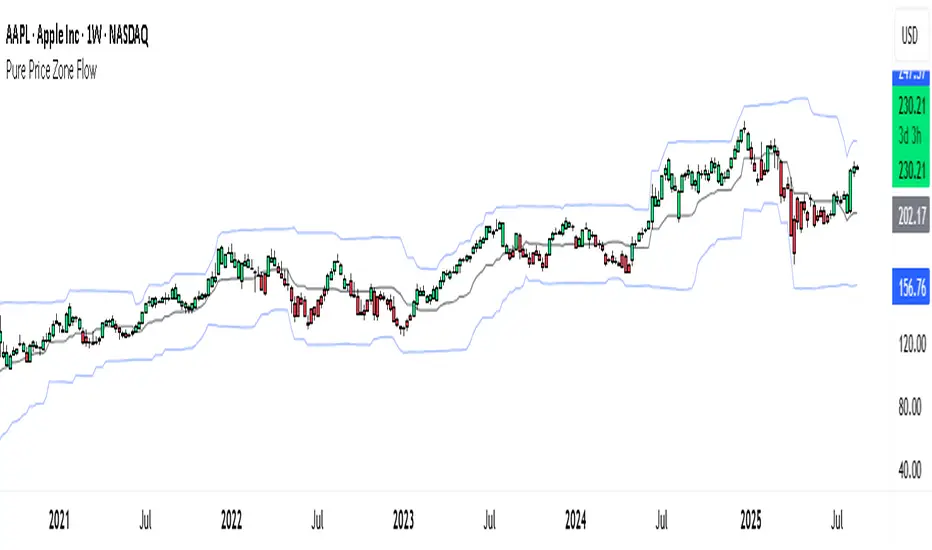

Pure Price Zone Flow🔎 What this indicator is

It’s a price-action-based zone indicator. Unlike moving average systems, this one relies only on:

1. Swing Highs & Swing Lows → The highest and lowest points within a recent lookback period (like "mini support & resistance").

2. ATR (Average True Range) → A volatility measure that expands the zone, making it more adaptive to different market conditions.

3. Breakouts & Retests → When price breaks above a swing high (bullish) or below a swing low (bearish), the indicator marks it and highlights the new trend.

👉 The goal is to spot clean structure shifts and define clear trend zones where traders can position themselves.

________________________________________

⚙️ How it is calculated

1. Swing High & Swing Low

o We look back len candles (default 20).

o Find the highest high (swingHigh) and the lowest low (swingLow) in that window.

o This forms the price range zone.

2. ATR Expansion

o We calculate ATR over the same len.

o Add/subtract it (multiplied by atrMult) to the zone edges to expand them.

o This ensures the zones breathe with volatility (tight in quiet markets, wide in choppy ones).

3. Mid-Zone

o Simply the average of swingHigh and swingLow.

o If price is above mid → bullish bias.

o If below mid → bearish bias.

o This gives us the trend color for candles.

4. Breakouts

o If the close crosses above swingHigh, we mark a bullish breakout with a label.

o If the close crosses below swingLow, we mark a bearish breakdown.

________________________________________

📊 How it helps traders

This indicator helps by:

1. Identifying Structure Shifts

o Many traders watch swing highs/lows for breakouts or reversals.

o This automates the process and visually confirms when structure is broken.

2. Dynamic Zone Trading

o Instead of fixed support/resistance, the ATR expansion adapts to volatility.

o This avoids false signals in high-volatility conditions.

3. Trend Bias at a Glance

o Candle coloring instantly tells you whether price is in bullish or bearish territory relative to the mid-zone.

4. Breakout Confirmation

o The labels show when a breakout has occurred, so traders can react quickly (e.g., enter with trend, wait for retest, or avoid fading moves).

________________________________________

🌍 Markets it works best in

• Crypto (Bitcoin, Ethereum, etc.): Very effective since crypto is breakout-driven and respects swing levels.

• Forex: Good for volatility-adaptive structure analysis, especially in trending pairs.

• Indices (SPX, NASDAQ, DAX, NIFTY): Useful for breakout trading during session opens or key news events.

• Commodities (Gold, Oil, Silver): Works well to define intraday ranges and breakout levels.

⚠️ Less useful in low-volatility, mean-reverting assets (like some penny stocks or sideways ranges), because breakouts may be rare or fake.

________________________________________

💡 How it adds value

• Strips away unnecessary complexity (no lagging averages).

• Focuses directly on what price is doing structurally.

• Adaptive → works across different markets & timeframes.

• Easy visualization → zones, trend coloring, breakout markers.

• Helps traders trade with the flow of the market, instead of guessing tops/bottoms.

________________________________________

👉 In short:

This indicator turns raw price action into clear, actionable zones.

It highlights when the market shifts from balance to breakout, so traders can align with momentum rather than fighting it.

Cerca negli script per "spx"

RRG Relative Strength# RRG Relative Strength (RRG RS)

Compare any symbol to a benchmark using two RRG-style lines: **RS-Ratio** (trend of relative strength) and **RS-Momentum** (momentum of that trend). Both are centered at **100**:

- **RS-Ratio > 100** → outperforming the benchmark

- **RS-Ratio < 100** → underperforming

- **RS-Momentum** often **leads** RS-Ratio (crosses 100 earlier)

# How it works

1) Relative Strength (RS): RS = Close(symbol) / Close(benchmark)

2) Normalize around 100: smooth RS with EMA and divide RS by that EMA

3) RS-Ratio: EMA( RS / EMA(RS, Length), LenSmooth ) * 100

4) RS-Momentum: RS-Ratio / EMA(RS-Ratio, LenSmooth) * 100

# Inputs

- Length (default 14): normalization window for RS

- Length Smooth (default 20): smoothing window for RS-Ratio & RS-Momentum

# Benchmark (auto)

- US: SP:SPX (S&P 500)

- Vietnam: HOSE:VNINDEX

- Crypto: INDEX:BTCUSD

(Modify the mapping if needed, or replace with your own input.symbol().)

# How to read

- Improving: RS-Momentum crosses above 100 while RS-Ratio turns up

- Leading: RS-Ratio > 100 with RS-Momentum ≥ 100

- Weakening: RS-Momentum drops below 100; RS-Ratio often follows

# Timeframes & presets

- Works on Daily and Weekly charts

- Daily (fast): 14 / 20

- Approx. weekly behavior on Daily: 50 / 60

Note: Values usually hover near 100 (e.g., ~90–110) but are not strictly bounded. Ensure your symbol and benchmark trade in comparable sessions/currencies.

Extended CANSLIM Indicator❖ Extended CANSLIM Indicator.

The Extended CANSLIM indicator is an indicator that concentrates all the tools usually used by CANSLIM traders.

It shows a table where all the stock fundamental information is shown at once first for the last quarter and then up to 5 years back.

The fundamental data is checked against well known CANSLIM validation criteria and is shown over 4 state levels.

1. Good = Value is CANSLIM Compliant.

2. Acceptable = Value is not CANSLIM compliant but still good. value is shown with a lighter background color.

3. Warning = Value deserves special attention. Value is shown over orange background color.

3. Stop = Value is non CANSLIM compliant or indicates a stop trading condition. Value is shown over red background color.

The indicator has also a set of technical tools calculated on price or index and shown directly on the chart.

❖ Fundamental data shown in the table.

The table is arranged in 4 sets of data:

1. Table Header, showing Indicator and Company data.

2. CANSLIM.

3. 3Rs: RS Rating, Revenue and ROE.

4. Extra Data: Piotroski score, ATR, Trend Days, D to E, Avg Vol and Vol today.

Sets 3 and 4 can be hidden from the table.

❖ Indicator and Compay Data.

The table header shows, Indicator name and version.

It then displays Company Name, sector and industry, human size and its capitalization.

❖ CANSLIM Data.

Displays either genuine CANSLIM data from TradinView or custom data as best effort when that data cannot be obtained in TV.

C = EPS diluted growth, Quarterly YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

A = EPS diluted growth, Annual YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

N = New High as best effort (Cust).

Always Good

S = Float shares as best effort.

Always Good

L = One year performance relative to S&P 500 (Cust),

Positive : 0% .. 50% = Neutral, 50%+ = Leader, 80%+ = Leader+, 100%+ = Leader++

Negative : 0% .. -10% = Laggard, -10% .. -30% = Laggard+, -30%+ = Laggard++

>= 50% = Good, >= 0% = Acceptable, >= -10% Warning, < -10% = Stop

I = Accumulation/Distribution days over last 25 days as a clue for institutional support (Cust).

A delta is calculated by subtracting Distribution to Accumulation days.

> 0 = Good, = 0 = Acceptable, < 0 = Warning, < -5 = Stop

M = Market direction and exposure measured on S&500 closing between averages (Cust).

Varies from 0% Full Bear to 100% Full Bull

>= 80% = Good, >= 60% = Acceptable, >= 40% = Warning, < 40% = Stop

❖ Extra non CANSLIM Data.

RS = RS Rating.

>= 90 = Good, >= 80 = Accept, >= 50 = Warning, < 50 = Stop

Rev. = Revenue Growth Quarterly YoY.

