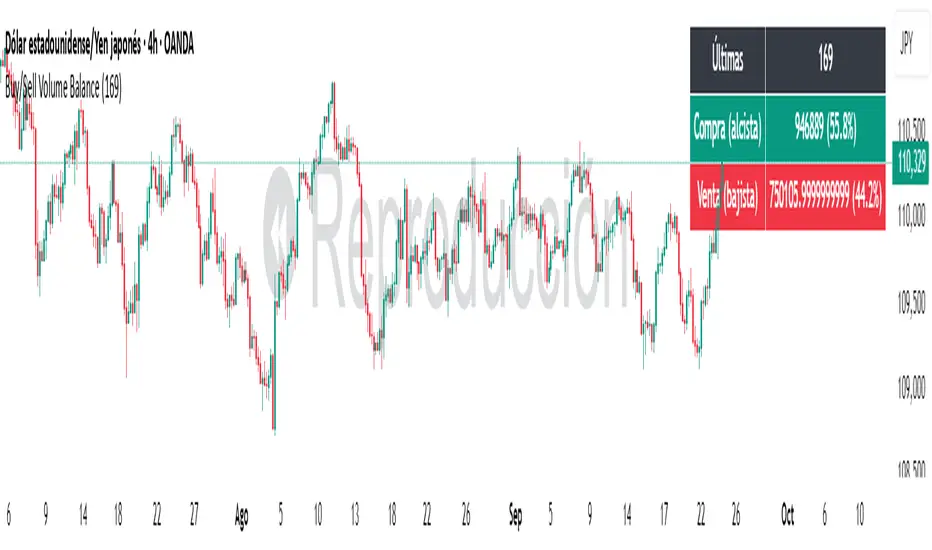

Buy/Sell Volume BalanceDESCRIPTION

Buy/Sell Volume Balance is a simple yet powerful indicator designed to measure and visualize the balance between buying and selling volume over a customizable number of recent candles. It helps traders quickly assess market pressure during consolidation phases or ranges, in order to anticipate the most likely breakout direction.

How it works

The indicator analyzes the last N candles (default = 100, user-editable).

Each candle’s total volume is classified as:

Bullish volume (Buy volume): if the candle closes above or equal to its open.

Bearish volume (Sell volume): if the candle closes below its open.

The volumes are summed separately to calculate:

Total Buy Volume

Total Sell Volume

The percentage of each side relative to the total is also displayed.

All results are shown in a fixed table at the top of the chart for quick interpretation.

Purpose

This tool is specifically designed to help traders evaluate the internal battle between buyers and sellers during a range or sideways market. By understanding which side is accumulating more volume within the range, traders can anticipate which direction is more likely when the price breaks out.

If Buy volume dominates → potential bullish breakout.

If Sell volume dominates → potential bearish breakout.

If both sides are nearly balanced, it signals indecision and a higher chance of false breakouts.

Imbalance Threshold

In practice, traders often consider a clear imbalance when one side reaches at least 55–60% of the total volume.

Above this threshold, the dominant side is more likely to dictate the breakout direction.

Below this threshold, the market is usually in indecision and further confirmation is needed before acting.

How to use it

Add the indicator to your chart and choose the lookback period (number of candles).

Focus on ranges or consolidation zones where price is moving sideways.

Observe the balance of Buy vs Sell volume in the top-right box:

A clear imbalance (>55–60%) suggests the stronger side is more likely to push the breakout.

A balanced ratio (<55–60%) indicates indecision and possible false breakouts.

Use it in combination with support/resistance zones, breakout patterns, or volume spikes for best results.

✅ In summary: This indicator does not give direct buy/sell signals, but it provides valuable context about market pressure, helping you to align your trades with the most probable breakout direction.

Cicli

Sinusoidal Cycles OscillatorTitle: Sinusoidal Cycles Oscillator – Multi-Cycle Market Indicator

Description:

Discover market rhythm with the Sinusoidal Cycles Oscillator, a powerful tool for technical analysis and cyclical trading.

Three customizable cycles track short, medium, and long-term market oscillations.

Cycle 1 serves as the main reference wave with an optional mirror envelope.

Cycles 2 & 3 provide supporting harmonics for deeper insight.

Composite wave averages all cycles to reveal overall market phase.

Features:

Fully adjustable periods and amplitude.

Visualize tops, bottoms, and turning points at a glance.

Oscillator ranges from -1 to +1 with clear threshold guides.

Ideal for traders using cycle analysis, harmonic trading, or market timing.

Easy-to-read visual overlay and separate panel option.

Use it to:

Identify potential price reversals.

Compare market cycles across multiple timeframes.

Enhance timing and entry/exit decisions.

