MACD (KST Based) V2This is the next version of the original indicator:

To anyone unfamiliar with KST, it is a cousin of RSI. Basically, this indicator is analyzed like we would analyze charts using Stochastic RSI. It is basically an "energy oscillator".

This indicator considers price with the theory of relativity.

Relativity works this way: A downward moving MACD means that price velocity is slowing down. An upward moving one means that price is accelerating .

KST-Based MACD is all about relative performance. Exponential charts behave identically to horizontal ones.

Compare SPX and SPX/CURRCIR and see for yourself.

Just like the classic MACD, bear/bull signals appear on the histogram.

A band is drawn around the MACD, which is useful to pinpoint overbought/oversold conditions / squeezes.

It is also very useful for pinpointing / confirming divergences.

Tread lightly, for this is hallowed ground.

-Father Grigori

P.S. This is version 2 of the original one. Custom formulae are used all around this indicator. Basically, every formula has been reimagined for it to work in super-long-term timeframes. This indicator, compared to the previous one, doesn't ignore any chart data. It takes every single candle into consideration.

P.S.2. Pro tip: Use two separate windows, one with KST-MACD and one with KST-Histogram, just like in the cover.

Cerca negli script per "spx"

Murder Algo Stats: last portion of Indices closing hour (S&P)Stats regarding the 'murder algo' (last 10mins of the closing hour). Works on all sub-1hr timeframes. Best used on 5min, 10min 15min timeframe. Ideal use on 10min timeframe.

Can be applied to other user input sessions also

What i'm calling the 'Murder Algo' is the tendency of dynamic lower time frame price action in the final 10minutes of the S&P closing hour (or any of the three major US indices: S&P, Nasdaq, Dow).

If there are un-met liquidity targets (i.e. clean highs or lows) as we come into the last portion of the closing hour, price has a tendency to stretch up or down to reach these targets, swiftly.

These statisitics are somewhat experimental/research; trying to quantify this tendency. Please comment below if you think of some additions / modifications that may prove useful.

//Purpose:

-To get statistics of the tendency to 'reach' of the final bar (10minute bar in the above) of the closing hour in Indices (3pm - 4pm NY time).

-Specifically to see how often price reaches for HH or LL in the final bar of the closing hour (most of the time); and to see how far it reaches one way when it does (Mean, median, mode).

//Notes:

-Two sets of historical stats; one is based on the 'solo reach' of the last bar; the other is based on the reach of the last bar from the average price of the preceding bars of the session (purple line in the above)

-Works on any timeframe below hourly. Ideally used on 10min timeframe, but may be interesting to plot on 15min or 5min timeframe also.

-Should also work on custom user-defined session; though this indicator was explicly designed to investigate the 'murder algo': that final rush and/or whipsaw tendency of price in the last few minutes of Regular trading on Indices.

-For S&P, best used on SPX, which gives the longest history of all the S&P variants due to only showing Regular trading hours bars (500 days of history on 10min timeframe, for premium users)

-For most stats, i've rounded to ES1! mintick (i.e. rounded to nearest quarter dollar) =>> This allows more meaningful values for 'mode' statistical measure.

-I trade S&P; but this 'muder algo' phenomenon also obviously presents in Nasdaq and Dow.

//User Inputs:

-Session time input (defaults to closing hour 3pm - 4pm NY time)

-Average method (for the average of all the input session EXCEPT the final bar)

-Toggle on/off Average line.

-other formatting options: text color, table position, line color/style/size.

Example usage with annotations on SPX 500 chart 15m timeframe; using closing hour (3pm-4pm NY time) as our session:

LNL Simple Hedging ToolLNL Simple Hedging Tool

Simple Hedging Tool was created specifically for swing traders who struggle with hedging. This tool helps to spot the ideal moments to put the hedges on (protection of the portfolio during "high risk" times). Simple Hedging Tool will not help you when day trading. It was designed for the daily charts. It is called simple because it is pretty much self-explanatory indicator. The candles are either blue or yellow. Meaning of the colors depend on the version you are using. This tool consist of two versions:

SPX Version:

This version was designed for indexes & overall market benchmarks. In contrast with the VIX version, the SPX version is little more sophisticated since it is based on key market internals. Blue arrows above the candles? More often than not this is signalizing that the key market internals are now approaching bearish signals which means it is the best time to hedge any bullish positions. On the contrary, the yellow arrows are the good reason to lighten up of the shorts & ease off the gas pedal on any bearish outlooks.