>= 0% = Good, <0% = Stop

ROE = Return on Equity, Quarterly YoY.

>= 17% = Good, >= 0% = Acceptable, < 0% = Stop

Piotr. = Piotroski Score, www.investopedia.com (TV)

>= 7 = Good, >= 4 = Acceptable, < 4 = Stop

ATR = Average True Range over the last 20 days (Cust).

0% - 2% = Acceptable, 2% - 4% = Ideal, 4% - 6% = Warning, 5%+ = Stop.

Trend Days = Days since EMA150 is over EMA200 (Cust).

Always Good

D. to E. = Days left before Earnings. Maybe not a good idea buying just before earnings (Cust).

>= 28 = Good, >= 21 = Acceptable, >= 14 = Warning, < 14 = Stop

Avg Vol. = 50d Average Volume (Cust).

>= 100K = Good, < 100K = Acceptable

Vol. Today = Today's percentage volume compared to 50d average (Cust).

Always Good.

❖ Historical Data.

Optionally selectable historical data can be displayed for C, A, Revenue and ROE up to 20 quarters if available.

Quarterly numbers can also be displayed for A, C and Revenue.

Information can be shown in Chronological or Reverse Chronological order (default).

Increasing growth quarters are shown in white, while diminuing ones are shown in Yellow.

Transition from Losing to Profitable quarters are shown with an exclamation mark ‘!’

Finally, losing quarters are shown between parenthesis.

❖ MAs on chart.

Displays 200, 100, 50 and 20 days MAs on chart.

The MAs are also automatically scaled in the 1W time frame.

❖ New 52 Week High on chart.

A sun is shown on the chart the first time that a new 52 week high is reached.

The N cell shows a filled sun when a 52 week high is no older than a month, an lighter sun when it’s no older than a quarter or a moon otherwise.

❖ Pocket Pivots on chart.

Small triangles below the price are signaling pocket pivots.

❖ Bases on chart, formerly Darvas Boxes.

Draw bases as defined by Darvas boxes, both top or bottom of bases can be selected to be shown in order to only show resistance or support.

❖ Market exposure/direction indicator.

When charting S&P500 (SPX), Nasdaq 100 Index (NDX), Nasdaq composite (IXIC) or Dow Jownes Index (DJIA), the indicator switches to Market Exposure indicator, showing also Accumulation/Distribution days when volume information is available. This indication which varies from 0% to 100% is what is shown under the M letter in the CANSLIM table which is calculated on the S&P500.

❖ Follow Through Days indicator.

If you are an adept of the Low-cheat entry, then you will be highly interested by the Follow Through days indicator as measured in the S&P 500 and shown as diamonds on the chart.

The follow-through days are calculated on S&P500 but shown in current stock chart so you don’t need to chart the S&P 500 to know that a follow through day occurred.

Follow Through days show correctly on Daily time frame and most are also shown on the Weekly time frame as well.

They are also classified according to the market zone in which they occur:

0%-5% from peak = Pullback : FT day is not shown.

5%-10% from peak = Minor Correction : Minor FT days is shown.

10%-20% from peak = Correction : Intermediate FT days us shown

20+% from peak = Bear Market : Makor FT days is shown

❖ RS Line and Rating indicator.

A RS Line and Rating indicator can be added to the chart.

Relative Strength Rating Accuracy.

Please note that the RS Rating is not 100% accurate when compared to IBD values.

❖ Earning Line indicator.

An Earning Line indicator can be added to the chart.

❖ ATR Bands and ATR Trade calculator.

The motivation for this calculator came from my own need to enter trades on volatile stocks where the simple 7% Stop Loss rule doest not work.

It simply calculates the number of shares you can buy at any moment based on current stock price and using the lower ATR band as a stop loss.

A few words about the ATR Bands.

On this indicator the ATR bands are not drawn as a classical channel that follows the price.

The lower band is drawn as a support until it’s broken on a closing basis. It can’t be in a down trend.

The upper band is drawn as a resistance until it’s broken on a closing basis. It can’t be in an up trend.

The idea is that when price starts to fall down from a peak, it should not violate its lower band ATR and that means that we can use that level as a Stop Loss.

You must look back for the stock volatility and find out which ATR multiplier works well meaning that the ATR bands are not violated on normal pullbacks. By default, the indicator uses 5x multiplier.

❖ Extra things, visual features and default settings.

The first square cell of current quarter displays a check mark ‘V’ if the CANSLIM criteria is OK or acceptable or a cross ‘X’ otherwise.

The first square cell of historical C and Rev show respectively the count of last consecutive positive quarters.

There are different color themes from “Forest” to “Space” you can chose from to best fit your eyes.

You also have different table sizes going from “Micro” to “Huge” for better adjustment to the size of your display.

The default settings view show: Pocket Pivots, FT Days, MA50, RS Line and ATR Bands.

That's all, Enjoy!

Adaptive Correlation Engine (ACE)🧠 Adaptive Correlation Engine (ACE)

Quantify inter-asset relationships with adaptive lag detection and actionable insights.

📌 What is ACE?

The Adaptive Correlation Engine (ACE) is a precision tool for seeking to uncover meaningful relationships between two assets — not just raw correlation, but also lag dynamics, leader detection, and alignment vs. divergence classification.

Unlike static correlation tools, ACE intelligently scans multiple lag windows to find:

✅ The maximum correlation between the base asset and a comparison symbol

⏱️ The optimal lag (if any) at which the correlation is strongest

🧭 Whether the assets are Aligned (positive correlation) or Divergent (inverse)

🔁 Which symbol is leading, and by how many bars

📈 Actionable signal strength based on a user-defined correlation threshold

⚙️ How It Works

Correlation Scan:

For each bar, ACE checks the correlation between the charted asset (close) and a lagged version of the comparison asset across a sliding window of lookback periods.

Lag Optimization:

The engine searches from lag 0 up to your specified Max Lag to find where the correlation (positive or negative) is most significant.

Relationship Classification:

The indicator classifies the relationship as:

Aligned: Positive correlation above the threshold

Divergent: Negative correlation above the threshold

Synchronous: No lag detected

Low Signal: Correlation is weak or noisy

Visual & Tabular Insights:

ACE plots the highest detected correlation on the chart and shows an insight table displaying:

- Correlation value

- Detected lag

- Direction type (aligned/divergent)

- Leading asset

- Suggested action (e.g., “Likely continuation” or “Possible mean reversion”)

💡 How to Use It

Use ACE to identify leadership patterns between assets (e.g., ETH leads altcoins, SPX leads crypto, etc.)

Spot potential lagging trade setups where one asset’s move may soon echo in another

Confirm or challenge correlation-based trading assumptions with data

Combine with technical indicators or price action to time entries and exits more confidently

🔔 Alerts

Built-in alerts notify you when correlation strength crosses your actionable threshold, classified by alignment or divergence.

🛠️ Inputs

Compare Symbol: The asset to compare against (e.g., INDEX:ETHUSD)

Correlation Lookback: Rolling window for calculating correlation

Max Lag Bars: Maximum lag shift to test

Minimum Actionable Correlation: Signal threshold for trade-worthy insights

⚠️ Disclaimer

This tool is for research and informational purposes only. It does not constitute financial advice or a trading signal. Always perform your own due diligence and consult a financial advisor before making investment decisions.

Dynamic 5DMA/EMA with Color for Multiple Products🔹 Dynamic 5DMA/EMA with Slope-Based Coloring (All Timeframes)

This indicator plots a dynamic 5-period moving average that adapts intelligently to your chart's timeframe and product type — giving you a clean, slope-sensitive visual edge across intraday, daily, and weekly views.

✅ Key Features:

📈 Dynamic MA Length Scaling:

On intraday timeframes, the MA adjusts for your selected market session (RTH, ETH, VIX, or Futures), calculating a true 5-day average based on actual session length — not just a flat bar count.

🔄 Automatic Timeframe Detection:

Daily Chart: Uses standard 5DMA or 5EMA.

Weekly Chart: Applies a true 5-week MA.

Intraday Charts: Converts 5 days into bar-length equivalent dynamically.

🎨 Color-Coded Slope Logic:

Green = Rising MA (bullish slope)

Red = Falling MA (bearish slope)

Neutral slope = previous color held for visual continuity

No more guessing — direction is instantly clear.

⚠️ Built-In Slope Flip Alerts:

Set alerts when the slope of the MA turns up or down. Ideal for timing pullback entries or exits across any product.

⚙️ Session Settings for Proper Scaling:

Choose your product's market structure to ensure accurate 5-day conversion on intraday charts:

Stocks - RTH: 390 mins/day

Stocks - ETH: 780 mins/day

VIX: 855 mins/day

Futures: 1440 mins/day

This ensures the MA reflects 5 full trading days, regardless of session irregularities or bar interval.

📌 Why Use This Indicator?

Most MAs misrepresent trend direction on intraday charts because they assume static daily bar counts. This tool corrects that, then adds slope-based coloring to give you a fast, visual read on short-term momentum. Whether you’re swing trading SPY, scalping VIX, or position trading futures, this indicator keeps your view aligned with how institutions see moving averages across timeframes.