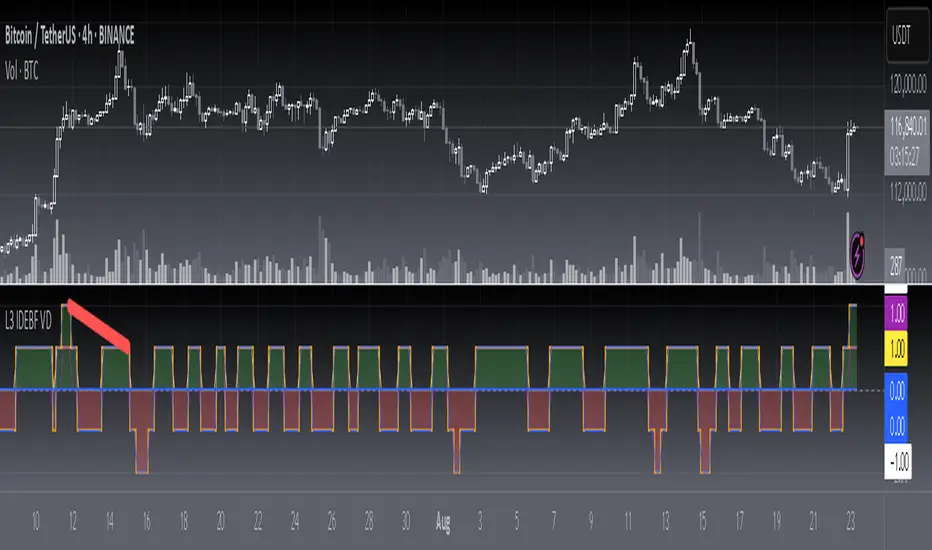

[blackcat] L3 Improved Dual Ehlers BPF for Volatility DetectionOVERVIEW

This script implements an advanced L3 Improved Dual Ehlers Bandpass Filter (BPF) for volatility detection, combining both L1 and L2 calculation methods to create a comprehensive trading signal. The script leverages John Ehlers' sophisticated digital signal processing techniques to identify market cycles and extract meaningful trading signals from price action. By combining multiple cycle detection methods and filtering approaches, it provides traders with a powerful tool for identifying trend changes, momentum shifts, and potential reversal points across various market conditions and timeframes. The L3 approach uniquely combines the outputs of both L1 (01 range) and L2 (-11 range) methods, creating a signal that ranges from -1~2 and provides enhanced sensitivity to market dynamics.

FEATURES

🔄 Dual Calculation Methods: Choose between L1 (01 range), L2 (-11 range), or combine both for L3 signal (-1~2 range) to match your trading style

📊 Multiple Cycle Detection: Seven different dominant cycle calculation methods including HoDyDC (Hilbert Transform Dominant Cycle), PhAcDC (Phase Accumulation Dominant Cycle), DuDiDC (Duane Dominant Cycle), CycPer (Cycle Period), BPZC (Bandpass Zero Crossing), AutoPer (Autocorrelation Period), and DFTDC (Discrete Fourier Transform Dominant Cycle)

🎛️ Flexible Mixing Options: Six sophisticated mixing methods including weighted averaging, simple sum, difference extraction, dominant-only, subdominant-only, and adaptive mixing that adjusts based on signal strength

🌊 Bandpass Filtering: Precise bandwidth control for both dominant and subdominant filters, allowing fine-tuning of frequency response characteristics

📈 Advanced Divergence Detection: Robust algorithm for identifying bullish and bearish divergences with customizable lookback periods and range constraints

🎨 Comprehensive Visualization: Extensive customization options for all signals, colors, plot styles, and display elements

🔔 Comprehensive Alert System: Built-in alerts for divergence signals, zero line crosses, and various market conditions

📊 Real-time Cycle Information: Optional display of dominant and subdominant cycle periods for educational purposes

🔄 Adaptive Signal Processing: Dynamic adjustment of parameters based on market conditions and volatility

🎯 Multiple Signal Outputs: Simultaneous generation of L1, L2, and L3 signals for different trading strategies

HOW TO USE

Select Calculation Method: Choose between "l1" (01 range), "l2" (-11 range), or "both" (L3, -1~2 range) in the Calculation Method settings based on your preferred signal characteristics

Configure Cycle Detection: Select your preferred Dominant Cycle Method from the seven available options and adjust the Cycle Part parameter (0.1-0.9) to fine-tune cycle sensitivity

Set Subdominant Parameters: Configure the subdominant cycle either as a ratio of the dominant cycle or as a fixed period, depending on your analysis approach

Adjust Filter Bandwidth: Fine-tune the bandwidth settings for both dominant and subdominant filters (0.1-1.0) to control the frequency response and signal smoothing

Choose Mixing Method: Select how to combine the filters - weighted averaging for balance, sum for maximum sensitivity, difference for trend isolation, or adaptive mixing for dynamic response

Configure Smoothing: Select from SMA, EMA, or HMA smoothing methods with adjustable length (1-20 bars) to reduce noise in the final signal

Customize Visualization: Enable/disable individual plots, divergence detection, zero line, fill areas, and customize all colors to match your chart preferences

Set Divergence Parameters: Configure lookback ranges (5-60 bars) for divergence detection to match your trading timeframe and style

Monitor Signals: Watch for crosses above/below zero line and divergence patterns, paying attention to signal strength and consistency

Set Up Alerts: Configure alerts for divergence signals, zero line crosses, and other market conditions to stay informed of trading opportunities

LIMITATIONS

The script requires the dc_ta library from blackcat1402 for several advanced cycle calculation methods (HoDyDC, PhAcDC, DuDiDC, CycPer, BPZC, AutoPer, DFTDC)

L1 method operates in 01 range while L2 method uses -11 range, requiring different interpretation approaches

Combined L3 signal ranges from -1~2 when both methods are selected, creating unique signal characteristics that traders must adapt to

Divergence detection accuracy depends on proper lookback period settings and market volatility conditions

Performance may be impacted with very long lookback ranges (>60 bars) or when multiple plots are simultaneously enabled

The script is designed for non-overlay use and may not display correctly on certain chart types or with conflicting indicators

Adaptive mixing method requires careful threshold tuning to avoid excessive signal fluctuation

Cycle detection algorithms may produce unreliable results during low volatility or highly choppy market conditions

The script assumes regular price data and may not perform optimally with irregular or gapped price sequences

NOTES

The script implements advanced mathematical calculations including bandpass filters, Hilbert transforms, and various cycle detection algorithms developed by John Ehlers

For optimal results, experiment with different cycle detection methods and bandwidth settings across various market conditions and timeframes

The adaptive mixing method automatically adjusts weights based on signal strength, providing dynamic response to changing market conditions

Divergence detection works best when the "Plot Divergence" option is enabled and when combined with other technical analysis tools

Zero line crosses can indicate potential trend changes or momentum shifts, especially when confirmed by volume or other indicators

The script includes commented code for cycle information display that can be enabled if you want to monitor cycle periods in real-time

Different calculation methods may perform better in different market environments - L1 tends to be smoother while L2 is more sensitive

The subdominant cycle helps filter out noise and provides additional confirmation for signals generated by the dominant cycle

Bandwidth settings control the filter's frequency response - lower values provide more smoothing while higher values increase sensitivity

Mixing methods offer different approaches to combining signals - weighted averaging is generally most reliable for most trading applications

THANKS

Special thanks to John Ehlers for his pioneering work in cycle analysis and digital signal processing for financial markets. This script implements and significantly improves upon his bandpass filter methodology, incorporating multiple advanced techniques from his extensive body of work. Also heartfelt thanks to blackcat1402 for the dc_ta library that provides essential cycle calculation methods and for maintaining such a valuable resource for the Pine Script community. Additional appreciation to the TradingView platform for providing the tools and environment that make sophisticated technical analysis accessible to traders worldwide. This script represents a collaborative effort in advancing the field of algorithmic trading and technical analysis.