VIX Version:

Apart from the black swan events (big market crashes) Vix usually oscillates between the daily extremes. The VIX version is based on a simple bollinger band technique which is visualized with blue & yellow arrows. Whenever the yellow arrows & candles appear, it is good time to put the hedges on & perhaps lighten up on longs.

IMPORTANT DISCLAIMER:

The signals from this tool WILL NOT TELL YOU where to buy or sell! But rather when is a good time TO NOT buy or TO NOT sell. Once the signals appear it does not necessarily mean that the move is over & reversion willl happen immidiately. These signals can be flashing for days even weeks. They are not flashing for you to change the bias but rather tighten up your exposure in case your portfolio is mostly one sided.

Hope it helps.

ADD 2This is a modification to the original ADD script by Tom1trader

I added the option to choose the timeframe, moving average type and length.

Note from the original script:

"This is the NYSE Advancers - decliners which the SPX pretty much follows. You can chart it like any index (ADD -NYSE $ADV MINUS $DECL) but I find it more useful in a separate panel with colors for direction.

The level gives an idea of days move (example: plus or minus 500 is not much movement through the session) but I follow the direction as when more stocks advance (green) or decline (red) the index tends to track it pretty closely.

On SPX , SPY and correlates - very useful for intra-day trading (Scalping or 0DTE option trades) but not for higher time frames at all. If you chart the ADD in a chart and compare 5 minute to daily you will see what I mean."

RSI with Keltner Channel (+EMA Ribbon)Note that the EMA Ribbon is not embedded into the custom RSI with KC. In the future I plan to embed it. The EMA Ribbon I use is the following:

This is my very first attempt at modifying an indicator. I basically attempted to add a Keltner Channel around RSI.

This was used as an alternative channel to the standard Bollinger Band. KC goes hand-in-hand with the EMA Ribbon. KC also helps to better pinpoint relative-overbought/oversold conditions.

In my belief, the 20-80 levels don't behave as overbought/oversold levels. An exponential chart would always be overbought. So a Keltner Channel could in theory (and in practice) give us greater understanding on chart analysis.

This custom indicator is a bodge . It has lots of extra calculations that can be removed. I post this rough indicator for the community to give feedback on how I can improve it, or perhaps give an idea to some of you. Please don't judge me, I wouldn't post it but lately some have asked me about it.

In the future I would like to embed an EMA ribbon in this RSI indicator, just like I did in the following idea.

During this period, I don't really have the time to fix this indicator to my standards. So I will leave it as is for the foreseeable future.

If you have the will and knowledge however, feel free to built upon this indicator and share it!

Tread lightly, for this is hallowed ground.

-Father Grigori

PS. In this indicator, I would replace all the moving averages with an EMA Ribbon "average".

Correlation prix [SP500, TESLA, BTCBefore you see this post I want to thank all the TradingView team. Every day that passes I learn better and better to use Pine script and I owe this to all those who publish and to the philosophy of TradingView. Thanks from Amos

This trading indicator compares the prices of the S&P 500 Index (SP500), Tesla (TSLA), and Bitcoin (BTC) to find correlations between them. To make the prices of SP500 and Tesla comparable to the price of Bitcoin, the indicator multiplies the closing price of Tesla by 114 and the closing price of the S&P 500 Index by 5.6.

In this way we can superimpose the prices on the BTC chart and see what happens.

Average BTC price/ tesla price = 114, so if we multiply the tesla price by 114 times we can superimpose it on the BTC price

At average BTC/SPX price = 5.6, also in this case we multiply the price of SPX by 5.6 to overlay the graph and see any correlations.

The indicator then calculates the average price between SP500 and Tesla, using the formula (SP500 + Tesla) / 2. This calculation creates a new line on the chart that represents the average price between these two assets.

The BTC_SP_TE variable is then calculated as the average of the closing price of Bitcoin and the previously calculated average price of SP500 and Tesla, using the formula (Btc + SP_TE) / 2. This calculation creates another line on the chart that represents the average price between Bitcoin and the previously calculated average between SP500 and Tesla.

