Money Flow DivergenceThe Money Flow Divergence indicator is designed to help traders identify periods when there is a significant divergence between the growth of the U.S. M2 money supply and the S&P 500 index (SPX).

This divergence can provide insights into potential market turning points, making it a valuable tool for long-term investors and traders looking to capitalize on macroeconomic trends.

How It Works:

Data Sources:

S&P 500 Index (SPX) and U.S. M2 Money Supply.

Calculating Growth Rates:

SPX Growth: The script calculates the percentage growth of the S&P 500 index by comparing the current closing price with the previous period's closing price.

M2 Growth: Similarly, it calculates the percentage growth of the U.S. M2 money supply by comparing the current value with the previous period's value.

Growth Gap/Delta:

Growth Gap: The core of the indicator is the "growth gap" or "delta," which is the difference between the M2 money supply growth and the SPX growth. This gap indicates whether liquidity in the economy (represented by M2) is outpacing or lagging behind the performance of the stock market.

Interpretation:

Positive Gap (Green Bars): When the M2 growth outpaces SPX growth, the gap is positive, indicating that there is more liquidity in the system than what is being reflected in the stock market. This scenario often signals potential upward momentum in the market, making it a good time to consider buying.

Negative Gap (Red Bars): When the SPX growth outpaces M2 growth, the gap is negative, suggesting that the market may be overextended relative to the available liquidity. This can be a warning sign of potential market corrections or downturns.

Visualization:

The indicator plots the growth gap as a histogram with bars colored based on the gap value:

Green Bars: Indicate a positive gap where M2 growth is higher than SPX growth.

Red Bars: Indicate a negative gap where SPX growth is higher than M2 growth.

The bars are thickened for better visibility, and a horizontal line at zero is plotted to help users easily distinguish between positive and negative gaps.

How To Use It:

Time Frame Selection: Users can select the desired time frame (e.g., monthly, weekly) for the data. This flexibility allows traders to analyze the indicator over different periods, depending on their investment horizon.

Monthly time frames seem to work best.

Interpreting the Indicator:

Bullish Signals: Look for sustained periods of positive growth gaps (green bars), which may indicate a favorable environment for buying or holding long positions.

Bearish Signals: Be cautious during periods of negative growth gaps (red bars), which could signal overvaluation in the market or potential pullbacks.

Enjoy and let me know if you have any questions.

Cerca negli script per "spx"

Enio_SPX_Accumulation/DistributionThis indicator handles the same inputs used for classic Accumulation and Distribution indicators, but performs the calculations in a different way.

This indicator is used to compare the positive volume (up volume) and the number of advancing stocks against the negative volume (down volume) and the number of declining stocks.

This indicator only measures SPX market breadth (Advancing issues, Declining issues) and SPX volume (Up and down volume)so it is for use only with SPX, SPY or MES. It can also be used with ES, but data outside of regular trading hours is not provided, the indicator in those cases will print a block of the same height and same color as the last RTH bar.

When the histogram is positive or green, the bars change to a lighter color if the current bar is less than the average of the last 3 bars. A continued set of bars with a lighter color could mean that the trend is about to change.

When the histogram is negative or red, the bars change to a lighter color if the current bar is greater than the average of the last 3 bars. A continued set of bars with a lighter color could mean that the trend is about to change.

When the histogram height is low, could signal a choppy market (SPX).

The histogram can help indicate a trending market when the opening trend is maintained and the color of the bars does not change, for example, a solid green increasing histogram can indicate a bullish trending market, while a solid red decreasing histogram will indicate a strong bearish trend.

In intraday trading the indicator can signal if the SPX price changes are supported by volume and market breadth and also allows you to see when these changes or trend are weakening.

The change from green (positive) to red (negative) and vice versa should not be taken alone as a buy/sell signal but as a confirmation of signals from other indicators you trust.

Due to the great specific weight that some stocks have within the SPX price calculation, the divergences of this indicator with SPX, can be taken as warning signals, but should not become an element of trading decisions. . You could see a negative histogram while SPX is positive and vice versa.

Max Value Gap [MOT]📊 Max Value Gap — Intraday Fill Zones + Stats Dashboard

Max Value Gap is a real-time gap fill detection system that visualizes institutional-style intraday price inefficiencies on major indices like SPX and NDX. Built for scalpers and short-term traders, it helps identify prime reversal areas where price is likely to return — often within the same session.

This script tracks U.S. regular market hour gaps only (9:30 AM to 4:00 PM ET) and is designed for high-precision execution on the 1-minute chart.

🧠 What Is an SPX Intraday Gap?

An SPX intraday gap occurs when the market creates a void between candles due to rapid price movement — often following volatility spikes, liquidation breaks, or aggressive buyer/seller imbalances. These unfilled zones act like magnetic targets, drawing price back into them as liquidity rebalances.

Unlike overnight gaps, these are formed and resolved within the same session, making them ideal for intraday strategies.

🔍 Key Features

✅ 1. Automatic Gap Detection

Scans only during official U.S. equity market hours (9:30 AM – 4:00 PM EST)

Gap Up: A green candle opens above the previous high

Gap Down: A red candle opens below the previous low

Each valid gap is outlined using colored boxes:

🟩 Green Box = Gap Up

🟥 Red Box = Gap Down

📸 Image : Chart with both green and red boxes marking gaps on SPX.

✅ 2. Dynamic Gap Zone Tracking

Once a gap is identified, the box extends forward until price fills the zone

A gap is considered filled when:

Price trades back into the gap zone

For gap ups: price crosses below the bottom of the gap

For gap downs: price crosses above the top of the gap

Users have the option to auto-delete filled boxes for clarity

📸 Image: Chart with price re-entering and completing a gap fill with box extending only until that point.

✅ 3. Real-Time Statistics Table

Located in the bottom-right of your chart, the built-in dashboard shows:

Total gaps formed

Gaps filled intraday

Gaps filled same day

Percentages of successful fills

📸 Image: Picture of statistics table

This live table helps assess whether the current day’s gaps are behaving in line with historical probabilities — no guesswork required.

🔄 Futures Execution Strategy

While the gaps are plotted on the SPX (or index) chart, the actual trades are taken on MNQ, NQ, or ES, using the gap levels as entry targets.

Sample Trading Flow:

A gap down forms on SPX at 1:45 PM (EST)

Price starts showing reversal signs back toward the gap

Enter long MNQ or NQ targeting a move into the gap zone

Take profit once price fully fills the zone

Repeat throughout the session — trend or chop, gaps are a magnet

This method mirrors institutional mean reversion techniques, capitalizing on market inefficiencies without chasing momentum.

📸 SPX Gap Being Filled with Corresponding MNQ Move Overlay

✅ Best Practices

Works best during morning session volatility (9:30–11:30 AM ET)

Combine with reversal candles or momentum tools for high-quality entries

Avoid during low-volume lunch chop unless tracking larger gap zones

Use on SPX while executing trades on MNQ/NQ/ES

⚠️ Disclaimer

This script is provided for educational and informational purposes only. It does not offer investment advice or trade signals. Past performance does not guarantee future results. Use appropriate risk management. Redistribution or resale is strictly prohibited.

Combined EMA Technical AnalysisThis script is written in Pine Script (version 5) for TradingView and creates a comprehensive technical analysis indicator called "Combined EMA Technical Analysis." It overlays multiple technical indicators on a price chart, including Exponential Moving Averages (EMAs), VWAP, MACD, PSAR, RSI, Bollinger Bands, ADX, and external data from the S&P 500 (SPX) and VIX indices. The script also provides visual cues through colors, shapes, and a customizable table to help traders interpret market conditions.

Here’s a breakdown of the script:

---

### **1. Purpose**

- The script combines several popular technical indicators to analyze price trends, momentum, volatility, and market sentiment.

- It uses color coding (green for bullish, red for bearish, gray/white for neutral) and a table to display key information.

---

### **2. Custom Colors**

- Defines custom RGB colors for bullish (`customGreen`), bearish (`customRed`), and neutral (`neutralGray`) signals to enhance visual clarity.

---

### **3. User Inputs**

- **EMA Colors**: Users can customize the colors of five EMAs (8, 20, 9, 21, 50 periods).

- **MACD Settings**: Adjustable short length (12), long length (26), and signal length (9).

- **RSI Settings**: Adjustable length (14).

- **Bollinger Bands Settings**: Length (20), multiplier (2), and proximity threshold (0.1% of band width).

- **ADX Settings**: Adjustable length (14).

- **Table Settings**: Position (e.g., "Bottom Right") and text size (e.g., "Small").

---

### **4. Indicator Calculations**

#### **Exponential Moving Averages (EMAs)**

- Calculates five EMAs: 8, 20, 9, 21, and 50 periods based on the closing price.

- Used to identify short-term and long-term trends.

