ATR with Donchian Channels and SMAsThis script combines the Average True Range (ATR), Donchian Channels, and Simple Moving Averages (SMAs) to provide a comprehensive tool for volatility and trend analysis.

Key Components:

ATR Calculation: The ATR is used to measure market volatility. It is calculated as a moving average of the true range over a specified length, which you can customize using different smoothing methods: RMA, SMA, EMA, or WMA. ATR helps identify periods of high and low volatility, giving insights into potential breakout or consolidation phases in the market.

Donchian Channels on ATR: The Donchian Channels are calculated based on the highest and lowest values of the ATR over a user-defined period. The upper and lower bands provide a volatility range, and the middle line represents the average of the two. This can help visualize the range of market volatility and detect possible trend reversals or continuations.

SMAs on ATR: Two Simple Moving Averages (SMA) are applied to the ATR values. These SMAs act as a smoothed version of the ATR, providing additional insight into volatility trends. By adjusting the length of these SMAs, you can track short-term and long-term volatility movements, helping in decision-making for potential entries and exits.

Inputs:

ATR Length: Set the length for calculating the ATR.

Smoothing Method: Choose from RMA, SMA, EMA, or WMA for smoothing the ATR calculation.

Donchian Channel Length: Set the length for calculating the highest and lowest ATR values for Donchian Channels.

SMA Lengths: Two adjustable lengths for applying SMAs to the ATR.

Visualization:

ATR Plot: The ATR is plotted in red, allowing you to see the market's volatility at a glance.

Donchian Channels: Blue lines represent the upper and lower bands, while the green line represents the middle line of the Donchian Channels, helping you visualize the volatility range.

SMAs: Two SMAs (green and orange) are plotted to smooth out the ATR and identify trends in volatility.

Use Cases:

Breakout Detection: High ATR values breaking out of the Donchian Channels may signal increased volatility and a potential breakout.

Trend Analysis: SMAs on ATR help smooth volatility trends, aiding in determining if the market is entering a more volatile or stable period.

Stop-Loss Placement: ATR and Donchian Channels can be used to set dynamic stop-loss levels based on market volatility.

This script is versatile and can be used across different asset classes, such as stocks, forex, crypto, and commodities. It is especially useful for traders who want to incorporate volatility into their trading strategies for better risk management and trend detection.

Average True Range (ATR)

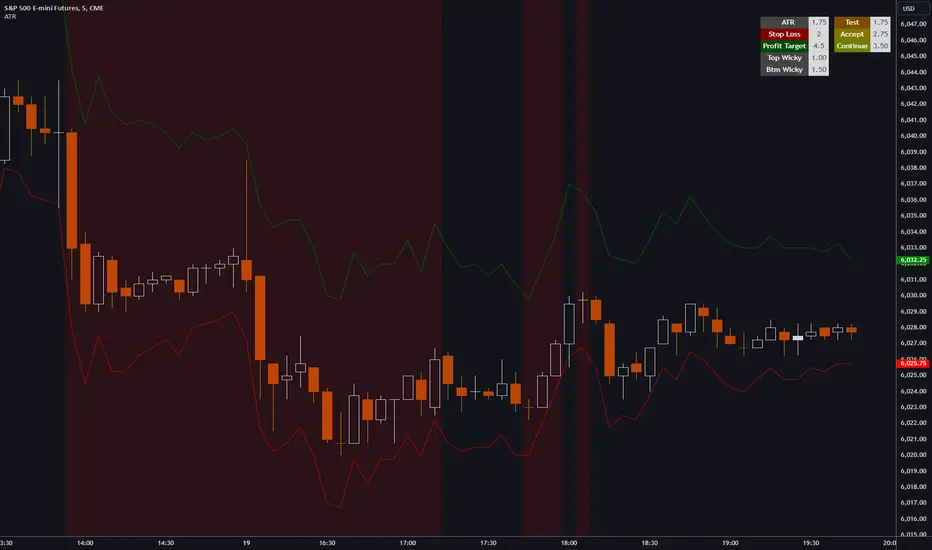

ATR, Chop, Profit Target and Stop Loss TableThe ATR Table indicator is a versatile tool that helps traders visually and quantitatively manage risk, identify market conditions, and set profit targets and stop-loss levels. It is designed to enhance decision-making by incorporating key volatility and chop (market consolidation) signals into a comprehensive table format.

Key Features:

Average True Range (ATR) Calculation : The indicator computes the ATR over a user-defined period (default 14). ATR helps to measure market volatility, providing insights into how much an asset's price typically moves within a given period.

Stop Loss and Profit Target Calculation : You can configure stop-loss and profit target levels using multipliers based on the ATR. This allows dynamic risk management that adjusts to market volatility:

Stop Loss : Defined as a multiple of the ATR to help control losses.

Profit Target : Also based on a multiple of the ATR to lock in gains. The user can specify whether they are trading long or short, and the indicator adjusts the levels accordingly.

Customizable Plot Lines : The indicator can display the Stop Loss and Profit Target levels directly on the chart. Users can toggle these lines on or off and customize their colors.

Chop Signa l: The indicator highlights potential consolidation periods (chop) using a wick-based analysis. It calculates the highest upper or lower wick values and compares them to the ATR to detect periods of indecision or consolidation.

Table Display : When these wick values exceed the ATR by a user-defined multiplier, the corresponding table rows are highlighted.

Background Alerts : Optionally, users can activate background color changes on the chart to visually alert them when chop conditions are detected.

Customizable Table Layout : A table displaying the key values (ATR, Stop Loss, Profit Target, Upper/Lower Wickiness) is placed on the chart. You can choose the table's position, adjust its color scheme, and decide which rows to display.

Chop Background Customization : For users who prefer more visual cues, the indicator allows you to enable or disable background shading when chop conditions are met. You can also choose the color of this background for better customization.

KAMA CloudDescription:

The KAMA Cloud indicator is a sophisticated trading tool designed to provide traders with insights into market trends and their intensity. This indicator is built on the Kaufman Adaptive Moving Average (KAMA), which dynamically adjusts its sensitivity to filter out market noise and respond to significant price movements. The KAMA Cloud leverages multiple KAMAs to gauge trend direction and strength, offering a visual representation that is easy to interpret.

How It Works:

The KAMA Cloud uses twenty different KAMA calculations, each set to a distinct lookback period ranging from 5 to 100. These KAMAs are calculated using the average of the open, high, low, and close prices (OHLC4), ensuring a balanced view of price action. The relative positioning of these KAMAs helps determine the direction of the market trend and its momentum.

By measuring the cumulative relative distance between these KAMAs, the indicator effectively assesses the overall trend strength, akin to how the Average True Range (ATR) measures market volatility. This cumulative measure helps in identifying the trend’s robustness and potential sustainability.

The visualization component of the KAMA Cloud is particularly insightful. It plots a 'cloud' formed between the base KAMA (set at a 100-period lookback) and an adjusted KAMA that incorporates the cumulative relative distance scaled up. This cloud changes color based on the trend direction — green for upward trends and red for downward trends, providing a clear, visual representation of market conditions.

Benefits:

Dynamic Sensitivity: By adapting to the market's volatility, KAMA provides more reliable signals than traditional moving averages.

Trend Clarity: The color-coded cloud visually enhances the perception of the trend’s direction and strength, making it easier for traders to decide on their trading strategy.

Versatility: Suitable for various asset classes, including stocks, forex, commodities, and cryptocurrencies, across different timeframes.

Decision Support: Helps traders understand not just the direction but the strength of trends, aiding in more informed decision-making regarding entries, exits, and risk management.

Usage:

The KAMA Cloud is ideal for traders who need a robust trend-following tool that adjusts according to market dynamics. It can be used as a standalone indicator or in conjunction with other technical analysis tools to enhance trading strategies. Look for the cloud’s color shifts as potential signals for trend reversals or continuations, and consider the cloud’s thickness as an indication of trend strength.

Whether you are a day trader, swing trader, or long-term investor, the KAMA Cloud offers a unique approach to understanding market trends, helping you navigate the complexities of various market conditions with confidence.

Iceberg Trade Revealer [CHE]Unveiling Iceberg Trades: A Deep Dive into Low Volatility Market Phases

Introduction

In the dynamic world of trading, hidden forces often influence market movements in ways that aren't immediately apparent. One such force is the phenomenon of iceberg trades—large orders that are concealed to prevent significant market impact. This presentation explores the concept of iceberg trades, explains why they are typically hidden during periods of low volatility, and introduces an indicator designed to reveal these elusive trades.