Jackson Hole Meetings - Lines and LabelsThis TradingView Pine Script indicator marks the dates of the Federal Reserve’s annual Jackson Hole Economic Symposium meetings on your chart. For each meeting date from 2020 through 2025, it draws a red dashed vertical line directly on the corresponding daily bar. Additionally, it places a label above the bar indicating the year of the meeting (e.g., "JH 2025").

Features:

Marks all known Jackson Hole meeting dates from 2020 to 2025.

Draws a vertical dashed line on each meeting day for clear visual identification.

Displays a label above the candle with the meeting year.

Works best on daily timeframe charts.

Helps traders quickly spot potential market-moving events related to Jackson Hole meetings.

Use this tool to visually correlate price action with these key Federal Reserve events and enhance your trading analysis.

FVG Zones – shrink on fill (bull/bear)Detects classic 3-candle FVGs (ICT definition).

Draws zones as boxes that extend to the right.

On each bar close:

Checks overlap with the current candle.

Shrinks the zone when price wicks into it (bullish: top moves down; bearish: bottom moves up).

Deletes the zone once it’s completely filled/closed.

Inputs: bullish/bearish zone color, border color, and max number of visible FVGs.

Possible extensions:

Multi-timeframe FVGs (e.g. H1 FVGs shown on M5).

Separate limits for bullish and bearish zones.

Alerts for new FVG, partial fill, or closed FVG.

Option “Body only” (ignore wicks when detecting overlap).

Minimum FVG size filter (ticks/ATR).

Liquidity-Weighted Business Cycle (Satoshi Global Base)🌍 BTC-Affinity Global Liquidity Business Cycle (MACD Model)

This indicator models Bitcoin’s macroeconomic business cycle using a BTC-weighted global liquidity index as its foundation. It adapts a MACD-based framework to visualize expansions and contractions in fiat liquidity across major economies with high Bitcoin affinity.

🔍 What It Does:

🧠 Constructs a Global M2 Liquidity Index from the top 10 most BTC-relevant fiat currencies

(USD, EUR, JPY, GBP, INR, CNY, KRW, BRL, CAD, AUD)

— each weighted by its Bitcoin adoption score and FX-converted into USD.

📊 Applies a MACD (Moving Average Convergence Divergence) signal to the index to detect macro liquidity trends.

🟢 Plots a histogram of business cycle momentum (red = expansion, green = contraction).

🔴 Marks potential cycle peaks, useful for macro trading alignment.

⚖️ BTC Affinity-Weighted Countries:

🇺🇸 United States

🇪🇺 Eurozone

🇯🇵 Japan

🇬🇧 United Kingdom

🇮🇳 India

🇨🇳 China

🇰🇷 South Korea

🇧🇷 Brazil

🇨🇦 Canada

🇦🇺 Australia

Weights are user-adjustable to reflect evolving capital controls, regulation, and real-world BTC adoption trends.

✅ Use Cases:

Confirm macro risk-on vs risk-off regimes for BTC and crypto.

Identify ideal entry and exit zones in macro pair trades (e.g., MSTR vs MSTY).

Monitor how global monetary expansion feeds into BTC valuations.

US Liquidity-Weighted Business Cycle📈 BTC Liquidity-Weighted Business Cycle

This indicator models the Bitcoin macro cycle by comparing its logarithmic price against a log-transformed liquidity proxy (e.g., US M2 Money Supply). It helps visualize cyclical tops and bottoms by measuring the relative expansion of Bitcoin price versus fiat liquidity.

🧠 How It Works:

Transforms both BTC and M2 using natural logarithms.

Computes a liquidity ratio: log(BTC) – log(M2) (i.e., log(BTC/M2)).

Runs MACD on this ratio to extract business cycle momentum.

Plots:

🔴 Histogram bars showing cyclical growth or contraction.

🟢 Top line to track the relative price-to-liquidity trend.

🔴 Cycle peak markers to flag historical market tops.

⚙️ Inputs:

Adjustable MACD lengths

Toggle for liquidity trend line overlay

🔍 Use Cases:

Identifying macro cycle tops and bottoms

Timing long-term Bitcoin accumulation or de-risking

Confirming global liquidity's influence on BTC price movement

Note: This version currently uses US M2 (FRED:M2SL) as the liquidity base. You can easily expand it with other global M2 sources or adjust the weights.

[blackcat] L1 Dual Ehlers Bandpass FilterOVERVIEW

The Dual Ehlers Bandpass Filter combines two bandpass filters tuned to the dominant and subdominant market cycles, creating a powerful signal extraction tool. This indicator uses John Ehlers' advanced digital signal processing techniques to isolate specific frequency components from price data. By mixing the outputs of two bandpass filters, it provides a smoother, more responsive signal that captures both primary and secondary market cycles. The indicator includes divergence detection capabilities and multiple mixing methods for customizable signal extraction.