The idea behind calculating these averages is to find correlations and patterns between the prices of these assets, which can help identify potential trading opportunities. By comparing the average prices of different assets, the trader can look for trends and patterns that might not be apparent when looking at each asset individually.

The indicator plots these prices on a chart and fills the area between them with either green or fuchsia, depending on which one is higher. The strategy suggests buying Bitcoin when the average price of SP500 and Tesla is higher than the current price of Bitcoin, and selling when it is lower.

To add visual cues to the trading strategy, the indicator uses the plotchar function to display a small triangle below the chart when it detects a potential buying opportunity. This is done with the following parameters:

Value: BTC_SP_TE < Btc and Btc > Btc1 and Btc1 > Btc , which is a logical expression that checks whether the average price of SP500 and Tesla is less than the current price of Bitcoin (BTC_SP_TE < Btc), and whether the current price of Bitcoin is higher than the price 10 bars ago (Btc > Btc1 ) and higher than the price on the previous bar (Btc1 > Btc ).

Text: "Moyen BTC_SP_Te", which is the text to display inside the marker.

Symbol: "▲", which is the symbol to use for the marker. In this case, it is a small triangle pointing upwards.

Location: location.belowbar, which specifies that the marker should be placed below the bar.

I hope this is an example of how to create an indicator on TradingView, remember that correlations do not always last, it is possible that when you see the graph this correspondence no longer exists, do your studies and get inspired.

Fair Value Strategy - ekmllThis is a strategy using SPX's Fair Value derived from Net Liquidity.

The main difference between this one and calebsandfort's one is net liquidity values in this one are calculated in TradingView and doesn't need author's daily library updates to function.

Net Liquidity function is simply: Fed Balance Sheet - Treasury General Account - Reverse Repo Balance

Formula for calculating the fair value of and Index using Net Liquidity looks like this: (WALCL - WTREGEN - RRPONTSYD)/1000000000/scalar - subtractor

The Index Fair Value is then subtracted from the Index value which creates an oscillating diff value.

When diff is greater than the overbought threshold, Index is considered overbought and we go short/sell.

When diff is less than the oversold signal, Index is considered oversold and we cover/buy.

Parameters:

Index: SPX, NDX, RUT

Strategy: Short Only, Long Only, Long/Short

Inverse (bool): check if using an inverse ETF to go long instead of short.

Scalar (float)

Subtractor (int)

Overbought Threshold (int)

Oversold Threshold (int)

Start After Date: When the strategy should start trading

Close Date: Day to close open trades. I just like it to get complete results rather than the strategy ending with open trades.

I've optimized the parameters for SPX.

QQQ Fair Value BandsThis is similar to the SPX Fair Value Bands indicator, but for QQQ.

It is based on the Net Liquidity model:

Net Liquidity = FED - RRP - TGA

RSI Multi Symbol/Time Frame DetectorThis code is an implementation of the Relative Strength Index (RSI) indicator, which is a popular momentum indicator used in technical analysis. The RSI measures the strength of an asset's price action and provides information on whether the asset is overbought or oversold. The code also calculates a moving average of the RSI and allows the user to choose the type of moving average to be calculated (SMA, EMA, SMMA, WMA, or VWMA).

The user can select from different time frames (5, 15, 60, or 240), symbols (SP:SPX, OANDA:EURUSD, or OANDA:NZDUSD), RSI lengths, and moving average types and lengths.

The code starts by defining a function called "ma" for calculating different types of moving averages. This function takes as input the source data for the moving average calculation (the RSI), the length of the moving average, and the type of moving average. The function uses a switch statement to return the appropriate calculation based on the inputted moving average type.

Next, the code calculates the RSI and its moving average. The RSI is calculated using the well-known formula for the RSI, which involves calculating the average gains and losses over a specified period of time and then dividing the average gains by the average losses. The moving average is calculated using the "ma" function defined earlier.

Finally, the code allows the user to choose the symbol and time frame to be used in the RSI calculation, as well as the length of the RSI and the moving average, and the type of moving average. The user can choose from three symbols (SP:SPX, OANDA:EURUSD, OANDA:NZDUSD) and four time frames (5, 15, 60, and 240 minutes). The code then uses the "request.security" function to retrieve the RSI calculation for the selected symbol and time frame.