Agenda

1. Understanding Iceberg Trades

- Definition and Purpose

- Impact on Market Dynamics

2. The Low Volatility Concealment

- Why Low Volatility Phases?

- Strategies Behind Hiding Large Orders

3. Introducing the Iceberg Trade Revealer Indicator

- How the Indicator Works

- Key Components and Calculations

4. Demonstration and Use Cases

- Interpreting the Indicator Signals

- Practical Trading Applications

5. Conclusion

- Summarizing the Insights

- Q&A Session

1. Understanding Iceberg Trades

Definition and Purpose

- Iceberg Trades are large single orders divided into smaller lots to disguise the total order quantity.

- Traders use iceberg orders to minimize market impact and avoid unfavorable price movements.

Impact on Market Dynamics

- Concealed Volume: Iceberg orders hide true supply and demand levels.

- Price Stability: They prevent sudden spikes or drops by releasing orders gradually.

- Market Sentiment: Their presence can influence perceptions of market strength or weakness.

2. The Low Volatility Concealment

Why Low Volatility Phases?

- Less Market Attention: Low volatility periods attract fewer traders, making it easier to conceal large orders.

- Reduced Slippage: Prices are more stable, reducing the risk of executing orders at unfavorable prices.

- Strategic Advantage: Large players can accumulate or distribute positions without tipping off the market.

Strategies Behind Hiding Large Orders

- Order Splitting: Breaking down large orders into smaller pieces.

- Time Slicing: Executing orders over an extended period.

- Algorithmic Trading: Using sophisticated algorithms to optimize order execution.

3. Introducing the Iceberg Trade Revealer Indicator

How the Indicator Works

- Core Thesis: Iceberg trades can be detected by analyzing periods of unusually low volatility.

- Volatility Analysis: Uses the Average True Range (ATR) and Bollinger Bands to identify low volatility phases.

- Signal Generation: Marks periods where iceberg trades are likely occurring.

Key Components and Calculations

1. Average True Range (ATR)

- Measures market volatility over a specified period.

- Lower ATR values indicate less price movement.

2. Bollinger Bands

- Creates a volatility envelope around the ATR.

- Bands tighten during low volatility and widen during high volatility.

3. Timeframe Adjustments

- Utilizes multiple timeframes to enhance signal accuracy.

- Options for auto, multiplier, or manual timeframe selection.

4. Signal Conditions

- Iceberg Trade Detection: ATR falls below the lower Bollinger Band.

- Revealed Volatility: ATR rises above the upper Bollinger Band, indicating potential market moves after iceberg trades.

4. Demonstration and Use Cases

Interpreting the Indicator Signals

- Iceberg Trade Zones: Highlighted areas where large hidden orders are likely.

- Revealed Volatility Zones: Areas indicating the market's response to the execution of iceberg trades.

Practical Trading Applications

- Entry and Exit Points: Use signals to time trades alongside institutional activity.

- Risk Management: Adjust strategies during detected low volatility phases.

- Market Analysis: Gain insights into underlying market mechanics.

5. Conclusion

Summarizing the Insights

- Iceberg Trades play a significant role in market movements, especially when concealed during low volatility phases.

- The Iceberg Trade Revealer Indicator provides a tool to uncover these hidden activities, offering traders a strategic edge.

- Understanding and utilizing this indicator can enhance trading decisions by aligning them with the actions of major market players.

Best regards Chervolino ( Volker )

Q&A Session

- Questions and Discussions: Open the floor for any queries or further explanations.

Thank You!

By delving into the hidden aspects of market activity, traders can better navigate the complexities of financial markets. The Iceberg Trade Revealer Indicator serves as a bridge between observable market data and the concealed strategies of large institutions.

References

- Average True Range (ATR): A technical analysis indicator that measures market volatility.

- Bollinger Bands: A volatility indicator that creates a band of three lines which are plotted in relation to a security's price.

- Iceberg Orders: Large orders divided into smaller lots to hide the actual order quantity.

Note: Always consider multiple factors when making trading decisions. Indicators provide tools, but they do not guarantee results.

Educational Content Disclaimer:

Disclaimer:

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Neural Momentum StrategyThis strategy combines Exponential Moving Average (EMA) analysis with a multi-timeframe approach. It uses a neural scoring system to evaluate market momentum and generate precise trading signals. The strategy is implemented in Pine Script v5 and is designed for use on TradingView.

Key Components

The strategy utilizes short-term (10-period) and long-term (25-period) EMAs. It calculates the difference between these EMAs to assess trend direction and strength. A neural scoring system evaluates EMA crossovers (weight: 12 points), trend strength (weight: 10 points), and price acceleration (weight: 4 points). The system implements a score smoothing algorithm using a 10-period EMA.

Multi-timeframe Analysis

The strategy automatically selects a higher timeframe based on the current chart timeframe. It calculates scores for both the current and higher timeframes, then combines these scores using a weighted average. The higher timeframe factor ranges from 3 to 6, depending on the current timeframe.

Trading Logic

Entry occurs when the final combined score turns positive after a change. Exit happens when the final combined score turns negative after a change. The strategy recalculates scores on each bar, ensuring responsive trading decisions.

Risk Management

An optional adaptive stop-loss system based on Average True Range (ATR) is available. The default ATR period is 10, and the stop factor is 1.2. Stop levels are dynamically adjusted on the higher timeframe.

Customization Options

Users can adjust EMA periods, signal line period, scoring weights, and enable/disable multi-timeframe analysis. The strategy allows setting specific date ranges for backtesting and deployment.

Position Sizing

The strategy uses a percentage-of-equity position sizing method, with a default of 30% of account equity per trade.

Code Structure

The strategy is built using TradingView's strategy framework. It employs efficient use of the request.security() function for multi-timeframe analysis. The main calculation function, calculate_score(), computes the neural score based on EMA differences and acceleration.

Performance Considerations

The strategy adapts to various market conditions through its multi-faceted scoring system. Multi-timeframe analysis helps filter out noise and identify stronger trends. The neural scoring approach aims to capture subtle market dynamics often missed by traditional indicators.

Limitations

Performance may vary across different markets and timeframes. The strategy's effectiveness relies on proper calibration of its numerous parameters. Users should thoroughly backtest and forward test before live implementation.

To summarize, the Neural Momentum Strategy represents a sophisticated approach to market analysis. It combines traditional technical indicators with advanced scoring techniques and multi-timeframe analysis. This strategy is designed for traders seeking a data-driven and adaptive method. It aims to identify high-probability trading opportunities across various market conditions.

This Neural Momentum Strategy is for informational and educational purposes only. It should not be considered financial advice. The strategy may exhibit slight repainting behavior due to the nature of multi-timeframe analysis and the use of the request.security() function. Historical values might change as new data becomes available.

Trading carries a high level of risk, and may not be suitable for all investors. Before deciding to trade, you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss of some or all of your initial investment. Therefore, you should not invest money that you cannot afford to lose.

Past performance is not indicative of future results. The author and TradingView are not responsible for any losses incurred as a result of using this strategy. Always exercise caution when using this or any trading strategy, and thoroughly test it before implementing in live trading scenarios.

Users are solely responsible for any trading decisions they make based on this strategy. It is strongly recommended that you seek advice from an independent financial advisor if you have any doubts.

$TUBR: Stop Loss IndicatorATR-Based Stop Loss Indicator for TradingView by The Ultimate Bull Run Community: TUBR

**Overview**

The ATR-Based Stop Loss Indicator is a custom tool designed for traders using TradingView. It helps you determine optimal stop loss levels by leveraging the Average True Range (ATR), a popular measure of market volatility. By adapting to current market conditions, this indicator aims to minimize premature stop-outs and enhance your risk management strategy.

---

**Key Features**

- **Dynamic Stop Loss Levels**: Calculates stop loss prices based on the ATR, providing both long and short stop loss suggestions.

- **Customizable Parameters**: Adjust the ATR period, multiplier, and smoothing method to suit your trading style and the specific instrument you're trading.

- **Visual Aids**: Plots stop loss lines directly on your chart for easy visualization.

- **Alerts and Notifications** (Optional): Set up alerts to notify you when the price approaches or hits your stop loss levels.