#### **Volume Weighted Average Price (VWAP)**

- Resets daily and calculates the average price weighted by volume.

- Color-coded: green if price > VWAP (bullish), red if price < VWAP (bearish), white if neutral.

#### **MACD (Moving Average Convergence Divergence)**

- Uses short (12) and long (26) EMAs to compute the MACD line, with a 9-period signal line.

- Displays "Bullish" (green) if MACD > signal, "Bearish" (red) if MACD < signal.

#### **Parabolic SAR (PSAR)**

- Calculated with acceleration factors (start: 0.02, increment: 0.02, max: 0.2).

- Indicates trend direction: green if price > PSAR (bullish), red if price < PSAR (bearish).

#### **Relative Strength Index (RSI)**

- Measures momentum over 14 periods.

- Highlighted in green if > 70 (overbought), red if < 30 (oversold), white otherwise.

#### **Bollinger Bands (BB)**

- Uses a 20-period SMA with a 2-standard-deviation multiplier.

- Color-coded based on price position:

- Green: Above upper band or close to it.

- Red: Below lower band or close to it.

- Gray: Neutral (within bands).

#### **Average Directional Index (ADX)**

- Manually calculates ADX to measure trend strength:

- Strong trend: ADX > 25.

- Very strong trend: ADX > 50.

- Direction: Bullish if +DI > -DI, bearish if -DI > +DI.

#### **EMA Crosses**

- Detects bullish (crossover) and bearish (crossunder) events for:

- EMA 9 vs. EMA 21.

- EMA 8 vs. EMA 20.

- Visualized with green (bullish) or red (bearish) circles.

#### **SPX and VIX Data**

- Fetches daily closing prices for the S&P 500 (SPX) and VIX (volatility index).

- SPX trend: Bullish if EMA 9 > EMA 21, bearish if EMA 9 < EMA 21.

- VIX levels: High (> 25, fear), Low (< 15, stability).

- VIX color: Green if SPX bullish and VIX low, red if SPX bearish and VIX high, white otherwise.

---

### **5. Visual Outputs**

#### **Plots**

- EMAs, VWAP, and PSAR are plotted on the chart with their respective colors.

- EMA crosses are marked with circles (green for bullish, red for bearish).

#### **Table**

- Displays a summary of indicators in a customizable position and size.

- Indicators shown (if enabled):

- EMA 8/20, 9/21, 50: Green dot if bullish, red if bearish.

- VWAP: Green if price > VWAP, red if price < VWAP.

- MACD: Green if bullish, red if bearish.

- MACD Zero: Green if MACD > 0, red if MACD < 0.

- PSAR: Green if price > PSAR, red if price < PSAR.

- ADX: Arrows for very strong trends (↑/↓), dots for weaker trends, colored by direction.

- Bollinger Bands: Arrows (↑/↓) or dots based on price position.

- RSI: Numeric value, colored by overbought/oversold levels.

- VIX: Numeric value, colored based on SPX trend and VIX level.

---

### **6. Alerts**

- Triggers alerts for EMA 8/20 crosses:

- Bullish: "EMA 8/20 Bullish Cross on Candle Close!"

- Bearish: "EMA 8/20 Bearish Cross on Candle Close!"

---

### **7. Key Features**

- **Flexibility**: Users can toggle indicators on/off in the table and adjust parameters.

- **Visual Clarity**: Consistent use of green (bullish), red (bearish), and neutral colors.

- **Comprehensive**: Combines trend, momentum, volatility, and market sentiment indicators.

---

### **How to Use**

1. Add the script to TradingView.

2. Customize inputs (colors, lengths, table position) as needed.

3. Interpret the chart and table:

- Green signals suggest bullish conditions.

- Red signals suggest bearish conditions.

- Neutral signals indicate indecision or consolidation.

4. Set up alerts for EMA crosses to catch trend changes.

This script is ideal for traders who want a multi-indicator dashboard to monitor price action and market conditions efficiently.

CNN Fear and Greed Index JD modified from minusminusCNN Fear and Greed Index - www.cnn.com

Modified from minusminus -

See Documentation from CNN's website

CNN's Fear and Greed index is an attempt to quantitatively score the Fear and Greed in the SPX using 7 factors:

Market Momentum- S&P 500 (SPX) and its 125-day moving average

Stock Price Strength -Net new 52-week highs and lows on the NYSE

Stock Price Breadth - McClellan Volume Summation Index

Put and Call options - 5-day average put/call ratio

Market Volatility - VIX and its 50-day moving average

Safe Haven Demand - Difference in 20-day stock and bond returns

Junk Bond Demand - Yield spread: junk bonds vs. investment grade

Each Factor has a weight input for the final calculation initially set to a weight of 1. The final calculation of the index is a weighted average of each factor.

3 Factors have separate functions for calculation : See Code for Clarity

SPX Momentum : difference between the Daily CBOE:SPX index value and it's 125 Day Simple moving average.

Stock Price Strength : Net New 52-week highs and lows on the NYSE.

Function calculates a measure of Net New 52-week highs by:

NYSE 52-week highs (INDEX:MAHN) - all new NYSE Highs (INDEX:HIGH)

measure of Net New 52-week lows by:

NYSE 52-week lows (INDEX:MALN) - all new NYSE Lows (INDEX:LOWN)

Then calculate a ratio of Net New 52-week Highs and Lows over Total Highs and Lows then takes a 5-day moving average of that ratio-See Code

Stock Price Breadth is the McClellan Volume Summation Index :

First Calculate the McClellan Oscillator

Second Calculate the Summation Index

4 Factors are Straight data requests

5 Day Simple Moving Average of the Put-Call Ratio on SPY

50 Day Simple Moving Average of the SPX VIX

Difference between 20 Day Simple Moving Average of SPX Daily Close and 20 Day Simple Moving Average of 10Y Constant Maturity US Treasury Note

Yield Spread between ICE BofA US High Yield Index and ICE BofA US Investment Grade Corporate Yield Index

The Fear and Greed Index is a weighted average of these factors - which is then normalized to scale from 0 to 100 using the past 25 values - length parameter.

3 Zones are Shaded: Red for Extreme Fear, Grey for normal jitters, Green for Extreme Greed.

Disclaimer: This is not financial advice. These are just my ideas, and I am not an investment advisor or investment professional. This code is for informational purposes only and do your own analysis before making any investment decisions. This is an attempt to replicate in spirt an index CNN publishes on their website and in no way shape or form infringes on their content, calculations or proprietary information.

From CNN: www.cnn.com

FEAR & GREED INDEX FAQs

What is the CNN Business Fear & Greed Index?

The Fear & Greed Index is a way to gauge stock market movements and whether stocks are fairly priced. The theory is based on the logic that excessive fear tends to drive down share prices, and too much greed tends to have the opposite effect.

How is Fear & Greed Calculated?

The Fear & Greed Index is a compilation of seven different indicators that measure some aspect of stock market behavior. They are market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility, and safe haven demand. The index tracks how much these individual indicators deviate from their averages compared to how much they normally diverge. The index gives each indicator equal weighting in calculating a score from 0 to 100, with 100 representing maximum greediness and 0 signaling maximum fear.

How often is the Fear & Greed Index calculated?

Every component and the Index are calculated as soon as new data becomes available.

How to use Fear & Greed Index?

The Fear & Greed Index is used to gauge the mood of the market. Many investors are emotional and reactionary, and fear and greed sentiment indicators can alert investors to their own emotions and biases that can influence their decisions. When combined with fundamentals and other analytical tools, the Index can be a helpful way to assess market sentiment.

Global Market Pulse + [Combined]The Global Market Pulse + is a multi-functional analytical tool designed for traders and investors working with cryptocurrencies, stocks, and macroeconomic assets. It integrates 7 independent analytical modules into a single script, providing a comprehensive market assessment.

Operating Modes

1️⃣ Crypto Mode

Function: Monitors the crypto market health by analyzing:

Altcoin market capitalization (excluding BTC)

Bitcoin and Ethereum dominance shifts

Trading volume dynamics

Output: Pulse line (0-100 scale) with:

Accumulation Zone (Bullish)

Distribution Zone (Bearish)

2️⃣ Equity Mode

Function: Tracks traditional markets via:

S&P 500 (SPX) momentum

US Dollar Index (DXY) trends

Gold/Silver ratio

Use Case: Identifies "risk-on/risk-off" periods affecting crypto.