Note: This code is example for you to use multi timeframe/symbol in your indicator or Strategy , also prevent Repainting Calculation

Global Net Liquidity - Dow Jones Global Fair ValueThis is similar to Global Net Liquidity - SPX Fair Value except it's for Dow Jones Global (symbol: W1DOW here on TradingView).

This is experimental and may change at any time.

Cash VIX Term StructureLet’s first start with some definitions:

VIX9D: The CBOE S&P 500 9-Day Volatility Index estimates the expected 9-day volatility of S&P 500® stock returns.

www.cboe.com

VIX: The CBOE Volatility Index® (VIX® ) is considered by many to be the world's premier barometer of equity market volatility. The VIX Index is based on real-time prices of options on the S&P 500® Index (SPX) and is designed to reflect investors' consensus view of future (30-day) expected stock market volatility. The VIX Index is often referred to as the market's "fear gauge".

www.cboe.com

VIX3M: The CBOE 3-Month Volatility Index is designed to be a constant measure of 3-month implied volatility of the S&P 500® (SPX) Index options.

www.cboe.com

VIX6M: The CBOE S&P 500 6-Month Volatility Index is an estimate of the expected 6-month volatility of the S&P 500® Index.

www.cboe.com

VIX1Y: The CBOE S&P 500 1-Year Volatility Index is an estimate of the expected 1-Yeaer volatility of the S&P 500® Index.

www.cboe.com

This indicator visually displays the relationship between all the above products (short term vol vs long term vol). It also displays the current value and daily percentage change.

The shape of the term structure can tell us a lot about the market:

When the slope of the term structure is upward sloping (longer term VIX are higher than shorter term VIX), we say the term structure is in contango. This usually means that market is stable.

When the slope of the term structure is downward sloping (longer term VIX are lower than shorter term VIX), we say the term structure is in backwardation. This usually happens in periods of extreme market volatility.

Sometimes VIX9D will be higher than VIX but the rest of the curve is in contango. This means that there might be some event in the next 9 days that we need to pay attention to.

I also added a few ratios that I personally track like VIX9D/VIX, VIX/VIX3M and VIX/VIX6M.

When trading short term, I tend to focus on the front end of the curve. When trading long term, I tend to look at VIX/VIX6M.

In addition to the ratios, I added some historical parameters (lookback date can be set from the indicator’s settings) like Highest Value, Lowest Value, Percentile Rank, Average, Median and Mode.

Percentile ranks are displayed for both individual products and their ratios (that’s how I like to see them).

I hope you guys like this indicator.

Happy trading!

Market SnapshotGet a snapshot of the market with the index's last price, distance to selectable moving averages, and breadth data.

Choose to see data based on the Nasdaq or SPX, as well as net highs / lows for the Nasdaq, NYSE or combined.

Snapshot shows:

- Index's (SPX or Nasdaq's) last price

- Put call ratio

- % of stocks above the 50 day moving average for the index of your choice

- % of stocks above the 200 day moving average for the index of your choice

- Distance to or from two selectable moving averages. (negative number means price is below the moving average, positive means price is above)

Configurable options:

- Which moving averages to use

- Where to display the table on your chart

- Table size, background and text colors

Markets vs Inflation [x7.am]Markets vs Inflation(CPI US) also known as Inflation-Adjusted Return.

The inflation-adjusted return is the measure of return that takes into account the time period's inflation rate. The purpose of the inflation-adjusted return metric is to reveal the return on an investment after removing the effects of inflation.

Removing the effects of inflation from the return of an investment allows the investor to see the true earning potential of the security without external economic forces. The inflation-adjusted return is also known as the real rate of return or required rate of return adjusted for inflation. It is a more accurate measure of investment performance than the nominal rate of return.

The inflation-adjusted return accounts for the effect of inflation on an investment's performance over time.

Also known as the real return, the inflation-adjusted return provides a more realistic comparison of an investment's performance.

Inflation will lower the size of a positive return and increase the magnitude of a loss.

Assume you have saved $10,000 to buy a car but decide to invest the money for a year before buying to ensure that you have a small cash cushion left over after getting the car. Earning 5% interest, you have $10,500 after 12 months. However, because prices increased by 3% during the same period due to inflation, the same car now costs $10,300.

Consequently, the amount of money that remains after you buy the car—which represents your increase in purchasing power—is $200, or 2% of your initial investment. This is your real rate of return, as it represents the amount that you gained after accounting for the effects of inflation.