---

**Understanding the Indicator**

1. **Average True Range (ATR)**:

- **What It Is**: ATR measures market volatility by calculating the average range between high and low prices over a specified period.

- **Why It's Useful**: A higher ATR indicates higher volatility, which can help you set stop losses that accommodate market fluctuations.

2. **ATR Multiplier**:

- **Purpose**: Determines how far your stop loss is placed from the current price based on the ATR.

- **Example**: An ATR multiplier of 1.5 means the stop loss is set at 1.5 times the ATR away from the current price.

3. **Smoothing Methods**:

- **Options**: Choose from RMA (default), SMA, EMA, WMA, or Hull MA.

- **Effect**: Different smoothing methods can make the ATR more responsive or smoother, affecting where the stop loss is placed.

---

**How the Indicator Works**

- **Long Stop Loss Calculation**:

- **Formula**: `Long Stop Loss = Close Price - (ATR * ATR Multiplier)`

- **Purpose**: For long positions, the stop loss is set below the current price to protect against downside risk.

- **Short Stop Loss Calculation**:

- **Formula**: `Short Stop Loss = Close Price + (ATR * ATR Multiplier)`

- **Purpose**: For short positions, the stop loss is set above the current price to protect against upside risk.

- **Plotting on the Chart**:

- **Green Line**: Represents the suggested stop loss level for long positions.

- **Red Line**: Represents the suggested stop loss level for short positions.

---

**How to Use the Indicator**

1. **Adding the Indicator to Your Chart**:

- **Step 1**: Copy the PineScript code of the indicator.

- **Step 2**: In TradingView, click on **Pine Editor** at the bottom of the platform.

- **Step 3**: Paste the code into the editor and click **Add to Chart**.

- **Step 4**: The indicator will appear on your chart with the default settings.

2. **Adjusting the Settings**:

- **ATR Period**:

- **Definition**: Number of periods over which the ATR is calculated.

- **Adjustment**: Increase for a smoother ATR; decrease for a more responsive ATR.

- **ATR Multiplier**:

- **Definition**: Factor by which the ATR is multiplied to set the stop loss distance.

- **Adjustment**: Increase to widen the stop loss (less likely to be hit); decrease to tighten the stop loss.

- **Smoothing Method**:

- **Options**: RMA, SMA, EMA, WMA, Hull MA.

- **Adjustment**: Experiment to see which method aligns best with your trading strategy.

- **Display Options**:

- **Show Long Stop Loss**: Toggle to display or hide the long stop loss line.

- **Show Short Stop Loss**: Toggle to display or hide the short stop loss line.

3. **Interpreting the Indicator**:

- **Long Positions**:

- **Action**: Set your stop loss at the value indicated by the green line when entering a long trade.

- **Short Positions**:

- **Action**: Set your stop loss at the value indicated by the red line when entering a short trade.

- **Adjusting Stop Losses**:

- **Trailing Stops**: You may choose to adjust your stop loss over time, moving it in the direction of your trade as the ATR-based stop loss levels change.

4. **Implementing in Your Trading Strategy**:

- **Risk Management**:

- **Position Sizing**: Use the stop loss distance to calculate your position size based on your risk tolerance.

- **Consistency**: Apply the same settings consistently to maintain discipline.

- **Combining with Other Indicators**:

- **Enhance Decision-Making**: Use in conjunction with trend indicators, support and resistance levels, or other technical analysis tools.

- **Alerts Setup** (If included in the code):

- **Purpose**: Receive notifications when the price approaches or hits your stop loss level.

- **Configuration**: Set up alerts in TradingView based on the alert conditions defined in the indicator.

---

**Benefits of Using This Indicator**

- **Adaptive Risk Management**: By accounting for current market volatility, the indicator helps prevent setting stop losses that are too tight or too wide.

- **Minimize Premature Stop-Outs**: Reduces the likelihood of being stopped out due to normal price fluctuations.

- **Flexibility**: Customizable settings allow you to tailor the indicator to different trading instruments and timeframes.

- **Visualization**: Clear visual representation of stop loss levels aids in quick decision-making.

---

**Things to Consider**

- **Market Conditions**:

- **High Volatility**: Be cautious as ATR values—and thus stop loss distances—can widen, increasing potential losses.

- **Low Volatility**: Tighter stop losses may increase the chance of being stopped out by minor price movements.

- **Backtesting and Optimization**:

- **Historical Analysis**: Test the indicator on past data to evaluate its effectiveness and adjust settings accordingly.

- **Continuous Improvement**: Regularly reassess and fine-tune the parameters to adapt to changing market conditions.

- **Risk Per Trade**:

- **Alignment with Risk Tolerance**: Ensure the stop loss level keeps potential losses within your acceptable risk per trade (e.g., 1-2% of your trading capital).

- **Emotional Discipline**:

- **Stick to Your Plan**: Avoid making impulsive changes to your stop loss levels based on emotions rather than analysis.

---

**Example Usage Scenario**

1. **Setting Up a Long Trade**:

- **Entry Price**: $100

- **ATR Value**: $2

- **ATR Multiplier**: 1.5

- **Calculated Stop Loss**: $100 - ($2 * 1.5) = $97

- **Action**: Place a stop loss order at $97.

2. **During the Trade**:

- **Price Increases to $105**

- **ATR Remains at $2**

- **New Stop Loss Level**: $105 - ($2 * 1.5) = $102

- **Action**: Move your stop loss up to $102 to lock in profits.

---

**Final Tips**

- **Documentation**: Keep a trading journal to record your trades, stop loss levels, and observations for future reference.

- **Education**: Continuously educate yourself on risk management and technical analysis to enhance your trading skills.

- **Support**: Engage with trading communities or seek professional advice if you're unsure about implementing the indicator effectively.

---

**Conclusion**

The ATR-Based Stop Loss Indicator is a valuable tool for traders looking to enhance their risk management by setting stop losses that adapt to market volatility. By integrating this indicator into your trading routine, you can improve your ability to protect capital and potentially increase profitability. Remember to use it as part of a comprehensive trading strategy, and always adhere to sound risk management principles.

---

**How to Access the Indicator**

To start using the ATR-Based Stop Loss Indicator, follow these steps:

1. **Obtain the Code**: Copy the PineScript code provided for the indicator.

2. **Create a New Indicator in TradingView**:

- Open TradingView and navigate to the **Pine Editor**.

- Paste the code into the editor.

- Click **Save** and give your indicator a name.

3. **Add to Chart**: Click **Add to Chart** to apply the indicator to your current chart.

4. **Customize Settings**: Adjust the input parameters to suit your preferences and start integrating the indicator into your trading strategy.

---

**Disclaimer**

Trading involves significant risk, and it's possible to lose all your capital. The ATR-Based Stop Loss Indicator is a tool to aid in decision-making but does not guarantee profits or prevent losses. Always conduct your own analysis and consider seeking advice from a financial professional before making trading decisions.

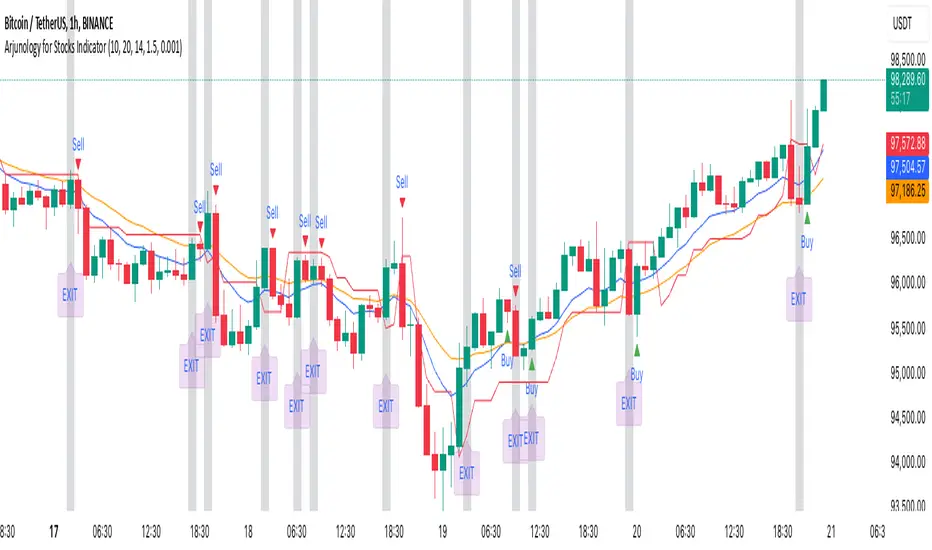

Arjunology for Stocks IndicatorArjunology for Stocks Indicator is a unique trend-following and exit management system that combines the power of Exponential Moving Averages (EMA) and Average True Range (ATR) to capture market trends and manage trade exits dynamically. It is designed to help traders identify potential buy and sell points based on market trends while incorporating volatility adjustments to avoid false signals and provide more reliable trade entries and exits.