3️⃣ Correlation Mode

Function: Calculates BTC's correlation with:

SPX | Gold | Oil | Custom assets (user-defined)

Thresholds:

+0.7+ Strong positive correlation

-0.7- Inverse correlation

4️⃣ Altseason Mode

Function: Detects altcoin investment opportunities using:

Altcoin Dominance Oscillator

Custom OB/OS levels

Signals:

Buy: Oversold + Volume spike

Sell: Overbought + Volume drop

5️⃣ Cycle Mode

Function:

Auto-detects market cycle lengths

Predicts future turning points

Features:

Adaptive timeframe-based settings

Anomaly detection (deviations from mean)

6️⃣ RSX-MACD Mode

Function: Hybrid momentum indicator combining:

RSX (smoothed RSI)

Classic MACD logic

Advantage: Reduced false signals vs traditional MACD.

7️⃣ Dual-RSX Mode

Function: Dual-speed RSX indicator with:

Fast line (short-term)

Slow line (long-term)

Key Features

Adaptive Logic: Auto-adjusts parameters based on:

Selected timeframe (M1 - Weekly)

Market type (Crypto/Stocks)

Multi-Timeframe Analysis: Processes higher timeframe data on any chart.

Custom Assets: Add any ticker for correlation studies.

Visual Alerts: Color-coded signals for quick interpretation.

Usage Recommendations

For Crypto Traders:

Combine Crypto + Altseason modes for altcoin timing.

Use Correlation to filter macro risks.

Stock Investors:

Equity + Cycle modes for SPX/gold entry points.

Algorithmic Trading:

RSX-MACD/Dual-RSX provide ready-made conditions for bots.

⚠ Disclaimer: Educational tool only. Always confirm signals with additional analysis.

Global Market Pulse + — это многофункциональный инструмент для анализа крипторынка, акций и макроактивов. Он объединяет 7 независимых модулей в одном скрипте.

Режимы работы

1️⃣ Crypto (Крипторынок)

Анализ:

Капитализация альткоинов (без BTC)

Доминирование BTC/ETH

Объемы торгов

Сигналы:

Аккумуляция (бычья зона)

Дистрибуция (медвежья зона)

2️⃣ Equity (Фондовый рынок)

Анализ:

Динамика S&P 500 (SPX)

Индекс доллара (DXY)

Соотношение золото/серебро

Применение: Определение "risk-on/risk-off" периодов.

3️⃣ Correlation (Корреляции)

Анализ: Корреляция BTC с:

SPX | Золото | Нефть | Пользовательскими активами

Пороги:

+0.7+ Сильная прямая связь

-0.7- Обратная корреляция

4️⃣ Altseason (Альтсезон)

Анализ:

Осциллятор доминирования альткоинов

Уровни перекупленности/перепроданности

Сигналы:

Покупка: Перепроданность + рост объемов

Продажа: Перекупленность + падение объемов

5️⃣ Cycle (Циклы)

Функции:

Автовыявление длительности циклов

Прогноз точек разворота

Особенности:

Автоподстройка под таймфрейм

Детекция аномалий

6️⃣ RSX-MACD

Особенности: Гибрид RSX (сглаженный RSI) и MACD.

Преимущество: Меньше ложных сигналов.

7️⃣ Dual-RSX

Функция: Двойной RSX с:

Быстрой линией (краткосрок)

Медленной линией (долгосрок)

Уровни: 20 (перепрод.) / 50 (центр) / 80 (перекуп.)

Ключевые особенности

Автоподстройка под таймфрейм и тип рынка.

Мультитаймфрейм-анализ на любом графике.

Кастомизация: Добавление любых активов для корреляций.

Визуальные сигналы: Цветовая индикация состояний.

Рекомендации по использованию

Криптотрейдерам:

Комбинация Crypto + Altseason для торговли альткоинами.

Correlation для учета макрорисков.

Инвесторам:

Equity + Cycle для точек входа в SPX/золото.

Алготрейдинг:

RSX-MACD/Dual-RSX как условия для торговых роботов.

⚠ Важно: Инструмент для анализа. Не является торговой рекомендацией.

Rule Of 20 - Fair Value Estimation by Inflation & Earnings (TG)The Rule Of 20 is a heuristic calculation to find the fair value of an asset or market given its earnings and current inflation.

Its calculation is straightforward: the fair multiple of the price or price-to-earnings ratio of a stock should be 20 minus the rate of inflation.

In math terms: fair_price-to-earnings_ratio = (20 - inflation) ; fair_value = current_price * fair_price-to-earnings_ratio / real_price-to-earnings_ratio

For example, if a stock or index was trading on 11 times earnings and inflation was 2%, then the theory would be that the fair price-to-earnings ratio would be 20-2 = 18, which is much higher than the real price-to-earnings ratio of 11, and hence the asset would be undervalued.

Conversely, a market or company that was trading on 18 times price-to-earnings ration when inflation was 8% was seen as overvalued, because of the fair price-to-earnings ratio being 20-8=12, hence much lower than the real price-to-earnings ratio of 18.

We can then project the delta between the fair PE and real PE onto the asset's value to obtain the projected fair value, which may be a target of future value the asset may reach or hover around.

For example, as of 1st November 2022, SPX stood at 3871.97, with a PE ratio of 20.14 and an inflation in the US of 7.70. Using the Rule Of 20, we find that the fair PE ratio is 20-7.7=12.3, which is much lower than the current PE ratio of 20.14 by 39%! This may indicate a future possibility of a further downside risk by 39% from current valuation levels.

The origins of this rule are unknown, although the legendary US fund manager Peter Lynch is said to have been an active proponent when he was directing the Fidelity’s Magellan fund from 1977 to 1990.

For more infos about the Rule Of 20, reading this article is recommended: www.sharesmagazine.co.uk

This indicator implements the Rule Of 20 on any asset where the Financials are availble to TradingView, and also for the entire SP:SPX index as a way to assess the wider US stock market. Technically, the calculation is a bit different for the latter, as we cannot access earnings of SPX through Financials on TradingView, so we access it using the QUANDL:MULTPL/SP500_PE_RATIO_MONTH ticker instead.

By default are displayed:

current asset value in red

fair asset value according to the Rule Of 20 in white for SPX, or different shades of purple/maroon for other assets. Note that for SPX there is only one calculation, whereas for other assets there are multiple different ways to calculate earnings, so different fair values can be computed.

fair price-to-earnings ratio (PE ratio) in light grey.

real price-to-earnings ratio in darker grey.

This indicator can be used on SP:SPX ticker, and on most NASDAQ:* tickers, since they have Financials integrated in TradingView. Stocks tickers from other exchanges may not provide Financials data, so this indicator won't work then. If this happens, try to find the same ticker on NASDAQ instead.

Note that by default, only the US stock market is considered. If you want to consider stocks or assets in other regions of the world, please change the inflation ticker to a ticker that reflect the target region's inflation.

Also adding a table to ease interpretation was considered, but then the Timeframe MTF parameter would not work, and since the big advantage of this indicator is to allow for historical comparisons, the table was dropped.

Enjoy, and keep in mind that all models are wrong, but some are useful.

Trade safely!

TG

Price Correction to fix data manipulation and mispricingPrice Correction corrects for index and security mispricing to the extent possible in TradingView on both daily and intraday charts. Price correction addresses mispricing issues for specific securities with known issues, or the user can build daily candles from intraday data instead of relying on exchange reported daily OHLC prices, which can include both legitimate special auction and off-exchange trades or illegitimate mispricing. The user can also detect daily OHLC prices that don’t reflect the intraday price action within a specified percent deviation. Price Correction functions as normal candles or bars for any time frame when correction is not needed.

On the 4th of October 2022, the AMEX exchange, owned by the New York Stock Exchange, decided to misprice the daily OHLC data for the SPY, the world’s largest ETF fund. The exchange eliminated the overnight gap that should have occurred in the daily chart that represents regular trading hours by showing a wick connecting near the close of the previous day. Neither the SPX, the SP500 cash index that the SPY ETF tracks, nor other SPX ETFs such as VOO or IVV show such a wick because significant price action at that level never occurred. The intraday SPY chart never shows the price drop below 372.31 that day, but there is a wick that extends to 366.57. On the 6th of October, they continued this practice of using a wick that connects with the close of the previous day to eliminate gaps in daily price action. The objective of this indicator is to fix such inconsistent mispricing practices in the SPY, NYA, and other indices or securities.

Price Correction corrects for the daily mispricing in the SPY to agree with the price action that actually occurred in the SPX index it tracks, as well as the other SPX ETFs, by using intraday data. The chart below compares the Price Correction of the SPY (top) to the SPX (middle) and the original mispriced SPY (bottom) with incorrect wicks. Price correction (top) removes those incorrect wicks (bottom) to match the SPX (middle).

