:

RSI is between lower and upper bounds (e.g., 40 < RSI < 60) ✅

ADX is below the trend threshold (e.g., ADX < 20) ✅

ATR is below the volatility threshold (e.g., ATR < 2.5) ✅

These combined conditions suggest a low-volatility, low-trend strength, and balanced momentum zone—perfect for anticipating breakouts or strong directional moves.

Open Range Candle [TradeWithRon]This Open Range Break indicator is a tool designed to help traders identify and visualize key price levels using the Opening Range Breakout (ORB) strategy. This indicator dynamically plots critical levels such as the high, low, and middle of a predefined range, along with Fibonacci retracement levels for further analysis. It also features several customization options to fit various trading styles.

Key Features:

Session Setup: Allows the user to set the time offset in GMT - or + to adjust the ORB session to their local time zone.

The default ORB session is set at 9:45 AM but can be adjusted based on user preferences.

Warning: Only supports 5-minute and 15-minute timeframes.

Visual Customization:

Line Styles: Users can choose from Solid, Dotted, or Dashed lines to represent key price levels.

Color Adjustments: Customizable colors for the high, middle, and low levels of the range, as well as Fibonacci levels and vertical lines.

Labeling Options: The labels can be customized in terms of size and color, helping to keep the chart clean and clear.

Fibonacci Retracement Levels: Fibonacci retracement levels are automatically drawn between the high and low of the range. Users can toggle these on or off and customize the offset to suit different trading instruments.

Time-Based Visuals: A vertical line is drawn at the start of the ORB session, providing a clear visual marker of where the breakout starts. This is useful for pinpointing key trade setups.

The indicator supports both 5-minute and 15-minute timeframes.

EMA Integration: The user can enable an Exponential Moving Average (EMA) on any chosen timeframe with adjustable parameters such as the length and color, providing additional trend context.

Dynamic Labeling: The indicator labels the high, middle, and low points of the ORB with custom text. These labels are updated in real-time as new data becomes available.

Limit on Lines and Labels: The indicator allows for a limit on the number of lines and labels drawn to maintain a clean chart, preventing unnecessary clutter as more ORB levels are plotted.

Daily Bias Information: The indicator assesses the daily trend bias (bullish or bearish) based on the relationship between the open and close prices for the last three daily candles, providing context for the current trading session.

Countdown Timer: The remaining time until the end of the current session is displayed in a countdown format, which helps traders to time their entries and exits more precisely.

How To Use:,

- Set the Timeframe to 15 minutes.

- Adjust the Time Zone Offset if needed, based on your local time zone.

- Enable the Show ORB feature for the first 15-minute candle to be drawn as the opening range. - The indicator will automatically mark the high, middle, and low points of the range.

Identify Breakout Points:

Bullish Breakout: If the price breaks above the high of the 15-minute opening range, this indicates a potential bullish breakout. The indicator will plot a vertical line marking the breakout point for further confirmation.

Bearish Breakout: If the price breaks below the low of the 15-minute opening range, this signals a potential bearish breakout. Again, the indicator will plot the breakout point with a vertical line for easy identification.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (Tradewithron) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future

Chonky ATR Levels 2.0Show ATR based high/low projections.

Choose a custom ATR calculation in the indicator's settings.

The default is a 20day RMA based ATR.

----------How projections are calculated----------

To project the ATR High, the ATR value is added to the low of the current candle that matches the ATR's timeframe.

To project the ATR Low, the ATR value is subtracted from the high of the current candle that matches the ATR's timeframe.

Example:

If a 20day RMA ATR is used:

- the ATR High will be the current day's low + the ATR value.

- the ATR Low will be the current day's high - the ATR value.

*However*, if the price action exceeds either ATR projection, the opposite ATR level will be fixed to the extreme of the period.

See the AUDUSD screenshot above for an example.

The ATR Low was exceeded, so the ATR High projection is capped at the high of day.

If the ATR High is exceeded, the ATR Low would be capped at the low of day.

Rachas ATR AssistHey Traders!

This indicator is a simple, it uses Average True Range (ATR) data from the daily chart and the current timeframe to estimate potential range and volatility.