Key Features:

1. Exponential Moving Averages (EMAs):

• Two EMAs (Short EMA and Long EMA) are used to determine trend direction and potential crossover signals.

• Short EMA reacts quickly to price changes, giving an indication of shorter-term trends.

• Long EMA provides a more stable measure of the overall trend direction, helping filter out market noise.

• Bullish Crossovers: When the short EMA crosses above the long EMA, it signals a potential uptrend (buy condition).

• Bearish Crossovers: When the short EMA crosses below the long EMA, it signals a potential downtrend (sell condition).

2. Average True Range (ATR):

• ATR is used to assess market volatility and avoid false signals during low volatility periods.

• A trailing stop loss mechanism based on ATR ensures that the indicator adapts to the current market environment, with higher volatility allowing for wider stops and lower volatility leading to tighter stops.

• A flat ATR threshold is used to avoid signals during quiet periods, where price movement may be too insignificant to trade effectively.

3. Buy and Sell Visual Cues:

• Green Triangle at the bottom of the candle when a bullish crossover (buy) condition is met.

• Red Triangle at the top of the candle when a bearish crossover (sell) condition is met.

• These visual cues help traders quickly identify trade entry points based on the trend signals.

4. Dynamic Exit Management:

• The indicator provides an Blue candle background to highlight exit points, with an “EXIT” label at the bottom of the candle in blue. This visual exit signal ensures clarity when a trade should be exited based on the trend reversal.

Justification for Combining EMAs and ATR in This Script:

The Exponential Moving Averages (EMAs) and Average True Range (ATR) serve complementary purposes in this script, enhancing each other’s functionality to provide a more complete trading system:

1. Trend Identification with EMAs:

• The combination of short and long EMAs is a widely trusted method for determining the trend direction. The crossovers between these EMAs provide clear entry signals for buy or sell trades. However, relying solely on EMAs can lead to false signals during periods of low volatility or market consolidation.

2. ATR for Volatility and Stop Loss:

• To prevent false signals during low-volatility conditions, the script uses ATR as a filter. This ensures that trades are only taken when the market has enough momentum, reducing the risk of being caught in “choppy” conditions where price action may be flat and untradeable.

• Additionally, the ATR-based trailing stop provides dynamic trade management, adjusting stop-loss levels according to the current volatility. This makes the system adaptive and prevents tight stops in volatile conditions or unnecessarily wide stops in calm markets.

3. Why They Work Together:

• The EMAs handle the trend direction, which is the foundation of the trading system, while the ATR adjusts the trade management to account for changing volatility. This means that the trader is always entering trades that are likely to follow a strong trend, while avoiding stagnant markets and using volatility-adaptive exit points.

• Without ATR, EMAs might generate signals during low-volatility periods that are unreliable. On the other hand, ATR alone wouldn’t provide a clear direction for trend-following. Together, these indicators create a balanced approach where trades are not only timely but also carefully managed.

How to Use:

• Buy Entry: Enter when the green triangle appears, indicating a bullish EMA crossover.

• Sell Entry: Enter short when the red triangle appears, indicating a bearish EMA crossover.

• Exit: Follow the orange background and blue “EXIT” label as a visual cue to exit the trade.

The combination of these tools allows traders to identify meaningful trend reversals while also managing risk dynamically, making the Arjunology for Stocks Indicator both versatile and effective for various market conditions.

Multi-Step FlexiSuperTrend - Indicator [presentTrading]This version of the indicator is built upon the foundation of a strategy version published earlier. However, this indicator version focuses on providing visual insights and alerts for traders, rather than executing trades. This one is mostly for @thorcmt.

█ Introduction and How it is Different

The **Multi-Step FlexiSuperTrend Indicator** is a versatile tool designed to provide traders with a highly customizable and flexible approach to trend analysis. Unlike traditional supertrend indicators, which focus on a single factor or threshold, the **FlexiSuperTrend** allows users to define multiple levels of take-profit targets and incorporate different trend normalization methods.

It comes with several advanced customization features, including multi-step take profits, deviation plotting, and trend normalization, making it suitable for both novice and expert traders.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The **Multi-Step FlexiSuperTrend** works by calculating a supertrend based on multiple factors and incorporating oscillations from trend deviations. Here’s a breakdown of how it functions:

🔶 SuperTrend Calculation

At the heart of the indicator is the SuperTrend formula, which dynamically adjusts based on price movements.

🔶 Normalization of Deviations

To enhance accuracy, the **FlexiSuperTrend** calculates multiple deviations from the trend and normalizes them.

🔶 Multi-Step Take Profit Levels

The indicator allows setting up to three take profit levels, which are displayed via price level alerts. lows traders to exit part of their position at various profit intervals.

For more detail, please check the strategy version - Multi-Step-FlexiSuperTrend-Strategy:

and 'FlexiSuperTrend-Strategy'

█ Trade Direction

The **Multi-Step FlexiSuperTrend Indicator** supports both long and short trade directions.

This flexibility allows traders to adapt to trending, volatile, or sideways markets.

█ Usage

To use the **FlexiSuperTrend Indicator**, traders can set up their preferences for the following key features:

- **Trading Direction**: Choose whether to focus on long, short, or both signals.

- **Indicator Source**: The price source to calculate the trend (e.g., close, hl2).

- **Indicator Length**: The number of periods to calculate the ATR and trend (the larger the value, the smoother the trend).

- **Starting and Increment Factor**: These adjust how reactive the trend is to price movements. The starting factor dictates how far the initial trend band is from the price, and the increment factor adjusts subsequent trend deviations.

The indicator then displays buy and sell signals on the chart, along with alerts for each take-profit level.

Local picture

█ Default Settings

The default settings of the **Multi-Step FlexiSuperTrend** are carefully designed to provide an optimal balance between sensitivity and accuracy. Let’s examine these default parameters and their effect on performance:

🔶 Indicator Length (Default: 10)

The **Indicator Length** determines the lookback period for the ATR calculation. A smaller value makes the indicator more reactive to price changes, but may generate more false signals. A longer length smooths the trend and reduces noise but may delay signals.

Effect on performance: Shorter lengths perform better in volatile markets, while longer lengths excel in trending markets.

🔶 Starting Factor (Default: 0.618)

This factor adjusts the starting distance of the SuperTrend from the current price. The smaller the starting factor, the closer the trend is to the price, making it more sensitive. Conversely, a larger factor allows more distance, reducing sensitivity but filtering out false signals.

Effect on performance: A smaller factor provides quicker signals but can lead to frequent false positives. A larger factor generates fewer but more reliable signals.

🔶 Increment Factor (Default: 0.382)

The **Increment Factor** controls how the trend bands adjust as the price moves. It increases the distance of the bands from the price with each iteration.

Effect on performance: A higher increment factor can result in wider stop-loss or trend reversal bands, allowing for longer trends to develop without frequent exits. A lower factor keeps the bands closer to the price and is more suited for shorter-term trades.

🔶 Take Profit Levels (Default: 2%, 8%, 18%)

The default take-profit levels are set at 2%, 8%, and 18%. These values represent the thresholds at which the trader can partially exit their positions. These multi-step levels are highly customizable depending on the trader’s risk tolerance and strategy.

Effect on performance: Lower take-profit levels (e.g., 2%) capture small, quick profits in volatile markets, while higher levels (8%-18%) allow for a more gradual exit in strong trends.

🔶 Normalization Method (Default: None)

The default normalization method is **None**, meaning the deviations are not normalized. However, enabling normalization (e.g., **Max-Min**) can improve the clarity of the indicator’s signals in volatile or choppy markets by smoothing out the noise.

Effect on performance: Using a normalization method can reduce the effect of extreme deviations, making signals more stable and less prone to false positives.