The daily mispricing of the SPY follows after the successful deployment of the NYSE Composite Index mispricing, NYA, an index that represents all common stocks within the New York Stock Exchange, the largest exchange in the world. The importance of the NYA should not be understated. It is the price counterpart to NYSE’s market internals or statistics. Beginning in 2021, the New York Stock Exchange eliminated gaps in daily OHLC data for the NYA by using the close of the previous day as the open for the following day, in violation of their own NYSE Index Series Methodology. The Methodology states for the opening price that “The first index level is calculated and published around 09:30 ET, when the U.S. equity markets open for their regular trading session. The calculation of that level utilizes the most updated prices available at that moment.” You can verify for yourself that this is simply not the case. The first update of the NYA price for each day matches the close of the previous day, not the “most updated prices available at that moment”, causing data providers to often represent the first intraday bar with a huge sudden price change when an overnight price change occurred instead. For example, on 13 Jun 2022, TradingView shows a one-minute bar drop 2.3%. With a market capitalization of roughly 23 trillion dollars, the NYSE composite capitalization did not suddenly drop a half-trillion dollars in just one minute as the intraday chart data would have you believe. All major US indices, index ETFs, and even foreign indices like the Toronto TAX, the Australian ASXAL, the Bombay SENSEX, and German DAX had down gaps that day, except for the mispriced NYSE index. Price Correction corrects for this mispricing in daily OHLC data, as shown in the main chart at the top of this page comparing the original NYA (top) to the Price Corrected NYA (bottom).

Price Correction also corrects for the intraday mispricing in the NYA. The chart below shows how the Price Correction (top) replaces the incorrect first one-minute candles with gaps (bottom) from 22 Sep 2022 to 29 Sep 2022. TradingView is inconsistent in how intraday data is reported for overnight gaps by sometimes connecting the first intraday bar of the day to the close of the previous day, and other times not. This inconsistency may be due to manually changing the intraday data based on user support tickets. For example, after reporting the lack of a major gap in the NYA daily OHLC prices that existed intraday for 13 Jun 2022, TradingView opted to remove the true gap in intraday prices by creating a 2.3% half-a-trillion-dollar one-minute bar that connected the close of the previous day to show a sudden drop in price that didn’t occur, instead of adding the gap in the daily OHLC data that actually took place from overnight price action.

Price Correction allows users to detect daily OHLC data that does not reflect the intraday price action within a certain percent difference by changing the color of those candles or bars that deviate. The chart below clearly shows the start of the NYSE disinformation campaign for NYA that started in 2021 by painting blue those candles with daily OHLC values that deviated from the intraday values by 0.1%. Before 2021, the number of deviating candles is relatively sparse, but beginning in 2021, the chart is littered with deviating candles.

If there are other index or security mispricing or data issues you are aware of that can be incorporated into Price Correction, please let me know. Accurate financial data is indispensable in making accurate financial decisions. Assert your right to accurate financial data by reporting incorrect data and mispricing issues.

How to use the Price Correction

Simply add this “indicator” to your chart and remove the mispriced default candles or bars by right clicking on the chart, selecting Settings, and de-selecting Body, Wick, and Border under the Symbol tab. The Presets settings automatically takes care of mispricing in the NYA and SPY to the extent possible in TradingView. The user can also build their own daily candles based off of intraday data to address other securities that may have mispricing issues.

MenthorQ Levels ConversionLevels Conversion helps traders accurately overlay price levels from spot/index ETFs and indices (like SPX, SPY, QQQ, NDX) onto futures charts (like ES, NQ, etc.).

Because futures and spot/index prices don’t trade at the same price, your levels will be misaligned if you plot them directly. Futures typically trade at a spread or ratio versus their related index/ETF. This indicator solves that by calculating the conversion ratio automatically, so your levels stay aligned on the futures chart.

How it works

This script calculates the ratio between Asset A and Asset B and applies it to convert levels from one instrument to the other (for example, SPX → ES, QQQ → NQ).

Ratio options (3 modes)

You can choose one of three ratio sources:

✅ T1 Ratio (Morning Snapshot)

Select a specific time to “lock” the ratio.

Default: 10:00 AM ET (morning session snapshot)

✅ T2 Ratio (Afternoon Snapshot)

Select a second time to “lock” the ratio.

Default: 3:30 PM ET (afternoon snapshot)

✅ Last Price Ratio (Live)

Uses the last traded price of both assets to compute the ratio.

Note: To refresh the “Last Price” baseline, simply remove and re-add the indicator.

Learn more about Levels Conversions: menthorq.com

Common levels conversions

Some popular use-cases include:

- SPX Gamma Levels → ES

- SPY Gamma Levels → ES

- QQQ Gamma Levels → NQ

- NDX Gamma Levels → NQ

- SPX Intraday Gamma Levels → ES

- QQQ Intraday Gamma Levels → NQ

- SPX Swing Trading Levels → ES

- QQQ Swing Trading Levels → NQ

- GLD Levels → GC

- DIA Levels → YM

- USO Levels → CL

- NVDA / MAG7 Levels → QQQ

Fabian Z-ScoreFabian Z-Score — % Distance & Z-Scores for SPX / DJI / XLU

What it does

This indicator measures how far three market proxies are from a moving average and standardizes those distances into z-scores so you can spot stretch/mean-reversion and relative out/under-performance.

Universe: S&P 500 (SPX), Dow Jones (DJI) and Utilities (XLU). You can change any of these in Inputs.

Anchor MA: user-selectable MA type (SMA/EMA/RMA/WMA/VWMA/HMA/LSMA/ALMA) and length (default 39; a popular weekly anchor).

Outputs

% from MA: 100 × (𝐶𝑙𝑜𝑠𝑒 − 𝑀𝐴) / 𝑀𝐴

Time-series Z: z-score of the last N % distances (default 39) → “how stretched vs its own history?”

Cross-sectional Z: z-score of each % distance within the trio on this bar → “who’s strongest vs the others right now?”

A compact mini table (top-right) shows the latest values for each symbol: % from MA, Z(ts) and Z(xsec).

Panels & Visualization

Toggle what you want to see in View:

Plot % distance — raw % above/below the MA (0% line shown).

Plot time-series Z — standardized stretch with ±Threshold guides (default ±2σ).

Plot cross-sectional Z — relative z across SPX, DJI, XLU (0 = at the trio’s mean).

Smoothing — optional light MA on the plotted series (set to 1 for none).

A price-panel Moving Average is drawn with your chosen type/length for visual context.

Colors: SPX = teal, DJI = orange, XLU = purple.

Alerts

Two built-in alert conditions (time-series Z only):

“Z(ts) crosses up +Thr” — any of the three crosses above +Threshold.

“Z(ts) crosses down -Thr” — any crosses below −Threshold.

When enabled, the chart background tints faint green (up cross) or red (down cross) on those bars.

How to use (ideas, not advice)

On weekly charts, a 39-length MA/Z lookback often captures major risk-on/off swings. (Fabian Timing)

Deep negative Z(ts) (e.g., ≤ −2σ or −3σ) frequently accompanies panic and mean-reversion setups.

High positive Z(ts) suggests over-extension; watch for momentum fades.

Cross-sectional Z helps rank leadership today:

Z(xsec) > 0 → stronger than the trio’s mean this bar; Z(xsec) < 0 → weaker.

Utilities (XLU) turning positive x-sec while the others are negative can hint at defensive rotation.

If all 3 are above 0, go long, if below 0 go cash.

Combine: look for extreme Z(ts) aligning with lead/lag Z(xsec) to time entries/exits or hedges.

Inputs (quick reference)

Symbols: SPX / DJI / XLU (editable).

MA type & length: SMA, EMA, RMA, WMA, VWMA, HMA, LSMA, ALMA; default EMA(39).

Z-score lookback (ts): default 39.

Smoothing on plots: default 1 (off).

Z threshold (±): default 2.0 (guide lines & alerts).

Money Flow Divergence IndicatorOverview

The Money Flow Divergence Indicator is designed to help traders and investors identify key macroeconomic turning points by analyzing the relationship between U.S. M2 money supply growth and the S&P 500 Index (SPX). By comparing these two crucial economic indicators, the script highlights periods where market liquidity is outpacing or lagging behind stock market growth, offering potential buy and sell signals based on macroeconomic trends.

How It Works

1. Data Sources

S&P 500 Index (SPX500USD): Tracks the stock market performance.

U.S. M2 Money Supply (M2SL - Federal Reserve Economic Data): Represents available liquidity in the economy.

2. Growth Rate Calculation

SPX Growth: Percentage change in the S&P 500 index over time.

M2 Growth: Percentage change in M2 money supply over time.

Growth Gap (Delta): The difference between M2 growth and SPX growth, showing whether liquidity is fueling or lagging behind market performance.

3. Visualization

A histogram displays the growth gap over time:

Green Bars: M2 growth exceeds SPX growth (potential bullish signal).

Red Bars: SPX growth exceeds M2 growth (potential bearish signal).

A zero line helps distinguish between positive and negative growth gaps.