Markets vs Inflation indicators use in 1 months interval

SP:SPX , INDEX:BTCUSD , TVC:GOLD , TVC:DJI

(CD|RS) Caruso Divergence Relative StrengthCaruso Divergence Relative Strength (CD|RS) helps an investor to identify when a security does not make a lower low vs a benchmark. The standard application is to compare a stock to the S&P 500 (SPX). If the SPX makes a lower low and the stock does not, it displays significant Relative Strength.

This indicator allows you to select both your benchmark for comparing against as well as how far back to make the analysis by selecting the pivot lookback (how many prior ‘pivots’ or ‘market lows’ back to compare against).

Divergences can appear when markets are weak, and they make lower lows, but they can also appear in uptrends as stocks and indexes make higher highs. CD|RS also identifies when RS takes place “On Strength.” If the security and its benchmark both decline but the security can make new highs above its prior peak before the benchmark, it is once again displaying relative strength. Therefore CD|RS is helpful in finding Divergence Relative Strength in both up and down trends.

CD|RS works on any timeframe.

CD|RS has an accompanying indicator called CD|RS Signal which helps display the divergence in a different format and can be placed in a separate pane if the user wishes to keep the price chart clean.

[TTI] Ned Davis 3 day Price Thrust IndicatorThe NedDavis 3 Day Price Thrust Indicator

HISTORY AND CREDITS –––––––––––––––––––––––––––––––––––––––––––––––––––––––

The indicator is inspired by studies from Ned Davis' NDR Institutional Service. I have shared before the backtest of this indicator, and now have coded it for TradingView so that you can have it on your charts.

Link to idea here:

WHAT IT DOES ––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

Thrusts occur when the S&P 500 rises at least 1.5% for one day, at least 1.15% for a second day, and at least 1.5% on the third day. The record since 1970 is perfect one year later. However, the prior 18 cases, ending in 1938, only show 11 out of 18 profitable one year later.

HOW TO USE IT –––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

I use the indicator as a gauge tool, in other words it is a piece of the puzzle to justify bullish or bearish trades. I put this type of analysis in my secondary tools that give me additional confidence for market direction and aggressiveness in my trading

Newzage - Fed Net LiquidityThe Fed Net Liquidity indicator is a concept discovered by Max Anderson to calculate the fair value of SPX (S&P 500 Index).

The formula he shared on Twitter uses the Fed Balance Sheet, TGA (Treasury General Account), and Reverse Repo.

Net Liquidity = Fed Balance Sheet - (TGA + Reverse Repo)

The data for each component above is accessible on the FRED website.

Fed Balance Sheet fred.stlouisfed.org

Treasury General Account (TGA) fred.stlouisfed.org

Reverse Repo fred.stlouisfed.org

This script uses net liquidity (NL) fair value calculation for SPX, then estimates entry and next target exit target for both long and short trades on SPY.

The script added RSI oversold/overbought signal to the original NL signal from Max... improving the "precision" of the buy/sell signals.

The script also uses RSI to estimate targets based on how overbought or oversold the index/SPY is.

Williams Vix Fix ultra complete indicator (Tartigradia)Williams VixFix is a realized volatility indicator developed by Larry Williams, and can help in finding market bottoms.

Indeed, as Williams describe in his paper, markets tend to find the lowest prices during times of highest volatility, which usually accompany times of highest fear. The VixFix is calculated as how much the current low price statistically deviates from the maximum within a given look-back period.

Although the VixFix originally only indicates market bottoms, its inverse may indicate market tops. As masa_crypto writes : "The inverse can be formulated by considering "how much the current high value statistically deviates from the minimum within a given look-back period." This transformation equates Vix_Fix_inverse. This indicator can be used for finding market tops, and therefore, is a good signal for a timing for taking a short position." However, in practice, the Inverse VixFix is much less reliable than the classical VixFix, but is nevertheless a good addition to get some additional context.

For more information on the Vix Fix, which is a strategy published under public domain:

* The VIX Fix, Larry Williams, Active Trader magazine, December 2007, web.archive.org

* Fixing the VIX: An Indicator to Beat Fear, Amber Hestla-Barnhart, Journal of Technical Analysis, March 13, 2015, ssrn.com

* Replicating the CBOE VIX using a synthetic volatility index trading algorithm, Dayne Cary and Gary van Vuuren, Cogent Economics & Finance, Volume 7, 2019, Issue 1, doi.org

Created By ChrisMoody on 12-26-2014...