Uptrick: Market MoodsThe "Uptrick: Market Moods" indicator is an advanced technical analysis tool designed for the TradingView platform. It combines three powerful indicators—Relative Strength Index (RSI), Average True Range (ATR), and Bollinger Bands—into one cohesive framework, aimed at helping traders better understand and interpret market sentiment. By capturing shifts in the emotional climate of the market, it provides a holistic view of market conditions, which can range from calm to stressed or even highly excited. This multi-dimensional analysis tool stands apart from traditional single-indicator approaches by offering a more complete picture of market dynamics, making it a valuable resource for traders looking to anticipate and react to changes in market behavior.

The RSI in the "Uptrick: Market Moods" indicator is used to measure momentum. RSI is an essential component of many technical analysis strategies, and in this tool, it is used to identify potential market extremes. When RSI values are high, they indicate an overbought condition, meaning the market may be approaching a peak. Conversely, low RSI values suggest an oversold condition, signaling that the market could be nearing a bottom. These extremes provide crucial clues about shifts in market sentiment, helping traders gauge whether the current emotional state of the market is likely to result in a reversal. This understanding is pivotal in predicting whether the market is transitioning from calm to stressed or from excited to overbought.

The Average True Range adds another layer to this analysis by offering insights into market volatility. Volatility is a key factor in understanding the mood of the market, as periods of high volatility often reflect high levels of excitement or stress, while low volatility typically indicates a calm, steady market. ATR is calculated based on the range of price movements over a given period, and the higher the value, the more volatile the market is. The "Uptrick: Market Moods" indicator uses ATR to dynamically gauge volatility levels, helping traders understand whether the market is currently moving in a way that aligns with its emotional mood. For example, an increase in ATR accompanied by an RSI value that indicates overbought conditions could suggest that the market is in a highly excited state, with the potential for either strong momentum continuation or a sharp reversal.

Bollinger Bands complement these tools by providing visual cues about price volatility and the range within which the market is likely to move. Bollinger Bands plot two standard deviations away from a simple moving average of the price. This banding technique helps traders visualize how far the price is likely to deviate from its average over a certain period. The "Uptrick: Market Moods" indicator uses Bollinger Bands to establish price boundaries and identify breakout conditions. When prices break above the upper band or below the lower band, it often signals that the market is either highly stressed or excited. This breakout condition serves as a visual representation of the market mood, alerting traders to moments when prices are moving beyond typical ranges and when significant emotional shifts are occurring in the market.

Technically, the "Uptrick: Market Moods" indicator has been developed using TradingView’s Pine Script language, a highly efficient language for building custom indicators. It employs functions like ta.rsi, ta.atr, and ta.sma to perform the necessary calculations. The use of these built-in functions ensures that the calculations are both accurate and efficient, allowing the indicator to operate in real-time without lagging, even in volatile market conditions. The ta.rsi function is used to compute the Relative Strength Index, while ta.atr calculates the Average True Range, and ta.sma is used to smooth out price data for the Bollinger Bands. These functions are applied dynamically within the script, allowing the "Uptrick: Market Moods" indicator to respond to changes in market conditions in real time.

The user interface of the "Uptrick: Market Moods" indicator is designed to provide a visually intuitive experience. The market mood is color-coded on the chart, making it easy for traders to identify whether the market is calm, stressed, or excited at a glance. This feature is especially useful for traders who need to make quick decisions in fast-moving markets. Additionally, the indicator includes an interactive table that updates in real-time, showing the most recent mood state and its frequency. This provides valuable statistical insights into market behavior over specific time frames, helping traders track the dominant emotional state of the market. Whether the market is in a prolonged calm state or rapidly transitioning through moods, this real-time feedback offers actionable data that can help traders adjust their strategies accordingly.

The RSI component of the "Uptrick: Market Moods" indicator helps detect the speed and direction of price movements, offering insight into whether the market is approaching extreme conditions. By providing signals based on overbought and oversold levels, the RSI helps traders decide whether to enter or exit positions. The ATR element acts as a volatility gauge, dynamically adjusting traders’ expectations in response to changes in market volatility. Meanwhile, the Bollinger Bands help identify trends and potential breakout conditions, serving as an additional confirmation tool that highlights when the price has moved beyond normal boundaries, indicating heightened market excitement or stress.

Despite the robust capabilities of the "Uptrick: Market Moods" indicator, it does have limitations. In markets affected by sudden shifts, such as those driven by major news events or external economic factors, the indicator’s performance may not always be reliable. These external factors can cause rapid mood swings that are difficult for any technical analysis tool to fully anticipate. Additionally, the indicator’s complexity may pose a learning curve for novice traders, particularly those who are unfamiliar with the concepts of RSI, ATR, and Bollinger Bands. However, with practice, traders can become proficient in using the tool to its full potential, leveraging the insights it provides to better navigate market shifts.

For traders seeking a deeper understanding of market sentiment, the "Uptrick: Market Moods" indicator is an invaluable resource. It is recommended for those dealing with medium to high volatility instruments, where understanding emotional shifts can offer a strategic advantage. While it can be used on its own, integrating it with other forms of analysis, such as fundamental analysis and additional technical indicators, can enhance its effectiveness. By confirming signals with other tools, traders can reduce the likelihood of false signals and improve their overall trading strategy.

To further enhance the accuracy of the "Uptrick: Market Moods" indicator, it can be integrated with volume-based tools like Volume Profile or On-Balance Volume (OBV). This combination allows traders to confirm the moods identified by the indicator with volume data, providing additional confirmation of market sentiment. For example, when the market is in an excited mood, an increase in trading volume could reinforce the reliability of that signal. Conversely, if the market is stressed but volume remains low, traders may want to proceed with caution. Using multiple indicators together creates a more comprehensive trading approach, helping traders better manage risk and make informed decisions based on multiple data points.

In conclusion, the "Uptrick: Market Moods" indicator is a powerful and unique addition to the suite of technical analysis tools available on TradingView. It provides traders with a multi-dimensional view of market sentiment by combining the analytical strengths of RSI, ATR, and Bollinger Bands into a single tool. Its ability to capture and interpret the emotional mood of the market makes it an essential tool for traders seeking to gain an edge in understanding market behavior. While the indicator has certain limitations, particularly in rapidly shifting markets, its ability to provide real-time insights into market sentiment is a valuable asset for traders of all experience levels. Used in conjunction with other tools and sound trading practices, the "Uptrick: Market Moods" indicator offers a comprehensive solution for navigating the complexities of financial markets.

ATR Price Targets (Daily, Weekly, Monthly)This indicator calculates and displays dynamic price targets based on the Average True Range (ATR) for daily, weekly, and monthly timeframes. It’s designed to help traders set volatility-based price targets for more precise stop-losses, take-profit levels, and trade management.

Features:

Daily, Weekly, and Monthly ATR Targets: Automatically calculates and plots upper and lower price targets based on ATR values for each timeframe.

Risk Management Tool: Ideal for setting stop-loss and take-profit levels based on market volatility.

Customizable Settings: You can adjust the ATR length and multiplier to match your preferred trading style and risk tolerance.

Visual Alerts: Background colors change when price reaches or exceeds the calculated targets, providing easy visual cues for decision-making.

How to Use:

Use the upper and lower price targets to set realistic exit points for your trades.

Adjust the ATR multiplier for more or less conservative targets based on market volatility.

Apply this across multiple timeframes to combine long-term and short-term volatility trends.

This indicator is perfect for traders looking to incorporate volatility analysis into their trading strategy using ATR.