FEATURES

- Dual bandpass filtering with dominant and subdominant cycle detection

- Multiple dominant cycle calculation methods (HoDyDC, PhAcDC, DuDiDC, CycPer, BPZC)

- Flexible mixing options: weighted, sum, difference, dominant-only, or subdominant-only

- Adjustable bandwidth parameters for both filters

- Built-in divergence detection with customizable lookback periods

- Optional display of individual filter components

- Color-coded signals and alerts for bullish/bearish divergences

HOW TO USE

1. Select your preferred price source (close, high, low, etc.)

2. Choose the dominant cycle calculation method from the available options

3. Set the subdominant cycle ratio (typically 0.1-0.9 of the dominant cycle)

4. Adjust bandwidth parameters for both filters (0.1-1.0 range)

5. Select your preferred mixing method:

- Weighted: Mix based on adjustable weights

- Sum: Add both filter outputs

- Difference: Subtract subdominant from dominant

- Dominant: Show only the dominant filter

- Subdominant: Show only the subdominant filter

6. Enable divergence detection to identify potential trend reversals

7. Optionally enable individual filter plots for analysis

LIMITATIONS

- The indicator requires sufficient historical data for accurate cycle detection

- Dominant cycle calculations may vary significantly during low volatility periods

- Divergence signals are lagging indicators and should be used with confirmation

- Bandpass filters may produce false signals during choppy market conditions

- The indicator is not suitable for all trading styles and timeframes

NOTES

- The indicator uses the blackcat1402/dc_ta library for advanced cycle calculations

- Zero line crossing can indicate potential trend changes

- Positive values typically suggest bullish momentum, negative values bearish momentum

- Divergence signals appear as colored dots and labels on the chart

- Alert conditions are available for both bullish and bearish divergences

THANKS

Special thanks to John Ehlers for his pioneering work in digital signal processing for financial markets.

Ludvig Indicator PROThe Ludvig Indicator is designed to identify high-probability breakout setups by combining trend, volume, volatility, and relative strength filters. It helps you enter stocks (or ETFs/crypto) when institutional money is likely flowing in, while avoiding false breakouts and weak trends.

🔑 Core Features

Zero-Lag EMA (ZLEMA)

Faster, less lagging trend detection compared to traditional EMAs.

Used as the basis for dynamic ATR bands.

ATR Volatility Bands

Adaptive bands based on the Average True Range (ATR).

Define the zone where price must close outside to confirm trend strength.

Breakout Confirmation

Requires price to close above recent highs (lookback configurable).

Ensures signals are “true breakouts,” not just noise around moving averages.

Volume Filter (Relative Volume)

Validates breakouts with significantly higher volume than average.

Prevents low-liquidity signals from triggering.

Trend Strength (ADX)

Built-in ADX calculation ensures only strong, trending moves are considered.

Default filter: ADX ≥ 18 (configurable).

Relative Strength vs. Benchmark

Compares the asset’s momentum against a benchmark (default: SPY).

Only signals when the asset is outperforming the benchmark.

Useful for sector rotation and picking leaders instead of laggards.

Alerts & Signals

Breakout entries are marked with small green triangles.

Built-in alerts for automated notifications (TradingView alerts).

Sweep2Trade Pro [CHE]Sweep2Trade Pro \ — Liquidity Sweep → Trend → Confirmation

Sweep2Trade Pro \ helps you catch high-probability reversals or continuations that start with a liquidity sweep, align with the T3 trend, and finalize with a structure confirmation (BOS). It’s designed to reduce noise, time your entries, and keep you out of weak, chop-driven signals.

What’s a “sweep”?

A liquidity sweep happens when price briefly breaks a prior swing high/low (where many stops sit), triggers those stops, and then snaps back. This “stop-hunt” creates liquidity for bigger players and often precedes a sharp move in the opposite direction if the break fails, or fuels continuation if structure actually shifts.

What’s a BOS (Break of Structure)?

A BOS is a price action event where the market takes out a recent swing level in the trend’s direction, signaling continuation and confirming that structure has shifted (bullish BOS through a recent swing high, bearish BOS through a recent swing low).

How the indicator works (at a glance)

1. Regime Filter (T3 + R²)

T3 Moving Average: A smoother, faster-responding moving average that aims to reduce lag while filtering noise, so trend direction changes are clearer.

R² (Coefficient of Determination): Measures how “linear” the recent price path is (0→1). Higher values = stronger, cleaner trend; lower values = more chop. Used here to allow trades only when trend quality exceeds a user-set threshold.

2. Sweep Detection

Bullish sweep: price pokes below a prior swing low and closes back above it.

Bearish sweep: price pokes above a prior swing high and closes back below it.

Lookback length is configurable.

3. Sequence Lock (built-in FSM)

The script manages state in phases so you don’t jump the gun:

Phase 1: Sweep detected → wait for T3 to turn in the corresponding direction.

Phase 2: T3 direction confirmed → show “SWEEP OK” and wait for final confirmation.

Trade Signal: Only fires if confirmation arrives before a timeout.

4. Confirmation Layer

BOS via wick or close (you choose),

Strong close toward the signal (top/bottom quartile of the candle),

Optional “close above/below T3” condition.

These checks help avoid weak sweeps that immediately fade.

5. Alerts & Visuals

“SWEEP OK” markers show when the sweep + T3 direction align.

Final BUY/SELL arrows appear only when the confirmation layer passes.

Ready-made alert conditions for automation.

What you can do with it

Time reversals after sweeps: Enter when a stop-hunt fades and structure confirms.

Ride continuations: Use BOS with the T3 trend to pyramid or re-enter with structure on your side.

Filter chop: Let R² gate entries to periods with cleaner directional drift.

Automate: Use the included alerts with your platform or webhook setup.

Inputs (key settings)

Regime Filter

T3 Length / Volume Factor: Controls smoothness and responsiveness. Smaller length → faster, more sensitive; higher volume factor → smoother curve.

R² Lookback & Threshold: Length of the linear fit window and the minimum “trend quality” required. Higher thresholds mean fewer, cleaner signals.

Sweep / Sequence

Swing Lookback: How far back to define the “reference” high/low for sweeps.

Timeout: Maximum bars allowed between phases to keep signals fresh.

Restart timeout on Phase 2: Optional safety so entries don’t go stale.

Confirmation

BOS Lookback: Micro-pivot window for structure breaks.

Wick vs Close BOS: Conservative traders may prefer close.

Require close above/below T3: Tightens confirmation with trend alignment.

Practical guide (quick start)

1. Timeframe & markets: Works across majors, indices, and crypto. Start with 5m–1h intraday or 1h–4h swing; adjust R² threshold upward on noisier pairs.

2. Entry recipe (Long):

Bullish sweep of a prior low → T3 turns up → BOS/strong close.

Optional: enable “close above T3” for extra confirmation.