This indicator compares the daily ATR to the current daily wick range (from low to high), helping you gauge how much "room" might be left for price movement within the day. Alongside that, it shows the ATR over the last 14 candles and 5 candles on your current chart for intraday volatility awareness—ideal for setting stops, targets, or position sizing.

Gauge Daily Potential Movement:

The "Day Range Difference" cell shows how much of the expected daily range (based on ATR) is still unfilled. If the market has moved less than the average, there's still potential for expansion. If it's close to or above the ATR, expect a slowdown or reversal.

Position Sizing & Stop Losses:

Use the 14-period ATR and 5-period ATR on your current timeframe to understand recent volatility. This helps in choosing logical stop loss levels and adjusting position sizes based on market conditions.

Volatility Awareness:

Knowing the average daily range and how much of it has been used lets you avoid entering trades too late in the move or placing stops in overly tight spots.

Table Position & Font:

You can adjust the table location (top/bottom left/right) and font size to best fit your chart layout.

Order Block Indicator | DTDHello trader comuunity!

I'm uploading a basic script that I felt necessary to make to help me with some gaps in my day trading. I personally am a visual trader that benefits greatly from automating some the ideas I have in my head. There are awesome builders out there and me creating this script isn't a knock on what's currently available to us, but something I wanted to be able to manage. I am opening up what I've found extremely helpful to my own trading to the community.

Here we have a very simple ATR-based order block (OB) finder. It's not anything original, but I do find consistent opportunities when combined with other tools I use to measure the market. It takes into consideration the previous 25 candles to determine if the OB is significant enough to mark. I use the average of 25 because I simply like it. I use the 25 EMA as part of my "trending" templates and find it to be a hybrid timeframe of sorts. You can find macro and micro trade locations by switching timeframes.

The main elements of the script are:

1. ATR based tracking | A bullish OB is defined as a down close candle that is eclipsed by an up-close candle that closes above its high and sustained for 2 consecutive candles. Inversely, a bearish OB is defined by an up-close candle immediately followed by a down-close candle that closes below the low of the up-close candle and sustains for 2 consecutive candles.

2. Coloring the OB | Though up-close and down-close define bearish and bullish levels, with this script I basically make OBs to switch colors based on where price is relative to the block. So a bullish block can become bearish and bearish can become bullish. Each block also has a dashed midpoint.

3. Order Block Mitigation | When price retests an OB by closing inside of it and retracing back out, that is considered mitigation. You will see price tap into it, but continues to track as a valid block, it's because it didn't close inside the block. This is subject to change in the future, but it's how the script functions for now.

______________

There are nuances to the script that you will see as you use it. Sometimes mitigated OBs act as levels to consider as well. When multiple blocks overlap I consider that a high traffic area. I would never suggest to use an indicator by itself for trade ideas, but blocks that align on multiple timeframes are good to consider.

At the end of the day it's a support and resistance measure. I'll comment an update with a snapshot of the indicator with another proprietary indicator I've made that provides ample intraday trading opportunities.

Cheers,

DTD

Rolling ATR Momentum

Rolling ATR Momentum Indicator – User Manual

---

🔍 Overview

The Rolling ATR Momentum Indicator is a simple yet powerful tool designed to detect shifts in market volatility. It compares the current Average True Range (ATR) with the ATR from a previous point in time to measure how market volatility is changing.

This indicator is especially useful for:

- Spotting the beginning or fading of a momentum phase

- Filtering out low-volatility market conditions

- Enhancing timing for entries and exits in trending or breakout trades

---

📊 Key Components

✅ ATR Delta (Rolling)

- Definition: `ATR Delta = Current ATR - Past ATR`

- Inputs:

- ATR Period (default: 14): The base ATR calculation window

- Lookback Period (default: 5): How many bars ago to compare ATR

- Interpretation:

- Positive ATR Delta (Green Line): Market volatility is increasing

- Negative ATR Delta (Red Line): Market volatility is decreasing

📈 Zero Line

- A horizontal baseline at zero helps you easily see when ATR momentum shifts from negative to positive (or vice versa).

🟩/🟥 Background Color

- Green Background: ATR Delta is positive (rising volatility)

- Red Background: ATR Delta is negative (falling volatility)

🔵 Optional: ATR Reference Lines

- You can optionally display raw Current ATR and Past ATR by changing their visibility settings.