V3 MAJOR Update on 1-05-2014

tista merged LazyBear's Black Dots filter in 2020:

Extended by Tartigradia in 10-2022:

* Can select a symbol different from current to calculate vixfix, allows to select SP:SPX to mimic the original VIX index.

* Inverse VixFix (from masa_crypto and web.archive.org)

* VixFix OHLC Bars plot

* Price / VixFix Candles plot (Pro Tip: draw trend lines to find good entry/exit points)

* Add ADX filtering, Minimaxis signals, Minimaxis filtering (from samgozman )

* Convert to pinescript v5

* Allow timeframe selection (MTF)

* Skip off days (more accurate reproduction of original VIX)

* Reorganized, cleaned up code, commented out parts, commented out or removed unused code (eg, some of the KC calculations)

* Changed default Bollinger Band settings to reduce false positives in crypto markets.

Set Index symbol to SPX, and index_current = false, and timeframe Weekly, to reproduce the original VIX as close as possible by the VIXFIX (use the Add Symbol option, because you want to plot CBOE:VIX on the same timeframe as the current chart, which may include extended session / weekends). With the Weekly timeframe, off days / extended session days should not change much, but with lower timeframes this is important, because nights and weekends can change how the graph appears and seemingly make them different because of timing misalignment when in reality they are not when properly aligned.

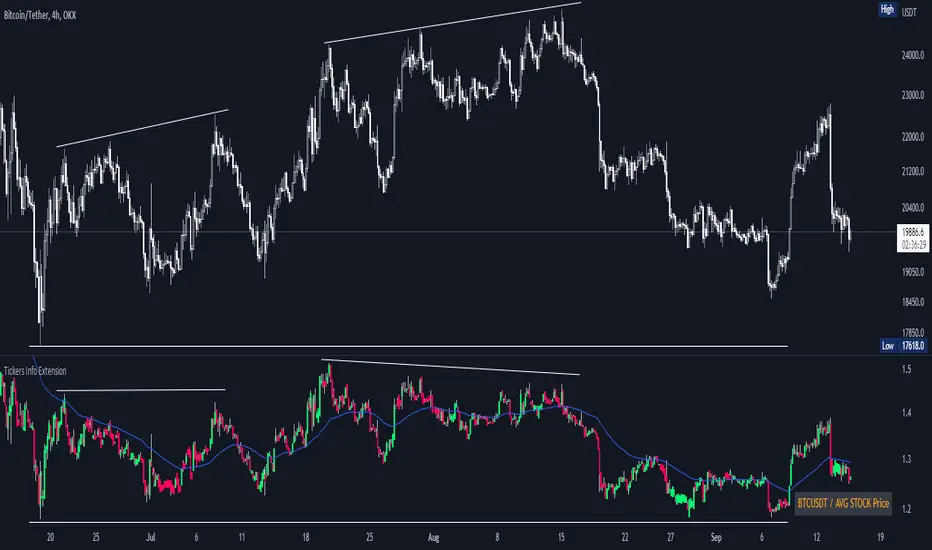

Tickers Info ExtensionWith the indicator you can easily evaluate or compare any ticker with the one you choose in the options.

You can choose any of the tickers I provide in the mod options to your liking :

XAU

DXY

BTC

ETH

SPX

NASDAQ

AVG Stable Dominance

AVG Stock Price

Custom

You can also select or create your own ticker if you select the Custom in Mode option.

If the Compare mode is enabled, then the current ticker you are viewing is divided by the ticker selected in the indicator (in the Mode option).

Thus, you create a new pair and can evaluate the strength of this or that asset.

For example, if you have the ticker BTCUSDT open. And the ticker XAU is selected in the Mode option in the indicator. And the Compare mode is also enabled. Then you will get a new BTCUSDT/XAU pair. That means that now you can see the bitcoin/gold ratio. (Same as EUR/USD etc.)

If the Compare option is switched off then you will see the usual ticker you choose in the Mode option. You can also see if there is a correlation between the selected pairs.