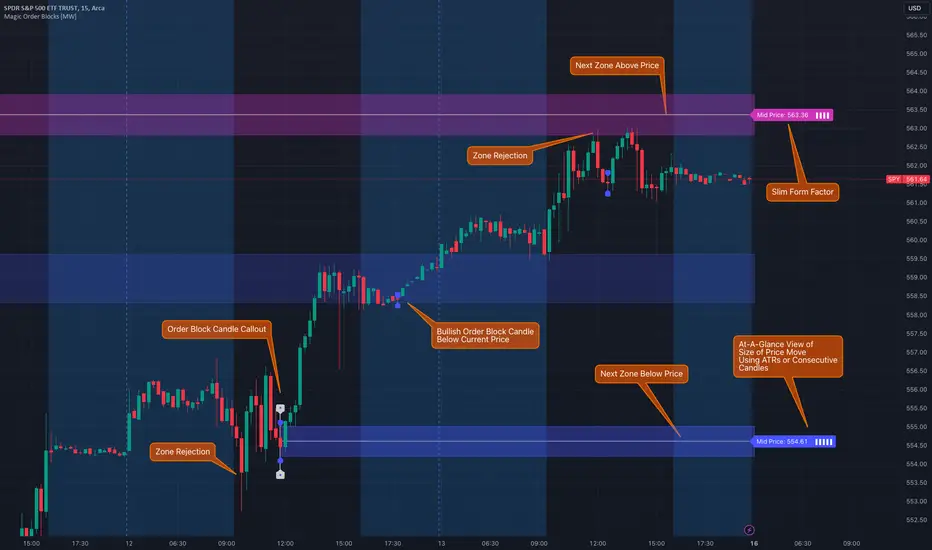

Magic Order Blocks [MW]Add a slim design, minimalist view of the most relevant higher and lower order blocks to your chart. Use our novel method of filtering that uses both the the number of consecutive bullish or bearish candles that follow the order block, and the number of ATRs that the asset’s price changed following the order block. View just the order blocks above and below the current price, or view the backgrounds for each and every one. And, if you're up to it, dig into a comprehensive view of the data for each order block candle.

Settings:

General Settings

Minimum # of Consecutive Bars Following Order Block

Show Bullish Order Blocks Below / Hide Last Bullish Block

Show Bearish Order Blocks Above / Hide Last Bearish Block

Use ATR Filter - Select # of ATRs Below

Closest Order Block is Followed by This Many ATRs

Preferences

Right Offset of Indicator Label

Show Mid-Line from Recent Order Block Indicator Label

Use ATRs Instead of Consecutive Candles in Label Indicator

Show Timestamp of Recent Order Block

Show Large Order Block Detail Labels

Show Small Order Block Labels

Background Settings

Show Background for Recent Order Block Indicator Label

# of Backgrounds to Show Before Now

Show All Bullish Order Block Backgrounds

Show All Bearish Order Block Backgrounds

Calculations

This indicator creates a matrix of each order block that is followed by the user-specified number of consecutive bullish or bearish candles. The data can be further filtered by the number of ATRs that the price moves after the order block - also user-defined. The most recent bearish order block above the current price takes arrays from the initial filtered matrix of arrays, filters once more by the “mid-price” of the order block (the average between the order block candle high and low) and selects the last element from this order block matrix. The same follows for the latest bearish order block above the current price.

How to Use

An order block refers to a price range or zone on a chart where large institutional orders have been placed, causing a significant shift in market direction. These zones are crucial because they often indicate areas of strong buying or selling interest, which can lead to future support or resistance levels. Traders use order blocks to identify potential points of market reversal or continuation.

The Magic Order Blocks default view shows the most recent overhead bearish order block above the current price, and the most recent bullish order block below. These can presumably act as support or resistance levels, because they reflect the last price where a significant price move occurred. “Significant” meaning that the order block candle was followed by many consecutive bullish or bearish candles. Based on the user-defined settings, it can also mean that price moved multiples of the asset's average true range (ATR). More consecutive candles means that the duration of the move lasted a long time. A higher ATR move indicates that the price moved impulsively in one direction.

The default view also shows a label to the right of the current price that provides the price level, the time stamp of the order block (optional), and a sequence of bars that show the significance of the level. By default, these bars represent the number of ATRs that price rose or fell following the order block, but they can be toggled to show the number of consecutive bullish or bearish candles that followed the order block.

Although the default view provides the zones that are most relevant to the current price, past order block candles can also be identified visually with labels as well with translucent backgrounds color-coded for bullish or bearish bias. Overlapping backgrounds can identify an area that has been repeatedly been an area of support or resistance.

A detailed view of each order block can also be viewed the includes the following data points:

Bar Index

Timestamp

Consecutive Accumulated Volume

Consecutive Bars

Price Change over Consecutive Bars

Price/Volume Ratio Over Consecutive Bars

Mid Price of Order Block

High Price of Order Block

Low Price of Order Block

ATRs over Consecutive Bars

- Other Usage Notes and Limitations:

The calculations used only provide an estimated relationship or a close approximation, and are not exact.

It's important for traders to be aware of the limitations of any indicator and to use them as part of a broader, well-rounded trading strategy that includes risk management, fundamental analysis, and other tools that can help with reducing false signals, determining trend direction, and providing additional confirmation for a trade decision. Diversifying strategies and not relying solely on one type of indicator or analysis can help mitigate some of these risks.

Things to keep in mind. Longer timeframes don’t necessarily have a as many consecutive candle drops or gains as with shorter timeframes, so be sure to adjust your settings when moving to 1 hour, 1 day, or 1 week timeframes from 1 minute, 5 minute, or 15 minute timeframes.

Average True Range with Price MAATR with Price Moving Average Indicator

This custom indicator combines the Average True Range (ATR) with a Price Moving Average (MA) to help traders analyze market volatility in percent to the price.

Key Components:

Average True Range (ATR)

Price Moving Average (MA)

ATR/Price in Percent

ATR/Price in Percent

Purpose: This ratio helps traders understand the relative size of the ATR compared to the current price, providing a clearer sense of how significant the volatility is in proportion to the price level.

Calculation: ATR is divided by the current closing price and multiplied by 100 to express it as a percentage. This makes it easier to compare volatility across assets with different price ranges.

Plot: This is plotted as a percentage, making it easier to gauge whether the volatility is proportionally high or low compared to the asset's price.

Usage:

This indicator is designed to help identify the most volatile tokens, making it ideal for configuring a Grid Bot to maximize profit. By focusing on high-volatility assets, traders can capitalize on larger price swings within the grid, increasing the potential for more profitable trades.

Features:

Customizable Smoothing Method: Choose from RMA (Relative Moving Average), SMA (Simple Moving Average), EMA (Exponential Moving Average), or WMA (Weighted Moving Average) for both ATR and the Price Moving Average.

Dual Perspective: The indicator provides both volatility analysis (ATR) and trend analysis (Price MA) in a single view.

Proportional Volatility: The ATR/Price (%) ratio adds a layer of context by showing how volatile the asset is relative to its current price.

Bidirectional Trend Reversal StrategyBidirectional Trend Reversal Strategy

This strategy aims to identify potential trend reversals and execute trades accordingly, focusing on both long and short positions. It uses a crossover of the Simple Moving Average (SMA) with price action as a key signal. When the price crosses above the SMA and the previous period was bearish (closed lower than it opened), the script opens a long position ("o-Long"). The exit ("e-Long") occurs when the target or stop-loss levels are hit, which are dynamically set using the ATR (Average True Range).

For short trades, when the price crosses below the SMA and the previous period was bullish (closed higher than it opened), the script opens a short position ("o-Short"). The exit ("e-Short") follows the same ATR-based logic for stop-loss and take-profit.

All settings, including SMA and ATR parameters, are fully customizable, allowing users to adapt the strategy to different market conditions and personal trading preferences.

This approach provides a systematic way to capture trend reversals and manage trades with clear entry and exit signals based on market momentum and volatility.

Example Setup:

Market: Forex

Pair: USD/GBP

Order size: 100,000 Contracts (1 Lot)

Timeframe: 15 minutes

SMA: 93

ATR Length: 15

Stop-Loss (ATR Multiplier): 7

Take-Profit Multiplier: 2

Experiment with different settings to achieve the best results for your trading style and market conditions.

[DarkTrader] Strong High LowThe Strong High Low indicator calculates strong high and low pivots based on price action and the Average True Range (ATR). The calculation for both the high and low pivots involves analyzing recent candle behavior to identify significant levels where price reversal is likely. Specifically, it looks for consecutive bearish or bullish candles to determine whether a strong high or low has been established.

Indicator In Use :

For strong highs, the indicator checks if three consecutive candles are bearish, meaning their closing price is lower than their opening price. It further examines prior candles to confirm that they followed a specific pattern where a reversal could occur. If one of these earlier candles closed higher than it opened, the indicator assumes that this was a strong high, and it records either the high of the second or third candle from the pattern, depending on their relationship to each other.

Similarly, for strong lows, the indicator searches for three consecutive bullish candles where the close is higher than the open. The algorithm then reviews prior candles in the sequence to ensure that the market condition supports a potential low pivot. If an earlier candle closes lower than it opens, it marks this as a strong low. The final low point for the pivot is chosen based on a comparison between the second and third candles of the pattern.