3. Entry recipe (Short): Mirror the above.

4. Stops: Common choices are just beyond the sweep wick (tighter) or past the BOS invalidation (safer).

5. Targets: Previous structural levels, measured move, or a T3 trail (exit when price closes back through T3).

6. Avoid low-quality contexts: If R² is very low, market is likely ranging erratically—skip or widen filters.

Tips & best practices

Context first: The same sweep means different things in a strong trend vs. flat regime; that’s why the T3+R² filter exists.

BOS choice: Wick-based BOS is earlier but noisier; close-based BOS is slower but cleaner. Tune per market.

Backtest -> Forward test: Validate settings per symbol/timeframe; then paper trade before going live.

Risk: Fixed fractional risk with asymmetric R\:R (e.g., 1:1.5–1:3) generally performs better than “all-in” discretionary sizing.

Behind the scenes (for the curious)

T3 is a multi-stage EMA construction that produces a smooth curve with reduced lag versus simple/standard EMAs.

R² is the square of correlation (0–1). Here it’s used as a moving gauge of how well price aligns to a linear path—our “trend quality” dial.

Stop-hunts / sweeps are a recognized microstructure phenomenon where clustered stops provide the liquidity that fuels the next move.

Disclaimer

No indicator guarantees profits. Sweep2Trade Pro \ is a decision aid; always combine with solid risk management and your own judgment. Backtest, forward test, and size responsibly.

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence 🚀

Happy trading

Chervolino

Custom Support & Resistance Levels (Manual Input)This indicator lets you plot your own support levels (and can be extended for resistance) directly on the chart by entering them as comma-separated values.

📌 Supports manual input for multiple price levels.

📊 Lines are extended across the chart for clear visualization.

🎨 Dynamic coloring:

Green if the current price is above the level.

Red if the current price is below the level.

🧹 Old lines are automatically cleared to avoid clutter.

This tool is ideal if you:

Prefer to mark your own key zones instead of relying only on auto-detected levels.

Want clean and simple visualization of critical price areas.

👉 Coming soon: Resistance levels input (commented in the code, can be enabled).

Same Day Past CandlesSame-Day Past Candles

This indicator is a tool that plots the shapes of the candles from the same date one and two years ago directly on the current chart. By visually comparing past price movements, it can help you analyze seasonality and cyclical patterns.

Key Features

Plots Past Candles: Displays candles from the same date one and two years ago on your current chart.

Toggle Visibility: You can individually turn the display of the "1 year ago candle" and "2 years ago candle" on or off in the indicator's settings.

Candle Shape: The open, high, low, and close prices of the past candles are plotted, scaled to the current price range.

How to Use

Add this indicator to a daily chart for best results. The plotted candles are slightly offset upwards so they don't overlap with the current price, making it easier to compare the shape of the past candles with the current chart movement.

Visually checking how specific past price changes are reflected on the same day this year can provide insights for your trading strategy.

I do not speak English at all. Please understand that if you send me a message, I may not be able to reply, or my reply may have a different meaning. Thank you for your understanding.

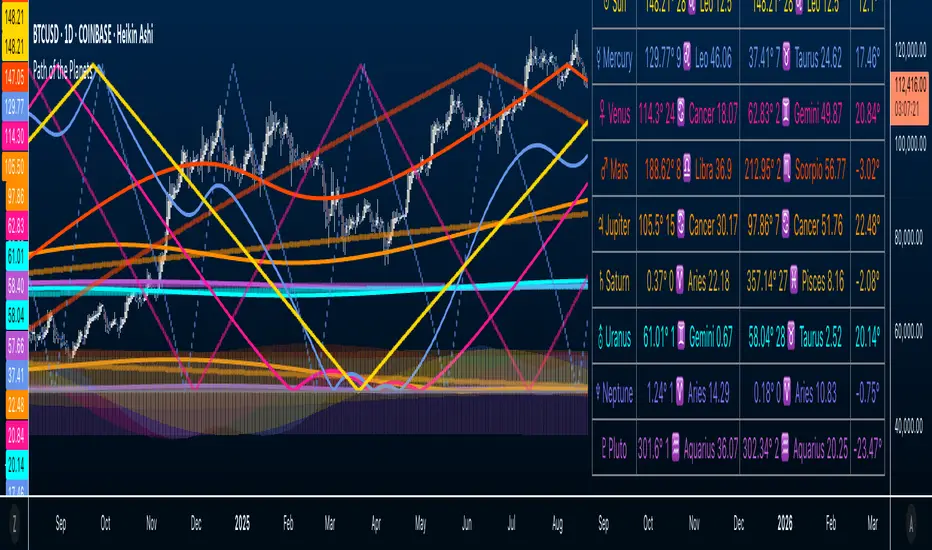

Path of the Planets🪐 Path of the Planets

Path of the Planets is an open-source Pine Script™ v6 indicator. It is inspired by W.D. Gann’s Path of Planets chart, specifically the Chart 5-9 artistic replica by Patrick Mikula "shown below". The script visualizes planetary positions so you can explore possible correlations with price. It overlays geocentric and heliocentric longitudes and declinations using the AstroLib library and includes an optional positions table that shows, at a glance, each body’s geocentric longitude, heliocentric longitude, and declination. This is an educational tool only and not trading advice.

Key Features

Start point: Choose a date and time to begin plotting so studies can align with market events.

Adjustments: Mirror longitudes and shift by 360° multiples to re-frame cycles.

Planets: Toggle geocentric and heliocentric longitudes and declinations for Sun, Mercury, Venus, Earth, Mars, Jupiter, Saturn, Uranus, Neptune, and Pluto. Moon declination is available.

Positions table: Optional color-coded table (bottom-right) with three columns labeled Geo, Helio, and Dec. Values show degrees with the zodiac sign for the longitudes and degrees for declinations.

Visualization: Solid lines for geocentric longitudes, circles for heliocentric longitudes, and columns for declinations. Includes a zero-declination reference line.

How It Works

Converts bar timestamps to Julian days via AstroLib.

Fetches positions with AstroLib types: geocentric (0), heliocentric (1), and declination (3).