Option ' AVG STABLE.D ' = Calculated as: USDT.D + USDC.D + DAI.D

- This is the average domination of the most important Stable Coins

Option ' AVG STOCK Price ' = Calculated as: (DJI + SPX + NDQ) / 3

- This is the average price of the most important Indexes.

Auto Fibonacci Levels + Auto Trend Line generatorAnother indicator for you guys!!!

This indicator consists of the 5 key Fibonacci retracement levels, plotted automatically to user input settings. I also have included an auto support/resistance trend line generator.

What is a Fibonacci retracement?

'Fibonacci retracement is a method of technical analysis for determining support and resistance levels. It is named after the Fibonacci sequence of numbers, whose ratios provide price levels to which markets tend to retrace a portion of a move before a trend continues in the original direction.' - Wikipedia

How to use the Fibonacci retracement?

- The Fibonacci levels are default. These percentiles from price to the average of the high in a sample and low in a sample give you a guideline of where a bottom may be, where a top may be, and where a range is being created.

- Look for the price to reject from 61.8% and 76.4%, and also look for price to bounce from 38.2% and 23.6%. If a lower low/higher high is made, the fib levels will follow and the percentiles within will be recalculated after a 5 candle offset period.

- If you see price trending towards the lower percentiles (38&23) and using the 50% as resistance, look for a break downwards and vice versa.

-This Fibonacci set as all others is subject to fake-out, always use this with another series indicator, or don't use it as a signal for entry at all (unless you have a backdated strategy)

How to use the trend line generator?

-The trend line generator will only plot when a lower low/higher high has taken place within the input amount of candles. It is also offset by a user amount.

-The check box will give the option to have the trend line's plot or not.

- If you see a green/red dot it means that that will be your first coordinate for the trend line, and until the computations are complete it will give you an idea of which direction it will be in (resistance or support)

-When opening this indicator zoom out all the way to connect any trend lines that do not load automatically.

Let me know if you have any questions, suggestions or issues! Thank you everyone!

-Cheatcode1 :)

SP:SPX TVC:DXY BMFBOVESPA:EUR1! CME:BTC1! BINANCE:BTCUSDT

Rate Of Change Trend Strategy (ROC)This is very simple trend following or momentum strategy. If the price change over the past number of bars is positive, we buy. If the price change over the past number of bars is negative, we sell. This is surprisingly robust, simple, and effective especially on trendy markets such as cryptos.

Works for many markets such as:

INDEX:BTCUSD

INDEX:ETHUSD

SP:SPX

NASDAQ:NDX

NASDAQ:TSLA

Intraday Super SectorsMotivated by Cody to finish what I'd started ...

This indicator plots the two 'Super Sectors' (Cyclical and Defensive) intraday change, viz-a-viz SPX price

* for convenience, it uses the ETF's, rather than the actual sectors. This might make it 0.0001% inaccurate.

For reference:

Defensive Sectors:

XLE Energy (not always considered a true defensive sector, but I've thrown it in here for balance)

XLP Consumer Staples

XLU Utilities

XLV Health Care

Cyclical Sectors:

XLB Materials

XLC Communication Services

XLF Financials

XLI Industrials

XLK Information Technology

XLRE Real Estate

XLY Consumer Discretionary

Why the (soft) red/green cloud?

Well, the theory says is that if the Cyclical Sector is down, while the Defensive Sector is up, this isn't exactly bullish (so a soft red cloud), or if Defensive Stocks are down, while Cyclical Stocks are up, this is perhaps bullish.

Of course, if SPX is down 10%, with Defensive Stocks down 20%, and Cyclical Stocks down 5%, you might get a green cloud, but it ain't exactly a bullish sign