🔧 Best For:

VIX & volatility traders

Short-term SPY/SPX traders

Swing traders who value clean setups

Anyone wanting a true 5-day trend anchor on any chart

[ayana] TFPS - TradFi Pressure ScoreTFPS - TradFi Pressure Score: Your Market Pressure Barometer

Understand what moves Wall Street, before it moves Crypto.

This indicator is your real-time barometer for the influence of traditional financial markets (TradFi) on Crypto. It measures the combined pressure from four key quadrants—Risk Appetite (S&P 500), Market Stress (VIX), Liquidity (DXY), and Macro Expectations (US10Y)—to answer one question: "Do I have a tailwind or a headwind from the global markets?"

How to Read Your "Cockpit" in 60 Seconds

The Main Line (Overall Market Pressure)

GREEN / ABOVE 0: Bullish Tailwind. The macro environment is supportive for Crypto.

RED / BELOW 0: Bearish Headwind. The macro environment is creating pressure on Crypto.

BRIGHT Color: Pressure is ACCELERATING.

DARK Color: Pressure is DECELERATING (losing momentum).

The Dashboard (Your Command Center)

Lead/Lag Analysis: The game-changer. Tells you if TradFi is currently leading the price or vice-versa. This is your key to knowing whether to watch macro news or focus on crypto-specifics.

TradFi Influence (R²): Shows you HOW RELEVANT the macro pressure is right now. High R² means Wall Street's influence is dominant. Low R² means crypto is moving on its own narrative.

Dynamic Weights: Reveals the market's primary NARRATIVE. Is the pressure coming from Fear (VIX), Liquidity (DXY), or general Risk Appetite (SPX)?

Extreme Signals (Reversal Zones)

Stress Cloud (Z-Score): Large, opaque bars warn of statistically EXTREME greed or fear levels.

Extreme Dots: Pinpoint the moments when pressure has likely reached an unsustainable peak, often preceding turning points.

Key Strategies & Use Cases

As a Trend Filter: Simply avoid fighting the color. Don't force long trades when the TFPS shows a strong red headwind.

For Precision Entry/Exits: Use the Extreme Dots and a decelerating color on the Main Line to time your entries in confluence with your own strategy.

For Strategic Decisions: Use the Lead/Lag and R² metrics to decide where to focus your attention and how to manage portfolio risk based on the current macro regime.

Configuration

For best results, leave the engine settings on their default (auto-adaptive) mode. The indicator's core intelligence lies in its ability to adapt to changing market dynamics automatically. You can adjust the visual theme to match your chart.

Institutional Analyst LLM📊 Institutional Analyst Board LLM – Smart Money Confluence Scanner for XAUUSD, Forex, Crypto 🔍 Overview The Institutional Analyst Board is a complete multi-timeframe smart money toolkit designed for traders who demand clarity, confluence, and precision. It brings together institutional-grade metrics—Order Blocks (OB), Fair Value Gaps (FVG), Liquidity Sweeps, MACD/RSI...

PTS Ultimate Analysis Board (Flexible Position + Ticker)

GoldenTradeClub

GoldenTradeClub

Updated

Jul 15

PTS Ultimate Analysis Board (Flexible Position + Ticker) Version: Pine v5 Description: This indicator builds a fully customizable, multi-timeframe dashboard table that surfaces 19 key metrics for any ticker (current chart TF, 1 h, 4 h). You can position the table at the top-right or bottom-right of your chart and toggle each metric on or off. Key...

Trading Engine AI Light

GoldenTradeClub

GoldenTradeClub

Jul 14

The Trading Engine includes the best and most effective technical analysis tools. It has 27 different Buy Signal parameters and 26 different Sell Signal parameters. Furthermore, it also has 9 Stop Loss triggers for Long Positions and 8 Stop Loss triggers for Short Positions. Many of the Buy or Sell Signal parameters function as Take Profit and Stop Loss signals...

Elliott Wave Complete

GoldenTradeClub

GoldenTradeClub

Jul 4

1. Indicator Presentation Name: Elliott Wave Complete Type: Pine Script v5 overlay dashboard for TradingView Purpose: Automates Elliott Wave motive (1-5) and corrective (A-B-C) pattern detection on any timeframe, enriches it with classic ZigZag pivots, dynamic Fibonacci projection levels, optional wave-count info box, and real-time alerts—all in one...

💀⚡ PTS WIZARD 666™ ULTIMATE SUPREME V5.0 - COMPLETE FIXED ⚡💀

GoldenTradeClub

GoldenTradeClub

Jul 4

1. Indicator Presentation Name: 💀⚡ PTS WIZARD 666™ ULTIMATE SUPREME V5.0 – COMPLETE FIXED Short ID: PTS-666-SUPREME Type: Pine Script v5 overlay dashboard for TradingView Purpose: An all-in-one trading overlay that integrates advanced WaveTrend momentum, RSI/MFI analysis, POC volume profiling, multiple Fibonacci golden/ultimate zones, volume footprint & imbalance...

🔥 PTS TRADE 666™ ULTIMATE BOOKMAP + QUANTUM ENGINE

GoldenTradeClub

GoldenTradeClub

Jul 4

1. Indicator Presentation Name: 🔥 PTS TRADE 666™ ULTIMATE BOOKMAP + QUANTUM ENGINE Short ID: PTS666_QUANTUM_FINAL Type: Pine Script v5 overlay dashboard for TradingView Purpose: A cutting-edge, institutional-grade suite that unifies bookmap-style footprint volume profiling, dynamic heatmap liquidity analysis, AI-driven pattern recognition, smart-money protocols,...

🔥 PTS TRADE 666™ - ULTIMATE INSTITUTIONAL TOOL 🔥

GoldenTradeClub

GoldenTradeClub

Jul 4

1. Indicator Presentation Name: 🔥 PTS TRADE 666™ – ULTIMATE INSTITUTIONAL TOOL V2.0 Short ID: PTS666_UIT_V2 Type: Pine Script v5 overlay dashboard for TradingView Purpose: Combines institutional-grade footprint volume analysis, smart-money structure detection, statistical anomaly checks, multi-timeframe divergence, Ichimoku insights, pattern recognition, and an...

PTS Wizard

GoldenTradeClub

GoldenTradeClub

Jul 4

1. Indicator Presentation Name: PTS Wizard Short Title: PTS Wizard Type: Pine Script v5 overlay dashboard for TradingView Purpose: A unified multi-strategy toolkit that overlays key market insights—liquidity zones, smart-money structure, footprint-style volume profile, consolidation ranges, statistical deviation bands, price forecasts, and session analysis—into a...

🔥 PTS.TRADE 666™ ULTIMATE HYBRID + MTF V3

GoldenTradeClub

GoldenTradeClub

Jul 4

1. Indicator Presentation Name: 🔥 PTS.TRADE 666™ ULTIMATE HYBRID + MTF V3 Short ID: PTS666_ULTIMATE_MTF_V3 Type: Overlay dashboard for TradingView Purpose: A next-level hybrid trading suite that merges institutional-grade order-flow analysis, smart-money concepts, AI-driven insights, classic momentum oscillators (WaveTrend, divergence, “Gold” signals),...

🧙♂ PTS WIZARD V3.0 - FINAL EDITION

GoldenTradeClub

GoldenTradeClub

Jul 4

1. Indicator Presentation Name: 🧙♂ PTS WIZARD V3.0 – FINAL EDITION Short Title: PTS-WIZARD-V3-FINAL Type: Overlay trading dashboard for TradingView Purpose: A comprehensive multi-module indicator that blends classic cipher momentum signals, Elliott Wave pattern detection, advanced statistical analyses (Z-Score, Benford’s Law, Ehlers SNR), footprint-style volume...

🧙♂ PTS WIZARD V3.0 + FOOTPRINT ULTIMATE

GoldenTradeClub

GoldenTradeClub

Jul 4

Name: PTS WIZARD V3.0 + FOOTPRINT ULTIMATE Type: Overlay trading dashboard for TradingView Purpose: Combines classic cipher-style momentum signals with an advanced footprint volume profile, multi-timeframe bias, statistical filters, and a fusion-score system—displayed in a customizable on-chart dashboard. Core Modules Cipher Momentum Signals WaveTrend...

🧙♂ PTS WIZARD V3.0 - BASIC

GoldenTradeClub

GoldenTradeClub

Jul 1

PTS WIZARD V3.0 Basic – Ultimate Multi-Tool Trading Dashboard An all-in-one overlay combining classic cipher signals, Elliott Wave pattern detection, volume analytics, divergence spotting, and smart-entry timing—backed by advanced statistical filters and a live dashboard. Key Features Cipher Signals WaveTrend with overbought/oversold zones & cross signals RSI...

Trading Engine vCD AI

GoldenTradeClub

GoldenTradeClub

Jun 15

The Trading Engine includes the best and most effective technical analysis tools. It has 27 different Buy Signal parameters and 26 different Sell Signal parameters. Furthermore, it also has 9 Stop Loss triggers for Long Positions and 8 Stop Loss triggers for Short Positions. Many of the Buy or Sell Signal parameters function as Take Profit and Stop Loss signals...