---

✅ How to Use It

Entry Timing (Futures/Options)

- Use ATR Delta as a filter:

- Only take trades when ATR Delta is positive → confirms momentum is building

- Avoid trades when ATR Delta is negative → market might be slow, sideways, or losing steam

Breakout Anticipation

- A rising ATR Delta after a tight range or consolidation can suggest that a breakout is underway

Stop-loss Strategy

- Use high ATR periods for wider stops (to avoid noise)

- Use low ATR periods for tighter stops or skip trading

---

🧠 Pro Tips

- This indicator doesn’t predict direction—combine with trend or price structure tools (like EMA, PPMA, candlesticks)

- Works best in trending or breakout environments

- Add it to multi-timeframe layouts to see volatility buildup on higher timeframes

---

⚙️ Settings

| Parameter | Description |

|----------|-------------|

| ATR Period | Length of the ATR calculation (default 14) |

| Lookback Period | How many bars back to compare ATR values |

---

🧭 Best For:

- Index futures (Nifty, BankNifty)

- Option buyers needing volatility confirmation

- Intraday & swing traders looking to trade momentum setups

---

Use the Rolling ATR Momentum indicator as your volatility radar—simple, clean, and highly effective for staying on the right side of market energy.

End of Manual

Rolling ATR Momentum - EnhancedATR Rolling Momentum Indicator – User Manual

---

🔍 Overview

The ATR Rolling Momentum Indicator is a dynamic volatility tool built on the Average True Range (ATR). It not only tracks increasing or decreasing momentum but also provides early warnings and confirmation signals for potential breakout moves. It’s especially powerful for futures and options traders looking to align with expanding price action.

---

📊 Core Components

✅ ATR Delta (Rolling ATR)

- Definition: Difference between current ATR and past ATR (user-defined lookback).

- Use: Tells whether volatility is expanding (positive delta) or contracting (negative delta).

- Visual: Green line for rising momentum, red for declining.

🟣 ATR Delta Slope

- Definition: Measures acceleration in momentum.

- Use: Helps identify early signs of breakout buildup.

- Visual: Purple line. Watch for slope turning up from below.

🟡 Volatility Squeeze (Yellow Dot)

- Definition: Current ATR is significantly lower than its 20-period average.

- Use: Indicates the market is coiling—possible breakout ahead.

🔼 Momentum Start (Green Triangle)

- Definition: ATR Delta slope turns from negative to positive.

- Use: Early warning to prepare for volatility expansion.

🔷 Breakout Confirmation (Blue Label Up)

- Definition: ATR Delta exceeds its high of the last 10 candles.

- Use: Confirms volatility breakout—trade opportunity if direction aligns.

🟩/🟥 Background Color

- Green Background: Momentum rising (positive ATR delta)

- Red Background: Momentum falling (negative ATR delta)

- Yellow Tint: Active squeeze zone

---

✅ How to Use It (Futures/Options Focus)

Step-by-Step:

1. Squeeze Detected (Yellow Dot) → Stay alert. Market is coiling.

2. Green Triangle Appears → Momentum is starting to rise.

3. Background Turns Green → Confirmed rising momentum.

4. Blue Label Appears → Confirmed breakout (enter trade if trend aligns).

Directional Bias:

- Use your main chart setup (price action, EMAs, trendlines, etc.) to decide direction (Call or Put, Long or Short).

- ATR Momentum only tells you how strong the move is—not which way.

---

⚙️ Inputs & Settings

- ATR Period: Default 14 (core volatility measure)

- Rolling Lookback: Used to calculate delta (default 5)

- Slope Length: Used to measure acceleration (default 3)

- Squeeze Factor: Default 0.8 — lower = more sensitive squeeze detection

- Breakout Lookback: Checks ATR delta against last X bars (default 10)

---

🧠 Pro Tips

- Works great when paired with EMA stacks, price structure, or breakout patterns.

- Avoid taking trades based only on squeeze or momentum—combine with chart confirmation.

- If background turns red after a breakout, it may be losing momentum—book partials or tighten stops.