Normalizes longitudes to the −180° to +180° range, applies optional mirroring and 360° shifts, and converts longitudes to zodiac sign labels for the table.

Plots and the table update only on and after the selected start time.

Usage Tips

Apply on daily or higher timeframes when studying broader cycles. For degrees, use the left scale.

Limitations at the moment: default latitude, longitude, and timezone are set to 0; aspects and retrogrades are not included; the focus is on raw paths.

License and Credits

Dependency: @BarefootJoey Astrolib

Contributions and observations are welcome.

Ichimoku Trading Signals 2Swing Trading (Strategy 1, H4+ timeframes)

Use the Kumo Cloud to identify the trend: price above a green cloud = uptrend; price below a red cloud = downtrend.

Entry signals occur when price or the Tenkan-sen line crosses the Kijun-sen line, confirmed by Chikou Span momentum.

Exit triggers when price crosses back through the Kijun-sen or when Tenkan-sen crosses back below (for long positions) or above (for short positions).

Place stop-loss orders just beyond the nearest swing low/high candle cluster to manage risk tightly.

Market Sessions [odnac]

This indicator highlights the three main global market sessions (USA, Europe, Asia) and their overlaps directly on the chart.

It helps traders quickly identify active trading periods and potential high-liquidity overlaps.

Features:

Customizable start and end times for each session

Optional daily dividers with weekday labels

Session markers displayed as circles above the candles

Overlap sessions displayed in distinct colors

Adjustable opacity for better chart visibility

Option to hide weekends

Sessions included:

USA Market Session (default 13:30–20:00 UTC)

Europe Market Session (default 07:00–16:00 UTC)

Asia Market Session (default 00:00–09:00 UTC)

Overlaps: USA + Europe, USA + Asia, Europe + Asia

This tool is designed for intraday timeframes (1m–60m) and can be useful for scalping, day trading, or session-based strategies.

DMI MTF Color Table v5DMI Multi-Timeframe Color Table v5

A comprehensive DMI (Directional Movement Index) table that displays trend direction and strength across multiple timeframes simultaneously. This indicator helps traders quickly assess market conditions and identify confluence across different time horizons.

Features:

Multi-timeframe analysis (7 configurable timeframes)

Color-coded cells based on trend strength and direction

Real-time current market condition display

Customizable strength thresholds and color schemes

Multiple display modes (All, DI+ Only, DI- Only, ADX Only)

Text-based strength classifications (STRONG/MEDIUM/WEAK)

Directional bias indicators (BULL/BEAR)

How It Works:

The table shows DI+, DI-, and ADX values across your chosen timeframes with intelligent color coding:

Green shades indicate bullish momentum (DI+ > DI-)

Red shades indicate bearish momentum (DI- > DI+)

Color intensity reflects trend strength based on ADX values

Current market condition appears in top-right corner

Display Options:

Toggle numerical values, strength text, and timeframe labels

Adjustable table size and transparency

Customizable color schemes for all conditions

Optional current timeframe DMI plot overlay

Educational Use:

This tool is designed for educational purposes to help understand multi-timeframe analysis and DMI interpretation. All trading decisions should be based on your own analysis and risk management.

Credits:

Original concept and development by Profitgang. If you use or modify this script, please provide appropriate credit to the original author.

Note: This indicator is for analysis purposes only. Past performance does not guarantee future results. Always conduct your own research and consider your risk tolerance before making trading decisions.

ICT Structure Levels (ST/IT/LT) - v7 (by Jonas E)ICT Structure Levels (ST/IT/LT) – Neighbor-Wick Pivots

This indicator is designed for traders following ICT-style market structure analysis. It identifies Short-Term (ST), Intermediary (IT), and Long-Term (LT) swing highs and lows, but with a stricter filter that reduces false signals.

Unlike standard pivot indicators, this script requires not only that a bar makes a structural high/low, but also that the neighboring bars’ extremes are formed by wicks rather than flat-bodied candles. This wick condition helps confirm that the level is a true liquidity sweep and not just random price action.

How it works (conceptual):

Detects pivots based on user-defined left/right bars.

Validates that extremes on both sides of the pivot are wick-driven (high > body for highs, low < body for lows).

Marks valid STH/STL, ITH/ITL, and LTH/LTL directly on the chart with optional price labels.

Uses ATR offset for better label readability.

Alerts can be enabled to notify when a new structural level is confirmed.

How to use it:

Map market structure across multiple layers (ST/IT/LT).

Identify true liquidity grabs and avoid false highs/lows.

Integrate with Break of Structure (BOS) and Change of Character (CHoCH) strategies.

Combine with other ICT concepts (Order Blocks, Fair Value Gaps, Liquidity Pools).

What makes it unique:

Most pivot indicators mark every high/low indiscriminately. This script filters pivots using wick validation, which significantly reduces noise and focuses only on the levels most relevant to liquidity-based trading strategies.

Auto-Fit Growth Trendline# **Theoretical Algorithmic Principles of the Auto-Fit Growth Trendline (AFGT)**

## **🎯 What Does This Algorithm Do?**

The Auto-Fit Growth Trendline is an advanced technical analysis system that **automates the identification of long-term growth trends** and **projects future price levels** based on historical cyclical patterns.

### **Primary Functionality:**

- **Automatically detects** the most significant lows in regular periods (monthly, quarterly, semi-annually, annually)

- **Constructs a dynamic trendline** that connects these historical lows

- **Projects the trend into the future** with high mathematical precision

- **Generates Fibonacci bands** that act as dynamic support and resistance levels

- **Automatically adapts** to different timeframes and market conditions

### **Strategic Purpose:**

The algorithm is designed to identify **fundamental value zones** where price has historically found support, enabling traders to:

- Identify optimal entry points for long positions

- Establish realistic price targets based on mathematical projections

- Recognize dynamic support and resistance levels

- Anticipate long-term price movements

---

## **🧮 Core Mathematical Foundations**

### **Adaptive Temporal Segmentation Theory**

The algorithm is based on **dynamic temporal partition theory**, where time is divided into mathematically coherent uniform intervals. It uses modular transformations to create bijective mappings between continuous timestamps and discrete periods, ensuring each temporal point belongs uniquely to a specific period.