Trading Engine vCD

GoldenTradeClub

GoldenTradeClub

Updated

Mar 21

The Trading Engine includes the best and most effective technical analysis tools. It has 27 different Buy Signal parameters and 26 different Sell Signal parameters. Furthermore, it also has 9 Stop Loss triggers for Long Positions and 8 Stop Loss triggers for Short Positions. Many of the Buy or Sell Signal parameters function as Take Profit and Stop Loss signals...

TE CLIENT v13

GoldenTradeClub

GoldenTradeClub

Updated

Mar 15

The Trading Engine includes the best and most effective technical analysis tools. It has 27 different Buy Signal parameters and 26 different Sell Signal parameters. Furthermore, it also has 9 Stop Loss triggers for Long Positions and 8 Stop Loss triggers for Short Positions. Many of the Buy or Sell Signal parameters function as Take Profit and Stop Loss signals...

Trading Engine v13

GoldenTradeClub

GoldenTradeClub

Updated

Mar 15

The Trading Engine includes the best and most effective technical analysis tools. It has 27 different Buy Signal parameters and 26 different Sell Signal parameters. Furthermore, it also has 9 Stop Loss triggers for Long Positions and 8 Stop Loss triggers for Short Positions. Many of the Buy or Sell Signal parameters function as Take Profit and Stop Loss signals...

Trading Engine B2B

GoldenTradeClub

GoldenTradeClub

Updated

Jan 14

The Trading Engine includes the best and most effective technical analysis tools. It has 25 different Buy Signal parameters and 24 different Sell Signal parameters. Furthermore, it also has 9 Stop Loss triggers for Long Positions and 8 Stop Loss triggers for Short Positions. Many of the Buy or Sell Signal parameters function as Take Profit and Stop Loss signals...

Trading Engine B2B FX V9

GoldenTradeClub

GoldenTradeClub

Updated

Jan 14

The VFLOW Trading Engine includes the best and most effective technical analysis tools. It has 20 different Buy Signal parameters and 18 different Sell Signal parameters. Furthermore, it also has 7 Stop Loss triggers for Long Positions and 5 Stop Loss triggers for Short Positions. Many of the Buy or Sell Signal parameters function as Take Profit and Stop Loss...

English

Select market data provided by ICE Data services.

Select reference data provided by FactSet. Copyright © 2025 FactSet Research Systems Inc.

© 2025 TradingView, Inc.

More than a product

Supercharts

Screeners

Stocks

ETFs

Bonds

Crypto coins

CEX pairs

DEX pairs

Pine

Heatmaps

Stocks

ETFs

Crypto

Calendars

Economic

Earnings

Dividends

More products

Yield Curves

Options

News Flow

Pine Script®

Apps

Mobile

Desktop

Tools & subscriptions

Features

Pricing

Market data

Trading

Overview

Brokers

Special offers

CME Group futures

Eurex futures

US stocks bundle

About company

Who we are

Athletes

Blog

Careers

Media kit

Merch

TradingView store

Tarot cards for traders

The C63 TradeTime

Policies & security

Terms of Use

Disclaimer

Privacy Policy

Cookies Policy

Accessibility Statement

Security tips

Bug Bounty program

Status page

Community

Social network

Wall of Love

Refer a friend

House Rules

Moderators

Ideas

Trading

Education

Editors' picks

Pine Script

Indicators & strategies

Wizards

Freelancers

Business solutions

Widgets

Charting libraries

Lightweight Charts™

Advanced Charts

Trading Platform

Growth opportunities

Advertising

Brokerage integration

Partner program

Education program

Look First

Close

Updated 3 hours ago

Institutional Analyst Board

Manage access

Remove from favorites

Use on chart

0

11

Jul 19

📊 Institutional Analyst Board – Smart Money Confluence Scanner for XAUUSD, Forex, Crypto

🔍 Overview

The Institutional Analyst Board is a complete multi-timeframe smart money toolkit designed for traders who demand clarity, confluence, and precision. It brings together institutional-grade metrics—Order Blocks (OB), Fair Value Gaps (FVG), Liquidity Sweeps, MACD/RSI bias, VWAP positioning, and Break of Structure (BoS)—into a single powerful visual dashboard.

This indicator is especially optimized for Gold (XAUUSD) but is also compatible with Crypto and Forex assets.

🧠 Key Features

✅ Multi-Timeframe Dashboard (5M / 15M / 1H)

✅ Order Block Detection with dynamic zones that extend until broken

✅ Fair Value Gap Detection with clear zone shading and border distinction

✅ MACD + RSI Confluence for momentum and bias alignment

✅ VWAP Positioning to identify premium/discount zones

✅ Liquidity Sweeps (internal/external range breaks)

✅ Killzone Highlighting (Asia / London / New York)

✅ Break of Structure (BoS) with advanced confluence filters

✅ Gold Bias Flags across timeframes (BUY / SELL / NEUTRAL)

✅ Dynamic Price Watermark with real-time data

✅ Fully customizable colors, transparencies, and text labels

🧠 How It Works

The Board uses institutional logic to analyze the chart in real time:

Metric Purpose

OB Zones Highlight potential smart money footprints where price is likely to react.

FVG Zones Identify imbalance areas between buyers and sellers—ideal for mean reversion entries.

MACD/RSI Confirm momentum direction and relative strength confluence.

VWAP Determine whether price is trading at a premium or discount.

Liquidity Sweeps Detect manipulative moves before major reversals.

BoS Mark potential trend reversals, filtered by institutional confluence.

Each signal is computed across 3 timeframes and visualized in a clean board that updates live. You’ll also see labels, alerts, and session overlays for maximum clarity.

📌 Ideal Use Case

This tool is perfect for:

Funded Challenge Traders (FTMO, MyForexFunds, etc.)

Gold scalpers and intraday traders

Crypto price action traders using BTC, ETH, SOL, etc.

Smart Money Concept (SMC) and ICT followers

⚙️ Customization Options

Toggle each module (OB, FVG, VWAP, MACD/RSI, etc.)

Set transparency and color for each zone type

Adjust Killzone timing (Asia, London, NY)

Control board position (Top/Bottom) and metric visibility

📈 Compatible Assets

✅ XAUUSD (optimized)

✅ Forex majors/minors

✅ Crypto pairs (BTC, ETH, SOL, etc.)

✅ Indices (GER40, NASDAQ, SPX with minor adaptation)

🛠️ Requirements

Use on TradingView v5

Set chart time to UTC+0 or UTC+3 for optimal Killzone accuracy

For crypto, redefine Killzone hours if needed (24/7 market)

🧠 Pro Tip

Pair this indicator with volume profile tools, CVD/Delta Flow, or Footprint overlays to build high-confidence trade setups with clear institutional confluence.

NDX Levels Adjusted to Active TickerThis indicator allows you to plot custom NDX levels directly on the NQ1! (E-mini NASDAQ-100 Futures) chart, automatically adjusting for the spread between NDX and NQ1!. This is particularly useful for traders who perform technical analysis on NDX but execute trades on NQ1!.

Features:

Input up to three NDX key levels to track (e.g., 23000, 24000, 25000).

The script adjusts these levels in real-time based on the current spread between NDX and NQ1!

Displays the spread in the chart header for quick reference

Plots updated horizontal lines that move with the spread

Includes optional labels showing the spread periodically to reduce clutter

Supports Multiple Tickers: NQ1!, QQQ, NAS100 and NAS100USD.

Ideal for futures traders who want SPX context while trading NQ1!, QQQ, NAS100 or NAS100USD..

IV PercentileIV Percentile Indicator - Brief Description

What It Does

The IV Percentile Indicator measures where current implied volatility ranks compared to the past year, showing what percentage of time volatility was lower than today's level.

How It Works

Data Collection:

Tracks implied volatility (or historical volatility as proxy) for each trading day

Stores the last 252 days (1 year) of volatility readings

Uses VIX data for SPY/SPX, historical volatility for other stocks

Calculation:

IV Percentile = (Days with IV below current level) ÷ (Total days) × 100

Example: If IV Percentile = 75%, it means current volatility is higher than 75% of the past year's readings.

Visual Output

Main Display:

Blue line showing percentile (0-100%)

Reference lines at key levels (20%, 30%, 50%, 70%, 80%)

Color-coded backgrounds for quick identification

Info table with current readings

Key Levels:

80%+ (Red): Very high IV → Sell premium

70-79% (Orange): High IV → Consider selling

30-20% (Green): Low IV → Consider buying

<20% (Bright Green): Very low IV → Buy premium

Trading Application

When IV Percentile is HIGH (70%+):

Options are expensive relative to recent history

Good time to sell premium (iron condors, credit spreads)

Expect volatility to decrease toward normal levels

When IV Percentile is LOW (30%-):

Options are cheap relative to recent history

Good time to buy premium (straddles, long options)

Expect volatility to increase from compressed levels

Core Logic

The indicator helps answer: "Is this a good time to buy or sell options based on how expensive/cheap they are compared to recent history?" It removes the guesswork from volatility timing by providing historical context for current option prices.