How to Use It

✅ Bullish Signal: When green bars appear consistently, indicating that liquidity is outpacing stock market growth. This suggests a favorable environment for buying or holding positions.

❌ Bearish Signal: When red bars appear consistently, meaning stock market growth outpaces liquidity expansion, signaling potential overvaluation or a market correction.

Best Timeframes for Analysis

This indicator works best on monthly timeframes (M) since it is designed for long-term investors and macro traders who focus on broad economic cycles.

Who Should Use This Indicator?

📈 Long-term investors looking for macroeconomic trends.

📊 Swing traders who incorporate liquidity analysis in their strategies.

💰 Portfolio managers assessing market liquidity conditions.

🚀 Use this indicator to stay ahead of market trends and make informed investment decisions based on macroeconomic liquidity shifts! 🚀

GEX Profile [PRO] Real Auto-Updated Gamma Exposure Levels𝗥𝗲𝗮𝗹 𝗚𝗘𝗫 𝗟𝗲𝘃𝗲𝗹𝘀 𝘄𝗶𝘁𝗵 𝗦𝗲𝗮𝗺𝗹𝗲𝘀𝘀 𝗔𝘂𝘁𝗼-𝗨𝗽𝗱𝗮𝘁𝗲𝘀 𝗳𝗼𝗿 𝗼𝘃𝗲𝗿 𝟭𝟲𝟱+ 𝗼𝗳 𝘁𝗵𝗲 𝗠𝗼𝘀𝘁 𝗟𝗶𝗾𝘂𝗶𝗱 𝗨.𝗦. 𝗠𝗮𝗿𝗸𝗲𝘁 𝗦𝘆𝗺𝗯𝗼𝗹𝘀 (including 𝟬𝗗𝗧𝗘 𝗳𝗼𝗿 𝗦𝗣𝗫, SPY, QQQ, TLT, IWM, etc...)

🔃 Dynamic Updates : Receive precise GEX levels with auto-updating metrics up to 5 times a day throughout the trading session—no manual refresh needed!

🍒 Strategically Developed : Built by experienced options traders to meet the needs of serious options market participants.

🕒 0DTE? No Problem! : Designed with 0DTE traders in mind, our indicator keeps you updated with GEX levels and seamless auto-refresh to capture every crucial market shift.

📈 Optimized for Option Traders : See accurate GEX and NETGEX profiles for multiple expirations to maximize strategic potential.

🔶 Comprehensive GEX Levels

This indicator provides unparalleled insight into market dynamics with levels like Call/Put Support, Resistance, HVL (High Volatility Level), and Call/Put Walls. These levels are auto-updated based on live market movements and reflect gamma shifts and volatility signals essential for options traders.

🔶 Ideal for 0DTE and Multi-Leg Strategies

Track essential GEX levels across expirations with our unique Cumulative (⅀) and Selected Alone (⊙) calculation models. Customize your view to reveal high-impact levels across multiple expirations or focus on a specific expiration for a targeted strategy.

🔶 Coverage of 165+ Highly Liquid U.S. Symbols

Compatible with over 165 U.S. market symbols, including SP:SPX , AMEX:SPY , NASDAQ:QQQ , NASDAQ:TLT , AMEX:GLD , NASDAQ:NVDA , and more. The watchlist is expanding continuously to meet the needs of active traders. List of Compatible Symbols Available Here: www.tradingview.com

🔶How does the indicator work and why is it unique?

This is not just another GEX indicator. It incorporates 15min delayed option chain data from ORATS as data provider, processes and refines the delayed data package using pineseed, and sends it to TradingView, visualizing the key GEX levels using specific formulas (see detailed below). This method of incorporating options data into a visualization framework is unique and entirely innovative on TradingView.

Unlike other providers that only set GEX levels at market open, this indicator adjusts dynamically throughout the day, providing updated insights across the trading day and capturing gamma shifts as the market moves.

_________________________________

-----------------------------------------------

🌑 𝗗 𝗢 𝗖 𝗨 𝗠 𝗘 𝗡 𝗧 𝗔 𝗧 𝗜 𝗢 𝗡 🌑

-----------------------------------------------

_________________________________

🔶 Understanding GEX (Gamma Exposure) and Gamma Profiling

Gamma Exposure (GEX) is a crucial concept in options trading because it reveals how options market positions can influence the dynamics of asset prices. In essence, GEX measures the collective gamma exposure of options market participants, impacting overall market stability and price movements.

🔹 What is GEX?

At its core, GEX captures the aggregate impact of gamma, a key options Greek, which tells us how an option's delta changes in response to price movements in the underlying asset. Positive or negative GEX levels can reflect the collective bullish or bearish stance of the market:

Positive GEX (far above HVL) : Indicates a net bullish positioning by options holders. When GEX is strongly positive, it suggests that as the asset price increases, market participants might need to buy more of the asset to maintain their hedges. This behavior can fuel further upward momentum.

Negative GEX (far below HVL) : Implies a net bearish positioning. In a strongly negative GEX environment, declines in the asset's price might prompt participants to sell, potentially exacerbating the downward movement.

🔹 The Influence of GEX on Strike Prices and Expiration

A unique feature of GEX is its impact near expiration dates. As options approach expiration, GEX levels can “pin” the price to specific strike levels, where options positions are concentrated. This pinning effect arises as market makers adjust their hedging strategies, often causing the asset price to gravitate towards certain strike prices, where a large volume of options contracts sits.

🟨 Overview of our GEX Calculation Models for Options Traders 🟨

Our GEX indicator models were developed with serious options traders in mind, providing flexibility beyond typical GEX providers. We know that using GEX levels for multi-leg strategies, where the underlying doesn't need a strong trend to be profitable , calls for a nuanced approach that aligns with different trading horizons. Here’s a detailed breakdown of our GEX calculation models and how they support strategic trading across varying timeframes.

Thus, the HVL an orher CALL/PUT WALLS depends on the indicator's selected calculation mode and expiration. The NETGEX profile of the chosen expiration appears on the HVL line , which automatically updates five times during trading hours , except for 0DTE, which reflects the value set at market open.

🔶 Cumulative Expiration (⅀) Calculation Method

This method aggregates GEX data for all expirations up to the selected date , giving you a more comprehensive view of market dynamics. We recommend using this method, as it allows you to see how combined expirations impact GEX levels, which can be critical when setting up trades with a longer time horizon.

🔶 Selected Alone (⊙) Calculation Method

This option displays the GEX profile specific to only the chosen expiration , providing a unique, time-bound view. This approach is ideal for those seeking precise insight into how an individual expiration is performing without the broader context of other expirations.

🔶 Example of using calculation methods:

With options trading, especially for multi-leg strategies, choosing the right expiration and calculation model is crucial. Let’s break down an example:

Suppose you’re considering a Friday (4DTE) front-leg diagonal on the SPX at the start of the week. In this case, the focus isn’t strictly on any single expiration (like 0DTE or 4DTE individually), but rather on what might happen cumulatively by Friday across all expirations . Here, the Cumulative Expiration (⅀) model comes into play, as it shows you an aggregated view of the GEX profile, factoring in all strikes and legs for all expirations leading up to the selected date.

For most use cases, we recommend setting your indicator to the Cumulative (⅀) model , which provides a broad and insightful look at GEX levels across multiple expirations. However, you can always switch to Selected Alone (⊙) for targeted analysis of an individual expiration. Remember, 0DTE defaults to “Selected Alone”, and Every Expiry always shows a cumulative value by default.

_________________________________

-----------------------------------------------

🟦 HVL (High Volatility Level) 🟦

Also known as the Gamma FLIP level or Zero Gamma , it represents the price level at which the gamma environment transitions from positive to negative or vice versa. The High Volatility Level (HVL) is a critical point for understanding gamma shifts and anticipating volatility. This shift influences how market makers hedge their positions, potentially increasing or dampening market volatility.

🔷 Understanding the Gamma Flip and HVL

At its core, the gamma flip represents the point where market makers may transition from a net positive to a net negative gamma position, or the reverse. When prices move above HVL, gamma is positive, often leading to lower volatility due to the stabilizing effects of market makers’ hedging. Conversely, when prices drop below HVL, gamma flips negative, and hedging by market makers can amplify volatility as they trade with the direction of price movements.

The HVL (High Volatility Level) is particularly important as it signals a shift in the impact of price movements on the GEX profile. Using the cumulative calculation mode, GEX values are aggregated across all strikes and expirations up to the selected expiration, helping to pinpoint the point where the GEX curve's slope changes from negative to positive.

🔷 Implications for Traders and Market Makers

For market makers, crossing below HVL into a negative gamma zone means that they hedge in the same direction as price movements, potentially amplifying volatility. For traders, understanding HVL's role is essential to choosing strategies that align with the prevailing volatility regime:

Positive GEX 🟢:

Above HVL, where GEX is positive, market makers hedge by buying stocks as prices fall and selling as prices rise. This has a stabilizing effect, creating a lower-volatility environment.