---

🧭 Ideal For:

- Nifty/BankNifty Futures

- Option directional trades (call/put buying)

- Index scalping and momentum swing setups

---

Use this tool as your volatility compass—it won't tell you where to go, but it'll tell you when the wind is strong enough to move fast.

End of Manual

Smart Money Breakout & Order Block StrategySmart Money Breakout & Order Block Strategy

Created by Shubham

This strategy was developed by Shubham, designed to provide traders with a structured approach to smart money trading by combining breakout entries and order block reversals. It focuses on liquidity zones, volatility filters, and ATR-based stop management to adapt to different market conditions.

🔹 Strategy Overview

The Smart Money Breakout & Order Block Strategy is built for traders who want to identify institutional moves while avoiding false breakouts. This non-repainting strategy helps traders detect:

✅ Momentum Breakouts – Price breaking key support & resistance levels.

✅ Order Block Reversals – Institutional buying & selling zones.

✅ Dynamic Stop Management – No fixed SL/TP; uses ATR-based trailing stops.

✅ Volatility Filtering – Avoids choppy market conditions.

🔹 Trading Logic

1️⃣ Breakout Trading (Momentum Entries)

Long Entry: When price breaks above resistance with high volatility.

Short Entry: When price breaks below support with high volatility.

2️⃣ Order Block Reversals (Liquidity Entries)

Bullish Order Block: A strong price rejection after consecutive bearish candles signals smart money accumulation, triggering a long trade.

Bearish Order Block: A strong price rejection after consecutive bullish candles signals smart money distribution, triggering a short trade.

3️⃣ Volatility Filter (False Signal Prevention)

Uses normalized volatility to ensure breakouts are backed by strong momentum.

Helps filter out low-volume, choppy market conditions.

4️⃣ ATR-Based Position Management (Dynamic Stops & Trailing Stop)

No fixed SL/TP → Uses ATR-based stop-loss to adapt to market volatility.

Implements a trailing stop for maximizing potential profits in trending markets.

🔹 Key Features

✔️ Developed by Shubham – Designed for precision trading with institutional techniques.

✔️ Smart Money Concept – Identifies liquidity zones, breakouts, and order blocks.

✔️ Volatility Filter – Prevents false breakouts by analyzing market momentum.

✔️ ATR-Based Dynamic Stops – No fixed SL/TP, making it more adaptive.

✔️ Trailing Stop Functionality – Allows profits to run while reducing risk.

✔️ Fully Automated Execution – Uses TradingView’s strategy functions for automatic trade placement and exits.

✔️ Commission-Adjusted Backtesting – Includes realistic commission settings to ensure accurate results.

📊 Backtesting & Realistic Expectations

✅ Best for Higher Timeframes (1H, 4H, Daily) – Avoids market noise.

✅ Most Effective in Trending & Volatile Markets – Crypto, forex, indices, and commodities.

✅ Performance Varies with Market Conditions – Works best in strong trends.

✅ No Unrealistic Promises – Strategy performance is dependent on market behavior and risk management.

📌 IMPORTANT DISCLAIMER:

This strategy is provided for educational purposes only and should not be considered financial advice. Past performance in backtesting does not guarantee future results. Users should conduct their own research before applying this strategy in live markets.

🚀 Developed by Shubham – Test it yourself and see how it performs! 🚀

Smart Grid Scalping (Pullback) Strategy[BullByte]The Smart Grid Scalping (Pullback) Strategy is a high-frequency trading strategy designed for short-term traders who seek to capitalize on market pullbacks. This strategy utilizes a dynamic ATR-based grid system to define optimal entry points, ensuring precise trade execution. It integrates volatility filtering and an RSI-based confirmation mechanism to enhance signal accuracy and reduce false entries.

This strategy is specifically optimized for scalping by dynamically adjusting trade levels based on current market conditions. The grid-based system helps capture retracement opportunities while maintaining strict trade management through predefined profit targets and trailing stop-loss mechanisms.

Key Features :

1. ATR-Based Grid System :

- Uses a 10-period ATR to dynamically calculate grid levels for entry points.

- Prevents chasing trades by ensuring price has reached key levels before executing entries.

2. No Trade Zone Protection :

- Avoids low-volatility zones where price action is indecisive.