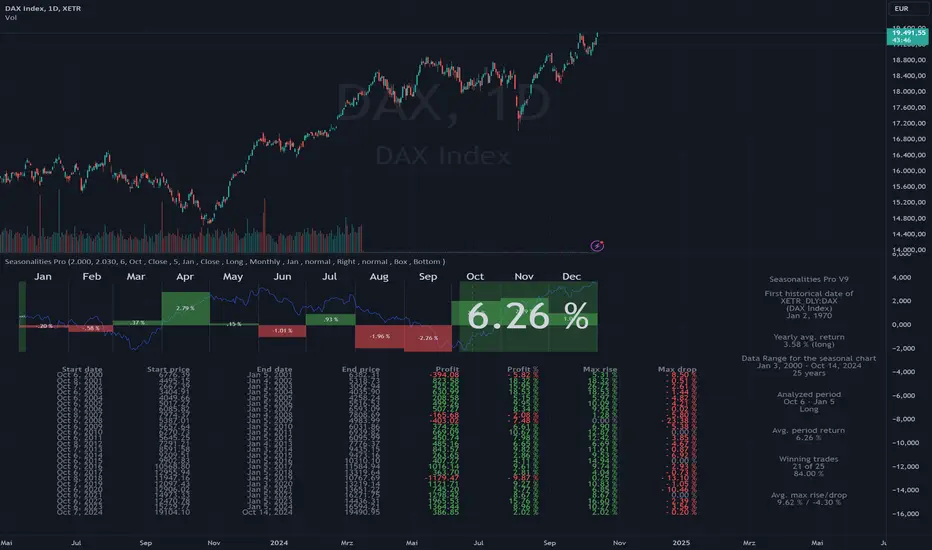

Seasonalities ProSeasonalities Pro indicator for TradingView - identify, evaluate and exploit seasonal patterns

Identification of seasonal investment opportunities

Easy to use without prior knowledge with just a few clicks

Statistical evaluation over an adjustable data basis (5 to 40 years)

Period to be considered also across year boundaries

Applicable to all instruments/symbols (indices, stocks, commodities, currencies, cryptos) that TradingView provides

Best price/performance ratio

Differences between Lite and Pro

Pro: Evaluation of all symbols available at TradingView up to 40 years in the past.

Lite: Like Pro, but only "DAX", "SPX" and "NDX" up to 40 years in the past, all other symbols 5 years.

Der Seasonalities Pro Indikator für TradingView – saisonale Muster erkennen, auswerten und nutzen

Identifizierung von saisonalen Investmentmöglichkeiten

Einfache Anwendung ohne Vorkenntnisse mit wenigen Klicks

Statistische Auswertung über eine einstellbare Datenbasis (5 bis 40 Jahre)

Zu betrachtende Periode auch über die Jahresgrenze hinweg

Anwendbar auf alle Instrumente/Symbole (Indizes, Aktien, Rohstoffe, Währungen, Cryptos) die TradingView zur Verfügung stellt

Bestes Preis-/Leistungsverhältnis

Unterschiede zwischen Lite und Pro

Pro: Auswertung aller bei TradingView verfügbaren Symbole bis zu 40 Jahre in die Vergangenheit

Lite: Wie Pro, jedoch nur "DAX", "SPX" und "NDX" bis zu 40 Jahre in die Vergangenheit, alle anderen Symbole 5 Jahre.

Seasonalities LiteSeasonalities Pro indicator for TradingView - identify, evaluate and exploit seasonal patterns

Identification of seasonal investment opportunities

Easy to use without prior knowledge with just a few clicks

Statistical evaluation over an adjustable data basis (5 to 40 years)

Period to be considered also across year boundaries

Applicable to all instruments/symbols (indices, stocks, commodities, currencies, cryptos) that TradingView provides

Best price/performance ratio

Differences between Lite and Pro

Pro: Evaluation of all symbols available at TradingView up to 40 years in the past.

Lite: Like Pro, but only "DAX", "SPX" and "NDX" up to 40 years in the past, all other symbols 5 years.

Der Seasonalities Pro Indikator für TradingView – saisonale Muster erkennen, auswerten und nutzen

Identifizierung von saisonalen Investmentmöglichkeiten

Einfache Anwendung ohne Vorkenntnisse mit wenigen Klicks

Statistische Auswertung über eine einstellbare Datenbasis (5 bis 40 Jahre)

Zu betrachtende Periode auch über die Jahresgrenze hinweg

Anwendbar auf alle Instrumente/Symbole (Indizes, Aktien, Rohstoffe, Währungen, Cryptos) die TradingView zur Verfügung stellt

Bestes Preis-/Leistungsverhältnis

Unterschiede zwischen Lite und Pro

Pro: Auswertung aller bei TradingView verfügbaren Symbole bis zu 40 Jahre in die Vergangenheit

Lite: Wie Pro, jedoch nur "DAX", "SPX" und "NDX" bis zu 40 Jahre in die Vergangenheit, alle anderen Symbole 5 Jahre.