Once the high and low pivots are determined, the indicator adjusts these levels using the ATR value. The ATR is added to the strong high pivot and subtracted from the strong low pivot to create slightly modified levels. This helps accommodate market volatility by widening the range of the high and low pivots, making the levels more reliable in reflecting potential reversal zones.

Finally, the strong high and low pivot lines are drawn on the chart, extending both to the left and right of the current price, based on the user-defined offset values. These lines give a visual cue of where key resistance and support levels exist, with labels marking the exact pivot values for easy reference.

Super Trend ReversalsMain Concept

The core idea behind the Super Trend Reversals indicator is to assess the momentum of automated trading bots (often referred to as 'Supertrend bots') that enter the market during critical turning points. Specifically, the indicator is tuned to identify when the market is nearing bottoms or peaks, but just before it shifts direction based on the triggered Supertrend signals. This approach helps traders engage with the market right as the reversal momentum builds up, allowing for entry just as conditions become favorable and exit before momentum wanes.

How It Works

The Super Trend Reversals uses multiple Supertrend calculations, each with different period and multiplier settings, to form a comprehensive view of the trend. The total trend score from these calculations is then analyzed using the Relative Strength Index (RSI) and Exponential Moving Averages (EMA) to gauge the strength and sustainability of the trend.

A key feature of this indicator is the isCurrentRangeSmaller() function, which evaluates if the current price range is lower than the average over the recent period. This function is critical as it helps determine the stability of the market environment, reducing the likelihood of entering or exiting trades based on erratic price movements that could lead to false signals.

ATR+Order Block IndicatorThe ATR+Order Block Indicator is a unique and comprehensive tool designed to combine volatility-based analysis with key price action levels to provide traders with reliable entry and exit points. This indicator merges the Average True Range (ATR) for dynamic trailing stop calculation with order block detection to identify significant support and resistance zones on the chart. This combination offers traders a powerful blend of trend-following and price level analysis for improved trading decisions.

How the Components Work Together:

1. ATR-Based Trailing Stop:

• The Average True Range (ATR) is a widely used volatility indicator that measures the degree of price movement over a specified period. In this indicator, the ATR is used to create a trailing stop that dynamically adjusts to market conditions.

• How It Works: The ATR value is multiplied by a user-defined multiplier (ATR Multiplier) to set the distance of the trailing stop from the current price. This trailing stop moves with the price:

• If the price moves upwards, the trailing stop adjusts higher, ensuring it only moves in the direction of the trade.

• If the price moves downwards, the trailing stop adjusts lower accordingly.

• Purpose: This trailing stop helps traders manage risk by automatically adjusting to market volatility, ensuring that stops are not too tight in volatile conditions or too wide in quieter markets. It also helps lock in profits while maintaining a position in the market’s direction.

2. Order Block Detection:

• Order blocks are areas on the chart where significant buying (accumulation) or selling (distribution) has occurred. These zones often act as potential support or resistance levels due to the presence of unfilled buy or sell orders by large institutions or traders.

• How It Works: The indicator identifies the highest high (seller order block) and the lowest low (buyer order block) within a user-defined lookback period. These are plotted on the chart:

• Buyer Order Block: Represents a potential support area where buying interest is likely to reappear.

• Seller Order Block: Represents a potential resistance area where selling interest may reemerge.

• Purpose: By identifying these order blocks, traders can anticipate potential price reversals or continuations, aligning their trades with key market levels where significant buying or selling has occurred.

Justification for Combining These Components:

1. Enhanced Signal Accuracy and Context:

• The combination of ATR-based trailing stops with order block detection provides a dual-layered approach to trade decisions:

• ATR Trailing Stop offers trend-following signals based on volatility, helping traders capture market momentum.

• Order Blocks provide context to these signals by highlighting critical price levels where market participants have previously shown strong interest.

• This fusion allows traders to filter signals more effectively, ensuring trades are aligned with both market trends and key support/resistance zones.

2. Dynamic Risk Management:

• Using the ATR to set a dynamic trailing stop ensures that the stop-loss level adapts to the changing volatility of the market. When combined with order block detection, traders gain an additional layer of risk management:

• Stop Loss Placement: Traders can place stops just outside identified order blocks to protect against sudden price reversals while maintaining a tight stop aligned with current market volatility.

3. Reducing Market Noise and Avoiding False Signals:

• The indicator includes a mechanism to avoid repetitive signals, requiring a minimum gap between signals. This reduces noise and helps traders avoid multiple false entries in choppy market conditions.

• Order Blocks provide additional validation: For example, a buy signal generated near a Buyer Order Block carries more weight, as it aligns both with the ATR-based momentum and a key support area.

4. Improving Entry and Exit Strategies:

• Entry Points: The indicator generates buy (long) signals when the price crosses above the ATR trailing stop and sell (short) signals when it crosses below. These signals are enhanced by considering their proximity to order blocks, ensuring trades are initiated at strategic price levels.

• Exit Points: The ATR trailing stop provides a dynamic exit strategy, allowing trades to run while adjusting to market volatility. Traders can also use order blocks as targets or potential reversal points to exit trades.

5. Providing a Comprehensive Trading Tool:

• This indicator is unique in its integration of volatility and price level analysis, offering a well-rounded approach to trading. It combines the best of both worlds: trend-following momentum with the ATR and price action sensitivity through order blocks, making it suitable for different market conditions and trading styles.

How to Use the Indicator:

• Set the Parameters:

• Choose an ATR Period (default is 10) to define the number of bars for ATR calculation.

• Set the ATR Multiplier (default is 1.5) to adjust the sensitivity of the trailing stop.

• Define the Order Block Lookback Period (default is 20) to determine how many bars back the script will search for order blocks. Recommended 50.

• Interpret the Signals:

• BUY Signal: When the price crosses above the ATR trailing stop, indicating upward momentum. Confirm this signal by checking if it is near a Buyer Order Block.

• SELL Signal: When the price crosses below the ATR trailing stop, indicating downward momentum. Look for proximity to a Seller Order Block for added confidence.

• Monitor and Manage Trades:

• Use the ATR trailing stop for dynamic stop-loss placement.

• Watch for price action around the order blocks to make informed decisions about taking profits or cutting losses.

Conclusion:

The ATR+Order Block Indicator combines volatility and price action analysis in a unique way that offers traders a comprehensive tool for making informed trading decisions. By leveraging the strengths of both ATR-based dynamic stops and order block detection, it provides a balanced approach to trend-following and support/resistance trading, enhancing overall trading effectiveness and confidence.

Kijun_ATROVERVIEW

Kijun + ATR is an indicator that combines Lagging Kijun Base Line From Ichimoku Cloud (direction indicator) and Volatility Indicator ATR.

By combining ATR with kijun we can filter out noise from Base Line.

CALCULATIONS

Kijun is calculated by taking average of lowest and highest point of price over set lenght.

ATR is just default Tradingview Indicator that calculates average true range of price over set period of time.

WORKING

When both close > lower and not close < upper are true indicator indicate long by color limeand indicates short when close < upper by color fuchsia (Color can be changed in settings)

Indicator works best in Trending Market Regimes can have problems by signaling tops in Consolidating Market Regimes during bear markets and by sygnaling bottom in short consolidating market regimes during bull market.

Dema AFR | viResearchDema AFR | viResearch

Conceptual Foundation and Innovation

The "Dema AFR" indicator combines the Double Exponential Moving Average (DEMA) with an Average True Range (ATR)-based adaptive factor to create a responsive and adaptable trend-following system. The DEMA is known for its ability to smooth price data while reducing lag, making it highly effective for trend detection. By incorporating the ATR as a volatility factor, this indicator adapts dynamically to market conditions, allowing traders to capture trends while accounting for changes in volatility. The result is the Adaptive Factor Range (AFR), which provides clear signals for potential trend shifts and helps manage risk through its adaptive nature. This combination of DEMA smoothing and an ATR-based factor enables traders to follow trends more effectively while maintaining sensitivity to changing market conditions.