Reversal Signal avec TICK + RSIThis indicator is a potential reversal indicator for SCALPING, don't use it for swing. It's base on TICK and on an overbrought/oversold condition of the RSI. You can play with the setting, typicaly I like my TICK to be over reacting an 800/-800 and my rsi over 20 and 80, but it give not enough signal. So I set the TICK signal at 651/-651 and the RSI at 25/75. This indicator is made for SP500 and Nasdaq, so SPY/QQQ/SPX/ES/NQ should work well. It's the first version of it, so maybe I'll add so more data to it to increase signal and lower false one. For now I've test it on live market yet(26/7/25).

The RSI is Fast(5 period), I like to use it on the 1 or 5 min chart.

Please not that it only work during 9h30am to 4pm EST.(Because of the TICK)

Feel free to try and even comment. Don't be harsh on me, it's my first try!

(Sorry for my 'english' it's not my first language)

FAUCON

Mean Reversion Trading With IV Metrics (By MC) - Mobile FriendlyThis script is a comprehensive toolkit for traders who want to combine price mean reversion analysis with advanced volatility metrics, including Implied Volatility Rank (IVR), Implied/“Fair” Volatility projections, and real-time market volatility indicators. It is optimized for both desktop and mobile use, providing a detailed statistics table directly on the chart, and is suitable for stocks, ETFs, indices, and even paired asset analysis.

Key Features & How They Work Together

1. Mean Reversion Probability & Z-Score

Mean Reversion Analysis: Calculates z-scores and statistical probabilities that the asset’s price will revert to its mean, using customizable lookback windows (e.g., 10-60 bars). This helps traders spot potentially overbought or oversold conditions.

Strong & Moderate Signals: Highlights strong and moderate reversion opportunities based on user-defined probability thresholds, providing clear visual cues for timing entries and exits.

2. Paired Asset Correlation

Pairs Trading Support: Allows comparison of two symbols (e.g., SPY vs TLT). It computes the ratio, rolling mean, standard deviation, and correlation, helping traders identify divergence/convergence opportunities in pairs trading.

3. Volatility Metrics & Projections

Historical & Implied Volatility: Estimates implied volatility (IV) using historical price data, calculates IVR (the asset’s IV relative to its own history), and provides user-customized percentile bands (e.g., 20th/80th percentiles).

Fair IV Calculation: Offers three methods to compute “fair” volatility:

Market-Aware (relative to VIX/SPX HV)

SMA of historical volatility

SMA of VIX Traders can choose the method that best fits current market conditions.

Future Projections: Projects IV, “Fair” IV, and IVR for a user-defined future period, giving insight into potential volatility trends.

4. Implied Move Range

Implied Move Calculation: Shows the expected price range (upper/lower bounds) for the forecast period based on the current IV, making risk management and target setting more objective.

Dynamic Labels: Automatically updates labels with the latest projected moves and bounds, keeping traders informed in real time.

5. Market Volatility Dashboard

Broad Market Indicators: Displays real-time values and daily changes for VIX, VIX1D, VVIX, MOVE (bond volatility), GVZ (gold volatility), and OVX (oil volatility). Color-coded thresholds help traders gauge market stress across asset classes.

Correlation to SPY: Shows how closely the asset moves with SPY, aiding in diversification and hedging decisions.

6. Performance Metrics

Daily Move Analysis: Tracks today’s price move (absolute and percentage), average rises/falls, and the percentage of green/red days over a custom period.

Trade Quality Assessment: Ranks trade opportunities (High/Moderate/Low/Very Low) based on mean reversion probability.

7. Highly Customizable Table

Mobile Friendly: The stats table can be placed anywhere on the chart, toggled between compact/full/extra modes, and resized for readability on any device.

Visual Cues: Color coding and dynamic labels make interpretation easy and fast.

8. Alert Conditions

Built-in alerts for strong/moderate mean reversion, IV crossing above/below “Fair” IV, allowing proactive trade management.

9. VIX-Based Expected Move Bands

Optionally plots ±1, 2, 3 standard deviation bands using VIX-based expected move, helping to visualize potential price extremes.

How These Features Help Traders

Unified Trading Dashboard: All key mean reversion and volatility insights are available at a glance, reducing the need to switch between multiple indicators or screens.

Informed Entries & Exits: By combining mean reversion probabilities, IV projections, and market volatility, traders can time trades more confidently and avoid false signals.

Risk Management: The implied move bounds and volatility levels support realistic stop-loss and target setting, adapting dynamically to market conditions.

Cross-Asset Awareness: Market-wide volatility metrics and asset correlation to SPY provide context, helping traders avoid surprises from macro shocks.

Pairs Trading: Direct support for ratio and correlation analysis streamlines pairs strategies.

Customization & Clarity: The flexible UI and color-coded stats make the tool accessible for both beginners and advanced users.

Mean Reversion, Correlation value & interpretation:

For Meant Reversion % Probability:

Lookback Period to use:

| Trading Horizon | Lookback Period (Length) | Rationale |

| 5–10 days | 10–20 bars | More sensitive, good for quick reversals |

| 10–20 days | 20–30 bars | Standard for short swing |

| 20–40 days | 40–60 bars | More stable mean for longer swing |

Interpretation Guide:

Only consider trades if Correlation ≥ 0.6 or Reversion % ≥ 75%.

Avoid trades with Reversion % < 20%.

Correlation and Reversion % together form a powerful trade quality filter.

| Reversion % | Correlation | Signal Strength | Action |

| ≥ 75% | ≥ 0.4 | High Probability | Consider full position |

| ≥ 50% | ≥ 0.6 | Moderate Probability | Trade with standard size |

| ≥ 75% | < 0.4 | Uncorrelated Edge | Trade small or hedge carefully |

| < 50% | Any | Weak | Avoid |

| Any | < 0.3 | Low Coherence | Avoid unless extreme Reversion |

| Correlation Value | Interpretation |

| +1.0 | Perfect positive correlation (price of both move in the same direction)|

| +0.7 to +0.9 | Strong positive correlation |

| +0.4 to +0.6 | Moderate positive correlation |

| 0 | No correlation (independent) |

| -0.4 to -0.6 | Moderate negative correlation |

| -0.7 to -0.9 | Strong negative correlation |

| -1.0 | Perfect negative correlation (price both move in the opposite direction)|

Summary:

This script empowers traders to navigate markets with a robust, data-driven approach, seamlessly blending mean reversion analytics with deep volatility insight—all in a mobile-friendly, customizable dashboard.

Disclaimer

This tool is for informational and educational purposes only. It does not provide financial advice or trading signals. Always do your own research and consult a professional before making investment decisions.

FG_Index v1.5.3 Pro (Multi-Asset Time4H) === FG_Index 4H Sentiment Indicator ===

// 多品种4小时情绪评分指标,适用于黄金、比特币、美股、原油等。

// 分数范围 0~100:

// - score > 70:贪婪,考虑减仓

// - score < 30:恐慌,关注低吸

// - score > 80:极度贪婪,注意风险

// - score < 20:极度恐慌,可能超卖

// 建议搭配趋势/结构指标一起使用

// 图表自动显示主因子解释,辅助判断情绪来源

//

// === English Usage ===

// FG_Index is a 4H sentiment score indicator for multi-assets (Gold, BTC, SPX, Oil, etc.).

// Score scale: 0–100

// - score > 70: Greed – consider reducing positions

// - score < 30: Fear – potential buy zone

// - score > 80: Extreme greed – risk warning

// - score < 20: Extreme fear – may be oversold

// Recommended to use with trend/structure filters

// Top factor contributions are displayed on chart

Custom Portfolio [BackQuant]Custom Portfolio {BackQuant]

Overview

This script turns TradingView into a lightweight portfolio optimizer with institutional-grade analytics and real-time position management capabilities.

Rank up to 15 tickers every bar using a pair-wise relative-strength "league table" that compares each asset against all others through your choice of 12 technical indicators.

Auto-allocate 100% of capital to the single strongest asset and optionally apply dynamic leverage when the aggregate market is trending, with full position tracking and rebalancing logic.

Track performance against a custom buy-and-hold benchmark while watching a fully fledged stats dashboard update in real time, including 15 professional risk metrics.

How it works

Relative-strength engine – Each asset is compared against every other asset with a user-selectable indicator (default: 9/21 EMA cross). The system generates a complete comparison matrix where Asset A vs Asset B, Asset A vs Asset C, and so on, creating strength scores. The summed scores crown a weekly/daily/hourly "winner" that receives the full allocation.

Regime filter – A second indicator applied to TOTAL crypto-market cap (or any symbol you choose) classifies the environment as trending or mean-reverting . Leverage activates only in trending regimes, protecting capital during choppy or declining markets. Choose from indicators like Universal Trend Model, Relative Strength Overlay, Momentum Velocity, or Custom RSI for regime detection.

Capital & position logic – Equity grows linearly when flat and multiplicatively while invested. The system tracks entry prices, calculates returns including leverage adjustments, and handles position transitions seamlessly. Optional intra-trade leverage rebalancing keeps exposure in sync with market conditions, recalculating position sizes as regime conditions change.