**What does this achieve?** It allows the algorithm to automatically identify natural market cycles (annual, quarterly, etc.) without manual intervention, adapting to the inherent periodicity of each asset.

The temporal mapping function implements a **discrete affine transformation** that normalizes different frequencies (monthly, quarterly, semi-annual, annual) to a space of unique identifiers, enabling consistent cross-temporal comparative analysis.

---

## **📊 Local Extrema Detection Theory**

### **Multi-Point Retrospective Validation Principle**

Local minima detection is founded on **relative extrema theory with sliding window**. Instead of using a simple minimum finder, it implements a cross-validation system that examines the persistence of the extremum across multiple historical periods.

**What problem does this solve?** It eliminates false minima caused by temporal volatility, identifying only those points that represent true historical support levels with statistical significance.

This approach is based on the **statistical confirmation principle**, where a minimum is only considered valid if it maintains its extremum condition during a defined observation period, significantly reducing false positives caused by transitory volatility.

---

## **🔬 Robust Interpolation Theory with Outlier Control**

### **Contextual Adaptive Interpolation Model**

The mathematical core uses **piecewise linear interpolation with adaptive outlier correction**. The key innovation lies in implementing a **contextual anomaly detector** that identifies not only absolute extreme values, but relative deviations to the local context.

**Why is this important?** Financial markets contain extreme events (crashes, bubbles) that can distort projections. This system identifies and appropriately weights them without completely eliminating them, preserving directional information while attenuating distortions.

### **Implicit Bayesian Smoothing Algorithm**

When an outlier is detected (deviation >300% of local average), the system applies a **simplified Kalman filter** that combines the current observation with a local trend estimation, using a weight factor that preserves directional information while attenuating extreme fluctuations.

---

## **📈 Stabilized Extrapolation Theory**

### **Exponential Growth Model with Dampening**

Extrapolation is based on a **modified exponential growth model with progressive dampening**. It uses multiple historical points to calculate local growth ratios, implements statistical filtering to eliminate outliers, and applies a dampening factor that increases with extrapolation distance.

**What advantage does this offer?** Long-term projections in finance tend to be exponentially unrealistic. This system maintains short-to-medium term accuracy while converging toward realistic long-term projections, avoiding the typical "exponential explosions" of other methods.

### **Asymptotic Convergence Principle**

For long-term projections, the algorithm implements **controlled asymptotic convergence**, where growth ratios gradually converge toward pre-established limits, avoiding unrealistic exponential projections while preserving short-to-medium term accuracy.

---

## **🌟 Dynamic Fibonacci Projection Theory**

### **Continuous Proportional Scaling Model**

Fibonacci bands are constructed through **uniform proportional scaling** of the base curve, where each level represents a linear transformation of the main curve by a constant factor derived from the Fibonacci sequence.

**What is its practical utility?** It provides dynamic resistance and support levels that move with the trend, offering price targets and profit-taking points that automatically adapt to market evolution.

### **Topological Preservation Principle**

The system maintains the **topological properties** of the base curve in all Fibonacci projections, ensuring that spatial and temporal relationships are consistently preserved across all resistance/support levels.

---

## **⚡ Adaptive Computational Optimization**

### **Multi-Scale Resolution Theory**

It implements **automatic multi-resolution analysis** where data granularity is dynamically adjusted according to the analysis timeframe. It uses the **adaptive Nyquist principle** to optimize the signal-to-noise ratio according to the temporal observation scale.

**Why is this necessary?** Different timeframes require different levels of detail. A 1-minute chart needs more granularity than a monthly one. This system automatically optimizes resolution for each case.

### **Adaptive Density Algorithm**

Calculation point density is optimized through **adaptive sampling theory**, where calculation frequency is adjusted according to local trend curvature and analysis timeframe, balancing visual precision with computational efficiency.

---

## **🛡️ Robustness and Fault Tolerance**

### **Graceful Degradation Theory**

The system implements **multi-level graceful degradation**, where under error conditions or insufficient data, the algorithm progressively falls back to simpler but reliable methods, maintaining basic functionality under any condition.

**What does this guarantee?** That the indicator functions consistently even with incomplete data, new symbols with limited history, or extreme market conditions.

### **State Consistency Principle**

It uses **mathematical invariants** to guarantee that the algorithm's internal state remains consistent between executions, implementing consistency checks that validate data structure integrity in each iteration.

---

## **🔍 Key Theoretical Innovations**

### **A. Contextual vs. Absolute Outlier Detection**

It revolutionizes traditional outlier detection by considering not only the absolute magnitude of deviations, but their relative significance within the local context of the time series.

**Practical impact:** It distinguishes between legitimate market movements and technical anomalies, preserving important events like breakouts while filtering noise.

### **B. Extrapolation with Weighted Historical Memory**

It implements a memory system that weights different historical periods according to their relevance for current prediction, creating projections more adaptable to market regime changes.

**Competitive advantage:** It automatically adapts to fundamental changes in asset dynamics without requiring manual recalibration.

### **C. Automatic Multi-Timeframe Adaptation**

It develops an automatic temporal resolution selection system that optimizes signal extraction according to the intrinsic characteristics of the analysis timeframe.

**Result:** A single indicator that functions optimally from 1-minute to monthly charts without manual adjustments.

### **D. Intelligent Asymptotic Convergence**

It introduces the concept of controlled asymptotic convergence in financial extrapolations, where long-term projections converge toward realistic limits based on historical fundamentals.

**Added value:** Mathematically sound long-term projections that avoid the unrealistic extremes typical of other extrapolation methods.

---

## **📊 Complexity and Scalability Theory**

### **Optimized Linear Complexity Model**

The algorithm maintains **linear computational complexity** O(n) in the number of historical data points, guaranteeing scalability for extensive time series analysis without performance degradation.

### **Temporal Locality Principle**

It implements **temporal locality**, where the most expensive operations are concentrated in the most relevant temporal regions (recent periods and near projections), optimizing computational resource usage.