- Ensures only high-momentum trades are executed to improve success rate.

3. RSI-Based Entry Confirmation :

- Long trades are triggered when RSI is below 30 (oversold) and price is in the lower grid zone.

- Short trades are triggered when RSI is above 70 (overbought) and price is in the upper grid zone.

4. Automated Trade Execution :

- Long Entry: Triggered when price drops below the first grid level with sufficient volatility.

- Short Entry: Triggered when price exceeds the highest grid level with sufficient volatility.

5. Take Profit & Trailing Stop :

- Profit target set at a customizable percentage (default 0.2%).

- Adaptive trailing stop mechanism using ATR to lock in profits while minimizing premature exits.

6. Visual Trade Annotations :

- Clearly labeled "LONG" and "SHORT" markers appear at trade entries for better visualization.

- Grid levels are plotted dynamically to aid decision-making.

Strategy Logic :

- The script first calculates the ATR-based grid levels and ensures price action has sufficient volatility before allowing trades.

- An additional RSI filter is used to ensure trades are taken at ideal market conditions.

- Once a trade is executed, the script implements a trailing stop and predefined take profit to maximize gains while reducing risks.

---

Disclaimer :

Risk Warning :

This strategy is provided for educational and informational purposes only. Trading involves significant risk, and past performance is not indicative of future results. Users are advised to conduct their own due diligence and risk management before using this strategy in live trading.

The developer and publisher of this script are not responsible for any financial losses incurred by the use of this strategy. Market conditions, slippage, and execution quality can affect real-world trading outcomes.

Use this script at your own discretion and always trade responsibly.

VIDYA Auto-Trading(Reversal Logic)Overview

This script is a dynamic trend-following strategy based on the Variable Index Dynamic Average (VIDYA). It adapts in real time to market volatility, aiming to enhance entry precision and optimize risk management.

⚠️ This strategy is intended for educational and research purposes. Past performance does not guarantee future results. All results are based on historical simulations using fixed parameters.

Strategy Objectives

The objective of this strategy is to respond swiftly to sudden price movements and trend reversals, providing consistent and reliable trade signals under historical testing conditions. It is designed to be intuitive and efficient for traders of all levels.

Key Features

Momentum Sensitivity via VIDYA: Reacts quickly to momentum shifts, allowing for accurate trend-following entries.

Volatility-Based ATR Bands: Automatically adjusts stop levels and entry conditions based on current market volatility.

Intuitive Trend Visualization: Uptrends are marked with green zones, and downtrends with red zones, giving traders clear visual guidance.

Trading Rules

Long Entry: Triggered when price crosses above the upper band. Any existing short position is closed.

Short Entry: Triggered when price crosses below the lower band. Any existing long position is closed.

Exit Conditions: Positions are reversed based on signal changes, using a position reversal strategy.

Risk Management Parameters

Market: ETHUSD(5M)

Account Size: $3,000 (reasonable approximation for individual traders)

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted to comply with TradingView guidelines for realistic risk levels)

Number of Trades: 251 (based on backtest over the selected dataset)

⚠️ The risk per trade and other values can be customized. Users are encouraged to adapt these to their individual needs and broker conditions.

Trading Parameters & Considerations

VIDYA Length: 10

VIDYA Momentum: 20

Distance factor for upper/lower bands: 2

Source: close

Visual Support

Trend zones, entry points, and directional shifts are clearly plotted on the chart. These visual cues enhance the analytical experience and support faster decision-making.

Visual elements are designed to improve interpretability and are not intended as financial advice or trade signals.

Strategy Improvements & Uniqueness

Inspired by the public work of BigBeluga, this script evolves the original concept with meaningful enhancements. By combining VIDYA and ATR bands, it offers greater adaptability and practical value compared to conventional trend-following strategies.

This adaptation is original work and not a direct copy. Improvements are designed to enhance usability, risk control, and market responsiveness.

Summary

This strategy offers a responsive and adaptive approach to trend trading, built on momentum detection and volatility-adjusted risk management. It balances clarity, precision, and practicality—making it a powerful tool for traders seeking reliable trend signals.

⚠️ All results are based on historical data and are subject to change under different market conditions. This script does not guarantee profit and should be used with caution and proper risk management.