Technical Composition and Calculation

The "Dema AFR" script consists of two main components: the Double Exponential Moving Average (DEMA) and the Adaptive Factor Range (AFR). The DEMA is calculated over a user-defined length, smoothing out price fluctuations while reducing lag compared to traditional moving averages. The ATR is used to create a dynamic factor that adjusts the AFR based on market volatility. The factor is calculated by multiplying the ATR by a user-defined factor value, which scales the ATR to define upper and lower bounds for the AFR. The Adaptive Factor Range is derived from the DEMA, with upper and lower bounds set by adding or subtracting the ATR-based factor from the DEMA. When the price moves outside these bounds, the AFR is adjusted, and signals are generated. If the lower bound is exceeded, the AFR adjusts upward, while exceeding the upper bound causes the AFR to adjust downward. This dynamic adjustment helps the indicator stay responsive to market movements.

Features and User Inputs

The "Dema AFR" script provides several customizable inputs, allowing traders to tailor the indicator to their strategies. The DEMA Length controls the smoothing period for the DEMA, while the ATR Period defines the window for calculating the Average True Range. The ATR Factor determines the scale of the adaptive factor, controlling how much the AFR adjusts to volatility. Additionally, customizable bar colors and alert conditions allow traders to visualize the trend direction and receive notifications when key trend shifts occur.

Practical Applications

The "Dema AFR" indicator is designed for traders who want to capture trends while adapting to market volatility. The adaptive nature of the AFR makes it responsive to trend changes, providing early signals of potential trend reversals as the AFR adjusts to market movements. By incorporating ATR into the AFR calculation, the indicator adjusts to changing volatility, helping traders manage risk by staying aligned with market conditions. The AFR also helps confirm whether a price move is supported by momentum, improving the accuracy of trade entries and exits.

Advantages and Strategic Value

The "Dema AFR" script offers a significant advantage by combining the smoothness of the DEMA with the adaptability of the ATR-based factor. This dynamic combination allows the indicator to adjust to market conditions, providing more reliable trend signals in both trending and volatile markets. The adaptive nature of the AFR reduces the risk of false signals and helps traders stay on the right side of the trend while managing risk through volatility-adjusted ranges.

Alerts and Visual Cues

The script includes alert conditions that notify traders of key trend changes. The "Dema AFR Long" alert is triggered when the AFR indicates a potential upward trend, while the "Dema AFR Short" alert signals a potential downward trend. Visual cues such as color changes in the bar chart help traders quickly identify shifts in trend direction, allowing them to make informed decisions in real time.

Summary and Usage Tips

The "Dema AFR | viResearch" indicator provides traders with a powerful tool for trend analysis by combining DEMA smoothing with an ATR-based adaptive factor. This script helps traders stay aligned with trends while accounting for market volatility, improving their ability to detect trend reversals and manage risk. By incorporating this indicator into your trading strategy, you can make more informed decisions, whether in trending or volatile market environments. The "Dema AFR" offers a reliable and flexible solution for traders at all levels.

Note: Backtests are based on past results and are not indicative of future performance.

Trailing Stop ProTrailing Stop Pro is a sophisticated TradingView indicator designed to enhance your trading strategy by dynamically managing trailing stops based on market volatility. This tool leverages the Average True Range (ATR) to adjust stop levels, providing traders with a robust mechanism to protect profits and minimize losses.

Key Features:

Dynamic Trailing Stops: Automatically adjusts stop levels using ATR, allowing for responsive and adaptive risk management.

Customizable Inputs: Tailor the indicator to your trading style with adjustable parameters such as ATR Length, ATR Multiplier, and Source Vector.

Visual Clarity: Distinct color settings for long and short stops, with adjustable line thickness and transparency, ensuring clear visualization on your charts.

Professional Grade: The "Pro" designation signifies advanced features suitable for both novice and experienced traders seeking reliable and efficient stop management.

How It Works:

To set up the indicator, begin by defining the Chrono Point, which specifies the exact time you want the trailing stop mechanism to activate. This allows for precise control over when your stops begin to trail. Next, set the Credit Unit as the initial entry price for your trade, serving as the baseline from which the trailing stops will adjust.

The indicator uses ATR-based adjustments to determine stop levels. Customize the sensitivity of the trailing stop by adjusting the ATR Length (default is 14) and ATR Multiplier (default is 0.5). A longer ATR length smooths out volatility, while a higher multiplier increases the distance of the stop from the price.

Select your Source Vector from "High/Low," "Close," or "Open" prices as the basis for stop calculation. This flexibility allows you to align the indicator with your preferred trading strategy. The indicator plots trailing stops directly on the chart, with color-coded lines indicating long (teal) and short (red) positions. You can adjust the line thickness and transparency for optimal visibility.

The Mission Status feature automatically detects whether the trade is long or short and adjusts the trailing stop accordingly. If the price hits the trailing stop, the trade is considered exited, and the indicator calculates the profit or loss percentage.

Benefits:

Risk Management: Protect your trades from adverse market movements while locking in profits as prices move favorably.

Automation: Reduce manual intervention with automatic stop adjustments, allowing you to focus on strategic decision-making.

User-Friendly Interface: Intuitive settings and clear visual cues make it easy to integrate into your existing trading workflow.

Conclusion:

Trailing Stop Pro is an essential tool for traders looking to enhance their risk management strategies with precision and ease. By automating the trailing stop process and providing clear visual feedback, this indicator empowers you to navigate the markets with confidence. Whether you're a seasoned trader or just starting, Trailing Stop Pro offers the functionality and flexibility needed to optimize your trading performance.

The Trailing Stop Pro indicator is a tool designed to assist traders in managing risk and optimizing their trading strategies. However, it should not be considered as financial advice or a guarantee of profitability. Trading involves significant risk, and it is possible to lose more than your initial investment. Users are encouraged to thoroughly test the indicator in a demo environment and consider their own financial situation and risk tolerance before using it in live trading. Past performance is not indicative of future results, and users should seek advice from a qualified financial advisor if needed.

DataDoodles ATR RangeThe "DataDoodles ATR Range" indicator provides a comprehensive visual representation of the Average True Range (ATR) levels based on the previous bar's close price . It includes both the raw ATR and an Exponential Moving Average (EMA) of the ATR to offer a smoother view of the range volatility. This indicator is ideal for traders who want to quickly assess potential price movements relative to recent volatility.

Key Features:

ATR Levels Above and Below Close: The indicator calculates and displays three levels of ATR-based ranges above and below the previous close price. These levels are visualized on the chart using distinct colors:

- 1ATR Above/Below

- 2ATR Above/Below

- 3ATR Above/Below

EMA of ATR

Includes the EMA of ATR to provide a smoother trend of the ATR values, helping traders identify long-term volatility trends.

Color-Coded Ranges: The plotted ranges are color-coded for easy identification, with warm gradient tones applied to the corresponding data table for quick reference.

Customizable Table: A data table is displayed at the bottom right corner of the chart, providing real-time values for ATR, EMA ATR, and the various ATR ranges.

Usage

This indicator is useful for traders who rely on volatility analysis to set stop losses, take profit levels, or simply understand the current market conditions. By visualizing ATR ranges directly on the chart, traders can better anticipate potential price movements and adjust their strategies accordingly.

Customization

ATR Length: The default ATR length is set to 14 but can be customized to fit your trading strategy.

Table Positioning: The data table is placed in the bottom right corner by default but can be moved as needed.

How to Use

Add the "DataDoodles ATR Range" indicator to your chart.

Observe the plotted lines for potential support and resistance levels based on recent volatility.

Use the data table for quick reference to ATR values and range levels.

Disclaimer: This indicator is a tool for analysis and should be used in conjunction with other indicators and analysis methods. Always practice proper risk management and consider market conditions before making trading decisions.

Displacement [QuantVue]Displacement refers to a significant and forceful price movement that indicates a potential shift in market sentiment or trend. Displacement is characterized by a strong push in price action, often seen after a period of consolidation or within a trending market. It is a key concept used to identify the strength of a move and to confirm the direction of the market.

The "Displacement" indicator does this by focusing on identifying strong, directional price movements by combining candlestick analysis with volatility (ATR).

Displacement often appears as a group of candles that are all positioned in the same direction, these candles typically have large bodies and short wicks.

How the indicator works:

Body Size Requirement: Ensures that only candles with a significant body size (relative to their total range) are considered, helping to identify strong market moves.

Consecutive Candle Analysis: Identifies shifts in market sentiment by requiring a series of consecutive bullish or bearish candles to confirm a potential change in trend.

ATR-Based Analysis: Uses the Average True Range (ATR) to gauge market volatility and filter out minor price fluctuations, focusing on substantial movements.

Once all of the requirements are met a triangle is plotted above or below the bar.