---

## **🎯 Convergence and Stability**

### **Probabilistic Convergence Theory**

The system guarantees **probabilistic convergence** toward the real underlying trend, where projection accuracy increases with the amount of available historical data, following **law of large numbers** principles.

**Practical implication:** The more history an asset has, the more accurate the algorithm's projections will be.

### **Guaranteed Numerical Stability**

It implements **intrinsic numerical stability** through the use of robust floating-point arithmetic and validations that prevent overflow, underflow, and numerical error propagation.

**Result:** Reliable operation even with extreme-priced assets (from satoshis to thousand-dollar stocks).

---

## **💼 Comprehensive Practical Application**

**The algorithm functions as a "financial GPS"** that:

1. **Identifies where we've been** (significant historical lows)

2. **Determines where we are** (current position relative to the trend)

3. **Projects where we're going** (future trend with specific price levels)

4. **Provides alternative routes** (Fibonacci bands as alternative targets)

This theoretical framework represents an innovative synthesis of time series analysis, approximation theory, and computational optimization, specifically designed for long-term financial trend analysis with robust and mathematically grounded projections.

MMA, Mid-Price Moving Averages (Open + Close Based MAs)📝 Script Description

This script introduces a custom set of moving averages based on the mid-price, calculated as the average of the open and close prices:

Mid Price = (Open + Close) / 2

Instead of traditional close-based MAs, this approach reflects the average sentiment throughout the trading session, offering a smoother and more realistic view of price action.

🔍 Key Features:

✅ Gap-aware smoothing

Captures opening gaps, offering a better representation of intraday shifts.

✅ Reduced noise

Less vulnerable to sharp closing moves or one-off spikes, making it easier to identify true trend breaks or supports.

✅ Closer to actual flow

Reflects a more natural midline of price movement, ideal for traders who prioritize clean, sustained trends.

✅ Better support/resistance alignment

Especially useful for identifying stable uptrends and minimizing false breakout signals.

📐 Included Moving Averages:

MA 5

MA 10

MA 20

MA 60

MA 120

MA 200

(All based on mid-price, not close)

🎯 Recommended For:

Traders seeking smoother and more reliable trendlines

Those who want a more realistic depiction of support and resistance

Ideal for filtering out noisy movements while focusing on clean, straight-moving charts

Daily Seasonality Strength + Prediction TableDaily Seasonality Strength + Prediction Table

Return Estimates:

This indicator uses historical price data to calculate average returns for each day (of the week or month) and uses these to predict the next day’s return.

Seasonality Strength:

It measures seasonality strength by comparing predicted returns with actual returns, using the inverse of MSE (higher values mean stronger seasonality).

supports up to 10 assets

This script is for informational and educational purposes only. It does not constitute financial, investment, or trading advice. I am not a financial advisor. Any decisions you make based on this indicator are your own responsibility. Always do your own research and consult with a qualified financial professional before making any investment decisions.

Past performance is no guarantee of future results. The value of the instruments may fluctuate and is not guaranteed

Transfer Function Filter [theUltimator5]The Transfer Function Filter is an engineering style approach to transform the price action on a chart into a frequency, then filter out unwanted signals using Butterworth-style filter approach.

This indicator allows you to analyze market structure by isolating or removing different frequency components of price movement—similar to how engineers filter signals in control systems and electrical circuits.

🔎 Features

Four Filter Types

1) Low Pass Filter – Smooths price data, highlighting long-term trends while filtering out short-term noise. This filter acts similar to an EMA, removing noisy signals, resulting in a smooth curve that follows the price of the stock relative to the filter cutoff settings.

Real world application for low pass filter - Used in power supplies to provide a clean, stable power level.

2) High Pass Filter – Removes slow-moving trends to emphasize short-term volatility and rapid fluctuations. The high pass filter removes the "DC" level of the chart, removing the average price moves and only outputting volatility.

Real world application for high pass filter - Used in audio equalizers to remove low-frequency noise (like rumble) while allowing higher frequencies to pass through, improving sound clarity.

3) Band Pass Filter – Allows signals to plot only within a band of bar ranges. This filter removes the low pass "DC" level and the high pass "high frequency noise spikes" and shows a signal that is effectively a smoothed volatility curve. This acts like a moving average for volatility.

Real world application for band pass filter - Radio stations only allow certain frequency bands so you can change your radio channel by switching which frequency band your filter is set to.

4) Band Stop Filter – Suppresses specific frequency bands (cycles between two cutoffs). This filter allows through the base price moving average, but keeps the high frequency volatility spikes. It allows you to filter out specific time interval price action.

Real world application for band stop filter - If there is prominent frequency signal in the area which can cause unnecessary noise in your system, a band stop filter can cancel out just that frequency so you get everything else

Configurable Parameters

• Cutoff Periods – Define the cycle lengths (in bars) to filter. This is a bit counter-intuitive with the numbering since the higher the bar count on the low-pass filter, the lower the frequency cutoff is. The opposite holds true for the high pass filter.

• Filter Order – Adjust steepness and responsiveness (higher order = sharper filtering, but with more delay).

• Overlay Option – Display Low Pass & Band Stop outputs directly on the price chart, or in a separate pane. This is enabled by default, plotting the filters that mimic moving averages directly onto the chart.

• Source Selection – Apply filters to close, open, high, low, or custom sources.

Histograms for Comparison

• BS–LP Histogram – Shows distance between Band Stop and Low Pass filters.

• BP–HP Histogram – Highlights differences between Band Pass and High Pass filters.

Histograms give the visualization of a pseudo-MACD style indicator

Visual & Informational Aids

• Customizable colors for each filter line.

• Optional zero-line for histogram reference.

• On-chart info table summarizing active filters, cutoff settings, histograms, and filter order.

📊 Use Cases

Trend Detection – Use the Low Pass filter to smooth noise and follow underlying market direction.

Volatility & Cycle Analysis – Apply High Pass or Band Pass to capture shorter-term patterns.

Noise Suppression – Deploy Band Stop to remove specific choppy frequencies.

Momentum Insight – Watch the histograms to spot divergences and relative filter strength.