Negative GEX 🔴:

Below HVL, where GEX is negative, market makers' hedging aligns with price movements, increasing volatility. Here, they buy as prices rise and sell as they fall, reinforcing price direction.

🔷 HVL as a Momentum and Volatility Indicator

The HVL offers traders insight into potential shifts in market momentum. For example, above HVL, if the price increases, Net GEX also rises, which stabilizes prices as market makers hedge in opposition to price direction. Below HVL, however, a price rise decreases Net GEX, creating conditions where market makers’ hedging amplifies price movements, resulting in a more volatile environment.

HVL also acts as a significant support level, often preceding put supports. If the price falls below this level, traders may expect heightened volatility and increased bearish sentiment.

Knowing the location of HVL is vital for positioning yourself on the right side of volatility. By monitoring the HVL, traders can better anticipate shifts in sentiment and align strategies with prevailing market dynamics.

_________________________________

-----------------------------------------------

🟩 Call Resistance and Call Wall Levels 🟩

In options trading, understanding GEX levels like Call Resistance and Call Wall levels is crucial for navigating potential price inflection points. Our indicator provides these levels directly on your chart, allowing you to customize and optimize your trading approach. Here’s a detailed guide to help you understand and use Call Resistance and additional Call Wall levels effectively.

🟢 Call Resistance Level

The Call Resistance Level is a key point where our model indicates heightened Call GEX concentration. This level serves as a potential resistance area where price movement may face a barrier, slowing or even reversing before a breakout. Here’s how the Call Resistance Level can influence market behavior:

Resistance and Price Reversal ⬇️ : Similar to the Put Support level, the Call Resistance acts as a "sticky" price level, where upward movement encounters resistance. When the price approaches this level, it’s common for market makers to begin shorting to maintain delta neutrality. This shorting activity, combined with the potential monetization of calls, introduces a technical bearish force in the short term, often causing the price to bounce downward.

Upside Acceleration Point ⬆️ : If investors reposition calls to higher strikes as the price reaches Call Resistance, this level can roll up, allowing the price to push upward and potentially accelerating the rally. This effect can drive the market to higher levels as market makers adjust their positions accordingly.

🟢 Additional Call Wall Levels

Our model identifies the second and third-highest Call GEX levels, known as additional Call Walls. These levels are often secondary resistance points but hold significance as they add layers of possible resistance or breakout points. They offer similar potential as the primary Call Resistance level, acting as either:

Resistance Zones: Slowing the price momentum as it approaches these levels.

Inflection Points for Upside Momentum: Allowing for a possible continuation of upward movement if prices break through.

🟢 How to Trade the Call Resistance Level

To use the Call Resistance level effectively, look for possible price rejections or consolidations as the price approaches this zone. Here are the main scenarios:

Bounce to Downside: As the price nears the Call Resistance level, market makers’ delta-hedging activity (through shorting) can turn this level into a short-term bearish force, leading to price pullbacks.

Rolling the Position: For bulls, a key objective at the Call Resistance level is to see investors roll their call positions higher, effectively moving the resistance up. This repositioning may lead to incremental price gains as the Call Resistance level rises with each roll.

_________________________________

-----------------------------------------------

🟥 Put Support and Put Wall Levels 🟥

In options trading, understanding GEX levels like Put Support and secondary Put Wall levels is essential for managing potential price support points and gauging downside risk. Our indicator places these levels directly on your chart, allowing for customization to enhance your trading strategy. Here’s a detailed guide to help you leverage the Put Support and additional Put Wall levels effectively.

🔴 Put Support Level

The Put Support Level is a key zone where our model shows the highest concentration of negative GEX, representing an area with substantial put option interest. This level functions as a potential support zone, where price may stabilize or bounce upward, or as an inflection point, signaling increased downside momentum. Here’s how the Put Support Level can affect market behavior:

Support and Price Reversal🔺 : Similar to how Call Resistance operates on the upside, the Put Support Level often acts as a "sticky" level on the downside, where price finds support. As the asset price moves closer to this level, market makers begin adjusting their positions, frequently buying to maintain delta neutrality. This activity can create a temporary short squeeze, pushing prices back up.

Downside Acceleration Point 🔻 : If the asset continues moving lower, triggering more hedging activity, this level can become a tipping point for accelerated downside momentum.

🔴 Additional Put Wall Levels

Our model also identifies the second and third-highest negative GEX levels, known as secondary Put Walls. These levels are often seen as secondary support points and hold significance by adding layers of support or potential downside inflection points. Like the primary Put Support Level, they can act in two ways:

Support Zones: Helping slow price declines as they approach these levels.

Downside Inflection Points: Allowing further price decline if the support fails.

🔴 How Investors Hedge with Put Options

Investors commonly use put options to hedge long positions and protect portfolios, especially during times of market stress when implied volatility rises. This demand for puts increases the Put Skew, as market makers short to remain delta hedged.

As prices approach the Put Support Level, the hedging activity often intensifies because more puts become At the Money (ATM) or In the Money (ITM). To realize the value of their hedges, investors typically monetize these puts at this level, triggering the closing of short positions by market makers and resulting in a price bounce.

🔴 The Role of Implied Volatility

Implied Volatility (IV) is also a critical factor since it directly influences market flows. If IV driving put flows decreases, market makers may buy back shorts, which contributes to the bounce at the Put Support Level. Additionally, another Greek, Vanna—representing changes in delta due to IV shifts—plays a vital role here. As IV changes, Vanna affects delta-hedging adjustments, adding a layer of complexity to understanding market makers' actions around these support levels.

🔴 Possible Price Scenarios at the Put Support Level

When the price reaches the Put Support Level, there are generally two scenarios:

Bounce to Upside🔺 : The Put Support Level is where substantial put hedging activity happens. As prices approach, market makers adjust their delta by buying, which can push prices back up.

Roll Positions🔻 : After monetizing puts, investors have two options: roll hedges to higher strikes if they expect a bullish move, or open new out-of-the-money puts at lower strikes. If new hedges are set at lower levels, the Put Support level may also shift lower, creating a new bearish force as market makers begin hedging these new positions.

🟨 Customizing Put Support/Call Resistance and Put/Call Wall Levels on Your Chart

Our indicator settings provide extensive customization options for displaying Put Support, Call Resistance, and Put/Call Wall levels.

You can:

adjust the depth to highlight the highest positive or negative NETGEX levels

choose to display relative data, show only the colored strike line

adjust the offset for enhanced visibility.

This flexibility helps you focus on the critical details that best align with your trading strategy, ensuring a clearer and more tailored view of the GEX levels on your chart.

Currently, we examine the top three levels with the highest positive and negative NETGEX values, allowing you to view seven key GEX levels on your chart (3 Call + 1 HVL + 3 Put). However, in the near future, we plan to expand this to seven levels per side, resulting in a total of up to 15 significant GEX levels on the chart instead of the current 7. This enhancement will cater to all needs, especially benefiting 0DTE traders.

_________________________________

-----------------------------------------------

🔶 ADDITIONAL IMPORTANT COMMENTS

🔹- Why is there a slight difference between the displayed data and other GEX provider's data like MenthorQ, GammaEdge, SpotGamma, GEXBot, etc?

There are two reasons for this, and one is beyond our control:

🔹 (1) Option-data update frequency:

According to TradingView's regulations and guidelines, we can update external data a maximum of 5 times per day. We strive to use these updates in the most optimal way:

(1st update) 15 minutes after U.S. market open

(2nd, 3rd, 4th updates) 1.5–3 hours during U.S. market open hours

(5th update) 10 minutes before U.S. market close.

You don’t need to refresh your window; our latest refreshed data pack is always automatically applied to your indicator. You can see the time elapsed since the last update by hovering over the HVL.

🔹 (2) GEX Levels with Intraday Updates Based on Price Movements

The TanukiTrade Options GEX Indicator for TradingView provides open interest data with a 15-minute delay after the market opens. Using this data, we calculate and update the relevant levels throughout the trading day, reflecting almost real-time price changes and gamma values. Unlike other GEX providers, who set their GEX levels solely at market open without further updates, we dynamically adjust our levels intraday to capture significant price shifts.

🔹 Automatic & Seamless Intraday Updates and Special Cases

For our indicator, the HVL (High Volatility Level) reflects the selected calculation mode and expiration. We update these NETGEX profiles five times throughout the trading day, with one exception: 0DTE data, which is set at market open and does not update intraday due to the rapid narrowing of gamma levels . Note that similar to other GEX providers, our 0DTE remains fixed at open, while cumulative values update during the day based on almost real-time market movements.