Risk & performance analytics – Every confirmed bar records return, drawdown, VaR/CVaR, Sharpe, Sortino, alpha/beta vs your benchmark, gain-to-pain, Calmar, win-rate, Omega ratio, portfolio variance, skewness, and annualized statistics. All metrics render in a professional table for instant inspection with proper annualization based on your selected trading days (252 for traditional markets, 365 for crypto).

Key inputs

Backtest window – Hard-code a start date or let the script run from series' inception with full date range validation.

Asset list (15 slots) – Works with spot, futures, indices, even synthetic spreads (e.g., BYBIT:BTCUSDT.P). The script automatically cleans ticker symbols for display.

Indicator universe – Switch the comparative metric to DEMA, BBPCT, LSMAz adaptive scores, Volatility WMA, DEMA ATR, Median Supertrend, and more proprietary indicators.

With more always being added!

Leverage settings – Max leverage from 1x to any multiple, auto-rebalancing toggle, trend/reversion thresholds with precision controls.

Visual toggles – Show/hide equity curve, rolling drawdown heat-map, daily PnL spikes, position label, advanced metrics table, buy-and-hold comparison equity.

Risk-free rate input – Customize the risk-free rate for accurate Sharpe ratio calculations, supporting both percentage and decimal inputs.

On-chart visuals

Color-coded equity curve with "shadow" offset for depth perception that changes from green (profitable) to red (losing) based on recent performance momentum.

Rolling drawdown strip that fades from light to deep red as losses widen, with customizable maximum drawdown scaling for visual clarity.

Optional daily-return histogram line and zero reference for understanding day-to-day volatility patterns.

Bottom-center table prints the current winning ticker in real time with clean formatting.

Top-right metrics grid updates every bar with 15 key performance indicators formatted to three decimal places for precision.

Benchmark overlay showing buy-and-hold performance of your selected index (default: SPX) for relative performance comparison.

Typical workflow

Add the indicator on a blank chart (overlay off).

Populate ticker slots with the assets you actually trade from your broker's symbol list.

Pick your momentum or mean-reversion metric and a regime filter that matches your market hypothesis.

Set max leverage (1 = spot only) and decide if you want dynamic rebalancing.

Press the little " L " on the price axis to view the equity curve in log scale for better long-term visualization.

Enable the metrics table to monitor Sharpe, Sortino, and drawdown in real time.

Iterate through different asset combinations and indicator settings; compare performance vs buy-and-hold; refine until you find robust parameters.

Who is it for?

Systematic crypto traders looking for a one-click, cross-sectional rotation model with professional risk management.

Portfolio quants who need rapid prototyping without leaving TradingView or exporting to Python/R.

Swing traders wanting an at-a-glance health check of their multi-coin basket with instant position signals.

Fund managers requiring detailed performance attribution and risk metrics for client reporting.

Researchers backtesting momentum and mean-reversion strategies across multiple assets simultaneously.

Important notes & tips

Set Trading Days in a Year to 252 for traditional markets; 365 for 24/7 crypto to ensure accurate annualization.

CAGR and Sharpe assume the backtest start date you choose—short windows can inflate stats, so test across multiple market cycles.

Leverage is theoretical; always confirm your broker's margin rules and account for funding costs not modeled here.

The script is computationally heavy at 15 assets due to the N×N comparison matrix—reduce the list or lengthen the timeframe if you hit execution limits.

Best results often come from mixing assets with different volatility profiles rather than highly correlated instruments.

The regime filter symbol can be changed from CRYPTOCAP:TOTAL to any broad market index that represents your asset universe.

Orthogonal Projections to Latent Structures (O-PLS)Version 0.1

Orthogonal Projections to Latent Structures (O-PLS) Indicator for TradingView

This indicator, named "Orthogonal Projections to Latent Structures (O-PLS)", is designed to help traders understand the relevance or predictive power of various market variables on the future close price of the asset it's applied to. Unlike standard correlation coefficients that show a simple linear relationship, O-PLS aims to separate variables into "predictive" (relevant to Y) and "orthogonal" (irrelevant noise) components. This Pine Script indicator provides a simplified proxy of the relevance score derived from O-PLS principles.

Purpose of the Indicator

The primary purpose of this indicator is to identify which technical factors (such as price, volume, and other indicators) have the strongest relationship with the future price movement of the current trading instrument. By providing a "relevance score" for each input variable, it helps traders focus on the most influential data points, potentially leading to more informed trading decisions.

Inputs

The indicator offers the following user-definable inputs:

* **Lookback Period:** This integer input (default: 100, min: 10, max: 500) determines the number of past bars used to calculate the relevance scores for each variable. A longer lookback period considers more historical data, which can lead to smoother, less reactive scores but might miss recent shifts in variable importance.

* **External Asset Symbol:** This symbol input (default: `BINANCE:BTCUSDT`) allows you to specify an external asset (e.g., `BINANCE:ETHUSDT`, `NASDAQ:TSLA`) whose close price will be included in the analysis as an additional variable. This is useful for cross-market analysis to see how other assets influence the current chart.

* **Plot Visibility Checkboxes (e.g., "Plot: Open Price Relevance", "Plot: Volume Relevance", etc.):** These boolean checkboxes allow you to toggle the visibility of individual relevance score plots on the chart, helping to declutter the display and focus on specific variables.

Outputs

The indicator provides two main types of output:

Relevance Score Plots: These are lines plotted in a separate pane below the main price chart. Each line corresponds to a specific market variable (Open Price, Close Price, High Price, Low Price, Volume, various RSIs, SMAs, MFI, and the External Asset Close). The value of each line represents the calculated "relevance score" for that variable, typically scaled between 0 and 10. A higher score indicates a stronger predictive relationship with the future close price.

Sorted Relevance Table : A table displayed in the top-right corner of the chart provides a clear, sorted list of all analyzed variables and their corresponding relevance scores. The table is sorted in descending order of relevance, making it easy to identify the most influential factors at a glance. Each variable name in the table is colored according to its plot color, and the external asset's name is dynamically displayed without the "BINANCE:" prefix.

How to Use the Indicator

1. **Add to Chart:** Apply the "Orthogonal Projections to Latent Structures (O-PLS)" indicator to your desired trading chart (e.g., ETH/USDT).

2. **Adjust Inputs:**

* **Lookback Period:** Experiment with different lookback periods to see how the relevance scores change. A shorter period might highlight recent correlations, while a longer one might show more fundamental relationships.

* **External Asset Symbol:** If you trade BTC/USDT, you might add ETH/USDT or SPX as an external asset to see its influence.

3. **Analyze Relevance Scores:**

* **Plots:** Observe the individual relevance score plots over time. Are certain variables consistently high? Do scores change before significant price moves?

* **Table:** Refer to the sorted table on the latest confirmed bar to quickly identify the top-ranked variables.

4. **Incorporate into Strategy:** Use the insights from the relevance scores to:

* Prioritize certain indicators or price actions in your trading strategy. For example, if "Volume" has a high relevance score, it suggests volume confirmation is critical for future price moves.

* Understand the influence of inter-market relationships (via the External Asset Close).

How the Indicator Works

The indicator works by performing the following steps on each bar:

1. **Data Fetching:** It gathers historical data for various price components (open, high, low, close), volume, and calculated technical indicators (SMA, RSI, MFI) for the specified `lookback` period. It also fetches the close price of an `External Asset Symbol` .

2. **Standardization (Z-scoring):** All collected raw data series are standardized by converting them into Z-scores. This involves subtracting the mean of each series and dividing by its standard deviation . Standardization is crucial because it brings all variables to a common scale, preventing variables with larger absolute values from disproportionately influencing the correlation calculations.

3. **Correlation Calculation (Proxy for O-PLS Relevance):** The indicator then calculates a simplified form of correlation between each standardized input variable and the standardized future close price (Y variable) . This correlation is a proxy for the relevance that O-PLS would identify. A high absolute correlation indicates a strong linear relationship.

4. **Relevance Scaling:** The calculated correlation values are then scaled to a range of 0 to 10 to provide an easily interpretable "relevance score" .

5. **Output Display:** The relevance scores are presented both as time-series plots (allowing observation of changes over time) and in a real-time sorted table (for quick identification of top factors on the current bar) .

How it Differs from Full O-PLS

This indicator provides a *simplified proxy* of O-PLS principles rather than a full, mathematically rigorous O-PLS model. Here's why and how it differs:

* **Dimensionality Reduction:** A full O-PLS model would involve complex matrix factorization techniques to decompose the independent variables (X) into components that are predictive of Y and components that are orthogonal (unrelated) to Y but still describe X's variance. Pine Script's array capabilities and computational limits make direct implementation of these matrix operations challenging.

* **Orthogonal Components:** A true O-PLS model explicitly identifies and removes orthogonal components (noise) from the X data that are unrelated to Y. This indicator, in its simplified form, primarily focuses on the direct correlation (relevance) between each X variable and Y after standardization, without explicitly modeling and separating these orthogonal variations.