🔹Consistent SPX 0DTE GEX Levels with Morning Open Interest Updates Only

For SPX, the 0DTE (Zero Days to Expiration) options and GEX levels are calculated based on openinterest data provided by the clearinghouse at market open. Due to the exponential narrowing of gamma levels throughout the day, we do not update these levels intraday, unlike other expirations. Therefore, if you select the expiring contract on that day, you’ll see the exact morning level, as it was calculated at market open. This status is also published the previous evening, based on the data available then, so you can already view the levels for the following day’s 1DTE (next day’s 0DTE) before market close. After market open, around 15 minutes later, this level is updated with the latest open interest data and remains unchanged for the rest of the day. Other providers take a similar approach. We do not support intraday volume-based GEX calculations, as our benchmarks show this can produce misleading results.

Disclaimer:

Our option indicator uses approximately 15min-3 hour delayed option market snapshot data to calculate the main option metrics. Exact realtime option contract prices are never displayed; only derived GEX metrics are shown to ensure accurate and consistent visualization. Due to the above, this indicator can only be used for decision support; exclusive decisions cannot be made based on this indicator. We reserve the right to make errors.This indicator is designed for options traders who understand what they are doing. It assumes that they are familiar with options and can make well-informed, independent decisions. We work with paid delayed data and we are not a data provider; therefore, we do not bear any financial or other liability.

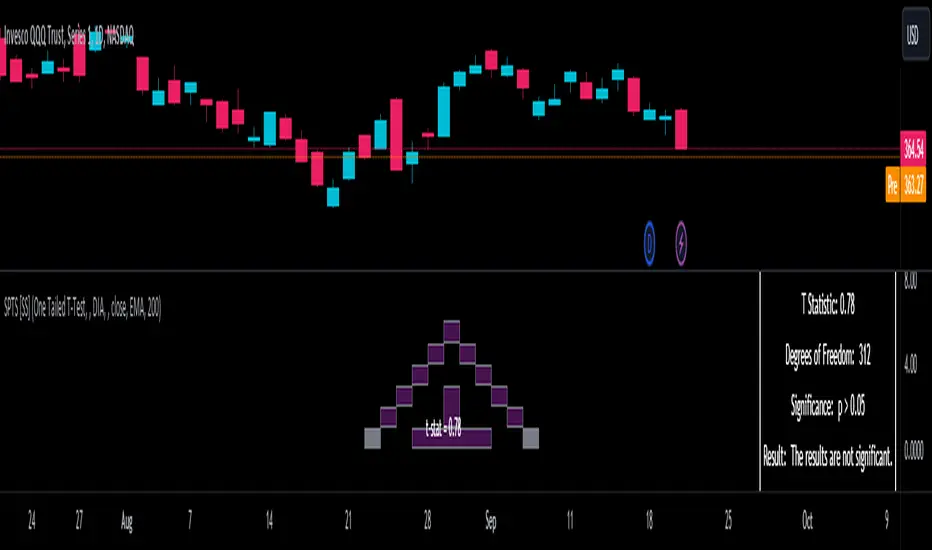

Statistical Package for the Trading Sciences [SS]

This is SPTS.

It stands for Statistical Package for the Trading Sciences.

Its a play on SPSS (Statistical Package for the Social Sciences) by IBM (software that, prior to Pinescript, I would use on a daily basis for trading).

Let's preface this indicator first:

This isn't so much an indicator as it is a project. A passion project really.

This has been in the works for months and I still feel like its incomplete. But the plan here is to continue to add functionality to it and actually have the Pinecoding and Tradingview community contribute to it.

As a math based trader, I relied on Excel, SPSS and R constantly to plan my trades. Since learning a functional amount of Pinescript and coding a lot of what I do and what I relied on SPSS, Excel and R for, I use it perhaps maybe a few times a week.

This indicator, or package, has some of the key things I used Excel and SPSS for on a daily and weekly basis. This also adds a lot of, I would say, fairly complex math functionality to Pinescript. Because this is adding functionality not necessarily native to Pinescript, I have placed most, if not all, of the functionality into actual exportable functions. I have also set it up as a kind of library, with explanations and tips on how other coders can take these functions and implement them into other scripts.

The hope here is that other coders will take it, build upon it, improve it and hopefully share additional functionality that can be added into this package. Hence why I call it a project. Okay, let's get into an overview:

Current Functions of SPTS:

SPTS currently has the following functionality (further explanations will be offered below):

Ability to Perform a One-Tailed, Two-Tailed and Paired Sample T-Test, with corresponding P value.

Standard Pearson Correlation (with functionality to be able to calculate the Pearson Correlation between 2 arrays).

Quadratic (or Curvlinear) correlation assessments.

R squared Assessments.

Standard Linear Regression.

Multiple Regression of 2 independent variables.

Tests of Normality (with Kurtosis and Skewness) and recognition of up to 7 Different Distributions.

ARIMA Modeller (Sort of, more details below)

Okay, so let's go over each of them!

T-Tests

So traditionally, most correlation assessments on Pinescript are done with a generic Pearson Correlation using the "ta.correlation" argument. However, this is not always the best test to be used for correlations and determine effects. One approach to correlation assessments used frequently in economics is the T-Test assessment.

The t-test is a statistical hypothesis test used to determine if there is a significant difference between the means of two groups. It assesses whether the sample means are likely to have come from populations with the same mean. The test produces a t-statistic, which is then compared to a critical value from the t-distribution to determine statistical significance. Lower p-values indicate stronger evidence against the null hypothesis of equal means.

A significant t-test result, indicating the rejection of the null hypothesis, suggests that there is statistical evidence to support that there is a significant difference between the means of the two groups being compared. In practical terms, it means that the observed difference in sample means is unlikely to have occurred by random chance alone. Researchers typically interpret this as evidence that there is a real, meaningful difference between the groups being studied.

Some uses of the T-Test in finance include:

Risk Assessment: The t-test can be used to compare the risk profiles of different financial assets or portfolios. It helps investors assess whether the differences in returns or volatility are statistically significant.

Pairs Trading: Traders often apply the t-test when engaging in pairs trading, a strategy that involves trading two correlated securities. It helps determine when the price spread between the two assets is statistically significant and may revert to the mean.

Volatility Analysis: Traders and risk managers use t-tests to compare the volatility of different assets or portfolios, assessing whether one is significantly more or less volatile than another.

Market Efficiency Tests: Financial researchers use t-tests to test the Efficient Market Hypothesis by assessing whether stock price movements follow a random walk or if there are statistically significant deviations from it.

Value at Risk (VaR) Calculation: Risk managers use t-tests to calculate VaR, a measure of potential losses in a portfolio. It helps assess whether a portfolio's value is likely to fall below a certain threshold.

There are many other applications, but these are a few of the highlights. SPTS permits 3 different types of T-Test analyses, these being the One Tailed T-Test (if you want to test a single direction), two tailed T-Test (if you are unsure of which direction is significant) and a paired sample t-test.

Which T is the Right T?

Generally, a one-tailed t-test is used to determine if a sample mean is significantly greater than or less than a specified population mean, whereas a two-tailed t-test assesses if the sample mean is significantly different (either greater or less) from the population mean. In contrast, a paired sample t-test compares two sets of paired observations (e.g., before and after treatment) to assess if there's a significant difference in their means, typically used when the data points in each pair are related or dependent.

So which do you use? Well, it depends on what you want to know. As a general rule a one tailed t-test is sufficient and will help you pinpoint directionality of the relationship (that one ticker or economic indicator has a significant affect on another in a linear way).

A two tailed is more broad and looks for significance in either direction.

A paired sample t-test usually looks at identical groups to see if one group has a statistically different outcome. This is usually used in clinical trials to compare treatment interventions in identical groups. It's use in finance is somewhat limited, but it is invaluable when you want to compare equities that track the same thing (for example SPX vs SPY vs ES1!) or you want to test a hypothesis about an index and a leveraged share (for example, the relationship between FNGU and, say, MSFT or NVDA).

Statistical Significance

In general, with a t-test you would need to reference a T-Table to determine the statistical significance of the degree of Freedom and the T-Statistic.

However, because I wanted Pinescript to full fledge replace SPSS and Excel, I went ahead and threw the T-Table into an array, so that Pinescript can make the determination itself of the actual P value for a t-test, no cross referencing required :-).

Left tail (Significant):

Both tails (Significant):

Distributed throughout (insignificant):

As you can see in the images above, the t-test will also display a bell-curve analysis of where the significance falls (left tail, both tails or insignificant, distributed throughout).

That said, I have not included this function for the paired sample t-test because that is a bit more nuanced. But for the one and two tailed assessments, the indicator will provide you the P value.

Pearson Correlation Assessment

I don't think I need to go into too much detail on this one.

I have put in functionality to quickly calculate the Pearson Correlation of two array's, which is not currently possible with the "ta.correlation" function.