* **Predictive Model:** A full O-PLS model is ultimately a predictive model that can be used for regression (predicting Y). This indicator, however, focuses solely on **identifying the relevance/correlation of inputs to Y**, rather than building a predictive model for Y itself. It's more of an analytical tool for feature importance than a direct prediction engine.

* **Computational Intensity:** Full O-PLS involves Singular Value Decomposition (SVD) or Partial Least Squares (PLS) algorithms, which are computationally intensive. The indicator uses simpler statistical measures (mean, standard deviation, and direct correlation calculation over a lookback window) that are feasible within Pine Script's execution limits.

In essence, this Pine Script indicator serves as a practical tool for gaining insights into variable relevance, inspired by the spirit of O-PLS, but adapted for the constraints and common use cases of a TradingView environment.

Spread AnalysisSpread Analysis - Futures vs Spot Price Analysis

Advanced spread analysis tool that compares futures/perp prices with spot prices across multiple exchanges, providing insights into market sentiment and potential trading opportunities.

Multi-Asset Support: Automatically detects and analyzes crypto perpetual vs spot spreads, index futures vs cash indices (ES/SPX, NQ/NDX, YM/DJI), and commodity futures vs spot prices (GC/GOLD, CL/USOIL)

Multi-Exchange Aggregation: For crypto, aggregates prices from Binance, BitMEX, Kraken, Bybit, OKX, and Coinbase to calculate mean perp and spot prices

Z-Score Based Alerts: Uses statistical Z-score analysis to identify extreme spread conditions that may signal potential reversals or continuation patterns

Visual Histogram Display: Shows spread differences as colored columns - green for futures premium, red for futures discount

Flexible Calculation Methods: Supports absolute price differences, percentage spreads, or basis point calculations

Trading Applications: Identify market sentiment divergence, spot potential reversal opportunities, and confirm trend strength

Risk Management: Use extreme Z-scores to identify overvalued conditions and potential mean reversion setups

Market Analysis: Understand the relationship between futures and spot markets across different asset classes

Timing Tool: Spread momentum often precedes price moves, providing early signals for entry/exit decisions

Perfect for traders who want to understand the relationship between futures and spot markets, identify divergences, and spot potential reversal opportunities across crypto, indices, and commodities.

Key Features:

• Automatic asset detection and appropriate spread calculation

• Configurable Z-score alerts for extreme conditions

• Comprehensive tooltips and information guide

• Multiple calculation methods (absolute, percentage, basis points)

• Clean, customizable visual display

Use Cases:

• Crypto traders analyzing perp vs spot relationships

• Futures traders monitoring basis relationships

• Mean reversion strategies using extreme spreads

• Trend confirmation using spread momentum

• Market sentiment analysis across asset classes

NY Open Breakout [ATR-5000]# **New York Open Breakout Indicator **

## **📌 Overview**

This **Pine Script** indicator identifies high-probability breakout opportunities at the **New York market open (13:30 UTC)** based on **volatility filters** using **customizable ATR periods and thresholds**.

### **🔹 Key Features**

✅ **Fully Customizable ATR Periods** (2 to **5000** bars)

✅ **Adjustable Thresholds** (0.01% to 5.00%)

✅ **Opening Range (OR) Filter** (0.01% to 5.00%)

✅ **Clean Visuals** – Only highlights the **13:30 UTC candle** when conditions are met

✅ **Real-Time Info Panel** – Displays current ATR & threshold settings

✅ **Automatic Daily Reset** – Fresh signals every trading day

---

## **📊 How It Works**

### **1️⃣ Volatility Check (13:25 UTC)**

- Calculates **two ATR values** (user-defined periods)

- Compares them against **custom % thresholds**

- Only proceeds if **both ATRs exceed** their required volatility levels

### **2️⃣ Opening Range Confirmation (13:30 UTC)**

- Measures the **high-low range** of the 13:30 candle

- Validates if the range meets the **minimum % threshold**

- If all conditions pass → **Highlights the candle** in your chosen color

### **3️⃣ Visual Feedback**

- **🟣 Colored Candle** → Valid breakout signal

- **📊 Info Table** → Shows current ATR settings & thresholds

---

## **⚙️ Customization Options**

| **Setting** | **Default** | **Adjustable Range** |

|---------------------------|------------|----------------------|

| **First ATR Period** | 14 | **2–5000** bars |

| **Second ATR Period** | 161 | **2–5000** bars |

| **First ATR Threshold** | 0.42% | **0.01%–5.00%** |

| **Second ATR Threshold** | 0.40% | **0.01%–5.00%** |

| **OR Range Threshold** | 0.42% | **0.01%–5.00%** |

| **Candle Color** | Purple | **Any color** |

---

## **📈 Best Use Cases**

✔ **Forex (EURUSD, GBPUSD)** – Captures NY session momentum

✔ **Indices (SPX, NASDAQ)** – Works well with opening volatility

✔ **Commodities (Gold, Oil)** – Filters out low-energy days

---

## **🔧 How to Adjust Settings**

1. **Click the gear icon (⚙️)** on your TradingView chart

2. **Modify ATR periods & thresholds** as needed

3. **Change the candle color** for better visibility

---

## **🚀 Why This Indicator?**

- **No repainting** – Signals lock in after candle close

- **No clutter** – Only marks valid 13:30 candles

- **Adaptable** – Works on **any market & timeframe**

- **Fully automated** – No manual adjustments needed

---

### **📥 Apply & Start Trading!**

Simply **load the script** on TradingView and customize it to fit your strategy! 🚀

Daily GEX Zones & Dashboard by JCThis script plots daily options-driven gamma zones alongside a live sentiment dashboard to help traders visualize dealer positioning, support/resistance clusters, and expected price behavior.

Features:

📅 Date-based GEX Zones: Automatically draws GEX Resistance, GEX Support, Max Pain Zone, and Zero Gamma Line for a specific trading day.

📊 Gamma Flow Dashboard: Displays real-time GEX, DEX, Vanna, and Charm flows using intuitive dropdowns (Negative, Neutral, Positive) — no manual number typing.

🔢 Combo ID Calculation: Combines your gamma flow selections into a single Combo ID, quantifying net positioning pressure.

🎯 Automatic Bias Classification: Instantly highlights whether the day’s gamma structure is likely Pinned/Stable, Unpinned/Wild, Choppy, or Trap/Expansion — color-coded for quick reading.

📈 Zero Gamma Lines: Plots two critical levels where gamma flips from long to short, providing valuable confluence for intraday support/resistance.

How to Use:

1️⃣ Pick your target date (e.g., current day) to activate the GEX boxes.

2️⃣ Enter the day’s Resistance Wall, Support Wall, Max Pain, and Zero Gamma levels from your option chain analysis.

3️⃣ Use the radio-style dropdowns to select sentiment for GEX, DEX, Vanna, and Charm based on your interpretation of open interest, hedging, dealer flow, and market structure.

4️⃣ The dashboard will auto-calculate your Combo ID and bias class.

Designed for:

SPX, SPY, QQQ, NVDA, or any high-liquidity underlying with active options flow.

Active day traders, gamma scalpers, and market makers tracking dealer positioning.

Tip:

Combine with price action levels, VWAP, and intraday structure for high probability trade zones.

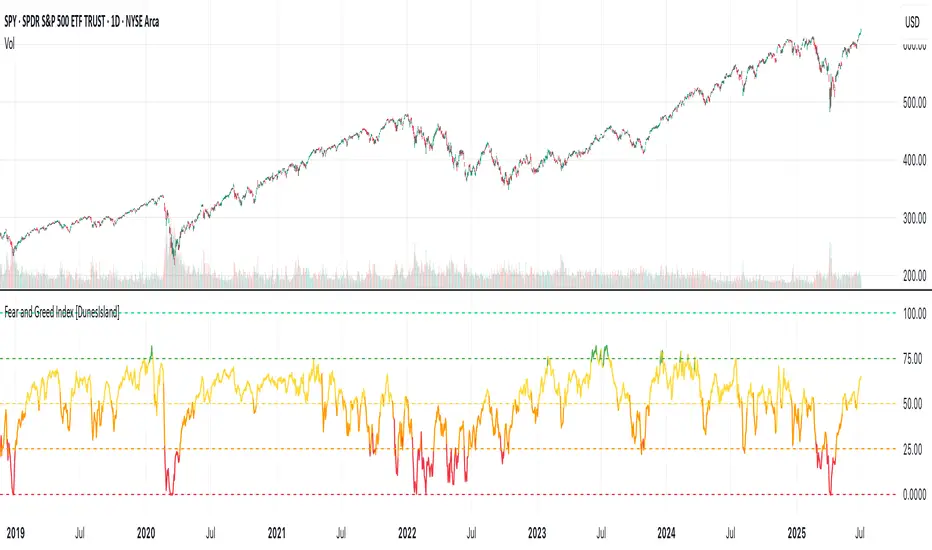

Fear and Greed Index [DunesIsland]The Fear and Greed Index is a sentiment indicator designed to measure the emotions driving the stock market, specifically investor fear and greed. Fear represents pessimism and caution, while greed reflects optimism and risk-taking. This indicator aggregates multiple market metrics to provide a comprehensive view of market sentiment, helping traders and investors gauge whether the market is overly fearful or excessively greedy.How It WorksThe Fear and Greed Index is calculated using four key market indicators, each capturing a different aspect of market sentiment:

Market Momentum (30% weight)

Measures how the S&P 500 (SPX) is performing relative to its 125-day simple moving average (SMA).

A higher value indicates that the market is trading well above its moving average, signaling greed.

Stock Price Strength (20% weight)

Calculates the net number of stocks hitting 52-week highs minus those hitting 52-week lows on the NYSE.

A greater number of net highs suggests strong market breadth and greed.

Put/Call Options (30% weight)

Uses the 5-day average of the put/call ratio.

A lower ratio (more call options being bought) indicates greed, as investors are betting on rising prices.

Market Volatility (20% weight)

Utilizes the VIX index, which measures market volatility.

Lower volatility is associated with greed, as investors are less fearful of large market swings.

Each component is normalized using a z-score over a 252-day lookback period (approximately one trading year) and scaled to a range of 0 to 100. The final Fear and Greed Index is a weighted average of these four components, with the weights specified above.Key FeaturesIndex Range: The index value ranges from 0 to 100:

0–25: Extreme Fear (red)

25–50: Fear (orange)

50–75: Neutral (yellow)

75–100: Greed (green)

Dynamic Plot Color: The plot line changes color based on the index value, visually indicating the current sentiment zone.

Reference Lines: Horizontal lines are plotted at 0, 25, 50, 75, and 100 to represent the different sentiment levels: Extreme Fear, Fear, Neutral, Greed, and Extreme Greed.

How to Interpret

Low Values (0–25): Indicate extreme fear, which may suggest that the market is oversold and could be due for a rebound.

High Values (75–100): Indicate greed, which may signal that the market is overbought and could be at risk of a correction.

Neutral Range (25–75): Suggests a balanced market sentiment, neither overly fearful nor greedy.

This indicator is a valuable tool for contrarian investors, as extreme readings often precede market reversals. However, it should be used in conjunction with other technical and fundamental analysis tools for a well-rounded view of the market.

Daily Trading Barometer (DTB) with DJIA OverlayThe "Daily Trading Barometer (DTB) with DJIA Overlay" is a custom technical indicator designed to identify intermediate-term overbought and oversold conditions in the stock market, inspired by Edson Gould's original DTB methodology. This indicator combines three key components:

A 7-day advance-decline oscillator, a 20-day volume oscillator, and a 28-day DJIA price ratio, normalized into a composite index scaled around 110–135. Values below 110 signal potential oversold conditions, while values above 135 indicate overbought territory, aiding in timing market reversals.

The overlay of a normalized DJIA plot allows for visual correlation with the broader market trend. Use this tool to anticipate turning points in oscillating markets, though it’s best combined with other indicators for confirmation. Ideal for traders seeking probabilistic insights into bear or bull market transitions.

How to use -

If the DTB line (blue) and normalized DJIA (orange) are under the green dashed line, high probability for a long and reversal.

Use with the symbol SPX/QQQ

Dow Jones Industrial Average - DJIA

Double Bottom Strategy (Long Only, ATR Trailing Stop + Alerts)This script implements a long-only breakout strategy based on the recognition of a Double Bottom price pattern, enhanced with a 50 EMA trend filter and a dynamic ATR-based trailing stop. It is suitable for traders looking to capture reversals in trending markets using a structured pattern-based entry system.

🧠 Key Features:

Double Bottom Detection: Identifies double bottom structures using pivot lows with configurable tolerance.

ATR-Based Trailing Stop: Manages exits using a trailing stop calculated from Average True Range (ATR), dynamically adjusting to market volatility.

EMA Filter (Optional): Filters trades to only go long when price is above the 50 EMA (trend confirmation).

Alerts: Real-time alerts on entry and exit, formatted in JSON for webhook compatibility.

Backtest Range Controls: Customize historical testing period with start and end dates.

✅ Recommended Markets:

Gold (XAUUSD)

S&P 500 (SPX, ES)

Nasdaq (NDX, NQ)

Stocks (Equities)

⚠️ Not recommended for Forex due to differing behavior and noise levels in currency markets.

🛠️ User Guidance:

Tune the pivot period, tolerance, and ATR settings for best performance on your chosen asset.

Backtest thoroughly over your selected date range to assess historical effectiveness.

Use small position sizes initially to test viability in live or simulated environments.

TA Pressure GaugeThe Pressure Gauge indicator is composed of two main plotted elements in Oscillator Mode: the Up/Down Volume Ratio (UDVR) as a histogram, and the Relative Strength (RS) Score as a continuous line. These two metrics work together to provide real-time insights into both volume momentum and relative performance.

The UDVR histogram measures the ratio of buying volume to selling volume. Specifically, if the current close is greater than the previous close, the volume for that bar is classified as up volume. If the current close is lower than the previous close, it’s classified as down volume. Over a 50-bar rolling window (or fewer if limited history exists), the sum of up volume is divided by the sum of down volume to calculate the UDVR. The result is normalized and plotted as vertical bars centered around a baseline value of 50. A UDVR value greater than 1 indicates bullish dominance—more buying than selling—while a value less than 1 indicates bearish pressure. The histogram bars are dynamically color-coded:

Lime or Green when the UDVR is rising and remains above 1, signaling increasing buying strength.

Red or Maroon when the UDVR is falling and below 1, indicating growing selling pressure.

The second component is the Relative Strength Score (RS Score), plotted as a line graph overlaid on the oscillator. This is calculated by dividing the current closing price of the selected asset by the closing price of a benchmark index (e.g., SPX). The result is normalized over a selectable lookback period—63 bars (3 months), 126 bars (6 months), or 251 bars (12 months)—and then converted into a value between 1 and 99. This RS line reflects how well the asset is performing compared to the broader market. When the RS Score is above 70, it indicates strong outperformance and leadership; below 30 suggests underperformance.

The true value of Oscillator Mode is in its ability to combine these two readings visually. When both the UDVR histogram is green and elevated, and the RS line is rising and above 70, it often indicates strong institutional accumulation and momentum—key ingredients for high-probability breakout or trend-following trades. This dual-layered confirmation system enables traders to cut through noise and focus on setups that align both in volume strength and market relative performance. The oscillator can be fully customized within the script to change colors, sizing, and input periods, making it flexible for various trading styles and timeframes.

Look at this textbook flag forming on ticker symbol WGS. The setup was clean, and the Pressure Gauge was already showing bullish signals.

Following the breakout, you can see how the move confirmed what the Pressure Gauge was indicating early on—strong buying pressure and clear relative strength.

M2 Lag Correlation | QuantumResearch🧠 M2 Lag Correlation | QuantumResearch

Global M2 vs. Asset Lagged Correlation Dashboard

Measuring delayed macroeconomic impact across regions and asset classes

🌍 Why Is It Unique?

This is the first macro-financial correlation tool on TradingView that tracks and aggregates lagged money supply (M2) data across 20 global economies, FX-adjusted into USD equivalence, and overlays it against your selected chart (BTC, ETH, SPX, etc.).

It does more than just plot macro data — it quantifies the delayed correlation between asset price action and macro liquidity trends, providing a unique macro-lag insight tool for serious analysts and long-term investors.

📌 What It Does:

Computes the global M2 aggregate using 20 region-specific M2 datasets, normalized via local exchange rates

Lets you shift the M2 data forward using a customizable day offset (default: 96D) to model macro lag effects

Calculates rolling Pearson correlation between your charted asset and the lagged M2 line

Outputs correlation scores across four windows:

🟢 30D (Monthly)

🟢 90D (Quarterly)

🟢 182D (Semester)

🟢 365D (Yearly)

➕ Includes a composite Average Score

Displays values in a clean dashboard-style table with color-coded feedback

🔍 Use Cases:

Detect how macro liquidity expansion or contraction influences your asset

Determine the macro lag window — the period after which monetary supply affects asset prices

Validate cycle transitions using data-backed macro alignment

Compare lag response between assets (e.g., BTC vs. ETH vs. NASDAQ)

📊 Macro Lag Insight:

As of recent data:

Bitcoin (BTC) shows the strongest correlation with global M2 at approximately 97 days of lag

Ethereum (ETH) shows its peak correlation around 108 days of lag

These lag values are not static and may evolve over time as macro conditions shift. The script allows users to explore such relationships interactively.

⚙️ Customizable Parameters:

🔄 Offset (Days) – Slide the M2 curve forward to match historical asset reactions

🎨 Color Mode – 8 color palettes to match your visual preferences

📍 Table Position – Place the correlation display wherever you want on your chart

✅ Requirements:

Access to ECONOMICS and FX_IDC feeds on TradingView

Chart timeframe: preferably daily or higher for macro relevance

⚠️ Disclaimer:

Disclaimer: The content on this indicator is for informational and educational purposes only. Nothing contained within should be considered financial, investment, legal, or other professional advice. Past performance does not guarantee future results. Trading cryptocurrencies involves substantial risk of loss and is not suitable for every investor.

Correlation does not imply causation. This tool offers macro-aligned insight, not direct price prediction. Use it alongside a broader macro and market framework.