Quadratic (Curvlinear) Correlation

Not everything in life is linear, sometimes things are curved!

The Pearson Correlation is great for linear assessments, but tends to under-estimate the degree of the relationship in curved relationships. There currently is no native function to t-test for quadratic/curvlinear relationships, so I went ahead and created one.

You can see an example of how Quadratic and Pearson Correlations vary when you look at CME_MINI:ES1! against AMEX:DIA for the past 10 ish months:

Pearson Correlation:

Quadratic Correlation:

One or the other is not always the best, so it is important to check both!

R-Squared Assessments:

The R-squared value, or the square of the Pearson correlation coefficient (r), is used to measure the proportion of variance in one variable that can be explained by the linear relationship with another variable. It represents the goodness-of-fit of a linear regression model with a single predictor variable.

R-Squared is offered in 3 separate forms within this indicator. First, there is the generic R squared which is taking the square root of a Pearson Correlation assessment to assess the variance.

The next is the R-Squared which is calculated from an actual linear regression model done within the indicator.

The first is the R-Squared which is calculated from a multiple regression model done within the indicator.

Regardless of which R-Squared value you are using, the meaning is the same. R-Square assesses the variance between the variables under assessment and can offer an insight into the goodness of fit and the ability of the model to account for the degree of variance.

Here is the R Squared assessment of the SPX against the US Money Supply:

Standard Linear Regression

The indicator contains the ability to do a standard linear regression model. You can convert one ticker or economic indicator into a stock, ticker or other economic indicator. The indicator will provide you with all of the expected information from a linear regression model, including the coefficients, intercept, error assessments, correlation and R2 value.

Here is AAPL and MSFT as an example:

Multiple Regression

Oh man, this was something I really wanted in Pinescript, and now we have it!

I have created a function for multiple regression, which, if you export the function, will permit you to perform multiple regression on any variables available in Pinescript!

Using this functionality in the indicator, you will need to select 2, dependent variables and a single independent variable.

Here is an example of multiple regression for NASDAQ:AAPL using NASDAQ:MSFT and NASDAQ:NVDA :

And an example of SPX using the US Money Supply (M2) and AMEX:GLD :

Tests of Normality:

Many indicators perform a lot of functions on the assumption of normality, yet there are no indicators that actually test that assumption!

So, I have inputted a function to assess for normality. It uses the Kurtosis and Skewness to determine up to 7 different distribution types and it will explain the implication of the distribution. Here is an example of SP:SPX on the Monthly Perspective since 2010:

And NYSE:BA since the 60s:

And NVDA since 2015:

ARIMA Modeller

Okay, so let me disclose, this isn't a full fledge ARIMA modeller. I took some shortcuts.

True ARIMA modelling would involve decomposing the seasonality from the trend. I omitted this step for simplicity sake. Instead, you can select between using an EMA or SMA based approach, and it will perform an autogressive type analysis on the EMA or SMA.

I have tested it on lookback with results provided by SPSS and this actually works better than SPSS' ARIMA function. So I am actually kind of impressed.

You will need to input your parameters for the ARIMA model, I usually would do a 14, 21 and 50 day EMA of the close price, and it will forecast out that range over the length of the EMA.

So for example, if you select the EMA 50 on the daily, it will plot out the forecast for the next 50 days based on an autoregressive model created on the EMA 50. Here is how it looks on AMEX:SPY :

You can also elect to plot the upper and lower confidence bands:

Closing Remarks

So that is the indicator/package.

I do hope to continue expanding its functionality, but as of now, it does already have quite a lot of functionality.

I really hope you enjoy it and find it helpful. This. Has. Taken. AGES! No joke. Between referencing my old statistics textbooks, trying to remember how to calculate some of these things, and wanting to throw my computer against the wall because of errors in the code, this was a task, that's for sure. So I really hope you find some usefulness in it all and enjoy the ability to be able to do functions that previously could really only be done in external software.

As always, leave your comments, suggestions and feedback below!

Take care!

Market InternalsMarket internals can be a powerful tool for determining future moves, overall trend health and provide a means of directional confidence.

This indicator watches a handful of SPX and US stocks based internals to determine key areas of sentiment changes, the internals monitored are:

US Stocks Ticks

Call and Put SPX Volume

SPX Gamma Dispersion

US Stocks Ask and Big Volume

US Stocks Advancing and Declining Issues

Each time there's a bullish or bearish sentiment change it will be market with green/red flag and a single letter that identifies what market internal has changed.

SPX gamma dispersion events aren't to be considered directional from historical observations made but can be a sign of liquidity adjustments and when paired with any of the other aforementioned internals sentiment changes can be used as a powerful signal.

If it's observed that market internals are changing erratically then it's a clear indication of market chop and best to wait for cleaner trends.

Future updates may include non-SPX based internals analysis, change in display, alerts/alertconditions and more. Feel free to comment with any desired changes and we can discuss!

TradeChartist Drifter™𝗧𝗿𝗮𝗱𝗲𝗖𝗵𝗮𝗿𝘁𝗶𝘀𝘁 𝗗𝗿𝗶𝗳𝘁𝗲𝗿 is an adeptly designed, functional and a visual indicator that plots trend-following Support and Resistance walls by employing the concepts of Trend-based Support and Resistance, Momentum and Volatility, based on user defined lookback length, and includes three extremely useful Visualizers - Drift Bands Visualizer , Drift Strength Visualizer and Drifter AutoFibs Visualizer to help visualize the Price action in relation to the Support and Resistance Walls.

===================================================================================================================

™𝗧𝗿𝗮𝗱𝗲𝗖𝗵𝗮𝗿𝘁𝗶𝘀𝘁 𝗗𝗿𝗶𝗳𝘁𝗲𝗿 𝗨𝘀𝗲𝗿 𝗠𝗮𝗻𝘂𝗮𝗹

===================================

Concept of Drift

™TradeChartist Drifter combines concepts of Trend-based Support and Resistance, Momentum and Volatility to plot continuous Drifter Support and Resistance Walls that encloses the price action ( Drift ) within it (If the source price is price candle/bar based price like open,close,high,low,hl2,hl3 or ohlc4). In fact, these walls are generated by the price action ( Drift ) itself and helps the user see the price trend clearly as price makes higher highs/lows and lower highs/lows.

The Drifter walls are based on the user defined lookback length which can be changed in the Lᴇɴɢᴛʜ ғᴏʀ Dʀɪғᴛᴇʀ Wᴀʟʟs input box.

Drifter walls can be viewed or hidden by enabling or disabling 𝐒𝐡𝐨𝐰 𝐃𝐫𝐢𝐟𝐭𝐞𝐫 𝐖𝐚𝐥𝐥𝐬 .

Price Highs and Lows breaching the Drifter Walls can be viewed or hidden by enabling or disabling Sʜᴏᴡ Dʀɪғᴛᴇʀ Hɪɢʜs ᴀɴᴅ Lᴏᴡs .

Understanding and Visualizing ( Drift ) is important as it helps traders see the price action clearly. Price Volatility, Trend and Momentum are dependent on the period they are analysed. In order to visualize the drift, the user must enter the number of bars lookback in the Dʀɪғᴛ Lᴏᴏᴋʙᴀᴄᴋ input box.

===================================================================================================================

Three Types of Visualizers

One of the three types of Visualizers can be selected from Vɪsᴜᴀʟɪᴢᴇʀ Tʏᴘᴇ dropdown.

Drifter AutoFibs Visualizer is dependent on the Lᴇɴɢᴛʜ ғᴏʀ Dʀɪғᴛᴇʀ Wᴀʟʟs only as it fills the Drifter with Automatic Fibonacci Levels based on the distance between the Drifter Walls.

Drift Strength Visualizer is dependent on the Dʀɪғᴛ Lᴏᴏᴋʙᴀᴄᴋ only as it detects the Drift Strength based on Drift length. This Visualizer detects the Bull and the Bear zones based on the lookback. This helps visualize the Trend and Momentum clearly as the zones are filled with user selected theme based Bull and Bear colours.

Drift Bands Visualizer plots Drift Bands based on either Average True Range (ATR) or Standard Deviation along with the Bull or Bear Trend clearly shown using the color of the Mean or Basis line of the Drift Bands.

===================================================================================================================

╔═════════ 𝗗𝗿𝗶𝗳𝘁 𝗕𝗮𝗻𝗱𝘀 ══════════╗

Drift Bands are based on either ATR or Standard Deviation and consists of an Upper Band, a Lower Bands and a Mean or Basis Line. Drift Bands are extremely effective and highly useful in spotting the trend as the breakout from the upper or the lower band signals a change in the Drift based on the Dʀɪғᴛ Lᴏᴏᴋʙᴀᴄᴋ .